Determinants of Tax Ethics in Society: Statistical and Logistic Regression Approach

Abstract

:1. Introduction

1.1. Literature Review

1.2. Main Hypotheses

2. Materials and Methods

2.1. Sample

- z is z-statistics,

- p is the proportion in the population,

- n is the sample size,

- N is the size of the population, in this case: 4,222,130.

- p is the proportion in the population,

- N is the size of the population,

- s.e. is the standard error of the estimate, which was calculated as:

- m.e. is the margin of error, which was set to 3%, and z is the z-statistic, which is equal to 1.96 at the 95% confidence level.

2.2. Structure of Respondents

- sex: men, women,

- completed education: elementary, secondary, university,

- source of income: employee, self-employed person/entrepreneur, unemployed, pensioner, full-time student.

2.3. Questionnaire

- information on the respondents, in relation to the characteristics of the quota sample.

- questions focused on the respondents’ personal experience with tax situations and their tax knowledge.

- respondents’ tax morale and their sense of the tax burden.

- respondents’ willingness to improve their tax behaviour.

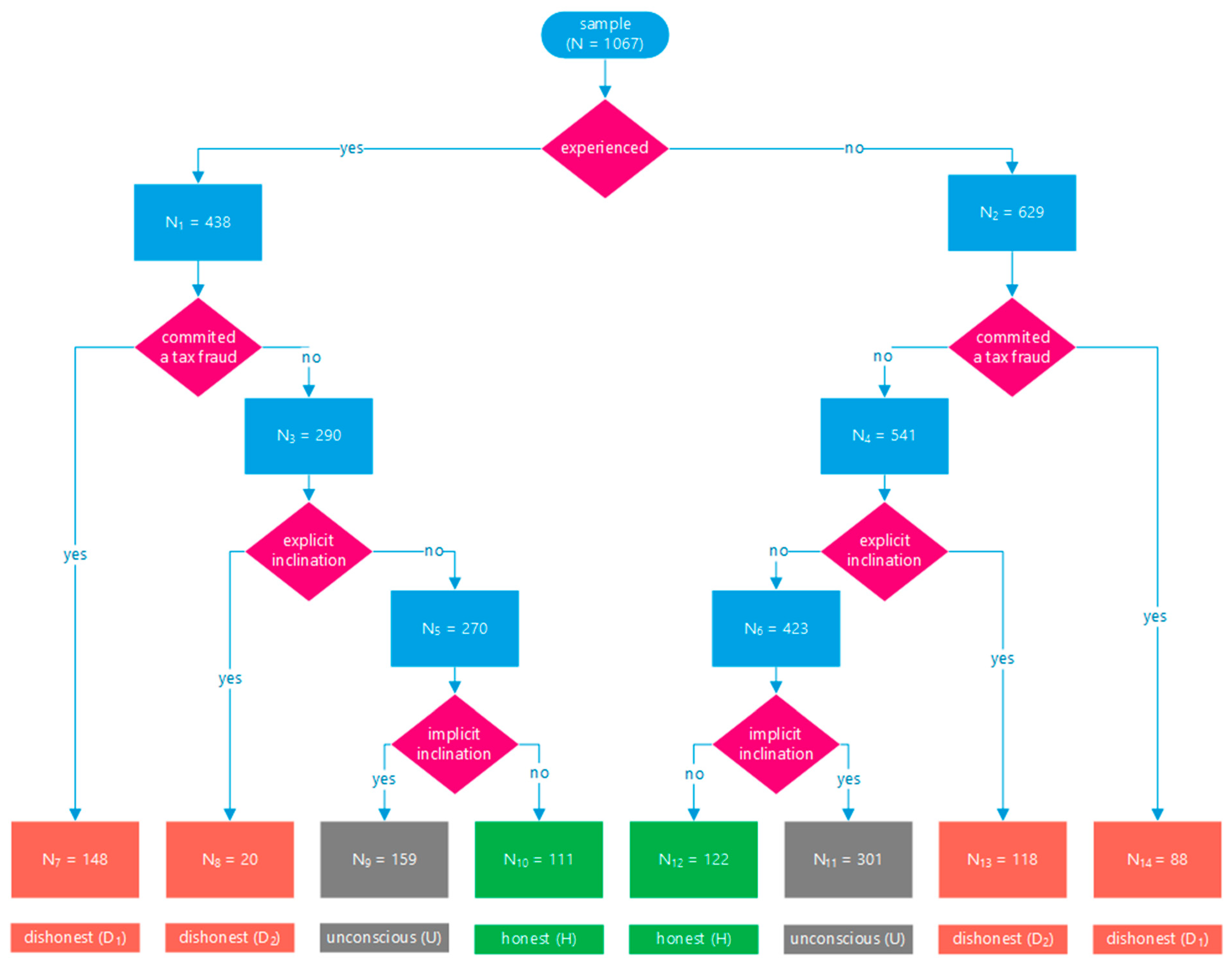

2.4. Sorting Methodology

- whether they had committed deliberate tax evasion or tax fraud at least once in their lives.

