The Impact of Brexit on the Stock Markets of the Greater China Region

Abstract

:1. Introduction

2. Economic and Political Uncertainty Effects on Stock Markets

3. Background on Brexit and Implications for China

3.1. China’s Aspirations in Terms of a Market Economy

3.2. Is Brexit a Real Concern for China?

4. Data and Methodological Approach

4.1. Data Description

4.2. Uncertainty Measures (VIX and EPU)

4.3. Empirical Models

5. Findings and Analysis

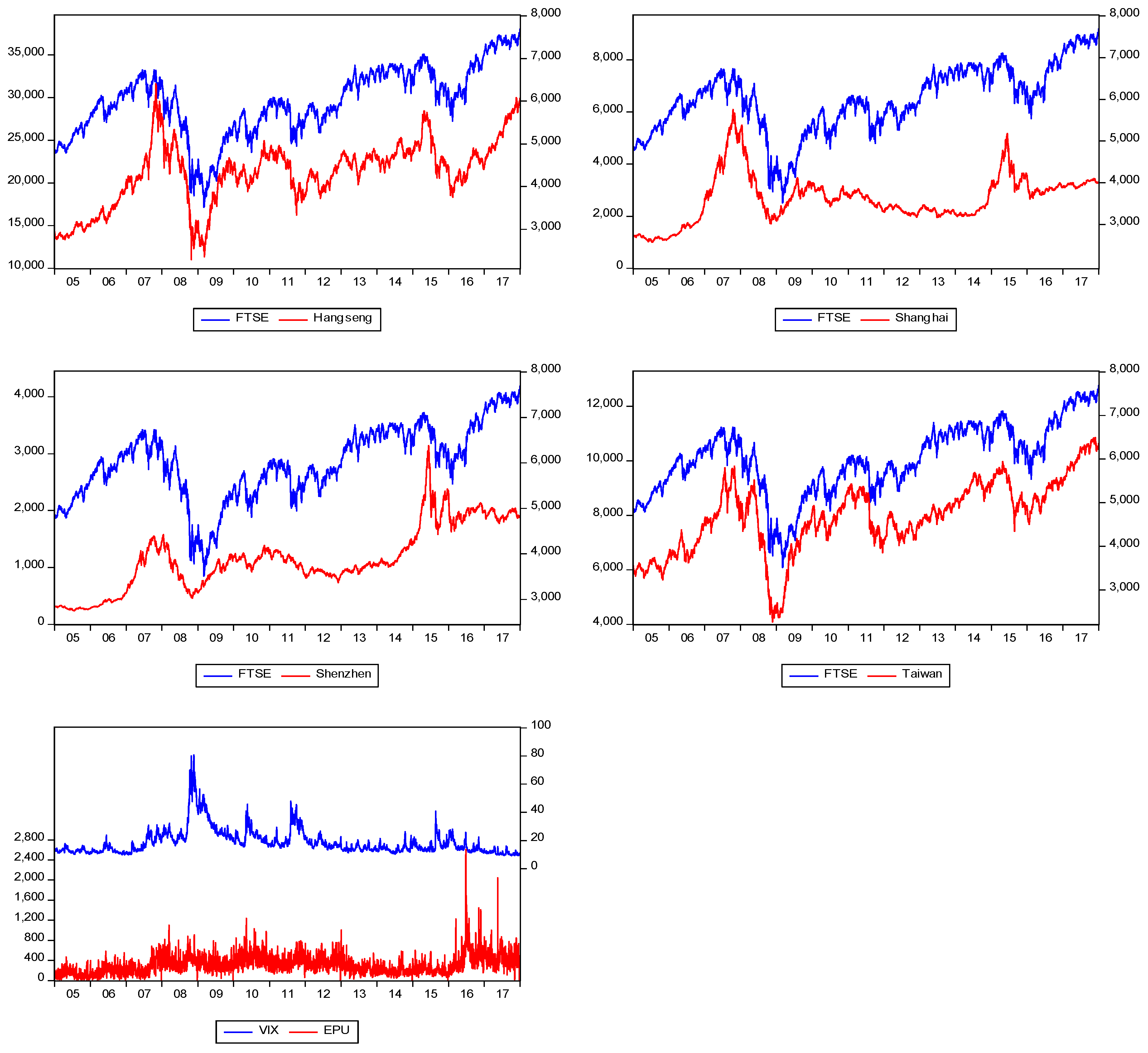

5.1. Preliminary Data Analysis

5.2. Market Models Analysis

5.3. Has the UK Political Instability Spilled-Over to Chinese Stock Markets?

6. Critical Insights and Conclusions

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Residuals Tests | Model 01 | Model 02 | Model 03 | |||

