1. Introduction

The world faced many challenges in 2020, starting with the new coronavirus (COVID-19) pandemic, moving to the oil price crash, and ending with new variants of the coronavirus. Since the declaration of COVID-19 as a global pandemic on 11 March 2020, followed by the announcement of worldwide lockdowns, all financial and non-financial sectors have been in shock. Lockdowns were the first response of governments and regulatory bodies to this pandemic. However, the lockdowns hurt all macroeconomic indicators (e.g., unemployment rates, inflation rates) and deteriorated the liquidity and stability of stock markets (

Zhang et al. 2020;

Baig et al. 2021). Nonetheless, different regulatory bodies applied many actions to mitigate the catastrophic effect of the COVID-19 pandemic. Incentive packages and credit facilities were provided by the governments of developed and emerging countries to offset some effects of the pandemic (

Capelle-Blancard and Desroziers 2020;

Topcu and Gulal 2020).

Accordingly, the effects of this pandemic became a key interest to many scholars. They have linked the COVID-19 pandemic to many financial and non-financial aspects. Several scholars investigated the effects of COVID-19 on financial market indices, primarily a significant negative effect (

Zhang et al. 2020;

Topcu and Gulal 2020;

Li et al. 2020;

Shehzad et al. 2020;

Liu et al. 2020;

Anh and Gan 2020;

Erdem 2020). With regards to

Akhtaruzzaman et al. (

2021a) the authors investigated how financial contagion has occurred between China and G7 countries through financial and non-financial firms during the COVID-19 period. Their results showed that financial and non-financial firms have experienced a significant increase in conditional correlations between their stock returns. Moreover, the magnitude of the increase has been higher for financial firms during the COVID-19 outbreak. Moreover, in

Akhtaruzzaman et al. (

2021b) the authors examined the dynamic relationship between the COVID-19 media coverage index (MCI) and ESG leader indices. On the one hand, their findings provide evidence that the MCI plays a role in facilitating the transmission of contagion to advanced and emerging equity markets during the pandemic. On the other hand, the COVID-19 outbreak has had a substantial effect on financial markets’ volatility. Specifically,

Harjoto et al. (

2020) and

Ali et al. (

2020) showed that this pandemic has had a significant effect in increasing the volatility and risk of financial markets. Moreover,

Baig et al. (

2021) showed that COVID-19 indicators presented by increasing the number of confirmed cases and deaths are associated with a significant increase in US equity market volatility. In the same field, although

Salisu et al. (

2020a) found that emerging markets are more exposed to the risk of pandemics and epidemics (UPE), these markets show less hedging status compared with developed markets. In addition, the findings of

Hevia and Neumeyer (

2020) showed that the effect of the COVID-19 pandemic was worse in developing countries compared with developed countries, as developing countries have suffered from deteriorating exports and diminishing remittances within the pandemic period.

This pandemic affects stock market indices in general and specific sector indices in specific cases. One of the vital sector indices is the banking sector index, which has the highest volume. It is considered the main driver of the financial market index and has a strong effect on both the economy and financial markets. Only a few researchers have investigated the impact of COVID-19 on the banking sector and banking sector index, and they have found a severe effect of the pandemic on the banking sector (

Singh and Bodla 2020;

Wu and Olson 2020;

Cakranegara 2020;

Li et al. 2021). In

Elnahass et al. (

2021), the authors provided strong evidence that, in the global banking sector, the COVID-19 outbreak has had a detrimental effect on financial performance across many indicators of financial performance and financial stability. According to

Demirgüç-Kunt et al. (

2021), although financial sector policy announcements (i.e., liquidity support, monetary easing, and borrower assistance programs) moderated the negative impact of the pandemic, this impact has varied significantly across banks and countries. Besides, the findings of

Demir and Danisman (

2021) indicated that listed banks’ returns, accompanied with better bank-specific factors (i.e., higher capitalization and deposits, more diversification, fewer non-performing loans, and larger size) have been more resilient to the COVID-19 pandemic.

