Mobile Financial Services and the Shadow Economy in Southern African Countries: Does Regulatory Quality Matter?

Abstract

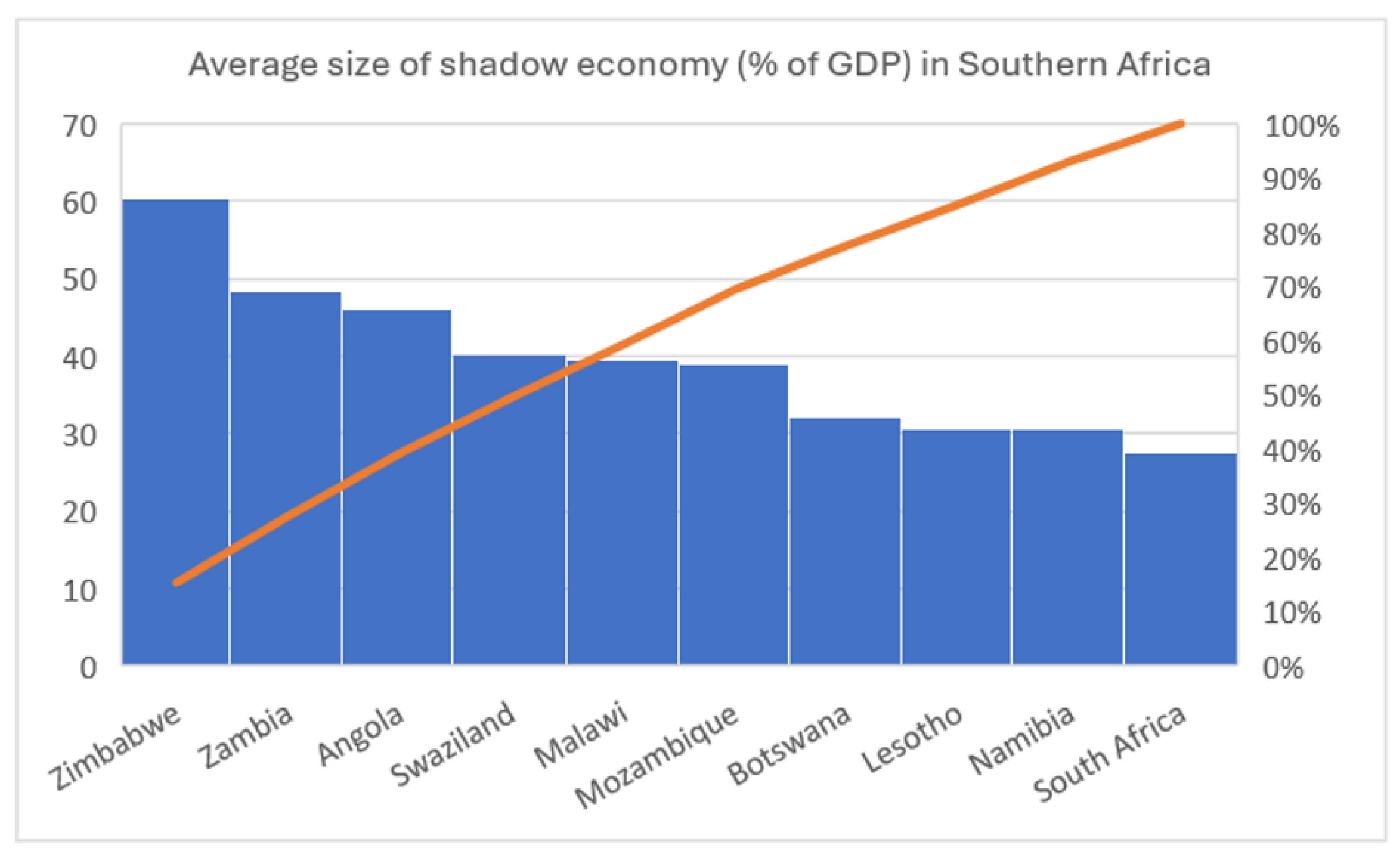

:1. Introduction

2. Theoretical and Empirical Literature

2.1. Theoretical Literature

2.2. Empirical Literature

3. Results and Discussion

4. Materials and Methods

4.1. Data Description

4.2. Model Specification

4.3. Methods

4.3.1. Cross-Sectional Dependence and Unit Root Tests

4.3.2. Panel Cointegration Test

4.3.3. Estimation of Parameters

5. Conclusions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ajide, Folorunsho M. 2021. Shadow economy in Africa: How relevant is financial inclusion? Journal of Financial Regulation and Compliance 29: 297–316. [Google Scholar] [CrossRef]

