TARGET2 Imbalances and the ECB as Lender of Last Resort

Abstract

:

1. Introduction

2. The ECB as a Lender of Last Resort and the Potential Reflections in the TARGET2 System

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Financial Institution—Country A | National Central Bank—Country A | ||

| Assets | Liabilities | Assets | Liabilities |

| −Δ debits financial institution B | +Δ loans financial institution A | −Δ deposits financial institution A | |

| −Δ deposits National central bank A | +Δ loans National central bank A | +Δ liabilities TARGET2 ECB | |

| European Central Bank | |||

| Assets | Liabilities | ||

| +Δ claims TARGET2 National central bank A | +Δ liabilities TARGET2 National central bank B | ||

| National Central Bank—Country B | Financial Institution—Country B | ||

| Assets | Liabilities | Assets | Liabilities |

| −Δ loans financial institution B | +Δ deposits financial institution B | −Δ credits financial institution A | |

| +Δ claim TARGET2 ECB | +Δ deposits National central bank B | −Δ loans National central bank B | |

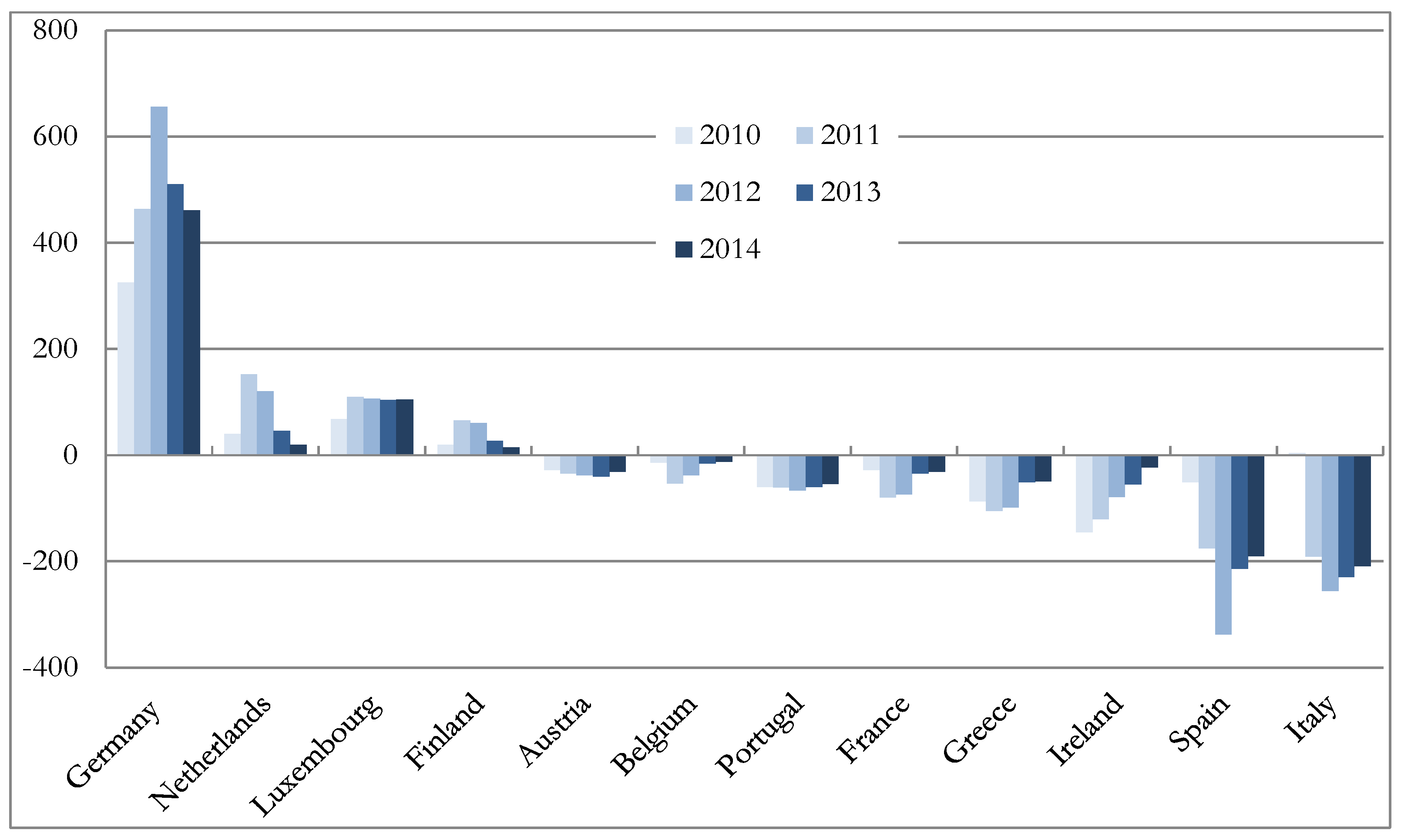

3. The Determinants of the Dynamic of the TARGET2 Balances

3.1. Macroeconomic Performance of the Peripheral Member States between the Adoption of the Euro and the Financial Crisis

3.2. Political Decisions and the TARGET2 Imbalances

4. The Need of a Lender of Last Resort

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix

| Variable | 1. Real GDP Rate of Growth | 2. Value Added Industry | 3. Value Added Construction | 4. Value Added Trade | 5. Value Added Financial Services | 6. Value Added Real Estate |

| Member State/Time | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 |

| Germany | 1.6 | 25.6 | 4.4 | 16.3 | 4.9 | 11.2 |

| Ireland | 6.4 | 26.7 | 8.3 | 16.5 | 8.7 | 7.0 |

| Greece | 4.0 | 13.6 | 7.7 | 25.9 | 4.4 | 11.7 |

| Spain | 3.9 | 19.5 | 10.9 | 23.2 | 4.8 | 7.1 |

| Italy | 1.5 | 21.1 | 5.4 | 21.1 | 5.0 | 11.3 |

| Portugal | 1.8 | 18.9 | 7.2 | 22.5 | 6.6 | 8.2 |

| Variable | 7. Deficit/Surplus-to-GDP-ratio | 8. Debt-to-GDP ratio | 9. Debt-to-GDP ratio | 10. Debt-to-GDP ratio | ||

