Optimization of Asset and Liability Management of Banks with Minimum Possible Changes

,

,

and

and

Abstract

1. Introduction

2. Literature Review

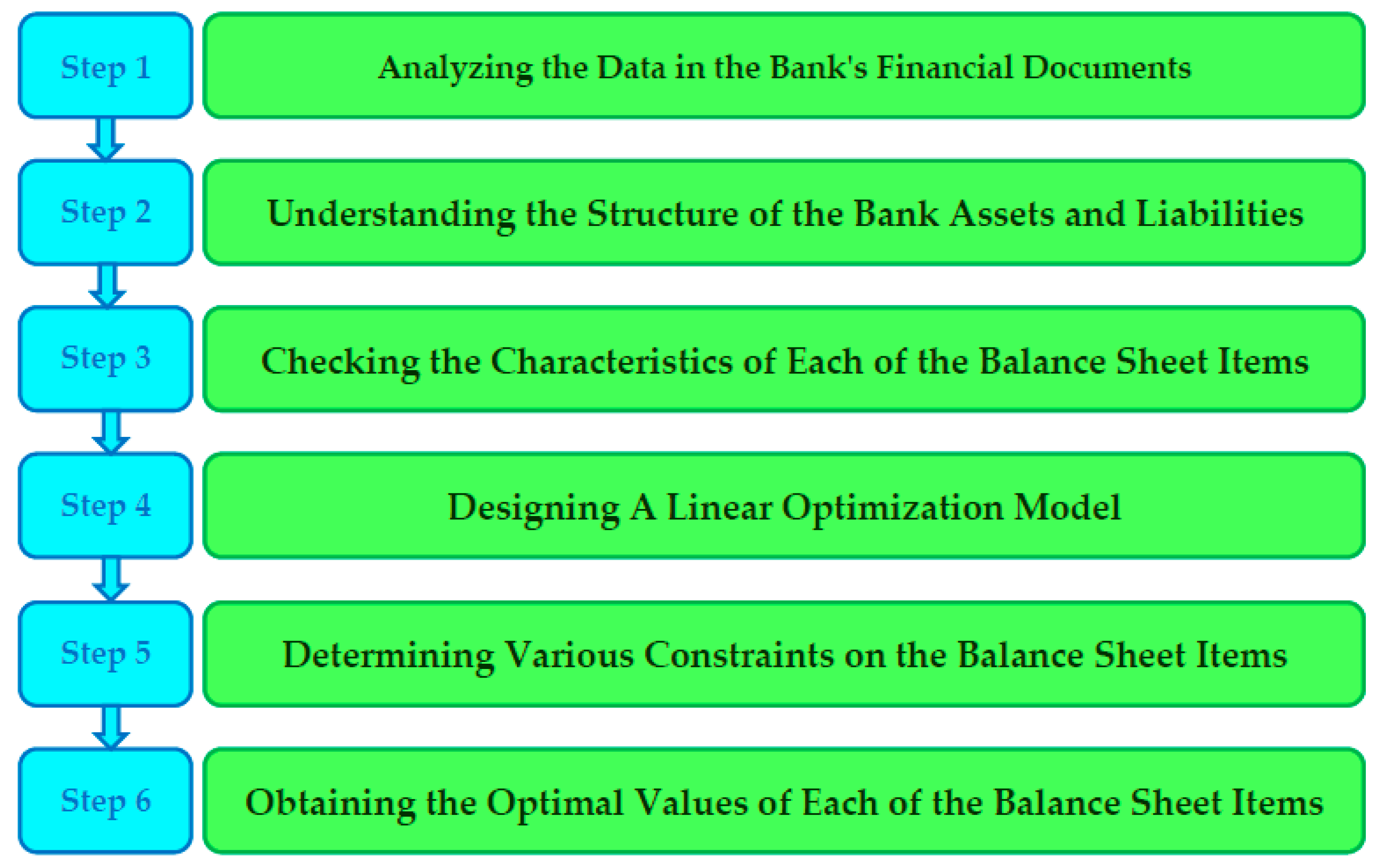

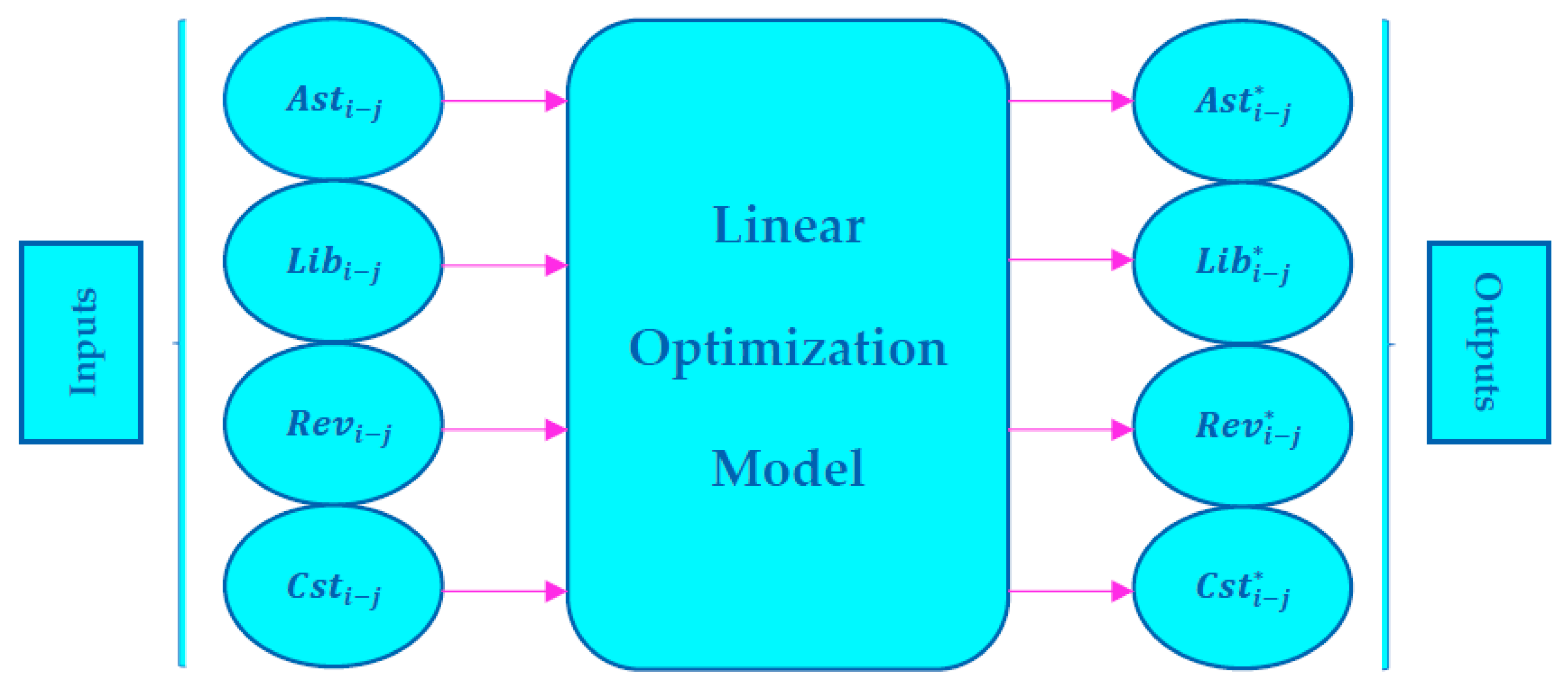

3. Methodology

4. Results

5. Conclusions and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Varma, P.; Nijjer, S.H.; Sood, K.; Grima, S.; Rupeika-Apoga, R. Thematic Analysis of Financial Technology (Fintech) Influence on the Banking Industry. Risks 2022, 10, 186. [Google Scholar] [CrossRef]

