Why Is the Correlation between Crude Oil Prices and the US Dollar Exchange Rate Time-Varying?—Explanations Based on the Role of Key Mediators

Abstract

:1. Introduction

2. Data and Empirical Model

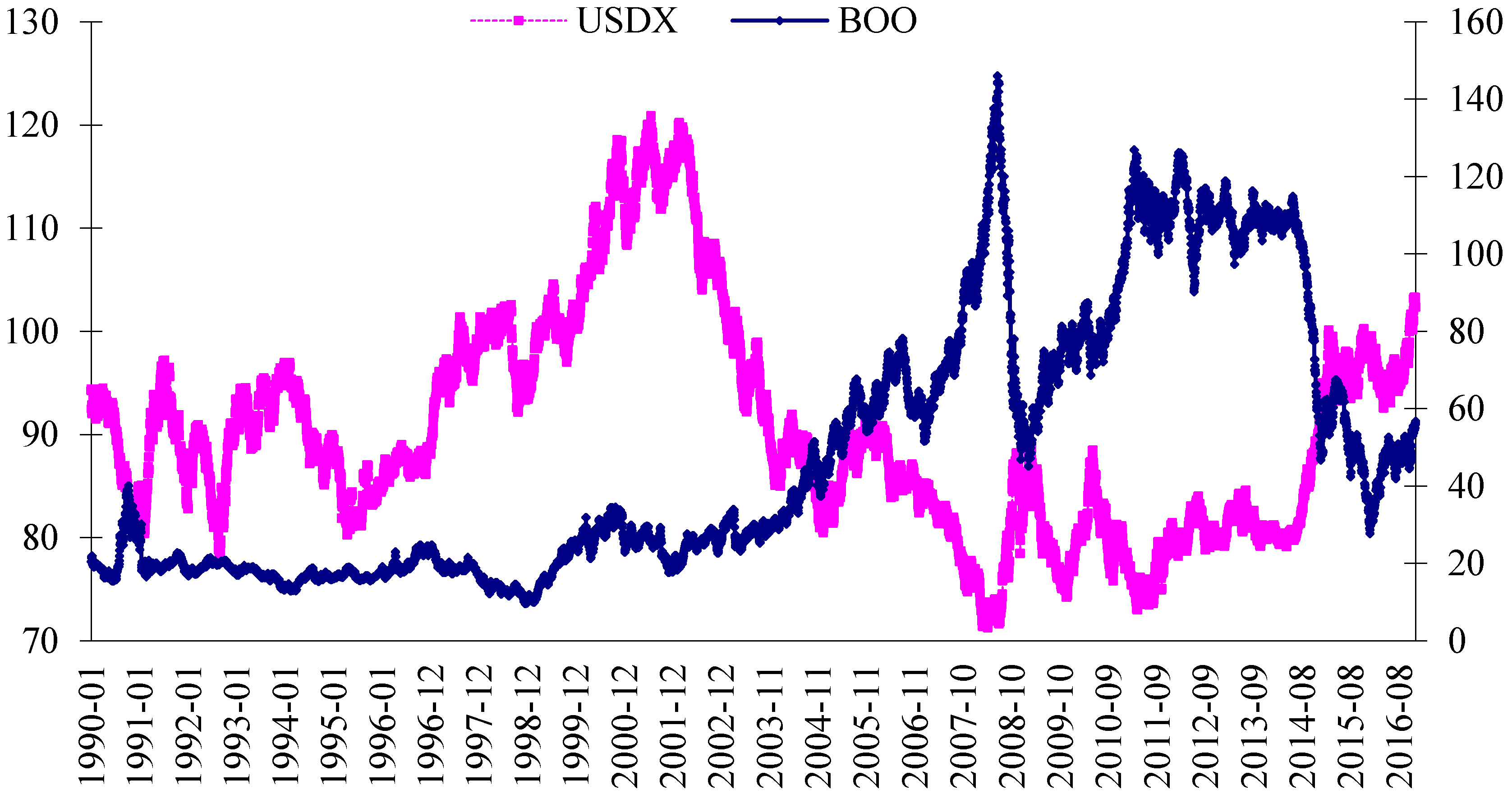

2.1. Data

2.2. DCC–GARCH Method

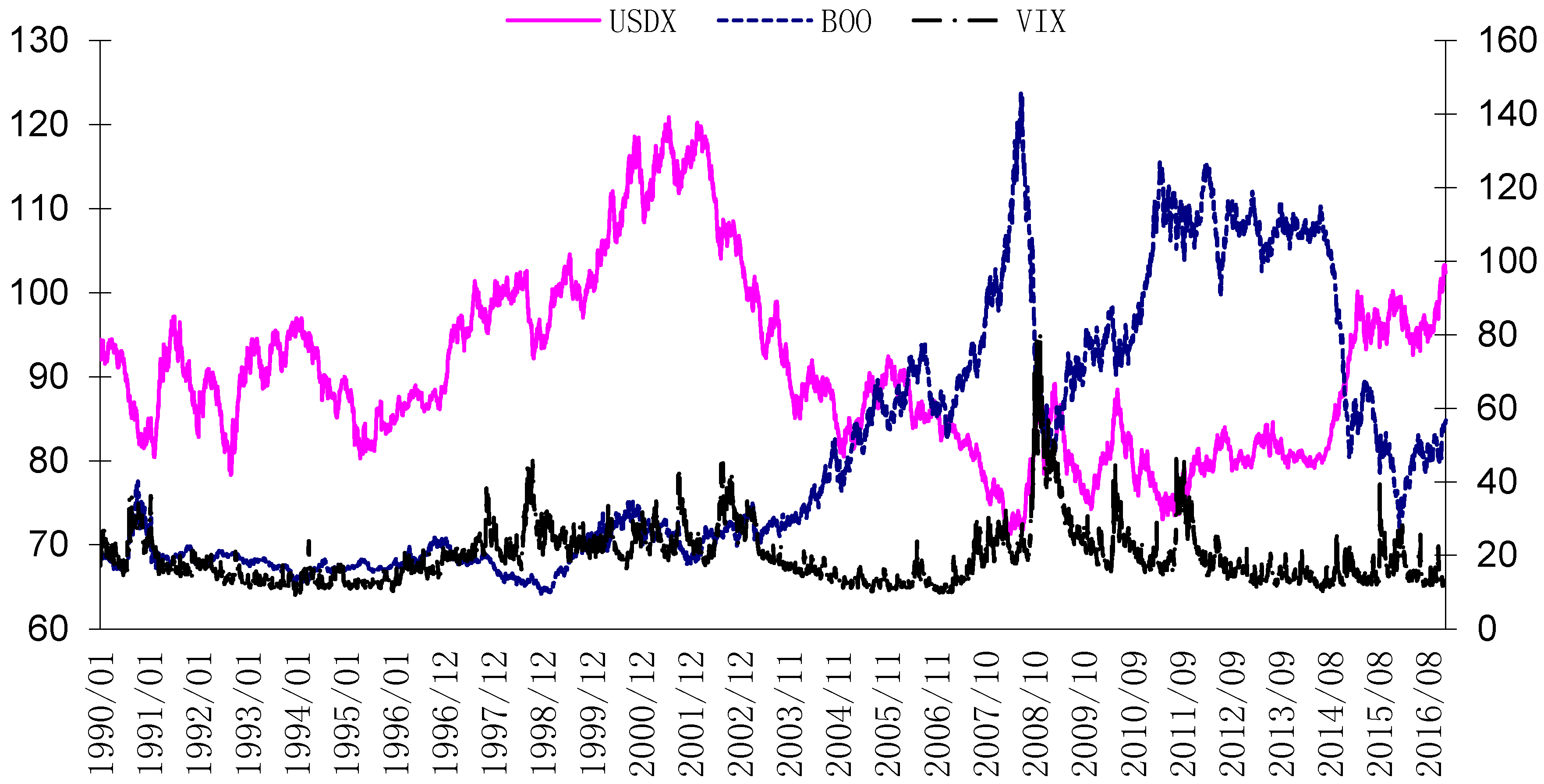

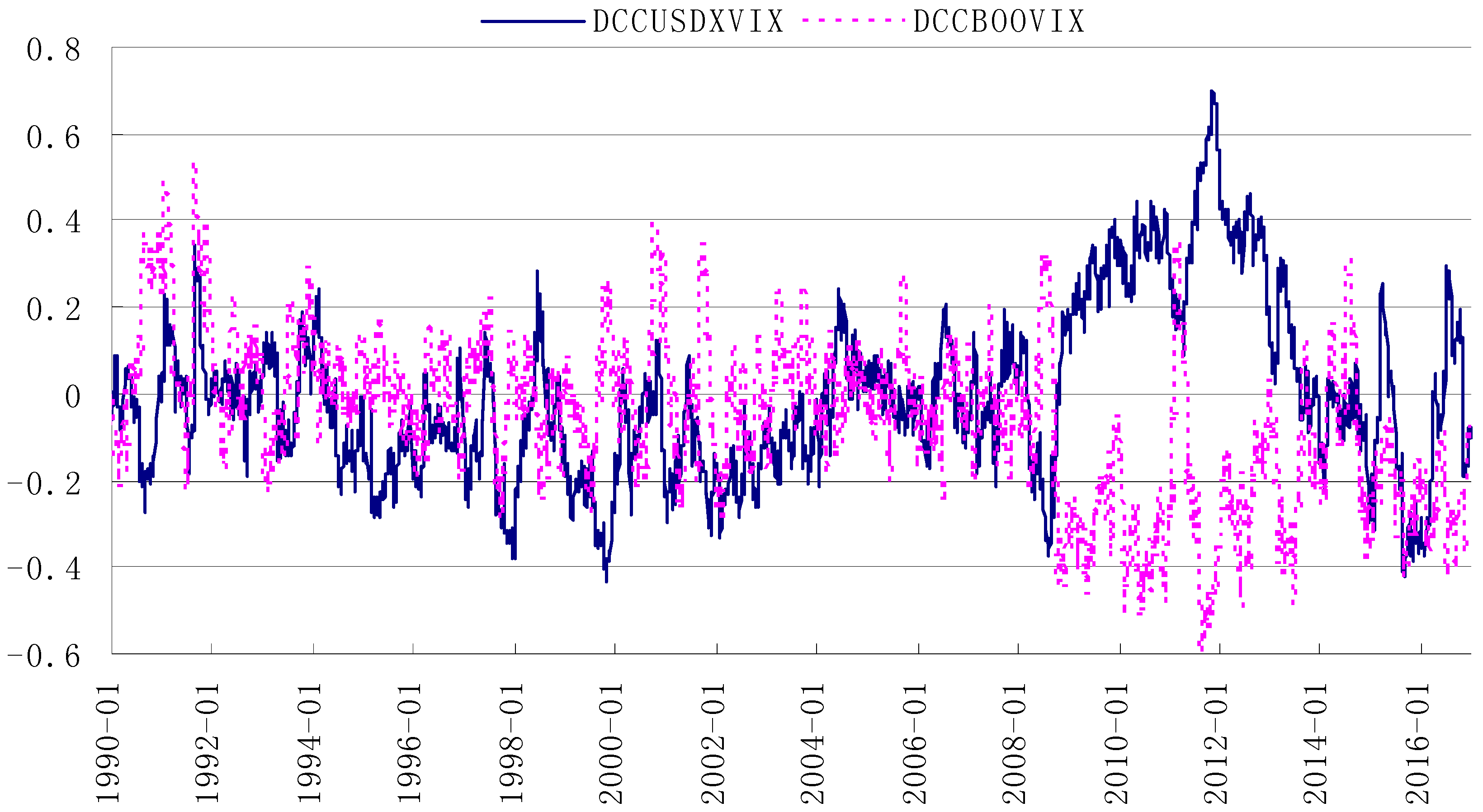

2.3. Empirical Results

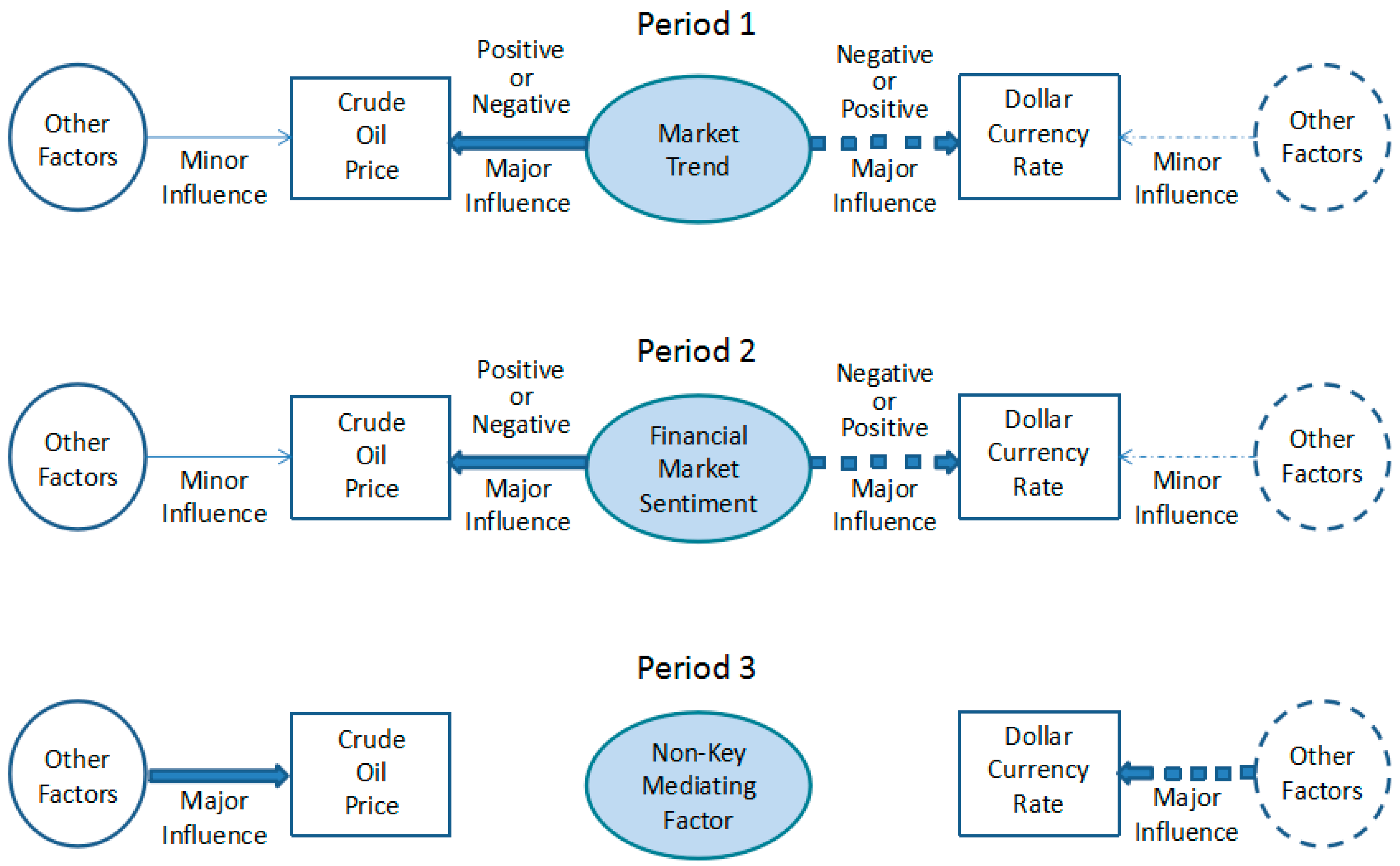

