Pathways to Prosperity: Navigating Post-Stagnation Growth and Revitalizing Business

Abstract

:1. Introduction

- –

- It identifies factors that enhance the probability of firms transitioning to growth after stagnation.

- –

- It unravels patterns of financial outcomes during periods of stagnation and subsequent growth.

- –

- It compares growth probabilities and dynamics between firms experiencing post-stagnation growth and those undergoing traditional rapid growth, within the ambit of organizational life cycle theory. Our study represents a novel enterprise-level exploration of the phenomenon of enterprise growth restart. While the existing literature has examined similar dynamics at macrolevels and in regional studies (Otiman 2008), this specific focus is unprecedented.

- –

- Profit: Although this metric reflects the firm’s stability and favorable market conditions, it is susceptible to rapid changes due to external factors, making it challenging to analyze growth determinants solely based on profit. Additionally, the relationship between growth and profitability merits separate investigation (Markman and Gartner 2002).

- –

- Employment or Fixed Assets: These are industry-specific measures with long-term characteristics that tend to change gradually at the onset of stagnation. It is generally observed that corporate growth leads to job creation (Davidsson and Delmar 2017). However, there are instances where job dynamics can sometimes move inversely to company growth (Brouwer et al. 1993).

- –

- Output: Performance indicators measured in physical units are inherently incomparable. A single enterprise may produce a variety of goods with different production dynamics. Thus, comparing physical output does not necessarily reflect company growth dynamics but rather market dynamics for specific goods. This perspective also considers growth resulting from productivity enhancements and production scale decisions (Aiello et al. 2011).

- –

- Sales: This metric is fundamental to evaluating company growth and presents no inherent contradictions in its dynamics. It allows for uniform assessment across various types of companies without necessitating differentiation based on other metrics (Delmar et al. 2003).

2. Literature Review

2.1. High-Growth Firms

2.2. Unpacking the Drivers and Varieties of Restarting Growth

- –

- A period of no positive revenue (sales) growth for three consecutive years during stagnation.

- –

- Subsequently, a positive sales growth rate for at least three out of four years during the growth period, categorized as follows:

- The first group of enterprises with an annual growth rate of 10% (accumulating to 30% or more over four years).

- The second group of enterprises with an annual growth rate exceeding 20% (accumulating to 60% or more over four years).

- The third group of enterprises with revenue growth for less than three years but an overall increase exceeding 60% over four years (to be addressed in a separate publication).

2.3. ‘Growth Firms’ versus ‘Growth Episodes’

3. Development of Research Hypotheses

3.1. Firm Age and Restarting Growth

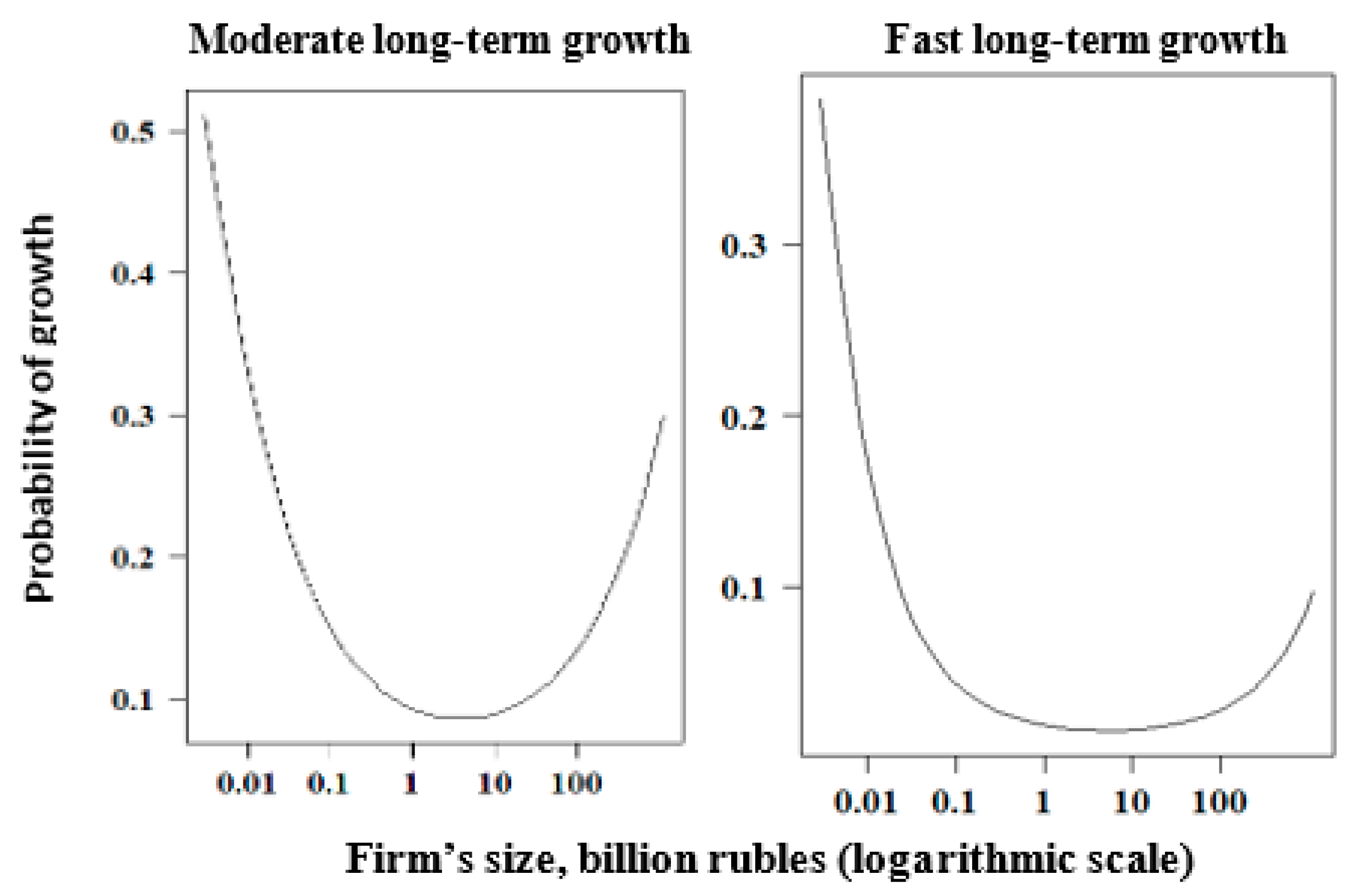

3.2. Firm Size and Restarting Growth

3.3. Decline in Sales during a Period of Stagnation and Restarting Growth

3.4. Investments in Fixed Assets and Restarting Growth

4. Methodological Framework

4.1. Data and Sample

- Moderate long-term growth: This category includes firms achieving an annual sales growth rate above 10% for at least three out of four post-stagnation years, with total sales growth over these four years surpassing 30%.