- Akgüller, O.; Balcı, M.A.; Batrancea, L.M.; Gaban, L. Path-Based Visibility Graph Kernel and Application for the Borsa Istanbul Stock Network. Mathematics 2023, 11, 1528. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Fetita, A. Empirical Research Study on the Determinants of Market Indicators for 41 Financial Institutions. J. Risk Financ. Manag. 2023, 16, 78. [Google Scholar] [CrossRef]

- Jungo, J.; Madaleno, M.; Botelho, A. The Effect of Financial Inclusion and Competitiveness on Financial Stability: Why Financial Regulation Matters in Developing Countries? J. Risk Financ. Manag. 2022, 15, 122. [Google Scholar] [CrossRef]

- Ngepah, N.; da Silva, M.L.A.; Shaaba Saba, C.H. The Impact of Commodity Price Shocks on Banking System Stability in Developing Countries. Economies 2022, 10, 91. [Google Scholar] [CrossRef]

- Bektas, E.; Elbadri, M.; Molyneux, P.H. Do institutions, religion and the economic cycle impact bank stability in dual banking systems? J. Int. Financ. Manag. Account. 2022, 33, 252–284. [Google Scholar] [CrossRef]

- Alam, N.; Sivarajah, G.; Bhatti, M.I. Do Deposit Insurance Systems Promote Banking Stability? Int. J. Financ. Stud. 2021, 9, 52. [Google Scholar] [CrossRef]

- Teresienė, D.; Keliuotytė-Staniulėnienė, G.; Kanapickienė, R. Sustainable Economic Growth Support through Credit Transmission Channel and Financial Stability: In the Context of the COVID-19 Pandemic. Sustainability 2021, 13, 2692. [Google Scholar] [CrossRef]

- Alam, S.H.; Rabbani, M.R.; Tausif, M.R.; Abey, J. Banks’ Performance and Economic Growth in India: A Panel Cointegration Analysis. Economies 2021, 9, 38. [Google Scholar] [CrossRef]

- Elnahass, M.; Trinh, V.Q.; Li, T. Global banking stability in the shadow of COVID-19 outbreak. J. Int. Financ. Mark. Inst. Money 2021, 72, 101322. [Google Scholar] [CrossRef]

- Guerra, P.; Castelli, M. Machine Learning Applied to Banking Supervision a Literature Review. Risks 2021, 9, 136. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Danisman, G.O.; Demir, E.; Tarazi, A. Economic uncertainty and bank stability: Conventional vs. Islamic banking. J. Financ. Stab. 2021, 56, 100911. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Rathnaswamy, M.K.; Batrancea, I. A Panel Data Analysis on Determinants of Economic Growth in Seven Non-BCBS Countries. J. Knowl. Econ. 2021, 13, 1651–1665. [Google Scholar] [CrossRef]

- Nisar, S.H.; Peng, K.; Wang, S.; Ashraf, B.N. The Impact of Revenue Diversification on Bank Profitability and Stability: Empirical Evidence from South Asian Countries. Int. J. Financ. Stud. 2018, 6, 40. [Google Scholar] [CrossRef]

- Jayakumar, M.; Pradhan, R.; Dash, S.; Maradana, R.; Gaurav, K. Banking competition, banking stability, and economic growth: Are feedback effects at work? J. Econ. Bus. 2018, 96, 15–41. [Google Scholar] [CrossRef]

- Fernández, A.; González, F.; Suárez, N. Banking stability, competition, and economic volatility. J. Financ. Stab. 2016, 22, 101–120. [Google Scholar] [CrossRef]

- Peykani, P.; Sargolzaei, M.; Takaloo, A.; Valizadeh, S. The Effects of Monetary Policy on Macroeconomic Variables through Credit and Balance Sheet Channels: A Dynamic Stochastic General Equilibrium Approach. Sustainability 2023, 15, 4409. [Google Scholar] [CrossRef]

- Batrancea, L.M. Determinants of Economic Growth across the European Union: A Panel Data Analysis on Small and Medium Enterprises. Sustainability 2022, 14, 4797. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Balcı, M.A.; Chermezan, L.; Akgüller, Ö.; Masca, E.S.; Gaban, L. Sources of SMEs Financing and Their Impact on Economic Growth across the European Union: Insights from a Panel Data Study Spanning Sixteen Years. Sustainability 2022, 14, 15318. [Google Scholar] [CrossRef]

- Batrancea, L.M.; Balcı, M.A.; Akgüller, Ö.; Gaban, L. What Drives Economic Growth across European Countries? A Multimodal Approach. Mathematics 2022, 10, 3660. [Google Scholar] [CrossRef]

- Mirzaei, A.; Moore, T.; Liu, G. Does market structure matter on banks’ profitability and stability? J. Bank. Financ. 2013, 37, 2920–2937. [Google Scholar] [CrossRef]

- Ali, M.; Alam, N.; Khattak, M.A.; Azmi, W. Bank Risk-Taking and Legal Origin: What Do We Know About Dual Banking Economies? J. Risk Financ. Manag. 2022, 15, 224. [Google Scholar] [CrossRef]

- Xie, Z.H.; Liu, X.; Najam, H.; Fu, Q.; Abbas, J.; Comite, U.; Cismas, L.M.; Miculescu, A. Achieving Financial Sustainability through Revenue Diversification: A Green Pathway for Financial Institutions in Asia. Sustainability 2022, 14, 3512. [Google Scholar] [CrossRef]

- Miklaszewska, E.; Kil, K.; Idzik, M. How the COVID-19 Pandemic Affects Bank Risks and Returns: Evidence from EU Members in Central, Eastern, and Northern Europe. Risks 2021, 9, 180. [Google Scholar] [CrossRef]

- Nguyen, D.T.; Le, T.D.Q.; Ho, T.H. Intellectual Capital and Bank Risk in Vietnam—A Quantile Regression Approach. J. Risk Financ. Manag. 2021, 14, 27. [Google Scholar] [CrossRef]

- Korzeb, Z.; Niedziółka, P. Determinants of Differentiation of Cost of Risk (CoR) among Polish Banks during COVID-19 Pandemic. J. Risk Financ. Manag. 2021, 14, 110. [Google Scholar] [CrossRef]

- Choudhury, T.; Scagnelli, S.; Yong, J.; Zhang, Z.H. Non-Traditional Systemic Risk Contagion within the Chinese Banking Industry. Sustainability 2021, 13, 7954. [Google Scholar] [CrossRef]

- Ely, R.A.; Tabak, B.M.; Teixeira, A.M. The transmission mechanisms of macroprudential policies on bank risk. Econ. Model. 2021, 94, 598–630. [Google Scholar] [CrossRef]

- Zheng, C.H.; Chen, S.H.; Dong, Z.H. Economic Fluctuation, Local Government Bond Risk and Risk-Taking of City Commercial Banks. Sustainability 2021, 13, 9871. [Google Scholar] [CrossRef]

- Rastogi, S.H.; Gupte, R.; Meenakshi, R. A Holistic Perspective on Bank Performance Using Regulation, Profitability, and Risk-Taking with a View on Ownership Concentration. J. Risk Financ. Manag. 2021, 14, 111. [Google Scholar] [CrossRef]