Saudi Arabia is located at the heart of the Arab world. It is the world’s largest oil exporter and second largest producer of oil in the world. The country is considered a World Bank high-income economy and is a member of the Gulf Corporation Council, OPEC, and the only Arab member of the G20. According to Saudi Vision 2030, the kingdom is deploying its strategic location to build its role as an integral driver of international trade and to connect three continents: Africa, Asia, and Europe. In addition, Saudi Arabia is using its investment power to create a diverse and sustainable economy. Even though the Saudi economy is the largest in the Middle East and the ninth largest in the world, it has experienced negative consequences due to COVID-19, the subsequent lockdowns, and the later oil prices crash. The consequences of COVID-19 for the Saudi economy worsened most of the macroeconomic indicators in 2020; GDP growth decreased to −3.7%, the budget deficit reached approximately SAR 298 billion, public debt rose to SAR 854 billion, the TASI hit the bottom at −29.7%, and the unemployment rate increased to 15.4%. As a consequence, the Fitch and Moody’s credit rating agencies downgraded the outlook of the Saudi economy.

Moreover, the Saudi economy and banking sector have been facing a difficult period as the economy faces a dual threat from COVID-19 and oil prices. The pandemic has caused substantial deterioration in Saudi banks’ asset quality, heavy losses in savings accounts, and increased demand for credit with no genuine tendency to save. Therefore, Saudi banking aggregate income decreased by 28% in September 2020 as income fell from SAR 34.77 billion in September 2019 to SAR 25.07 billion in the same period of 2020. Although the Saudi government intervened in the early stages of COVID-19, the Saudi stock market index and banking sector index faced serious challenges and obstacles in mitigating the severe outcomes of the pandemic. Few researchers have investigated the effect of this pandemic on the Saudi financial market index, and even fewer have examined the Saudi banking sector (

Chaouachi and Slim 2020;

Al-Tamimi and Abdalla 2021).

Many researchers studied the effect of the pandemic on different equity markets’ indices. However,

Zhang et al. (

2020),

Baig et al. (

2021),

Akhtaruzzaman et al. (

2020), and

Akhtaruzzaman et al. (

2021a) concentrated on the damage that was accompanied by their financial markets in developed and emerging countries. Few researchers focused on the effect of this pandemic on either developing markets or on Saudi Arabia’s financial market. Besides, researchers were interested in studying the effect of COVID-19 on the whole index with no specification for special sectors. Few academics studied the effect on specific sectors, such as the banking sector index (

Elnahass et al. 2021;

Demirgüç-Kunt et al. 2021;

Demir and Danisman 2021). In investigating the effect of this pandemic on equity markets, most researchers applied different models of regression analysis. However, researchers rarely used advanced prediction and intelligent models to specify the ability to build robust prediction systems that can be used in any similar circumstances in the future. Moreover, the importance of these prediction models appears strongly dependent on their ability to specify the best parameters for future prediction. Furthermore, the COVID-19 indicators that were implemented by scholars differ from one study to another. Some researchers focused on the number of confirmed cases and death cases, whereas a few examined the effect of government regulations and decreasing interest rate. Even fewer researchers link the effect of oil crash on different equity markets.