- Fast long-term growth: This category encompasses firms achieving an annual sales growth rate above 20% for at least three out of four post-stagnation years, with total sales growth over these four years exceeding 60%.

4.2. Models and Variables

4.2.1. Dependent Variables

4.2.2. Independent Variables

- Firm’s Age (Age): This variable is measured as the number of years elapsed from the company’s inception to the current date, as recorded in the SPARK database.

- Firm’s Size (Size): Firm size is operationalized using the natural logarithm of the firm’s total assets. To ensure temporal consistency in value terms, adjustments are applied based on the inflation index. This method of quantifying firm size aligns with the approaches adopted in previous studies (Bon and Hartoko 2022; Dang et al. 2018).

- Sales Dynamics in the Last Year of Stagnation (Sales Dynamics): This metric is computed as the percentage change in sales. It is determined by the ratio of the difference in sales between year t (the final year of stagnation) and year t − 1 to the sales in year t − 1 and then multiplied by 100%. This measure aims to capture the sales momentum or contraction as the firm transitions out of the stagnation phase.

- Intensity of Investment in Fixed Capital (Investment): We calculate this variable as the ratio of investment in fixed capital in the final year of the stagnation period to the value of the firm’s total assets, subsequently multiplied by 100%. This metric is designed to assess the firm’s investment activities relative to its asset base during the stagnation period.

4.2.3. Control Variables

- Leverage (Share of Borrowed Capital): Defined as the ratio of borrowed capital to total assets, multiplied by 100%. Leverage can aid in business modernization and expansion, potentially leading to growth following a period of stagnation (Arellano et al. 2012; Lin 2015; Baule 2018; Spitsin et al. 2020a).

- Net Return on Assets (ROA): Calculated as the ratio of net profit to total assets, multiplied by 100%. While a high ROA can generate internal funds for business development, it may also act as a disincentive for change (Coad and Srhoj 2019; Mansikkamäki 2023).

- Asset Turnover (Turnover): This metric is determined by the ratio of sales to total assets, multiplied by 100%. A reduction in turnover is typically observed during stagnation phases, indicating potential for operational efficiency improvements (Spitsin et al. 2021).

- Firms with State Participation (Firms with State): This variable accounts for the influence of state involvement in corporate activities in Russia, particularly during crises when the state may provide support. A dummy variable is used to control this factor’s impact on restarting growth.

- Industry Effects (Mining and HighTech): To account for industry-specific dynamics, two dummy variables are introduced for the mining industry and high-tech sector, respectively. These variables take the value of 1 for firms within these industries, reflecting expectations of differing restarting growth intensities across sectors (Ostapenko et al. 2022).

- External Conditions (GDP Growth): To control for the broader economic environment, a variable reflecting the total GDP dynamics over the four years corresponding to firms’ restarting growth is included. This variable captures the economic conditions of the country’s development (Athari et al. 2023).

- –

- A model that includes only control variables (Model 1). Based on Table 2, the logistic regression model expression for Model 1 can indeed be expressed as

- The logistic regression model employed in our study, referred to as Model 2, incorporates a comprehensive set of variables. This includes control variables, independent variables, and notably, a squared term for the variable ‘Size’ (Size2). The inclusion of Size2 is particularly significant as it allows for the testing of the non-linear relationship hypothesis concerning firm size and its impact on restarting growth, as described earlier in the study. This model formulation aligns with the methodological framework established for testing the hypotheses and ensures a robust and nuanced analysis of the factors influencing firm growth dynamics.