- Moiseev, N.; Sorokin, A.; Zvezdina, N.; Mikhaylov, A.; Khomyakova, L.; Shah Danish, M.S. Credit Risk Theoretical Model on the Base of DCC-GARCH in Time-Varying Parameters Framework. Mathematics 2021, 9, 2423. [Google Scholar] [CrossRef]

- Doko, F.; Kalajdziski, S.; Mishkovski, I. Credit Risk Model Based on Central Bank Credit Registry Data. J. Risk Financ. Manag. 2021, 14, 138. [Google Scholar] [CrossRef]

- Botshekan, M.H.; Takaloo, A.; Soureh, R.; Abdollahi Poor, M.S. Global Economic Policy Uncertainty and Non-Performing Loans in Iranian Banks: Dynamic Correlation using the DCC-GARCH Approach. J. Money Econ. 2021, 16, 187–212. [Google Scholar]

- Yeo, E.; Jun, J. Peer-to-Peer Lending and Bank Risks: A Closer Look. Sustainability 2020, 12, 6107. [Google Scholar] [CrossRef]

- Martínez-Malvar, M.; Baselga-Pascual, L. Bank Risk Determinants in Latin America. Risks 2020, 8, 94. [Google Scholar] [CrossRef]

- Harkin, S.M.; Mare, D.S.; Crook, J.N. Independence in bank governance structure: Empirical evidence of effects on bank risk and performance. Res. Int. Bus. Financ. 2020, 52, 101177. [Google Scholar] [CrossRef]

- Rahman, M.M.; Begum, M.; Ashraf, B.N.; Masud, A.K. Does Trade Openness Affect Bank Risk-Taking Behavior? Evidence from BRICS Countries. Economies 2020, 8, 75. [Google Scholar] [CrossRef]

- Bai, H.; Ba, S.H.; Huang, W.; Hu, W. Expected government support and bank risk-taking: Evidence from China. Financ. Res. Lett. 2020, 36, 101328. [Google Scholar] [CrossRef]

- Feridun, M.; Güngör, H. Climate-Related Prudential Risks in the Banking Sector: A Review of the Emerging Regulatory and Supervisory Practices. Sustainability 2020, 12, 5325. [Google Scholar] [CrossRef]

- Andries, A.M.; Galasan, E. Measuring Financial Contagion and Spillover Effects with a State-Dependent Sensitivity Value-at-Risk Model. Risks 2020, 8, 5. [Google Scholar] [CrossRef]

- Wu, J.; Yao, Y.; Chen, M.; Nam Jeon, B. Economic uncertainty and bank risk: Evidence from emerging economies. J. Int. Financ. Mark. Inst. Money 2020, 68, 101242. [Google Scholar] [CrossRef]

- Zabala Aguayo, F.; Ślusarczyk, B. Risks of Banking Services’ Digitalization: The Practice of Diversification and Sustainable Development Goals. Sustainability 2020, 12, 4040. [Google Scholar] [CrossRef]

- Tran, S.H.; Nguyen, L. Financial Development, Business Cycle and Bank Risk in Southeast Asian Countries. J. Asian Financ. Econ. Bus. 2020, 7, 127–135. [Google Scholar] [CrossRef]

- Nicola, G.; Cerchiello, P.; Aste, T. Information Network Modeling for U.S. Banking Systemic Risk. Entropy 2020, 22, 1331. [Google Scholar] [CrossRef]

- Nguyen, K.H.N. Revenue Diversification, Risk and Bank Performance of Vietnamese Commercial Banks. J. Risk Financ. Manag. 2019, 12, 138. [Google Scholar] [CrossRef]

- Elamer, A.A.; Ntim, C.G.; Abdou, H.A. The Impact of Multi-Layer Governance on Bank Risk Disclosure in Emerging Markets: The Case of Middle East and North Africa. In Accounting Forum; Routledge: Abingdon-on-Thames, UK, 2019; Volume 43, pp. 246–281. [Google Scholar] [CrossRef]

- Galletta, S.; Mazzù, S. Liquidity Risk Drivers and Bank Business Models. Risks 2019, 7, 89. [Google Scholar] [CrossRef]

- Munkhdalai, L.; Munkhdalai, T.; Namsrai, O.E.; Lee, J.Y.; Ryu, K.H. An Empirical Comparison of Machine-Learning Methods on Bank Client Credit Assessments. Sustainability 2019, 11, 699. [Google Scholar] [CrossRef]

- Leo, M.; Sharma, S.; Maddulety, K. Machine Learning in Banking Risk Management: A Literature Review. Risks 2019, 7, 29. [Google Scholar] [CrossRef]

- Siddika, A.; Haron, R. Capital regulation and ownership structure on bank risk. J. Financ. Regul. Compliance 2019, 28, 39–56. [Google Scholar] [CrossRef]

- Angori, G.H.; Aristei, D.; Gallo, M. Determinants of Banks’ Net Interest Margin: Evidence from the Euro Area during the Crisis and Post-Crisis Period. Sustainability 2019, 11, 3785. [Google Scholar] [CrossRef]

- Dan Dang, V. Should Vietnamese Banks Need More Equity? Evidence on Risk-Return Trade-Off in Dynamic Models of Banking. J. Risk Financ. Manag. 2019, 12, 84. [Google Scholar] [CrossRef]

- Chen, S.; Nazir, M.I.; Hashmi, S.H.; Shaikh, R. Bank Competition, Foreign Bank Entry, and Risk-Taking Behavior: Cross Country Evidence. J. Risk Financ. Manag. 2019, 12, 106. [Google Scholar] [CrossRef]

- Al Rahahleh, N.; Bhatti, M.I.; Misman, F.N. Developments in Risk Management in Islamic Finance: A Review. J. Risk Financ. Manag. 2019, 12, 37. [Google Scholar] [CrossRef]

- Jumreornvong, S.; Chakreyavanich, C.H.; Treepongkaruna, S.; Jiraporn, P. Capital Adequacy, Deposit Insurance, and the Effect of Their Interaction on Bank Risk. J. Risk Financ. Manag. 2018, 11, 79. [Google Scholar] [CrossRef]

- Zhang, X.; Li, F.; Li, Z.H.; Xu, Y. Macroprudential Policy, Credit Cycle, and Bank Risk-Taking. Sustainability 2018, 10, 3620. [Google Scholar] [CrossRef]

- Yüksel, S.; Mukhtarov, S.H.; Mammadov, E.; Özsarı, M. Determinants of Profitability in the Banking Sector: An Analysis of Post-Soviet Countries. Economies 2018, 6, 41. [Google Scholar] [CrossRef]

- Cui, Y.; Geobey, S.; Weber, O.; Lin, H. The Impact of Green Lending on Credit Risk in China. Sustainability 2018, 10, 2008. [Google Scholar] [CrossRef]

- Ashraf, B.N.; Arshad, S.; Yan, L. Trade Openness and Bank Risk-Taking Behavior: Evidence from Emerging Economies. J. Risk Financ. Manag. 2017, 10, 15. [Google Scholar] [CrossRef]

- Giordana, G.A.; Schumacher, I. An Empirical Study on the Impact of Basel III Standards on Banks’ Default Risk: The Case of Luxembourg. J. Risk Financ. Manag. 2017, 10, 8. [Google Scholar] [CrossRef]

- Ashraf, B.N.; Arshad, S.; Hu, Y. Capital Regulation and Bank Risk-Taking Behavior: Evidence from Pakistan. Int. J. Financ. Stud. 2016, 4, 16. [Google Scholar] [CrossRef]

