Efficient Monte Carlo Methods for Multidimensional Modeling of Slot Machines Jackpot

Abstract

:1. Introduction

1.1. General Framework

1.2. Bet Collection

1.3. Jackpot Winning

2. Algorithms and Methods

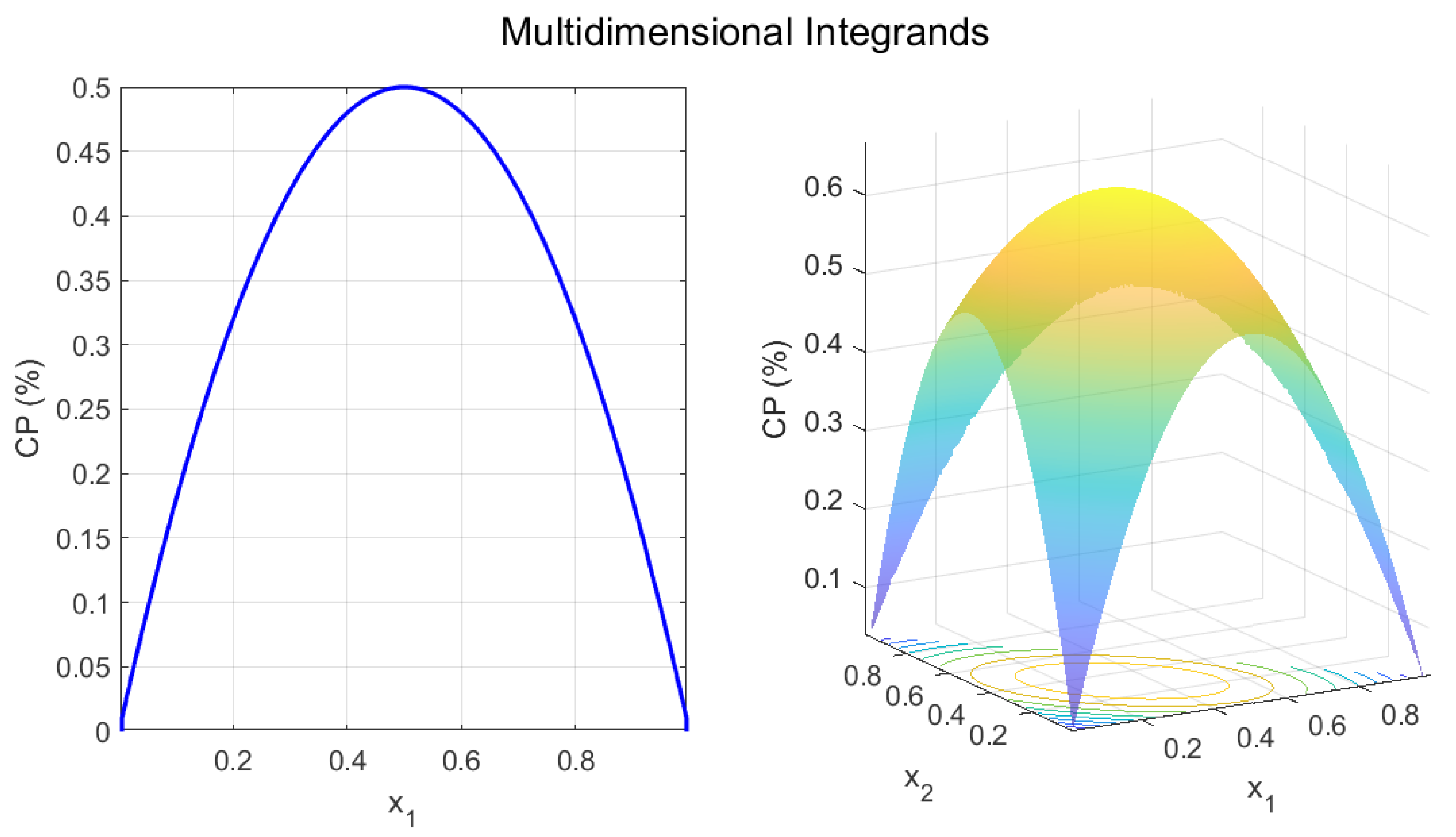

2.1. Integral Representation

- For :

- For :

- For :

- For :

2.2. Algorithm for Drawing Point for (4)

2.3. Algorithm for Drawing Point for (6)

2.4. Monte Carlo Algorithms

3. Results and Discussion

4. A Real Case Study

5. Conclusions

- Disclaimer: This paper must not be understood as advice to play slot games or not to do so. Its aim is to propose an algorithm for practical and applied scientific purposes.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| RTP | Return-To-Player |

| CP | Consolation prize |

| LHS | Latin hypercube sampling |

| SS | Stratified sampling |

| (Q)MC | (Quasi-) Monte Carlo |

| (F)CBC | (Fast) component-by-component |

| CI | Confidence interval(s) |

References

- Fitch, R.A.; Mueller, J.M.; Ruiz, R.; Rousse, W. Recreation matters: Estimating millennials’ preferences for native American cultural tourism. Sustainability 2022, 14, 11513. [Google Scholar] [CrossRef]

- Cooper, M. Sit and spin; How slot machines give gamblers the business. The Atlantic. 2005. Available online: https://www.theatlantic.com/magazine/archive/2005/12/sit-and-spin/304392/ (accessed on 28 December 2022).