- for respondents who did a tax liability calculation or tax return for themselves or another person, whether these persons tried to reduce the tax liability against the law.

- for respondents who did not do any calculation of tax liability or tax return for themselves or any other person, if they had the opportunity, would they try to reduce the tax liability by violating the law?

- unconscious behaviour of respondents in dealing with common situations that involve potential tax evasion.

- experienced, i.e., they have experience in resolving tax issues (they have done tax returns, participated in tax proceedings, tax audits, or do business).

- inexperienced, i.e., they have no experience in dealing with tax issues.

- committed tax fraud, i.e., people who have done deliberate tax evasion.

- did not commit tax fraud, i.e., people who have never done conscious tax evasion.

- explicitly inclined—people who would do tax evasion if they had the opportunity,

- explicitly not inclined—people who would not commit any tax evasion, even if they had the opportunity.

- implicitly inclined—people with an implicit tendency to commit tax evasion. Respondents chose an answer in which there was any tax evasion.

- implicitly not inclined—people with an implicit denial to commit any tax evasion. Respondents chose an answer to the question in which there was no tax evasion.

3. Results

3.1. Descriptive Analysis

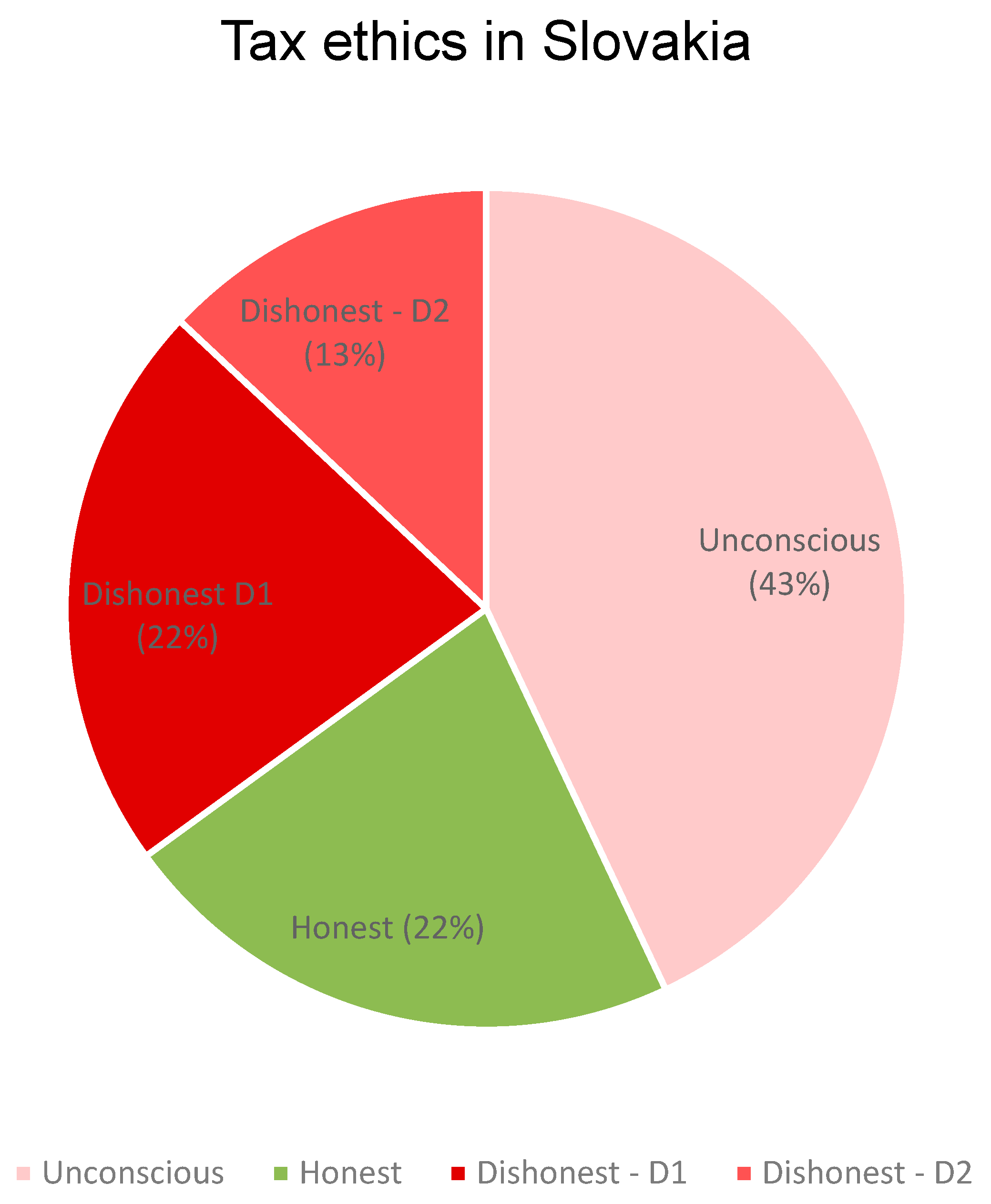

- 43% of respondents chose an answer that would lead to tax evasion. If these respondents found themselves in a situation in which they had a chance to commit tax evasion, they would do it or participate in it. However, we assume that it would be unconscious tax evasion, primarily due to ignorance of tax law, without the intention of violating tax laws. These respondents also showed a tendency to tax evasion, although not aware. We labelled this part of the sample as unconscious (U).

- 22% of respondents chose an answer, the implementation of which would not violate tax law. This part of the respondents did not have a conscious or unconscious tendency to tax evasion. We named this group as honest (H).

3.2. Hypotheses Testing

3.2.1. Main Hypotheses

3.2.2. Tax Ethics and Socio-Demographic Factors

- E1: Tax ethics vary depending on sex.

- E2: Tax ethics vary depending on education.

- E3: Tax ethics vary with age.

- E4: Tax ethics vary depending on the main source of income.