- Härle, P.H.; Havas, A.; Samandari, H. The Future of Bank Risk Management; McKinsey Company: New York, NY, USA, 2016. [Google Scholar]

- Pakhchanyan, S. Operational Risk Management in Financial Institutions: A Literature Review. Int. J. Financ. Stud. 2016, 4, 20. [Google Scholar] [CrossRef]

- Gavalas, D.; Syriopoulos, T.H. Bank Credit Risk Management and Rating Migration Analysis on the Business Cycle. Int. J. Financ. Stud. 2014, 2, 122–143. [Google Scholar] [CrossRef]

- Li, J.; Liang, C.H.; Zhu, X.; Sun, X.; Wu, D. Risk Contagion in Chinese Banking Industry: A Transfer Entropy-Based Analysis. Entropy 2013, 15, 5549–5564. [Google Scholar] [CrossRef]

- Manganelli, S.; Altunbas, Y.; Marqués-Ibáñez, D. Bank Risk during the Financial Crisis: Do Business Models Matter? Working Paper Series 1394; European Central Bank: Frankfurt, Germany, 2011. [Google Scholar] [CrossRef]

- Inanoglu, H.; Jacobs, M. Models for Risk Aggregation and Sensitivity Analysis: An Application to Bank Economic Capital. J. Risk Financ. Manag. 2009, 2, 118–189. [Google Scholar] [CrossRef]

- Lysiak, L.; Masiuk, I.; Chynchyk, A.; Yudina, O.; Olshanskiy, O.; Shevchenko, V. Banking Risks in the Asset and Liability Management System. J. Risk Financ. Manag. 2022, 15, 265. [Google Scholar] [CrossRef]

- Li, X.; Lu, T.; Lin, J.H. Bank Interest Margin and Green Lending Policy under Sunflower Management. Sustainability 2022, 14, 8643. [Google Scholar] [CrossRef]

- Chen, S.H.; Huang, F.W.; Lin, J.H. Borrowing-Firm Emission Trading, Bank Rate-Setting Behavior, and Carbon-Linked Lending under Capital Regulation. Sustainability 2022, 14, 6633. [Google Scholar] [CrossRef]

- Jiang, B.; Tzavellas, H.; Yang, X. Deposit Competition, Interbank Market, and Bank Profit. J. Risk Financ. Manag. 2022, 15, 194. [Google Scholar] [CrossRef]

- Batrancea, L.M. An Econometric Approach on Performance, Assets, and Liabilities in a Sample of Banks from Europe, Israel, United States of America, and Canada. Mathematics 2021, 9, 3178. [Google Scholar] [CrossRef]

- Simões, C.; Oliveira, L.; Bravo, J.M. Immunization Strategies for Funding Multiple Inflation-Linked Retirement Income Benefits. Risks 2021, 9, 60. [Google Scholar] [CrossRef]

- Orlando, G.; Bace, E. Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA). Adm. Sci. 2021, 11, 62. [Google Scholar] [CrossRef]

- Bayliss, C.H.; Serra, M.; Nieto, A.; Juan, A.A. Combining a Matheuristic with Simulation for Risk Management of Stochastic Assets and Liabilities. Risks 2020, 8, 131. [Google Scholar] [CrossRef]

- Bidabad, B.; Allahyarifard, M. Assets and Liabilities Management in Islamic Banking. Int. J. Islam. Bank. Financ. Res. 2019, 3, 32–43. [Google Scholar] [CrossRef]

- Dutta, G.; Rao, H.V.; Basu, S.; Tiwari, M.K. Asset liability management model with decision support system for life insurance companies: Computational results. Comput. Ind. Eng. 2019, 128, 985–998. [Google Scholar] [CrossRef]

- Sgambati, S. The art of leverage: A study of bank power, money-making and debt finance. Rev. Int. Political Econ. 2019, 26, 287–312. [Google Scholar] [CrossRef]

- Erwin, K.; Abubakar, E.; Muda, I. The relationship of lending, funding, capital, human resource, asset liability management to non-financial sustainability of rural banks (BPRs) in Indonesia. J. Appl. Econ. Sci. 2018, 13, 520–542. [Google Scholar]

- Boateng, K. Credit Risk Management and Performance of Banks in Ghana: The ‘Camels’ Rating Model Approach. Int. J. Bus. Manag. Invent. 2018, 8, 41–48. [Google Scholar]

- Anagnostopoulos, T.H.; Skouloudis, A.; Han, N.; Evangelinos, K. Incorporating Sustainability Considerations into Lending Decisions and the Management of Bad Loans: Evidence from Greece. Sustainability 2018, 10, 4728. [Google Scholar] [CrossRef]

- Riet, A.V. The ECB’s Fight against Low Inflation: On the Effects of Ultra-Low Interest Rates. Int. J. Financ. Stud. 2017, 5, 12. [Google Scholar] [CrossRef]

- Badeeb, R.A.; Lean, H.H. Natural Resources and Productivity: Can Banking Development Mitigate the Curse? Economies 2017, 5, 11. [Google Scholar] [CrossRef]

- Anderson-Parson, J.A.; Keasler, T.R.; Byerly, R.T. Bond Indenture Consent Solicitations as a Debt Management Tool. Int. J. Financ. Stud. 2015, 3, 230–243. [Google Scholar] [CrossRef]

- Dragoe, S.; Oprean-Stan, C. A New International Monetary System on the Horizon? Econ. Comput. Econ. Cybern. Stud. Res. 2018, 52, 89–105. [Google Scholar] [CrossRef]

- Bucur, A.; Dobrotă, G.; Oprean-Stan, G.; Tănăsescu, C. Economic and Qualitative Determinants of the World Steel Production. Metals 2017, 7, 163. [Google Scholar] [CrossRef]

- Dsouza, S.; Rabbani, M.R.; Hawaldar, I.T.; Jain, A.K. Impact of Bank Efficiency on the Profitability of the Banks in India: An Empirical Analysis Using Panel Data Approach. Int. J. Financ. Stud. 2022, 10, 93. [Google Scholar] [CrossRef]

- Neves, M.E.D.; Gouveia, M.D.C.; Proenca, C.A.N. European Bank’s Performance and Efficiency. J. Risk Financ. Manag. 2020, 13, 67. [Google Scholar] [CrossRef]

- Dewasurendra, S.; Judice, P.; Zhu, Q. The Optimum Leverage Level of the Banking Sector. Risks 2019, 7, 51. [Google Scholar] [CrossRef]

- Barmuta, K.; Ponkratov, V.; Maramygin, M.; Kuznetsov, N.; Ivlev, V.; Ivleva, M. Mathematical Model of Optimizing the Balance Sheet Structure of the Russian Banking System with Allowance for The Foreign Exchange Risk Levels. Entrep. Sustain. Issues 2019, 7, 1. [Google Scholar] [CrossRef]

- Almaqtari, F.A.; Al-Homaidi, E.A.; Tabash, M.I.; Farhan, N.H. The determinants of profitability of Indian commercial banks: A panel data approach. Int. J. Financ. Econ. 2019, 24, 168–185. [Google Scholar] [CrossRef]

- Barik, D.N.; Chakrabarty, S.P. Does Limited Liability Reduce Leveraged Risk? The Case of Loan Portfolio Management. J. Risk Financ. Manag. 2022, 15, 519. [Google Scholar] [CrossRef]