- Ajide, Folorunsho M., and James T. Dada. 2024. Globalization and shadow economy: A panel analysis for Africa. Review of Economics and Political Science 9: 166–89. [Google Scholar] [CrossRef]

- Aker, Jenny C., Rachid Boumnijel, Amanda McClelland, and Niall Tierney. 2016. Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger. Economic Development and Cultural Change 65: 1–37. [Google Scholar] [CrossRef]

- Akhter, Nahid, and Baqui Khalily. 2017. Impact of Mobile Financial Services on Financial Inclusion in Bangladesh. Institute for Inclusive Finance and Development. Institute for Inclusive Finance and Development Working Paper No. 52. Available online: https://inm.org.bd/wp-content/uploads/2017/07/Working-paper-52.pdf (accessed on 7 November 2024).

- Alm, James, and Abel Embaye. 2013. Using dynamic panel methods to estimate shadow economies around the world, 1984–2006. Public Finance Review 41: 510–43. [Google Scholar] [CrossRef]

- Anarfo, Ebenezer Bugri, Joshua Yindenaba Abor, and Kofi Achampong Osei. 2020. Financial regulation and financial inclusion in Sub-Saharan Africa: Does financial stability play a moderating role? Research in International Business and Finance 51: 101070. [Google Scholar] [CrossRef]

- Arogundade, Sodiq, Adewale Samuel Hassan, and Santos Bila. 2022. Diaspora income, financial development and ecological footprint in Africa. International Journal of Sustainable Development & World Ecology 29: 440–54. [Google Scholar] [CrossRef]

- Aron, Janine. 2017. ‘Leapfrogging’: A Survey of the Nature and Economic Implications of Mobile Money. Oxford: University of Oxford. Available online: https://ideas.repec.org/p/csa/wpaper/2017-02.html (accessed on 15 April 2024).

- Álvarez-Herránz, Agustin, Daniel Balsalobre, Jose Maria Cantos, and Muhammad Shahbaz. 2017. Energy innovations-GHG emissions nexus: Fresh empirical evidence from OECD countries. Energy Policy 101: 90–100. [Google Scholar] [CrossRef]

- Banerjee, Anindya, Lynne Cockerell, and Bill Russell. 2001. An I (2) analysis of inflation and the markup. Journal of Applied Econometrics 16: 221–40. [Google Scholar] [CrossRef]

- Barth, James R., Gerard Caprio, Jr., and Ross Levine. 2004. Bank regulation and supervision: What works best? Journal of Financial Intermediation 13: 205–48. [Google Scholar] [CrossRef]

- Beck, Thorsten, Asli Demirgüç-Kunt, and Ross Levine. 2007. Finance, inequality and the poor. Journal of Economic Growth 12: 27–49. [Google Scholar] [CrossRef]

- Beck, Thorsten, Haki Pamuk, Ravindra Ramrattan, and Burak R. Uras. 2018. Payment instruments, finance and development. Journal of Development Economics 133: 162–86. [Google Scholar] [CrossRef]

- Berdiev, Aziz N., and James W. Saunoris. 2018. Does globalisation affect the shadow economy? The World Economy 41: 222–41. [Google Scholar] [CrossRef]

- Besong, Susan Enyang, Telma Longy Okanda, and Simon Arrey Ndip. 2022. An empirical analysis of the impact of banking regulations on sustainable financial inclusion in the CEMAC region. Economic Systems 46: 100935. [Google Scholar] [CrossRef]

- Blackburn, Keith, Niloy Bose, and Salvatore Capasso. 2012. Tax evasion, the underground economy and financial development. Journal of Economic Behavior & Organization 83: 243–53. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, and Joseph Ntayi. 2020. Trust: Mediator between mobile money adoption and usage and financial inclusion. Social Responsibility Journal 16: 1215–37. [Google Scholar] [CrossRef]

- Buehn, Andreas, and Friedrich Schneider. 2012. Shadow economies around the world: Novel insights, accepted knowledge, and new estimates. International Tax and Public Finance 19: 139–71. [Google Scholar] [CrossRef]