5. Empirical Results

6. Ad Hoc Analysis: Comprehensive Sales Dynamics throughout Stagnation and Subsequent Restarting Growth

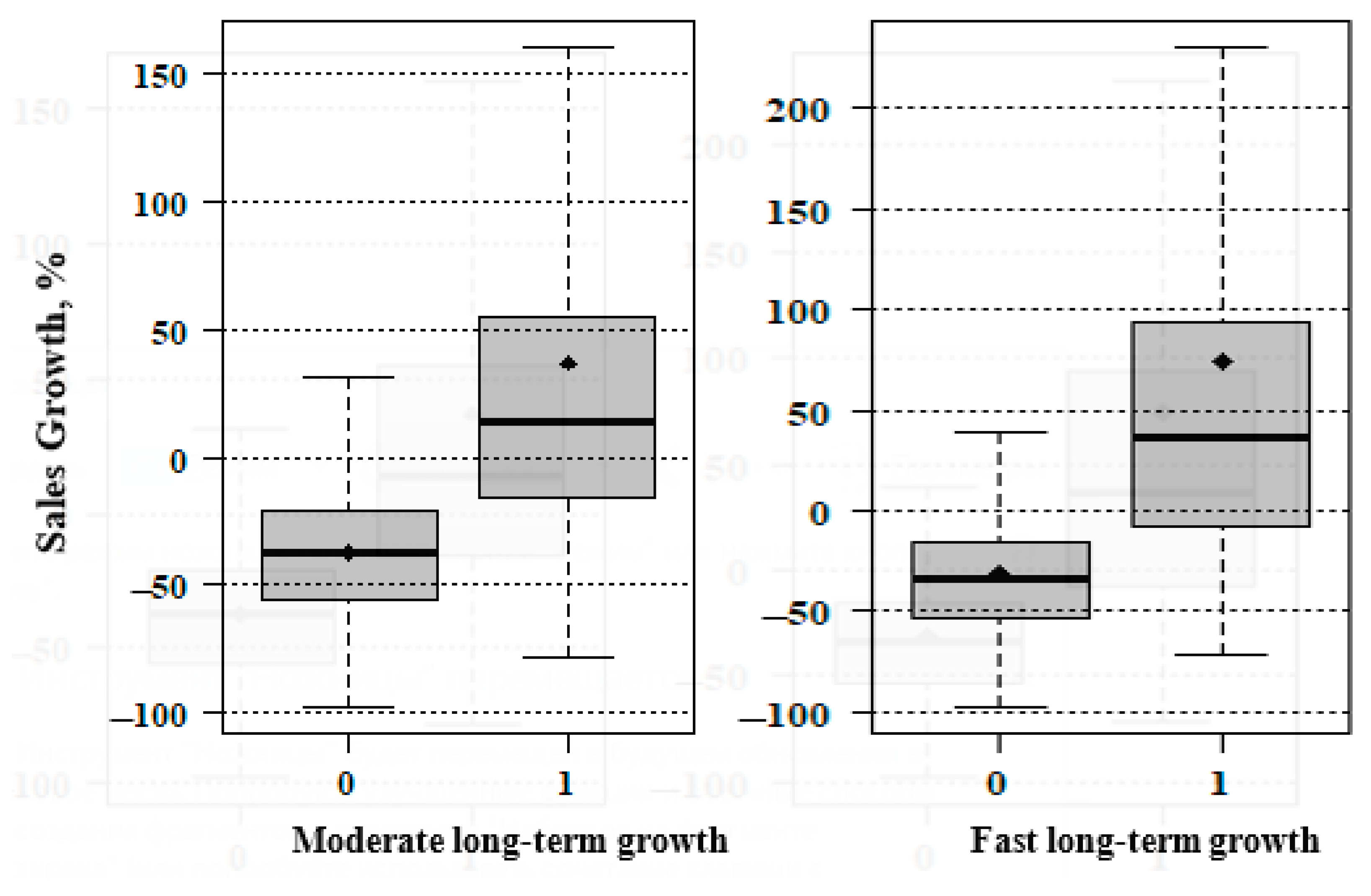

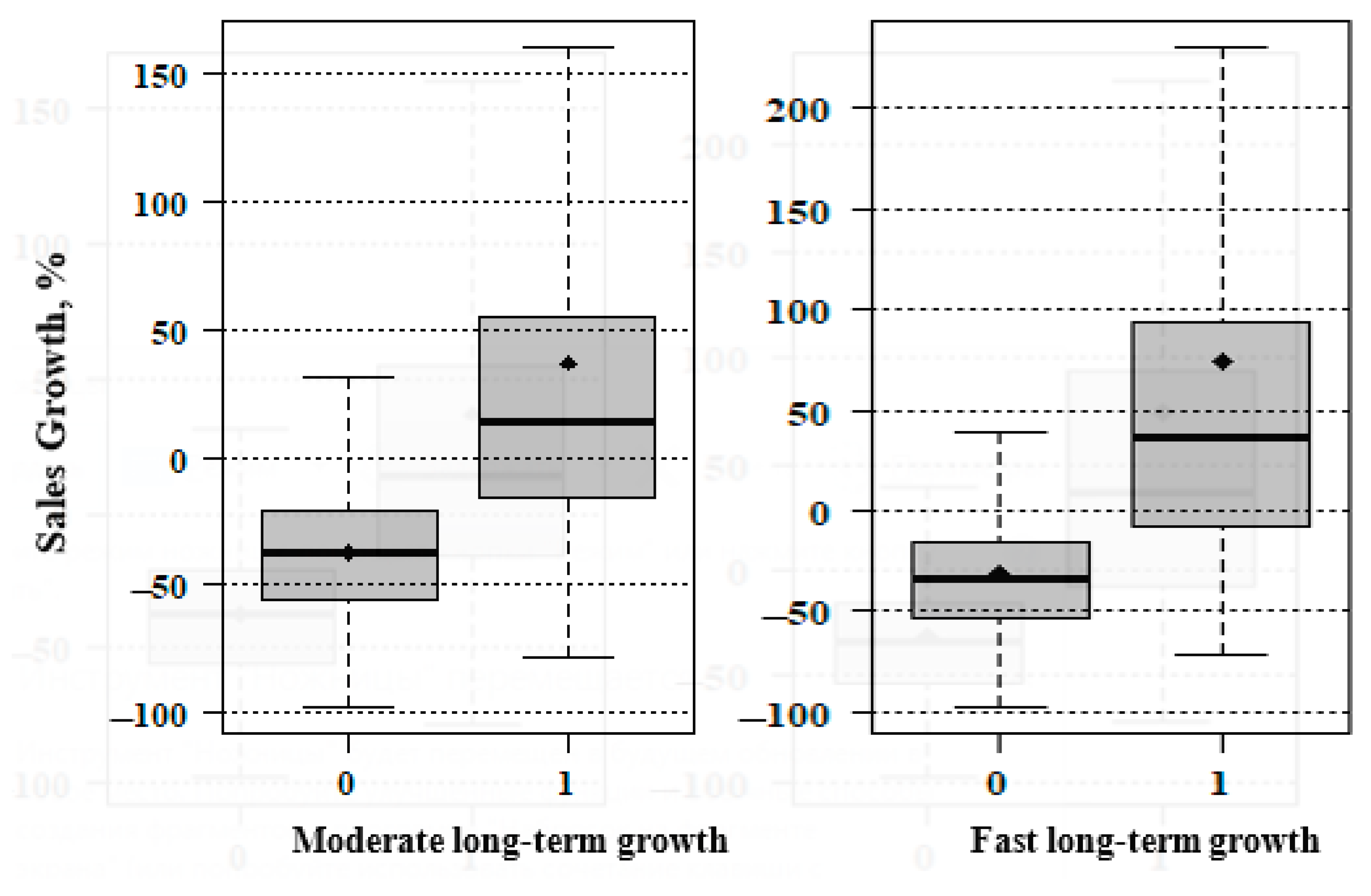

- –

- Sales Growth in group 1 is significantly higher than in group 0.

- –

- Sales Growth in group 1 is significantly higher than zero Sales Growth.

- –

- Sales Growth in group 0 is significantly lower than zero Sales Growth.

7. Robustness Check

8. Discussion

8.1. Theoretical Contribution

8.2. Practical Implementation

9. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Acs, Zoltan J., and Pamela Mueller. 2008. Employment Effects of Business Dynamics: Mice, Gazelles and Elephants. Small Business Economics 30: 85–100. [Google Scholar] [CrossRef]

- Adizes, I. 2004. Managing Corporate Lifecycles. Santa Barbara: The Adizes Institute Publishing. 460p. [Google Scholar]

- Aganbegyan, A. G. 2022. RUSSIA: FROM STAGNATION TO SUSTAINABLE SOCIO-ECONOMIC GROWTH. Scientific Works of the Free Economic Society of Russia 237: 310–62. [Google Scholar] [CrossRef]

- Aiello, Francesco, Camilla Mastromarco, and Angelo Zago. 2011. Be Productive or Face Decline. On the Sources and Determinants of Output Growth in Italian Manufacturing Firms. Empirical Economics 41: 787–815. [Google Scholar] [CrossRef]

- Albaz, Abdulaziz, Tarek Mansour, Tarek Rida, and Jörg Schubert. 2020. Setting Up Small and Medium-Size Enterprises for Restart and Recovery. June 9. Available online: http://dln.jaipuria.ac.in:8080/jspui/bitstream/123456789/10866/1/Setting-up-small-and-medium-size-enterprises-for-restart-and-recovery.pdf (accessed on 6 October 2023).