|---|---|---|---|---|---|---|

| Serial Correlation | Heterokedasticity | Serial Correlation | Heterokedasticity | Serial Correlation | Heterokedascticity | |

| Hang Seng | 1.857 (0.1568) | 16.57 * (0.000) | 1.999 (0.1362) | 20.285 * (0.000) | 14.680 * (0.000) | 26.383 (0.000) |

| Shanghai | 2.712 (0.0671) *** | 48.65 (0.000) | 2.272 (0.1039) | 50.034 * (0.000) | 7.417 * (0.000) | 41.296 (0.000) |

| Shenzhen | 1.644 (0.1945) | 37.274 (0.000) * | 0.8068 (0.4467) | 37.2635 * (0.000) | 6.7633 * (0.001) | 27.618 * (0.000) |

| Taiwan | 1.542 (0.2145) | 82.399 * (0.000) | 0.9262 (0.3966) | 80.1406 * (0.000) | 12.4208 * (0.000) | 18.7637 * (0.000) |

References

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and George Filis. 2013. Dynamic co-movements between stock market returns and policy uncertainty. Economics Letters 120: 87–92. [Google Scholar] [CrossRef] [Green Version]

- Arouri, Mohamed, Christophe Estay, Christophe Rault, and David Roubaud. 2016. Economic policy uncertainty and stock markets: Long-run evidence from the US. Finance Research Letters 18: 136–41. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2014. Measuring Economic Policy Uncertainty. Unpublished Working paper. Stanford, CA, USA: Stanford University, Chicago, IL, USA: University of Chicago. [Google Scholar]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic Policy uncertainty. The Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Baker, Scott, Nicholas Bloom, and Steven J. Davis. 2012. Measuring Economic Policy Uncertainty. Working Paper Series, Stanford, CA, USA: Stanford University. [Google Scholar]

- Benáček, Vladimir, Helena Lenihan, Bernadette Andreosso-O’Callaghan, Eva Michalíkovác, and Denis Kan. 2014. Political Risk, Institutions and Foreign Direct Investment: How Do They Relate in Various European Countries? The World Economy 37: 625–53. [Google Scholar] [CrossRef]

- Bin, Feng-Shun, Lloyd P. Blenman, and Dar-Hsin Chen. 2004. Valuation impact of currency crises: Evidence from the ADR market. International Review of Financial Analysis 13: 411–32. [Google Scholar] [CrossRef]

- Brewer, Thomas L. 1981. Political Risk Assessment for Foreign Direct Investment Decisions: Better Methods for Better Results. Columbia Journal of World Business 16: 5–12. [Google Scholar]

- Brogaard, Jonathan, and Andrew Detzel. 2014. The Asset Pricing Implications of Government Economic Policy Uncertainty. Management Science 61: 3–18. [Google Scholar] [CrossRef]

- Chang, Tsangyao, Wen-Yin Chen, Rangan Gupta, and Duc Khuong Nguyen. 2015. Are stock prices related to political uncertainty index in OECD countries? Evidence from bootstrap panel causality test. Economic Systems 39: 288–300. [Google Scholar] [CrossRef]

- Cheng, Hwahsin, and John L. Glascock. 2005. Dynamic Linkages between the Greater China Economic Area Stock Markets—Mainland China, Hong Kong, and Taiwan. Review of Quantitative Finance and Accounting 24: 343–57. [Google Scholar] [CrossRef]

- Chen, Xiurong, Yixiang Tian, and Rubo Zhao. 2017. Study of the cross-market effects of Brexit based on the improved symbolic transfer entropy GARCH model—An empirical analysis of stock-bond correlations. PLoS ONE 12: e0183194. [Google Scholar] [CrossRef] [PubMed]

- Clark, Ephraim. 1997. Valuing Political Risk. Journal of International Money and Finance 16: 477–90. [Google Scholar] [CrossRef]

- Clark, Ephraim, and Radu Tunaru. 2003. Quantification of Political Risk with Multiple Dependent Sources. Journal of Economics and Finance 27: 125–35. [Google Scholar] [CrossRef]

- European Parliament. 2016. China’s Proposed Market Economy Status: Defend EU Industry and Jobs. Available online: http://www.europarl.europa.eu/news/en/news-room/20160504IPR25859/china%E2%80%99s-proposed-market-economy-status-defend-eu-industryand-jobs-urge-meps (accessed on 11 December 2017).