- Murtza, I.; Saadia, A.; Basri, R.; Imran, A.; Almuhaimeed, A.; Alzahrani, A. Forex Investment Optimization Using Instantaneous Stochastic Gradient Ascent—Formulation of an Adaptive Machine Learning Approach. Sustainability 2022, 14, 15328. [Google Scholar] [CrossRef]

- Tran, K.L.; Le, H.A.; Nguyen, T.H.H.; Nguyen, D.T. Explainable Machine Learning for Financial Distress Prediction: Evidence from Vietnam. Data 2022, 7, 160. [Google Scholar] [CrossRef]

- Yang, C.H.; Shen, W. Non-Financial Enterprises’ Shadow Banking Business and Total Factor Productivity of Enterprises. Sustainability 2022, 14, 8150. [Google Scholar] [CrossRef]

- Reis, P.M.N.; Pinto, A.P.S. How Do Banking Characteristics Influence Companies’ Debt Features and Performance during COVID-19? A Study of Portuguese Firms. Int. J. Financ. Stud. 2022, 10, 98. [Google Scholar] [CrossRef]

- Munir, W.; Gallagher, K.P. Scaling Up for Sustainable Development: Benefits and Costs of Expanding and Optimizing Balance Sheet in the Multilateral Development Banks. J. Int. Dev. 2020, 32, 222–243. [Google Scholar] [CrossRef]

- Montesi, G.; Papiro, G.; Fazzini, M.; Ronga, A. Stochastic Optimization System for Bank Reverse Stress Testing. J. Risk Financ. Manag. 2020, 13, 174. [Google Scholar] [CrossRef]

- De Haan, J.; Fang, Y.; Jing, Z.H. Does the risk on banks’ balance sheets predict banking crises? New evidence for developing countries. Int. Rev. Econ. Financ. 2020, 68, 254–268. [Google Scholar] [CrossRef]

- Gorskiy, M.A.; Reshulskaya, E.M. Parametric models for optimizing the credit and investment activity of a commercial bank. J. Appl. Econ. Sci. 2018, 13, 105–113. [Google Scholar]

- Liu, H.; Huang, W. Sustainable Financing and Financial Risk Management of Financial Institutions—Case Study on Chinese Banks. Sustainability 2022, 14, 9786. [Google Scholar] [CrossRef]

- El-Chaarani, H.; Abraham, R. The Impact of Corporate Governance and Political Connectedness on the Financial Performance of Lebanese Banks during the Financial Crisis of 2019–2021. J. Risk Financ. Manag. 2022, 15, 203. [Google Scholar] [CrossRef]

- Van den Heuvel, S. The Welfare Effects of Bank Liquidity and Capital Requirements. In Finance and Economics Discussion Series 2022; No. 2022-72; Federal Reserve System: Washington, DC, USA, 2022. [Google Scholar]

- Xiong, L.; Fang, J. An Economic Evaluation of Targeted Reserve Requirement Ratio Reduction on Bank Ecosystem Development. Systems 2022, 10, 66. [Google Scholar] [CrossRef]

- Katusiime, L. COVID 19 and Bank Profitability in Low Income Countries: The Case of Uganda. J. Risk Financ. Manag. 2021, 14, 588. [Google Scholar] [CrossRef]

- Pham, H.L.; Daly, K.J. The Impact of BASEL Accords on the Management of Vietnamese Commercial Banks. J. Risk Financ. Manag. 2020, 13, 228. [Google Scholar] [CrossRef]

- Rahman, H.; Yousaf, M.W.; Tabassum, N. Bank-Specific and Macroeconomic Determinants of Profitability: A Revisit of Pakistani Banking Sector under Dynamic Panel Data Approach. Int. J. Financ. Stud. 2020, 8, 42. [Google Scholar] [CrossRef]

- Abbas, F.; Iqbal, S.H.; Aziz, B. The Role of Bank Liquidity and Bank Risk in Determining Bank Capital: Empirical Analysis of Asian Banking Industry. Rev. Pac. Basin Financ. Mark. Policies 2020, 23, 2050020. [Google Scholar] [CrossRef]

- Igan, D.; Mirzaei, A. Does going tough on banks make the going get tough? Bank liquidity regulations, capital requirements, and sectoral activity. J. Econ. Behav. Organ. 2020, 177, 688–726. [Google Scholar] [CrossRef]

- Huang, K.; Yao, Q.; Li, C.H. Impacts of Financial Market Shock on Bank Asset Allocation from the Perspective of Financial Characteristics of Banks. Int. J. Financ. Stud. 2019, 7, 29. [Google Scholar] [CrossRef]

- Gemar, P.; Gemar, G.; Guzman-Parra, V. Modeling the Sustainability of Bank Profitability Using Partial Least Squares. Sustainability 2019, 11, 4950. [Google Scholar] [CrossRef]

- Atta Mills, E.; Yu, B.; Zeng, K. Satisfying Bank Capital Requirements: A Robustness Approach in a Modified Roy Safety-First Framework. Mathematics 2019, 7, 593. [Google Scholar] [CrossRef]

- Oguzsoy, C.B.; Guven, S. Bank asset and liability management under uncertainty. Eur. J. Oper. Res. 1997, 102, 575–600. [Google Scholar] [CrossRef]

- Kosmidou, K.; Zopounidis, C. An Optimization Scenario Methodology for Bank Asset Liability Management. Oper. Res. Int. J. 2002, 2, 279–287. [Google Scholar] [CrossRef]

- Papi, M.; Sbaraglia, S. Optimal Asset–Liability Management with Constraints: A Dynamic Programming Approach. Appl. Math. Comput. 2006, 173, 306–349. [Google Scholar] [CrossRef]

- Yan, W.Y. A class of continuous-time portfolio selection with liability under jump-diffusion processes. Int. J. Control 2009, 82, 2277–2283. [Google Scholar] [CrossRef]

- Chiu, M.C.; Li, D. Asset-Liability Management under the Safety-First Principle. J. Optim. Theory Appl. 2009, 143, 455–478. [Google Scholar] [CrossRef]

- Ferstl, R.; Weissensteiner, A. Asset-Liability Management under Time-Varying Investment Opportunities. J. Bank. Financ. 2011, 35, 182–192. [Google Scholar] [CrossRef]

- Yang, W.; Xu, X.; Cai, Y. Segmented Dynamic Optimization Model for Asset-Liability Management of Commercial Banks and Its Applications. J. Shanghai Jiaotong Univ. (Sci.) 2012, 17, 114–120. [Google Scholar] [CrossRef]

- Halaj, G. Dynamic Balance Sheet Model with Liquidity Risk. Int. J. Theor. Appl. Financ. 2016, 19, 1650052. [Google Scholar] [CrossRef]

- Pan, J.; Xiao, Q. Optimal Dynamic Asset-Liability Management with Stochastic Interest Rates and Inflation Risks. Chaos Solitons Fractals 2017, 103, 460–469. [Google Scholar] [CrossRef]

- Cui, X.; Li, X.; Wu, X.; Yi, L. A mean-field formulation for multi-period asset–liability mean–variance portfolio selection with an uncertain exit time. J. Oper. Res. Soc. 2017, 69, 487–499. [Google Scholar] [CrossRef]

- Ahmadian, A.; Shahchera, M. Effect of Asset and Liability Management on Liquidity Risk of Iranian Banks. J. Money Econ. 2018, 13, 107–123. [Google Scholar]

- Oliveira, A.D.; Filomena, T.P.; Righi, M.B. Performance Comparison of Scenario-Generation Methods Applied to a Stochastic Optimization Asset and Liability Management Model. Pesqui. Oper. 2018, 38, 53–72. [Google Scholar] [CrossRef]

