Capital Structure Theory: Past, Present, Future

1

Department of Mathematics, Financial University under the Government of Russian Federation, 125167 Moscow, Russia

2

Department of Financial and Investment Management, Financial University under the Government of Russian Federation, 125167 Moscow, Russia

*

Author to whom correspondence should be addressed.

Mathematics 2023, 11(3), 616; https://doi.org/10.3390/math11030616

Submission received: 21 December 2022

/

Revised: 11 January 2023

/

Accepted: 17 January 2023

/

Published: 26 January 2023

(This article belongs to the Special Issue Modern Mathematical Models in Investment: Theory and Practice)

Abstract

:The purpose of this review is to analyze all existing theories of the capital structure (with their advantages and disadvantages) in order to understand all aspects of the problem and make correct management decisions in practice. The role of the capital structure is that the correct determination of the optimal capital structure allows the company’s management to maximize the capitalization of the company and the long-term goal of the function of any company. The review examines the state of the capital structure and capital cost theory from the middle of the last century, when the first quantitative theory was created, to the present. The two main theories, Modigliani–Miller (MM) and Brusov–Filatova–Orekhova (BFO), are discussed and analyzed, as well as their numerous modifications and generalizations. Additionally, discussed is the latest stage in the development of the theory of capital structure, which began a couple of years ago and is associated with the adaptation of the two main theories of capital structure (Brusov–Filatova–Orekhova and Modigliani–Miller) to establish the practice of the function of companies. This generalization takes into account the real conditions of the work of the companies. It was noted that taking into account some effects that are present in economic practice (such as variable income, frequent payments of tax on income, advance payments of tax on income, etc.) brings both theories closer, and even the Modigliani–Miller theory, with all its many limitations, becomes more applicable in economic practice. However, it should be remembered that the Modigliani–Miller theory is only true for perpetual companies, while the BFO theory is valid for companies of any age, and from this point of view, they never coincide.

Keywords:

capital structure; Modigliani–Miller (MM) theory; Brusov–Filatova–Orekhova (BFO) theory; trade-off theoryMSC:

91G50; 91G801. Introduction

The capital structure refers to the ratio between the company’s own and borrowed capital. Does the capital structure affect the main parameters of the company, such as the cost of capital, profit, company value, and others, and if so, how? The choice of the optimal capital structure, i.e., a capital structure that minimizes the weighted average cost of capital WACC and maximizes the company’s capitalization, V, is one of the most important tasks solved by the company’s financial manager. Modigliani and Miller (1958) were the first to seriously study (and the first quantitative study) the effect of a company’s capital structure on its performance. Prior to this study, there was an approach (let us call it traditional) based on the analysis of empirical data. The aim of this review was to analyze all existing theories of the capital structure (with their advantages and disadvantages) in order to understand all aspects of the problem and make correct management decisions in practice. The role of the capital structure is that the correct determination of the optimal capital structure allows the company’s management to maximize the capitalization of the company and the long-term goal of the functioning of any company. The moment of breakthrough was the theory of Modigliani–Miller, which was the first quantitative theory. However, it had a large number of limitations and is of little use in practice. At present, there are increased requirements for making high-quality management decisions in the fields of financial management and corporate finance. This increases the requirements for financial analytics and the use of mathematical methods in economic analysis. The importance of the problem has led to great interest in it and great efforts by scientists to modify the Modigliani–Miller theory.

2. Basic Theories of Capital Structure

2.1. A Historical Point of View

From a historical point of view, five stages in the development of the capital structure theory can be distinguished: First (before 1958), the traditional approach, based on practical experience and existed before the appearance of the first quantitative theory by Modigliani and Miller (the second stage) (1958–1963) [1,2,3,4,5]. The third stage (1964–2008 and later) is the numerous attempts by scientists to modify the Modigliani–Miller theory [6,7,8,9,10,11,12,13,14,15,16,17,18,19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77,78,79,80,81,82,83,84,85,86,87,88,89,90,91,92,93,94,95,96,97,98,99,100,101,102,103,104]. The fourth stage (2008–2019) is the appearance of the Brusov–Filatova–Orekhova (BFO) theory, which removed the main restriction of the Modigliani–Miller (MM) theory associated with the infinite lifetime of a company [16,17,18,19,20,21,22,23]. Additionally, finally, the fifth stage (2019 up to now), which began a couple years ago and is associated with the adaptation of the two main theories of the capital structure (Brusov–Filatova–Orekhova and Modigliani–Miller) to the established financial practice of the company’s functioning by taking into account the real conditions of their work [105,106,107,108,109,110,111,112,113,114].

One of the most important assumptions of the Modigliani–Miller theory is that all financial flows and all companies exist in perpetuity. This limitation was lifted by Brusov–Filatova–Orekhova in 2008 [16], who created the BFO (Brusov–Filatova–Orekhova) theory—a modern theory of capital cost and capital structure for companies of arbitrary age (BFO–1 theory) and for companies of arbitrary lifetime (BFO–2 theory) [17]. Figure 1 shows the historical development of the theory of capital structure from the empirical traditional approach to the general theory of capital structure, BFO, through the perpetuity Modigliani–Miller theory.

One-year companies were studied by Steve Myers in 2001 [71], who showed that the weighted average cost of capital WACC is greater in this case than in the perpetual Modigliani–Miller case, and the value of company V is therefore less. Only two results for the capital structure of the company were known by 2008, when the BFO theory appeared: Modigliani–Miller for perpetual companies and Myers for one-year companies (see Figure 2). The created BFO theory filled the entire interval between t = 1 and t = . This expands capital structure theory for companies of arbitrary ages and/or arbitrary lifetimes. Many new meaningful effects have been discovered in the BFO theory.

2.2. The Empirical (Traditional) Approach

In the traditional approach, based on practical experience and existing before the advent of the first quantitative theory of Modigliani and Miller, the weighted average cost of capital WACC and the associated capitalization of the company, , depend on the capital structure and the level of debt load, L. The cost of debt is always lower than the cost of equity, because the former has less risk due to the fact that the claims of creditors are satisfied before the claims of shareholders in the event of bankruptcy. As a result, an increase in the share of cheaper borrowed capital in the total capital structure to the limit that does not cause a violation of financial stability and an increase in the risk of bankruptcy leads to a decrease in the weighted average cost of capital WACC.

The return required by investors (equal to the cost of equity) is growing; however, its growth did not offset the benefits of using cheaper borrowed capital. Therefore, the traditional approach welcomes the increase in leverage and the associated increase in the value of the company . The empirical, traditional approach existed until the appearance of the first quantitative theory by Modigliani and Miller (1958).

Based on existing practical experience traditional approach, the competition between the advantages of debt financing at a low leverage level and its disadvantages at a high leverage level forms the optimal capital structure, defined as the leverage level, at which WACC is minimal and company value, V, is maximum.

2.3. The Modigliani–Miller Theory

2.3.1. The Modigliani–Miller Theory with Taxes

There are two versions of the Modigliani–Miller theory: without taxes and with taxes. For without taxes, the following expressions for V, WACC, and ke are applicable.

where V0 stands for the unlevered company value, EBIT stands for earnings before interest and taxes, and k0 stands for the equity cost at zero leverage level L.

From (1), one gets the weighted average cost of capital WACC:

From the expression for WACC

and according to (1), one gets the equity cost, ke,

Here, D stands for debt capital value; S stands for equity capital value; kd and wd stand for the cost and share of the company’s debt capital; ke and we stand for the equity capital cost and share. It is seen from (4), that the equity increases linearly with the leverage level.

2.3.2. The Modigliani–Miller Theory with Taxes

Within the framework of the Modigliani–Miller theory with taxes [1,2,3,4,5], the following expression was postulated for the value of a company using borrowed funds, V,

The expression for WACC immediately follows from (5).

The following formula for the cost of equity ke can be obtained from (6) within the framework of the Modigliani–Miller theory with taxes.

The two, Formulas (7) (MM with taxes) and (4) (MM without taxes), differ by the multiplier (1 − t), called the tax corrector. It is less than one unit, thus, the ke (L) curve slope decreases with the accounting of taxes.

2.4. Modifications of Modigliani–Miller Theory

Since the creation of Modigliani-Miller theory, numerous attempts have been made to improve and develop this theory. We will discuss some of these modifications below. One of them is Hamada model.

2.4.1. Hamada Model

The Modigliani–Miller theory, with the accounting of taxes has been united with CAPM (capital asset pricing model) in 1961 by Hamada [38]. For the cost of equity of a leveraged company, the below formula has been derived.

Here, bU is the β–coefficient of the unlevered company. The first term represents risk-free profitability kF, the second term is business risk premium, , and the third term is financial risk premium .

In the case of an unlevered company (D = 0), the financial risk (the third term) is zero, and its shareholders receive only a business risk premium.