- Kamanas, P.-A.; Sifaleras, A.; Samaras, N. Slot machine RTP optimization using variable neighborhood search. Math. Probl. Eng. 2021, 2021, 8784065. [Google Scholar] [CrossRef]

- Turner, N.; Horbay, R. How do slot machines and other electronic gamblingmachines actually work? J. Gambl. Issues 2004, 11, 11. [Google Scholar]

- Oses, N. Markov chain applications in the slot machine industry. Insight 2008, 21, 9–21. [Google Scholar] [CrossRef]

- Bărboianu, C. The Mathematics of Slots: Configurations, Combinations, Probabilities; INFAROM Publishing: Craiova, Romania, 2013. [Google Scholar]

- Epstein, R.A. The Theory of Gambling and Statistical Logic, 2nd ed.; Academic Press: Oxford, UK, 2012. [Google Scholar]

- Balabanov, T. Estimation of volatility based on the estimation of segmentation. Probl. Eng. Cybern. Robot. 2021, 77, 3–10. [Google Scholar]

- Balabanov, T. Volatility index estimation by reverse engineering. Proc. Int. Sci. Conf. UniTech 2021, 1, 229–234. [Google Scholar]

- Keremedchiev, D.; Tomov, P.; Barova, M. Slot machine base game evolutionary RTP optimization. In Proceedings of the International Conference on Numerical Analysis and Its Applications, Lozenetz, Bulgaria, 15–22 June 2016; Dimov, I., Faragó, I., Vulkov, L., Eds.; Springer: Cham, Switzerland, 2017; Volume 10187, pp. 406–413. [Google Scholar]

- Balabanov, T.; Zankinski, I.; Shumanov, B. Slot machine RTP optimization and symbols wins equalization with discrete differential evolution. In Large-Scale Scientific Computing (LSSC 2015); Lirkov, I., Margenov, S.D., Waśniewski, J., Eds.; Springer: Berlin, Germany, 2015; Volume 9374, pp. 210–217. [Google Scholar]

- Balabanov, T.; Zankinski, I.; Shumanov, B. Slot machines RTP optimization with genetic algorithms. In Numerical Methods and Applications (NMA 2014); Dimov, I., Fidanova, S., Lirkov, I., Eds.; Springer: Berlin, Germany, 2015; Volume 8962, pp. 55–61. [Google Scholar]

- Metropolis, N.; Ulam, S. The Monte Carlo Method. J. Amer. Stat. Assoc. 1949, 44, 335–341. [Google Scholar] [CrossRef]

- Dimov, I.T. Monte Carlo Methods For Applied Scientists; World Scientific: Singapore, 2007. [Google Scholar]

- Sobol, I.M. Monte Carlo Numerical Methods; Nauka: Moscow, Russia, 1973. (In Russian) [Google Scholar]

- Kalos, M.A.; Whitlock, P.A. Monte Carlo Methods, Volume 1: Basics; Wiley: New York, NY, USA, 1986. [Google Scholar]

- Paskov, S.H. Computing High Dimensional Integrals with Applications to Finance; Technical Report CUCS-023-94; Columbia University: New York, NY, USA, 1994. [Google Scholar]

- Barr, G.D.I.; Durbach, I.N. A Monte Carlo analysis of hypothetical multi-line slot machine play. Int. Gambl. Stud. 2008, 8, 265–280. [Google Scholar] [CrossRef]

- Tomov, P.; Zankinski, I.; Balabanov, T. Slot machine reels reconstruction with Monte-Carlo search. Proc. Int. Sci. Conf. UniTech 2017, 2, 384–387. [Google Scholar]

- McKay, M.D.; Beckman, R.J.; Conover, W.J. A comparison of three methods for selecting values of input variables in the analysis of output from a computer code. Technometrics 1979, 21, 239–245. [Google Scholar]

- Eglajs, V.; Audze, P. New approach to the design of multifactor experiments. Probl. Dyn. Strengths 1977, 35, 104–107. (In Russian) [Google Scholar]

- Minasny, B.; McBratney, B. A conditioned Latin hypercube method for sampling in the presence of ancillary information. J. Comput. Geosci. Arch. 2006, 32, 1378–1388. [Google Scholar] [CrossRef]

- Minasny, B.; McBratney, B. Conditioned Latin Hypercube Sampling for Calibrating Soil Sensor Data to Soil Properties. In Proximal Soil Sensing; Progress in Soil Science; Springer: Dordrecht, The Netherlands, 2010; pp. 111–119. [Google Scholar]

- Karaivanova, A.; Dimov, I.; Ivanovska, S. A quasi-monte carlo method for integration with improved convergence. In Large-Scale Scientific Computing (LSSC 2001); Lirkov, I., Margenov, S.D., Waśniewski, J., Eds.; Springer: Berlin, Germany, 2001; Volume 2179, pp. 158–165. [Google Scholar]

