A Note on a Generalized Gerber–Shiu Discounted Penalty Function for a Compound Poisson Risk Model

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Recursion Calculation of

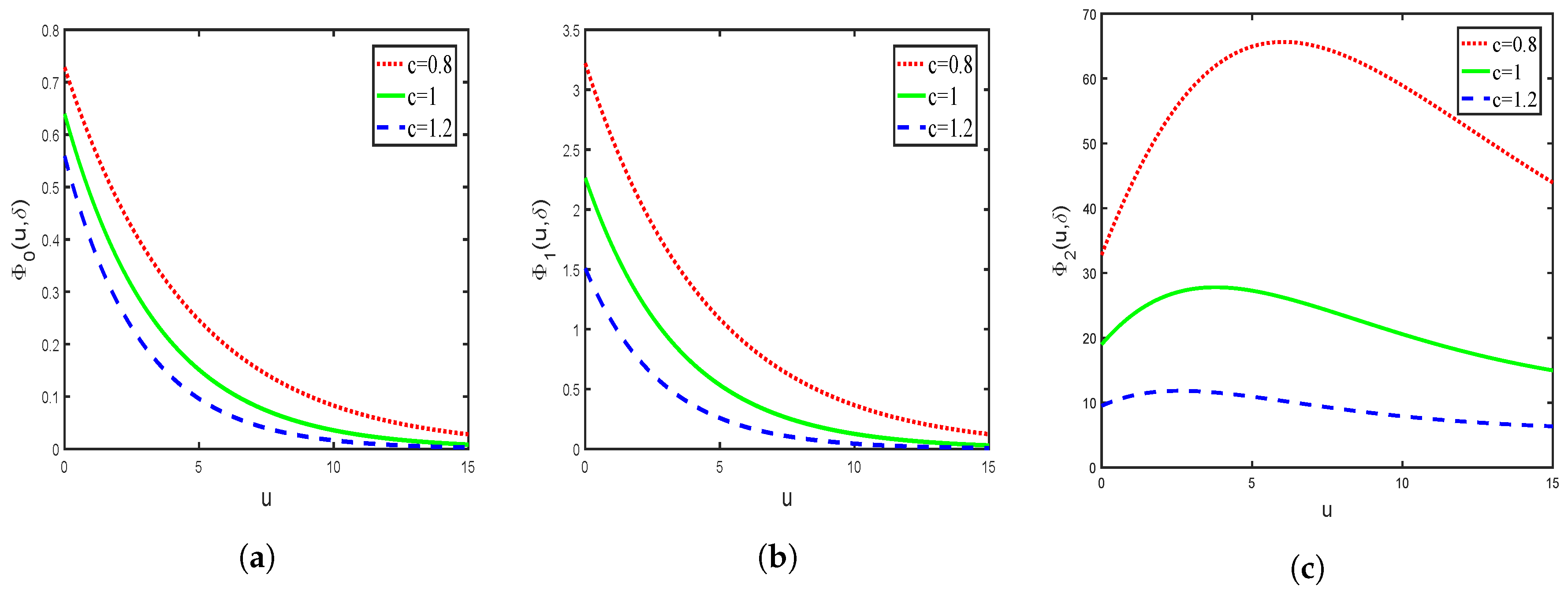

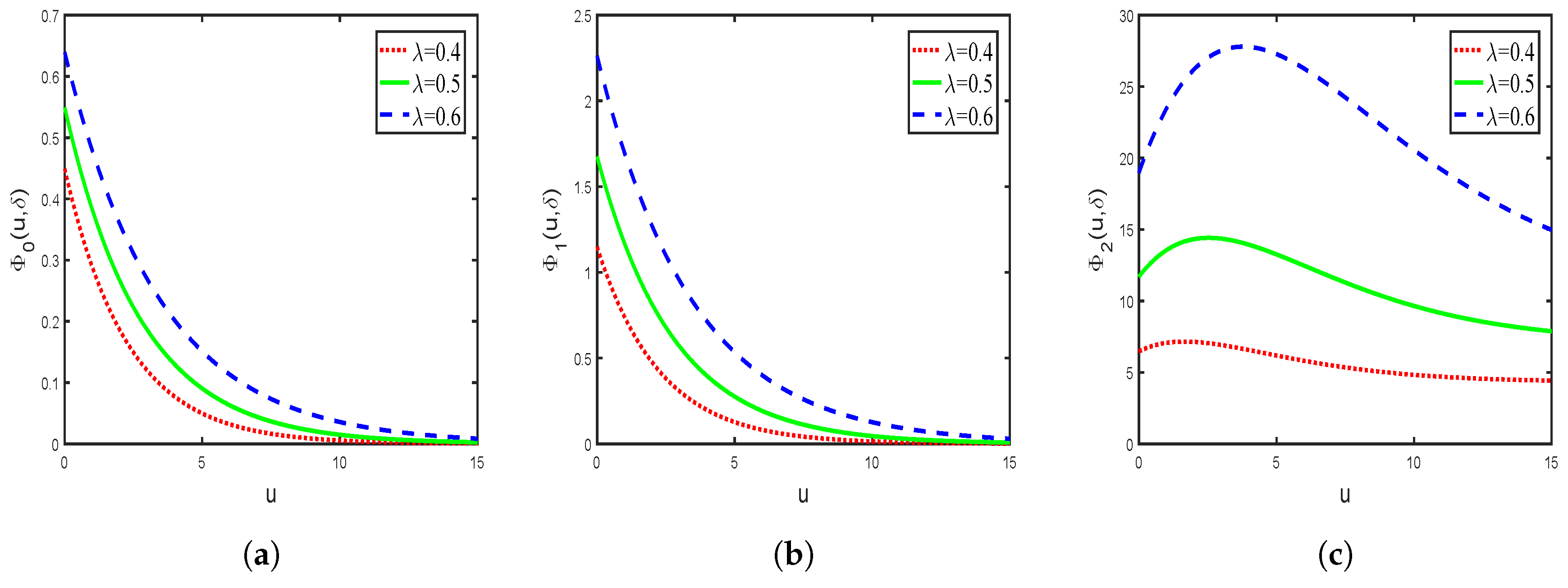

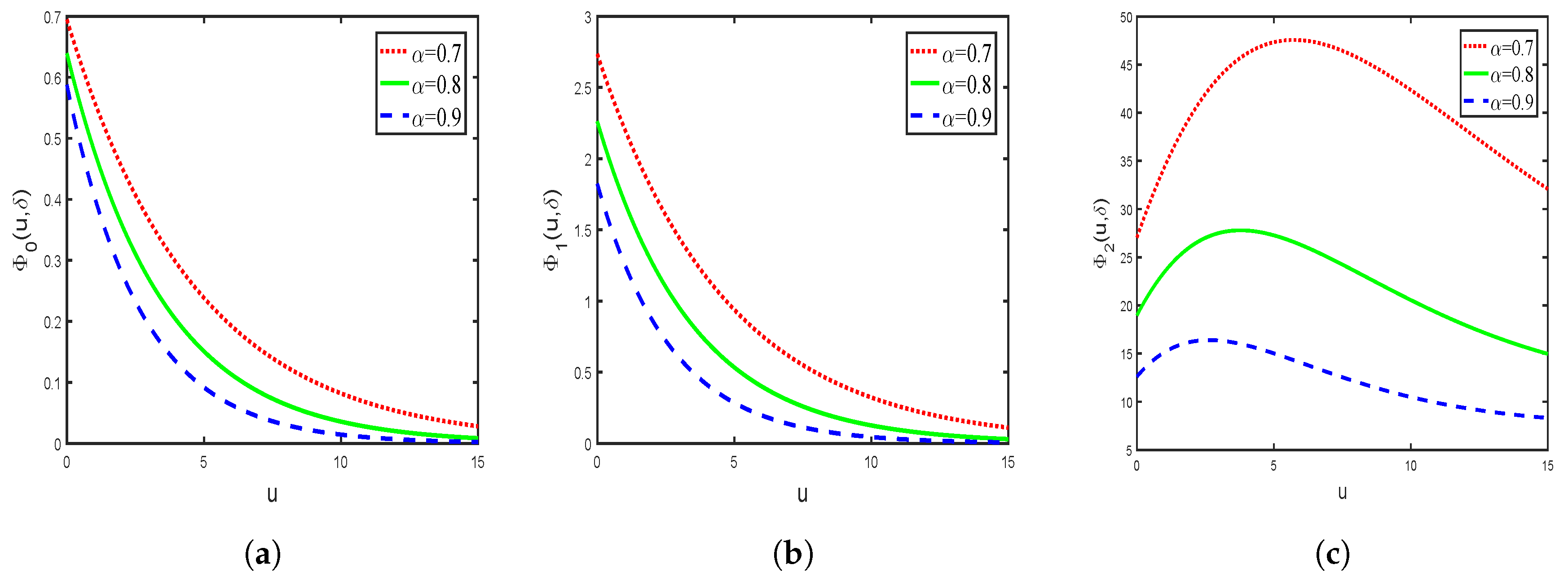

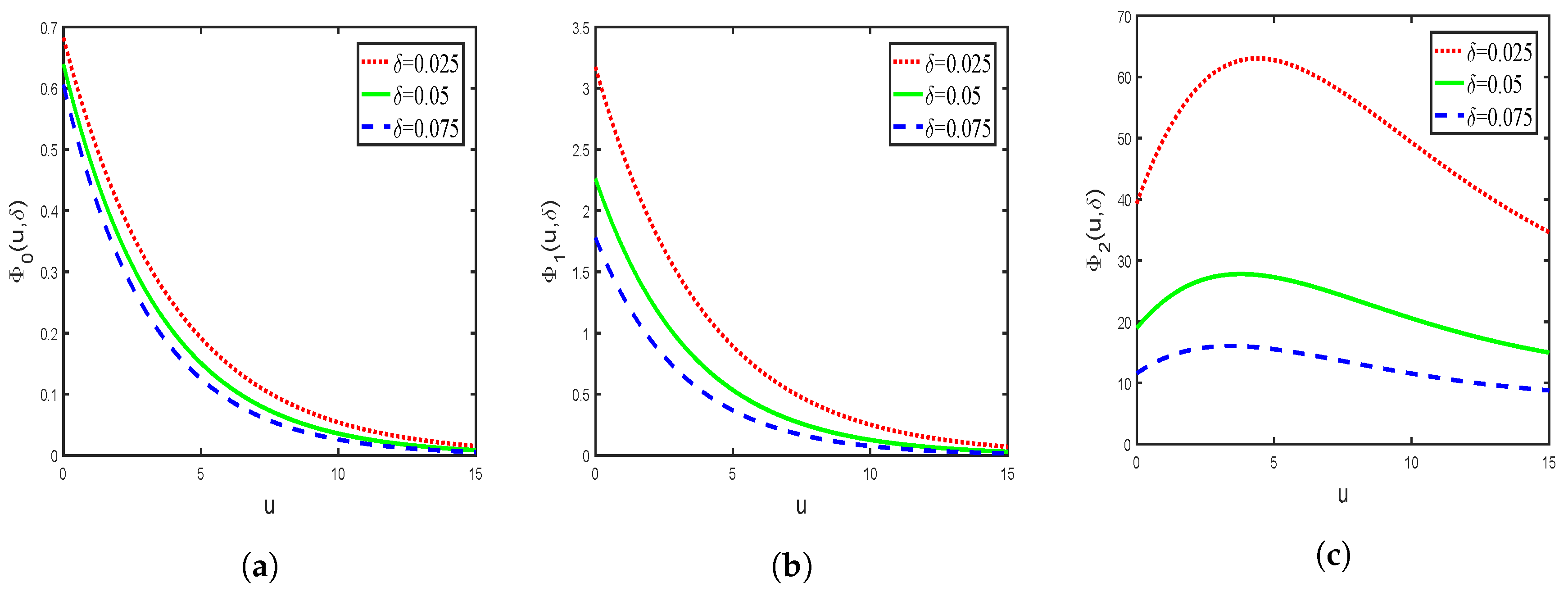

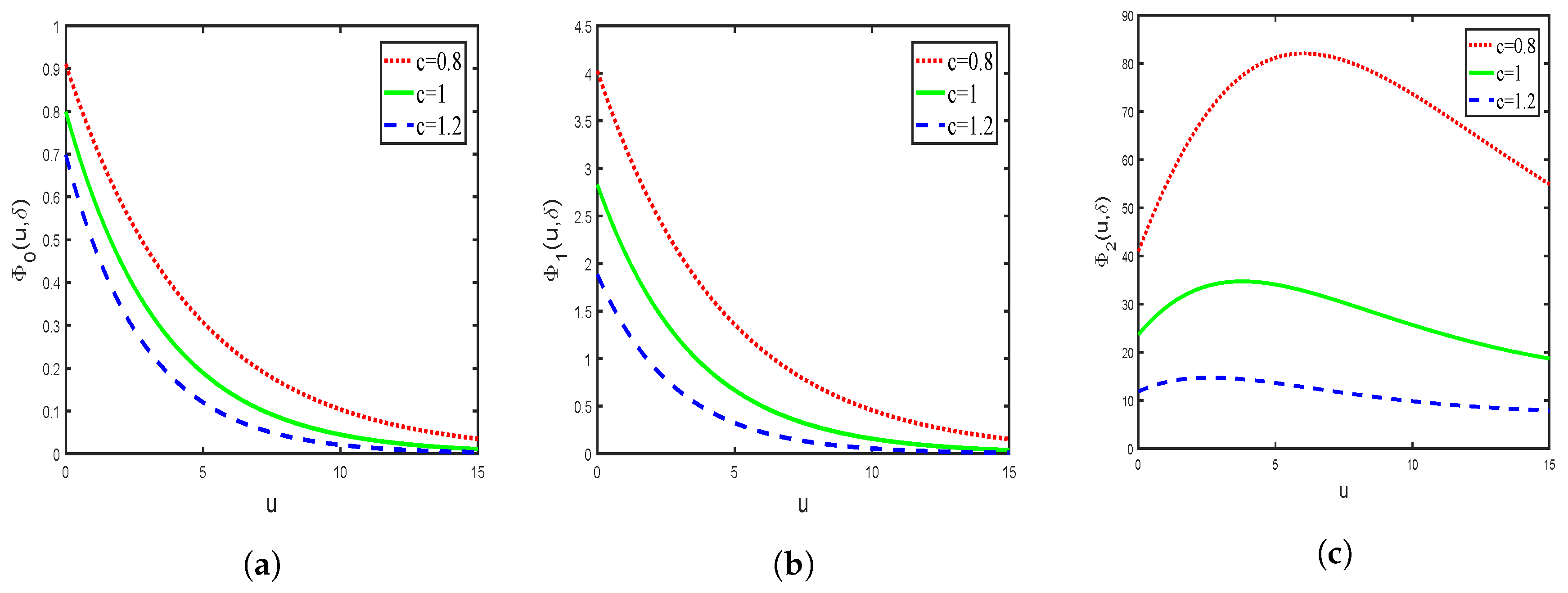

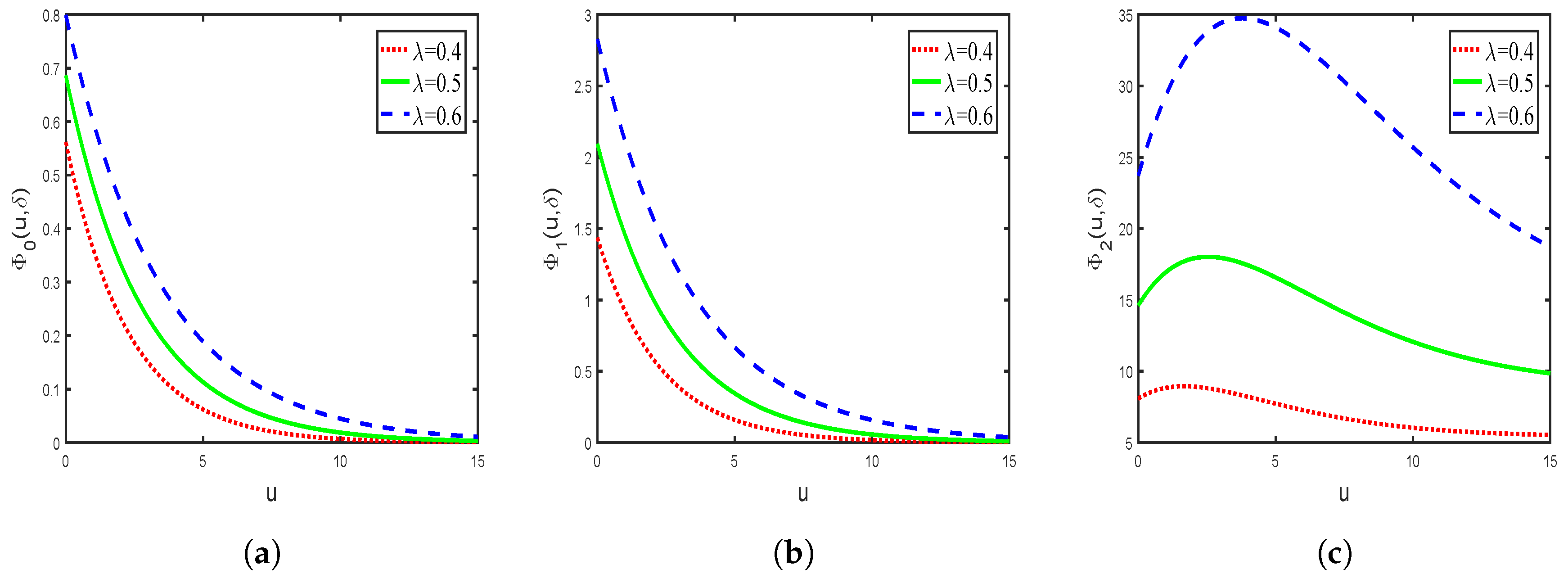

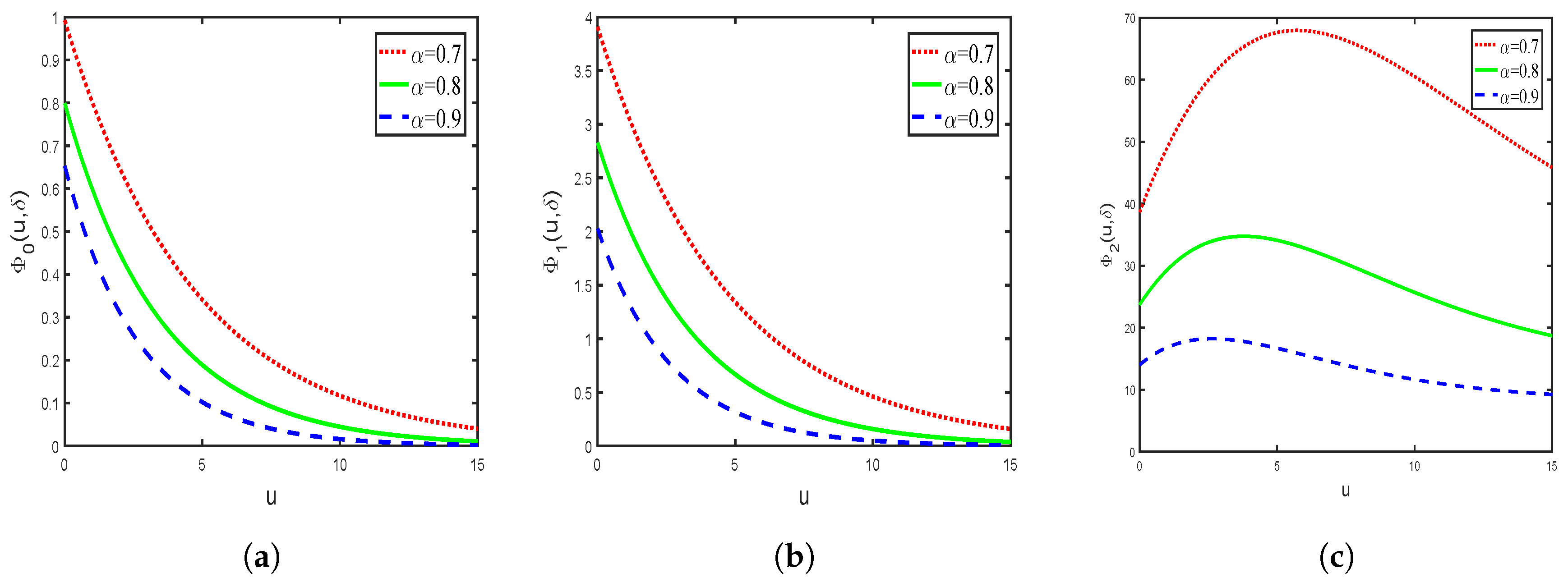

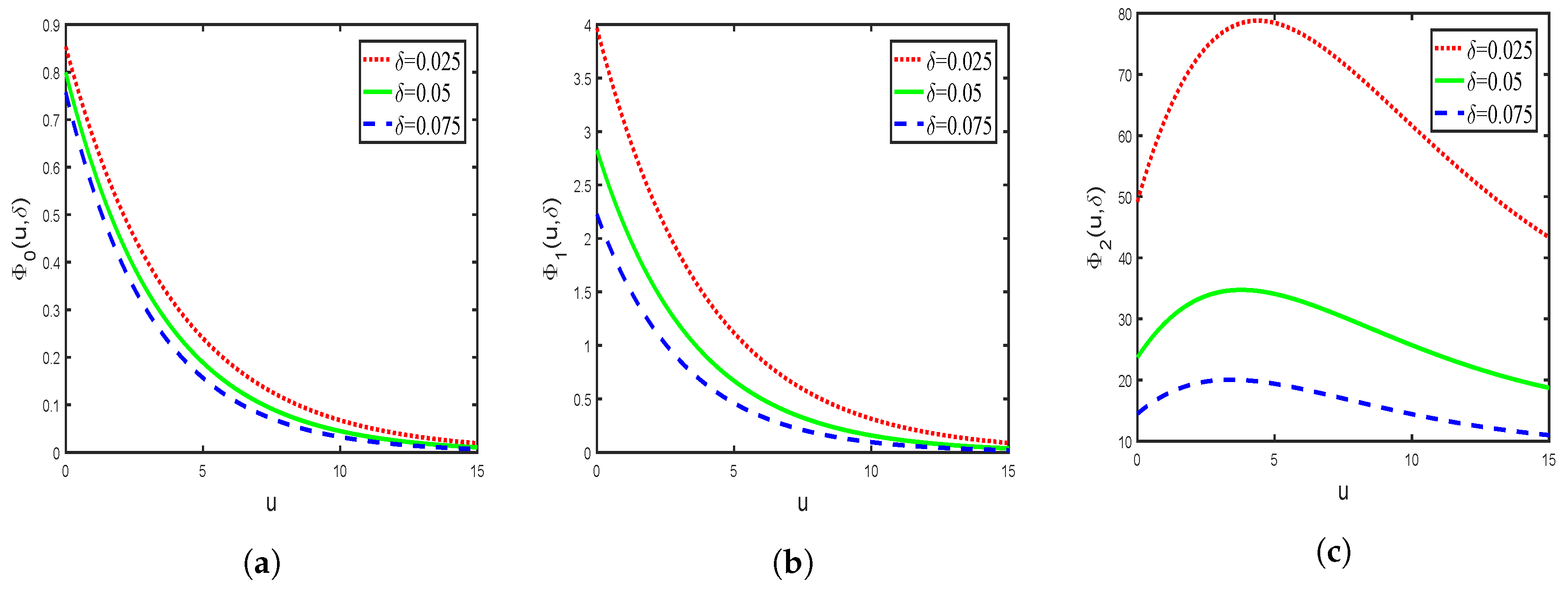

3. Explicit Expressions for Exponential Claim Distribution and Numerical Examples

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Lin, X.S.; Willmot, G.E.; Drekic, S. The classical risk model with a constant dividend barrier: Analysis of the Gerber–Shiu discounted penalty function. Insur. Math. Econ. 2003, 33, 391–408. [Google Scholar]

- Zhang, H.Y.; Zhou, M.; Guo, J.Y. The Gerber–Shiu discounted penalty function for classical risk model with a two-step premium rate. Stat. Probab. Lett. 2006, 76, 1211–1218. [Google Scholar] [CrossRef]

- Yu, W.G. Some results on absolute ruin in the perturbed insurance risk model with investment and debit interests. Econ. Model. 2013, 31, 625–634. [Google Scholar] [CrossRef]

- Yu, W.G. On the expected discounted penalty function for a Markov regime switching risk model with stochastic premium income. Discret. Dyn. Nat. Soc. 2013, 2013, 1–9. [Google Scholar] [CrossRef]

- Wang, Y.Y.; Yu, W.G.; Huang, Y.J.; Yu, X.L.; Fan, H.L. Estimating the expected discounted penalty function in a compound Poisson insurance risk model with mixed premium income. Mathematics 2019, 7, 305. [Google Scholar] [CrossRef]

- Avram, F.; Palmowski, Z.; Pistorius, M.R. On Gerber–Shiu functions and optimal dividend distribution for a Lévy risk process in the presence of a penalty function. Ann. Appl. Probab. 2015, 25, 1868–1935. [Google Scholar] [CrossRef]

- Zhang, Z.M. Estimating the Gerber–Shiu function by Fourier-Sinc series expansion. Scand. Actuar. J. 2017, 2017, 898–919. [Google Scholar] [CrossRef]

- Chi, Y.C. Analysis of expected discounted penalty function for a general jump diffusion risk model and applications in finance. Insur. Math. Econ. 2010, 46, 385–396. [Google Scholar] [CrossRef]

- Peng, J.Y.; Wang, D.C. Uniform asymptotics for ruin probabilities in a dependent renewal risk model with stochastic return on investments. Stochastics 2018, 90, 432–471. [Google Scholar] [CrossRef]

- Li, S.M.; Lu, Y.; Sendova, K.P. The expected discounted penalty function: From infinite time to finite time. Scand. Actuar. J. 2019, 2019, 336–354. [Google Scholar] [CrossRef]

- Huang, Y.J.; Yu, W.G.; Pan, Y.; Cui, C.R. Estimating the Gerber–Shiu expected discounted penalty function for Lévy risk model. Discrete Dyn. Nat. Soc. 2019, 2019, 1–15. [Google Scholar] [CrossRef]

- Preischl, M.; Thonhauser, S. Optimal reinsurance for Gerber–Shiu functions in the Cramér-Lundberg model. Insur. Math. Econ. 2019, 87, 82–91. [Google Scholar] [CrossRef]

- Zeng, Y.; Li, D.P.; Chen, Z.; Yang, Z. Ambiguity aversion and optimal derivative–based pension investment with stochastic income and volatility. J. Econ. Dyn. Control 2018, 88, 70–103. [Google Scholar] [CrossRef]

- Zeng, Y.; Li, D.P.; Gu, A.L. Robust equilibrium reinsurance–investment strategy for a mean–variance insurer in a model with jumps. Insur. Math. Econ. 2016, 66, 138–152. [Google Scholar] [CrossRef]

- Yu, W.G.; Huang, Y.J.; Cui, C.R. The absolute ruin insurance risk model with a threshold dividend strategy. Symmetry 2018, 10, 377. [Google Scholar] [CrossRef]

- Dickson, D.C.M.; Qazvini, M. Gerber–Shiu analysis of a risk model with capital injections. Eur. Actuar. J. 2016, 6, 409–440. [Google Scholar] [CrossRef]

- Zhang, Z.M.; Su, W. A new efficient method for estimating the Gerber–Shiu function in the classical risk model. Scand. Actuar. J. 2018, 2018, 426–449. [Google Scholar] [CrossRef]

- Zhang, Z.M.; Su, W. Estimating the Gerber–Shiu function in a Lévy risk model by Laguerre series expansion. J. Comput. Appl. Math. 2019, 346, 133–149. [Google Scholar] [CrossRef]

- Li, J.C.; Dickson, D.C.M.; Li, S.M. Some ruin problems for the MAP risk model. Insur. Math. Econ. 2015, 65, 1–8. [Google Scholar] [CrossRef]

- Zhao, Y.X.; Yin, C.C. The expected discounted penalty function under a renewal risk model with stochastic income. Appl. Math. Comput. 2012, 218, 6144–6154. [Google Scholar] [CrossRef]

- Cai, J.; Feng, R.; Willmot, G.E. On the total discounted operating costs up to default and its applications. Adv. Appl. