Abstract

We estimate foreign direct investment elasticities of output, of unskilled and skilled labor, and of unskilled and skilled wages for Chile, both at an aggregate level and for eight economic sectors. We use regional data from official Chilean sources ranging from 2012 to 2019 and data from economic sectors in each region for the period 1996–2011. Estimates are based on a simultaneous equation approach, which considers the two-way relationships between FDI and output as well as the relationships between output, labor, and wages stressed by the duality theory of production in economics. The estimations confirm that FDI triggers growth and that FDI follows growth. Due to the positive effects on output, FDI boosts employment creation, particularly of skilled labor. The estimated effects on wages are not significant, either statistically or practically. The output and labor effects of FDI are positive and significant in all economic sectors, but point estimates suggest that they could be larger for the agriculture-forestry-fishing sector. The results indicate that realistic increases in FDI can have substantial output and employment effects in Chile.

1. Introduction

Foreign direct investment (FDI) can trigger a range of economic effects in receiving countries and regions. The literature shows that, compared to domestic firms, FDI firms are, on average, more productive (Driffield and Taylor 2000; Negash et al. 2020), more technology-intensive (Driffield 1999), and more prone to innovation (Fernandes and Paunov 2012). In addition, inward FDI can boost domestic firms’ productivity through a range of economic spillover effects (Haskel et al. 2007; AlAzzawi 2012). Through input-output linkages, FDI can also create sizable multiplier effects in local and regional economies (Wang 2010; Ascani and Iammarino 2018). Furthermore, when FDI promotes cleaner production technologies, it may also contribute to a greener economy, as found, for instance, in the case of China (Ayamba et al. 2019) and Latin America (Dhrifi et al. 2020).

By stimulating domestic productivity and growth, FDI can also have several effects on the labor markets of host economies. The evidence shows that FDI firms are particularly intensive in the use of skilled labor, which has an effect on the demand for skills that spill over to other firms in local labor markets (Brazys and Kotsadam 2020). The increases in the demand for skilled labor prompted by FDI firms may push skilled wages up (Driffield et al. 2009). In addition, FDI firms usually offer better work conditions and are more gender-equal than domestic firms (Kodama et al. 2018). Employment created by FDI firms may also help dwindle the shadow economy and thus contribute to improving institutional quality (Huynh et al. 2020). In light of this evidence, countries worldwide have implemented sizable programs of FDI attraction, particularly as part of regional development policies targeted to chronically laggard regions (Armstrong and Taylor 2000) or to regions struck by economic globalization (Driffield and Taylor 2000). Nevertheless, FDI can also bring unintended consequences in labor markets, such as the displacement of domestic employment (Driffield 1999) or the substitution of unskilled labor; this latter lowering unskilled wages and increasing wage inequality (Gopinath and Chen 2003; Driffield and Taylor 2000). Displacement effects coupled with factor substitution and a crowding out of domestic firms may lead to negative effects of FDI on aggregated employment, and even on skilled employment, as shown by recent research in a developing country (Nguyen et al. 2020).

The objective of this paper is to provide evidence on the role of FDI as a driver of economic development in a less-developed country, Chile. To do so, we estimate the effects of FDI on output, employment, and wages at an average level and for the different economic sectors. The example of Chile is relevant due to institutional changes related to the derogation in 2016 of the main public instrument of FDI attraction since the mid-1970s, the Decree Law 600. The results of this research are also relevant in a post-pandemic scenario, where countries need to promote foreign direct investments to resume economic growth and tackle increased poverty. Methodologically, most aggregate-level analyses of the economic effects of inward FDI are based either on time series analysis (Chowdhury and Mavrotas 2006; Hansen and Rand 2006) or on cross-section or panel reduced-form estimates (Cipollina et al. 2012; Driffield et al. 2009). In the present article, we estimate FDI elasticities of output, labor, and wages following a simultaneous equations approach, which models explicitly the two-way relationship between FDI and output (Ayamba et al. 2019; Hansen and Rand 2006; Berthélemy and Démurger 2000) and the linkages between output, employment, and wages stressed by the duality theory of production in economics (Shephard 1953; Anríquez and López 2007). Average elasticities are calculated, as well as elasticities for eight economic sectors. Average elasticities are estimated using official data for Chilean regions for the period 2012–2019, and sectorial elasticities are obtained using data from the different sectors in each region for the period 1996–2011. We show, first, that both FDI and output influence each other positively in Chile. Second, we show that, through its effects on output, FDI increases the demand for labor, particularly in the case of skilled labor. Third, we find that despite the outward shift in the demand for labor, the effects of FDI on wages are not significant, either statistically or practically. Fourth, we find that the effects of FDI on output and labor are significant in all sectors, albeit possibly larger in the agriculture-forestry-fishing (AFF) sector.

Chile is an interesting case for analyzing the output and labor market effects of FDI. First, because previous research reports that while growth causes FDI in Chile, FDI does not cause growth (Chowdhury and Mavrotas 2006). This could be related to the low levels of domestic productivity, technology, and human capital, which may dampen the spillover and linkage effects of FDI (Borensztein et al. 1998; AlAzzawi 2012; Negash et al. 2020). Our results, on the contrary, show clear positive effects of FDI on aggregate and sectoral output. Second, because most research on the labor market effects of FDI has been conducted in developed countries (Driffield and Taylor 2000; Driffield et al. 2009; Becker et al. 2020). In these countries, the intensity of the use of capital, knowledge, and skilled labor is much higher than in less-developed economies, particularly in those still highly reliant on natural resources, such as Chile. In less-developed countries, one might expect that productivity differentials among FDI and domestic firms are even larger than those reported in the developed world, and, therefore, the economic effects of FDI (at least in terms of output and skilled jobs creation) could be higher (e.g., Gopinath and Chen 2003). Our results largely support this claim. Third, because the Chilean labor force is skewed towards low-skilled labor in non-tradable, unsophisticated activities (Gollin et al. 2016). In such conditions, the potential negative effects of FDI on unskilled labor and wages found elsewhere (Gopinath and Chen 2003; Driffield and Taylor 2000) could be particularly important. We do not find such negative effects. Fourth, because factors such as market structure, average productivity, and export orientation show marked differences across economic sectors. These heterogeneous sector conditions may create differences in the effects of FDI on output and employment (Nguyen et al. 2020; Asongu et al. 2018). Unlike previous studies in developing countries, our estimates indicate positive effects across all industries and of similar magnitude, except for the agriculture-forestry-fishing sector, for which point estimates are larger (although imprecisely estimated).

The rest of this paper is organized as follows: Section 2 presents the methodology and the data used to estimate the FDI elasticities of output, labor, and wages in Chile. Section 3 presents and discusses the estimation results. In Section 4, we use estimated elasticities to simulate changes in these economic outcomes in a region of Chile. Section 5 concludes and outlines some lessons for FDI attraction programs in Chile and worldwide.

2. Conceptual Framework

There is a wealth of research on the drivers and effects of foreign direct investment (FDI) in the economics literature. The theoretical foundations for the decision of firms to invest abroad are provided by Markusen (1984); Markusen and Venables (2000); and Helpman (1984). Grossly speaking, the literature on the development impacts of FDI can be divided into macro and micro studies (Alfaro 2017). Macro studies use data at the level of countries, industries, or sub-national units and are relevant to understanding the local factors that attract FDI and analyzing its impacts on economic growth and related development outcomes. Micro studies, instead, are usually based on firm-level data and are particularly suited to shed light on the mechanisms underlying the aggregated effects reported in macro studies, such as externalities and inter-firm spillovers, complementarities, and productive linkages. Our approach follows the tradition of macro studies, using Chilean aggregate data.