Equating CAPM formula to right side of (8), one gets:

or

Below are the formulas for the equity cost, ke, debt cost, kd, and WACC in the CAPM model and (in parenthesis) in the Modigliani–Miller theory [1,2,3,4,5]

The equity cost for an unlevered company:

The equity cost and the debt cost for a levered company:

The weighted average cost of capital WACC

2.4.2. The Cost of Capital under Risky Debt

In the Modigliani–Miller theory, there are two assets types: risky equity and risk-free debt). However, assuming about the risk of bankruptcy of the company and the ability to nonpayment of debt may change the situation with debt. It has been shown by Stiglitz (1969) [115] and Rubinstein (1973) [116] that the assumption concerning risky debt does not change the company’s value with respect to the Modigliani and Miller results under free of risk debt [1,2,3,4,5]. However, the debt cost is changed from a constant value kd = kF to a variable one. As Hsia (1981) [117], based on the models of pricing options, Modigliani–Miller and CAPM, has shown in the formula for the net discount profit, a term, reflecting tax shield should be discounted at the rate:

where

—cumulative normal distribution of probability of random value d1 and t—a moment of payment a credit.

2.4.3. The Account of Corporate and Individual Taxes (Miller Model)

Modigliani and Miller considered only corporate taxes, but they did not take into account the individual taxes of investors.

Miller (1997) [3] has developed the model with an account of the corporate and individual taxes and studied the impact of leverage on the company’s value.

The model is described by the following formula for levered company value:

Here, the first term is the unlevered company’s value

where TS stands for the tax on income of an individual investor from his ownership by the corporation stock rate, TC stands for the tax rate on corporate income, TD stands for the tax rate on interest income from the provision of investor–individuals of credits to other investors and companies.

The Miller model estimates the value of a levered company, accounting for corporate tax, as well as tax on individuals. The second term is the Miller formula.

represents the gains from use of debt capital. This term replaces the tax shield in the Modigliani–Miller model with corporate taxes:

2.4.4. Alternative Expression for WACC

Alternative formula for the WACC, different from Modigliani–Miller, one has been derived in [32,33] from the WACC definition and the balance identity (see Berk and De Marzo, 2007):

where k0, kd, and kTS are the expected returns on the unlevered company, the debt, and the tax shield, respectively.

Some additional conditions are required for Equation (21) to have practical applicability. If the WACC is constant over time, as stated in Farber, A. et al., 2006, the levered company capitalization is found by discounting with the WACC of the unlevered company.

In textbooks [12,13,14], formulas for the special cases, where the WACC is constant, could be found.

In 1963, Modigliani and Miller assume that the debt value D is constant. Then, as the expected after-tax cash flow of the unlevered firm is fixed, V0 is constant as well. By assumption, kTS = kD and the value of the tax shield is TS = tD. Thus, the capitalization of the company V is a constant, and the alternative Formula (21) becomes a formula for a constant WACC:

Since the debt kd and the tax shield kTS have a debt nature, it seems reasonable that the expected returns are equal, as suggested by the “classical” Modigliani–Miller (MM) theory, which has been modified by Brusov et al. for cases of practical meaning.

2.4.5. The Miles–Ezzell Model Versus the Modigliani–Miller Theory

Denis M. Becker (2021) [11] discussed the differences between the Modigliani–Miller theory [1,2,3,4,5] and the Miles–Ezzell model [61], which deal with the stochasticity of free cash flows. The Modigliani–Miller theory considers a stationary process, while in the Miles–Ezzell model the process is stochastic. The author conducts a numerical experiment that allows you to determine the values and discount rates using a risk-neutral approach. He analyzes three formulas:

Miles–Ezzell model [61],

Cooper, I.A. and Nyborg, K.G. (2006) [118]

where kf stands for the risk-free rate, which equals the required return of the debt holders.

The author shows that in the Miles–Ezzell model, all cash flows and the values depend on the path, in contrast to the Modigliani–Miller theory. Additionally, in the Miles–Ezzell model, all discount rates are time independent, with the exception of the discount rate used to discount tax shields, which depends on the duration of the cash flows. Conversely, in the Modigliani–Miller theory, all discount rates change over time except for the constant tax shield discount rate. This affects the applicability of the well-known formula for annuities and the development of models for estimating both finite and perpetual cash flows.

In this paper, Becker (2021) [11] raises the issue of paying the debt body together with the payment of interest on the debt. Regarding this issue, we would like to note that in both classical MM and BFO theories, the body of the debt is not paid. In the framework of the Modigliani–Miller theory, such an account is fundamentally impossible, while in the BFO theory it can be conducted and was conducted in the framework of the BFO-2 theory, where the amount of debt D decreases with time. This decrease in the value of debt D results in a decrease in the tax shield (see BFO-2 theory).

3. Trade–Off Theory

For decades, one of the main theories of capital structure was the trade-off theory. There are two modifications of the trade-off theory: the static and dynamic [119,120,121,122].

3.1. Static Theory

The static trade-off theory accounts for income tax and the cost of bankruptcy. Within this theory, the optimal capital structure is formed by the balancing act between the benefits of debt financing at a low leverage level (from the tax shield from interest deduction) and the disadvantages of debt financing at a high leverage level (from the increased financial distress and expected bankruptcy costs). The tax shield benefit is equal to the product of the corporate income tax rate and the market value of debt, and the expected bankruptcy costs are equal to the product of the probability of bankruptcy and the estimated bankruptcy costs.

The static version of the trade-off theory does not take into account the costs of adapting the capital structure to the optimal one, the economic behavior of managers, owners, and other participants in an economic process, as well as a number of other factors.

3.2. Dynamic Theory

The dynamic version of trade-off theory suggests that the costs of adjusting the capital structure are high, and therefore, companies will only change their capital structure if the benefits outweigh the costs. Therefore, there is an optimal range that varies on the outside of each lever but remains the same on the inside. Companies try to adjust their leverage when it reaches the edge of the optimal range. Depending on the type of adaptation costs, companies reach the target ratio faster or slower. Proportional changes involve a small adjustment, while fixed changes imply significant costs.

In the dynamic version of the trade-off theory, a company’s capital structure decision in the current period depends on the expected company income in the next period.

As it has been shown within BFO theory (Brusov et al., 2013 [19]), under increased financial distress costs and bankruptcy risk, the optimal capital structure is absent. This means that the trade-off theory does not work in either the static or dynamic versions.

3.3. Proof of the Bankruptcy of the Trade-Off Theory

Brusov et al. [19] tested whether assumptions about risky debt financing (and about rising lending rates in the run-up to bankruptcy) did not lead to an increase in the weighted average cost of capital, WACC. They used the following model:

and showed that under the above conditions, WACC still decreases with leverage (Figure 3).

This means there is no minimum for WACC with leverage changes, and no maximum for company capitalization with leverage changes. Thus, this means that there is no optimal capital structure in the famous theory of trade-offs. This fact has been explained by Brusov et al. [19]. The explanation to this fact has been done within the Brusov–Filatova–Orekhova theory by studying the dependence of the equity cost ke on leverage. The explanation for this fact is as follows: The dependence of the cost of equity, ke, on the level of leverage undergoes significant changes when the growth in the cost of debt capital, kd, with the level of leverage is included (Figure 4 and Figure 5). The linear growth of the cost of equity ke at a low level of leverage is replaced by its fall, starting from a certain value L0. The value of L0 sometimes correlates exactly with the initial growth point kd with leverage level, but sometimes it takes values much higher.

The rate of decline in the cost of equity ke with leverage increases with an increase in the growth rate of the cost of debt kd, as well as when moving from linear to quadratic growth and exponential growth. Thus, we come to the conclusion that the increase in the cost of debt capital kd with leverage leads to the decrease in equity cost ke with leverage, starting with some value, L0. This is the cause of the absence of weighted average capital cost growth with leverage at all its values. The conclusions made are independent of rate of growth of kd with leverage.

Thus, this means that there is no optimal capital structure in the famous theory of trade-offs. This paradoxical conclusion explains the absence of an optimal capital structure in the famous trade-off theory. This means that the competition between the benefits of leverage and the cost of financial hardship (or the cost of bankruptcy) is not balanced, and the hope that trade-off theory gives us an optimal capital structure is unfortunately not realized. Mechanism of formation of the company’s optimal capital structure, different from suggested by trade-off theory has been developed by Brusov et al. (2014) [21].

4. Accounting for Transaction Costs

If the cost of changing the capital structure to its optimal value is high, the company may decide not to change the capital structure and maintain the current capital structure.

The company may decide that it is more cost effective not to change the capital structure, even if it is not optimal, for a certain period of time. Due to this, the actual and target capital structure may differ.

5. Accounting for Asymmetries of Information

In real financial markets, information is asymmetric (company managers have more reliable information than investors and creditors), and the rationality of economic entities is limited.

6. Signaling Theory

7. Pecking Order Theory

The pecking order theory (Myers 1984 [72,73], Fama E., French 2004 [31]) describes a preferred sequence of funding types for raising capital. That is, companies first use financing from retained earnings (internal equity), the second source is debt, and the last source is the issuance of new shares of common stock (external equity). Empirical data on the leverage level of non-financial companies, combined with the decision-making process of top management and the board of directors, indicate a greater commitment to the pecking order theory. Note that this theory contradicts both MM and BFO theories, which underline the importance of debt financing.

