A Linear Mixed Model Approach for Determining the Effect of Financial Inclusion on Bank Stability: Comparative Empirical Evidence for Islamic and Conventional Banks in Kuwait

,

,  and

and

Abstract

1. Introduction

2. Literature Review

3. Research Methodology

3.1. Sample and Data

3.2. Variables Construction and Measurement

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Control Variables

3.3. Linear Mixed Model (LMM)

3.4. Robustness of the Results

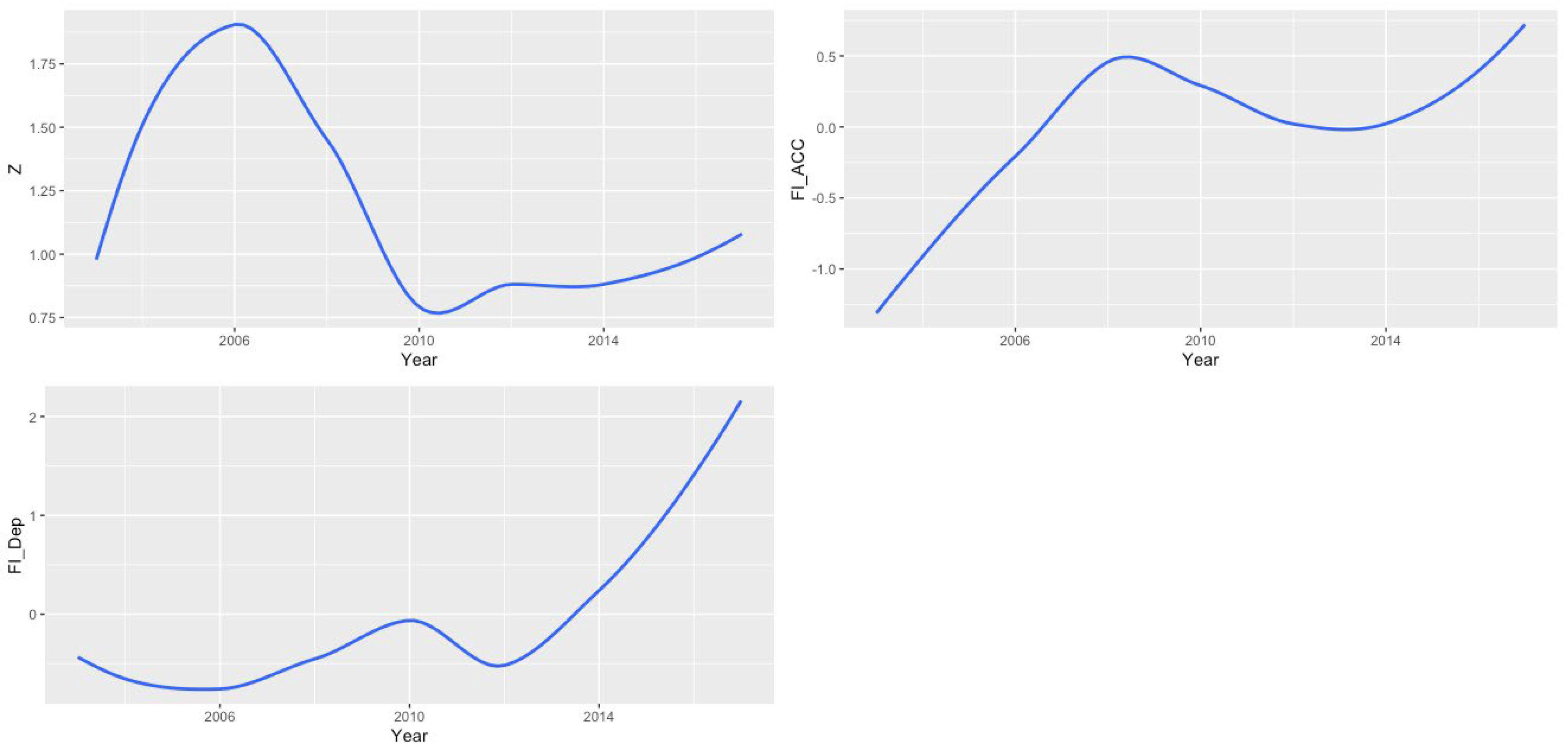

4. Empirical Results

4.1. Descriptive Statistics and Correlations

4.2. Main Findings

4.3. Robustness of the Model

4.4. Financial Crisis

5. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Demirguc-Kunt, A.; Klapper, L.; Singer, D. Financial Inclusion and Inclusive Growth: A Review of Recent Empirical Evidence; Policy Research Working Paper Series 8040; The World Bank: Washington, DC, USA, 2017; Available online: http://documents.worldbank.org/curated/en/403611493134249446/pdf/WPS8040.pdf (accessed on 15 February 2023).

- Le, T.; Chuc, A.; Taghizadeh-Hesary, F. Financial inclusion and its impact on financial efficiency and sustainability: Empirical evidence from Asia. Borsa Istanb. Rev. 2019, 19, 310–322. [Google Scholar] [CrossRef]

- Babajide, A.; Adegboye, F.; Omankhanlen, A. Financial inclusion and economic growth in Nigeria. Int. J. Econ. Financ. Issues 2015, 5, 629–637. [Google Scholar]

- Machdar, N. Financial inclusion, financial stability and sustainability in the banking sector: The case of Indonesia. Int. J. Econ. Bus. Adm. 2020, 5, 193–202. [Google Scholar]

- Morgan, P.; Pontines, V. Financial Stability and Financial Inclusion; SSRN Scholarly Paper ID 2464018; Social Science Research Network: Rochester, NY, USA, 2014. [Google Scholar] [CrossRef]