| Member State/Time | Average 1999–2007 | 1999 | Average 1999–2007 | Average rate of change 1999–2007 | ||

| Germany | −2.2 | 60.2 | 62.4 | 0.8 | ||

| Ireland | 1.6 | 46.7 | 31.1 | −7.9 | ||

| Greece | NA | NA | NA | |||

| Spain | 0.2 | 60.9 | 48.2 | −6.1 | ||

| Italy | −2.9 | 109.6 | 102.9 | −1.2 | ||

| Portugal | −4.3 | 51.0 | 59.6 | 3.2 | ||

| Variable | 11. Net current account | 12. Net good and services | 13. Export | 14. Import | 15. Net income | 16. Net current transfers |

| Member State/Time | Average 1999–2007 | Average 1999–2007 | Average rate of change 1999–2007 | Average rate of change 1999–2007 | Average 1999–2007 | Average 1999–2007 |

| Germany | 2.7 | 3.7 | 5.8 | 5.0 | 0.3 | −1.3 |

| Ireland | −1.6 | 13.1 | −4.6 | −3.2 | −15.1 | 0.3 |

| Greece | −7.9 | −8.1 | 4.7 | 4.0 | −2.1 | 2.3 |

| Spain | −5.5 | −3.6 | −0.1 | 2.3 | −1.8 | −0.1 |

| Italy | −0.5 | 0.6 | 1.9 | 3.7 | −0.4 | −0.6 |

| Portugal | −9.3 | −8.9 | 1.2 | 1.0 | −2.5 | 2.1 |

| Variable | 17. Net direct investment | 18. Net dividends and distributed branch profits | 19. Net reinvesting earnings and undistributed branch profits | 20. Net income on debt (interest) | 21. Net portfolio investment | 22. Net current transfer general government |

| Member State/Time | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 | Average 1999–2007 |

| Ireland | −17.1 | −11.3 | −6 | 0.4 | 0.9 | −0.6 |

| Variable | 23. Net IIP | 24. Net IIP | 25. Valuation effect | 26. Sovereign bond holding, resident | 27. Sovereign bond holding, resident | 28. Sovereign bond holding, resident |

| Member State/Time | 1999 | Average 1999–2007 | Average 1999–2007 | 1999 | 2007 | Average 1999–2007 |

| Germany | 4.4 | 12.3 | 0.3 | 65% | 53% | 60% |

| Ireland | 49.4 | −8.3 | −4.5 | 45% | 10% | 25% |

| Greece | −29.3 | −59.2 | −4.9 | 66% | 29% | 51% |

| Spain | −31.3 | −47.5 | −3.9 | 69% | 50% | 55% |

| Italy | −4.8 | −13.7 | −3.2 | 68% | 51% | 58% |

| Portugal | −31.2 | −57.6 | −0.9 | 46% | 24% | 32% |

References

- European Central Bank (ECB). “The TARGET2 System.” In Target Annual Report 2011. Frankfurt, Germany: European Central Bank (ECB), 2012, pp. 31–37. [Google Scholar]