- Pan, J.; Hu, S.H.; Zhou, X. Optimal investment strategy for asset-liability management under the Heston model. Optimization 2019, 68, 895–920. [Google Scholar] [CrossRef]

- Li, X.; Wu, X.; Yao, H. Multi-Period Asset-Liability Management with Cash Flows and Probability Constraints: A Mean-Field Formulation Approach. J. Oper. Res. Soc. 2019, 71, 1563–1580. [Google Scholar] [CrossRef]

- Abdollahi, H. Multi-Objective Programming for Asset-Liability Management: The Case of Iranian Banking Industry. Int. J. Ind. Eng. Prod. Res. 2020, 31, 75–85. [Google Scholar] [CrossRef]

- Chunxiang, A.; Shen, Y.; Zeng, Y. Dynamic Asset-Liability Management Problem in a Continuous-Time Model with Delay. Int. J. Control 2020, 95, 1315–1336. [Google Scholar] [CrossRef]

- Min, L.; Dong, J.; Liu, J.; Gong, X. Robust mean-risk portfolio optimization using machine learning-based trade-off parameter. Appl. Soft Comput. 2021, 113, 107948. [Google Scholar] [CrossRef]

- Alshehri, D.A.; Tayachi, T. Assets-Liability Management: A Comparative Study of National Commercial Bank and National Bank of Kuwait. PJAEE 2021, 18, 383–391. [Google Scholar]

- Owusu, F.B.; Alhassan, A.L. Asset-Liability Management and bank profitability: Statistical cost accounting analysis from an emerging market. Int. J. Financ. Econ. 2021, 26, 1488–1502. [Google Scholar] [CrossRef]

- Braiek, S.; Bedoui, R.; Belkacem, L. Islamic portfolio optimization under systemic risk: Vine Copula-CoVaR based model. Int. J. Financ. Econ. 2022, 27, 1321–1339. [Google Scholar] [CrossRef]

- Li, B.; Zhang, R.; Sun, Y. Multi-period portfolio selection based on uncertainty theory with bankruptcy control and liquidity. Automatica 2023, 147, 110751. [Google Scholar] [CrossRef]

- De Andrés, J.; Angla, J.; Cámara, X.; Molina, M.C.; Sardà, S. Asset liability management in bank portfolios with fuzzy linear programming. Fuzzy Econ. Rev. 2003, 8, 55. [Google Scholar] [CrossRef]

- Escudero, L.F.; Garín, A.; Merino, M.; Pérez, G. On multistage stochastic integer programming for incorporating logical constraints in asset and liability management under uncertainty. Comput. Manag. Sci. 2009, 6, 307–327. [Google Scholar] [CrossRef]

- Gülpinar, N.; Pachamanova, D. A robust optimization approach to asset-liability management under time-varying investment opportunities. J. Bank. Financ. 2013, 37, 2031–2041. [Google Scholar] [CrossRef]

- Gülpınar, N.; Pachamanova, D.; Çanakoğlu, E. A robust asset—liability management framework for investment products with guarantees. OR Spectr. 2016, 38, 1007–1041. [Google Scholar] [CrossRef][Green Version]

- Jain, M.K.; Dalela, A.K.; Tiwari, S.K. Application of Fuzzy Mathematical Model in Assets-Liabilities. Int. J. Trade Econ. Financ. 2010, 1, 247. [Google Scholar] [CrossRef]

- Pachamanova, D.; Gülpınar, N.; Çanakoğlu, E. Robust approaches to pension fund asset liability management under uncertainty. In Optimal Financial Decision Making under Uncertainty; Springer: Berlin/Heidelberg, Germany, 2017; pp. 89–119. [Google Scholar]

- Yang, X.; Liu, W.; Zhao, X.; Zhang, Y. Multi-period Fuzzy Asset-liability Portfolio Optimization Model with Bankruptcy Control. Oper. Res. Manag. Sci. 2021, 30, 147. [Google Scholar]

- Zenios, S.A. Asset/liability management under uncertainty for fixed-income securities. Ann. Oper. Res. 1995, 59, 77–97. [Google Scholar] [CrossRef]

- Zopounidis, C.; Pardalos, P.M.; Baourakis, G. Fuzzy Sets in Management, Economics, and Marketing; World Scientific: Singapore, 2001. [Google Scholar]

- Arabjazi, N.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F.; Behzadi, M.H. Stability analysis with general fuzzy measure: An application to social security organizations. PLoS ONE 2022, 17, e0275594. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Pishvaee, M.S.; Rostamy-Malkhalifeh, M.; Jabbarzadeh, A. A novel fuzzy data envelopment analysis based on robust possibilistic programming: Possibility, necessity and credibility-based approaches. RAIRO-Oper. Res. 2018, 52, 1445–1463. [Google Scholar] [CrossRef]

- Peykani, P.; Gheidar-Kheljani, J. Performance appraisal of research and development projects value-chain for complex products and systems: The fuzzy three-stage DEA approach. J. New Res. Math. 2020, 6, 41–58. [Google Scholar]

- Peykani, P.; Seyed Esmaeili, F.S. Malmquist productivity index under fuzzy environment. Fuzzy Optim. Model. J. 2021, 2, 10–19. [Google Scholar]

- Bhaskar, T.; Sundararajan, R.; Krishnan, P.G. A fuzzy mathematical programming approach for cross-sell optimization in retail banking. J. Oper. Res. Soc. 2009, 60, 717–727. [Google Scholar] [CrossRef]

- Emrouznejad, A.; Tavana, M. Performance Measurement with Fuzzy Data Envelopment Analysis; Springer: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Peykani, P.; Mohammadi, E.; Emrouznejad, A.; Pishvaee, M.S.; Rostamy-Malkhalifeh, M. Fuzzy data envelopment analysis: An adjustable approach. Expert. Syst. Appl. 2019, 136, 439–452. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Emrouznejad, A. An adjustable fuzzy chance-constrained network DEA approach with application to ranking investment firms. Expert. Syst. Appl. 2021, 166, 113938. [Google Scholar] [CrossRef]

- Peykani, P.; Namakshenas, M.; Arabjazi, N.; Shirazi, F.; Kavand, N. Optimistic and pessimistic fuzzy data envelopment analysis: Empirical evidence from Tehran stock market. Fuzzy Optim. Model. J. 2021, 2, 12–21. [Google Scholar]

- Guo, P.; Tanaka, H. Fuzzy DEA: A perceptual evaluation method. Fuzzy Sets Syst. 2001, 119, 149–160. [Google Scholar] [CrossRef]

- Kaur, R.; Puri, J. A novel dynamic data envelopment analysis approach with parabolic fuzzy data: Case study in the Indian banking sector. RAIRO-Oper. Res. 2022, 56, 2853–2880. [Google Scholar] [CrossRef]

- Khalili-Damghani, K.; Tavana, M.; Santos-Arteaga, F.J. A comprehensive fuzzy DEA model for emerging market assessment and selection decisions. Appl. Soft Comput. 2016, 38, 676–702. [Google Scholar] [CrossRef]

- Peykani, P.; Hosseinzadeh Lotfi, F.; Sadjadi, S.J.; Ebrahimnejad, A.; Mohammadi, E. Fuzzy chance-constrained data envelopment analysis: A structured literature review, current trends, and future directions. Fuzzy Optim. Decis. Mak. 2022, 21, 197–261. [Google Scholar] [CrossRef]