- Canh, Phuc Nguyen, Christophe Schinckus, and Su Dinh Thanh. 2021. What are the drivers of shadow economy? A further evidence of economic integration and institutional quality. The Journal of International Trade & Economic Development 30: 47–67. [Google Scholar] [CrossRef]

- Capasso, Salvatore, and Tullio Jappelli. 2013. Financial development and the underground economy. Journal of Development Economics 101: 167–78. [Google Scholar] [CrossRef]

- Chaudhry, Imran Sharif, Zulkornain Yusop, and Muzafhar Shah Habibullah. 2022. Financial inclusionenvironmental degradation nexus in OIC countries: New evidence from environmental Kuznets curve using DCCE approach. Environmental Science and Pollution Research 29: 5360–77. [Google Scholar] [CrossRef]

- Chen, Rong, and Raian Divanbeigi. 2019. Can Regulation Promote Financial Inclusion? World Bank Policy Research Working Paper 8711. Available online: https://documents1.worldbank.org/curated/en/689111547822970149/pdf/WPS8711.pdf (accessed on 7 November 2024).

- Chinoda, Tough, and Farai Kwenda. 2019. Do mobile phones, economic growth, bank competition and stability matter for financial inclusion in Africa? Cogent Economics & Finance 7: 1–20. [Google Scholar] [CrossRef]

- Chortareas, Georgios E., Claudia Girardone, and Alexia Ventouri. 2013. Financial freedom and bank efficiency: Evidence from the European Union. Journal of Banking and Finance 37: 1223–31. [Google Scholar] [CrossRef]

- Chudik, Alexander, and M. Hashem Pesaran. 2015. Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. Journal of Economics 188: 393–420. [Google Scholar] [CrossRef]

- Claessens, Stijn, and Liliana Rojas-Suarez. 2016. Financial regulations for improving financial inclusion. Center for Global Development 2: 44–53. [Google Scholar]

- Conway, Paul, and Giuseppe Nicoletti. 2006. Product Market Regulation in the Non-Manufacturing Sectors of OECD Countries: Measurements and Highlights. OECD Working Papers, Nr. 530. Paris: OECD. [Google Scholar]

- De Hoyos, Rafael E., and Vasilis Sarafidis. 2006. Testing for cross-sectional dependence in panel-data models. Stata Journal 6: 482–96. [Google Scholar] [CrossRef]

- Dell’Anno, Roberto. 2016. Analysing the determinants of the shadow economy with a “separate approach”. An application of the relationship between inequality and the shadow economy. World Development 84: 342–56. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, and Leora Klapper. 2012. Measuring Financial Inclusion: The Global Findex Database. Washington, DC: The World Bank. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora Klaper, Dorothe Singer, and Saniya Ansar. 2022. The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Washington, DC: World Bank Publications. [Google Scholar]

- Demirgüç-Kunt, Asli, Leora Klaper, Saniya A. Dorothe, and Jake Hess. 2018. Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution. Washington, DC: World Bank, CC BY 3.0 IGO. [Google Scholar] [CrossRef]

- D’Hernoncourt, Johanna, and Pierre-Guillaume Méon. 2012. The not so dark side of trust: Does trust increase the size of the shadow economy? Journal of Economic Behavior and Organization 81: 97–121. [Google Scholar] [CrossRef]

- Dima, Bogdan, and Stefana Maria Dima. 2018. Do Business Regulations Promote Growth in Low-income Countries? Economic Analysis 51: 33–56. [Google Scholar] [CrossRef]

- Ditzen, Jan. 2016. xtdcce: Estimating Dynamic Common Correlated Effects in Stata. SEEC Discussion Papers, 1601. Tokyo: SEEC. [Google Scholar]

- Donovan, Kevin. 2012. Mobile money for financial inclusion. Information and Communications for Development 61: 61–73. [Google Scholar]

- Dumitrescu, Elena-Ivona, and Christophe Hurlin. 2012. Testing for Granger non-causality in heterogeneous panels. Economic Modelling 29: 1450–60. [Google Scholar] [CrossRef]

- Elgin, Ceyhun, and Oguz Oztunali. 2012. Shadow Economies Around the World: Model Based Estimates. (Bogazici University Department of Economics Working Papers 5). pp. 1–48. Available online: http://ideas.econ.boun.edu.tr/RePEc/pdf/201205.pdf (accessed on 10 July 2024).