3. Hypothesis and Explanation of ‘Key Mediating Factors’

3.1. Market Trend

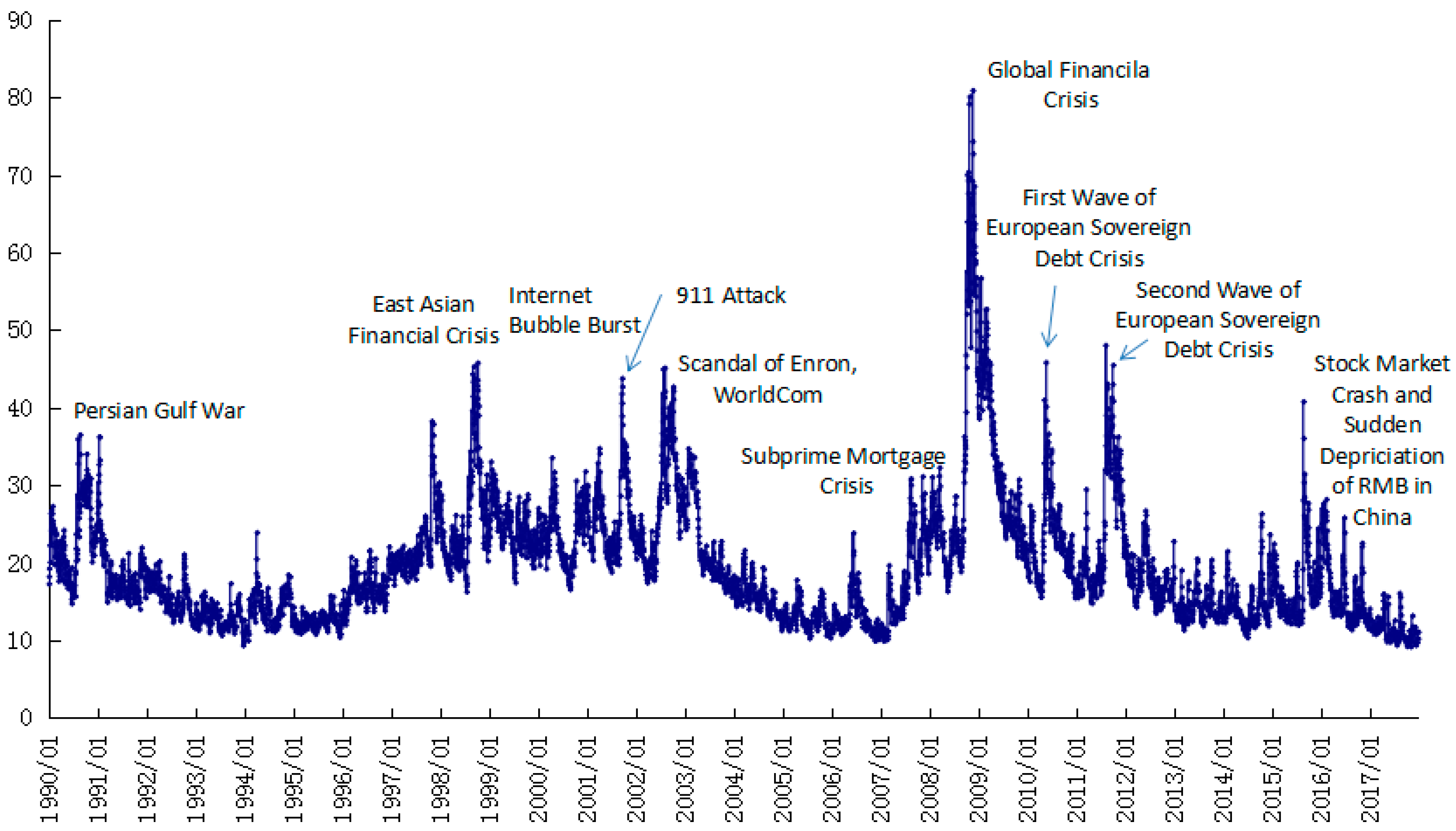

3.2. Financial Market Sentiment

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Anzuini, Alessio, Marco J. Lombardi, and Patrizio Pagano. 2012. The Impact of Monetary Policy Shocks on Commodity Prices. Bank of Italy Working Paper, No. 851. Roma, Italy. [Google Scholar] [Green Version]