- Peykani, P.; Memar-Masjed, E.; Arabjazi, N.; Mirmozaffari, M. Dynamic performance assessment of hospitals by applying credibility-based fuzzy window data envelopment analysis. Healthcare 2022, 10, 876. [Google Scholar] [CrossRef]

- Puri, J.; Yadav, S.P. A fuzzy DEA model with undesirable fuzzy outputs and its application to the banking sector in India. Expert. Syst. Appl. 2014, 41, 6419–6432. [Google Scholar] [CrossRef]

- Puri, J.; Yadav, S.P. A fully fuzzy DEA approach for cost and revenue efficiency measurements in the presence of undesirable outputs and its application to the banking sector in India. Int. J. Fuzzy Syst. 2016, 18, 212–226. [Google Scholar] [CrossRef]

- Singh, A.P.; Yadav, S.P.; Singh, S.K. A multi-objective optimization approach for DEA models in a fuzzy environment. Soft Comput. 2022, 26, 2901–2912. [Google Scholar] [CrossRef]

- Wanke, P.; Barros, C.P.; Emrouznejad, A. Assessing productive efficiency of banks using integrated Fuzzy-DEA and bootstrapping: A case of Mozambican banks. Eur. J. Oper. Res. 2016, 249, 378–389. [Google Scholar] [CrossRef]

- Peykani, P.; Namazi, M.; Mohammadi, E. Bridging the knowledge gap between technology and business: An innovation strategy perspective. PLoS ONE 2022, 17, e0266843. [Google Scholar] [CrossRef]

- Peykani, P.; Namakshenas, M.; Nouri, M.; Kavand, N.; Rostamy-Malkhalifeh, M. A possibilistic programming approach to portfolio optimization problem under fuzzy data. In Advances in Econometrics, Operational Research, Data Science and Actuarial Studies; Springer International Publishing: Cham, Switzerland, 2022; pp. 377–387. [Google Scholar]

- Wanke, P.; Barros, C.P.; Emrouznejad, A. A comparison between stochastic DEA and fuzzy DEA approaches: Revisiting efficiency in Angolan banks. RAIRO-Oper. Res. 2018, 52, 285–303. [Google Scholar] [CrossRef]

- Wen, M.; Li, H. Fuzzy data envelopment analysis (DEA): Model and ranking method. J. Comput. Appl. Math. 2009, 223, 872–878. [Google Scholar] [CrossRef]

- Aghayi, N.; Raayatpanah, M.A. A robust optimization approach to overall profit efficiency with data uncertainty: Application on bank industry. J. Chin. Inst. Eng. 2019, 42, 160–168. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E. Portfolio selection problem under uncertainty: A robust optimization approach. In Proceedings of the 3th International Conference on Intelligent Decision Science, Tehran, Iran, 9 May 2018. [Google Scholar]

- Bertsimas, D.; Gupta, V.; Kallus, N. Data-driven robust optimization. Math. Program. 2018, 167, 235–292. [Google Scholar] [CrossRef]

- Dehnokhalaji, A.; Khezri, S.; Emrouznejad, A. A box-uncertainty in DEA: A robust performance measurement framework. Expert. Syst. Appl. 2022, 187, 115855. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Farzipoor Saen, R.; Sadjadi, S.J.; Rostamy-Malkhalifeh, M. Data envelopment analysis and robust optimization: A review. Expert. Syst. 2020, 37, e12534. [Google Scholar] [CrossRef]

- Gabrel, V.; Murat, C.; Thiele, A. Recent advances in robust optimization: An overview. Eur. J. Oper. Res. 2014, 235, 471–483. [Google Scholar] [CrossRef]

- Lázaro, J.L.; Jiménez, Á.B.; Takeda, A. Improving cash logistics in bank branches by coupling machine learning and robust optimization. Expert. Syst. Appl. 2018, 92, 236–255. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Jabbarzadeh, A.; Rostamy-Malkhalifeh, M.; Pishvaee, M.S. A novel two-phase robust portfolio selection and optimization approach under uncertainty: A case study of Tehran stock exchange. PLoS ONE 2020, 15, e0239810. [Google Scholar] [CrossRef]

- Omrani, H.; Shamsi, M.; Emrouznejad, A.; Teplova, T. A robust DEA model under discrete scenarios for assessing bank branches. Expert. Syst. Appl. 2023, 219, 119694. [Google Scholar] [CrossRef]

- Qu, S.; Feng, C.; Jiang, S.; Wei, J.; Xu, Y. Data-Driven Robust DEA Models for Measuring Operational Efficiency of Endowment Insurance System of Different Provinces in China. Sustainability 2022, 14, 9954. [Google Scholar] [CrossRef]

- Peykani, P.; Emrouznejad, A.; Mohammadi, E.; Gheidar-Kheljani, J. A novel robust network data envelopment analysis approach for performance assessment of mutual funds under uncertainty. Ann. Oper. Res. 2022, 1–27. [Google Scholar] [CrossRef]

- Quaranta, A.G.; Zaffaroni, A. Robust optimization of conditional value at risk and portfolio selection. J. Bank. Financ. 2008, 32, 2046–2056. [Google Scholar] [CrossRef]

- Seyed Esmaeili, F.S.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F. A hybrid approach using data envelopment analysis, interval programming and robust optimisation for performance assessment of hotels under uncertainty. Int. J. Manag. Decis. Mak. 2021, 20, 308–322. [Google Scholar]

- Peykani, P.; Gheidar-Kheljani, J.; Farzipoor Saen, R.; Mohammadi, E. Generalized robust window data envelopment analysis approach for dynamic performance measurement under uncertain panel data. Oper. Res. Int. J. 2022, 22, 5529–5567. [Google Scholar] [CrossRef]

- Toloo, M.; Mensah, E.K.; Salahi, M. Robust optimization and its duality in data envelopment analysis. Omega 2022, 108, 102583. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, Y.; Bi, M.; Lai, J.; Chen, Y. A Robust Optimization Method for Location Selection of Parcel Lockers under Uncertain Demands. Mathematics 2022, 10, 4289. [Google Scholar] [CrossRef]

- Zhang, Z.; Jing, H.; Kao, C. High-Dimensional Distributionally Robust Mean-Variance Efficient Portfolio Selection. Mathematics 2023, 11, 1272. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Description | ||

|---|---|---|---|

| Assets | |||

| Cash | |||

| Receivables from banks and other credit institutions | Central Bank—Past Currency Liabilities | ||

| Central Bank—Overnight withdrawals from accounts | |||

| Central Bank of Shaparak Transactions | |||

| Central Bank—Government Deposits | |||

| Facilities Granted to Other Banks and Credit Institutions (Overnight Interbank) | |||

| Other | |||

| Claims from the Government | |||

| Facilities Granted and Claims from the Public Sector | |||

| Facilities Granted and Claims from the Non-Governmental Sector | Current Facilities of the Non-Governmental Sector | ||

| Non-Current Facilities of the Non-Governmental Sector | |||

| Investing in stocks and other securities | Stocks | ||

| Other Non-Government Securities | |||

| Other Government Securities | |||

| Claims on Subsidiaries and Affiliates | |||

| Other Accounts Receivable | |||

| Tangible Fixed Assets | |||

| Intangible Assets | |||

| Legal Deposit | Savings Deposits | ||

| Free Zone Branch Deposits | |||

| Other | |||

| Other Assets | Customer Liability for Long-term Letters of Credit | ||

| Proprietary Documents | |||

| Assets Ready for Sale | |||

| Other | |||

| Customer Liabilities for Letters of Credit | |||

| Customer Obligations for Guarantees | |||

| Other Obligations | |||

| Managed Funds and Similar Items | |||

| Total Assets | |||

| Liabilities | |||

| Total Liability Before Equity | Liability to Banks and Other Credit Institutions | ||