- Elgin, Ceyhun, M. Ayhan Kose, Franziska Ohnsorge, and Shu Yu. 2021. Understanding Informality. CEPR Discussion Paper 16497. London: CEPR. [Google Scholar]

- Engle, Robert F., and C. W. Granger. 1987. Co-integration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society 55: 251–76. [Google Scholar] [CrossRef]

- Enste, Dominik H. 2010. Regulation and shadow economy: Empirical evidence for 25 OECD-countries. Constitutional Political Economy 21: 231–48. [Google Scholar] [CrossRef]

- Enste, Dominik H., and Stefan Hardege. 2006. IW-Regulierungsindex: Methode, Analyse und Ergebnisse eines internationalen Vergleichs. Köln: IW-Analyse. [Google Scholar]

- Evans, David S., and Alexis Pirchio. 2014. An empirical examination of why mobile money schemes ignite in some developing countries but flounder in most. Review of Network Economics 13: 397–451. [Google Scholar] [CrossRef]

- Evans, Olaniyi. 2018. Connecting the poor: The internet, mobile phones and financial inclusion in Africa. Digital Policy, Regulation and Governance 20: 568–81. [Google Scholar] [CrossRef]

- Fritz, Thomas, and Sven Hilbig. 2019. Global Justice 4.0: The Impacts of Digitalisation on the Global South. Berlin: Brot für die Welt, Evangelisches Werk für Diakonie und Entwicklung eV. [Google Scholar]

- Gomis-Porqueras, Pedro, Adrian Peralta-Alva, and Christopher Waller. 2014. The shadow economy as an equilibrium outcome. Journal of Economic Dynamics and Control 41: 1–19. [Google Scholar] [CrossRef]

- GPFI. 2018. G20 Policy Guide: Digitisation and Informality—Harnessing Digital Financial Inclusion for Individuals and MSMEs in the Informal Economy. Available online: https://www.gpfi.org/sites/gpfi/files/documents/G20_Policy_Guide_Digitisation_and_Informality.pdf (accessed on 2 March 2024).

- GSMA. 2018. 2017 State of the Industry Report on Mobile Money. London: GSMA. [Google Scholar]

- GSMA. 2021. State of the Industry Report on Mobile Money 2021. London: GSMA. [Google Scholar]

- Hart, Keith. 2008. Informal Economy. In The New Palgrave Dictionary of Economics. Edited by Steven N. Durlauf and Lawrence E. Blume. London: Palgrave Macmillan, vol. 10, pp. 6481–84. [Google Scholar]

- Hassan, Adewale Samuel. 2021. Foreign aid and economic growth in Nigeria: The role of institutional quality. Studies of Applied Economics 39. [Google Scholar] [CrossRef]

- Hassan, Adewale Samuel. 2023a. Coal mining and environmental sustainability in South Africa: Do institutions matter? Environmental Science and Pollution Research 30: 20431–49. [Google Scholar] [CrossRef]

- Hassan, Adewale Samuel. 2023b. Modeling the linkage between coal mining and ecological footprint in South Africa: Does technological innovation matter? Mineral Economics 36: 123–38. [Google Scholar] [CrossRef]

- Hassan, Adewale Samuel, and Daniel Francois Meyer. 2021. Moderating effect of institutional quality on the external debt-economic growth nexus: Insights from highly indebted poor countries (HIPC). African Journal of Business and Economic Research 16: 7–28. [Google Scholar] [CrossRef]

- Hassan, Adewale Samuel, Daniel Francois Meyer, and Sebastian Kot. 2019. Effect of institutional quality and wealth from oil revenue on economic growth in oil-exporting developing countries. Sustainability 11: 3635. [Google Scholar] [CrossRef]

- Hoskins, Sean M., and Marc Labonte. 2015. An Analysis of the Regulatory Burden on Small Banks. Congressional Research Service (CRS) Report 7–5700. Washington, DC: Congressional Research Service (CRS). [Google Scholar]

- Ihrig, Jane, and Karine S. Moe. 2004. Lurking in the shadows: The informal sector and government policy. Journal of Development Economics 73: 541–57. [Google Scholar] [CrossRef]

- Izaguirre, Juan Carlos. 2020. Making Consumer Protection Regulation More Customer-Centric. Washington, DC: CGAP. Washington, DC: World Bank. [Google Scholar]

- Jacolin, Luc, Joseph Keneck Massil, and Alphonse Noah. 2021. Informal sector and mobile financial services in emerging and developing countries: Does financial innovation matter? The World Economy 44: 2703–37. [Google Scholar] [CrossRef]