- Sobol, I.M. Distribution of points in a cube and approximate evaluation of integrals. USSR Comput. Math. Math. Phys. 1967, 7, 86–112. [Google Scholar] [CrossRef]

- Niederreiter, H. Existence of good lattice points in the sense of Hlawka. Monat. Math. 1978, 86, 203–219. [Google Scholar] [CrossRef]

- Niederreiter, H. Random Number Generation and Quasi-Monte Carlo Methods; CBMS-NSF Regional Conference Series in Applied Mathematics 63; SIAM: Philadelphia, PA, USA, 1992. [Google Scholar]

- van der Corput, J. Verteilungsfunktionen I & II. Nederl. Akad. Wetensch. Proc. 1935, 38, 813–820 & 1058–1066. [Google Scholar]

- Halton, J. On the efficiency of certain quasi-random sequences of points in evaluating multi-dimensional integrals. Numer. Math. 1960, 2, 84–90. [Google Scholar] [CrossRef]

- Halton, J.; Smith, G.B. Algorithm 247: Radical-inverse quasi-random point sequence. Commun. ACM 1964, 7, 701–702. [Google Scholar] [CrossRef]

- Antonov, I.; Saleev, V. An economic method of computing LPτ-sequences. USSR Comput. Math. Math. Phys. 1979, 19, 252–256. [Google Scholar] [CrossRef]

- Bratley, P.; Fox, B. Algorithm 659: Implementing Sobol’s Quasirandom Sequence Generator. ACM Trans. Math. Softw. 1988, 14, 88–100. [Google Scholar] [CrossRef]

- Fox, B. Algorithm 647: Implementation and relative effciency of quasirandom sequence generators. ACM Trans. Math. Softw. 1986, 12, 362–376. [Google Scholar] [CrossRef]

- Joe, S.; Kuo, F. Remark on Algorithm 659: Implementing Sobol’s quasirandom sequence generator. ACM Trans. Math. Softw. 2003, 29, 49–57. [Google Scholar] [CrossRef]

- Kocis, L.; Whiten, W.J. Computational investigations of low-discrepancy sequences. ACM Trans. Math. Softw. 1997, 23, 266–294. [Google Scholar] [CrossRef]

- Matousek, J. On the L2-discrepancy for anchored boxes. J. Complex. 1998, 14, 527–556. [Google Scholar] [CrossRef] [Green Version]

- Sloan, I.H.; Kachoyan, P.J. Lattice methods for multiple integration: Theory, error analysis and examples. SIAM J. Numer. Anal. 1987, 24, 116–128. [Google Scholar] [CrossRef]

- Niederreiter, H. Monte Carlo and Quasi-Monte Carlo Methods; Springer: Berlin/Heidelberg, Germany, 2002. [Google Scholar]

- Hua, L.K.; Wang, Y. Applications of Number Theory to Numerical Analysis; Springer: Beijing, China, 1981. [Google Scholar]

- Wang, Y.; Hickernell, F.J. An historical overview of lattice point sets. In Monte Carlo and Quasi-Monte Carlo Methods; Fang, K.-T., Hickernell, F.J., Niederreiter, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2002; pp. 158–167. [Google Scholar]

- Sloan, I.H.; Joe, S. Lattice Methods for Multiple Integration; Oxford University Press: Oxford, UK, 1994. [Google Scholar]

- Kuo, F.Y.; Nuyens, D. Application of quasi-Monte Carlo methods to elliptic PDEs with random diffusion coefficients—A survey of analysis and implementation. Found. Comput. Math. 2016, 16, 1631–1696. [Google Scholar] [CrossRef] [Green Version]

- Nuyens, D.; Cools, R. Fast algorithms for component-by-component construction of rank-1 lattice rules in shift-invariant reproducing kernel Hilbert spaces. Math. Comp. 2006, 75, 903–920. [Google Scholar] [CrossRef] [Green Version]

- Nuyens, D.; Cools, R. Fast component-by-component construction of rank-1 lattice rules with a non-prime number of points. J. Complex. 2006, 22, 4–28. [Google Scholar] [CrossRef]

- Sloan, I.H.; Reztsov, A.V. Component-by-component construction of good lattice rules. Math. Comp. 2002, 71, 263–273. [Google Scholar] [CrossRef] [Green Version]

- Niederreiter, H. Finite fields, pseudorandom numbers, and quasirandom points. In Finite Fields, Coding Theory, and Advances in Communications and Computing; Mullen, G.L., Shiue, P.J.-S., Eds.; Marcel Dekker: New York, NY, USA, 1993; pp. 375–394. [Google Scholar]

- Lemieux, C.; L’ Ecuyer, P. Randomized polynomial lattice rules for multivariate integration and simulation. SIAM J. Sci. Comput. 2003, 24, 1768–1789. [Google Scholar] [CrossRef] [Green Version]

- Lidl, R.; Niederreiter, H. Introduction to Finite Fields and Their Applications, 1st ed.; Cambridge University Press: Cambridge, UK, 1994. [Google Scholar]