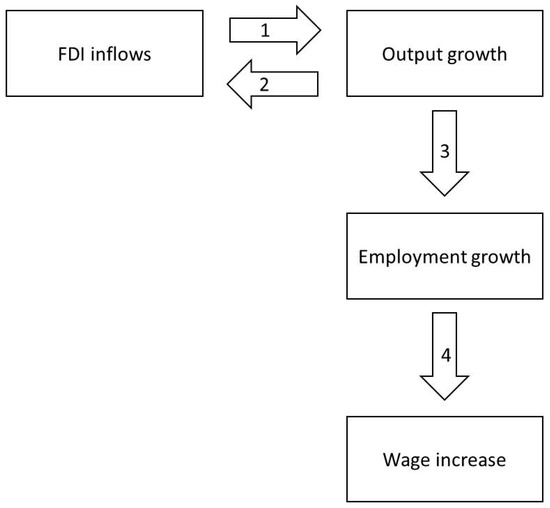

Figure 1 summarizes schematically the links between FDI, output, labor, and wages motivating our empirical strategy. The hypothetical role of FDI in boosting output is depicted as link 1 in Figure 1. Both the theory and most of the evidence confirm that inward FDI can raise the productivity of host economies. FDI firms embark on offshore activities once they have achieved key competitive capabilities (Falahat et al. 2020; Jiang et al. 2020), and outward FDI activities, in turn, increase their productivity (Kong et al. 2020). Thus, FDI firms are a select group of firms usually characterized by greater productivity, better management, and above-average innovative behavior (Zhang et al. 2015; Fernandes and Paunov 2012). Because of that, FDI firms stand out in the host economy for being more productive than domestic firms (Driffield and Taylor 2000; Negash et al. 2020). Furthermore, the greater levels of knowledge and innovation embedded in FDI operations might spill over to domestic firms, raising their performance and boosting the average productivity of the receiving industries and of other related industries (Haskel et al. 2007; Malikov and Zhao 2021). Similarly, through input-output linkages and multiplier effects, FDI firms can also kick-start localized processes of growth (Wang 2010; Jordaan 2016). Once settled, FDI firms may play the role of “anchor-tenants” (Sachs 2007; Wei and Leung 2005), creating demand externalities from which both domestic and other FDI firms may benefit. Nevertheless, spillover effects of FDI may be constrained by a lack of absorptive capacities in the receiving countries and regions, due to, for instance, scarce skilled human capital, little R&D effort, underdeveloped information and communications infrastructure, or weak institutions and policies (Caragliu and Nijkamp 2012; Asongu and Odhiambo 2020). Similarly, productive and trade linkages might be limited in situations of little embeddedness of FDI firms in the regional economy, as is the case, for example, of mining regions in Chile (Atienza and Modrego 2019). The empirical evidence is generally supportive of the positive effects of inward FDI on growth. Cipollina et al. (2012), for example, find a positive relationship between FDI inflows and industry growth using a sample of 22 countries and 14 industries. Likewise, Hansen and Rand (2006) report a positive relationship between FDI and growth using a sample of 31 countries over a span of 31 years. Chowdhury and Mavrotas (2006), using time-series analysis, report a positive effect of FDI on output growth in Malaysia and Thailand. At the subnational level, the evidence confirms the positive effect of FDI on regional economic growth in countries such as México (Jordaan and Rodríguez-Oreggia 2012) and China (Ayamba et al. 2019; Ng and Tuan 2006). Still, recent literature reviews report mixed effects of FDI on growth and conclude that the impacts are endogenous, that is, they depend on enabling local conditions and capabilities, such as the availability of advanced human capital, well-developed financial markets, and institutions that favor competition. According to this literature, the greatest impacts of FDI are rather vertical before horizontal (Harrison and Rodríguez-Clare 2010; Antrás and Yeaple 2014; Melitz and Redding 2014; Alfaro 2015).

Figure 1.

Relationships between FDI, output, employment, and wages.

The international evidence also shows that there is a simultaneous causation between FDI and growth; just as FDI boosts growth, FDI follows growth. This two-way relationship has been reported in countries such as Thailand and Malaysia (Chowdhury and Mavrotas 2006), China (Ayamba et al. 2019; Berthélemy and Démurger 2000), and also in cross-country analyses (Hansen and Rand 2006; Asongu et al. 2018). This is explained by the fact that one of the most relevant factors foreign direct investors consider when making location decisions is the growth potential of the host country (Hornberger et al. 2011; Asongu et al. 2018) and regions (Jordaan 2016). Other drivers of the location decision of foreign direct investors are infrastructure, the availability of specialized resources, business support services, and skilled human capital, as well as the investment climate, including trade openness, political stability, and institutions providing certainty to investments (Kinda 2010; Bhardwaj et al. 2007; Van Wyk and Lal 2010; Asongu et al. 2018; Huynh et al. 2020; Haudi et al. 2020). All these conditions are highly correlated to the levels of economic development (Bayraktar 2013). This relationship running from output to FDI is represented by the link 2 in Figure 1.

To relate the output effects of FDI to labor market outcomes, we borrow from duality production theory in economics (e.g., Shephard 1953). Our approach is similar to that of previous studies analyzing the employment effects of agricultural expansion (Anríquez and López 2007) and providing early estimates of the employment effect of COVID-19 in Chile (Modrego et al. 2020). According to mainstream economic theory, achieving greater output requires an increase in the use of inputs, including labor. Such a relationship is represented by the link 3 in Figure 1. Nevertheless, the evidence shows that the effects of FDI may be different for skilled and for unskilled labor. FDI firms are more intensive in the use of skilled labor (Driffield and Taylor 2000), and through spillover effects and productive linkages, inward FDI may increase the demand for skilled labor even in domestic firms (Driffield et al. 2009). Nevertheless, through input-substitution effects, FDI may end up displacing domestic labor, and particularly unskilled labor. Driffield and Taylor (2000), for example, note that posts required by FDI firms might be filled with workers previously working in domestic firms. Consequently, skilled vacancies either in other FDI firms or in domestic firms might end up taken by workers who are external to the local economy. These interwoven labor-market effects may lead to a neutral, or even a negative, net effect of FDI on total labor (Nguyen et al. 2020; Driffield and Taylor 2000). Summarizing, the net effect of FDI on the demand for labor would depend, to a large extent, on the reallocation of unskilled labor, and this reallocation could be hindered by the low levels of qualification of the domestic labor force (Driffield and Taylor 2000), as is the case in Chile. Given these potentially different effects of FDI, we estimate skilled and unskilled labor demand elasticities, following the classification of skilled and unskilled labor proposed by Anríquez and López (2007) for Chile.1

The outward shift in the demand for labor should bid up wages in the host economy. This indirect wage effect of FDI is represented as link 4 in Figure 1. The positive effects of FDI on skilled wages triggered by an increase in skilled labor demand have sufficient empirical support (Gopinath and Chen 2003; Driffield et al. 2009). On the contrary, the substitution of unskilled labor may lead to a decrease in unskilled wages and to raising wage inequality (Driffield and Taylor 2000; Gopinath and Chen 2003; Driffield et al. 2009). Thus, we estimate the FDI elasticities of both skilled and unskilled wages.

Finally, all these relationships linking FDI, output, labor, and wages can operate differently in each economic sector due to differences in conditions such as the qualification of the labor force, the intensity of the use of knowledge and technology, the level of embeddedness in the host economy, or the export orientation (Asongu et al. 2018; Asongu and Odhiambo 2020; Nguyen et al. 2020). For example, it has been shown that information technologies modulate FDI effects on growth in sub-Saharan Africa (Asongu and Odhiambo 2020). Similarly, FDI attraction policies may favor sectors with greater multiplier and innovation effects (Asongu et al. 2018). Nguyen et al. (2020) show that, in Vietnam, the employment effects of FDI are positive and larger in non-tradable sectors such as services, in which FDI establishes strong linkages with local firms. On the contrary, sectors such as agriculture experience negative employment effects from increased FDI inflows due to competition with traditional activities and a low embeddedness of FDI firms in this sector in the local economy.

3. Method

3.1. Econometric Model

The estimation approach departs from an aggregate production function in which output (y) depends on the quantity of unskilled labor (), skilled labor (), capital (), and, in accordance with link 1 in Figure 1, inward FDI as a shifter of total factor productivity as follows:

Link 2 in Figure 1 is modeled using a second equation in which FDI is a function of output and the stock of factors of production in the economy (Jordaan 2016) as follows:

To estimate the employment effects of FDI, we include unskilled and skilled labor demand equations, which derive from cost minimization given the production technology summarized in Equation (1), i.e., we are assuming an economy that uses inputs efficiently. Formally, for input j as follows:

Equation (3) states that the demand for input j = u, s, k () is the result of choosing the optimal inputs mix in order to minimize total production costs (C) given factor prices (). This problem is conditioned on the production technology summarized in the production function (1).

The solution of (3) yields the conditional factor demands as a function of unskilled wages (), skilled wages (), the price of capital () and output (y), this latter, from (1), being a function of FDI as follows:

Skilled and unskilled labor demand equations capture link 3 in Figure 1 in the econometric model.

Equations (1), (2), and (4) are the core of our estimation strategy. Together, they motivate the following system of five simultaneous equations, which is the empirical counterpart of the relationships in Figure 1:

In system (5), ln indicates that the variables are measured in natural logarithms. are parameters to be estimated, measuring the partial linear association between variable p = y, IED, qu, qs, qk, with respect to variable m = y, FDI, qu, qs, qk. are coefficients indicating year (t) dummy variables, and are the disturbances.