- Neaime, S.; Gaysset, I. Financial inclusion and stability in MENA: Evidence from poverty and inequality. Financ. Res. Lett. 2018, 24, 230–237. [Google Scholar] [CrossRef]

- Arora, R. The links between financial inclusion and financial stability: A study of BRICS. In The Oxford Handbook of BRICS and Emerging Economies; Anand, P., Comim, F., Fennell, S., Weiss, J., Eds.; Oxford University Press: New York, NY, USA, 2018. [Google Scholar]

- Danisman, G.O.; Tarazi, A. Financial inclusion and bank stability: Evidence from Europe. Eur. J. Financ. 2020, 26, 1842–1855. [Google Scholar] [CrossRef]

- Han, R.; Martin, M. Financial Inclusion for Financial Stability: Access to Bank Deposits and the Growth of Deposits in the Global Fi-nancial Crisis; WPS6577; The World Bank: Washington, DC, USA, 2013; Available online: http://documents.worldbank.org/curated/en/850681468325448388/Financialinclusion-for-financial-stability-access-to-bank-deposits-and-the-growth-of-deposits-in-theGlobal-Financial-Crisis (accessed on 15 February 2023).

- Mehrotra, A.; James, Y. Financial Inclusion and Optimal Monetary Policy; SSRN Scholarly Paper ID 2542220; Social Science Research Network: Rochester, NY, USA, 2014; Available online: https://papers.ssrn.com/abstract=2542220 (accessed on 15 February 2023).

- Mehrotra, A.; Yetman, J. Financial inclusion-issues for central banks. In BIS Quarterly Review; Department for Business Innovation and Skills: London, UK, 2015. [Google Scholar]

- Ratna, S.; Martin, C.; Papa, N.; Adolfo, B.; Srobona, M.; Annette, K.; Yen, N.; Seyed, R. Financial Inclusion; Can It Meet Multiple Macroeconomic Goals? 15/17. IMF Staff Discussion Notes; International Monetary Fund: Washington, DC, USA, 2015; Available online: https://ideas.repec.org/p/imf/imfsdn/15-17.html (accessed on 20 March 2023).

