1. Introduction

Earnings management (EM) has been covered intensively in the literature. EM is the intervention of management in the presentation of financial statements and related disclosures to achieve certain benefits for themselves or for the firm (

Healy and Wahlen 1999). One of the reasons for practicing EM is to improve the firm’s image (

Teixeira and Rodrigues 2022). The decision to implement corporate earnings management depends mainly on costs and benefits. When the benefits outweigh the costs, companies are motivated to employ earnings management. A major benefit of earnings management is business continuity (

Zhan and Jing 2022).

The firms that early adopted the IAS/IFRS reporting regime may have arguably high extant incentives to enhance their reporting and that were already reporting under (old) IAS/IFRS standards. While the late adopters and mandatory adopters exhibit an increase in earnings management practices after transitioning to the 2005 version of IFRS as documented by (

Capkun et al. 2016). This provides strong evidence that the 2005 changes to IAS/IFRS give the firms a wide range of flexibility in accounting choices and this, couple with the lack of implementation guidance, has contributed to increase the earnings management practices. This interpretation supports our assumption that the firms may benefit from the flexibility that exists in accounting choices, particularly in difficult circumstances, such as the COVID-19 pandemic, to manage their earnings and show their ability to survive.

A stream of literature focused on the perspective of EM as a consequence of using accounting standards (

Capkun et al. 2016;

Kim and Lee 2016;

Tutino et al. 2019;

Comporek 2020;

Lee and Lee 2020;

Kim 2022). After the Sarbanes–Oxley (SOX) Act was passed in 2002, the Financial Accounting Standards Board (FASB) started to develop more consistent standards based on principles or goals. Compared to rule-based standards, principle-based standards leave more room for different interpretations and are characterized by clearly defined goals, fewer scope exceptions, and fewer implementation instructions (

Bjornsen 2019).

COVID-19, like any other crisis, affects the continuity of firms and increases the probability of the bankruptcy threat. In turn, this threat affects the other related parties. Capital providers and managers are interested in the costs of these failures, as well as employees, who may face the risk of redundancy (

Charitou et al. 2007). As a result, the quality of financial information provided has captured the attention of both analysts and users, particularly when dealing with reports of financially distressed firms who have the incentives and potential to manage earnings (

Tsipouridou and Spathis 2014;

Yassin et al. 2015).

FASB issued a converged standard for the “Revenue from Contracts with Customers”; it was formed by the Accounting Standards Codification 606 (ASC 606), in collaboration with the International Accounting Standards Board (IASB), with the aim of enhancing transparency for the investors, thus, in turn, affecting the continuity of the business.

The purpose of implementing ASC 606 is to provide fairer representation and to prevent revenue steering. It is believed that adopting ASC 606 increases management discretion in revenue recognition. In addition, the new standard leads to a reduction in the informative value of revenue deferrals (

Kim 2022).

During the COVID-19 crisis, many businesses attempted to manage their earnings in order to continue operating. One of the tools that was used by many companies to achieve that aim was the variable considerations in ASC 606. Variable consideration refers to a contract whereby the promised amount varies depending on the potential outcomes (

Condren 2021).

Although few in number, there are significant motivations for this research. First, in 2020, larger firms were entering bankruptcy at higher rates. According to data from the American Bankruptcy Institute, the total number of Chapter 11 filings increased by 35% during the first six months of 2020 as compared to the same period in 2019. In addition, there was a 194% rise in bankruptcies of firms with more than USD 50 million in assets (

Greenwood et al. 2020;

Ventura 2020;

Wang et al. 2020). Moreover, the US Census Pulse survey declared that 74 percent of small businesses reported lost revenues in one week in the middle of the second quarter of 2020 (

U.S. Census Bureau 2020;

Wang et al. 2020). Secondly, although ASC 606 is one of the outcomes of a long series of projects between IASB and FASB, it has different characteristics with stricter requirements than IFRS 15. On the one hand, the IFRS standards offer greater accounting flexibility due to vague criteria, open and hidden options, and subjective estimates (

Capkun et al. 2016). On the other hand, GAAP is described as being principle-based; in addition, the US market is characterized as more prudent, with a stricter attitude against accounting policies and practices, because of significant fraud cases. Thus, GAAP limits the options of income recognition practices and requires more disclosures (

Zhou 2021).