| Customer Deposits | |||

| Dividends Payout | |||

| Performance Tax Reserve | |||

| Reserves and Other Liabilities | |||

| Allocation of Rial Sector Resources to Foreign Exchange Sector | |||

| Provision for Staff Termination Benefits | |||

| Investment Deposits Equity | Long-term Investment Deposits | ||

| Short-term Investment Deposits | |||

| Special Short-term Investment Deposits | |||

| Investment Deposits Received from Banks | |||

| Interest Payable on Short-term Deposits | |||

| Interest Payable on Long-term Deposits | |||

| Equity | Capital | ||

| Legal Reserve | |||

| Other Reserves | |||

| Foreign Exchange Differences | |||

| Retained Earnings | |||

| Asset Revaluation Surplus | |||

| Bank Liabilities for Letters of Credit | |||

| Bank Obligations for Guarantees | |||

| Other Obligations | |||

| Managed Funds and Similar Items | |||

| Total Liabilities | |||

| Revenues | |||

| Operating Income | Granted Facilities Income | ||

| Deposit Income and Bonds | |||

| Fee Income | |||

| Net Investment Profit and Loss | |||

| Net Foreign Exchange Profit and Loss | |||

| Other Operating Income | |||

| Non-Operating Income | Net Other Income and Expenses | ||

| Costs | |||

| Operational Cost | Deposit Interest Cost | ||

| Fee Cost | |||

| Non-Operating Costs | Administrative and General Expenses | ||

| Cost of Bad Debts | |||

| Financial Expenses | |||

| Depreciation Cost | |||

| Tax Cost | |||

| Other Costs | |||

| Assets | Liabilities | ||||

|---|---|---|---|---|---|

| Asset Variables | Optimal Values | Actual Values | Liability Variables | Optimal Values | Actual Values |

| 214,521,652 | 310,229,372 | 9,825,662,400 | 3,624,873,156 | ||

| 1,277,251,120 | 474,827,460 | 1,523,196,200 | 130,097,592 | ||

| 159,046,252 | 0 | 0 | 0 | ||

| 11,163,266 | 10,148,424 | 0 | 16,723,760 | ||

| 281,701 | 256,092 | 0 | 78,127,308 | ||

| 17,065,673 | 15,514,248 | 0 | 25,412,684 | ||

| 671,967,000 | 447,978,000 | 0 | 9,767,496 | ||

| 417,727,240 | 930,696 | 1,523,196,200 | 66,344 | ||

| 638,046,720 | 638,046,712 | 4,826,737,200 | 3,146,697,924 | ||

| 6,403,239,200 | 23,338,672 | 0 | 1,918,006,484 | ||

| 5,544,497,200 | 4,531,427,724 | 1,097,930,800 | 588,519,528 | ||

| 5,156,382,400 | 4,334,705,352 | 98,715,844 | 61,378,536 | ||

| 388,114,816 | 196,722,372 | 244,550,368 | 9,069,424 | ||

| 317,767,000 | 256,771,028 | 3,385,540,160 | 569,723,952 | ||

| 0 | 88,013,264 | 146,056 | 146,056 | ||

| 172,728,608 | 7,603,992 | 93,996,416 | 93,996,416 | ||

| 145,038,396 | 161,153,772 | 3,381,586,360 | 107,123,372 | ||

| 203,070,304 | 111,670,728 | 0 | −1,995,141,349 | ||

| 194,836,108 | 165,794,888 | 0 | 146,811,796 | ||

| 982,591,440 | 755,839,560 | 5,899,345,600 | 5,310,967,584 | ||

| 87,738,076 | 67,490,828 | 2,711,129,440 | 2,490,780,188 | ||

| 1,108,973,240 | 1,008,837,668 | 2,702,175,480 | 2,784,167,288 | ||

| 0 | 996,610,412 | 150 | −51,368,756 | ||

| 0 | 12,227,256 | 119,109,664 | 21,281,912 | ||

| 1,108,973,240 | 0 | 18,695,200 | 17,504,168 | ||

| 241,701,736 | −12,596,952 | 348,235,468 | 48,602,784 | ||

| 0 | 33,468,860 | 1,489,226,400 | 1,390,978,289 | ||

| 0 | 51,881,480 | 200,000,000 | 200,000,000 | ||

| 0 | 12,538,896 | 277,311,904 | 157,311,904 | ||

| 241,701,736 | −110,486,188 | 320,351,400 | 320,351,400 | ||

| 1,393,507,880 | 208,838,912 | 0 | 0 | ||

| 1,452,764,480 | 756,409,460 | 691,563,120 | 85,143,533 | ||

| 1,485,988,280 | 759,366,252 | 0 | 628,171,452 | ||

| 1,318,836,720 | 8,492,500 | 1,393,507,880 | 208,838,912 | ||

| 17,214,234,000 | 8,331,677,688 | 1,452,764,480 | 756,409,460 | ||

| 1,485,988,280 | 759,366,252 | ||||

| 1,318,836,720 | 8,492,500 | ||||

| Revenues | Costs | ||||

|---|---|---|---|---|---|

| Revenue Variables | Optimal Values | Actual Values | Cost Variables | Optimal Values | Actual Values |

| 2,076,628,360 | 1,616,378,376 | 1,476,628,360 | 1,515,936,972 | ||

| 1,967,804,360 | 1,532,667,608 | 668,823,120 | 675,106,200 | ||

| 792,082,520 | 805,051,156 | 615,069,600 | 619,853,088 | ||

| 1,002,935,520 | 197,988,452 | 53,753,496 | 55,253,112 | ||

| 83,625,080 | 76,022,800 | 807,805,240 | 840,830,772 | ||

| 13,744,786 | 13,365,456 | 342,885,944 | 352,451,792 | ||

| 62,215,456 | 427,038,752 | 212,653,944 | 279,727,912 | ||

| 13,200,992 | 13,200,992 | 18,201,837 | 22,752,296 | ||

| 108,824,000 | 83,710,768 | 14,261,920 | 10,970,708 | ||

| 108,824,000 | 83,710,768 | 219,801,596 | 174,928,064 | ||

| 0 | 0 | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Peykani, P.; Sargolzaei, M.; Botshekan, M.H.; Oprean-Stan, C.; Takaloo, A. Optimization of Asset and Liability Management of Banks with Minimum Possible Changes. Mathematics 2023, 11, 2761. https://doi.org/10.3390/math11122761

Peykani P, Sargolzaei M, Botshekan MH, Oprean-Stan C, Takaloo A. Optimization of Asset and Liability Management of Banks with Minimum Possible Changes. Mathematics. 2023; 11(12):2761. https://doi.org/10.3390/math11122761

Chicago/Turabian StylePeykani, Pejman, Mostafa Sargolzaei, Mohammad Hashem Botshekan, Camelia Oprean-Stan, and Amir Takaloo. 2023. "Optimization of Asset and Liability Management of Banks with Minimum Possible Changes" Mathematics 11, no. 12: 2761. https://doi.org/10.3390/math11122761

APA StylePeykani, P., Sargolzaei, M., Botshekan, M. H., Oprean-Stan, C., & Takaloo, A. (2023). Optimization of Asset and Liability Management of Banks with Minimum Possible Changes. Mathematics, 11(12), 2761. https://doi.org/10.3390/math11122761