8. Behavioral Theories

8.1. Manager Investment Autonomy

Company managers implement those decisions that, from their point of view, will be positively perceived by investors and, accordingly, will positively affect the market value of companies: when the market value of the company’s shares and the degree of consensus between the expectations of managers and investors is high, the company conducts an additional share issue, and in the opposite situation, it uses debt instruments. Thus, the company capital structure is more influenced by investors, whose expectations are taken into account by company managers.

8.2. The equity Market Timing Theory

The level of leverage is determined by market dynamics. Equity market timing theory means that a company should issue shares at a high price and repurchase them at a low price. The idea is to take advantage of the temporary fluctuations in the value of equity relative to the value of other forms of capital.

8.3. Information Cascades

To save costs and avoid mistakes, the company’s capital structure can be formed not on the basis of calculations of the optimal capital structure (this is a non-trivial task and its correct solution could be found within the framework of the BFO theory) or depending on the available sources of financing of the company, but borrowed from other companies, having successful, proven managers (heads of companies), as well as using (following the majority) the most popular methods of managing the capital structure, or even simply by copying of the capital structure of successful companies in a similar industry.

9. Theories of Conflict of Interests

9.1. Theory of Agency Costs

The company’s management may make decisions that are contrary to the interests of shareholders or creditors, respectively; expenses are necessary to control its actions. For solving the agency problem, the correct choice of the compensation package (the agent’s share in the property, bonuses, and stock options) is needed, which allows you to link the manager’s profit with the dynamics of equity capital and ensure the motivation of managers for the preservation and growth of equity capital (Jensen et al., 1973 [44]).

9.2. Theory of Corporate Control and Costs Monitoring

In the presence of information asymmetry, creditors providing capital are interested in the possibility of self-control over the effectiveness of its use and return. Monitoring costs are usually passed on to company owners by being included in the loan rate. The level of monitoring costs depends on the scale of the business; therefore, with the increase in the scale of the business, the company’s weighted average capital cost increases, and the company’s market value decreases.

9.3. Theory of Stakeholders

Stakeholder theory is a theory that defines and models the groups that are the stakeholders of a company. The diversity and intersection of interests of stakeholders, their different assessments of acceptable risk, give rise to conditions for a conflict of their interests, that is, they make adjustments to the process of the capital structure optimization.

10. BFO Theory

The restriction associated with the infinite life of companies and the eternity of cash flows within the framework of the MM theory was removed in 2008 by Brusov, Filatova, and Orekhova (Filatova et al., 2008 [16]), who created the modern theory of the cost of capital and capital structure—the BFO theory, which is valid both for companies of arbitrary age, as well as for companies with an arbitrary lifetime. A generalization of the assessment of the tax shield TS and the value of the company: without leverage V0 and with leverage V was required to modify the theory of MM (see the formulas below):

Here, S stands for the equity capital value, stands for the debt capital share, stands for the equity cost and the equity capital share, and stands for the value of financial leverage; D stands for the debt capital value.

For a one-year company Steve Myers in 2001 derived a formula, which could be obtained easily from Formula (11) by substituting n = 1.

By substituting we arrive to the Modigliani–Miller formula for WACC (Modigliani and Miller, 1963 [2]):

Dependence of WACC on leverage level for n = 1, n = 3, and see in Figure 6.The methods and the conclusions of the Brusov–Filatova–Orekhova (BFO) theory are well–known in the scientific literature. In a number of works the BFO theory is used in practical calculations.

Brusov–Filatova–Orekhova Theorem

Case of Absence of Corporate Taxes

Modigliani–Miller theory in case of absence of corporate taxes provides the following results for dependence of WACC and equity cost ke on leverage:

and thus,

For the finite lifetime (finite age) companies, the Modigliani–Miller theorem about equality of value of financially independent and financially dependent companies has the following view:

Using this relation, we have proven an important Brusov–Filatova–Orekhova theorem:

Under the absence of corporate taxes, the equity cost of the company, ke, as well as its weighted average cost of capital, WACC, does not depend on the lifetime (age) of the company and is equal, respectively, to

11. BFO Theory and Modigliani–Miller Theory under Inflation

The influence of inflation on cost of raising capital and the company value has been studied within modern theory of capital cost and capital structure Brusov–Filatova–Orekhova theory (BFO theory) [22] and within its perpetuity limit Modigliani–Miller theory. For the first time, it was shown by the direct incorporation of inflation into both theories that inflation not only increases the cost of raising capital (the equity cost and the weighted average cost of capital), but that it also changes their dependence on leverage. In particular, it increases the growth rate of equity costs with leverage. The company’s value decreases under inflation (Figure 7).

Formula (35) is the generalized Brusov–Filatova–Orekhova formula under inflation.

Here, . In the Modigliani–Miller theory,

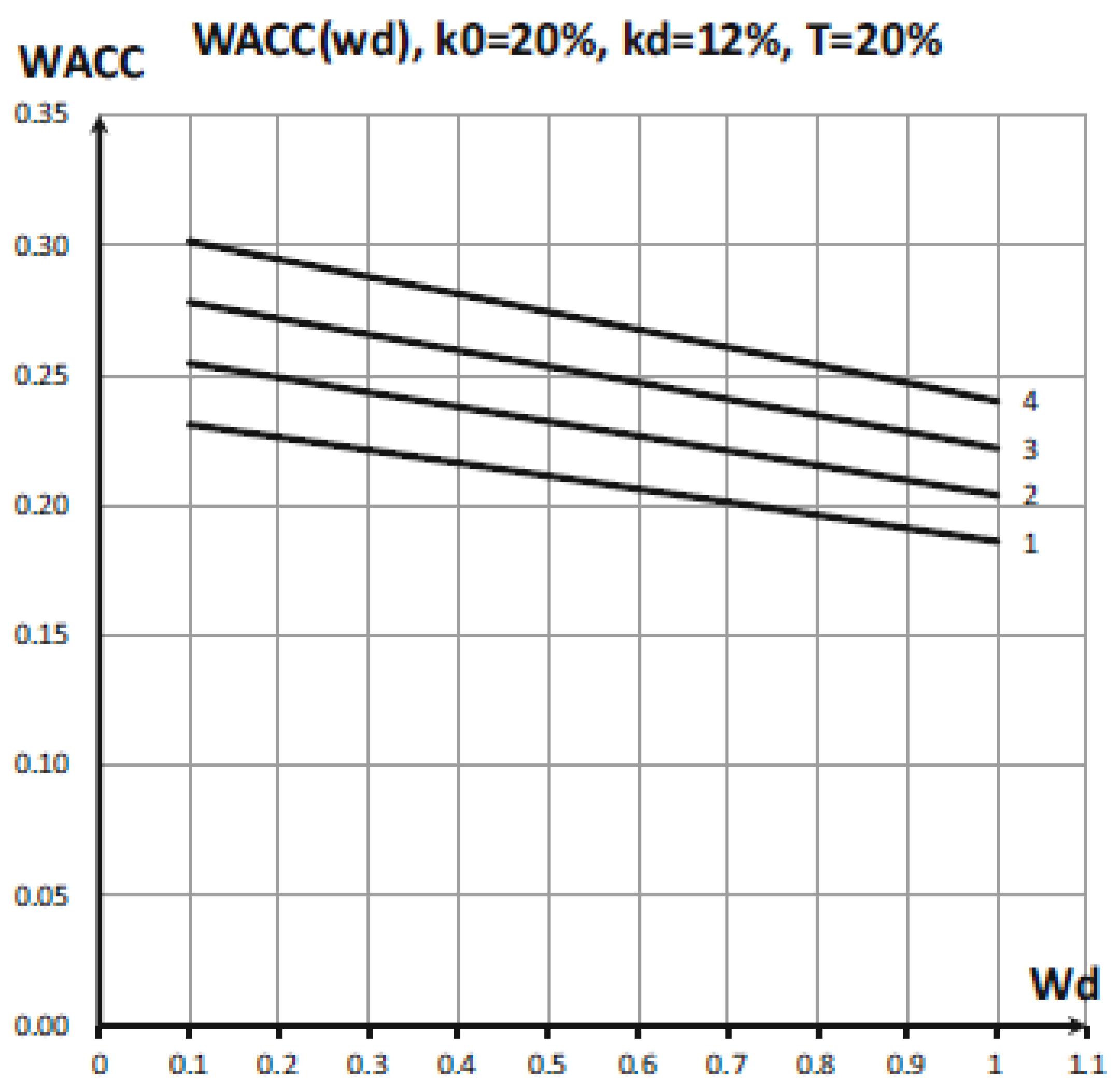

The modified equation for the weighted average cost of capital WACC, applicable to companies of arbitrary age under inflation, was derived in the framework of the modern theory of cost and capital structure—the theory of Brusov-Filatova-Orekhova (BFO theory). The modified BFO equation allows investigation of the dependence of the weighted average cost of capital, WACC, (see Figure 8) and the cost of equity, ke, on the level of financial leverage, L, on the income tax rate, t, on the age of the company, n, on the cost of equity, k0, and the cost of debt, kd, for various inflation rates α.