- Aldrich, Howard E., and Martin Ruef. 2018. Unicorns, Gazelles, and Other Distractions on the Way to Understanding Real Entrepreneurship in the United States. Academy of Management Perspectives 32: 458–72. [Google Scholar] [CrossRef]

- Ambrosio, F., A. Brasili, and K. Niakaros. 2021. European Scale-Up Gap: Too Few Good Companies or Too Few Good Investors; European Commission, Directorate-General for Research and Innovation. Available online: https://research-and-innovation.ec.europa.eu/knowledge-publications-tools-and-data/publications/all-publications/european-scale-gap-too-few-good-companies-or-too-few-good-investors_en (accessed on 6 October 2023).

- Andries, Petra, Koenraad Debackere, and Bart van Looy. 2013. Simultaneous Experimentation as a Learning Strategy: Business Model Development Under Uncertainty. Strategic Entrepreneurship Journal 7: 288–310. [Google Scholar] [CrossRef]

- Anyadike-Danes, Michael, Karen Bonner, Mark Hart, and Colin Mason. 2009. Measuring Business Growth: High Growth Firms and Their Contribution to Employment in the UK. London: National Endowment for Science, Technology and the Arts (NESTA). [Google Scholar]

- Arellano, Cristina, Yan Bai, and Jing Zhang. 2012. Firm Dynamics and Financial Development. Journal of Monetary Economics 59: 533–49. [Google Scholar] [CrossRef]

- Arrighetti, Alessandro, and Andrea Lasagni. 2013. Assessing the Determinants of High-Growth Manufacturing Firms in Italy. International Journal of the Economics of Business 20: 245–67. [Google Scholar] [CrossRef]

- Athari, Seyed Alireza, Farid Irani, and Abobaker AlAl Hadood. 2023. Country Risk Factors and Banking Sector Stability: Do Countries’ Income and Risk-Level Matter? Evidence from Global Study. Heliyon 9: e20398. [Google Scholar] [CrossRef]

- Åslund, A., and M. Snegovaya. 2021. The Impact of Western Sanctions on Russia and How They Can Be Made Even More Effective. Washington, DC: Atlantic Council, vol. 3. [Google Scholar]

- Bai, John (Jianqiu), Douglas Fairhurst, and Matthew Serfling. 2019. Employment Protection, Investment, and Firm Growth. Edited by David Denis. The Review of Financial Studies 33: 44–88. [Google Scholar] [CrossRef]

- Baranova, E. I. 2019. Patterns and evolution stages of the Russian high-growth firms. The Eurasian Scientific Journal 11: 1. Available online: https://esj.today/PDF/41ECVN119.pdf (accessed on 6 October 2023).

- Barrett, Richard. 2013. Liberating the Corporate Soul. Oxfordshire: Routledge. [Google Scholar] [CrossRef]

- Baule, Rainer. 2018. The Cost of Debt Capital Revisited. Business Research 12: 721–53. [Google Scholar] [CrossRef]

- Beck, Don Edward, and Christoher Cowan. 2014. Spiral Dynamics: Mastering Values, Leadership and Change. Hoboken: John Wiley and Sons. [Google Scholar]

- Bentzen, Jan, Erik Strøjer Madsen, and Valdemar Smith. 2012. Do Firms’ Growth Rates Depend on Firm Size? Small Business Economics 39: 937–47. [Google Scholar] [CrossRef]

- Birch, David. 1981. Who creates jobs? Public Interest 65: 3–14. [Google Scholar]

- Birch, David. 1987. Job Creation in America: How Our Smallest Companies Put the Most People to Work. New York: Free Press. [Google Scholar]

- Bloom, Nicholas, Robert Fletcher, and Ethan Yeh. 2021. The Impact of COVID-19 on US Firms. Cambridge, MA: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Bon, Sergius Fribontius, and Sri Hartoko. 2022. The Effect of Dividend Policy, Investment Decision, Leverage, Profitability, and Firm Size on Firm Value. European Journal of Business and Management Research 7: 7–13. [Google Scholar] [CrossRef]

- Brouwer, Erik, Alfred Kleinknecht, and Jeroen O. N. Reijnen. 1993. Employment Growth and Innovation at the Firm Level. Journal of Evolutionary Economics 3: 153–59. [Google Scholar] [CrossRef]

- Cabral, Luis. 1995. Sunk Costs, Firm Size and Firm Growth. The Journal of Industrial Economics 43: 161. [Google Scholar] [CrossRef]

- Campbell, Andrew, and Robert Park. 2005. The Growth Gamble. London: Nicholas Brealey International. [Google Scholar]

- Casnici, Cyntia Vilasboas Calixto. 2021. The Rise of Unicorn Companies: A Magical Growth? In The Palgrave Handbook of Corporate Sustainability in the Digital Era. Cham: Springer, pp. 581–93. [Google Scholar] [CrossRef]

- Chae, Ho-Chang. 2023. In Search of Gazelles: Machine Learning Prediction for Korean High-Growth Firms. Small Business Economics 62: 243–84. [Google Scholar] [CrossRef]

- Chen, Tain-Jy, and Ying-Hua Ku. 2000. The Effect of Foreign Direct Investment on Firm Growth: The Case of Taiwan’s Manufacturers. Japan and the World Economy 12: 153–72. [Google Scholar] [CrossRef]

- Coad, Alex, and Stjepan Srhoj. 2019. Catching Gazelles with a Lasso: Big Data Techniques for the Prediction of High-Growth Firms. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Croce, Annalisa, Elisa Ughetto, Stefano Bonini, and Vincenzo Capizzi. 2020. Gazelles, Ponies, and the Impact of Business Angels’ Characteristics on Firm Growth. Journal of Small Business Management 59: 223–48. [Google Scholar] [CrossRef]

- Dang, Chongyu, Zhichuan (Frank) Li, and Chen Yang. 2018. Measuring Firm Size in Empirical Corporate Finance. Journal of Banking & Finance 86: 159–76. [Google Scholar] [CrossRef]

- Daunfeldt, Sven-Olov, Dan Johansson, and Daniel Halvarsson. 2015. Using the Eurostat-OECD Definition of High-Growth Firms: A Cautionary Note. Journal of Entrepreneurship and Public Policy 4: 50–56. [Google Scholar] [CrossRef]

- Davidsson, Per, and Frédéric Delmar. 2017. Hunting for New Employment: The Role of High Growth Firms. In Small Firms and Economic Development in Developed and Transition Economies: A Reader. London: Routledge, pp. 7–19. [Google Scholar] [CrossRef]

- Decker, Ryan, John Haltiwanger, Ron Jarmin, and Javier Miranda. 2016. Where Has All the Skewness Gone? The Decline in High-Growth (Young) Firms in the U.S. Cambridge, MA: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Delmar, Frédéric, Per Davidsson, and William B. Gartner. 2003. Arriving at the High-Growth Firm. Journal of Business Venturing 18: 189–216. [Google Scholar] [CrossRef]

- Downs, Anthony. 1967. The life cycle of bureaus. Inside Bureaucracy 296: 309. [Google Scholar]

- Duruflé, Gilles, Thomas F. Hellmann, and Karen E. Wilson. 2016. From Start-Up to Scale-Up: Examining Public Policies for the Financing of High-Growth Ventures. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Eurostat-OECD. 2007. Manual on Business Demography Statistics. Available online: https://ec.europa.eu/eurostat/web/products-manuals-and-guidelines/-/ks-ra-07-010 (accessed on 6 October 2023).