- Bachas, P.; Paul, G.; Sean, H.; Enrique, S. How Debit Cards Enable the Poor to Save More; Working Paper 23252. Working Paper Series; National Bureau of Economic Research: Cambridge, MA, USA, 2017. [Google Scholar] [CrossRef]

- Khan, H. Financial Inclusion and Financial Stability: Are They Two Sides of the Same Coin? In Address by Shri H. R. Khan, Deputy Governor of the Reserve Bank of India, at BANCON; Indian Bankers Association: Mumbai, India; Indian Overseas Bank: Chennai, India, 2011. [Google Scholar]

- De la Torre AErik, F.; Alain, I. Financial development: Structure and dynamics. World Bank Econ. Rev. 2013, 27, 514–541. [Google Scholar]

- Cihak, M.; Davide, S.; Martin, M. The Nexus of Financial Inclusion and Financial Stability: A Study of Trade-Offs and Synergies; WPS7722; The World Bank: Washington, DC, USA, 2016; Available online: http://documents.worldbank.org/curated/en/138991467994676130/The-Nexusof-financial-inclusion-and-financial-stability-a-study-of-trade-offs-and-synergies (accessed on 15 February 2023).

- De la Torre, A.; Ize, A.; Schmukler, L. Financial Development in Latin America and the Caribbean: The Road Ahead; The World Bank: Washington, DC, USA, 2011. [Google Scholar]

- García, R.; Jose, M. Can financial inclusion and financial stability go hand in hand? Econ. Issues 2016, 21, 81–103. [Google Scholar]

- Gourène, A.; Mendy, P. Financial Inclusion and Economic Growth in WAEMU: A Multiscale Heterogeneity Panel Causality Approach. Munich Personal RePEc Archive (MPRA). 2017. Available online: https://mpra.ub.uni-muenchen.de/82251/ (accessed on 15 February 2023).

- Okoye, U.; Adetiloye, A.; Erin, O.; Modebe, N. Financial Inclusion as a Strategy for Enhanced Economic Growth and Development. J. Internet Bank. Commer. 2017, 22 (Suppl. S8), 1–14. [Google Scholar]

- Solovjova, I.; Rupeika-Apoga, R.; Romanova, I. Competitiveness Enhancement of International Financial Centers. Eur. Res. Stud. J. 2018, 21, 5–17. [Google Scholar] [CrossRef] [PubMed]

- Sharma, D. Nexus between financial inclusion and economic growth: Evidence from the emerging Indian economy. J. Financ. Econ. Policy 2016, 8, 13–36. [Google Scholar] [CrossRef]

- Kim, W.; Yu, S.; Hassan, K. Financial inclusion and economic growth in OIC countries. Res. Int. Bus. Financ. 2018, 43, 1–14. [Google Scholar] [CrossRef]

- Laeven, L.; Levine, R. Bank governance, regulation and risk taking. J. Financ. Econ. 2009, 93, 259–275. [Google Scholar] [CrossRef]

- Fang., Y.; Hasan., I.; Marton, K. Institutional development and bank stability: Evidence from transition countries. J. Bank. Financ. 2014, 39, 160–176. [Google Scholar] [CrossRef]

- Ahamed, M.M.; Mallick, S.K. Is financial inclusion good for bank stability? International evidence. J. Econ. Behav. Organ. 2019, 157, 403–427. [Google Scholar] [CrossRef]

- Pham, T.T.; Dao, L.K.; Nguyen, V.C. The determinants of bank’s stability: A system GMM panel analysis. Cogent Bus. Manag. 2021, 8, 1963390. [Google Scholar] [CrossRef]

- Ali, M.; Puah, C.H. Does bank size and funding risk effect banks’ stability? A lesson from Pakistan. Glob. Bus. Rev. 2018, 19, 1166–1186. [Google Scholar] [CrossRef]

- Ramzan, M.; Amin, M.; Abbas, M. How does corporate social responsibility affect financial performance, financial stability, and financial inclusion in the banking sector? Evidence from Pakistan. Res. Int. Bus. Financ. 2021, 55, 101314. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Merrouche, O. Islamic vs. conventional banking: Business model, efficiency and stability. J. Bank. Financ 2013, 37, 433–447. [Google Scholar] [CrossRef]