- P. Cour-Thimann. CESifo Forum Special Issue April 2013: Target Balances and the Crisis in the Euro Area. Munich, Germany: CESifo Forum, Center for Economic Studies and Ifo Institute (CESifo), 2013, Volume 14, pp. 5–50. [Google Scholar]

- H.-W. Sinn, and T. Wollmershäuser. Target Loans, Current Account Balances and Capital Flows: The ECB’s Rescue Facility. CESifo Working Paper No. 3500; Munich, Germany: Center for Economic Studies and Ifo Institute (CESifo), 2011. [Google Scholar]

- H.-W. Sinn, and T. Wollmershäuser. TARGET2 Balances and the German Financial Account in Light of the European Balance-of-Payment Crisis. CESifo Working Papers No. 4051; Munich, Germany: Center for Economic Studies and Ifo Institute (CESifo), 2012. [Google Scholar]

- H.-W. Sinn, and T. Wollmershäuser. “Target loans, current account balances and capital flows: The ECB’s rescue facility.” Int. Tax Public Financ. 19 (2012): 468–508. [Google Scholar] [CrossRef]

- S. Cesaratto. “Balance of Payments or Monetary Sovereignty? In Search of the EMU’s Original Sin—A Reply to Lavoie.” Int. J. Political Econ. 44 (2015): 142–156. [Google Scholar] [CrossRef]

- C. Panico, and F. Purificato. “Policy coordination, conflicting national interests and the European debt crisis.” Camb. J. Econ. 37 (2013): 585–608. [Google Scholar] [CrossRef]

- European Central Bank (ECB). “TARGET2 balances of national central banks in the Euro area.” Mon. Bull. 10 (2011): 35–40. [Google Scholar]

- European Central Bank (ECB). “The TARGET2 balances of national central banks (NCBs).” In TARGET2 Annual Report 2011. Frankfurt, Germany: European Central Bank (ECB), 2012, pp. 8–10. [Google Scholar]

- European Central Bank (ECB). “TARGET Balances and Monetary Policy Operations.” Mon. Bull. 5 (2013): 103–114. [Google Scholar]

- P. De Grauwe, and Y. Ji. What Germany Should Fear Most Is Its Own Fear. An analysis of TARGET2 and Current Account Imbalances. CEPS Working Paper No. 386; London, UK: Centre for Economic Policy Research (CEPR), 2012. [Google Scholar]

- Deutsche Bundesbank. “The dynamics of the Bundesbank’s TARGET2 balance.” Mon. Rep. 63 (2011): 34–35. [Google Scholar]

- M. Lavoie. “The Eurozone: Similarities to and Differences from Keynes’s Plan.” Int. J. Political Econ. 44 (2015): 1–15. [Google Scholar] [CrossRef]

- European Central Bank (ECB). “Verbatim of the remarks made by Mario Draghi: Speech by Mario Draghi, President of the European Central Bank at the Global Investment Conference in London, 26 July 2012.” Available online: https://www.ecb.europa.eu/press/key/date/2012/html/sp120726.en.html (accessed on 26 June 2015).

- European Central Bank (ECB). “Editorial.” Mon. Bull. 8 (2012): 5–7. [Google Scholar]

- U. Bindseil, and P.J. König. The Economics of TARGET2 Balances. SFB 649 Discussion Paper 2011-035; Frankfurt, Germany: European Central Bank (ECB), 2011. [Google Scholar]

- K. Whelan. “TARGET2 and central bank balance sheets.” Econ. Policy 29 (2014): 79–137. [Google Scholar] [CrossRef]

- M. Cecioni, and G. Ferrero. “Determinants of TARGET2 imbalances.” In Questioni di Economia e Finanza Banca d’Italia No. 136. Roma, Italy: Bank of Italy, 2012. [Google Scholar]

- R.A. Auer. “What drives TARGET2 balances? Evidence from a panel analysis.” Econ. Policy 29 (2014): 139–197. [Google Scholar] [CrossRef]

- S. Merler, and J. Pisani-Ferry. “Sudden Stops in the Euro Area.” Available online: http://bruegel.org/wp-content/uploads/imported/publications/pc_2012_06.pdf (accessed on 1 June 2015).

- W.H. Buiter, and E. Rahbari. “The European Central Bank as Lender of Last Resort for Sovereigns in the Eurozone.” J. Common Mark. Stud. 50 (2012): 6–35. [Google Scholar] [CrossRef]

- P. De Grauwe. “The European Central Bank as Lender of Last Resort in the Government Bond Markets.” CESifo Econ. Stud. 59 (2013): 520–535. [Google Scholar] [CrossRef]

- European Central Bank (ECB). The Implementation of Monetary Policy in the Euro Area. General Documentation on Eurosystem Monetary Policy Instruments and Procedures, Overview on the Monetary Policy Framework. Frankfurt, Germany: European Central Bank (ECB), 2011, pp. 9–14. [Google Scholar]

- K. Hu. “The Institutional Innovation of the Lender of Last Resort Facility in the Eurozone.” J. Eur. Integr. 36 (2014): 627–640. [Google Scholar] [CrossRef]

- S. Micossi. “The Monetary Policy of the European Central Bank (2002–2015).” In CEPS Special Report. Brussel, Belgium: Centre for European Policy Studies, 2015. [Google Scholar]

- N. Holinski, C.J. Kool, and J. Muysken. “Persistent macroeconomic imbalances in the euro area: Causes and consequences.” Fed. Reserv. Bank St. Louis Rev. 94 (2012): 1–20. [Google Scholar]

- Council of the European Union. “Statement by the Head of State or Government of the Euro Area and EU Institutions.” 21 July 2011. Available online: https://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/123978.pdf (accessed on 27 June 2015).

- European Central Bank (ECB). “Introductory statement to the press conference (with Q&A).” 7 July 2011. Available online: https://www.ecb.europa.eu/press/pressconf/2011/html/is110707.en.html (accessed on 27 June 2015).

- European Central Bank (ECB). “Introductory statement to the press conference (with Q&A).” 4 August 2011. Available online: https://www.ecb.europa.eu/press/pressconf/2011/html/is110804.en.html (accessed on 27 June 2015).

- European Central Bank (ECB). “Monetary and fiscal policy interactions in a monetary union.” Mon. Bull. 6 (2012): 51–64. [Google Scholar]

- Eurogroup. “Statement of the Eurogroup.” 30 March 2012. Available online: http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/129381.pdf (accessed on 27 June 2015).

- Council of the European Union. “Agreed lines of communication by Euro area Member States.” 30 January 2012. Available online: http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/127633.pdf (accessed on 27 June 2015).

- European Central Bank (ECB). “Introductory statement to the press conference (with Q&A).” 2 August 2012. Available online: https://www.ecb.europa.eu/press/pressconf/2012/html/is120802.en.html (accessed on 27 June 2015).

- European Central Bank (ECB). “Introductory statement to the press conference (with Q&A).” 6 September 2012. Available online: https://www.ecb.europa.eu/press/pressconf/2012/html/is120906.en.html (accessed on 27 June 2015).

- W. Buiter, J. Michels, and E. Rahbari. “ELA: An emperor without clothes? ” Citi Investment Research and Analysis, 21 January 2011. [Google Scholar]

- W. Buiter, and E. Rahbari. TARGET2 redux: The simple accountancy and slightly more complex economics of Bundesbank loss exposure through the Eurosystem. CEPR Discussion Paper No. DP9211; London, UK: Centre for Economic Policy Research (CEPR), 2012. [Google Scholar]

- O. Blanchard, and D. Leigh. “Growth Forecast Errors and Fiscal Multipliers.” Am. Econ. Rev. 103 (2013): 117–120. [Google Scholar] [CrossRef]

- A. Auerbach, and Y. Gorodnichenko. “Fiscal Multipliers in Recession and Expansion.” In Fiscal Policy after the Financial Crisis. Edited by G. Alesina. Chicago, IL, USA: University of Chicago Press, 2012, pp. 63–98. [Google Scholar]