- Evans, David S. 1987. The Relationship Between Firm Growth, Size, and Age: Estimates for 100 Manufacturing Industries. The Journal of Industrial Economics 35: 567. [Google Scholar] [CrossRef]

- Evans, Mark, and Elizabeth W. Garnsey. 2009. The Cambridge High Tech Cluster on the Eve of the Financial Crisis. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Ferrantino, Michael J., Megha Mukim, Alison Pearson, and Nathanael David Snow. 2012. Gazelles and Gazillas in China and India. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Foroni, Claudia, Massimiliano Marcellino, and Dalibor Stevanović. 2020. Forecasting the COVID-19 Recession and Recovery: Lessons from the Financial Crisis. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Gibrat, Robert. 1931. Les Inegalities Economiques. Paris: Sirey. [Google Scholar]

- Greiner, Larry E. 1997. Evolution and Revolution as Organizations Grow. Family Business Review 10: 397–409. [Google Scholar] [CrossRef]

- Grover Goswami, Arti, Denis Medvedev, and Ellen Olafsen. 2019. High-Growth Firms: Facts, Fiction, and Policy Options for Emerging Economies. Washington, DC: World Bank. [Google Scholar] [CrossRef]

- Hall, Bronwyn. 1986. The Relationship Between Firm Size and Firm Growth in the U.S. Manufacturing Sector. Cambridge, MA: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Halmai, Péter. 2021. COVID-Crisis and Economic Growth: Tendencies on Potential Growth in the European Union. Acta Oeconomica 71: 165–86. [Google Scholar] [CrossRef]

- Haltiwanger, John, Ian Hathaway, and Javier Miranda. 2014. Declining Business Dynamism in the U.S. High-Technology Sector. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Haltiwanger, John, Ron S. Jarmin, and Javier Miranda. 2013. Who Creates Jobs? Small versus Large versus Young. Review of Economics and Statistics 95: 347–61. [Google Scholar] [CrossRef]

- Haltiwanger, John, Ron S. Jarmin, and Robert B. Kulick. 2016. High Growth Young Firms: Contribution to Job, Output and Productivity Growth. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Halvarsson, Daniel. 2013a. Firm Dynamics: The Size and Growth Distribution of Firms. Doctoral dissertation, KTH Royal Institute of Technology, Stockholm, Sweden; p. 44. Available online: https://urn.kb.se/resolve?urn=urn:nbn:se:kth:diva-118333 (accessed on 6 October 2023).

- Halvarsson, Daniel. 2013b. Identifying High-Growth Firms. No 215, Ratio Working Papers, The Ratio Institute. Available online: https://www.diva-portal.org/smash/get/diva2:605658/FULLTEXT01.pdf (accessed on 6 February 2024).

- Hangstefer, James B. 2000. Revenue margin: A better way to measure company growth. Strategic Finance 82: 40. [Google Scholar]

- Hanks, Steven H. 1990. The organization life cycle: Integrating content and process. Journal of Small Business Strategy 1: 1–12. [Google Scholar]

- Hardy, Bryan, and Can Sever. 2021. Financial Crises and Innovation. European Economic Review 138: 103856. [Google Scholar] [CrossRef]

- Haveman, Heather A. 1993. Organizational Size and Change: Diversification in the Savings and Loan Industry after Deregulation. Administrative Science Quarterly 38: 20. [Google Scholar] [CrossRef]

- Heimonen, Tomi, and Markku Virtanen. 2012. Characteristics of Successful Gazelles—Problems in Approaches and Methods of Analysing the Data. International Journal of Business and Globalisation 9: 12. [Google Scholar] [CrossRef]

- Henderson, James, and Arild Moe. 2016. Gazprom’s LNG Offensive: A Demonstration of Monopoly Strength or Impetus for Russian Gas Sector Reform? Post-Communist Economies 28: 281–99. [Google Scholar] [CrossRef]

- Henrekson, Magnus, and Dan Johansson. 2010. Firm Growth, Institutions and Structural Transformation. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Hosmer, David W., Stanley Lemeshow, and Rodney X. Sturdivant. 2013. Applied Logistic Regression. Wiley Series in Probability and Statistics; Hoboken: John Wiley & Sons, Inc. [Google Scholar] [CrossRef]

- Johnson, Mark W., Clayton M. Christensen, and Henning Kagermann. 2008. Reinventing your business model. Harvard Business Review 86: 50–59. Available online: https://hbr.org/2008/12/reinventing-your-business-model (accessed on 6 October 2023).

- Jørgensen, Sveinung, and Lars Jacob Tynes Pedersen. 2018. RESTART Sustainable Business Model Innovation. Palgrave Studies in Sustainable Business In Association with Future Earth. Cham: Springer International Publishing. [Google Scholar] [CrossRef]

- Kirkham, Ksenia. 2016. The Formation of the Eurasian Economic Union: How Successful Is the Russian Regional Hegemony? Journal of Eurasian Studies 7: 111–28. [Google Scholar] [CrossRef]

- Knowles, Jonathan, Richard Ettenson, Patrick Lynch, and Joseph Dollens. 2020. Growth opportunities for brands during the COVID-19 crisis. MIT Sloan Management Review 61: 2–6. [Google Scholar]

- Kohler, Karsten, and Engelbert Stockhammer. 2021. Growing Differently? Financial Cycles, Austerity, and Competitiveness in Growth Models since the Global Financial Crisis. Review of International Political Economy 29: 1314–41. [Google Scholar] [CrossRef]

- Kudrin, Alexey, and Evsey Gurvich. 2015. A New Growth Model for the Russian Economy1. Russian Journal of Economics 1: 30–54. [Google Scholar] [CrossRef]