- Lenka, S.K.; Bairwa, A.K. Does financial inclusion affect monetary policy in SAARC countries? Cogent Econ. Financ. 2016, 4, 1127011. [Google Scholar] [CrossRef]

- Sarma, M. Measuring Financial Inclusion for Asian Economies. Financial Inclusion in Asia: Issues and Policy Concerns; Palgrave Macmillan: London, UK, 2016. [Google Scholar]

- Wang., X.; Guan, J. Financial inclusion: Measurement, spatial effects and influencing factors. Appl. Econ. 2017, 49, 1751–1762. [Google Scholar] [CrossRef]

- Ang, J.B.; McKibbin, W.J. Financial liberalization, financial sector development and growth: Evidence from Malaysia. J. Dev. Econ. 2007, 84, 215–233. [Google Scholar] [CrossRef]

- Adu, G.; Marbuah, G.; Mensah, J.T. Financial development and economic growth in Ghana: Does the measure of financial development matter? Rev. Dev. Financ. 2013, 3, 192–203. [Google Scholar] [CrossRef]

- Tram, T.X.; Lai, T.D.; Nguyen, T.T. Constructing a composite financial inclusion index for developing economies. Q. Rev. Econ. Financ. 2021, 87, 257–265. [Google Scholar] [CrossRef]

- Gupta, J.; Kashiramka, S. Financial stability of banks in India: Does liquidity creation matter? Pac.-Basin Financ. J. 2020, 64, 101439. [Google Scholar] [CrossRef]

- Ariff, M.; Shawtari, F.A. Efficiency, asset quality and stability of the banking sector in Malaysia. Malays. J. Econ. Stud. 2019, 56, 107–137. [Google Scholar] [CrossRef]

- Claeys., S.; Vander Vennet, R. Determinants of bank interest margins in Central and Eastern Europe: A comparison with the West. Econ. Syst. 2008, 32, 197–216. [Google Scholar] [CrossRef]

- Nguyen., M.; Skully, M.; Perera, S. Market power, revenue diversification and bank stability: Evidence from selected South Asian countries. J. Int. Financ. Mark. Inst. Money 2012, 22, 897–912. [Google Scholar] [CrossRef]

- Morris, C.N. Hierarchical models for educational data: An overview. J. Educ. Behav. Stat. 1995, 20, 190–200. [Google Scholar] [CrossRef]

- Kreft, I.G. Are Multilevel Techniques Necessary? An Overview, Including Simulation Studies; California State University Press: Los Angeles, CA, USA, 1996. [Google Scholar]

- Mundfrom, D.J.; Schultz, M.R. A Monte Carlo simulation comparing parameter estimates from multiple linear regression and hierarchical linear modeling. Mult. Linear Regres. Viewp. 2002, 28, 18–21. [Google Scholar]

- Raudenbush, S.W.; Bryk, A.S. Hierarchical Linear Models: Applications and Data Analysis Methods, 2nd ed.; Sage: Newbury Park, CA, USA, 2022; Volume 1. [Google Scholar]

- Tabachnick, B.G.; Fidell, L.S. Using Multivariate Statistics (5th ed.). 2007. Available online: http://library.wur.nl/WebQuery/clc/1828941 (accessed on 20 December 2019).

- Field, A. Discovering Statistics Using IBM SPSS Statistics; Sage: London, UK, 2013. [Google Scholar]

- Bani-Mustafa, A.; Matawie, M.; Finch, F.; Al-Nasser, A.; Ciavolino, E. Recursive residuals for linear mixed models. Qual. Quant. 2019, 53, 1263–1274. [Google Scholar] [CrossRef]

- Oskrochi, G.; Bani-Mustafa, A.; Oskrochi, Y. Factors affecting psychological well-being: Evidence from two nationally repre-sentative surveys. PLoS ONE 2018, 13, e0198638. [Google Scholar] [CrossRef] [PubMed]