- Kaffenberger, Michelle, Edoardo Totolo, and Matthew Soursourian. 2018. A Digital Credit Revolution: Insights from Borrowers in Kenya and Tanzania. Financial Sector Deepening Working Paper. Washington, DC: Consultative Group to Assist the Poor. [Google Scholar]

- Kapetanios, G., M. H. Pesaran, and T. Yamagata. 2011. Panels with nonstationary multifactor error structures. Journal of Economics 160: 326–48. [Google Scholar] [CrossRef]

- Kaufmann, D., Kraay A., and Mastruzzi M. 2011. The worldwide governance indicators: Methodology and analytical issues1. Hague Journal on the Rule of Law 3, 220–46. [Google Scholar] [CrossRef]

- Kelmanson, M. Ben, Koralai Kirabaeva, Leandro Medina, Borislava Mircheva, and Jason Weiss. 2019. Explaining the Shadow Economy in Europe: Size, Causes and Policy Options. Washington, DC: International Monetary Fund. [Google Scholar]

- Kiaga, Annamarie, and Vicky Leung. 2020. The Transition from the Informal to the Formal Economy in Africa. Global Employment Policy Review Background Paper No. 4. Geneva: Internation Labour Organisation. [Google Scholar]

- Klapper, Leora. 2017. How digital payments can benefit entrepreneurs. IZA World of Labor 396: 1–9. [Google Scholar] [CrossRef]

- Kodongo, Odongo. 2018. Financial regulations, financial literacy, and financial inclusion: Insights from Kenya. Emerging Markets Finance and Trade 54: 2851–73. [Google Scholar] [CrossRef]

- La Porta, Rafael, and Andrei Shleifer. 2014. Informality and development. Journal of Economic Perspectives 28: 109–26. [Google Scholar] [CrossRef]

- Laeven, Luc, and Ros Levine. 2009. Bank governance, regulation and risk taking. Journal of Financial Economics 93: 259–75. [Google Scholar] [CrossRef]

- Levine, Ross. 2012. The governance of financial regulation: Reform lessons from the recent crisis. International Review of Finance 12: 39–56. [Google Scholar] [CrossRef]

- Manduna, Kennedy. 2023. Zama Zamas: Victims, Not Criminals. The Sunday Times (SA). August 16. Available online: https://www.timeslive.co.za/sunday-times-daily/opinion-and-analysis/2023-08-16-kennedy-manduna-zama-zamas-victims-not-criminals/ (accessed on 25 June 2024).

- Mark, Nelson C., Masao Ogaki, and Donggyu Sul. 2005. Dynamic seemingly unrelated cointegrating regressions. Review of Economic Studies 72: 797–820. [Google Scholar] [CrossRef]

- Medina, Leandro, and M. Friedrich Schneider. 2018. Shadow Economies Around the World: What Did We Learn over the Last 20 Years? Washington, DC: International Monetary Fund. [Google Scholar]

- Mishra, Vishal, and Shailendra Singh Bisht. 2013. Mobile banking in a developing economy: A customer-centric model for policy formulation. Telecommunications Policy 37: 503–14. [Google Scholar] [CrossRef]

- Munyegera, Ghombe Kasim, and Tomoya Matsumoto. 2016. Mobile money, remittances, and household welfare: Panel evidence from rural Uganda. World Development 79: 127–37. [Google Scholar] [CrossRef]

- Neaime, Simon, and Isabelle Gaysset. 2018. Financial inclusion and stability in MENA: Evidence from poverty and inequality. Finance Research Letters 24: 230–37. [Google Scholar] [CrossRef]

- North, Douglass C. 1990. Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge University Press. [Google Scholar]

- Pesaran, M. Hashem. 2004. General Diagnostic Tests for Cross Section Dependence in Panels. CESifo Working Papers No 1233. Munich: CESifo, pp. 255–60. [Google Scholar]

- Pesaran, M. Hashem. 2007. A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Economics 22: 265–312. [Google Scholar] [CrossRef]

- Rangarajan, C. 2008. Report of the Committee on Financial Inclusion. FinDev Gateway. Available online: https://www.findevgateway.org/paper/2008/01/report-committee-financial-inclusion (accessed on 25 June 2024).