3.2. FDI Elasticities of Output, Labor, and Wages

Being log-linear equations, the estimation of the first equation of system (5) delivers directly the FDI elasticity of output (, a summary metric of the proportional change in output given changes in the stock of FDI as follows:

Equations (4) and (1) pose that unskilled and skilled labor demands depend indirectly on FDI. Using the chain rule, the FDI elasticity of input j = (u, s, k) demand () is the product of the FDI elasticity of output () times the output elasticity of input j demand ():

In terms of the estimated model, the FDI elasticities of unskilled () and skilled () labor are as follows:

To estimate the FDI elasticity of wages, we follow Anríquez and López (2007). Assuming that capital markets are well-integrated and, therefore, the price of capital is relatively fixed across regions (plausible assumption for Chile according to the authors), FDI elasticities of unskilled () and skilled wages () can be expressed in terms of the estimated coefficients as follows:2

where is the wage elasticity of the supply of unskilled labor, and is the wage elasticity of the supply of skilled labor. Anríquez and López (2007), based on previous studies in the country suggest a value of 1.8 for both elasticities, a value which is also used in other studies in the country (Modrego et al. 2020). Note that the dependence of the wage elasticities in the left-hand side of (8) on output elasticities of labor ( formalizes link 4 in Figure 1.

Using model (5) and Equations (6), (7), and (8), we also calculate FDI elasticities at the level of eight economic sectors for which the different datasets available could be merged: (i) agriculture, forestry, and fishing; (ii) mining; (iii) manufacture; (iv) electricity, gas, and water; (v) construction; (vi) retail, hotels, and restaurants; (vii) transport and communications; (viii) other services. The sectoral model is an expanded version of the model (5), which includes different intercepts and interactions between each right-hand-side variable in each equation and sector dummy variables. The sectoral model is estimated using specific data for each sector and industry (see Section 3.3).

3.3. Data and Estimation Method

The sample used to estimate system (5) is 104 observations of the former 13 regions (r) of Chile for the period 2012–2019.3 The Appendix A describes the variables in the model and the data sources. Table 1 summarizes the descriptive statistics of the estimation sample.

Table 1.

Descriptive statistics of the estimation simple of system (5) (N = 13 regions × 8 years = 104).

System (5) is estimated using the three-stages-least-squares (3SLS) method (Zellner and Theil 1962). However, system (5) is under-identified. Therefore, we use Bartik-style or shift-share instruments as excluded instruments. These instruments, first introduced by Bartik (1991) and brought to the spotlight by Blanchard and Katz (1992), are weighted averages of a common set of shocks, with weights reflecting heterogeneous shock exposure for each observation (Borusyak et al. 2022). Bartik-style instruments and their formally identical variants have been used in many fields in economics, including labor economics, public economics, development economics, macroeconomics, international trade, and finance (Goldsmith-Pinkham et al. 2020). Bartik instruments have also been used vastly in regional economic research (see Broxterman and Larson 2020). In our case, given the multiple endogenous variables in system (5), we build 12 instruments as follows:

where, is the instrument associated at j (=1, …, 12) economic sub-sectors on region i and year t, is the share of sub-sector j in the regional GDP in a fixed year (2010) and t is a common trend, the shift variable. The validity of these instruments in regression analysis depends on the assumptions about the shocks, exposure shares, or both. Borusyak et al. (2022) develop a framework assuming shock exogeneity, while Goldsmith-Pinkham et al. (2020) assume share exogeneity. In this case, we assume a predetermined share and exogenous shifts for each instrument. Recent studies analyzing the properties of Bartik-style instruments support their relevance and exogeneity under conditions, which are not too restrictive in real applications, as is our case (Autor et al. 2013; Broxterman and Larson 2020; Acemoglu et al. 2016; Acemoglu and Restrepo 2020). Additionally, we include the other following three instruments (Z): the regional population density, the region’s average years of schooling of unskilled workers, and the region’s average years of schooling of skilled workers.4

The sample used to estimate the sectoral system are 728 observations of the eight economic sectors in the former 13 Chilean regions and for seven years (1996, 1998, 2000, 2003, 2006, 2009 y 2011). Although somewhat dated, this is the only period for which we could match regional FDI data with the other variables. Between 1974 and 2015, FDI in Chile benefited from Decree Law 600 (DL 600). The DL600 was a regulatory tool establishing a protected and non-discriminatory tax scheme for foreign direct investments entering the country through this modality. During the period of analysis, the DL 600 was the most important mechanism for inward FDI in the country (Chakiel and Orellana 2014). As part of the contract between the FDI investor and the Chilean State, the investor had to declare the region and the economic sector of the foreign investment. The former Comité de Inversiones Extranjeras (now InvestChile) compiled and published annual statistics of regional FDI by economic sector up to 2012. The figures of the regional stock of FDI between 2012 and 2019 taken from the Chilean Central Bank are not available by economic sector. Appendix B describes the variables in the sectoral model and the data sources. Appendix C summarizes the descriptive statistics of the sample used to estimate the sectoral model. The model was again estimated by 3SLS, and the set of excluded instruments include the same Bartik style or shift-share and the same other three instruments used in the aggregate model.

4. Results

4.1. 3SLS Estimates

Table 2 summarizes the 3SLS estimation results of the system (5). The results are broadly consistent with both the theory and the evidence. The five equations are globally significant. The models’ fit is adequate even for the IED equation, for which the R2 is considerably smaller (0.41). More importantly, the output equation (column 1) yields a positive coefficient for the IED variable, which is significant at the 1% level. This result confirms the positive effect of FDI on economic growth suggested by previous studies (Asongu and Odhiambo 2020; Ayamba et al. 2019; Cipollina et al. 2012; Hansen and Rand 2006; Berthélemy and Démurger 2000). It contrasts, however, with that by Chowdhury and Mavrotas (2006), who, using time-series analysis, find that FDI does not cause GDP growth in Chile. Moreover, the coefficient of the output variable is positive and significant at the 1% level in the FDI equation (column 2). The estimated coefficient is large, indicating a product elasticity of FDI of around 3. This large elasticity indicates that FDI is very sensitive to changes in output in Chile. Overall, the results confirm that just as FDI triggers growth, FDI follows growth (Asongu et al. 2018; Hansen and Rand 2006; Berthélemy and Démurger 2000).

Table 2.

3SLS estimation results of system (5).

Regarding the factor demand equations, the results in columns (3), (4), and (5) largely concur with standard economic reasoning. In the first place, the negative and significant coefficients for the own-price variables indicate that the three-factor demands are decreasing in the factor’s price. Moreover, the positive and significant coefficients estimated for the output variable show that the three-factor demands are increasing in output, or put differently, that unskilled labor, skilled labor, and capital are all normal inputs. The cross-price coefficients are negative in general (with a couple being not significant), suggesting input complementarity before substitution.

4.2. FDI Elasticities of Output, Labor, and Wages

The coefficients in Table 2 are used to estimate the FDI elasticities of output, labor, and wages, using Equations (6), (7), and (8), respectively. Table 3 reports estimated elasticities and the 95% confidence intervals, obtained using the delta method. The FDI elasticity of output () indicates that a 1% increase in FDI translates into an around 0.054% increase in output, an effect that lies between 0.045% and 0.062% with a 95% confidence. The estimated output elasticity is equal to the long-run elasticity estimated by Pegkas (2015) using a panel of eighteen Eurozone countries. It is larger, although in the order of magnitude, than those reported by Al Nasser (2010) for a sample of Latin American countries (between 0.02 and 0.04), and also slightly larger than those reported by Berthélemy and Démurger (2000) for China (0.037). The estimated output elasticity is also larger than that reported by Driffield et al. (2009) for the U.K. (around 0.013).

Table 3.

Estimated elasticities and 95% confidence intervals.

Regarding the FDI elasticities of unskilled () and skilled () labor demand, a 1% increase in FDI relates to an around 0.039% increase in the demand for unskilled labor (with a 95% confidence interval of 0.031% and 0.047%), and to an around 0.049% increase in the demand for skilled labor (at a 95% confidence level, between 0.041% and 0.058% ). The estimated elasticities confirm the results of previous studies showing a positive effect of FDI on the demand for skilled labor (Driffield and Taylor 2000). Although not fully comparable, our estimated elasticities are, nevertheless, larger than previous estimates by Driffield et al. (2009) for the UK (around 0.011), but much smaller than employment elasticities of FDI reported for export processing zones in Bangladesh (around 0.45, Majumder et al. 2022). Remarkably, the estimated FDI elasticity of unskilled labor is positive and statistically significant, which does not support, for the Chilean case, claims of a displacement of unskilled labor due to FDI inflows in other contexts (Driffield and Taylor 2000). In any case, the estimated effects of FDI are larger for the demand for skilled labor than for unskilled labor, as suggested in the literature (Driffield et al. 2009). Overall, our results differ markedly with respect to findings of negative effects of FDI on aggregate and skilled employment reported in other less-developed countries (Nguyen et al. 2020).

Finally, the estimated FDI elasticities of unskilled () and skilled () wages are small (0.002 and 0.021, respectively), and statistically significant only in the case of skilled labor. Estimated skilled-wage elasticities are much smaller than the reduced-form elasticities reported by Gopinath and Chen (2003) for a cross-section of both developed and developing countries (around 0.12). In the case of FDI elasticities of unskilled labor, our results differ from the negative and significant effect reported by the same study (−0.067). Overall, the results suggest that, in the case of Chile, the outward shift in labor demands triggered by inflows of FDI is not large enough to induce substantial increases in either skilled or unskilled wages, likely because the share of FDI in total labor demand is still rather small.

Although seemingly small, estimated output and labor elasticities of FDI in Chile point to substantial effects of FDI increases, even in realistic scenarios of FDI growth. For example, a two-year increase in the stock of FDI—which corresponds to an around 11% increase at the national average growth rate for the period 2012–2020—translates into an around USD 838.5 MM increase in output and around 4,364 unskilled and 37,854 skilled jobs. On the contrary, the same increase in FDI is associated with an increase in skilled wages of only around USD 1.7 a month.5

4.3. Estimates by Sector

The estimation results of the system (5) for the eight economic sectors are presented in Table 4.6 Despite the fact that the periods are different and that the FDI figures are not fully comparable, the results confirm most of the findings of the aggregate model in Table 2. First, the coefficient of the linear FDI effect is positive and highly significant in the output equation. In general, the coefficients of the FID#sector interaction variables (not shown due to space limitations) are not significant individually at the 5% level and are not jointly significant either. This means that we fail to reject differences in the effects of FDI on output across sectors, or, put differently, that FDI is equally pro-growth in all sectors. Second, the coefficient of the linear GDP effect remains positive in the FDI equation and is now even larger (around 4.3). Nevertheless, now it is only marginally significant (at the 10% level). Again, the coefficients of the output#sector interaction variables (not shown) are not significant, indicating that we cannot discard that FDI is equally responsive to growth in all sectors. Regarding the FDI equation, it is worth noting that most reported coefficients are not significant, thus leaving most of the explanatory power to sector and year dummy variables and their interactions (not shown). This means that FDI in Chile concentrates on specific sectors (such as mining) and seems to be highly sensitive to industries’ cycles. One clear example is the “copper super cycle”, which took place more or less during the estimation period. The copper super cycle was initially characterized by a sharp increase in international copper prices, leading to sizable inflows of foreign investments in the Chilean mining sector (Atienza and Modrego 2019). A third important result is that the output variable remains positively related to the demand for both unskilled (column qu) and skilled labor (column qs), with estimated coefficients that remain highly significant. The output#sector interaction variables (not shown) indicate that the effects of output expansion are particularly strong in the agriculture-forestry-fishing (AFF) sector. On the contrary, this effect is the lowest in the mining sector, where the estimated interaction coefficient is the most negative (and statistically significant). This latter result is not surprising given the relatively high capital intensity of this industry in Chile, at least compared to other sectors (Anderson and Ponnusamy 2019). Finally, except for skilled labor, factor demands relate in general negatively to the factor’s price, as the theory indicates. The cross-price elasticities are somewhat variable across sectors, suggesting sector-specific substitution/complementarity relationships among production factors. The prevalent pattern is, however, negative cross-price elasticities, confirming factors’ complementarity found with the aggregate model.

Table 4.

3SLS estimation results of sectoral system (9).

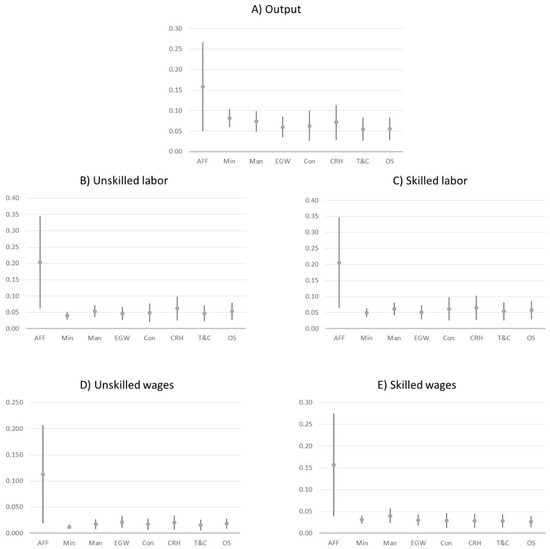

Figure 2 summarizes the estimated elasticities by economic sector and their 95% confidence intervals. Panel (a) presents the FDI elasticities of output. Overall, FDI has a positive effect on output in all sectors. Comparing the sectoral estimates with the elasticity obtained from the average model (0.054, Table 3), the estimated elasticities are slightly larger in all sectors except the AFF sector, for which they are considerably larger. However, the 95% confidence intervals contain the elasticity of the aggregate model for all sectors but mining. A 10% increase in sectoral FDI translates into around a 1.6% increase in AFF output, with elasticity that decreases to around 0.55% for the transport and communications sector. Still, differences in estimated elasticities are, in general, not statistically significant across sectors.

Figure 2.

FDI elasticities of output, labor, and wages by economic sector. Note: AFF = agriculture–forestry–fishing; Min = mining; Man = manufactures; EGW = electricity–gas–water; Con = construction; CRH = commerce–restaurants–hotels; T&C = transport and communications: OS = other services.

The panel (b) and (c) of Figure 2 show the estimated FDI elasticities of unskilled and skilled labor, respectively. The employment effects of FDI are positive and significant in all sectors, and again slightly larger but in the order of magnitude of those obtained with the aggregate model (0.039 and 0.049, Table 3). The exception is the AFF sector, where estimated elasticities are, again, considerably larger. Specifically, a 10% increase in FDI translates into increases in sectoral unskilled employment ranging from around 2 percent in the AFF sector to 0.4 percent in mining (Figure 2b). Similar is the case for skilled labor (Figure 2c). Estimated FDI elasticities range from 0.21 in the AFF sector to 0.05 in mining. Interesting contrasts can be found when comparing the FDI elasticities of output and labor across sectors. For example, the AFF sector stands out for the relatively high sensitivity of both outcomes to FDI inflows. This result is in accordance with the development impacts of agricultural expansion reported by Anríquez and López (2007). On the contrary, the results for Chile contrast with the findings by Nguyen et al. (2020) for Vietnam. Nguyen et al. (2020) report large positive effects of FDI on employment in the services sector, mild positive effects in the industry sector, and negative effects in the agriculture sector. Nevertheless, the large standard errors place a note of caution when drawing conclusions about larger labor effects of FDI in this sector from our estimates. Mining, on the contrary, stands out for the relatively high sensitivity of output to changes in FDI but at the same time for the relatively low sensitivity of both skilled and unskilled labor demand to FDI increases. This is another signal of the high capital intensity of this sector, limiting the pro-employment effects of mining growth. Another example is given by manufacturing and commerce. While the former has a larger output FDI elasticity, the latter has a larger labor elasticity, suggesting that inward FDI in commerce, hotels, and restaurants (which include tourism) is relatively more efficient in creating both skilled and unskilled jobs. Although interesting on their own, we note, once again, that these sectoral differences are only suggestive, because point estimates are not statistically different across most sectors.

Finally, sectoral estimates of FDI elasticities of unskilled and skilled labor are presented in Figure 2 panels (d) and (e), respectively. Regarding skilled wages, FDI has a positive and statistically significant effect in all sectors. The estimated elasticities are in the same order of magnitude as those estimated with the aggregate model (0.021, Table 3). The exception is, once more, the AFF sector, which has an elasticity that is much larger but that is estimated imprecisely. In this sector, a 10% increase in the sector’s FDI yields an estimated increase of around 1.6% in skilled wages (Figure 2d). This elasticity is closer to the FDI elasticities of wages reported by Gopinath and Chen (2003) and also concurs with the development impacts of agricultural expansion reported in Chile (Anríquez and López 2007). Apart from the AFF sector, the largest effect of FDI increases is estimated in the manufacturing sector (0.4% increase in skilled wages per each 10% increase in FDI). The smallest FDI elasticity of skilled wages is estimated for the “other services” sector, a broad sector encompassing a wide range of personal and community services. In this sector, a 10% increase in FDI translates into around a 0.3% increase in skilled wages. Nevertheless, sectoral differences in estimated FDI elasticities of skilled wages are, again, not statistically significant.