- Dick, J.; Pillichshammer, F. Digital Nets and Sequences: Discrepancy Theory and Quasi–Monte Carlo Integration; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Goda, T. Good interlaced polynomial lattice rules for numerical integration in weighted Walsh spaces. J. Comput. Appl. Math. 2015, 285, 279–294. [Google Scholar] [CrossRef]

- Baldeaux, J.; Dick, J.; Greslehner, J.; Pillichshammer, F. Construction algorithms for higher order polynomial lattice rules. J. Complex. 2011, 27, 281–299. [Google Scholar] [CrossRef] [Green Version]

- Baldeaux, J.; Dick, J.; Leobacher, G.; Nuyens, D.; Pillichshammer, F. Efficient calculation of the worst-case error and (fast) component-by-component construction of higher order polynomial lattice rules. Numer. Algor. 2012, 59, 403–431. [Google Scholar] [CrossRef] [Green Version]

- Dick, J.; Pillichshammer, F. Strong tractability of multivariate integration of arbitrary high order using digitally shifted polynomial lattice rules. J. Complex. 2007, 23, 436–453. [Google Scholar] [CrossRef] [Green Version]

- Dick, J.; Kuo, F.Y.; Sloan, I.H. High dimensional integration: The quasi-Monte Carlo way. Acta Numer. 2013, 22, 133288. [Google Scholar] [CrossRef]

- Joe, S.; Kuo, F.Y. Constructing Sobol’ sequences with better two-dimensional projections. SIAM J. Sci. Comput. 2008, 30, 2635–2654. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 1.6125e-04 | 5.9472e-03 | 1.2844e-04 | 7.2665e-04 | 1.0475e-03 | 5.9037e-04 | 1.0728e-03 | |

| 1.9346e-04 | 1.8509e-03 | 1.8755e-04 | 4.0143e-06 | 5.2541e-04 | 6.6748e-04 | 8.3025e-04 | |

| 3.4622e-05 | 5.8246e-04 | 2.4591e-04 | 1.5847e-05 | 9.0208e-04 | 1.0248e-04 | 4.4663e-04 | |

| 2.7674e-04 | 1.9345e-04 | 2.9789e-04 | 8.5159e-05 | 1.8386e-04 | 8.4683e-05 | 2.8420e-05 | |

| 7.8357e-05 | 2.0888e-06 | 2.3893e-04 | 2.6495e-05 | 2.7664e-04 | 1.5048e-05 | 1.3011e-04 | |

| 6.8036e-05 | 6.2652e-06 | 6.4250e-05 | 5.9894e-05 | 4.2919e-05 | 7.1324e-06 | 8.6867e-05 | |

| 6.7842e-05 | 5.6128e-06 | 2.7236e-05 | 2.0672e-05 | 4.6293e-05 | 4.2045e-05 | 4.2164e-05 | |

| 3.4242e-05 | 2.2065e-05 | 6.4611e-06 | 2.7191e-06 | 3.2974e-05 | 3.7721e-06 | 2.9521e-05 | |

| 1.3859e-05 | 1.4018e-05 | 4.3472e-06 | 5.2437e-06 | 3.4679e-05 | 5.4494e-06 | 1.9901e-06 | |

| 1.0718e-05 | 6.3245e-06 | 1.2579e-06 | 4.8620e-06 | 4.3226e-05 | 2.5429e-06 | 9.4656e-06 | |

| 3.5234e-05 | 2.6706e-06 | 2.8323e-06 | 3.3937e-06 | 8.7798e-06 | 5.1221e-06 | 8.2347e-06 | |

| 1.0182e-05 | 1.6646e-06 | 1.9961e-06 | 5.3631e-06 | 1.6481e-05 | 1.8632e-06 | 5.9903e-07 | |

| 2.2655e-05 | 3.2259e-07 | 1.6827e-06 | 2.4378e-06 | 2.4166e-06 | 4.2597e-07 | 7.2949e-07 | |

| 1.7509e-05 | 3.3866e-07 | 1.1103e-06 | 2.1528e-06 | 2.1024e-05 | 1.3517e-06 | 8.3793e-07 | |

| 1.6180e-05 | 1.3048e-07 | 2.9587e-07 | 6.1431e-07 | 9.9364e-06 | 2.1059e-07 | 3.7635e-07 | |

| 2.1837e-06 | 1.4345e-07 | 4.7869e-08 | 6.7600e-08 | 4.8745e-06 | 1.2202e-07 | 3.5241e-07 | |

| 9.3048e-07 | 8.9044e-08 | 1.9305e-07 | 2.4566e-08 | 8.1265e-07 | 2.4635e-07 | 1.3593e-07 | |

| 1.9097e-06 | 1.5722e-07 | 1.6952e-07 | 7.3093e-08 | 3.6900e-06 | 1.9022e-07 | 7.1400e-08 | |

| 3.1659e-06 | 2.5281e-07 | 2.0586e-07 | 1.3335e-07 | 4.5442e-06 | 1.3973e-07 | 8.8798e-08 | |

| 1.7997e-06 | 2.5890e-07 | 9.7798e-08 | 1.3165e-07 | 3.3598e-06 | 1.0323e-07 | 1.3916e-07 | |

| 7.0793e-07 | 2.1939e-07 | 1.2303e-07 | 1.1717e-07 | 1.9125e-06 | 8.8701e-08 | 1.5022e-07 |