- Hox, J. Multilevel Analysis: Techniques and Applications, 2nd ed.; Routledge: New York, NY, USA, 2010. [Google Scholar]

- Shek, T.; Ma, C. Longitudinal data analyses using linear mixed models in SPSS: Concepts, procedures and illustrations. Sci. World J. 2011, 11, 42–76. [Google Scholar] [CrossRef] [PubMed]

- Laird, M.; Ware, H. Random-effects models for longitudinal data. Biometrics 1982, 38, 963–974. [Google Scholar] [CrossRef]

- Newman, D.; Newman, I.; Salzman, J. Comparing OLS and HLM models and the questions they answer: Potential concerns for type VI errors. Mult. Linear Regres. Viewp. 2010, 36, 1–8. [Google Scholar]

- Yamen, A.; Allam, A.; Bani-Mustafa, A.; Uyar, A. Impact of institutional environment quality on tax evasion: A comparative investigation of old versus new EU members. J. Int. Account. Audit. Tax. 2018, 32, 17–29. [Google Scholar] [CrossRef]

- Bell, A.; Fairbrother, M.; Jones, K. Fixed and Random effects models: Making an informed choice. Qual. Quant. 2019, 53, 1051–1074. [Google Scholar] [CrossRef]

- Hegyi, G.; Garamszegi, Z. Using information theory as a substitute for stepwise regression in ecology and behavior. Behav. Ecol. Sociobiol. 2011, 65, 69–76. [Google Scholar] [CrossRef]

- Haque, F. The effects of board characteristics and sustainable compensation policy on carbon performance of UK firms. Br. Account. Rev. 2017, 49, 347–364. [Google Scholar] [CrossRef]

- Luo, L.; Lan, Y.-C.; Tang, Q. Corporate incentives to disclose carbon information: Evidence from the CDP Global 500 report. J. Int. Financ. Manag. Account. 2012, 23, 93–120. [Google Scholar] [CrossRef]

- Wang, R.; Luo, H.R. How does financial inclusion affect bank stability in emerging economies? Emerg. Mark. Rev. 2021, 51, 100876. [Google Scholar] [CrossRef]

- Kim, H.; Batten, J.A.; Ryu, D. Financial crisis, bank diversification, and financial stability: OECD countries. Int. Rev. Econ. Financ. 2020, 65, 94–104. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Index | Variables |

|---|---|

| Financial inclusion– access | Bank accounts per 1000 adults (demographic penetration) ATMs per 100,000 adults (demographic penetration) Bank branches per 100,000 adults (demographic penetration) |

| Financial inclusion– depth | Bank deposits (usage) Private sector credit (usage) Liquid assets (usage) |

| Variables * | Measurement | Source |

|---|---|---|

| Dependent: | ||

| Z score | ((ROA + Equity)/Assets))/Standard Deviation (ROA) | Authors’ calculations |