Contrary to the results of the aggregate model (Table 3), the estimated FDI elasticities of unskilled wages are now larger and statistically significant in all sectors (Figure 2e). Still, the FDI elasticities of unskilled wages remain considerably smaller than the FDI elasticities of skilled wages. The AFF sector is, once more, the one with the largest estimated elasticity (1.1% increase per each 10% increase in FDI), although the large confidence interval has a lower limit that is close to the estimated elasticity for the other sectors. Apart from the AFF sector, the electricity-gas-water and the commerce-hotels-restaurants sectors have the largest FDI elasticities of skilled wages. Notably, the smallest FDI elasticity of unskilled wages is estimated for the mining sector, the sector that expands the least the demand for this type of labor given a proportional increase in FDI (Figure 2, panel b).

To conclude, it is worth noting that, in spite of being statistically significant, estimated FDI elasticities of both unskilled and skilled wages are of little practical significance. For example, for the AFF sector—a sector having wage elasticities around 5–6 times those estimated for the following sector—a 27% increase in FDI (or around 5 years at the average growth rate of 2012–2020) translates into an increase of around USD 10 a month in average unskilled wages and of around USD 23 a month in average skilled wages.7

5. Conclusions

This research estimates the FDI elasticities of output, labor, and wages in Chile. The elasticities are obtained using a simultaneous equations model, which acknowledges the two-way relationship between FDI and output, and the relationships between output, labor, and wages remarked by the duality theory of production in economics. In doing so, this research has helped clarify the mechanisms linking aggregate inward FDI, output, and labor market outcomes. In addition, this research has shown that the mechanisms stressed by production theory in economics are in place in the aggregate of a less-developed economy as well as in each of its economic sectors. Thus, the findings in this paper advances our understanding of the linkages underlying reduced-form estimations showing employment effects of FDI in the macro studies literature.

The main results of this research can be summarized as follows:

- There is a positive and significant effect of FDI on output that is similar to or slightly larger than previous estimates in other countries;

- FDI responds to output increases, and the estimated output elasticity of FDI is large (around 3);

- Through output expansion, FDI increases the demand for labor, an effect that is larger in the case of skilled labor, as the literature on the labor market effects of FDI reports in advanced countries. We do not find the displacement of unskilled labor found in other contexts;

- Our estimates show no statistically significant effects of FDI on average unskilled wages, and the effects of FDI expansion on skilled wages are statistically significant, but not significant in a practical sense;

- The effects of FDI on output and labor are significant for all economic sectors. Although we fail to reject sectoral differences statistically, point estimates suggest effects of FDI that might be particularly relevant for the agriculture-forestry-fishing sector, presumably where productivity differences between FDI and domestic firms are the greatest;

- There are some notable qualitative differences in the economic effects of FDI expansion across sectors, which, to a large extent, are likely driven by sectoral differences in the relative intensity of the use of factors. For example, mining output is relatively sensitive to changes in FDI, whereas mining employment is less sensitive compared to other sectors. On the contrary, the commerce-hotels-restaurants sector has an around-average output elasticity, but a relatively high elasticity of labor with respect to changes in FDI. A caveat here is that these qualitative differences are not statistically significant in our estimates;

- FDI expansion has substantial output and labor effects for realistic scenarios of FDI expansion (say, 2 years of FDI growth given current growth rates).

The analysis in this paper has several limitations worth discussing.8 In the first place, functional forms used to estimate foreign direct investment elasticities of output, labor, and wages impose a constant (and unitary) elasticity of substitution among productive factors. In addition, estimated elasticities are linear functions of the estimated parameters. Both render our estimates reliant on an oversimplified and highly restrictive representation of the aggregate production technology. Future research should consider flexible functional forms, such as the translog (Christensen et al. 1971) or the generalized Leontieff (Diewert 1971) production functions. Such flexible specifications will permit varying elasticities of substitution and, thus, FDI elasticities that are non-linear and dependent on the levels of inputs in the different regions and sectors within each region. This approach would also allow testing output and labor effects of FDI that are non-linear in inward FDI, as one would expect. Second, the period considered here is not long enough to fully capture the effects of the key institutional change related to the abolition of the DL 600 in 2016. As said, the DL 600 was the most important policy targeted at the promotion of FDI in Chile since the mid-1970s, and its termination may have substantially changed both the quantity and the type of FDI inflows. Future research should expand the estimation period beyond 2019 in order to isolate the effects of this policy change and conduct statistical tests of the structural stability of the relationships estimated here. Finally, although our estimates of the output, employment, and wage effects of FDI have been compared to other estimates in the literature, cross-country studies using a standardized dataset and a common methodology would allow a comparison of different national economies in terms of the relations between FDI, output, and labor market outcomes. This is another relevant avenue for future research.

Bearing these limitations in mind, our results confirm that FDI can be a driver of growth and employment creation in Chile. In our view, this opportunity has not yet been fully realized in the country. In the last decades, FDI in Chile has benefitted from factors such as comparative advantages in natural resources industries, the country’s macroeconomic and institutional stability, and also specific incentives that have been in place since the mid-1970s (being the Decree Law 600 the most conspicuous example). Facing the challenges of post-pandemic recovery, social inequality, and environmental crises, today Chile needs to activate new levers for the attraction of an FDI that contributes to traditional development outcomes as those addressed in this research, but also to broader development outcomes such as gender equity (Kodama et al. 2018), environmental sustainability (Ayamba et al. 2019; Dhrifi et al. 2020) or institutional quality (Huynh et al. 2020). To achieve this goal, Chile should articulate a coherent set of economic policies reinvigorating growth and allowing the strengthening of innovation and productive ecosystems, in order to enhance its technology absorption capacity and raise its economic complexity and sophistication.

Finally, for those in charge of FDI attraction policies in Chile, it is relevant to monitor and evaluate the performance of the new institutional framework of FDI promotion. Monitoring and evaluation is crucial to adjust current instruments and agencies if needed, or to design new instruments to ensure that FDI keeps generating the impacts estimated here without what has been the main FDI attraction instrument in the country. In addition, Chile should advance toward more decentralized institutions and policies for the promotion of FDI. As the international experience demonstrates, the decentralization of FDI promotion is necessary to attract and retain an FDI that increasingly looks less to classical comparative advantages and instead seeks a hospitable and thriving environment, particularly at the local level. Such a decentralized institutional arrangement should be embedded in a broader national framework of economic promotion and institutional strengthening. Key elements of such a decentralization scheme are the transfer of responsibilities and competencies to subnational governments, as well as capacity-building programs targeted to the actors of the different regional innovation ecosystems (low-level governments and decentralized state agencies, local entrepreneurs, regional universities, local productive associations, etc.). Regional governments, in turn, should take a leading role in directing the efforts to attract more, but fundamentally more strategic, foreign direct investments.

Author Contributions

Conceptualization, F.M., J.O., L.P. and Á.A.; methodology, F.M. and J.O.; software, F.M. and J.O.; validation, F.M., J.O. and L.P.; formal analysis, F.M. and J.O.; investigation, F.M., J.O., L.P. and Á.A.; resources, F.M., J.O., L.P. and Á.A.; data curation, F.M. and J.O.; writing—original draft preparation, F.M., J.O., L.P. and Á.A.; writing—review and editing, F.M., J.O., L.P. and Á.A.; visualization, F.M., J.O. and L.P.; supervision, F.M., L.P. and Á.A.; project administration, Á.A., L.P. and F.M.; funding acquisition, Á.A., L.P. and F.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Regional Government and the Regional Council of the Region of O’Higgins, Chile, through project “Academia IED para promover y escalar la Innovación” [Grant: Innovation for Regional Competitiveness Fund (FIC) 40027307-0].

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in this research are available upon request from the authors.

Acknowledgments

The authors are grateful to two anonymous reviewers for their insightful comments and suggestions. Any errors are solely the authors responsibility.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Variables Used to Estimate System (5).

Table A1.