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 4.2424e-04 | 2.2186e-03 | 9.2765e-04 | 1.2899e-04 | 3.6004e-04 | 5.2874e-04 | 1.3937e-04 | |

| 4.6117e-04 | 7.0176e-04 | 1.4455e-04 | 8.9927e-05 | 2.3571e-04 | 2.1758e-04 | 3.0062e-05 | |

| 2.0007e-04 | 1.5822e-04 | 7.4068e-05 | 1.6044e-04 | 1.0083e-04 | 1.0073e-04 | 5.3337e-05 | |

| 2.0158e-04 | 7.0237e-05 | 1.4219e-04 | 1.9860e-05 | 2.8870e-05 | 1.4031e-05 | 8.7705e-05 | |

| 5.2760e-05 | 6.2024e-05 | 9.3461e-05 | 1.2797e-05 | 7.3244e-06 | 1.7751e-04 | 8.2802e-05 | |

| 8.2842e-05 | 4.4449e-05 | 5.5727e-05 | 1.9360e-05 | 4.9510e-07 | 1.0716e-04 | 1.3102e-04 | |

| 1.8965e-05 | 2.9679e-05 | 2.2945e-05 | 1.1282e-05 | 5.0190e-05 | 2.4556e-05 | 6.0506e-06 | |

| 1.0528e-06 | 6.9826e-06 | 2.1535e-05 | 1.4995e-05 | 3.0443e-06 | 1.5096e-05 | 5.2518e-05 | |

| 1.1727e-05 | 9.7206e-06 | 1.3592e-05 | 1.7442e-06 | 4.8608e-05 | 1.4890e-06 | 8.4102e-06 | |

| 1.1050e-06 | 8.7650e-06 | 3.6968e-06 | 2.0281e-06 | 2.1769e-05 | 2.1187e-06 | 7.0668e-06 | |

| 4.6550e-06 | 1.0659e-05 | 9.6641e-07 | 3.2260e-06 | 1.2835e-05 | 5.0257e-06 | 7.7813e-06 | |

| 9.9240e-06 | 3.3764e-06 | 1.9763e-07 | 1.0475e-06 | 9.2554e-07 | 8.3166e-07 | 8.3535e-06 | |

| 7.8955e-06 | 3.6975e-06 | 5.6247e-07 | 5.9110e-07 | 6.2199e-06 | 1.1169e-06 | 5.9651e-06 | |

| 4.3561e-06 | 4.1806e-06 | 9.6957e-07 | 6.9539e-07 | 1.2914e-06 | 5.4250e-07 | 4.6332e-06 | |

| 2.9360e-06 | 3.1509e-06 | 1.5560e-06 | 7.1811e-07 | 1.4429e-06 | 3.9447e-07 | 3.0476e-06 | |

| 1.1241e-06 | 2.6445e-06 | 4.2063e-07 | 3.8353e-07 | 2.2397e-06 | 3.1203e-07 | 2.1824e-06 | |

| 8.7692e-07 | 2.1141e-06 | 3.5672e-08 | 1.5187e-08 | 1.6691e-06 | 4.5273e-07 | 5.2714e-07 | |

| 4.3518e-07 | 1.0892e-07 | 1.4269e-07 | 1.4882e-07 | 2.9563e-06 | 3.6523e-07 | 2.6921e-07 | |

| 6.8053e-07 | 1.9842e-08 | 1.4691e-07 | 1.2274e-07 | 1.4889e-06 | 3.5155e-08 | 2.9726e-07 | |

| 4.9385e-07 | 2.8625e-07 | 2.4991e-08 | 5.3652e-08 | 7.4508e-07 | 7.1262e-08 | 1.2514e-07 | |

| 4.5742e-08 | 2.0564e-07 | 7.8722e-08 | 1.9992e-08 | 5.4737e-08 | 3.6093e-08 | 3.1281e-08 |

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 5.6739e-04 | 1.0656e-03 | 8.0536e-04 | 2.4543e-04 | 3.6416e-04 | 1.9768e-03 | 2.4082e-04 | |

| 5.0974e-04 | 1.3895e-04 | 3.1916e-04 | 9.8819e-05 | 2.2928e-04 | 7.7937e-04 | 1.8871e-05 | |

| 2.3304e-04 | 1.3790e-04 | 1.6958e-04 | 9.5142e-05 | 1.9455e-05 | 3.3060e-04 | 3.4341e-05 | |

| 1.1975e-04 | 5.3935e-05 | 2.3725e-05 | 1.8203e-05 | 2.0798e-05 | 8.4316e-05 | 9.2937e-05 | |

| 5.5627e-05 | 3.5630e-05 | 3.4593e-05 | 2.6009e-05 | 1.4971e-05 | 1.5621e-04 | 1.0520e-04 | |

| 2.1237e-05 | 1.8310e-06 | 8.2029e-06 | 2.9298e-05 | 2.4766e-06 | 8.9506e-05 | 9.4057e-05 | |