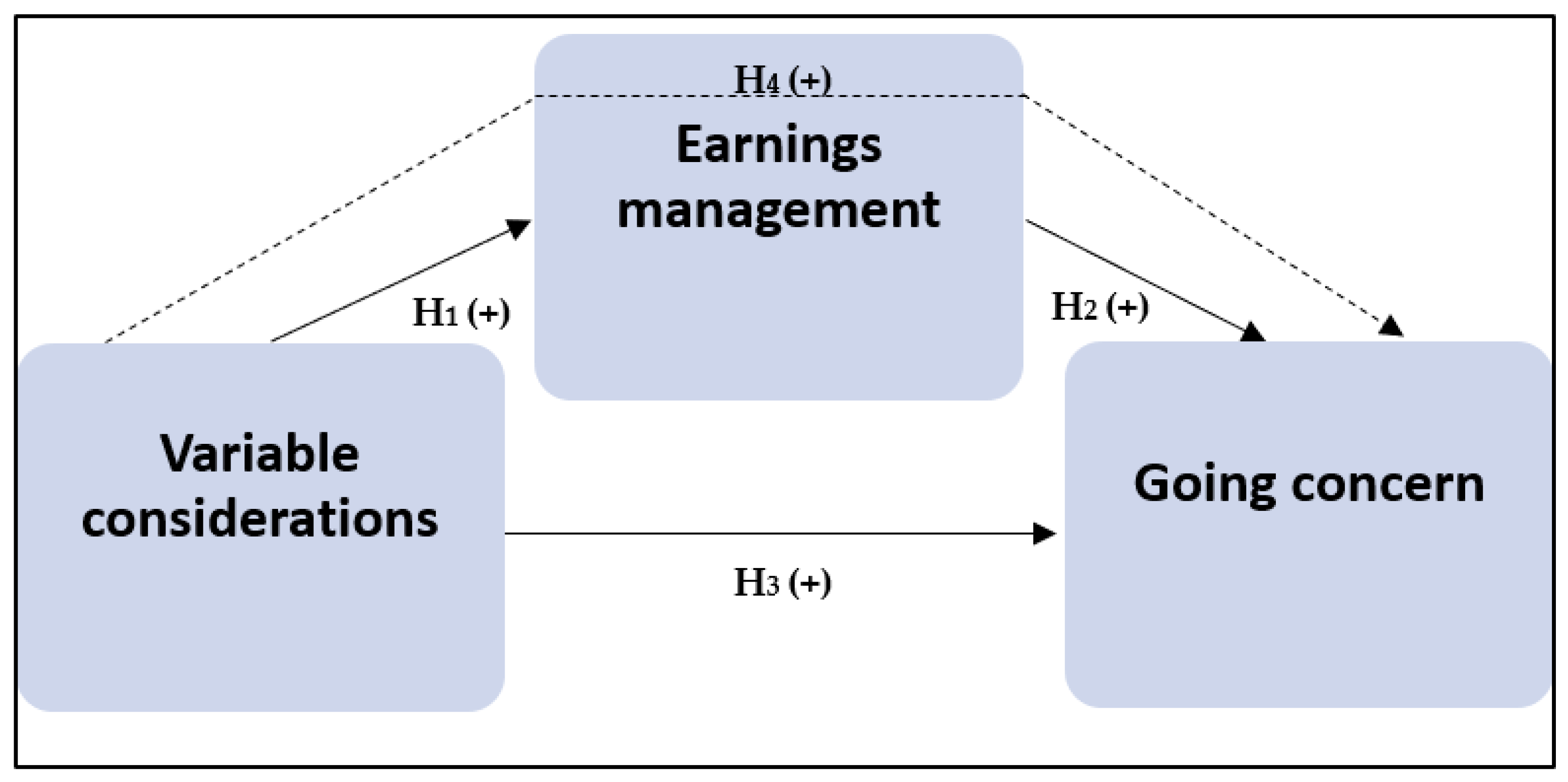

Against this background, this research aims at answering the following research question: “Are the variable considerations in ASC 606 used as a tool to manage earnings in order for a business entity to continue operating during COVID-19?”. More specifically, this research aims to achieve the following objectives:

- −

To explore the use of the variable considerations in ASC 606 as a tool to manage earnings during COVID-19;

- −

To examine the way in which earnings management is used to keep firms operating during COVID-19;

- −

To assess the effect of using the variable considerations in ASC 606 on the continuity of firms during COVID-19;

- −

To investigate the mediating role of managing earnings on the relationship between using the variable considerations in ASC 606 and the business continuity for business entities during COVID-19.