- Fernández-Villaverde, Jesús, Pablo Guerrón-Quintana, Keith Kuester, and Juan Rubio-Ramírez. 2014. Fiscal Volatility Shocks and Economic Activity. American Economic Review 105: 3352–84. [Google Scholar] [CrossRef]

- Goodell, John W., and Sami Vähämaa. 2013. US presidential elections and implied volatility: The role of political uncertainty. Journal of Banking and Finance 37: 1108–17. [Google Scholar] [CrossRef]

- Guidi, Francesco, Christos S. Savva, and Mehmet Ugur. 2016. Dynamic co-movements and diversification benefits: The case of the Greater China region, the UK and the US equity markets. Journal of Multinational Financial Management 35: 59–78. [Google Scholar] [CrossRef]

- Gulen, Huseyin, and Mihai Ion. 2013. Policy Uncertainty and Corporate Investment. Working paper. West Lafayette, IN, USA: Purdue University. [Google Scholar]

- Henderson, Jane, and Eva Pils. 2016. Brexit and International Relations. The impact of Brexit on Relations with Russia and China. King’s Law Journal 27: 473–88. [Google Scholar] [CrossRef]

- Ho, Kin-Yip, and Zhaoyong Zhang. 2012. Dynamic Linkages among Financial Markets in the Greater China Region: A Multivariate Asymmetric Approach. The World Economy 35: 500–23. [Google Scholar] [CrossRef]

- Hufbauer, Gary Clyde, and Cathleen Cimino-Isaacs. 2016. The Outlook for Market Economy Status for China. Washington: Petersen Institute for International Economics, Available online: https://piie.com/blogs/trade-investment-policy-watch/outlook-market-economystatus-china (accessed on 5 November 2017).

- Kang, Wensheng, and Ronald A. Ratti. 2013. Oil shocks, policy uncertainty and stock market return. Journal of International Financial Markets, Institutions and Money 26: 305–18. [Google Scholar] [CrossRef]

- Kang, Wensheng, and Ronald A. Ratti. 2015. Policy uncertainty in China, oil shocks and stock returns. Economic Transition 23: 657–76. [Google Scholar] [CrossRef]

- Le Corre, Philippe, and Jonathan Pollack. 2017. China’s Rise: What about a transatlantic dialog? Asia Europe Journal 15: 147–60. [Google Scholar] [CrossRef]

- Lean, Hooi Hooi, and Duc Khuong Nguyen. 2014. Policy Uncertainty and performance characteristics of sustainable investments across regions around the global financial crisis. Applied Financial Economics 24: 1367–73. [Google Scholar] [CrossRef]

- Leinen, Jo. 2016. Red lines for Brexit negotiations with the UK. In Fabian Policy Report: Facing the Unknown. Edited by O. Bailey. London: Fabian Society, p. 27. [Google Scholar]

- Li, Xiao-Ming, and Lu Peng. 2017. US economic policy uncertainty and co-movements between Chinese and US stock markets. Economic Modelling 61: 27–39. [Google Scholar] [CrossRef]

- Liu, Li, and Tao Zhang. 2015. Economic policy uncertainty and stock market volatility. Finance. Research Letters 15: 99–105. [Google Scholar] [CrossRef]

- Luo, Chih-Mei. 2017. Brexit and its Implications for European Integration. European Review 25: 519–31. [Google Scholar] [CrossRef]

- Mahbubani, Kishore. 2017. It’s a Problem that America is still unable to Admit it will Become #2 to China. New Perspectives Quaterly 34: 34–39. [Google Scholar]

- Manzoor, Hasnain. 2013. Impact of pak-US relationship news on KSE-100 Index. Basic Research Journal of Business Management and Accounts 2: 1–24. [Google Scholar]

- Palamalai, Srinivasan, Mariappan Kalaiwani, and Christopher Devakumar. 2013. Stock Market Linkages in Emerging Asia-Pacific Markets. Sage Open 3: 1–15. [Google Scholar] [CrossRef]

- Pan, Rui. 2015. China’s WTO Membership and the Non-Market Economy Status: Discrimination and impediment to China’s foreign trade. Journal of Contemporary China 24: 742–57. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2012. Uncertainty about Government Policy and Stock Prices. The Journal of Finance 67: 1219–64. [Google Scholar]

- Pastor, Lubos, and Pietro Veronesi. 2013. Political uncertainty and risk premia. Journal of Financial Economics 110: 520–45. [Google Scholar]

- People’s Daily. 2016. China’s Economy Likely to Follow “L-Shaped” Path in Coming Years, Says an “Authoritative Insider”. People’s Daily. May 9. Available online: http://en.people.cn/n3/2016/0509/c98649-9055137.html (accessed on 11 January 2018).