| 1.9101e-05 | 2.3731e-05 | 1.5520e-05 | 1.7346e-05 | 2.7570e-05 | 5.9149e-05 | 3.1495e-05 | |

| 4.3098e-06 | 1.1266e-05 | 1.2141e-06 | 1.4796e-05 | 2.0351e-05 | 3.5717e-05 | 7.5926e-06 | |

| 1.3111e-05 | 1.7714e-05 | 1.0349e-06 | 1.4350e-06 | 1.2427e-05 | 1.9233e-05 | 1.0986e-05 | |

| 9.3056e-06 | 9.2828e-06 | 1.2580e-06 | 3.1220e-06 | 1.3078e-06 | 4.6659e-06 | 2.1766e-06 | |

| 1.6502e-07 | 1.2191e-05 | 1.1799e-06 | 2.1905e-06 | 7.9287e-06 | 7.8017e-07 | 5.9582e-07 | |

| 7.7765e-06 | 1.5628e-06 | 9.5832e-07 | 1.9508e-06 | 2.1812e-06 | 4.3073e-06 | 1.2697e-06 | |

| 2.7534e-06 | 1.3731e-06 | 2.6880e-07 | 2.6999e-06 | 3.1743e-06 | 3.3863e-06 | 3.9830e-06 | |

| 2.7670e-06 | 1.6556e-06 | 6.9770e-07 | 1.5534e-06 | 2.9464e-06 | 3.5417e-06 | 2.7309e-06 | |

| 1.6428e-06 | 2.4656e-06 | 1.8664e-07 | 5.4349e-07 | 2.4260e-06 | 1.7892e-06 | 5.0548e-07 | |

| 1.2102e-06 | 2.0020e-06 | 7.5073e-07 | 3.9239e-08 | 1.0994e-06 | 4.6812e-07 | 4.4462e-07 | |

| 8.7894e-07 | 1.1624e-06 | 1.3480e-07 | 2.1915e-07 | 5.9294e-07 | 1.2355e-07 | 1.7329e-07 | |

| 4.1233e-07 | 2.6590e-07 | 1.4617e-07 | 2.3914e-07 | 1.0625e-06 | 4.3637e-07 | 7.5010e-08 | |

| 5.0533e-07 | 1.3181e-07 | 3.6327e-08 | 1.0879e-07 | 1.7287e-07 | 2.7534e-07 | 2.0400e-07 | |

| 7.8876e-08 | 7.3116e-08 | 9.0219e-09 | 3.5619e-08 | 8.0690e-08 | 2.2416e-07 | 5.2949e-08 | |

| 3.6846e-08 | 3.7030e-08 | 3.0655e-08 | 3.1748e-08 | 2.0135e-07 | 9.2595e-08 | 2.3311e-08 |

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 2.7181e-04 | 1.4648e-03 | 1.5098e-04 | 4.3883e-06 | 2.9901e-04 | 1.5932e-03 | 2.4472e-04 | |

| 1.1533e-04 | 3.7009e-04 | 1.9943e-04 | 5.6922e-05 | 2.2411e-04 | 6.5545e-04 | 5.3065e-05 | |

| 5.8559e-05 | 2.4444e-05 | 2.2240e-04 | 1.1855e-06 | 1.1090e-04 | 2.5692e-04 | 9.3302e-05 | |

| 3.0213e-05 | 7.7243e-05 | 1.3250e-05 | 5.0104e-05 | 6.3212e-05 | 1.0417e-04 | 8.1908e-05 | |

| 2.6176e-05 | 8.8000e-05 | 1.0513e-05 | 3.0773e-05 | 4.3708e-05 | 3.5951e-05 | 3.7869e-05 | |

| 2.5704e-05 | 2.2879e-05 | 6.0667e-06 | 1.5847e-05 | 3.1172e-05 | 2.4964e-05 | 5.4438e-05 | |

| 1.6400e-05 | 6.4601e-06 | 2.6509e-05 | 1.6833e-05 | 3.9807e-06 | 2.5353e-05 | 1.6738e-05 | |

| 2.5723e-05 | 2.3011e-06 | 9.4629e-06 | 3.7741e-06 | 1.4830e-06 | 2.0617e-05 | 3.5685e-06 | |

| 3.6339e-06 | 7.9537e-07 | 3.5313e-06 | 2.7030e-07 | 4.2998e-06 | 1.7559e-05 | 1.9698e-06 | |

| 2.4027e-06 | 3.4205e-06 | 2.1489e-06 | 9.8305e-07 | 1.3022e-06 | 7.8761e-06 | 2.7688e-06 | |

| 1.0616e-06 | 2.6758e-07 | 6.7986e-07 | 5.3424e-07 | 6.5435e-06 | 4.0980e-06 | 5.9513e-06 | |

| 1.2396e-06 | 3.5144e-08 | 2.5375e-07 | 1.5510e-06 | 3.7089e-07 | 7.6012e-07 | 6.1507e-06 | |

| 2.9497e-06 | 1.3839e-06 | 2.4879e-07 | 3.8104e-07 | 2.6274e-07 | 1.7574e-07 | 3.0190e-06 | |