- Reynolds, Travis W., Marieka Klawitter, Pierre E. Biscaye, and C. Leigh Anderson. 2018. Mobile money and branchless banking regulations affecting cash-in, cash-out networks in low-and middle-income countries. Gates Open Research 2: 64. [Google Scholar] [CrossRef]

- Rogerson, C. M. 1988. The underdevelopment of the informal sector: Street hawking in Johannesburg, South Africa. Urban Geography 9: 549–67. [Google Scholar] [CrossRef]

- Rud, Juan Pablo. 2012. Electricity provision and industrial development: Evidence from India. Journal of Development Economics 97: 352–67. [Google Scholar] [CrossRef]

- Sarma, Mandira, and Jesim Pais. 2011. Financial inclusion and development. Journal of International Development 23: 613–28. [Google Scholar] [CrossRef]

- Schneider, Friedrich. 2010. The influence of public institutions on the shadow economy: An empirical investigation for OECD countries. Review of Law & Economics 6: 441–68. [Google Scholar] [CrossRef]

- Schneider, Friedrich, and Dominik H. Enste. 2000. Shadow economies: Size, causes, and consequences. Journal of Economic Literature 38: 77–114. [Google Scholar] [CrossRef]

- Schneider, Friedrich, and Dominik H. Enste. 2013. The Shadow Economy: An International Survey. Cambridge: Cambridge University Press. [Google Scholar]

- Stats SA. 2020. Quarterly Labour Force Survey. Pretoria: Statistics South Africa. [Google Scholar]

- Sujee, Zain Jadewin. 2016. Anti-Money Laundering Framework in South Africa the United States and the United Kingdom. Master’s thesis, University of Pretoria (South Africa), Pretoria, South Africa. [Google Scholar]

- Svirydzenka, Katsiaryna. 2016. Introducing a New Broad-Based Index of Financial Development. (IMF Working Paper 16/15). Available online: https://www.imf.org/en/Publications/WP/Issues/2016/12/31/Introducing-a-New-Broad-based-Index-of-Financial-Development-43621 (accessed on 1 April 2024).

- Turkay, Mesut. 2017. Heterogeneity across emerging market central bank reaction functions. Central Bank Review 17: 111–16. [Google Scholar] [CrossRef]

- Ulyssea, Gabriel. 2018. Firms, informality, and development: Theory and evidence from Brazil. American Economic Review 108: 2015–47. [Google Scholar] [CrossRef]

- Westerlund, Joakim. 2007. Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics 69: 709–48. [Google Scholar] [CrossRef]

- Williams, Colin C., and F. Schneider. 2016. Measuring the Global Shadow Economy: The Prevalence of Informal Work and Labour. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- World Bank. 2014. Global Financial Development Report 2014: Financial Inclusion. Washington, DC: World Bank. [Google Scholar]

- World Bank. 2020. Doing Business 2020: Comparing Business Regulation in 190 Economies. Washington, DC: World Bank. [Google Scholar]

- Yakubi, Yusef Ali Yusef, Basuki Basuki, Rudi Purwono, and Idrianawati Usman. 2022. The impact of digital technology and business regulations on financial inclusion and socio-economic development in low-income countries. Sage Open 12: 1–15. [Google Scholar] [CrossRef]

- Younas, Zahid Irshad, Atiqa Qureshi, and Mamdouh Abdulaziz Saleh Al-Faryan. 2022. Financial inclusion, the shadow economy and economic growth in developing economies. Structural Change and Economic Dynamics 62: 613–21. [Google Scholar] [CrossRef]

{kind=link}

| Variable | SE | MOFIS | RQ | MOFIS∗RQ | GDP | FD | PS |

|---|---|---|---|---|---|---|---|

| CD test | 8.139 ** | 12.126 *** | 9.629 *** | 17.503 *** | 20.934 ** | 11.024 *** | 9.376 *** |