- L. Christiano, M. Eichenbaum, and S. Rebelo. “When Is the Government Spending Multiplier Large? ” J. Political Econ. 119 (2011): 78–121. [Google Scholar] [CrossRef]

- G. Eggertsson, and P. Krugman. “Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach.” Q. J. Econ. 127 (2012): 1469–1513. [Google Scholar] [CrossRef]

- P. Arestis. “Fiscal policy: A strong macroeconomic role.” Rev. Keynes. Econ. 1 (2012): 93–108. [Google Scholar] [CrossRef]

- European Commission. “Debt reduction and fiscal multipliers.” Q. Rep. Euro Area 3 (2012): 22–26. [Google Scholar]

- J. Boussard, F. de Castro, and M. Salto. “Fiscal Multipliers and Public Debt Dynamics in Consolidations.” Eur. Econ. Econ. Pap., 2012. [Google Scholar] [CrossRef]

- European Central Bank (ECB). “Introductory statement to the press conference (with Q&A).” 22 January 2012. Available online: https://www.ecb.europa.eu/press/pressconf/2015/html/is150122.en.html (accessed on 16 September 2015).

- 1TARGET stands for Trans-European Automated Real-time Gross settlement Express Transfer system.

- 2See European Central Bank [1].

- 3For a comprehensive analysis of the issues raised by the dynamics of TARGET2 balances, see Cour-Thimann [2].

- 4Notice here that there were also financial support programs promoted by the Council of the European Union in favour of the governments of Greece, Ireland and Portugal, which were beneficiaries of economic and financial adjustment programmes, and Spain, which agreed for a banking recapitalization and restructuring programme. Nevertheless, we focus on the support provided by the ECB to credit institutions because it was surely more relevant according to its economic size.

- 7An example of ex ante conditionality can be the request of a specific kind of collateral, whereas ex post conditionality can be intended as the request of policy implementation (strengthening of the banking sector, fiscal adjustment, correction of excessive deficit, growth enhancing reforms).

- 8See the Treaty on the Functioning of the European Union: particularly, Art. 127, first paragraph, Art. 129, first paragraph and Art. 282, first and second paragraphs; see also the Statute of the European System of Central Banks and of the European Central Bank: Art. 1, Art. 2, Art. 3, first paragraph, and Art. 9, second paragraph.

- 9See the guidelines for the implementation of monetary policy in the Euro area (ECB [23] (p. 9)).

- 10In country A, transferring the monetary base to country B implies either the contraction of the previous amount of monetary base, if the amount of deposits held by financial institutions to the national central banks decrease, or the stability of monetary base if, on the contrary, the loans increase. In country B, the money transfer from country A implies the increase of the existing monetary base, when the amount of deposits held by the financial institutions at the national central bank increase, or maintaining the existing level of the monetary base, when loans diminish (see Table 1).

- 111999 for 11 member States with the exception of Greece that joined in 2001.

- 12The following subsectors considered here are industry (excluding construction), construction, wholesale and retail trade (that includes as well transport accommodation, food and beverages), financial and insurance activities, real estate activities.

- 13The only available data of the series for Greece are relative to 2006 and 2007 (−6.1 per cent and −6.7 per cent respectively.

- 14The Eurostat time series used for all the other member States does not include data for Greece in the period we are considering, alternative sources as OECD and World Bank indicates a value of 103.0 per cent of the GDP.

- 15In terms of trade balance, Ireland showed a positive sign with an average value of 13.0 per cent of the GDP against the 3.7 per cent in Germany and the 0.6 per cent in Italy.

- 16The first available data for Ireland and Portugal date back respectively to 2000 and 2001.

- 17European institutions and the IMF launched the first and second adjustment programme for Greece in May 2010 and March 2012, respectively; until June 2012, the total disbursements were about 150.0 billion euro, while TARGET2 liabilities increased from 82.6 billion euro in April 2010 to 106.0 in June 2012. In Portugal, the TARGET2 liabilities did not change significantly during the programme, while in Ireland they began to decline after the programme was approved.

- 18Also Spain was a country under programme: European institutions launched the recapitalization programme for the banking sector in June 2012, but the disbursements took place between December 2012 and February 2013 (about 41.0 billion euro).