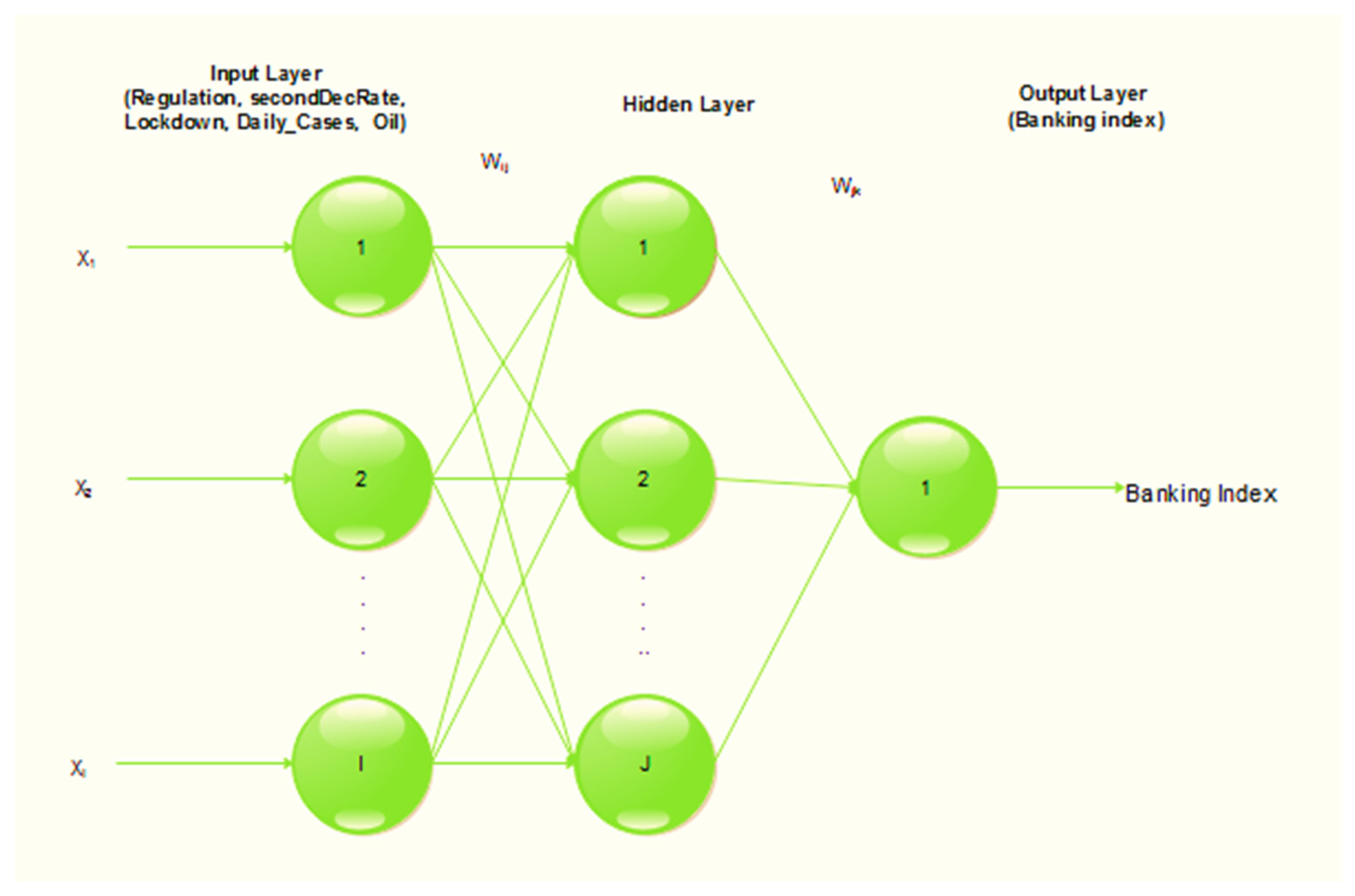

Our study makes the following contributions to the previous literature. First, our study focuses on examining the effect of different COVID-19 indicators, COVID-19 policy response, and oil prices on the Saudi banking index. Second, the COVID-19 indicators include the number of confirmed and number of death cases in Saudi Arabia. COVID-19 policy response includes lockdowns, decreasing the rates of repo and reverse repo, and new government regulations in the Saudi market through the pandemic. Third, we use regression analysis and an artificial neural network (ANN) model to build a prediction model for the Saudi banking index and to determine the most important factors for predicting the banking index. Fourth, we highlight the most important relative literature that studied the effect of the pandemic on different equity markets.