This paper contributes to the scholarship by exploring the practices of financial statement preparers during the COVID-19 pandemic regarding the revenue recognition application under ASC 606 to manage earnings, enabling businesses to survive. This provides evidence on the contingency theory, which is in line with

Donaldson (

2001) and

Damayanthi et al. (

2022), who argued that businesses form strategies and actions that help them to survive depending on the external environment. In addition, this study provides indicators of the importance of using the variable considerations in ASC 606 as a determinant of going concern during the pandemic. Furthermore, this research is expected to assist regulators and policy makers in finding the gaps resulting from the flexibility provided by FASB to financial statement preparers. Also, preparers will gain benefits concerning the use of variable considerations in ASC 606 as a tool to help their businesses in facing crises.

The study is structured as follows. The literature review of the effect of variable considerations in ASC 606 and earnings management, the way in which earnings management affects business continuity, and the effect of variable considerations in the ASC 606 business continuity are summarized in

Section 2. In addition, the development of the hypotheses is provided in this section. Subsequently,

Section 3 provides an explanation of the research methodology. In addition to highlighting the data analysis process, a discussion of the results is presented in

Section 4. Finally, the research concludes with practical and theoretical implications, as well as suggestions for further research.

5. Conclusions

The crisis of COVID-19 had a direct impact on business continuity. During such a crisis, the quality of reported financial information becomes questionable, especially when dealing with the reports of financially distressed firms. Such firms have considerable incentives to practice EM (

Tsipouridou and Spathis 2014), which could be a consequence of the latent and flexible standards issued by regulators. These provide users with more room to interpret and implement practices based on their specific situations (

Bjornsen 2019).

FASB issued ASC 606 with the objective to enhance transparency, to provide fairer representation, and to prevent revenue steering (

Kim 2022). During COVID-19, variable considerations in ASC 606 were used to manage earnings in order to keep businesses operating. This study builds on prior research by exploring the mediating effect of EM on the relationship between using the variable consideration in ASC 606 and going concerns.