- Behar, Alberto, and Robert A. Ritz. 2017. OPEC vs. US shale: Analyzing the shift to a market-share strategy. Energy Economics 63: 185–98. [Google Scholar] [CrossRef]

- Bu, Hui. 2014. Effect of inventory announcements on crude oil price volatility. Energy Economics 46: 485–94. [Google Scholar] [CrossRef]

- Büyükşahin, Bahattin, and Jeffrey H. Harris. 2011. Do Speculators Drive Crude Oil Futures? Energy Journal 32: 167–202. [Google Scholar] [CrossRef]

- Cairns, John, Corrinne Ho, and Robert N. McCauley. 2007. Exchange Rates and Global Volatility: Implications for Asia-Pacific Currencies. BIS Quarterly Review, 41–52. [Google Scholar]

- Chen, Hao, Hua Liao, Bao-Jun Tang, and Yi-Ming Wei. 2016. Impacts of OPEC’s political risk on the international crude oil prices: An empirical analysis based on the SVAR models. Energy Economics 57: 42–49. [Google Scholar] [CrossRef]

- Cheng, Kevin C. 2008. Dollar depreciation and commodity prices. In World Economic Outlook (April 2008). Washington: IMF, pp. 48–50. [Google Scholar]

- Cheng, Ing Haw, and Xiong Wei. 2013. The Financialization of Commodity Markets. NBER Working Paper No. 19642. Cambridge, MA, USA: NBER. [Google Scholar] [Green Version]