- E5: The tax ethics of people experienced in tax issues differs from tax ethics of people who are considered inexperienced in this area.

- EC1: Women are generally less prone to explicit tax evasion than men.

- EC2: Women are generally more likely to commit unconscious (implicit) tax evasion than men.

- EC3: People with only an elementary education are significantly more prone to tax evasion (explicit + implicit) than people with a secondary education.

- EC4: People with elementary education are significantly more prone to tax evasion (explicit + implicit) than people with a university degree.

- EC5: The tax ethics of the younger generation are worse than the tax ethics of the older generation (tested by: more young people state they would do tax evasion if they had the opportunity than the middle-aged generation).

- EC6: The 60+ age group is less prone to tax evasion (explicit + implicit) than the 31–60 age group.

- EC7: The 60+ age group is less prone to tax evasion (explicit + implicit) than the 18–30 age group.

- EC8: The tax ethics of entrepreneurs are worse than the tax ethics of non-entrepreneurs.

- EC9: Students’ tax ethics are worse than employees’ tax ethics.

- EC10: Students’ tax ethics are worse than the tax ethics of entrepreneurs.

- EC11: Tax ethics of pensioners are better than students’ tax ethics.

- EC12: Tax ethics of pensioners are better than other people’s tax ethics.

- EC13: The tax ethics of the experienced are better than the tax ethics of the inexperienced.

- EC14: Explicit inclination to tax evasion is higher in experienced people compared to inexperienced people.

3.2.3. Fulfilment of Tax Obligations

- O1: There is a statistical difference of fulfilment of tax obligations with regard to sex.

- O2: There is a statistical difference of fulfilment of tax obligations with regard to age.

- O3: There is a statistical difference of fulfilment of tax obligations with regard to education.

- O4: There is a statistical difference of fulfilment of tax obligations with regard to the main source of income.

- OC1: Women are more likely to be taxed voluntarily than men.

- OC2: The seniors are more likely to be taxed voluntarily than the middle generation group.

- OC3: The seniors are more likely to be taxed voluntarily than the young generation.

- OC4: Secondary-educated people are more likely to be taxed voluntarily than people with elementary education.