Using the modified BFO equation, authors analyzed the dependence of the weighted average cost of capital WACC on the share of debt wd at various income taxes t, as well as the inflation rate α.

It was shown that WACC decreases with an increase in leverage level L (or the share of debt, wd), and the faster it decreases, the higher the income tax rate t. The distance between the lines, corresponding to different values of the income tax rate at the same step (10%), increases with the growth of the inflation rate α. The area of change (with a change in the income tax rate t) of the weighted average cost of capital WACC increases with the inflation rate α, as well as with the age of the company n.

12. BFO Theory for the Companies Ceased to Exist at the Time Moment n (BFO–2 Theory)

The MM theory is only applicable to perpetual companies. As follows from the derivation of the BFO formula, the developed methodology is applied to companies of arbitrary age n (which have reached the age of n-years and continue to operate in the market). In other words, the BFO is applicable to the most interesting practical cases and allows you to analyze the financial condition of operating companies. However, the BFO theory also allows us to consider the financial condition of companies that have ceased to exist, i.e., those for where n does not mean age, but lifetime, i.e., the time of existence. There can be many schemes for terminating a company: bankruptcy, merger, takeover, etc. Below we will consider one of these schemes. When the value of debt capital D becomes equal to zero at the time of the termination of the company n, in this case, the BFO theory requires minimal updates, as shown below (Brusov et al., 2018 [17]).

From the formula for the company’s capitalization, it is easy to obtain an estimate of the “residual capitalization” of the company, discounted to the time moment k:

Substituting

one gets the expression for the tax shield for n years, subject to the termination of the company’s activities at time moment n:

Substituting this formula into the equation,

we arrive at the following equation (which determines the BFO–2 theory)

hence, it is possible to find WACC for companies with an arbitrary lifetime n, under the condition that the company ceases to operate at a time moment n.

13. The Modigliani–Miller Theory with Advance Payments of Tax on Profit

The first serious study (and first quantitative study) of influence of capital structure of the company on its indicators of activities was the work by Nobel Prize Winners Modigliani and Miller. Their theory has a lot of limitations. One of the most important and serious assumptions of the Modigliani–Miller theory is that all financial flows as well as all companies are in perpetuity. This limitation was lifted by Brusov–Filatova–Orekhova in 2008 (Filatova et al., 2008 [16]), who created the BFO theory—a modern theory of capital cost and capital structure for companies of arbitrary age. Despite the fact that the Modigliani–Miller theory is currently a particular case of the general theory of capital cost and capital structure—Brusov–Filatova–Orekhova (BFO) theory—is still widely used in the West.

Brusov et al., [105,106,107,108,109,110,111,112,113,114] discuss another limitation of the Modigliani-Miller theory: the method of paying income tax. The Modigliani-Miller theory accounts for these payments as immediate annuities, while in practice these payments are often made in advance and therefore must be accounted for annuities due. The authors generalized the Modigliani-Miller theory to the case of advance payments on income tax, which is widely used in practice. This generalization leads to a serious change in all the main provisions of Modigliani and Miller. These changes are as follows: When WACC begins to depend on the cost of debt kd, WACC turns out to be lower than in the case of the classical Modigliani–Miller theory, and the value of the company becomes higher. The formula for WACC has the following form:

Although the dependence of the cost of equity ke on the level of leverage L remains linear, the angle of inclination relative to the L axis turns out to be smaller: this may lead to a modification of the company’s dividend policy. Correct accounting for the method of paying income tax shows that the shortcomings of the Modigliani-Miller theory are more serious than everyone expected: the underestimation of WACC is indeed greater, as is the overestimation of the company’s capitalization. This means that the systematic risks arising from the use of the modified Modigliani-Miller theory (the MMM theory) (more correct than the “classical” theory) are in practice higher than it was supposed by the “classical” version of this theory.

14. The Modigliani–Miller Theory with Arbitrary Frequency of Payment of Tax on Profit

One of the conditions for the real functioning of companies is the payment of income tax with an arbitrary frequency (monthly, quarterly, every six months or annually). The return is not required more than once a year, but companies may be required to file estimated taxes based on profits earned. The authors of [109] generalized the Modigliani–Miller theory to the case of paying income tax with arbitrary periodicity. The formula for WACC has the following form Brusov et al., (2021 [110])

and for company value

They showed that the frequency of income tax payment affects all the main financial indicators of the company and leads to a number of important consequences. Theoretically, the authors derived all the main formulas of the modified Modigliani-Miller theory and used them to obtain all the main financial indicators of the company at arbitrary frequencies of income tax payment. They showed that: (1) all Modigliani–Miller theorems, assertions, and formulas have been changed; (2) all major financial indicators, such as the weighted average cost of capital (WACC), the value of the company, V and the cost of equity, ke, depend on the frequency of income tax payments; (3) in the case of paying tax on profit more than once a year (with p ≠ 1), as is the case in practice, WACC, company value, V and equity value, as well as equity cost ke start depend on the cost of debt, kd, and in the usual (classical) Modigliani–Miller theory, all these quantities do not depend on kd; (4) the results obtained allow the company to choose the number of tax on profit payments per year (of course, within the framework of the current tax legislation): more frequent tax on profit payments are beneficial to both parties, the company and the tax regulator.

15. Generalization of the Modigliani–Miller Theory for the Case of Variable Profit

In (Brusov et al., 2021 [108]), for the first time, the world-famous theory of Nobel laureates Modigliani and Miller was generalized to the case of variable income, which significantly expands the applicability of the theory in practice, in particular, in corporate finance, business valuation, investments, ratings etc. The following formulas for WACC and company value have been obtained

It was shown that all the theorems, assertions and formulas of Modigliani and Miller have been essentially changed. The authors obtained the following results: (1) WACC and k0 are no longer the discount rates as it takes place in case of classical Modigliani–Miller theory with constant profit. The role of discount rate for leverage company passes from the weighted average cost of capital, WACC, to WACC − g (where g is growing rate), for a financially independent company from k0 to k0 − g. The real discount rates WACC − g and k0 − g decrease with g, while WACC grows with g. This decrease leads to an increase in company value with g. (2) The slope of the equity cost ke(L) grows with g. Via the fact, that the economically justified value of dividends is equal to equity cost this will modify the company’s dividend policy. (3) It has been discovered the qualitatively new effect in corporate finance: the slope of the curve ke(L) at rate g < g* turns out to be negative. This effect significantly alters the company’s dividend policy principles.

16. The Generalization of the Brusov–Filatova–Orekhova Theory for the Case of Payments of Tax on Profit with Arbitrary Frequency

The Brusov-Filatova-Orekhova (BFO) theory and its limit of eternity, the Modigliani-Miller theory—both the main theories of the cost of capital and capital structure—consider income tax payments once a year. These payments in the real economy are made more frequently (every six months, quarter, month, etc.). In (Brusov et al., 2021 [109]) the Modigliani–Miller theory was generalized by Brusov et al., for the case of paying income tax with arbitrary periodicity. In (Brusov et al., 2022 [112]), for the first time, authors generalized the theory of Brusov–Filatova–Orekhova (BFO) to this case. Taking into account one of the features of the real functioning of companies—frequent payments of income tax—the authors brought the BFO theory closer to economic practice. Authors derived modified BFO formula

and showed that:

(1) All BFO formulas change; (2) all major financial parameters of a company, such as company capitalization, V, weighted average cost of capital, WACC, cost of equity, ke, etc. depend on the frequency of tax on profit payments. The cost of raising capital WACC decreases with the frequency of tax on profit payments and the company value, V increases with the frequency of tax on profit payments. A qualitatively new anomalous effect takes place at some age of the company, n, and at some frequency of income tax payments p: the cost of equity ke(L) decreases with leverage level L.

Since the economically justified amount of dividends is equal to the cost of equity, this fundamentally changes the company’s dividend policy. More frequent income tax payments are beneficial to both parties—the company and the tax regulator: the company, because it increases the value of the company, and the tax regulator, because it benefits from earlier payments due to the time value of money.

17. Benefits of Advance Payments of Tax on Profit: Consideration within the Brusov–Filatova–Orekhova (BFO) Theory

Both theories of capital structure—the Brusov–Filatova–Orekhova (BFO) and its limit of eternity, the theory of Modigliani–Miller—consider the case of paying tax on profit at the end of the year. However, in practice, companies could make these payments in advance. In (Brusov et al., 2020 [106]) the Modigliani-Miller theory was modified for the case of advance payments of tax on profit, and the results turned out to be completely different from the results of the usual Modigliani–Miller theory. In (Brusov et al., 2022 [111]), the Brusov–Filatova–Orekhova (BFO) theory was modified for the first time for advance payments on income tax. The impact of such a transition to advance payments is much more significant than in the theory of MM, and even leads to a qualitatively new effect in the cost of equity dependence on leverage. The authors derived a modified BFO formula for WACC:

It is concluded that the tax shield and the way it is formed (payments at the end of the year or in advance) have very important consequences, changing all the company’s financial indicators, such as the company’s value and capital raising costs, and also significantly changing the company’s dividend policy.