| 6.3118e-07 | 1.3022e-06 | 5.4231e-07 | 7.0660e-08 | 5.0872e-07 | 4.6938e-07 | 1.1428e-06 | |

| 3.9910e-07 | 5.6549e-07 | 4.2073e-08 | 8.2035e-08 | 1.0986e-06 | 9.7703e-07 | 1.0759e-06 | |

| 1.3857e-07 | 3.5614e-07 | 2.6281e-07 | 7.8423e-08 | 3.0330e-07 | 6.5340e-07 | 5.5114e-07 | |

| 1.2456e-07 | 3.1465e-07 | 1.4513e-07 | 5.6594e-08 | 5.2112e-07 | 6.7542e-07 | 1.6924e-07 | |

| 3.8877e-08 | 4.5444e-07 | 7.6692e-09 | 1.2056e-07 | 4.2312e-07 | 2.6774e-08 | 8.5632e-08 | |

| 4.9357e-08 | 3.1409e-07 | 3.2753e-09 | 5.7784e-08 | 3.3662e-07 | 3.2027e-07 | 8.3400e-08 | |

| 5.8756e-08 | 1.5696e-07 | 4.0094e-08 | 7.5299e-08 | 1.5620e-08 | 1.1288e-07 | 2.2737e-08 | |

| 4.7747e-08 | 1.3307e-07 | 1.7172e-09 | 1.8884e-08 | 5.4771e-08 | 5.3675e-08 | 3.3688e-08 |

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 1.3467e-04 | 8.6149e-04 | 2.5185e-05 | 1.2217e-05 | 2.2807e-05 | 1.5673e-03 | 4.0934e-04 | |

| 9.8530e-05 | 2.1244e-04 | 1.2350e-04 | 2.8501e-05 | 1.0423e-04 | 6.8519e-04 | 1.5751e-04 | |

| 6.4999e-05 | 1.4588e-05 | 1.4909e-04 | 8.1798e-05 | 4.0251e-05 | 3.1762e-04 | 1.1229e-04 | |

| 2.9633e-05 | 1.0840e-05 | 3.3027e-05 | 1.5929e-05 | 2.6352e-05 | 9.4241e-05 | 7.3354e-05 | |

| 2.2212e-05 | 4.6066e-05 | 2.2826e-05 | 1.1102e-05 | 7.2073e-06 | 2.6834e-05 | 5.0587e-05 | |

| 1.2054e-05 | 1.8725e-05 | 1.7282e-06 | 3.8114e-06 | 1.2671e-05 | 9.1230e-06 | 5.5251e-05 | |

| 1.2823e-05 | 3.0327e-06 | 1.1558e-05 | 3.7256e-06 | 1.1825e-06 | 2.3945e-05 | 1.7108e-05 | |

| 1.3401e-05 | 1.6111e-06 | 6.4843e-06 | 2.9136e-06 | 9.6110e-07 | 1.7040e-05 | 9.7979e-06 | |

| 6.8943e-06 | 6.7873e-06 | 3.5997e-07 | 1.4022e-06 | 1.4739e-06 | 1.7244e-05 | 9.7943e-07 | |

| 9.5558e-07 | 5.2841e-06 | 1.2372e-07 | 5.5378e-07 | 7.9296e-07 | 1.1623e-05 | 4.0592e-08 | |

| 2.5459e-06 | 3.9763e-06 | 2.3143e-07 | 6.7444e-07 | 3.3572e-06 | 4.4196e-06 | 6.9266e-07 | |

| 5.4562e-07 | 2.4796e-06 | 5.2787e-07 | 3.3814e-07 | 9.0660e-07 | 1.7345e-06 | 1.2081e-06 | |

| 1.2542e-06 | 4.9482e-07 | 2.2211e-07 | 2.8405e-07 | 9.3243e-07 | 9.0756e-09 | 1.6494e-07 | |

| 1.3561e-06 | 4.6829e-07 | 3.4447e-07 | 2.1075e-07 | 2.2970e-07 | 1.0215e-06 | 7.3312e-07 | |

| 4.1329e-07 | 4.0596e-07 | 3.7870e-07 | 1.9101e-07 | 1.0655e-07 | 9.1786e-07 | 1.1180e-07 | |

| 2.1102e-08 | 4.0582e-08 | 2.3473e-07 | 1.5027e-07 | 2.6465e-07 | 6.2692e-07 | 2.8602e-07 | |

| 1.6030e-07 | 1.0501e-07 | 7.5193e-08 | 2.5815e-07 | 4.3020e-07 | 3.1049e-07 | 3.1752e-07 | |

| 1.5580e-07 | 1.7071e-08 | 1.3795e-07 | 1.1045e-07 | 2.8985e-07 | 2.8060e-07 | 6.7037e-08 | |

| 9.5970e-08 | 3.6384e-08 | 5.3992e-08 | 1.1026e-07 | 1.2426e-07 | 1.6109e-08 | 4.2623e-08 | |

| 1.2839e-07 | 7.4896e-08 | 2.9562e-09 | 3.9335e-08 | 1.9903e-07 | 1.2624e-08 | 1.4648e-07 | |