- Cifarelli, Giulio, and Giovanna Paladino. 2010. Oil price dynamics and speculation: A multivariate financial approach. Energy Economics 32: 363–72. [Google Scholar] [CrossRef]

- Coudert, Virginie, and Valérie Mignon. 2016. Reassessing the empirical relationship between the oil price and the dollar. Energy Policy 95: 147–57. [Google Scholar] [CrossRef]

- Demirer, Rıza, and Ali M. Kutan. 2010. The behavior of crude oil spot and futures prices around OPEC and SPR announcements: An event study perspective. Energy Economics 32: 1467–76. [Google Scholar] [CrossRef]

- Engle, Robert F. 2002. Dynamic Conditional Correlation—A Simple Class of Multivariate GARCH Models. Journal of Business and Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Erten, Bilge, and Jose Antonio Ocampo. 2012. Super-cycles of commodity prices since the mid-nineteenth century. DESA Working Paper, No. 110. New York, NY, USA: United Nations Department of Economic and Social Affairs. [Google Scholar]

- Fattouh, Bassam, and Pasquale Scaramozzino. 2011. Uncertainty, Expectations, and Fundamentals: Whatever Happened to Long-Term Oil Prices? Oxford Review of Economic Policy 27: 186–206. [Google Scholar] [CrossRef]

- Golombeka, Rolf, Alfonso A. Irarrazabal, and Lin Ma. 2018. OPEC’s market power: An empirical dominant firm model for the oil market. Energy Economics 70: 98–115. [Google Scholar] [CrossRef]

- Jawadi, Fredj, Waël Louhichi, Hachmi Ben Ameur, and Abdoulkarim Idi Cheffou. 2016. On oil-US exchange rate volatility relationships: An intraday analysis. Economic Modelling 59: 329–34. [Google Scholar] [CrossRef]

- Karali, Berna, and Octavio A. Ramirez. 2014. Macro determinants of volatility and volatility spillover in energy markets. Energy Economics 46: 413–421. [Google Scholar] [CrossRef]

- Kaufmann, Robert, and Ben Ullman. 2009. Oil prices, speculation, and fundamentals: Interpreting causal relations among spot and futures prices. Energy Economics 31: 550–58. [Google Scholar] [CrossRef]

- Kilian, Lutz. 2009. Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market. American Economic Review 99: 1053–69. [Google Scholar] [CrossRef]

- Kilian, Lutz, and Thomas K. Lee. 2014. Quantifying the speculative component in the real price of oil: The role of global oil inventories. Journal of International Money and Finance 42: 71–87. [Google Scholar] [CrossRef]

- Killian, Lutz. 2016. The Impact of the Shale Oil Revolution on U.S. Oil and Gasoline Prices. Review of Environmental Economics and Policy 10: 185–205. [Google Scholar] [CrossRef] [Green Version]

- Krichene, Noureddine. 2005. A Simultaneous Equations Model for World Crude Oil and Natural Gas Markets. IMF Working Paper WP/05/32. Washington, DC, USA: IMF. [Google Scholar]

- Lizardo, Radhamés A., and André V. Mollick. 2010. Oil price fluctuations and U.S. dollar exchange rates. Energy Economics 32: 399–408. [Google Scholar] [CrossRef]

- Martina, Esteban, Eduardo Rodriguez, Rafael Escarela-Perez, and Jose Alvarez-Ramirez. 2011. Multiscale entropy analysis of crude oil price dynamics. Energy Economics 33: 936–47. [Google Scholar] [CrossRef]

- McCauley, Robert, and Peter McGuire. 2009. Dollar Appreciation in 2008: Safe Haven, Carry Trades, Dollar Shortage and Overhedging. BIS Quarterly Review, 85–93. [Google Scholar]

- McLeod, Roger C. D., and Andre Yone Haughton. 2018. The value of the US dollar and its impact on oil prices: Evidence from a non-linear asymmetric cointegration approach. Energy Economics 70: 61–69. [Google Scholar] [CrossRef]

- Mensah, Lord, Pat Obi, and Godfred Bokpin. 2017. Cointegration test of oil price and US dollar exchange rates for some oil dependent economies. Research in International Business and Finance 42: 304–11. [Google Scholar] [CrossRef]

- Qadan, Mahmoud, and Hazar Nama. 2018. Investor sentiment and the price of oil. Energy Economics 69: 42–58. [Google Scholar] [CrossRef]