18. Influence of Method and Frequency of Profit Tax Payments on Company Financial Indicators

In practice, income tax payments may (1) be made in advance and (2) more frequently than once a year. In (Brusov et al., 2022 [112]), the simultaneous influence of these two factors on the company’s financial performance was studied. To this end, the Brusov–Filatova–Orekhova (BFO) theory was first generalized to the case of advance payments of income tax with an arbitrary periodicity. The authors derived the following modified BFO formula for WACC:

It is concluded that all financial indicators of the company, such as the weighted average cost of capital (WACC) and the cost of equity (ke), the value of the company (V) depend on the frequency of income tax payment. WACC increased with the frequency of payments, and the value of the company decreased. This meant that infrequent payments could be beneficial to the company in the case of advance income tax payments. The slope of the cost of equity, ke(L), increased with the frequency of payments. Depending on the age of the company, ke(L) either increased for some payment frequencies or decreased with L for all payment frequencies. The authors compared these results with their results for income tax payments at the end of the periods (see Formula (48)) and found a huge difference: while in the latter case, WACC decreased with payment frequency, and the company capitalization increased with payment frequency, the value of WACC in this case remains bigger, and the company capitalization remains lower than in the case of advance income tax payments of any frequency. The importance of advance income tax payments has been underlined by this fact. The authors developed the recommendations to the regulator to increase the practice of advance payments of income tax due to the benefits of this for both parties: the companies and the state. A new effect—the decrease in equity cost with the level of leverage (L)—has been discovered.

19. The Brusov–Filatova–Orekhova (BFO) Theory with Variable Income

Two main theories of capital structure—Brusov–Filatova–Orekhova (BFO) and Modigliani–Miller consider the case of constant profit. However, in practice, the company’s income, of course, is variable. Both theories have recently been generalized to the case of variable income [113], which significantly expands the applicability of both theories of capital structure in practice. The following generalized BFO formula for WACC has been discovered:

In the theory of Brusov–Filatova–Orekhova (BFO) (Brusov et al., 2022d), generalized to the case of variable income, income tax payments are made at the end of periods, while in practice these payments can also be made in advance. In Brusov et al.’s, [113], work the authors considered two modifications of the Brusov–Filatova–Orekhova (BFO) theory with variable income: (1) with the payment of income tax at the end of the periods and (2) with advance payments of income tax.

For these two cases, BFO formulas were derived for the weighted average cost of capital, WACC, for the value of the company, V, and within these formulas, a comprehensive analysis of the dependence of WACC, of the discount rate, WACC–g (here g is the growth rate), company capitalization, V, the cost of equity, ke, on debt financing at different values of the growth rate, g, at different values of the cost of debt capital, kd, and at different values of the age of the company, n. The results for cases (1) and (2) are compared, which allows us to conclude that case (2) is always preferable for both the company and the regulator. This makes it possible to develop recommendations for both parties to expand the practice of advance income tax payments within the framework of real economic practice.

Brusov et al. emphasized an important observation. If in the classical versions of the Brusov–Filatova–Orekhova (BFO) theory and its perpetual limit—the theory of Nobel laureates Modigliani and Miller—the case of constant profit was considered, and where the gap between these two theories is huge (many qualitative effects that take place in the first theory, missing in the second), when taking into account variable profit, some effects of the BFO theory also take place in the Modigliani–Miller theory. This means that taking into account some effects that are present in economic practice (for example, variable income) brings both theories closer, and even the Modigliani–Miller theory, with all its many limitations, becomes more applicable in economic practice. However, it should be remembered that the Modigliani–Miller theory is only true for perpetual companies, while the BFO theory is valid for companies of any age, and from this point of view, they never coincide.

20. Qualitatively New Effects in the Theory of Capital Structure

Two qualitatively new effects in the theory of capital structure

Among the many new effects discovered in the framework of the BFO theory, we will describe only two new ones qualitatively:

- Golden and silver ages of the company

- Anomalous dependence of the cost of equity on the leverage level

20.1. Golden and Silver Ages of the Company

To determine the minimum cost of raising capital depending on the age of the company, Brusov et al., [17] studied the dependence of the cost of raising capital on the age of the company, n, at different levels of leverage, L, at different values of capital costs. The authors used the Brusov–Filatova–Orekhova theory [16,17].

It was shown for the first time that the value of WACC in the Modigliani–Miller theory is not minimal, and the value of the company is not maximal, contrary to the opinion of all financiers: it turned out that at a certain age of the company, the value of WACC is lower than in the eternal Modigliani–Miller theory, and the value of company V is greater than the value of company V in the Modigliani–Miller theory.

Authors discovered two types of WACC dependences on the age of company n: monotonic decreases with n and WACC decreases with passage through the minimum, followed by a limited growth [17] (Figure 9). The latter type of dependence of WACC on the age of company n allows the companies to take advantage of the benefits given at a certain stage of their development.

Moreover, since capital costs, ke and kd, affect the company’s golden age by changing it (for example, changing the value of dividend payments to reflect the cost of equity, etc.), the company can postpone or extend its golden age, at which the cost of raising capital is minimal (and less than its perpetual limit), and the value of companies is maximum (above their perpetual value).

1-1’—monotonic decrease in WACC, and company value, V, increases with the company age n;

2-2’—WACC decreasing with n, passage through minimum (at ), followed by a limited growth and increase in V with the passage through a maximum (at ) and then a limited decreasing.

It has been shown that the existence of the company “golden age” depends not on the capital cost values, but on the difference between equity k0 and debt kd costs. The effect of the company “golden age” takes place at small enough difference between k0 and kd costs, while at this difference the high value effect is absent: curve WACC(n) monotonic decreases with company age n. Curve WACC(L) for perpetuity limit is the lowest one for the companies without the “golden age” (Figure 10), while for the companies with the “golden age”, curve WACC(L) for perpetuity limit (n = ∞) lies between curves WACC(L) for one year (n = 1) and three years (n = 3) companies (Figure 6 and Figure 11).

20.2. Silver Age of the Company

On Figure 12 the effect of "Silver Age of the Company" is shown.

20.3. Anomalous Dependence of the Company’s Equity Value on Leverage

Brusov et al. (2013 [20]) found a qualitatively new effect in the capital structure: a decrease in the cost of equity at a leverage level L (Figure 13). This effect is absent in the perpetual Modigliani–Miller limit, but appears in companies of finite age at an income tax rate exceeding a certain value T*.

For some values of the cost of equity and the cost of debt, this effect exists at the tax on income values existing in financial practice. This ensures the practical significance of the discovered effect. Accounting for this effect is important when changing tax legislation and can significantly change the company’s dividend policy.

21. A Stochastic Extension of the Modigliani–Miller Theory

A stochastic extension of the Modigliani–Miller theory has been conducted in a few papers.

Demarzo (1988) [59] showed that the Modigliani–Miller theory is correct in a multi-period stochastic economy with incomplete markets. In the model the author developed, companies could trade securities, and stock prices and dividends became completely interdependent. Several corporate control mechanisms were considered, including maximizing the value of the company and shareholder voting. It is shown that equilibrium companies have no incentive to trade securities and that the set of equilibrium distributions does not change as a result of such trading.

Sethi et al. (1991) [96] studied the company value valuation problem under a partial equilibrium, a time-dependent discount rate, and a general stochastic environment in a discrete-time setting. The time path of the share price and the company value are obtained upon the assumption of risk neutrality.

22. Conclusions

The review analyzes all the main existing theories of capital structure, including Modigliani–Miller and BFO. Various modifications of these two and other theories, including the latest ones, related to the conditions of the real functioning of companies and developed in recent years are discussed in detail.

The generalization of the Modigliani–Miller theory for cases of practical interest led to a much more significant change in the Modigliani–Miller theory than in all previous modifications studied over the previous decades. Obtained results showed that under such a generalization there is some convergence of the Modigliani–Miller theory and the BFO theory. The former theory began to have some new properties similar to those of the BFO theory, which were not there in the classical Modigliani–Miller theory. Between the properties of the former and those of the BFO theory, there was a huge gap. Most of the innovative effects existing in the BFO theory are absent in the classical Modigliani–Miller theory.

All the above means that the considered effects, such as the variable income of the company, the frequent payment of income tax, advance payment of income tax, and the combinations of these conditions and others, are more important than the effects studied earlier and have much less influence on the Modigliani-Miller theory. Taking these effects into account leads to some convergence between the Modigliani-Miller theory and the BFO theory. At the same time, one must understand that the Modigliani-Miller theory remains perpetual and will never describe a company of arbitrary age, which is extremely important for the practical application of the theory.

Despite the great progress associated with the described generalization of both theories during the last couple of years, there are still some limitations that dictate the direction of further research.

If we talk about the two main theories of the structure of capital: Modigliani-Miller and BFO, then one of the limitations is that the BFO theory and the MM theory were generalized to the case of a variable company income, but with a constant growth rate g.