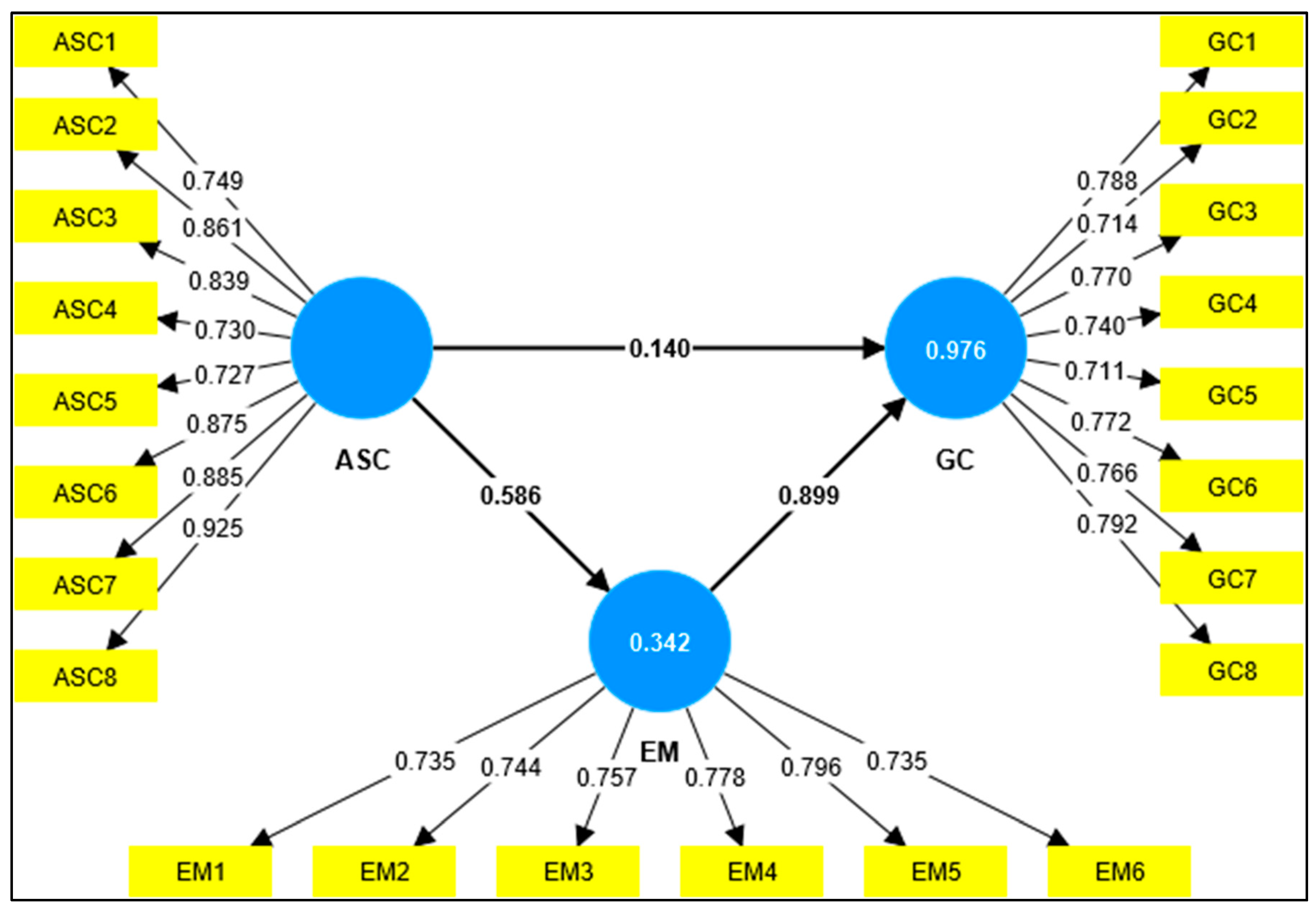

To achieve the objectives of this study, PLS-SEM was used. The results revealed that variable considerations in ASC 606 increased the use of earnings management practices. This finding contradicts prior research (

Tutino et al. 2019;

Comporek 2020;

Lee and Lee 2020). The finding is consistent with the hypothesis that firms tended to use variable considerations in ASC 606 as a tool for managing their earnings during COVID-19.

Another finding showed that the use of variable considerations in ASC 606 positively affects going concerns. The previous literature (

Glaze et al. 2020;

Levy 2020) also emphasized this finding, which confirms that companies may use various kinds of variable considerations in ASC 606 to keep their businesses operating during challenging times.

The results emphasized the mediation role of earnings management practices in the causal effect of using variable considerations in ASC 606 on the going concern of businesses. This result is a new finding that has not been previously researched in the literature and likely constitutes the most important contribution of this research. COVID-19 has forced firms to look for solutions to keep them operating. The crisis has shown the positive side of earnings management practice, whereby the variable considerations in ASC 606 were exploited to manage firms’ earnings, enabling them to survive.

Furthermore, different practical implications have been provided to regulators, policy makers, and preparers. The study made it easier for regulators and policy makers to find weaknesses arising from the flexibility granted by FASB to financial-statement preparers through the variable considerations in ASC606. In addition, preparers can benefit from the use of variable considerations in ASC 606 as a tool to help their businesses in facing crises. Through the results shown in this study and what was found in previous studies, companies, especially in times of crises, exploit the gaps and flexibility found in accounting policies and practices to show their best financial performance. Therefore, from an economic perspective, we can generalize the results obtained in this study, especially since our sample was from developed countries with strong economies that are supposed to practice accounting standards correctly.

However, this study has several limitations that can open the door for further research. The study was performed on public shareholding companies in the US market. Additionally, the sample size was limited due to the prohibitive cost of the data collection method used. Therefore, it is difficult to generalize the results of this study to other types of firms, although public shareholding companies have characteristics that allow the results to be generalized to other types of companies. The problem of generalizing the results may also be affected by the country in which the study was applied. Hence, future research should assess the variables on larger samples, in other countries, and in diverse types of businesses. To make the results more robust, we prepared a preliminary experiment by sending the questionnaire to thirty respondents from the target sample to conduct an initial survey (pilot test), where the initial results we found were consistent with the results obtained after sending all questionnaires to the respondents. This confirms that the mechanism used to extract the results is logical and consistent with the research methodology.

,

,

{kind=link}

{kind=link}