Variables Used to Estimate System (5).

| Variable | Description | Source |

|---|---|---|

| y | Real regional GDP (Chained volume, CLP thousands of millions of 2013). | Chilean Central Bank. https://si3.bcentral.cl/siete, accessed on 15 June 2021. Available for 2012–2019. |

| FDI | Stock of foreign direct investment in the region (Chained CLP millions of 2013). | Chilean Central Bank. Available for 2012–2019. |

| qu | Total employed people with less than eight years of schooling in the region. | Chilean National Institute of Statistics (INE), New National Employment Survey (NENE). Available for 2012–2019. |

| qs | Total of employed people with eight years of schooling or more in the region. | INE, New National Employment Survey (NENE). Available for 2012–2019. |

| qk | Fixed capital consumption in the region (CLP thousands of millions). | Chilean Central Bank. National fixed capital consumption allocated regionally using the regional share in national stock of capital estimated by Cerda (2018). Available for 2012–2019. |

| pu | Regional mean annual income of unskilled workers in their main occupation (constant CLP of 2020) | INE, New Supplementary Incomes Survey (NESI). Available for 2012–2019. |

| ps | Regional mean annual income of skilled workers in their main occupation (constant CLP of 2020) | INE, New Supplementary Incomes Survey (NESI). Available for 2012–2019. |

| pk | Price index of capital goods imports (100 = 2013) | Chilean Central Bank, national data. Available for 2012–2019. |

| Year dummies | ||

| Excluded instruments | ||

| Z1 | Regional population density (population/km2) | National System of Municipal Indicators of the Undersecretariat of Regional Development (SINIM). Available for 2012–2019. |

| Z2 | Region’s average years of schooling of unskilled workers | INE, New National Employment Survey (NENE). Available for 2012–2019. |

| Z3 | Region’s average years of schooling of skilled workers | INE, New National Employment Survey (NENE). Available for 2012–2019. |

| s_j | Share of sector j in regional GDP | Central Bank of Chile. Available for 2012–2019. |

Appendix B

Table A2.

Variables Used to Estimate the Sectoral System.

Table A2.

Variables Used to Estimate the Sectoral System.

| Variable | Description | Source |

|---|---|---|

| y | Real regional GDP by economic sector (Chained volume, CLP thousands of millions of 2013). | Chilean Central Bank. Available for 1996–2011. |

| FDI | Materialized foreign direct investment in the Region by economic sector entered through the Decree Law 600 (thousands CLP of 2020) | InvestChile, available for 1974–2012. |

| qu | Total employed people with less than eight years of schooling in the region by economic sector. | Ministry of Social Development and Family, CASEN survey. Available for 1996, 1998, 2000, 2003, 2006, 2009, and 2011. |

| qs | Total employed people with eight years of schooling or more in the region by economic sector. | Ministry of Social Development and Family, CASEN survey. Available for 1996, 1998, 2000, 2003, 2006, 2009, and 2011. |

| qk | Fixed capital consumption in the region by sector (CLP thousands of millions of 2013). | Chilean Central Bank. Available for 1996–2011. National data for each sector, allocated regionally using the regional share in national stock of capital estimated by Cerda (2018). |

| pu | Regional mean annual income of unskilled workers in their main occupation, by economic sector (constant CLP of 2020) | Ministry of Social Development and Family, CASEN survey. Available for 1996, 1998, 2000, 2003, 2006, 2009, and 2011. |

| ps | Regional mean annual income of skilled workers in their main occupation, by economic sector (constant CLP of 2020) | Ministry of Social Development and Family, CASEN survey. Available for 1996, 1998, 2000, 2003, 2006, 2009, and 2011. |

| pk | Price index of capital goods imports (100 = 2013) | Chilean Central Bank. National data. Available for 1996–2011. |

| Year dummies | ||

| Z1 | Regional population density (inh/km2) | National System of Municipal Indicators of the Undersecretariat of Regional Development (SINIM). Available for 2012–2019. |

| Z2 | Region’s average years of schooling of unskilled workers by economic sector | INE, New National Employment Survey (NENE). Available for 2012–2019. |

| Z3 | Region’s average years of schooling of skilled workers by economic sector | INE, New National Employment Survey (NENE). Available for 2012–2019. |

| s_i | Share of sub-sector j in regional GDP | Central Bank of Chile. Available for 2012–2019. |

Appendix C

Table A3.

Descriptive Statistics of the Estimation Simple of the Sectoral Model (N = 13 Regions × 8 Sectors × 7 Years = 728).

Table A3.

Descriptive Statistics of the Estimation Simple of the Sectoral Model (N = 13 Regions × 8 Sectors × 7 Years = 728).

| Variable | Description | N | Mean | Std. Deviation | Minimum | Maximum |

|---|---|---|---|---|---|---|

| y | Real regional GDP by economic sector (Chained volume, CLP thousands of millions of 2013). | 728 | 863.6 | 2214.2 | 0 | 26,787.9 |

| IED | Materialized foreign direct investment in the Region by economic sector entered through the Decree Law 600 (thousands CLP of 2020) | 728 | 23,857.8 | 123,137.6 | 0 | 1,622,906.0 |

| qu | Total employed people with less than eight years of schooling in the region by economic sector. | 728 | 16,055 | 27,725 | 0 | 200,155 |

| qs | Total employed people with eight years or more of schooling in the region by economic sector. | 728 | 41,282 | 104,931 | 11 | 1,068,536 |

| qk | Fixed capital consumption in the region by sector (CLP thousands of millions of 2013). | 728 | 157.7 | 422.5 | 1.3 | 5389.9 |

| pu/1 | Regional mean annual income of unskilled workers in their main occupation, by economic sector (constant CLP of 2020) | 722 | 3,854,955 | 1,449,861 | 369,702 | 14,656,358 |

| ps | Regional mean annual income of skilled workers in their main occupation, by economic sector (constant CLP of 2020) | 728 | 7,015,531 | 3,252,790 | 1,285,626 | 42,421,504 |

| pk | Price index of capital goods imports (100 = 2013) | 728 | 104.2 | 14.8 | 87.9 | 134.7 |

| Z1 | Densidad poblacional de la región (hab/Km2) | 728 | 47.7 | 85.8 | 0.8 | 451.1 |

| Z2/1 | Region’s average years of schooling of unskilled workers by economic sector | 723 | 5.9 | 0.7 | 0.8 | 8.0 |

| Z3 | Region’s average years of schooling of skilled workers by economic sector | 728 | 12.5 | 0.8 | 10.3 | 15.8 |

| s_1 | Share of agriculture in regional GDP | 728 | 0.059 | 0.049 | 0.000 | 0.169 |

| s_2 | Share of fishing and aquaculture in regional GDP | 728 | 0.015 | 0.021 | 0.000 | 0.112 |

| s_3 | Share of mining in regional GDP | 728 | 0.182 | 0.204 | 0.000 | 0.673 |

| s_4 | Share of manufacturing in regional GDP | 728 | 0.141 | 0.097 | 0.014 | 0.453 |

| s_5 | Share of electricity, gas, and water in regional GDP | 728 | 0.031 | 0.023 | 0.010 | 0.110 |

| s_6 | Share of construction in regional GDP | 728 | 0.075 | 0.025 | 0.025 | 0.157 |

| s_7 | Share of commerce, restaurants and hotels in regional GDP | 728 | 0.065 | 0.030 | 0.020 | 0.175 |

| s_8 | Share of transport and communications in regional GDP | 728 | 0.069 | 0.019 | 0.035 | 0.118 |

| s_9 | Share of financial and business services in regional GDP | 728 | 0.100 | 0.042 | 0.062 | 0.251 |

| s_10 | Share of housing services in regional GDP | 728 | 0.076 | 0.029 | 0.017 | 0.123 |

| s_11 | Share of personal services in regional GDP | 728 | 0.116 | 0.042 | 0.033 | 0.215 |

| s_12 | Share of public administration in regional GDP | 728 | 0.071 | 0.041 | 0.013 | 0.204 |

Note: /1 Missing data due to absence of unskilled workers in some sectors of some regions in a given round of the ENE-ESI surveys.