The directions for further research are as follows:

- generalization of the BFO theory and the MM theory to the case of a company’s variable-in-time income;

- generalization of the BFO theory to the stochastic case and to the case of a company’s variable-in-time income;

- further generalization of the BFO theory and MM theory on the conditions for the practical functioning of the company;

- study the dependence of the effects of the “golden and silver age of the company” on the growth rate of income in the case of a company’s variable income, on the frequency of income tax payment, on the advance payment of income tax, and on a combination of these conditions;

- develop a methodology for determining the financial parameters of a company in the event of a drop in income, in the event of an increase in the company’s income, as well as in the case of alternating growth and falling income.

The practical significance of the capital structure theory is as follows:

- -

- analysts can evaluate the company’s financial indicators for companies of arbitrary age;

- -

- allows for taking into account the conditions of the company’s real functioning;

- -

- allows to take into account the anomalous effects discovered in the BFO theory (such as “Golden age”, “abnormal dependence of equity cost with leverage”, etc.), which allow for making nonstandard effective management decisions;

- -

- allows the regulator to improve tax policy;

- -

- allows for the correct determination of the discount rate, which is extremely important in business valuation;

- -

- allows us to correctly determine the effectiveness of investments through the correct determination of the discount rate;

- -

- allows to correctly issue ratings of nonfinancial issuers, financial issuers, and investment projects.

In conclusion we present in Table 1 classification and summary of main theories of capital structures of company.

Author Contributions

Conceptualization, P.B. and T.F.; methodology, T.F.; software, P.B. and T.F.; validation, P.B.; formal analysis, P.B. and T.F.; investigation, P.B. and T.F.; writing—original draft preparation, P.B. and T.F.; numerical calculations, P.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available upon request from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. Am. Econ. Rev. 1958, 48, 261–296. [Google Scholar]

- Modigliani, F.; Miller, M.H. Corporate income taxes and the cost of capital: A correction. Am. Econ. Rev. 1963, 53, 433–443. [Google Scholar]

- Miller, M.H. Debt and taxes. J. Financ. 1977, 32, 261–276. [Google Scholar]

- Miller, M.H.; Modigliani, F. Dividend policy, growth and the valuation of shares. J. Bus. 1961, 34, 411–433. [Google Scholar] [CrossRef]

- Miller, M.H.; Modigliani, F. Some estimates of the cost of capital to the electric utility industry, 1954–1957. Am. Econ. Rev. 1966, 56, 333–391. [Google Scholar]

- Acharya, V.; Myers, S.C.; Rajan, R. The internal governance of firms. J. Financ. 2011, 66, 689–720. [Google Scholar] [CrossRef] [Green Version]

- Arrow, K.J. The role of securities in the optimal allocation of risk-bearing. Rev. Econ. Stud. 1964, 31, 91–96. [Google Scholar] [CrossRef]

- Asquith, P.; Mullins, D.W. Equity issues and offering dilution. J. Financ. Econ. 1986, 15, 61–89. [Google Scholar] [CrossRef]

- Baumol, W.; Panzar, J.G.; Willig, R.D. Contestable Markets and the Theory of Industry Structure; Harcourt College Publishers: New York, NY, USA, 1982. [Google Scholar]

- Black, F. Noise. J. Financ. 1986, 41, 529–543. [Google Scholar] [CrossRef]

- Becker, D.M. The difference between Modigliani–Miller and Miles–Ezzell and its consequences for the valuation of annuities. Cogent. Econ. Financ. 2021, 9, 1. [Google Scholar] [CrossRef]

- Berk, J.; DeMarzo, P. Corporate Finance; Pearson–Addison Wesley: Boston, MA, USA, 2007. [Google Scholar]

- Brealey, R.A.; Myers, S.C. Principles of Corporate Finance, 1st ed.; McGraw-Hill: New York, NY, USA, 1981. [Google Scholar]

- Brealey, R.A.; Myers, S.C.; Allen, F. Principles of Corporate Finance, 11th ed.; McGraw-Hill: New York, NY, USA, 2014. [Google Scholar]

- Bhattacharya, S. Project valuation with mean-reacting cash flows. J. Financ. 1978, 33, 1317–1331. [Google Scholar] [CrossRef]

- Filatova, Т.; Orehova, N.; Brusova, А. Weighted average cost of capital in the theory of Modigliani–Miller, modified for a finite life–time company. Bull FU 2008, 48, 68–77. [Google Scholar]

- Brusov, P.; Filatova, T.; Orehova, N.; Eskindarov, M. Modern Corporate Finance, Investments, Taxation and Ratings, 2nd ed.; Springer Nature Publishing: Cham, Switzerland, 2018; pp. 1–571. [Google Scholar]

- Brusov, P.; Filatova, T.; Eskindarov, M.; Orehova, N. Hidden global causes of the global financial crisis. J. Rev. Glob. Econ. 2012, 1, 106–111. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, P.; Orekhova, N. Absence of an optimal capital structure in the famous tradeoff theory! J. Rev. Glob. Econ. 2013, 2, 94–116. [Google Scholar] [CrossRef] [Green Version]

- Brusov, P.; Filatova, T.; Orehova, N. A qualitatively new effect in corporative finance: Abnormal dependence of cost of equity of company on leverage. J. Rev. Glob. Econ. 2013, 2, 183–193. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, P.; Orekhova, N. Mechanism of formation of the company optimal capital structure. different from suggested by trade off theory. Cogent Econ. Financ. 2014, 2, 1–13. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Orehova, N. Inflation in Brusov–Filatova–Orekhova theory and in its perpetuity limit–Modigliani–Miller theory. J. Rev. Glob. Econ. 2014, 3, 175–185. [Google Scholar] [CrossRef] [Green Version]

- Brusova, A. А comparison of the three methods of estimation of weighted average cost of capital and equity cost of company. Financ. Anal. Prob. Sol. 2011, 34, 36–42. [Google Scholar]

- Derrig, R. Theoretical considerations of the effect of federal income taxes on investment income in property-liability ratemaking. J. Risk Insur. 1994, 61, 691–709. [Google Scholar] [CrossRef]

- Diamond, D.A.; He, Z. A theory of debt maturity: The long and short of debt overhang. J. Financ. 2014, 69, 719–762. [Google Scholar] [CrossRef]

- Donaldson, G. Debt Capacity: A Study of Corporate Debt Policy and the Determination of Debt Capacity; Division of Research, Graduate School of Business Administration, Harvard University: Boston, MA, USA, 1961. [Google Scholar]

- Erel, I.; Myers, S.C.; Read, J.A., Jr. A theory of risk capital. J. Financ. Econ. 2015, 118, 620–635. [Google Scholar] [CrossRef]

- Fairley, W.B. Investment income and profit margins in property-liability insurance. Bell J. Econ. 1979, 10, 191–210. [Google Scholar] [CrossRef]

- Fama, E.F. Risk adjusted discount rates and capital budgeting under uncertainty. J. Financ. Econ. 1977, 5, 3–24. [Google Scholar] [CrossRef]

- Fama, E.F. Discounting under uncertainty. J. Bus. 1996, 69, 415–429. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K. Financing decisions: Who issues stock? J. Financ. Econ. 2005, 76, 549–582. [Google Scholar] [CrossRef]

- Farber, A.; Gillet, R.; Szafarz, A. A General Formula for the WACC. Int. J. Bus. 2006, 11, 211–218. [Google Scholar]

- Fernandez, P. A General Formula for the WACC: A Comment. Int. J. Bus. 2006, 11, 219. [Google Scholar]

- Fisher, F.M.; McGowan, J.J. On the misuse of accounting rates of return to infer monopoly profits. Am. Econ. Rev. 1983, 73, 82–97. [Google Scholar]

- Frank, M.Z.; Goyal, V.K. Testing the pecking order theory of capital structure. J. Financ. Econ. 2003, 67, 217–248. [Google Scholar] [CrossRef] [Green Version]

- Gordon, M.J.; Shapiro, E. Capital equipment analysis: The required rate of profit. Manag. Sci. 1956, 3, 102–110. [Google Scholar] [CrossRef] [Green Version]

- Graham, J.R.; Leary, M.T. A review of empirical capital structure research and directions for the future. Annu. Rev. Financ. Econ. 2011, 3, 309–345. [Google Scholar] [CrossRef]

- Hamada, R. Portfolio Analysis, Market Equilibrium, and Corporate Finance. J. Financ. 1969, 24, 13–31. [Google Scholar] [CrossRef]

- Harris, R.; Pringle, J. Risk–Adjusted Discount Rates—Extension form the Average–Risk Case. J. Financ. Res. 1985, 8, 237–244. [Google Scholar] [CrossRef]

- Hausman, J.; Myers, S.C. Regulating, U.S. railroads: The effects of sunk costs and asymmetric risk. J. Regul. Econ. 2002, 22, 287–310. [Google Scholar] [CrossRef]

- Healy, P.; Howe, C.; Myers, S.C. R&D accounting the tradeoff between relevance objectivity: A pharmaceutical industry simulation. J. Account. Res. 2002, 40, 677–710. [Google Scholar]