- Lin, Qi. 2015. Growth Options Effect on Leverage: Evidence from China. Pacific-Basin Finance Journal 34: 152–68. [Google Scholar] [CrossRef]

- Maiti, Moinak, Darko Vuković, Amrit Mukherjee, Pavan D. Paikarao, and Janardan Krishna Yadav. 2022. Advanced Data Integration in Banking, Financial, and Insurance Software in the Age of COVID-19. Software: Practice and Experience 52: 887–903. [Google Scholar] [CrossRef] [PubMed]

- Mansikkamäki, Susanna. 2023. Firm Growth and Profitability: The Role of Age and Size in Shifts between Growth–Profitability Configurations. Journal of Business Venturing Insights 19: e00372. [Google Scholar] [CrossRef]

- Markman, Gideon D., and William B. Gartner. 2002. Is Extraordinary Growth Profitable? A Study ofInc. 500High–Growth Companies. Entrepreneurship Theory and Practice 27: 65–75. [Google Scholar] [CrossRef]

- Marquardt, Donald W. 1980. A Critique of Some Ridge Regression Methods: Comment. Journal of the American Statistical Association 75: 87. [Google Scholar] [CrossRef]

- Mayr, Stefan, Christine Mitter, and Andrea Aichmayr. 2017. Corporate Crisis and Sustainable Reorganization: Evidence from Bankrupt Austrian SMEs. Journal of Small Business Management 55: 108–27. [Google Scholar] [CrossRef]

- McGrath, Rita Gunther. 2010. Business Models: A Discovery Driven Approach. Long Range Planning 43: 247–61. [Google Scholar] [CrossRef]

- Megaravalli, Amith Vikram. 2017. Estimating Growth of SMES Using a Logit Model: Evidence from Manufacturing Companies in Italy. Management Science Letters, 125–34. [Google Scholar] [CrossRef]

- Metzger, Georg. 2006. Once Bitten, Twice Shy? The Performance of Entrepreneurial Restarts. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Miller, Danny, and Peter H. Friesen. 1983. Successful and Unsuccessful Phases of the Corporate Life Cycle. Organization Studies 4: 339–56. [Google Scholar] [CrossRef]

- Nagelkerke, Nico. 1991. A Note on a General Definition of the Coefficient of Determination. Biometrika 78: 691–92. [Google Scholar] [CrossRef]

- National Endowment for Science, Technology and the Arts (NESTA). 2009. The Vital 6 per Cent: How High-Growth Innovative Businesses Generate Prosperity and Jobs, NESTA, London. Available online: www.nesta.org.uk/library/documents/Report-Summary-Vital-6-per-cent-v13.pdf (accessed on 6 October 2023).

- Nightingale, Paul, and Alex Coad. 2014. Muppets and Gazelles: Political and Methodological Biases in Entrepreneurship Research. Industrial and Corporate Change 23: 113–43. [Google Scholar] [CrossRef]

- Oliveira, Blandina, and Adelino Fortunato. 2006. Firm Growth and Liquidity Constraints: A Dynamic Analysis. Small Business Economics 27: 139–56. [Google Scholar] [CrossRef]

- Organisation for Economic Co-operation and Development (OECD). 2008. Eurostat-OECD Manual on Business Demography Eurostat Electronic Report. Available online: https://ec.europa.eu/eurostat/web/products-manuals-and-guidelines/-/ks-ra-07-010 (accessed on 6 October 2023).

- Ostapenko, Svitlana, Ana Paula Africano, and Raquel Meneses. 2022. Cluster Dynamics and Firms’ Strategies—An Integrative Framework. EuroMed Journal of Business, August 8. [Google Scholar] [CrossRef]

- Otiman, Paun Ioan. 2008. Rural development and agriculture: Opportunities to attenuate the economic and financial crisis and to resume economic growth. Agricultural Economics and Rural Development 5: 97–128. [Google Scholar]

- Park, Kwangmin, and SooCheong (Shawn) Jang. 2010. Firm Growth Patterns: Examining the Associations with Firm Size and Internationalization. International Journal of Hospitality Management 29: 368–77. [Google Scholar] [CrossRef]

- Perrini, Francesco, and Antonio Tencati. 2006. Sustainability and Stakeholder Management: The Need for New Corporate Performance Evaluation and Reporting Systems. Business Strategy and the Environment 15: 296–308. [Google Scholar] [CrossRef]

- Piaskowska, Dorota, Esther Tippmann, and Sinéad Monaghan. 2021. Scale-up Modes: Profiling Activity Configurations in Scaling Strategies. Long Range Planning 54: 102101. [Google Scholar] [CrossRef]

- Pokorná, Pavla. 2020. Financial Sources for Company Scale-Up. In Developing Entrepreneurial Competencies for Start-Ups and Small Business. Advances in Business Strategy and Competitive Advantage. Hershey: IGI Global, pp. 97–108. [Google Scholar] [CrossRef]

- Postelnicu, Cătălin, and Irina M. Ban. 2010. Some Empirical Approaches of the Competitiveness’ Diamond-The Case of Romanian Economy. Romanian Economic Journal 36: 53–77. [Google Scholar]

- Preisendörfer, Peter, and Thomas Voss. 1990. Organizational Mortality of Small Firms: The Effects of Entrepreneurial Age and Human Capital. Organization Studies 11: 107–29. [Google Scholar] [CrossRef]

- Savin, Ivan, and Maria Novitskaya. 2023. Data-Driven Definitions of Gazelle Companies That Rule out Chance: Application for Russia and Spain. Eurasian Business Review 13: 507–42. [Google Scholar] [CrossRef]

- Sirén, Charlotta, Henri Hakala, Joakim Wincent, and Dietmar Grichnik. 2017. Breaking the Routines: Entrepreneurial Orientation, Strategic Learning, Firm Size, and Age. Long Range Planning 50: 145–67. [Google Scholar] [CrossRef]

- Spark Information System. 2023. Available online: https://spark-interfax.com/ (accessed on 6 October 2023).