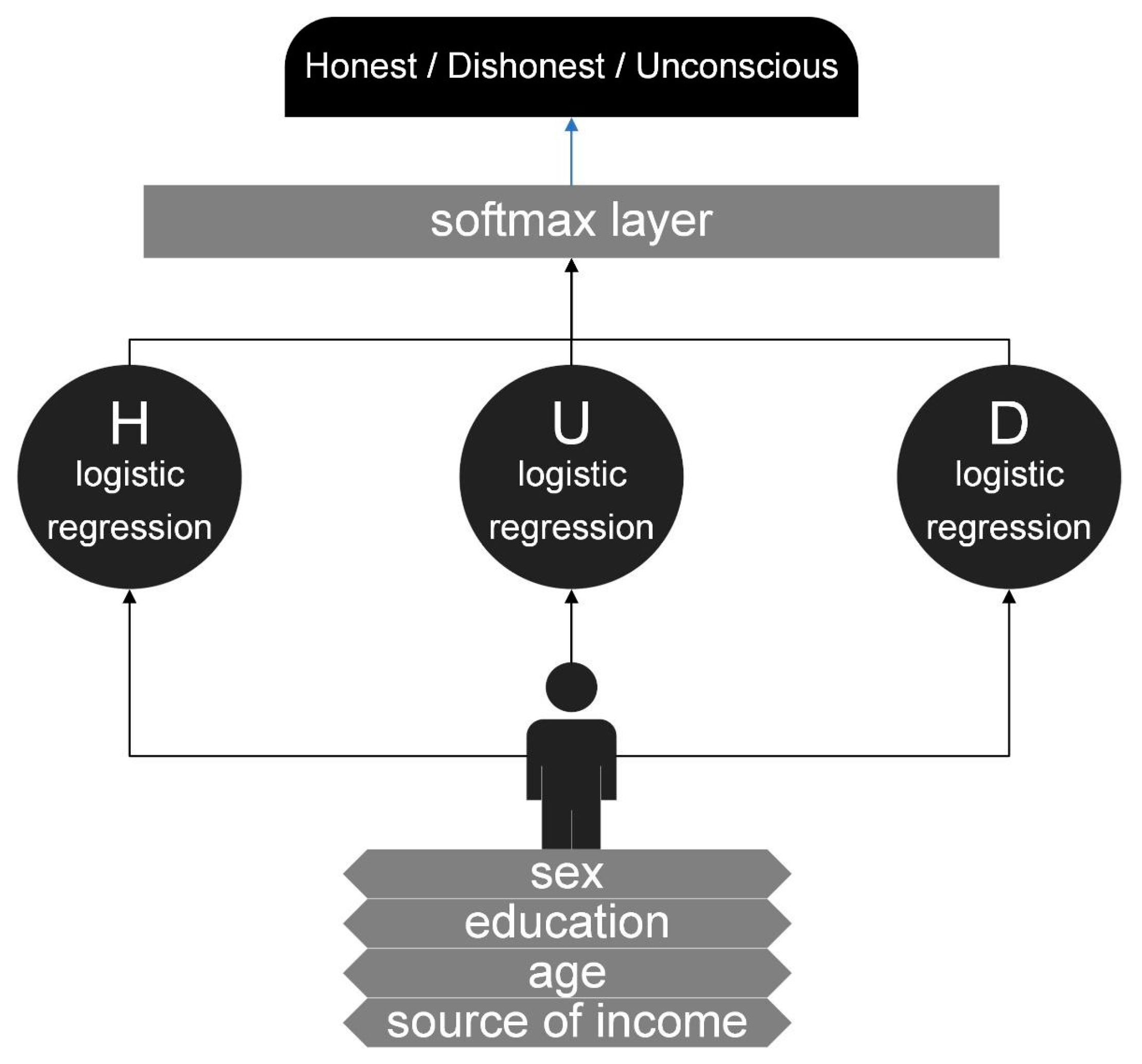

3.3. Logistic Regression Models

3.3.1. Statistical Significance

3.3.2. Backward Regression

4. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- European Commission. The Concept of Tax Gaps Report on VAT Gap Estimations by FISCALIS Tax Gap Project Group (FPG/041). 2016. Available online: https://taxation-customs.ec.europa.eu/system/files/2016-09/tgpg_report_en.pdf (accessed on 1 January 2021).

- Bánociová, A.; Vravec, J. Analysis of efficiency of VAT collection in Slovakia. Ved. Časopis Finanč. Trhy 2015, 4, 1–10. [Google Scholar]

- Bhuiyan, M.Z. Tax evasion and avoidance practices in some selected corporate firms of Bangladesh. World J. Soc. Sci. 2012, 2, 150–156. [Google Scholar]

- Durán-Cabré, J.M.; Moré, A.E.; Mas-Montserrat, M.; Salvadori, L. The tax gap as a public management instrument: Application to wealth taxes. Appl. Econ. Anal. 2019, 27, 207–225. [Google Scholar] [CrossRef]

- Alm, J.; Martinez-Vazquez, J.; McClellan, C. Corruption and firm tax evasion. J. Econ. Behav. Organ. 2016, 124, 146–163. [Google Scholar] [CrossRef]

- Center for Social and Economic Research Study and Reports on the VAT Gap in the EU-28 Member States. Final Report 2019. 2019. Available online: https://ec.europa.eu/taxation_customs/sites/taxation/files/vat-gap-full-report-2019_en.pdf (accessed on 1 January 2021).