In this study, we implemented our methodology by running stepwise regression and ANN models. According to the regression findings, oil prices and new confirmed cases have had a significant positive effect on the Saudi banking index. However, the lockdown announcement and the first decrease in interest rate have had a significant negative effect on the Saudi banking index. To enhance the performance of the linear regression model, the ANN model was built. The findings showed that the rank of the variables according to their importance is oil price, number of confirmed cases, the lockdown, decrease in interest rate, and regulations.

This study has seven sections.

Section 2 presents the literature review.

Section 3 describes the data.

Section 4 explains the methodology.

Section 5 discusses the conclusions, and

Section 6 provides the practical implications. Lastly,

Section 7 discusses the limitations and possible avenues for further study.

5. Conclusions

Our study aimed at studying the effect of COVID-19 indicators and policy response on the Saudi banks index for the period from 1 January 2020 until 3 December 2020. COVID-19 indicators were measured by the number of COVID-19 confirmed cases and the number of COVID-19 death cases. COVID-19 policy response was measured by the lockdown announcement, SAMA regulations, decrease in the interest rate of repo and reverse repo, and oil prices. The analysis was conducted by calculating the correlation matrix between variables, running stepwise regression analysis, then building an ANN model. Our results showed that the regression model of the Saudi banking index is significant with an adjusted R2 of 86.9% and standard error of around 250.7.

According to the regression analysis findings, oil prices and new confirmed cases had a significant positive effect on the Saudi banking index. Nevertheless, the lockdown announcement in Saudi Arabia and first decrease in the interest rate for repo and reverse repo had a significant negative effect on the Saudi banking index.