- Reboredo, Juan C., and Gazi Salah Uddin. 2016. Do financial stress and policy uncertainty have an impact on the energy and metals markets? A quantile regression approach. International Review of Economics and Finance 43: 284–98. [Google Scholar] [CrossRef]

- Root, Franklin. 1973. Analysing Political Risks in International Business. In Multinational Enterprise in Transition. Edited by Kapoor Ashok and Phillip D. Grub. Hoboken: Wiley Online Library. [Google Scholar]

- Simon, Jeffrey D. 1982. Political Risk Assessment: Past Trends and Future Prospects. Columbia Journal of World Business 17: 62–70. [Google Scholar]

- Yu, Jie. 2017. After Brexit: Risks and Opportunities to EU-China Relations. Global Policy 8: 109–14. [Google Scholar] [CrossRef]

- Yu, Jie. 2016a. China is an Unexpected Strong Supporter of the Remain Camp, LSE Blog. Available online: http://blogs.lse.ac.uk/brexit/2016/06/15/china-is-an-unexpectedly-strong-supporter-of-the-remaincamp/ (accessed on 13 December 2017).

- Yu, Jie. 2016b. China’s Brexit Dilemma, Heinrich Boell Stiftung Dossier. Available online: https://www.boell.de/en/2016/07/28/chinasbrexit-dilemma (accessed on 21 November 2017).

- Wang, Shucheng. 2017. Brexit’s Challenge to Globalization and Implications for Asia: A Chinese Perspective. Journal of East Asia and International Law 10: 47–64. [Google Scholar] [CrossRef]

- Wang, Yizhong, Carl R. Chen, and Ying Sophie Huang. 2014. Economic policy uncertainty and corporate investment: Evidence from China. Pacific-Basin Finance Journal 26: 227–43. [Google Scholar] [CrossRef]

| 1 | The results for the augmented Dickey–Fuller (ADF) test, vector autoregression (VAR) model for lag selection and Bai–Perron for structural breaks are not reported for the sake of brevity but are available upon request. |

| GCR Indices | UK Index | British Referendum | Risk Free Rate | Uncertainty Indices |

|---|---|---|---|---|

| Shanghai Se Composite (Mainland China) | FTSE 100 | 24th June 2016 to December 2017 * | UK T-Bill (3 month) | CBOE SPX Volatility (VIX) |

| Shenzhen Se Composite (Mainland China) | UK Economic Policy Uncertainty (EPUi) | |||

| Hang Seng (Hong Kong) | ||||

| TSE SE Composite (Taiwan) |

| Correlations | EPU | VIX | FTSE 100 | Hang Seng | Shanghai | Shenzhen | Taiwan |

|---|---|---|---|---|---|---|---|

| EPU | 1.00 | 0.10 | −0.07 | −0.06 | −0.02 | −0.03 | −0.04 |

| VIX | 0.10 | 1.00 | −0.49 | −0.24 | −0.17 | −0.16 | −0.23 |

| FTSE 100 | 1.00 | 0.46 | 0.16 | 0.15 | 0.40 | ||

| Hang Seng | 1.00 | 0.49 | 0.43 | 0.61 | |||

| Shanghai | 1.00 | 0.90 | 0.28 | ||||

| Shenzhen | 1.00 | 0.26 | |||||

| Taiwan | 1.00 |

| Daily Returns | FTSE 100 | Hang Seng | Shanghai | Shenzhen | Taiwan |

|---|---|---|---|---|---|

| Mean | 0.000143 | 0.000144 | −0.00046 | −0.00055 | 0.000132 |

| Std. Dev. | 0.01 | 0.01 | 0.02 | 0.02 | 0.01 |

| Skewness | −0.15 | −0.48 | −1.49 | −1.15 | −0.52 |

| Kurtosis | 5.86 | 6.36 | 11.22 | 7.31 | 7.14 |

| Jarque–Bera | 231.86 | 341.61 | 2142.47 | 670.65 | 510.21 |

| Observations | 673 | 673 | 673 | 673 | 673 |

| Index | ||||

|---|---|---|---|---|

| Hang Seng | −0.00114 *** (0.0641) | −0.17217 * (0.000) | 0.414099 * (0.000) | 0.002088 * (0.0098) |