Notes

| 1 | Anríquez and López (2007) define unskilled labor as workers with less than eight years of schooling. |

| 2 | The total derivative of the demand of labor j = (u,s), given the assumption of fixed prices of capital, is: . Equate this expression to the change in the supply of labor j given a change in wages: , and rearrange terms to arrive at Equation (7) in Anríquez and López (2007). Use this result along with Equation (7) above to arrive at expression (8) in this article. As explained in Anríquez and López (2007), this procedure reflects an automatic market-clearing adjustment to changes in the labor market. |

| 3 | Currently there are 16 regions due to the subdivision of the former I Region of Tarapacá, of the former X Region of Los Lagos (both in 2007), and of the former VIII Region of Biobío in 2018. |

| 4 | The results are largely robust to the exclusion of Bartik instruments, as well as to the exclusion of the other three instruments (results available upon request). |

| 5 | National values for 2020: real GDP = 141,174.4 USD MM, unskilled labor = 1.02 MM people, skilled labor = 7.02 MM people. Average unskilled wages = USD 363.1 a month; average skilled wages = USD 717.4 a month. 1 USD = 940.9 CLP (exchange rate of 19 July 2022). |

| 6 | The estimation output has been summarized due to space limitations but a complete output is available from the authors upon request. |

| 7 | National values for the AFF sector in 2020: average unskilled wages = USD 336.6 a month; average skilled wages = USD 549.1 a month. 1 USD = 940.9 CLP. (exchange rate of 19 July 2022). |

| 8 | We are grateful to two anonymous reviewers for raising this point. |

References

- Acemoglu, Daron, and Pascual Restrepo. 2020. Robots and Jobs: Evidence from US labor markets. Journal of Political Economy 128: 2188–244. [Google Scholar] [CrossRef]

- Acemoglu, Daron, David Autor, David Dorn, Gordon Hanson, and Brendan Price. 2016. Import competition and the great U.S. employment Sag of the 2000s. Journal of Labor Economics 34: 141–98. [Google Scholar] [CrossRef]

- Al Nasser, Omar. 2010. How does foreign direct investment affect economic growth? The role of local conditions. Latin American Business Review 11: 111–39. [Google Scholar] [CrossRef]

- AlAzzawi, Shireen. 2012. Innovation, productivity and foreign direct investment-induced R&D spillovers. The Journal of International Trade & Economic Development 21: 615–53. [Google Scholar]

- Alfaro, Laura. 2015. Foreign Direct Investment: Effects, Complementarities, and Promotion. In Partners or Creditors? Attracting Foreign Investment and Productive Development to Central America and Dominican Republic. Edited by Osmel Manzano, Sebastia’n Auguste and Mario Cuevas. Washington: Inter-American Development Bank, pp. 21–76. [Google Scholar]

- Alfaro, Laura. 2017. Gains from Foreign Direct Investment: Macro and Micro Approaches. The World Bank Economic Review 30: S2–S15. [Google Scholar] [CrossRef]

- Anderson, Kim, and Sundar Ponnusamy. 2019. Structural transformation to manufacturing and services: What role for trade? Asian Development Review 36: 32–71. [Google Scholar] [CrossRef]

- Anríquez, Gustavo, and Ramón López. 2007. Agricultural growth and poverty in an archetypical middle income country: Chile 1987–2003. Agricultural Economics 36: 191–202. [Google Scholar] [CrossRef]

- Antrás, Pol, and Stephen Yeaple. 2014. Multinational Firms and the Structure of International Trade. In Handbook of International Economics. Edited by Gita Gopinath, Elhanan Helpman and Kenneth Rogoff. Oxford: North Holland. [Google Scholar]

- Armstrong, Harvey, and Jim Taylor. 2000. Regional Economics and Policy, 3rd ed. Oxford: Blackwell. [Google Scholar]

- Ascani, Andrea, and Simona Iammarino. 2018. Multinational enterprises, service outsourcing and regional structural change. Cambridge Journal of Economics 42: 1585–611. [Google Scholar] [CrossRef]

- Asongu, Simplice, and Nicolas Odhiambo. 2020. Foreign direct investment, information technology and economic growth dynamics in Sub-Saharan Africa. Telecommunications Policy 44: 101838. [Google Scholar] [CrossRef]

- Asongu, Simplice, Uduak Akpan, and Salisu Isihak. 2018. Determinants of foreign direct investment in fast-growing economies: Evidence from the BRICS and MINT countries. Financial Innovation 4: 1–17. [Google Scholar] [CrossRef]

- Atienza, Miguel, and Félix Modrego. 2019. The spatially asymmetric evolution of mining services suppliers during the expansion and contraction phases of the copper super-cycle in Chile. Resources Policy 61: 77–87. [Google Scholar] [CrossRef]

- Autor, David, David Dorn, and Gordon Hanson. 2013. The China syndrome: Local labor market effects of import competition in the United States. American Economic Review 103: 2121–68. [Google Scholar] [CrossRef]

- Ayamba, Emmanuel, Chen Haibo, Abdul-Aziz Ibn Musah, Appiah Ruth, and Andrew Osei-Agyemang. 2019. An empirical model on the impact of foreign direct investment on China’s environmental pollution: Analysis based on simultaneous equations. Environmental Science and Pollution Research 26: 16239–48. [Google Scholar] [CrossRef] [PubMed]

- Bartik, Timothy. 1991. Who Benefits from State and Local Economic Development Policies? Kalamazoo: W.E. Upjohn Institute. [Google Scholar]

- Bayraktar, Nihal. 2013. Foreign direct investment and investment climate. Procedia Economics and Finance 5: 83–92. [Google Scholar] [CrossRef]

- Becker, Bettina, Nigel Driffield, Sandra Lancheros, and James Love. 2020. FDI in hot labour markets: The implications of the war for talent. Journal of International Business Policy 3: 107–33. [Google Scholar] [CrossRef]

- Berthélemy, Jean-Claude, and Sylvie Démurger. 2000. Foreign direct investment and economic growth: Theory and application to China. Review of Development Economics 4: 140–55. [Google Scholar] [CrossRef]

- Bhardwaj, Arjun, Joerg Dietz, and Paul Beamish. 2007. Host country cultural influences on foreign direct investment. Management International Review 47: 29–50. [Google Scholar] [CrossRef]

- Blanchard, Olivier, and Lawrence Katz. 1992. Regional evolutions. Brookings Papers on Economic Activity 1: 1–75. [Google Scholar] [CrossRef]

- Borensztein, Eduardo, José De Gregorio, and Jong-Wha Lee. 1998. How does foreign direct investment affect economic growth? Journal of International Economics 45: 115–35. [Google Scholar] [CrossRef]

- Borusyak, Kirill, Peter Hull, and Xavier Jaravel. 2022. Quasi-experimental shift-share research designs. The Review of Economic Studies 89: 181–213. [Google Scholar] [CrossRef]

- Brazys, Samuel, and Andreas Kotsadam. 2020. Sunshine or curse? foreign direct investment, the OECD anti-bribery convention, and individual corruption experiences in Africa. International Studies Quarterly 64: 956–67. [Google Scholar] [CrossRef]

- Broxterman, Daniel, and William Larson. 2020. An empirical examination of shift-share instruments. Journal of Regional Science 60: 677–711. [Google Scholar] [CrossRef]

- Caragliu, Andrea, and Peter Nijkamp. 2012. The impact of regional absorptive capacity on spatial knowledge spillovers: The Cohen and Levinthal model revisited. Applied Economics 44: 1363–74. [Google Scholar] [CrossRef]

- Cerda, Hernán. 2018. Inversión, stock de capital e infraestructuras en la economía chilena: Una aproximación por regiones y actividad económica, 1990–2010. Ph.D. Thesis, Universidad Complutense de Madrid, Madrid, Spain. [Google Scholar]

- Chakiel, Juan Eduardo, and Valeria Orellana. 2014. Inversión Extranjera Directa en Chile: Mecanismos de Ingreso y Compilación para la Balanza de Pagos. Estudios Económicos y Estadísticos del Banco Central de Chile N°109. Available online: https://www.bcentral.cl/documents/33528/133329/bcch_archivo_096501_es.pdf/4dd92ec9-f792-fc65-236b-86c6a57675a8?t=1655149111760 (accessed on 23 November 2022).