- Ranaldo, Angelo, and Paul Söderlind. 2007. Safe Haven Currencies. Swiss National Bank Working Papers No. 17. Zurich, Switzerland. [Google Scholar]

- Ratti, Ronald A., and Joaquin L. Vespignani. 2016. Oil prices and global factor macroeconomic variables. Energy Economics 59: 198–212. [Google Scholar] [CrossRef]

- Reboredo, Juan Carlos, Miguel A. Rivera-Castro, and Gilney F. Zebende. 2014. Oil and US dollar exchange rate dependence: A detrended cross-correlation approach. Energy Economics 42: 132–39. [Google Scholar] [CrossRef]

- Richard, Portes, and Helene Rey. 1998. Euro vs. dollar, Will the euro replace the dollar as the world currency? Economic Policy April: 306–42. [Google Scholar]

- Tang, Ke, and Xiong Wei. 2012. Index Investment and the Financialization of Commodities. Financial Analysts Journal 68: 54–74. [Google Scholar] [CrossRef] [Green Version]

- Wu, Chih-Chiang, Huimin Chung, and Yu-Hsien Chang. 2012. The economic value of co-movement between oil price and exchange rate using copula-based GARCH models. Energy Economics 34: 270–82. [Google Scholar] [CrossRef]

- Yousefi, Ayoub, and Tony S. Wirjanto. 2004. The empirical role of the exchange rate on the crude-oil price formation. Energy Economics 26: 783–99. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, Ying Fan, Hsien-Tang Tsai, and Yi-Ming Wei. 2008. Spillover effect of US dollar exchange rate on oil prices. Journal of Policy Modeling 30: 973–91. [Google Scholar] [CrossRef]

| 1 | Wind Information Co., Ltd (Wind Info) is a leading integrated service provider of financial data, information, and software. It has built up a substantial, highly-accurate, first-class financial database, which includes stocks, funds, bonds, FX, insurance, futures, derivatives, commodities, and macroeconomic and financial news. The company’s data are frequently quoted by Chinese and English media, in research reports, and in academic theses. More details about Wind Info, see website: http://www.wind.com.cn/en/aboutus.html. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Statistical Description | ||

|---|---|---|

| Mean | 0.000170 | −3.06 × 10−7 |

| Maximum | 0.147017 | 0.029498 |

| Minimum | −0.427223 | −0.032521 |

| Standard deviation | 0.021708 | 0.005240 |

| Skewness | −1.265616 | −0.065566 |

| Kurtosis | 29.47695 | 4.962633 |

| Jarque–Bera statistic | 194,132.2 | 1061.753 |

| Observations | 6972 | 6972 |

| Parameters | Coefficient |

|---|---|

| 0.000 ** | |

| 0.041 *** | |

| 0.933 *** | |

| 0.997 | |

| 0.000 *** | |

| 0.032 *** | |

| 0.967 *** | |

| 0.999 | |

| 0.004 *** | |

| 0.995 *** | |

| LogLikelihood | 44,886 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liao, J.; Shi, Y.; Xu, X. Why Is the Correlation between Crude Oil Prices and the US Dollar Exchange Rate Time-Varying?—Explanations Based on the Role of Key Mediators. Int. J. Financial Stud. 2018, 6, 61. https://doi.org/10.3390/ijfs6030061

Liao J, Shi Y, Xu X. Why Is the Correlation between Crude Oil Prices and the US Dollar Exchange Rate Time-Varying?—Explanations Based on the Role of Key Mediators. International Journal of Financial Studies. 2018; 6(3):61. https://doi.org/10.3390/ijfs6030061

Chicago/Turabian StyleLiao, Jia, Yu Shi, and Xiangyun Xu. 2018. "Why Is the Correlation between Crude Oil Prices and the US Dollar Exchange Rate Time-Varying?—Explanations Based on the Role of Key Mediators" International Journal of Financial Studies 6, no. 3: 61. https://doi.org/10.3390/ijfs6030061

APA StyleLiao, J., Shi, Y., & Xu, X. (2018). Why Is the Correlation between Crude Oil Prices and the US Dollar Exchange Rate Time-Varying?—Explanations Based on the Role of Key Mediators. International Journal of Financial Studies, 6(3), 61. https://doi.org/10.3390/ijfs6030061