- Hirshleifer, J. Investment decision under uncertainty: Choice-theoretic approaches. Q. J. Econ. 1965, 79, 509–536. [Google Scholar] [CrossRef]

- Hirshleifer, J. Investment decision under certainty: Applications of the state-preference approach. Q. J. Econ. 1966, 80, 252–277. [Google Scholar] [CrossRef]

- Jensen, M.C. Agency costs of free cash flow, corporate finance and takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Jin, L.; Myers, S.C. R2 around the world: New theory and new tests. J. Financ. Econ. 2006, 79, 257–292. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, S.; Ruback, R. The valuation of cash flow forecasts: An empirical analysis. J. Financ. 1995, 50, 1059–1093. [Google Scholar] [CrossRef]

- Myers, S.C. Finance, Theoretical and Applied. Annu. Rev. Financ. Econ. 2015, 7, 1–34. [Google Scholar] [CrossRef] [Green Version]

- Keynes, J.M. The General Theory of Employment, Interest and Money; Macmillan: New York, NY, USA, 1936. [Google Scholar]

- Kolbe, A.L.; Tye, W.B.; Myers, S.C. Regulatory Risk: Economic Principles and Applications to Natural Gas Pipelines and Other Industries; Springer: New York, NY, USA, 1993. [Google Scholar]

- Lambrecht, B.; Myers, S.C. A theory of takeovers and disinvestment. J. Financ. 2007, 62, 809–845. [Google Scholar] [CrossRef]

- Lambrecht, B.; Myers, S.C. Debt and managerial rents in a real-options model of the firm. J. Financ. Econ. 2008, 89, 209–231. [Google Scholar] [CrossRef]

- Lambrecht, B.; Myers, S.C. A Lintner model of dividends and managerial rents. J. Financ. 2012, 67, 1761–1810. [Google Scholar] [CrossRef]

- Lambrecht, B.; Myers, S.C. The Dynamics of Investment, Payout and Debt; Working Paper; Massachusetts Institute of Technology: Cambridge, MA, USA, 2015. [Google Scholar]

- Lemmon, M.L.; Roberts, M.R.; Zender, J. Back to the beginning: Persistence and the cross-section of corporate capital structure. J. Financ. 2008, 63, 1575–1608. [Google Scholar] [CrossRef]

- Lemmon, M.L.; Zender, J. Debt capacity and tests of capital structure theories. J. Financ. Quant. Anal. 2010, 45, 1161–1187. [Google Scholar] [CrossRef] [Green Version]

- Lintner, J. Distribution of incomes of corporations between dividends, retained earnings and taxes. Am. Econ. Rev. 1956, 46, 97–113. [Google Scholar]

- Lintner, J. Optimal dividends and corporate growth under uncertainty. Q. J. Econ. 1965, 77, 59–95. [Google Scholar] [CrossRef]

- Majd, S.; Myers, S.C. Tax asymmetries and corporate income tax reform. In The Effects of Taxation on Capital Accumulation; Feldstein, M., Ed.; University of Chicago Press: Chicago, IL, USA, 1987; pp. 343–373. [Google Scholar]

- Peter, M. DeMarzo an Extension of the Modigliani-Miller Theorem to Stochastic Economies with Incomplete Markets and Fully Interdependent Securities. J. Econ. Theory 1988, 45, 353–369. [Google Scholar]

- Merton, R.C.; Perold, A.F. Theory of risk capital in financial firms. J. Appl. Corp. Financ. 1993, 6, 16–32. [Google Scholar] [CrossRef]

- Miles, J.; Ezzell, R. The weighted average cost of capital, perfect capital markets and project life: A clarification. J. Financ. Quant. Anal. 1980, 15, 719–730. [Google Scholar] [CrossRef]

- Morck, R.; Yeung, B.Y.; Yu, W. The information content on stock markets: Why do emerging markets have synchronous stock price movements? J. Financ. Econ. 2000, 58, 215–260. [Google Scholar] [CrossRef] [Green Version]

- Mullins, D.W., Jr. Communications Satellite Corp. Case Study 276195; Harvard Bus. Sch.: Cambridge, MA, USA, 1976. [Google Scholar]

- Myers, S.C. Effects of Uncertainty on the Valuation of Securities and the Financial Decisions of the Firm. Ph.D. Thesis, Stanford University, Stanford, CA, USA, 1967. [Google Scholar]

- Myers, S.C. A time-state-preference model of security valuation. J. Financ. Quant. Anal. 1968, 3, 1–33. [Google Scholar] [CrossRef]

- Myers, S.C. Procedures for capital budgeting under uncertainty. Ind. Manag. Rev. 1968, 9, 1–20. [Google Scholar]

- Myers, S.C. Application of finance theory to public utility rates cases. Bell J. Econ. 1972, 3, 58–97. [Google Scholar] [CrossRef]

- Myers, S.C. A simple model of firm behavior under regulation and uncertainty. Bell J. Econ. 1973, 4, 304–315. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C. On public utility regulation under uncertainty. In Risk and Regulated Firms; Howard, R.H., Ed.; Mich. State Univ. Div. Res. Grad. Sch. Bus.: East Lansing, MI, USA, 1973; pp. 32–46. [Google Scholar]

- Myers, S.C. Interactions of corporate financing and investment decisions: Implications for capital budgeting. J. Financ. 1974, 29, 1–25. [Google Scholar] [CrossRef]

- Myers, S.C. Capital structure. J. Econ. Perspect. 2001, 15, 81–102. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C. Finance theory and financial strategy. Interfaces 1984, 14, 126–137. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C. The capital structure puzzle. J. Financ. 1984, 39, 575–592. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C. Fuzzy efficiency. Inst. Investig. 1988, 8–9. [Google Scholar]

- Myers, S.C. Still searching for optimal capital structure. In Are the Distinctions between Debt and Equity Disappearing? Kopke, R.W., Rosengren, E.S., Eds.; Federal Reserve Bank: Boston, MA, USA, 1989; pp. 80–95. [Google Scholar]

- Myers, S.C. Financial architecture. Eur. Financ. Manag. 1999, 5, 133–141. [Google Scholar] [CrossRef]

- Myers, S.C. Outside equity. J. Financ. 2000, 55, 1005–1037. [Google Scholar] [CrossRef]

- Myers, S.C.; Cohn, R. A discounted cash flow approach to property-liability insurance rate regulation. In Fair Rate of Return in Property Liability Insurance; Cummings, J.D., Harrington, S., Eds.; Kluwer-Nijhoff: Dordrecht, The Netherlands, 1987; pp. 55–78. [Google Scholar]

- Myers, S.C.; Dill, D.A.; Bautista, A.J. Valuation of financial lease contracts. J. Financ. 1976, 31, 799–819. [Google Scholar] [CrossRef]

- Myers, S.C.; Howe, C. A Life Cycle Model of Pharmaceutical R&D; Working Paper; Progr. Pharm. Ind.; Massachusetts Institute of Technology: Cambridge, MA, USA, 1997. [Google Scholar]

- Myers, S.C.; Kolbe, A.L.; Tye, W.B. Regulation and capital formation in the oil pipeline industry. Transp. J. 1984, 23, 25–49. [Google Scholar]

- Myers, S.C.; Kolbe, A.L.; Tye, W.B. Inflation and rate of return regulation. Res. Transp. Econ. 1985, 2, 83–119. [Google Scholar]

- Myers, S.C.; Majd, S. Abandonment value and project life. In Advances in Futures and Options Research; Fabozzi, F., Ed.; JAI: Greenwich, CT, USA, 1990; Volume 4, pp. 1–21. [Google Scholar]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C.; Pogue, G.A. A programming approach to corporate financial management. J. Financ. 1974, 29, 579–599. [Google Scholar] [CrossRef]

- Myers, S.C.; Rajan, R. The paradox of liquidity. Q. J. Econ. 1998, 113, 733–771. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C.; Read, J.A., Jr. Capital allocation for insurance companies. J. Risk Insur. 2001, 68, 545–580. [Google Scholar] [CrossRef]

- Myers, S.C.; Read, J.A., Jr. Real Options, Taxes and Leverage; Working Paper; Massachusetts Institute of Technology: Cambridge, MA, USA, 2014. [Google Scholar]

- Myers, S.C.; Shyam-Sunder, L. Measuring pharmaceutical industry risk and the cost of capital. In Competitive Strategies in the Pharmaceutical Industry; Helms, R.B., Ed.; American Enterpise Institute: Washington, DC, USA, 1996; pp. 208–237. [Google Scholar]

- Myers, S.C.; Turnbull, S.M. Capital budgeting and the capital asset pricing model: Good news and bad news. J. Financ. 1977, 32, 321–333. [Google Scholar] [CrossRef]

- Robichek, A.A.; Myers, S.C. Optimal Financing Decisions; Prentice-Hall: Upper Saddle River, NJ, USA, 1965. [Google Scholar]

- Robichek, A.A.; Myers, S.C. Conceptual problems in the use of risk-adjusted discount rates. J. Financ. 1966, 21, 727–730. [Google Scholar]