- Belmonte, A.; Dell’Anno, R.; Teobaldell, D. Tax morale, aversion to ethnic diversity, and decentralization. Eur. J. Polit. Econ. 2018, 55, 204–223. [Google Scholar] [CrossRef]

- Ciziceno, M.; Pizzuto, P. Life satisfaction and tax morale: The role of trust in government and cultural orientation. J. Behav. Exp. Econ. 2022, 97, 101824. [Google Scholar] [CrossRef]

- Cyan, M.R.; Koumpias, A.M.; Martinez-Vazquez, J. The determinants of tax morale in Pakistan. J. Asian Econ. 2016, 47, 23–34. [Google Scholar] [CrossRef]

- McGee, R.W.; Petrides, Y.; Zhou, J. Attitude toward tax evasion in Brazil, Russia, India and China (BRIC). Philos. Econ. Law Rev. 2022, 2, 70–84. [Google Scholar]

- McGee, W.R. Cheating on taxes: A comparative study of tax evasion ethics of 15 transition economies and 2 developed economies. In Proceedings of the IABPAD Conference Proceedings, Dallas, TX, USA, 24–27 April 2008; pp. 84–98. [Google Scholar]

- Nemore, F.; Morone, A. Public spirit on immigration issues and tax morale in Italy: An empirical investigation. J. Behav. Exp. Econ. 2019, 81, 11–18. [Google Scholar] [CrossRef]

- Luttmer, E.F.P.; Singhal, M. Tax morale. J. Econ. Perspect. 2014, 28, 149–168. [Google Scholar] [CrossRef]

- Torgler, B. Tax morale in Asian countries. J. Asian Econ. 2004, 15, 237–266. [Google Scholar] [CrossRef]

- Dell’Anno, R. Tax evasion, tax morale and policy maker’s effectiveness. J. Socio-Econ. 2009, 38, 988–997. [Google Scholar] [CrossRef]

- Blesse, S. Do your tax problems make tax evasion seem more justifiable? Evidence from a survey experiment. Eur. J. Political Econ. 2023, in press. [Google Scholar] [CrossRef]

- Alm, J.; Torgler, B. Culture differences and tax morale in the United States and in Europe. J. Econ. Psych. 2006, 27, 224–246. [Google Scholar] [CrossRef]

- Rodriguez-Justicia, D.; Theilen, B. Education and tax morale. J. Econ. Psychol. 2018, 64, 18–48. [Google Scholar] [CrossRef]

- Ferrer-i-Carbonell, A.; Gërxhani, K. Tax evasion and well-being: A study of the social and institutional context in Central and Eastern Europe. Eur. J. Political Econ. 2016, 45, 149–159. [Google Scholar] [CrossRef]

- Bilgin, C. Determinants of Tax Morale in Spain and Turkey: An Empirical Analysis. Eur. J. Gov. Econ. 2014, 3, 60–74. [Google Scholar] [CrossRef]

- Goksu, G.G.; Sahpaz, K.I. Comparison of Tax Morale of Turkish and Spanish Higher Education Students: The Samples of Sakarya University and the University of Zaragoza. Procedia Soc. Behav. Sci. 2015, 186, 222–230. [Google Scholar] [CrossRef]

- Torgler, B. The importance of faith: Tax morale and religiosity. J. Econ. Behav. Organ. 2006, 61, 81–109. [Google Scholar] [CrossRef]

- Daude, C.; Melguizo, Á. Taxation and More Representation?: On Fiscal Policy, Social Mobility and Democracy in Latin America. In OECD Development Centre Working Papers; No. 294; OECD Publishing: Paris, France, 2010. [Google Scholar] [CrossRef]

- Sezgin, S.; Yildiz, S.; Ayyildiz, Y. The Ethics of Tax Evasion: A Comparative Study of Turkey and Kyrgyzystan. J. Appl. Bus. Econ. 2011, 12, 75–90. [Google Scholar]

- Torgler, B.; Schneider, F. The Impact of Tax Morale and Institutional Quality on the Shadow Economy. J. Econ. Psychol. 2009, 30, 228–245. [Google Scholar] [CrossRef]

- Bruno, R.L. Tax enforcement, tax compliance and tax morale in transition economies: A theoretical model. Eur. J. Polit. Econ. 2019, 56, 193–211. [Google Scholar] [CrossRef]

- Pappa, E.; Sajedi, R.; Vella, E. Fiscal consolidation with tax evasion and corruption. J. Int. Econ. 2015, 96, 56–75. [Google Scholar] [CrossRef]

- Durisova, M.; Tokarcikova, E.; Virlanuta, F.O.; Chodasova, Z. The Corporate Performance Measurement and Its Importance for the Pricing in a Transport Enterprise. Sustainability 2020, 11, 6164. [Google Scholar] [CrossRef]