| Independent: | ||

| Financial inclusion– access | Index using PCA | World Bank |

| Financial inclusion–depth | Index using PCA | World Bank |

| Control: | ||

| TA | Total assets of the banks | DataStream |

| LLP | Loan/finance loss provisions to total loans | DataStream |

| BL | Bank loans to total assets | DataStream |

| EA | Earnings assets to total assets | DataStream |

| EQ | Equity to total assets | DataStream |

| NII | Non-interest income | DataStream |

| GDP | Gross domestic per capita | DataStream |

| ROA | Net income to total assets–return on assets | DataStream |

| Eff | Overhead costs to total assets | DataStream |

| Variable | Category | N | Mean | StDev | Median | Min | Max |

|---|---|---|---|---|---|---|---|

| Bank Stability | Islamic | 65 | 0.92 | 0.73 | 0.92 | −0.99 | 2.76 |

| Conventional | 74 | 1.46 | 1.43 | 1.11 | −5.22 | 4.98 | |

| Total | 139 | 1.21 | 1.18 | 0.99 | −5.22 | 4.98 | |

| FI_Access | Islamic | 65 | 25.02 | 6.37 | 26.57 | 0 | 31.06 |

| Conventional | 74 | 24.45 | 6.75 | 26.46 | 0 | 31.06 | |

| Total | 139 | 24.71 | 6.56 | 26.46 | 0 | 31.06 | |

| FI_Dep | Islamic | 65 | 69.88 | 18.03 | 61.42 | 48.36 | 103.06 |

| Conventional | 74 | 68.72 | 17.5 | 61.42 | 48.36 | 103.06 | |

| Total | 139 | 69.26 | 17.7 | 61.42 | 48.36 | 103.06 | |

| TA | 139 | 17,645,803.1 | 17,991,941.03 | 11,946,303 | 435,970 | 86,266,514 | |

| LLP | 139 | 0.01 | 0.01 | 0.01 | -0.01 | 0.08 | |

| BL | 139 | 0.74 | 0.1 | 0.74 | 0.4 | 0.93 | |

| EA | 133 | 83.27 | 26.5 | 92.71 | 5.56 | 97.45 | |

| EQ | 139 | 0.17 | 0.09 | 0.15 | 0.02 | 0.8 | |

| NII | 139 | 0.01 | 0.01 | 0.01 | −0.01 | 0.03 | |

| GDP | 139 | 39,472.4 | 9760 | 38,577.5 | 22,148.38 | 55,494.95 | |

| ROA | 139 | 1.42 | 1.23 | 1.3 | −6.87 | 4.21 | |

| Eff | 139 | 1.13 | 0.08 | 1.14 | 0.95 | 1.24 | |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||||

| −0.221 ** | 1 | |||||||||

| −0.236 ** | 0.339 ** | 1 | ||||||||

| 0.229 ** | 0.191 * | 0.209 * | 1 | |||||||

| −0.572 ** | 0.179 * | 0.075 | 0.104 | 1 | ||||||

| −0.079 | 0.200 * | 0.023 | −0.504 ** | −0.116 | 1 | |||||

| 0.012 | −0.021 | −0.027 | −0.489 ** | −0.159 | 0.710 ** | 1 | ||||

| −0.003 | −0.072 | −0.044 | −0.148 | −0.164 | −0.033 | 0.009 | 1 | |||

| 0.387 ** | −0.119 | −0.373 ** | 0.166 | −0.09 | −0.460 ** | −0.420 ** | −0.05 | 1 | ||

| 0.007 | 0.284 ** | −0.608 ** | 0.041 | 0.216 * | 0.186 * | −0.047 | 0.005 | 0.136 | 1 | |

| 0.880 ** | −0.273 ** | −0.317 ** | 0.001 | −0.645 ** | −0.115 | −0.026 | 0.039 | 0.511 ** | −0.085 | 1 |

| −0.123 | 0.432 ** | 0.252 ** | 0.176 * | 0.239 ** | 0.131 | −0.074 | 0.044 | −0.168 * | 0.336 ** | −0.269 ** |