- Robichek, A.A.; Myers, S.C. Problems in the theory of optimal capital structure. J. Financ. Quant. Anal. 1966, 1, 1–35. [Google Scholar] [CrossRef]

- Robichek, A.A.; Myers, S.C. Valuation of the firm: Effects of uncertainty in a market context. J. Financ. 1966, 21, 215–227. [Google Scholar] [CrossRef]

- Rosenbaum, J.; Pearl, J. Investment Banking, 2nd ed.; Wiley: New York, NY, USA, 2013. [Google Scholar]

- Sethi, S.; Derzko, N.A.; Lehoczky, J.P. A Stochastic Extension of the Miller-Modigliani Framework. Math. Financ. 1991, 1, 57–76. Available online: https://ssrn.com/abstract=1082940 (accessed on 21 December 2021). [CrossRef]

- Schwartz, E. The theory of the capital structure of the firm. J. Financ. 1959, 14, 18–39. [Google Scholar]

- Sharpe, W.F. Capital asset prices: A theory of market equilibrium under conditions of risk. J. Financ. 1965, 19, 425–442. [Google Scholar]

- Shleifer, A.; Summers, L.H. Breach of trust in hostile takeovers. In Corporate Takeovers: Causes and Consequences; Auerbach, A.J., Ed.; University of Chicago Press: Chicago, IL, USA, 1988; pp. 33–56. [Google Scholar]

- Shyam-Sunder, L.; Myers, S.C. Testing static tradeoff against pecking order models of capital structure. J. Financ. Econ. 1999, 51, 219–244. [Google Scholar] [CrossRef]

- Skinner, D.J. The evolving relation between earnings, dividends and stock repurchases. J. Financ. Econ. 2008, 87, 582–609. [Google Scholar] [CrossRef]

- Solomon, E.; Laya, J. Measurement of company profitability: Some systematic errors in the accounting rate of return. In Financial Research and Management Decisions; Robichek, A.A., Ed.; Wiley: New York, NY, USA, 1967; pp. 152–183. [Google Scholar]

- Van Horne, J. Capital budgeting decisions involving combinations of risky assets. Manag. Sci. 1966, 19, B84–B92. [Google Scholar] [CrossRef]

- Williams, J.B. The Theory of Investment Value; Harvard University Press: Cambridge, MA, USA, 1938. [Google Scholar]

- Brusov, P.N.; Filatova, T.V.; Orekhova, N.P.; Kulik, V.L.; Chang, S.I.; Lin, Y.C.G. Modification of the Modigliani–Miller Theory for the Case of Advance Payments of Tax on Profit. J. Rev. Glob. Econ. 2020, 9, 257–267. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Orekhova, N.; Kulik, V.; Chang, S.-I.; Lin, Y. Application of the Modigliani–Miller Theory, Modified for the Case of Advance Payments of Tax on Profit, in Rating Methodologies. J. Rev. Glob. Econ. 2020, 9, 282–292. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Chang, S.-I.; Lin, G. Innovative investment models with frequent payments of tax on income and of interest on debt. Mathematics 2021, 9, 1491. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Orekhova, N.; Kulik, V.; Chang, S.-I.; Lin, G. Generalization of the Modigliani–Miller theory for the case of variable profit. Mathematics 2021, 9, 1286. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T. The Modigliani–Miller theory with arbitrary frequency of payment of tax on profit. Mathematics 2021, 9, 1198. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Orekhova, N.; Kulik, V.; Chang, S.-I.; Lin, G. The Generalization of the Brusov–Filatova–Orekhova Theory for the Case of Payments of Tax on Profit with Arbitrary Frequency. Mathematics 2022, 10, 1343. [Google Scholar] [CrossRef]

- Brusov, P.; Filatova, T.; Kulik, V. Benefits of Advance Payments of Tax on Profit: Consideration within the Brusov–Filatova–Orekhova (BFO) Theory. Mathematics 2022, 10, 2013. [Google Scholar] [CrossRef]

- Peter, B.; Tatiana, F. Influence of Method and Frequency of Profit Tax Payments on Company Financial Indicators. Mathematics 2022, 10, 2479. [Google Scholar] [CrossRef]

- Peter, B.; Tatiana, F. Generalization of the Brusov–Filatova–Orekhova Theory for the Case of Variable Income. Mathematics 2022, 10, 3661. [Google Scholar] [CrossRef]

- Filatova, T.; Brusov, P.; Orekhova, N. Impact of Advance Payments of Tax on Profit on Effectiveness of Investments. Mathematics 2022, 10, 666. [Google Scholar] [CrossRef]

- Stiglitz, J. A Re–examination of the Modigliani–Miller Theorem. Am. Econ. Rev. 1969, 59, 784–793. [Google Scholar]

- Rubinstein, M. A Mean–Variance Synthesis of Corporate Financial Theory. J. Financ. 1973, 28, 167–181. [Google Scholar] [CrossRef]

- Hsia, С. Coherence of the Modern Theories of Finance. Financ. Rev. 1981, 16, 27–42. [Google Scholar] [CrossRef]

- Cooper, I.; Nyborg, K.G. Consistent valuation of project finance and LBO’s using the flow-to-equity method. Eur. Financ. Manag. 2018, 24, 34–52. [Google Scholar] [CrossRef]

- Brennan, M.; Schwartz, E. Corporate Income Taxes, Valuation, and the Problem of Optimal Capital Structure. J. Bus. 1978, 51, 103–114. [Google Scholar] [CrossRef]

- Leland, H. Corporate Debt Value, Bond Covenants, and Optimal Capital Structure. J. Financ. 1994, 49, 1213–1252. [Google Scholar] [CrossRef]

- Brennan, M.; Schwartz, E. Optimal Financial Policy and Firm Valuation. J. Financ. 1984, 39, 593–607. [Google Scholar] [CrossRef]

- Kane, A.; Marcus, A.; McDonald, R. How Big is the Tax Advantage to Debt? J. Financ. 1984, 39, 841–853. [Google Scholar] [CrossRef]

Figure 1.

The historical development of the theory of capital structure from the empirical traditional approach (TA) to the general theory of capital structure, BFO (Brusov–Filatova–Orekhova), through the perpetuity Modigliani–Miller theory.

Figure 1.

The historical development of the theory of capital structure from the empirical traditional approach (TA) to the general theory of capital structure, BFO (Brusov–Filatova–Orekhova), through the perpetuity Modigliani–Miller theory.

Figure 2.

Only two results for the capital structure of the company were known before the BFO theory: Modigliani–Miller (MM) for perpetual companies and Myers for one-year companies, while the newly created BFO theory filled the entire interval between n = 1 and .

Figure 2.

Only two results for the capital structure of the company were known before the BFO theory: Modigliani–Miller (MM) for perpetual companies and Myers for one-year companies, while the newly created BFO theory filled the entire interval between n = 1 and .

Figure 3.

Dependence of WACC on L.

Figure 4.

Dependence of equity cost ke on L.

Figure 5.

Dependence of equity cost ke, debt cost kd, and WACC on leverage L.

Figure 6.

Dependence of WACC on leverage level for n = 1, n = 3, and .

Figure 7.

Dependence of the equity cost and the weighted average cost of capital on leverage in the Modigliani–Miller theory without taxing under inflation. It is seen that the growing rate of equity costs increases with leverage. Axis y means capital costs–CC.

Figure 7.

Dependence of the equity cost and the weighted average cost of capital on leverage in the Modigliani–Miller theory without taxing under inflation. It is seen that the growing rate of equity costs increases with leverage. Axis y means capital costs–CC.

Figure 8.

Dependence of the weighted average cost of capital WACC on debt fraction wd at different inflation rate α (1, α = 3%; 2, α = 5%; 3, α = 7%; and 4, α = 9%) for a 5-year company.

Figure 8.

Dependence of the weighted average cost of capital WACC on debt fraction wd at different inflation rate α (1, α = 3%; 2, α = 5%; 3, α = 7%; and 4, α = 9%) for a 5-year company.

Figure 9.

Two types of dependences of WACC, and company value, V, on the company age n.

Figure 10.

The dependence of WACC on leverage level, L, at different company ages n (n = 1, 3, and 49).

Figure 10.

The dependence of WACC on leverage level, L, at different company ages n (n = 1, 3, and 49).

Figure 11.

The dependence of WACC on the leverage level, L, at different company ages n (n = 1, 3, and 45).

Figure 11.

The dependence of WACC on the leverage level, L, at different company ages n (n = 1, 3, and 45).

Figure 12.

Dependence of WACC on company age n: company “golden age” (curve 1) and company “silver age” (curve 2) under the existence of the “Kulik” effect, where n0 is the company “golden (silver) age” and n1 is the company age of local maximum in the dependence of WACC(n).

Figure 12.

Dependence of WACC on company age n: company “golden age” (curve 1) and company “silver age” (curve 2) under the existence of the “Kulik” effect, where n0 is the company “golden (silver) age” and n1 is the company age of local maximum in the dependence of WACC(n).

Figure 13.

Dependence of equity cost, , on leverage level L at different tax on income rate T. () (1—; 2—; 3—; 4—; 5—; 6—).

Figure 13.