- Potkany, M.; Hlatka, M.; Debnar, M.; Hanzl, J. Comparasion of the Lifecycle Cost Structure of Electric and Diesel Buses. Nase More 2018, 65, 270–275. [Google Scholar] [CrossRef]

- Hitka, M.; Lorincova, S.; Vetrakova, M.; Hajduchova, I.; Antalik, I. Factors related to gender and education affecting the employee motivation. Entrep. Sustain. 2020, 7, 3229–3241. [Google Scholar] [CrossRef]

- Makovicky, N.; Smith, R. Tax Beyond Social Contract. Soc. Anal. 2020, 64, 1–17. [Google Scholar] [CrossRef]

- Dou, G.; Cao, K. A joint analysis of environmental and economic performance of closed-loop chains under carbon tax regulation. Comput. Ind. Eng. 2020, 146, 106624. [Google Scholar] [CrossRef]

- Bejakovic, P.; Bezeredi, S. Determination of Tax Morle in Croatia: An Ordered Logit Model. Bus. Syst. Res. J. 2019, 10, 37–48. [Google Scholar] [CrossRef]

- Socoliuc, M.; Grosu, V.; Hlaciuc, E.; Stansiu, S. Analysis of Social Responsibility and Reporting Methods of Romanian Companies in the Countries of the European Union. Sustainability 2018, 10, 4662. [Google Scholar] [CrossRef]

- Van de Vijver, A.; Cassimon, D.; Engelen, P.J. A real Option Approach to Sustainable Corporate Tax Behaviour. Sustainability 2020, 12, 5406. [Google Scholar] [CrossRef]

- Grundmann, S.; Lambsdorff, J.G. How income and tax rates provoke cheating—An experimental investigation of tax morale. J. Econ. Psychol. 2017, 63, 27–42. [Google Scholar] [CrossRef]

- Lago-Peñas, I.; Lago-Peñas, S. The determinants of tax morale in comparative perspective: Evidence from European countries. Eur. J. Political Econ. 2010, 26, 441–453. [Google Scholar] [CrossRef]

- Torgler, B.; Demir, I.C.; Macintyre, A.; Schaffner, M. Causes and Consequences of Tax Morale: An Empirical Investigation. Econ. Anal. Policy 2008, 38, 313–339. [Google Scholar] [CrossRef]

- Kountouris, Y.; Remoundou, K. Is there a cultural component in tax morale? Evidence from immigrants in Europe. J. Econ. Behav. Organ. 2013, 96, 104–119. [Google Scholar] [CrossRef]

- Statistical Office of the Slovak Republic. Official Website of the Statistical Office of the Slovak Republic. 2017. Available online: https://statistics.sk (accessed on 1 January 2021).

- Slovak Business Agency. Analýzy a Prieskumy Podnikateľského Prostredia [Analysis and Surveys of the Enterprise Environment in Slovakia]. 2017. Available online: http://www.sbagency.sk/analyzy-a-prieskumy-podnikatelskeho-prostredia (accessed on 1 January 2021).

- Pearson, K. On the criterion that a given system of deviations from the probable in the case of a correlated system of variables is such that it can be reasonably supposed to have arisen from random sampling. Philos. Mag. 1900, 50, 157–175. [Google Scholar] [CrossRef]

- Fisher, R.A. On the interpretation of χ2 from contingency tables, and the calculation of P. J. R. Stat. Soc. 1922, 85, 87–94. [Google Scholar] [CrossRef]

- Inglehart, R.; Basanez, M.; Diez-Medrano, J.; Halman, L.; Luijkx, R. Human Beliefs and Values: A Cross-Cultural Sourcebook Based on the 1999–2002 Values Surveys; Siglo XXI Editores: Mexico City, Mexico, 2004. [Google Scholar]

- Harju, J.; Kosonen, T.; Slemrod, J. Missing miles: Evasion responses to car taxes. J. Public Econ. 2020, 181, 104108. [Google Scholar] [CrossRef]

- Harris, C.H.; Jenkins, M. Gender Differences in Risk Assessment: Why do Women Take Fewer Risks than Men? Judgm. Decis. Mak. 2006, 1, 48–63. [Google Scholar] [CrossRef]

- Alm, J.; Torgler, B. Estimating the Determinants of Tax Morale. National Tax Association—Tax Institute of America. Proc. Annu. Meet. 2004, 97, 269–274. [Google Scholar]

- McGee, W.R.; Smith, S.R. The Ethics of Tax Evasion: An Empirical Study of Utah Opinion; Andreas School of Business Working Paper; Barry University: Miami Shores, FL, USA, 2006. [Google Scholar]

- McGee, W.R.; Tusan, R. The Ethics of Tax Evasion: A survey of Slovak Opinion; Andreas School of Business Working Paper; Barry University: Miami Shores, FL, USA, 2006. [Google Scholar]