| Shanghai | −0.00174 *** (0.0627) | 0.035676 (0.3522) | 0.270693 * (0.000) | 0.001971 (0.1064) |

| Shenzhen | −0.00137 (0.2269) | 0.073093 *** (0.0580) | 0.238844 * (0.000) | 0.001261 (0.3961) |

| Taiwan | −0.00042 (0.4769) | −0.07306 *** (0.0741) | 0.232554 * (0.000) | 0.000914 (0.1367) |

| Index | ||||||||

|---|---|---|---|---|---|---|---|---|

| Hang Seng | −0.00111 *** (0.0724) | −0.2104 * (0.000) | 0.480941 * (0.000) | −0.00327 ** (0.0102) | 0.002076 ** (0.0101) | 0.08463 (0.3286) | −0.20593 ** (0.0420) | 0.003061 ** (0.0456) |

| Shanghai | −0.00162 *** (0.0833) | 0.034777 (0.3854) | 0.374193 * (0.000) | −0.00258 (0.1794) | 0.00199 (0.1026) | −0.06959 (0.6092) | −0.35048 ** (0.0133) | 0.003079 (0.1837) |

| Shenzhen | −0.00124 (0.2744) | 0.078269 *** (0.0586) | 0.364629 * (0.000) | −0.00456 *** (0.0515) | 0.001276 (0.3893) | −0.08247 (0.4620) | −0.44308 ** (0.0100) | 0.005348 *** (0.0581) |

| Taiwan | −0.00042 (0.3704) | −0.06704 (0.2035) | 0.226722 * (0.000) | −0.00135 (0.1682) | 0.000928 (0.1331) | −0.02231 (0.7914) | 0.009932 (0.8959) | 0.001094 (0.3522) |

| Index | ||||||||

|---|---|---|---|---|---|---|---|---|

| Hang Seng | −0.00103 *** (0.0761) | −0.22635 * (0.000) | 0.506766 * (0.000) | −0.05858 * (0.000) | 0.001976 * (0.009) | 0.103292 (0.2088) | −0.2245 ** (0.0196) | 0.048714 * (0.000) |

| Shanghai | −0.00157 *** (0.0842) | 0.02921 (0.4537) | 0.39167 * (0.000) | −0.06464 * (0.000) | 0.00193 (0.1031) | −0.06314 (0.6342) | −0.36605 * (0.008) | 0.063813 * (0.000) |

| Shenzhen | −0.00116 (0.2958) | 0.076432 *** (0.0590) | 0.387264 * (0.000) | −0.07237 * (0.000) | 0.001185 (0.4127) | −0.0818 (0.4568) | −0.46328 * (0.0060) | 0.071946 * (0.000) |

| Taiwan | −0.00032 (0.4716) | −0.10876 ** (0.0290) | 0.252908 * (0.000) | −0.04694 * (0.000) | 0.000823 (0.1559) | 0.020725 (0.7943) | −0.01671 (0.8155) | 0.046358 * (0.000) |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Morales, L.; Andreosso-O’Callaghan, B. The Impact of Brexit on the Stock Markets of the Greater China Region. Int. J. Financial Stud. 2018, 6, 51. https://doi.org/10.3390/ijfs6020051

Morales L, Andreosso-O’Callaghan B. The Impact of Brexit on the Stock Markets of the Greater China Region. International Journal of Financial Studies. 2018; 6(2):51. https://doi.org/10.3390/ijfs6020051

Chicago/Turabian StyleMorales, Lucía, and Bernadette Andreosso-O’Callaghan. 2018. "The Impact of Brexit on the Stock Markets of the Greater China Region" International Journal of Financial Studies 6, no. 2: 51. https://doi.org/10.3390/ijfs6020051

APA StyleMorales, L., & Andreosso-O’Callaghan, B. (2018). The Impact of Brexit on the Stock Markets of the Greater China Region. International Journal of Financial Studies, 6(2), 51. https://doi.org/10.3390/ijfs6020051