- Spitsin, Vladislav, Alexandr Mikhalchuk, Darko Vukovic, and Lubov Spitsina. 2023a. Technical Efficiency of High-Technology Industries in the Crisis: Evidence from Russia. Journal of the Knowledge Economy 14: 200–25. [Google Scholar] [CrossRef]

- Spitsin, Vladislav, Darko B. Vukovic, Lubov Spitsina, and Mustafa Özer. 2021. The Impact of High-Tech Companies’ Performance and Growth on Capital Structure. Competitiveness Review: An International Business Journal 32: 975–94. [Google Scholar] [CrossRef]

- Spitsin, Vladislav, Darko Vukovic, Alexander Mikhalchuk, Lubov Spitsina, and Daria Novoseltseva. 2023b. High-Tech Gazelle Firms at Various Stages of Evolution: Performance and Distinctive Features. Journal of Economic Studies 50: 674–95. [Google Scholar] [CrossRef]

- Spitsin, Vladislav, Darko Vukovic, Sergey Anokhin, and Lubov Spitsina. 2020a. Company Performance and Optimal Capital Structure: Evidence of Transition Economy (Russia). Journal of Economic Studies 48: 313–32. [Google Scholar] [CrossRef]

- Spitsin, Vladislav, Marina Ryzhkova, Darko Vukovic, and Sergey Anokhin. 2020b. Companies Profitability under Economic Instability: Evidence from the Manufacturing Industry in Russia. Journal of Economic Structures 9: 9. [Google Scholar] [CrossRef]

- Srhoj, Stjepan. 2022. Can We Predict High Growth Firms with Financial Ratios? Financial Internet Quarterly 18: 66–73. [Google Scholar] [CrossRef]

- Tomenendal, Matthias, Florian Becker-Ritterspach, and Christoph Dörrenbächer. 2022. Taking Stock and Moving Forward: Some Concluding Remarks on Gazelle Firms and Gazelle Research. In The Promises and Properties of Rapidly Growing Companies: Gazelles. Leeds: Emerald Publishing Limited, pp. 149–54. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh. 2019. Leverage and Corporate Investment—Evidence from Vietnam. Finance Research Letters 28: 1–5. [Google Scholar] [CrossRef]

- Vukovic, Darko B., Alexander Zobov, and Ekaterina Degtereva. 2022. The Nexus between Tourism and Regional Real Growth: Dynamic Panel Threshold Testing. Journal of the Geographical Institute “Jovan Cvijic” SASA 72: 111–16. [Google Scholar] [CrossRef]

- Vukovic, Darko B., Edin Hanic, and Hasan Hanic. 2017. Financial Integration in the European Union - the Impact of the Crisis on the Bond Market. Equilibrium. Quarterly Journal of Economics and Economic Policy 12: 195–210. [Google Scholar] [CrossRef]

- Wilber, Ken. 2005. Introduction to integral theory and practice. AQAL: Journal of Integral Theory and Practice 1: 2–38. [Google Scholar]

- Xiang, Shihui, Saad Rasool, Yong Hang, Kamran Javid, Tasawar Javed, and Alin Emanuel Artene. 2021. The Effect of COVID-19 Pandemic on Service Sector Sustainability and Growth. Frontiers in Psychology 12: 633597. [Google Scholar] [CrossRef]

- Yashin, Sergei, Yurii Trifonov, and Egor Koshelev. 2016. Forecasting the company growth rate based on reinvestment rate, profit margin and capital turnover. Финансы и кредит 1: 38–51. Available online: http://213.226.126.9/fc/2016/fc01/fc0116-38.pdf (accessed on 6 October 2023).

- Zekić-Sušac, Marijana, Nataša Šarlija, Adela Has, and Ana Bilandžić. 2016. Predicting Company Growth Using Logistic Regression and Neural Networks. Croatian Operational Research Review 7: 229–48. [Google Scholar] [CrossRef]

- Zhou, Kevin Zheng, David K. Tse, and Julie Juan Li. 2006. Organizational Changes in Emerging Economies: Drivers and Consequences. Journal of International Business Studies 37: 248–63. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| No. | Direction/Approach | Summary | Scholars |

|---|---|---|---|

| 1 | Terminal Decline | The life cycle concludes with the cessation of growth or the dissolution of the organization. The potential revival is seen as a transient phase preceding decline (Adizes). | (Downs 1967; Adizes 2004; Miller and Friesen 1983; Hanks 1990) |

| 2 | Renewal Post-Recession | The cycle concludes with a phase of renewal, leading to a new stage of development. | |

| 2.1 | Integral Theory—Spiral Dynamics Model—Discovery Driven Approach | Organizations evolve in a manner akin to human and social organisms, where organizational disbandment signals a new developmental phase (Wilber). External influences and their management can forestall organizational demise (Beck and Cowan), with growth emerging from ‘discovery’ under uncertainty (McGrath). | (Wilber 2005; Beck and Cowan 2014; McGrath 2010) |

| 2.2 | Organizational Life Cycle—Corporate Transformation Model | Corporate evolution involves navigating through crises via diverse strategies, such as reducing administrative burdens (Greiner) or altering organizational values (Barrett). | (Greiner 1997; Barrett 2013) |

| 2.3 | Restart Framework | Growth is achieved by redesigning business models and engaging in controlled experimentation, shifting focus to service-oriented and circular business models, and fostering collaborative alliances (Jørgensen and Pedersen 2018; Johnson et al. 2008; Andries et al. 2013). Outcome-driven business models are emphasized (Perrini and Tencati 2006). | (Jørgensen and Pedersen 2018; Johnson et al. 2008; Andries et al. 2013) |

| 2.4 | Reinvestment of Retained Earnings | Restarting growth is attributed to altering reinvestment strategies of retained earnings. Revenue response to investment may be delayed (Yashin et al. 2016), with reinvestment being a nuanced internal policy decision (Pokorná). | (Pokorná 2020; Yashin et al. 2016) |

| 2.5 | Serendipity | Rapid growth is not always feasible due to market rigidity and infrastructural limitations, which can amplify business risks. Growth thus is seen as an interplay of strategic actions and fortuitous events, cautioning against the pursuit of high growth rates. | (Campbell and Park 2005) |

| 2.6 | New Firm vs. Reestablishing a Firm | Entrepreneurs may either establish new firms alongside existing ones (‘portfolio entrepreneurs’) or disengage from current ventures to initiate new ones (‘restarters’). This bifurcation complicates the statistical tracking of growth restarts in the context of corporate restructuring. | (Metzger 2006) |

| 2.7 | Entrepreneur Personality | A firm’s growth correlates with the leader’s persona (encompassing human capital and prior business failures), although the leader’s influence tends to wane as the company matures. | (Preisendörfer and Voss 1990) |

| 2.8 | Systemic State Impact | Post-COVID, a widespread rejuvenation in the growth of companies, particularly SMEs, was necessitated. Discussions focus on aid for business resumption and the cultivation of personalized, systemic collaboration between government entities and SME ecosystems. | (Albaz et al. 2020) |