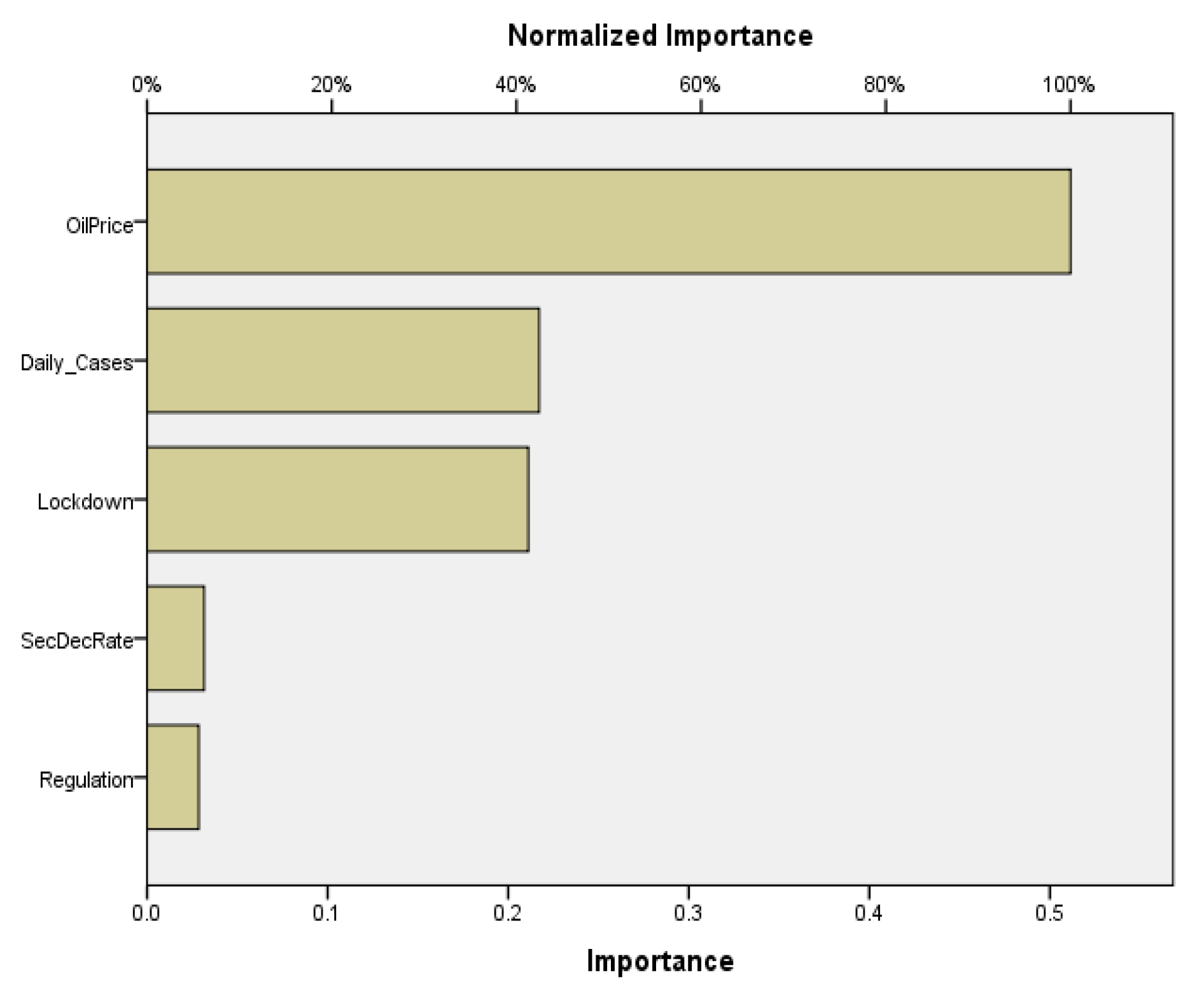

To enhance the performance of the linear regression model, an ANN model was built with R2 and RMSE of 96% and 194, respectively. The findings of ANN normalized importance showed that oil price is the most important variable that affects the Saudi banking index. This result is in line with Saudi Arabia’s economy being one of the greatest oil-based economies, with around one-quarter of world oil reserves.

The number of confirmed cases and lockdown announcement rank second and third, respectively, in importance on the Saudi banking index. These two indicators are the major direct consequences of COVID-19 that affect not only the Saudi banking index but economies worldwide. The second decrease in interest rate and regulations rank fourth and fifth. They are the corrective actions (i.e., monetary and fiscal policy tools) that were adopted by SAMA to minimize the impact of COVID-19 consequences on the Saudi economy and banking sector. Our results are consistent with related literature reviews of COVID-19 and its outcomes.

6. Practical and Theoretical Implications

Our research is theoretically and practically important. Our findings are important for stockholders and managers to understand the nature of stock markets, because these markets respond directly and randomly to any shocks in the economy, such as the COVID-19 pandemic. Investors should consider equity choices that are less risky than stock as an alternative investment and derivatives.

According to our result, the Saudi banking index depends heavily on oil price; hence, the Saudi government should take serious actions to minimize such dependence. Policymakers can benefit from our findings by building an early warning system and applying special strategies to predict possible future crises. Moreover, policymakers should enhance procedures that can increase investors’ confidence in the financial markets through minimizing media bias, given the increasing market volatility, investors’ random selection, or herding because of news (

Baek et al. 2020). Policymakers must assure that only correct and honest information is published and traded.

Banks rely heavily on the government’s support to regain customers’ trust and to rebuild the resilience of the banking sector. Accordingly, government support for sectors and individuals should be maintained and enhanced until they return to the pre-pandemic level. In addition, fintech in Saudi Arabia played a vital role in all sectors and proved its ability in facing different economic challenges. Therefore, fintech and R&D should always be in continuous improvement.

Finally, as one of the worst pandemics in this century, COVID-19 took a toll on the global economy and caused severe consequences in all aspects. Most importantly, the pandemic will never be diminished without increasing people’s awareness of this virus, implementing precautionary procedures, and having sufficient vaccine doses.

{kind=link}

{kind=link}

{kind=link}

{kind=link}