| p-value | 0.029 | 0.000 | 0.000 | 0.000 | 0.017 | 0.000 | 0.000 |

| Variable | CADF | CIPS | ||

|---|---|---|---|---|

| Level | First Difference | Level | First Difference | |

| SE | −2.492 | −3.296 *** | −1.218 | −4.772 ** |

| MOFIS | 0.821 | −5.339 *** | −1.241 | −4.249 *** |

| RQ | −2.318 | −6.380 *** | 1.383 | −7.437 *** |

| MOFIS∗RQ | 0.957 | −3.721 *** | −2.406 | −6.132 ** |

| GDP | 1.319 | −4.117 *** | 0.738 | −3.225 *** |

| FD | 2.427 | −5.194 ** | 0.859 | −8.312 *** |

| PS | −2.697 | −4.820 *** | −2.018 | −7.275 ** |

| Statistic | Value | z-Value | p-Value |

|---|---|---|---|

| Gt | −12.072 *** | −5.670 | 0.000 |

| Ga | −10.661 *** | 8.061 | 0.000 |

| Pt | −9.904 ** | −7.689 | 0.014 |

| Pa | −14.350 *** | 9.431 | 0.000 |

| Variables | Model 1 | Model 2 |

|---|---|---|

| Dynamic common-correlated effect (DCCE): | ||

| Mobile financial services | −0.042 *** (−5.420) | −0.116 *** (−3.529) |

| Regulatory quality | −0.095 *** (−4.550) | −0.173 *** (−2.926) |

| MOFIS∗RQ | −0.088 *** (−4.304) | |

| GDP per capita | −0.134 * (−1.921) | −0.106 ** (−2.048) |

| Financial development index | −0.068 ** (−2.133) | −0.017 ** (−2.311) |

| Government expenditure | 0.035 *** (−2.913) | 0.008 *** (4.138) |

| Dynamic seemingly unrelated regression (DSUR): | ||

| Mobile financial services | −0.191 *** (−2.855) | −0.110 ** (−2.101) |

| Regulatory quality | −0.006 *** (−3.232) | −0.058 *** (−4.673) |

| MOFIS∗RQ | −0.367 ** (−6.621) | |

| GDP per capita | −0.093 ** (−2.137) | 0.049 (1.308) |

| Financial development index | −0.130 *** (−5.913) | −0.008 * (−1.911) |

| Government expenditure | 0.062 * (1.922) | 0.065 ** (2.112) |

| Variable | SE | MOFIS | RQ | GDP | FD | PS |

|---|---|---|---|---|---|---|

| SE | 0.397 | 0.537 | 0.435 *** | 1.221 | 0.773 | |

| (0.152) | (1.904) | (6.917) | (0.717) | (1.393) | ||

| MOFIS | 0.038 *** | 0.192 | 0.337 *** | 0.139 | 0.227 | |

| (4.076) | (1.116) | (3.916) | (0.843) | (1.108) | ||

| RQ | 0.094 *** | 0.437 ** | 1.641 | 0.911 | 0.310 | |

| (6.115) | (2.110) | (1.304) | (1.005) | (1.49) | ||

| GDP | 0.371 ** | 0.523 | 1.024 | 2.172 | 1.874 | |

| (2.376) | (1.394) | (1.338) | (0.193) | (1.397) | ||

| FD | 0.081 *** | 0.078 *** | 0.070 | 0.371 | 0.315 | |

| (5.316) | (4.661) | (1.351) | (1.119) | (1.294) | ||

| PS | 0.288 | 0.534 | 0.302 | 0.004 | 0.219 | |

| (1.079) | (0.284) | (1.937) | (1.497) | (1.937) |

| Variables | Acronym | Measurement | Source |

|---|---|---|---|

| Shadow economy | SE | SE as a % of GDP | Elgin et al. (2021) |

| Mobile financial services | MOFISs | Mobile cellular subscriptions | WDI |

| Regulatory quality | RQ | Regulatory efficiency | Heritage Foundation |

| Economic development | GDP | GDP per capita | WDI |

| Financial development | FD | financial development index | IMF |

| Size of the public sector | PS | Government expenditure as a % of GDP | WDI |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hassan, A. Mobile Financial Services and the Shadow Economy in Southern African Countries: Does Regulatory Quality Matter? Int. J. Financial Stud. 2024, 12, 115. https://doi.org/10.3390/ijfs12040115

Hassan A. Mobile Financial Services and the Shadow Economy in Southern African Countries: Does Regulatory Quality Matter? International Journal of Financial Studies. 2024; 12(4):115. https://doi.org/10.3390/ijfs12040115

Chicago/Turabian StyleHassan, Adewale. 2024. "Mobile Financial Services and the Shadow Economy in Southern African Countries: Does Regulatory Quality Matter?" International Journal of Financial Studies 12, no. 4: 115. https://doi.org/10.3390/ijfs12040115

APA StyleHassan, A. (2024). Mobile Financial Services and the Shadow Economy in Southern African Countries: Does Regulatory Quality Matter? International Journal of Financial Studies, 12(4), 115. https://doi.org/10.3390/ijfs12040115