- 19The Eurogroup is an informal body which members are the Ministers of Economy from each of the countries belonging to the EMU and a chairman; its meetings are also attended by the European Commissioner for Economic and Financial Affairs and by the President of ECB. The Eurogroup’s main task is to coordinate the economic policies implemented by countries in the Euro area.

- 20The EFSF is a “société anonyme”, under Luxembourgish law, which is a special vehicle with the task of raising funds through the issuance of bonds backed by the States belonging to the EMU. The funds are, then, used to implement support programmes.

- 21With the exception of the United Kingdom and Czech Republic.

- 22The new framework is based on five regulations and one directive, hence the name “The Six Pack”. The Regulations n. 1175/2011, n. 1177/2011 and n. 1173/2011, respectively, defined the procedures to prevent and correct the occurrence of excessive deficit in the structural balance of public administration, as well as the penalties for not complying with the same procedures. Regulations n. 1176 and n. 1174 defined the procedures and sanctions related to the prevention and correction of macroeconomic imbalances that can lead to instability in European Union economies. Finally, the Directive n. 2011/85/EU defined the requirements and penalties relating to the proper preparation of the public administration budget and the independence of national statistical institutes.

- 23The statistical analysis conducted in Sinn and Wollmershäuser [5] confirms this occurrence, but they attribute it mainly to the second extraordinary refinancing operation carried out by the ECB. However, it should be stressed that during this month the macroeconomic framework of the two countries does not change and, thus, it is difficult to motivate the outflow of capital solely on difference between levels of competitiveness.

- 24The SMP was the first sovereign bonds buying programme on the secondary market launched by the ECB on 10 May 2010.

- 25However, as an anonymous referee has stressed, the ECB never claimed that with introducing the OMTs a role of lender of last resort for the governments of peripheral countries could be played.

- 26Actually, the already mentioned authors are perfectly aware of the regulatory environment in which the monetary policy is decided and implemented, see Sinn and Wollmershäuser [5] (p. 487).

- 27Since the beginning of the debate on TARGET2 balances, this point has been clearly underlined by the ECB [8] (p. 40).

- 28In addition, assuming the insolvency of the Eurosystem means denying the possibility for the Eurosystem to create monetary base. Where the financial institutions of the core countries were to ask for the liquidation of the assets held at the Eurosystem, this latter would merely accept that the monetary base, until then hold in its deposits, started to fuel the economic system. The only risk of this process, in the lack of a sterilization procedure, would be an increase in the price level with the corresponding reduction in the purchasing power (De Grauwe and Ji [11]). For a full discussion on this issue, see Buiter and Rahbari [36].

- 30In fact, at the end of 2014, TARGET2 imbalances were higher than their pre-crisis level; but they could reflect both the ordinary working of a monetary union where some peripheral countries are experiencing a slower recovery compared to core countries and the contagion effect connected with the new Greek political crisis. However, this paper cannot face this issue because only during last months the recovery has been strengthening and the political crisis in Greece has been finding a solution.

- 31The ABSPP and the CBPP3 started in November and October 2014, respectively. Their aim was to enhance the well-functioning of specific segments of the financial markets and to provide the non-financial corporation in the Euro area with an easier access to credit.

- 32In 2014, the Eurosystem implemented also the Targeted Longer-Term Refinancing Operations (TLTROs), that is, refinancing operations which can be accessible by the financial institution only if they provide the non-financial sector with loans (except for loans granted to households for house purchase). The TLTROs revealed somewhat disappointing: compared with a maximum limit of loans of approximately 400 billion euro, credit institutions requested and obtained loans for a total of just 212.1 billion euro; a sign of how the recession induced by the austerity measures weakened the credit demand by households and businesses.

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Purificato, F.; Astarita, C. TARGET2 Imbalances and the ECB as Lender of Last Resort. Int. J. Financial Stud. 2015, 3, 482-509. https://doi.org/10.3390/ijfs3040482

Purificato F, Astarita C. TARGET2 Imbalances and the ECB as Lender of Last Resort. International Journal of Financial Studies. 2015; 3(4):482-509. https://doi.org/10.3390/ijfs3040482

Chicago/Turabian StylePurificato, Francesco, and Caterina Astarita. 2015. "TARGET2 Imbalances and the ECB as Lender of Last Resort" International Journal of Financial Studies 3, no. 4: 482-509. https://doi.org/10.3390/ijfs3040482