- Chowdhury, Abdur, and George Mavrotas. 2006. FDI and growth: What causes what? The World Economy 29: 9–19. [Google Scholar] [CrossRef]

- Christensen, Laurits, Dale Jorgenson, and Lawrence Lau. 1971. Conjugate duality and the transcendental logarithmic production function. Econometrica 39: 255–56. [Google Scholar]

- Cipollina, Maria, Giorgia Giovannetti, Filomena Pietrovito, and Alberto Pozzolo. 2012. FDI and growth: What cross-country industry data say. The World Economy 35: 1599–629. [Google Scholar] [CrossRef]

- Dhrifi, Abdelhafidh, Raouf Jaziri, and Saleh Alnahdi. 2020. Does foreign direct investment and environmental degradation matter for poverty? Evidence from developing countries. Structural Change and Economic Dynamics 52: 13–21. [Google Scholar] [CrossRef]

- Diewert, W. 1971. An application of the Shephard duality theorem: A generalized Leontief production function. Journal of Political Economy 79: 481–507. [Google Scholar] [CrossRef]

- Driffield, Niguel. 1999. Indirect employment effects of foreign direct investment into the UK. Bulletin of Economic Research 51: 207–22. [Google Scholar] [CrossRef]

- Driffield, Niguel, and Karl Taylor. 2000. FDI and the labour market: A review of the evidence and policy implications. Oxford Review of Economic Policy 16: 90–103. [Google Scholar] [CrossRef]

- Driffield, Niguel, James Love, and Karl Taylor. 2009. Productivity and labour demand effects of inward and outward foreign direct investment on UK industry. The Manchester School 77: 171–203. [Google Scholar] [CrossRef]

- Falahat, Mohammad, T. Ramayah, Pedro Soto-Acosta, and Yan-Yin Lee. 2020. SMEs internationalization: The role of product innovation, market intelligence, pricing and marketing communication capabilities as drivers of SMEs’ international performance. Technological Forecasting and Social Change 152: 119908. [Google Scholar] [CrossRef]

- Fernandes, Ana, and Caroline Paunov. 2012. Foreign direct investment in services and manufacturing productivity: Evidence for Chile. Journal of Development Economics 97: 305–21. [Google Scholar] [CrossRef]

- Goldsmith-Pinkham, Paul, Isaac Sorkin, and Henry Swift. 2020. Bartik instruments: What, when, why, and how. American Economic Review 110: 2586–624. [Google Scholar] [CrossRef]

- Gollin, Douglas, Remi Jedwab, and Dietrich Vollrath. 2016. Urbanization with and without industrialization. Journal of Economic Growth 21: 35–70. [Google Scholar] [CrossRef]

- Gopinath, Munisamy, and Weiyan Chen. 2003. Foreign direct investment and wages: A cross-country analysis. Journal of International Trade & Economic Development 12: 285–309. [Google Scholar]

- Hansen, Henrik, and John Rand. 2006. On the causal links between FDI and growth in developing countries. The World Economy 29: 21–41. [Google Scholar] [CrossRef]

- Harrison, Ann, and Andrés Rodríguez-Clare. 2010. Trade, Foreign Investment, and Industrial Policy for Developing Countries. In Handbook of Development Economics. Edited by Dani Rodrik and Mark Rosenzweig. Oxford: North Holland, vol. 5, pp. 4039–214. [Google Scholar]

- Haskel, Jonathan, Sonia Pereira, and Matthew Slaughter. 2007. Does inward foreign direct investment boost the productivity of domestic firms? The Review of Economics and Statistics 89: 482–96. [Google Scholar] [CrossRef]

- Haudi, H. Hadion Wijoyo, and Yoyok Cahyono. 2020. Analysis of Most Influential Factors to Attract Foreign Direct Investment. Journal of Critical Reviews 7: 4128–35. [Google Scholar]

- Helpman, Elhanan. 1984. A Simple Theory of Trade with Multinational Corporations. Journal of Political Economy 92: 451–71. [Google Scholar] [CrossRef]

- Hornberger, Kusi, Joseph Battat, and Peter Kusek. 2011. Attracting FDI: How Much Does Investment Climate Matter? New York: The World Bank Group. [Google Scholar]

- Huynh, Cong Minh, Vu Hong Nguyen, Hoang Bao Nguyen, and Phuc Canh Nguyen. 2020. One-way effect or multiple-way causality: Foreign direct investment, institutional quality and shadow economy? International Economics and Economic Policy 17: 219–39. [Google Scholar] [CrossRef]

- Jiang, Guohua, Masaaki Kotabe, Feng Zhang, Andy Hao, Justin Paul, and Cheng Lu Wang. 2020. The determinants and performance of early internationalizing firms: A literature review and research agenda. International Business Review 29: 101662. [Google Scholar] [CrossRef]

- Jordaan, Jacob. 2016. Foreign Direct Investment, Agglomeration and Externalities: Empirical Evidence from Mexican Manufacturing Industries. New York: Routledge. [Google Scholar]

- Jordaan, Jacob, and Eduardo Rodríguez-Oreggia. 2012. Regional growth in Mexico under trade liberalisation: How important are agglomeration and FDI? The Annals of Regional Science 48: 179–202. [Google Scholar] [CrossRef]

- Kinda, Tidiane. 2010. Investment climate and FDI in developing countries: Firm-level evidence. World Development 38: 498–513. [Google Scholar] [CrossRef]

- Kodama, Naomi, Beata Javorcik, and Yukiko Abe. 2018. Transplanting corporate culture across international borders: Foreign direct investment and female employment in Japan. The World Economy 41: 1148–65. [Google Scholar] [CrossRef]

- Kong, Qunxi, Rui Guo, Yang Wang, Xiuping Sui, and Shimin Zhou. 2020. Home-country environment and firms’ outward foreign direct investment decision: Evidence from Chinese firms. Economic Modelling 85: 390–99. [Google Scholar] [CrossRef]

- Majumder, Shapan, Md Hasanur Rahman, and Anobua Martial. 2022. The effects of foreign direct investment on export processing zones in Bangladesh using Generalized Method of Moments Approach. Social Sciences & Humanities Open 6: 100277. [Google Scholar]

- Malikov, Emir, and Shunan Zhao. 2021. On the estimation of cross-firm productivity spillovers with an application to fdi. The Review of Economics and Statistics, 1–46. [Google Scholar] [CrossRef]

- Markusen, James. 1984. Multinationals, Multi-Plant Economies, and the Gains from Trade. Journal of International Economics 16: 205–26. [Google Scholar] [CrossRef]

- Markusen, James, and Anthony Venables. 2000. The Theory of Endowment, Intra-Industry and Multinational Trade. Journal of International Economics 52: 209–34. [Google Scholar] [CrossRef]

- Melitz, Marc, and Stephen Redding. 2014. Heterogeneous Firms and Trade. In Handbook of International Economics. Edited by Gita Gopinath, Elhanan Helpman and Kenneth Rogoff. Oxford: North-Holland, vol. 4. [Google Scholar]

- Modrego, Félix, Andrea Canales, and Héctor Bahamonde. 2020. Employment effects of COVID-19 across Chilean regions: An application of the translog cost function. Regional Science Policy & Practice 12: 1151–67. [Google Scholar]

- Negash, Engidaw, Wenjie Zhu, Yangyang Lu, and Zhikai Wang. 2020. Does Chinese inward foreign direct investment improve the productivity of domestic firms? Horizontal linkages and absorptive capacities: Firm-level evidence from Ethiopia. Sustainability 12: 3023. [Google Scholar] [CrossRef]

- Ng, Linda, and Chyau Tuan. 2006. Spatial agglomeration, FDI, and regional growth in China: Locality of local and foreign manufacturing investments. Journal of Asian Economics 17: 691–713. [Google Scholar] [CrossRef]

- Nguyen, Thai Quan, Lien Thi Tran, Phoung Linh Pham, and Thanh Duc Nguyen. 2020. Impacts of foreign direct investment inflows on employment in Vietnam. Institutions and Economies 12: 37–62. [Google Scholar]

- Pegkas, Panagiotis. 2015. The impact of FDI on economic growth in Eurozone countries. The Journal of Economic Asymmetries 12: 124–32. [Google Scholar] [CrossRef]

- Sachs, Jeffrey. 2007. The importance of investment promotion in the poorest countries. In World Investment Prospects, (Special Edition). London: The Economist Intelligence Unit Ltd., pp. 78–81. [Google Scholar]

- Shephard, Ronald. 1953. Cost and Production Functions. Princeton: Princeton University Press. [Google Scholar]

- Van Wyk, Jay, and Anil Lal. 2010. FDI location drivers and risks in MENA. Journal of International Business Research 9: 99–116. [Google Scholar]

- Wang, Yanling. 2010. FDI and productivity growth: The role of inter-industry linkages. Canadian Journal of Economics/Revue Canadienne D’économique 43: 1243–72. [Google Scholar] [CrossRef]

- Wei, Yehua, and Chi Kin Leung. 2005. Development zones, foreign investment, and global city formation in Shanghai. Growth and Change 36: 16–40. [Google Scholar] [CrossRef]

- Zellner, Arnold, and Henri Theil. 1962. Three stage least squares: Simultaneous estimate of simultaneous equations. Econometrica 29: 54–78. [Google Scholar] [CrossRef]

- Zhang, Sufang, Wei Wang, Lu Wang, and Xiaoli Zhao. 2015. Review of China’s wind power firms internationalization: Status quo, determinants, prospects and policy implications. Renewable and Sustainable Energy Reviews 43: 1333–42. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).