| N | Variable | Mean | Std. Deviation | VIF | 1 | 2 | 3 | 4 |

| 1 | Leverage | 54.52 | 39.24 | 1.17 | 1 | |||

| 2 | ROA | 2.61 | 14.36 | 1.14 | −0.26 *** | 1 | ||

| 3 | Turnover | 165.67 | 145.85 | 1.40 | 0.11 *** | 0.08 *** | 1 | |

| 4 | HighTech | 0.17 | 0.38 | 1.06 | 0.04 | 0.05 * | 0.03 | 1 |

| 5 | Mining | 0.03 | 0.18 | 1.14 | 0.04 λ | 0.08 ** | −0.11 *** | −0.08 *** |

| 6 | Firms with State | 0.04 | 0.19 | 1.04 | −0.07 ** | −0.01 | −0.06 ** | 0.16 *** |

| 7 | GDP Growth | 6.23 | 1.31 | 1.02 | −0.05 * | 0.00 | 0.04 | 0.02 |

| 8 | Age | 17.20 | 6.14 | 1.07 | −0.19 *** | −0.04 λ | −0.07 ** | −0.06 * |

| 9 | Size | 19.51 | 1.66 | 1.45 | −0.01 | −0.03 | −0.47 *** | −0.10 *** |

| 10 | Sales Dynamics | −14.57 | 13.34 | 1.11 | −0.08 *** | 0.18 ** | 0.19 *** | −0.05 * |

| 11 | Investment | 2.37 | 5.30 | 1.04 | −0.07 ** | 0.04 λ | −0.02 | −0.03 |

| N | Variable | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| 1 | Leverage | |||||||

| 2 | ROA | |||||||

| 3 | Turnover | |||||||

| 4 | HighTech | |||||||

| 5 | Mining | 1 | ||||||

| 6 | Firms with State | 0.01 | 1 | |||||

| 7 | GDP Growth | −0.10 *** | 0.00 | 1 | ||||

| 8 | Age | −0.01 | 0.07 ** | 0.05 * | 1 | |||

| 9 | Size | 0.31 *** | 0.03 | −0.09 *** | 0.09 *** | 1 | ||

| 10 | Sales Dynamics | 0.00 | −0.01 | 0.03 | 0.07 ** | 0.00 | 1 | |

| 11 | Investment | 0.10 *** | 0.00 | −0.03 | 0.05 * | 0.11 *** | 0.12 *** | 1 |

| Variables | Model 1 (MLTG) | Model 2 (MLTG) | Model 1 (FLTG) | Model 2 (FLTG) |

|---|---|---|---|---|

| Intercept | −1.82 *** (0.07) | −2.06 *** (0.09) | −3.08 *** (0.12) | −3.57 *** (0.17) |

| Leverage | 0.20 ** (0.06) | 0.15 * (0.06) | 0.17 * (0.09) | 0.15 (0.09) |

| ROA | −0.13 (0.08) | −0.09 (0.08) | −0.27 ** (0.10) | −0.16 (0.11) |

| Turnover | −0.32 *** (0.09) | −0.49 *** (0.11) | −0.11 (0.12) | −0.30 λ (0.16) |

| HighTech | 0.11 (0.06) | 0.03 (0.07) | 0.17 (0.10) | 0.04 (0.11) |

| Mining | −0.06 (0.07) | −0.05 (0.08) | 0.00 (0.11) | 0.05 (0.12) |

| Firms with State | −0.02 (0.07) | 0.00 (0.07) | 0.02 (0.10) | 0.05 (0.11) |

| GDP Growth | −0.08 (0.07) | −0.06 (0.07) | 0.04 (0.11) | 0.06 (0.12) |

| Age | −0.33 *** (0.07) | −0.26 * (0.11) | ||

| Size | −0.40 *** (0.10) | −0.62 *** (0.16) | ||

| Size2 | 0.13 ** (0.04) | 0.18 ** (0.07) | ||

| Sales Dynamics | −0.31 *** (0.06) | −0.56 *** (0.09) | ||

| Investment | 0.10 λ (0.06) | 0.14 λ (0.08) | ||

| Pseudo R2 | 0.037 | 0.105 | 0.031 | 0.140 |

| LR χ2 | 38.36 on 7 DF | 112.04 on 12 DF | 17.84 on 7 DF | 83.40 on 12 DF |

| p | <0.001 | <0.001 | 0.013 | <0.001 |

| Area under ROC Curve | 0.630 | 0.693 | 0.637 | 0.743 |

| Variables | Model 2 (MLTG) | Model 2 (FLTG) |

|---|---|---|

| Intercept | −2.06 *** (0.10) | −3.57 *** (0.17) |

| Leverage | 0.15 * (0.07) | 0.15 λ (0.08) |

| ROA | −0.09 (0.09) | −0.16 (0.13) |

| Turnover | −0.49 ** (0.17) | −0.30 (0.22) |

| HighTech | 0.03 (0.07) | 0.04 (0.12) |

| Mining | −0.05 (0.08) | 0.05 (0.13) |

| Firms with State | 0.00 (0.07) | 0.05 (0.11) |

| GDP Growth | −0.06 (0.07) | 0.06 (0.12) |

| Age | −0.33 *** (0.07) | −0.26 * (0.11) |

| Size | −0.40 *** (0.11) | −0.62 *** (0.18) |

| Size2 | 0.13 ** (0.04) | 0.18 ** (0.06) |

| Sales Dynamics | −0.31 *** (0.06) | −0.56 *** (0.10) |

| Investment | 0.10 λ (0.06) | 0.14 * (0.06) |

| Pseudo R2 | 0.105 | 0.140 |

| LR χ2 | 112.04 on 12 DF | 83.40 on 12 DF |

| p | <0.001 | <0.001 |

| Area under ROC Curve | 0.693 | 0.743 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Spitsin, V.; Vuković, D.B.; Ryzhkova, M.; Leonova, V. Pathways to Prosperity: Navigating Post-Stagnation Growth and Revitalizing Business. Economies 2024, 12, 55. https://doi.org/10.3390/economies12030055

Spitsin V, Vuković DB, Ryzhkova M, Leonova V. Pathways to Prosperity: Navigating Post-Stagnation Growth and Revitalizing Business. Economies. 2024; 12(3):55. https://doi.org/10.3390/economies12030055

Chicago/Turabian StyleSpitsin, Vladislav, Darko B. Vuković, Marina Ryzhkova, and Victoria Leonova. 2024. "Pathways to Prosperity: Navigating Post-Stagnation Growth and Revitalizing Business" Economies 12, no. 3: 55. https://doi.org/10.3390/economies12030055

APA StyleSpitsin, V., Vuković, D. B., Ryzhkova, M., & Leonova, V. (2024). Pathways to Prosperity: Navigating Post-Stagnation Growth and Revitalizing Business. Economies, 12(3), 55. https://doi.org/10.3390/economies12030055