- Torgler, B.; Valev, N.T. Gender and Public Attitudes toward Corruption and Tax Evasion. Contemp. Econ. Policy 2010, 28, 554–568. [Google Scholar] [CrossRef]

- McGee, R.W. The Ethics of Tax Evasion: A Survey of International Business Academics. In Proceedings of the 60th International Atlantic Economic Conference, New York, NY, USA, 6–9 October 2005. [Google Scholar]

- Nasadyuk, I.; McGee, R.W. The ethics of tax evasion: An empirical study of business and economics student opinion in Ukraine. In Taxation and Public Finance in Transition and Developing Economies; Andreas School of Business Working Paper; Barry University: Miami Shores, FL, USA, 2006. [Google Scholar]

- McGee, W.R.; Tyler, M. Tax Evasion and Ethics: A Comparative Study of 33 Countries. Proc. Int. Acad. Bus. Public Adm. Discip. 2007, 4, 709–729. [Google Scholar]

- Hug, S.; Spörri, F. Referendums, trust, and tax evasion. Eur. J. Political Econ. 2011, 27, 120–131. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Kudla, J.; Blaszczak, B.; Kopyt, M. Differences in tax evasion attitudes between students and entrepreneurs under the slippery slope framework. J. Econ. Behav. Organ. 2022, 200, 464–482. [Google Scholar] [CrossRef]

- Eicher, J.D.; Stuhldreher, T.J.; Stuhldreher, W.L. Taxes and Ethics: Taxpayer Attitudes over Time. J. Tax Pract. Proced. 2007, 9, 29–37. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Sex | Education | Employee | Entrepreneur | Unemployed | Retired | Student |

|---|---|---|---|---|---|---|

| Male | Basic | 1.12% | 0.47% | 0.66% | 0.94% | 0.56% |

| Secondary | 21.09% | 7.31% | 2.25% | 6.75% | 0.66% | |

| High | 5.44% | 1.50% | 0.28% | 3.00% | 0.47% | |

| Female | Basic | 1.03% | 0.09% | 0.56% | 1.50% | 0.56% |

| Secondary | 15.00% | 3.00% | 2.06% | 10.22% | 0.94% | |

| High | 6.28% | 0.66% | 0.47% | 4.50% | 0.66% |

| Chi-Square Test | Binomial Test | ||

|---|---|---|---|

| Hypothesis | Statistics (p-Value) | Effect Size (Cramer V) | Statistics (p-Value) |

| H1 | 1365.8 (<0.001) | 0.8000 | 0.7816 (<0.001) |

| H2 | 263.1 (<0.001) | 0.3511 | 0.2212 (<0.001) |

| H3 | 240.52 (<0.001) | 0.4345 | 0.3202 (<0.001) |

| H4 | 583.86 (<0.001) | 0.5231 | 0.4311 (<0.001) |

| Hypothesis | |||||

|---|---|---|---|---|---|

| E1 | E2 | E3 | E4 | E5 | |

| Chi-square statistics | 38.025 | 99.177 | 24.143 | 177.89 | 98.158 |

| p-value | (<0.001) | (<0.001) | (<0.001) | (<0.001) | (<0.001) |

| Effect size (Cramer V) | 0.1335 | 0.1524 | 0.0752 | 0.1667 | 0.2145 |

| Hypothesis | Binomial Test | |

|---|---|---|

| EC1 | probability | 0.2643 |

| p-value | (<0.001) | |

| EC2 | probability | 0.4813 |

| p-value | (<0.001) | |

| EC3 | probability | 0.925 |

| p-value | (<0.001) | |

| EC4 | probability | 0.925 |

| p-value | (<0.001) | |

| EC5 | probability | 0.0576 |

| p-value | (0.7787) | |

| EC6 | probability | 0.6198 |

| p-value | (<0.001) | |

| EC7 | probability | 0.6198 |

| p-value | (<0.001) | |

| EC8 | probability | 0.8849 |

| p-value | (<0.001) | |

| EC9 | probability | 0.9756 |

| p-value | (0.0029) | |

| EC10 | probability | 0.9756 |

| p-value | (0.0029) | |

| EC11 | probability | 0.9756 |

| p-value | (<0.001) | |

| EC12 | probability | 0.6063 |

| p-value | (<0.001) | |

| EC13 | probability | 0.7466 |

| p-value | (0.0014) | |

| EC14 | probability | 0.3836 |

| p-value | (0.0077) | |

| Chi-Square Statistic | Chi-Square p-Value | Effect Size (Cramer V) | Binomial Test |