| 5.5678e-08 | 6.7599e-08 | 1.8549e-08 | 3.0563e-08 | 7.2682e-08 | 1.4640e-08 | 8.7382e-08 |

| # of pts | Crude | Lattice Sequence | Halton (Scrambled) | Sobol (Scrambled) | LHS | Digital Sequence | Dig. Seq. (Interlaced) |

|---|---|---|---|---|---|---|---|

| 1.5710e-04 | 8.9419e-04 | 1.8618e-04 | 6.5101e-06 | 1.8320e-05 | 1.4589e-03 | 3.1380e-04 | |

| 9.2361e-05 | 4.4859e-04 | 2.8858e-05 | 3.8786e-05 | 2.8711e-05 | 6.6735e-04 | 1.2787e-04 | |

| 5.8379e-05 | 1.5565e-04 | 6.6255e-05 | 1.8726e-05 | 1.0374e-05 | 2.9109e-04 | 6.8179e-05 | |

| 3.3845e-05 | 8.1592e-05 | 2.4342e-05 | 7.1920e-07 | 1.3416e-05 | 9.8755e-05 | 5.6511e-05 | |

| 5.2370e-06 | 2.0600e-05 | 1.4788e-05 | 7.0306e-06 | 3.9418e-06 | 3.6814e-05 | 3.0916e-05 | |

| 2.7906e-07 | 7.7793e-06 | 9.4128e-06 | 1.3473e-06 | 1.1746e-05 | 1.7796e-05 | 4.0068e-05 | |

| 6.2211e-06 | 6.0242e-07 | 6.3586e-07 | 5.5014e-06 | 1.9997e-07 | 2.6316e-05 | 6.6292e-06 | |

| 6.4514e-06 | 3.7087e-06 | 5.8152e-06 | 7.0639e-06 | 1.7552e-06 | 1.6112e-05 | 3.7249e-06 | |

| 4.6898e-06 | 4.5985e-06 | 2.3757e-06 | 2.6404e-06 | 6.7808e-07 | 1.1124e-05 | 1.8802e-06 | |

| 1.6862e-06 | 1.7638e-06 | 4.1548e-06 | 1.3125e-06 | 3.1274e-06 | 7.7935e-06 | 8.1426e-07 | |

| 1.2556e-06 | 1.7011e-06 | 2.6991e-06 | 3.4837e-07 | 1.9031e-06 | 2.1677e-06 | 3.8992e-07 | |

| 1.1742e-07 | 2.4503e-06 | 7.1783e-07 | 5.2443e-08 | 8.0455e-07 | 9.4538e-07 | 3.3688e-07 | |

| 2.8181e-07 | 1.7158e-06 | 5.3859e-07 | 7.4264e-08 | 1.8953e-07 | 1.0210e-07 | 1.7921e-07 | |

| 2.6950e-07 | 8.0970e-08 | 1.6078e-07 | 2.3135e-07 | 5.4508e-07 | 4.9568e-07 | 9.5768e-07 | |

| 1.7559e-07 | 1.6269e-07 | 2.6148e-07 | 3.1655e-07 | 2.4941e-07 | 3.2188e-07 | 3.4249e-07 | |

| 7.1632e-09 | 1.5228e-07 | 2.8353e-07 | 8.7367e-08 | 2.1903e-07 | 5.2079e-07 | 1.4805e-07 | |

| 9.2080e-09 | 3.7241e-07 | 6.8674e-08 | 6.0311e-08 | 2.5069e-07 | 2.9650e-07 | 3.2618e-07 | |

| 1.1020e-07 | 1.7140e-07 | 3.9169e-08 | 9.4363e-08 | 2.0381e-07 | 2.2828e-07 | 9.1299e-08 | |

| 1.0817e-07 | 5.9808e-09 | 1.3801e-08 | 7.1774e-09 | 5.3067e-08 | 5.3760e-08 | 1.1753e-07 | |

| 5.3383e-08 | 3.8234e-08 | 5.0781e-09 | 1.1354e-09 | 8.3442e-08 | 2.6882e-08 | 5.3939e-08 | |

| 7.4783e-08 | 3.5218e-08 | 1.7194e-08 | 2.6418e-08 | 1.6789e-08 | 1.3200e-08 | 1.2365e-08 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Georgiev, S.; Todorov, V. Efficient Monte Carlo Methods for Multidimensional Modeling of Slot Machines Jackpot. Mathematics 2023, 11, 266. https://doi.org/10.3390/math11020266

Georgiev S, Todorov V. Efficient Monte Carlo Methods for Multidimensional Modeling of Slot Machines Jackpot. Mathematics. 2023; 11(2):266. https://doi.org/10.3390/math11020266

Chicago/Turabian StyleGeorgiev, Slavi, and Venelin Todorov. 2023. "Efficient Monte Carlo Methods for Multidimensional Modeling of Slot Machines Jackpot" Mathematics 11, no. 2: 266. https://doi.org/10.3390/math11020266

APA StyleGeorgiev, S., & Todorov, V. (2023). Efficient Monte Carlo Methods for Multidimensional Modeling of Slot Machines Jackpot. Mathematics, 11(2), 266. https://doi.org/10.3390/math11020266