| Fixed Effects | Model 1 | VIF |

|---|---|---|

| (Intercept) | 0.27 (0.66) | |

| Time | 3.19 **** (0.35) | |

| 0.62 *** (0.2) | ||

| 2.07 **** (0.23) | ||

| FI_ACC | −0.25 **** (0.04) | 1.8 |

| FI_Dep | −0.07 (0.04) | 3.9 |

| Eff | −0.74 (0.46) | 2.4 |

| TA_Z | −0.15 ** (0.06) | 2.2 |

| BL | −0.89 * (0.53) | 1.9 |

| EQ | −0.61 * (0.35) | 1.2 |

| NII | −15.24 ** (7.29) | 2.0 |

| ROA | 0.84 **** (0.03) | 1.8 |

| Random component standard deviation | ||

| Intercept | 0.49 *** | |

| Residuals | 0.25 | |

| AIC | 77.22 | |

| Fixed Effects | Islamic Banks | Conventional Banks |

|---|---|---|

| (Intercept) | 0.04 (0.64) | −0.92 ** (0.35) |

| Time | 2.19 **** (0.42) | 3.43 **** (0.32) |

| 0.55 ** (0.25) | 0.66 *** (0.22) | |

| 1.67 **** (0.23) | 1.82 **** (0.19) | |

| FI_ACC | −0.24 **** (0.06) | −0.27 **** (0.05) |

| FI_Dep | NS | NS |

| Eff | −1.13 * (0.62) | NS |

| TA_Z | NS | −0.22 *** (0.06) |

| BL | NS | NS |

| EQ | NS | NS |

| NII | NS | −36.21 ** (13.94) |

| ROA | 0.79 **** (0.05) | 0.89 **** (0.03) |

| Random component standard deviation | ||

| Intercept | 0.199 *** | 0.63 |

| Residuals | 0.21 | 0.23 |

| AIC | 16.5 | 35.65 |

| Fixed Effects | Full Model—All Banks | Islamic Banks | Conventional Banks |

|---|---|---|---|

| (Intercept) | 0.28 (0.65) | 0.19 (0.61) | −0.92 ** (0.35) |

| Time | 3.43 **** (0.35) | 2.53 **** (0.42) | 3.43 **** (0.32) |

| 1.13 **** (0.27) | 1.2 **** (0.34) | 0.66 *** (0.22) | |

| 2.21 **** (0.23) | 2.1 **** (0.27) | 1.82 **** (0.19) | |

| FI_ACC | −0.24 **** (0.04) | −0.22 **** (0.06) | −0.27 **** (0.05) |

| FI_Dep | NS | NS | NS |

| Financial Crisis | −0.31 ** (0.13) | −0.43 ** (0.16) | NS |

| Eff | NS | NS | NS |

| TA_Z | −0.16 *** (0.06) | NS | −0.22 **** (0.06) |

| BL | −0.98 * (0.53) | NS | NS |

| EQ | −0.59 * (0.35) | NS | NS |

| NII | −14.22 ** (7.17) | NS | −36.21 ** (13.94) |

| ROA | 0.82 **** (0.03) | 0.74 **** (0.05) | 0.89 **** (0.03) |

| Random component standard deviation | |||

| Intercept | 0.5 | 0.22 *** | 0.63 |

| Residuals | 0.25 | 0.21 | 0.23 |

| AIC | 73.7 | 18.2 | 35.65 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Damrah, S.; Elian, M.I.; Atyeh, M.; Shawtari, F.A.; Bani-Mustafa, A. A Linear Mixed Model Approach for Determining the Effect of Financial Inclusion on Bank Stability: Comparative Empirical Evidence for Islamic and Conventional Banks in Kuwait. Mathematics 2023, 11, 1698. https://doi.org/10.3390/math11071698

Damrah S, Elian MI, Atyeh M, Shawtari FA, Bani-Mustafa A. A Linear Mixed Model Approach for Determining the Effect of Financial Inclusion on Bank Stability: Comparative Empirical Evidence for Islamic and Conventional Banks in Kuwait. Mathematics. 2023; 11(7):1698. https://doi.org/10.3390/math11071698

Chicago/Turabian StyleDamrah, Sadeq, Mohammad I. Elian, Mohamad Atyeh, Fekri Ali Shawtari, and Ahmed Bani-Mustafa. 2023. "A Linear Mixed Model Approach for Determining the Effect of Financial Inclusion on Bank Stability: Comparative Empirical Evidence for Islamic and Conventional Banks in Kuwait" Mathematics 11, no. 7: 1698. https://doi.org/10.3390/math11071698

APA StyleDamrah, S., Elian, M. I., Atyeh, M., Shawtari, F. A., & Bani-Mustafa, A. (2023). A Linear Mixed Model Approach for Determining the Effect of Financial Inclusion on Bank Stability: Comparative Empirical Evidence for Islamic and Conventional Banks in Kuwait. Mathematics, 11(7), 1698. https://doi.org/10.3390/math11071698