|---|---|---|---|

| 251.93 | (<0.001) | 0.3444 | 0.2137 (<0.001) |

| O1 (Sex) | O2 (Age) | O3 (Education) | O4 (Income Source) | |

|---|---|---|---|---|

| p-value | (<0.001) | (<0.001) | (0.0134) | (<0.001) |

| OC1 | probability | 0.2465 |

| p-value | (<0.001) | |

| OC2 | probability | 0.3451 |

| p-value | (<0.001) | |

| OC3 | probability | 0.3451 |

| p-value | (<0.001) | |

| OC4 | probability | 0.1519 |

| p-value | (0.0883) |

| H-Logistic Regression | U-Logistic Regression | D-Logistic Regression | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) |

| Constant | −1.0986 *** (0.1155) | −1.3856 *** (0.0964) | −1.6006 *** (0.1672) | −1.5157 *** (0.1267) | −0.04001 (0.10002) | −0.3297 *** (0.0717) | −0.2580 ** (0.0986) | −0.1710 † (0.0977) | −1.0460 *** (0.1140) | −0.6111 *** (0.0759) | −0.5098 *** (0.1004) | −0.5643 *** (0.1013) |

| Male | −0.3524 * (0.1664) | −0.49799 *** (0.13960) | 0.8109 *** (0.1481) | |||||||||

| AgeGroup.L | 1.2138 *** (0.1811) | −0.1405 (0.1337) | −0.7617 *** (0.1424) | |||||||||

| AgeGroup.Q | 0.1987 (0.1516) | −0.2110 (0.1139) | −0.0643 (0.1196) | |||||||||

| Education.L | 1.0721 ** (0.3475) | −0.1141 (0.2005) | −0.4651 * (0.2042) | |||||||||

| Education.Q | −0.3894 (0.2167) | 0.0681 (0.1344) | 0.0767 (0.1372) | |||||||||

| SOI_entrepreneur | −0.5345 † (0.3207) | −0.6431 ** (0.2253) | 0.8827 *** (0.2150) | |||||||||

| SOI_unemployed | −0.4504 (0.4230) | −0.2933 (0.2891) | 0.5292 † (0.2836) | |||||||||

| SOI_pensioner | 1.0771 *** (0.1858) | −0.2125 (0.1669) | 0.8056 ** (0.1937) | |||||||||

| SOI_student | −1.9500 † (1.0221) | 0.7307 † (0.3748) | −0.1289 (0.3829) | |||||||||

| AIC | 894.18 | 837.87 | 887.65 | 844.34 | 1154.7 | 1162.1 | 1169.1 | 1158.3 | 1084.2 | 1084.2 | 1111.8 | 1067.7 |

| Variables | mH-Model | mU-Model | mD-Model |

|---|---|---|---|

| Constant | −1.8165 *** (0.1785) | −1.1304 (0.1517) | −0.7159 *** (0.1784) |

| Male | −0.4890 *** (0.1456) | 0.6449 *** (0.1562) | |

| AgeGroup.L | 1.2620 *** (0.1833) | −0.4152 † (0.2387) | −0.2389 (0.2438) |

| AgeGroup.Q | 0.2353 (0.1528) | −0.4060 ** (0.1547) | 0.2217 (0.1612) |

| Education.L | 1.2147 *** (0.3554) | −0.5092 * (0.2185) | |

| Education.Q | −0.5925 ** (0.2238) | 0.2572 † (0.1493) | |

| SOI_entrepreneur | −0.5398 * (0.2290) | 0.7882 *** (0.2208) | |

| SOI_unemployed | −0.3349 (0.2936) | 0.4696 (0.2951) | |

| SOI_pensioner | 0.3393 (0.3132) | −0.7245 * (0.3359) | |

| SOI_student | 0.8073 * (0.3992) | −0.5394 (0.4193) | |

| AIC (train) | 824.98 | 1142.5 | 1043.5 |

| Accuracy (train) | 0.7403 | 0.5652 | 0.6240 |

| Accuracy (test) | 0.6916 | 0.5327 | 0.6075 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Holkova, B.; Malichova, E.; Falat, L.; Pancikova, L. Determinants of Tax Ethics in Society: Statistical and Logistic Regression Approach. Mathematics 2023, 11, 2341. https://doi.org/10.3390/math11102341

Holkova B, Malichova E, Falat L, Pancikova L. Determinants of Tax Ethics in Society: Statistical and Logistic Regression Approach. Mathematics. 2023; 11(10):2341. https://doi.org/10.3390/math11102341

Chicago/Turabian StyleHolkova, Beata, Eva Malichova, Lukas Falat, and Lucia Pancikova. 2023. "Determinants of Tax Ethics in Society: Statistical and Logistic Regression Approach" Mathematics 11, no. 10: 2341. https://doi.org/10.3390/math11102341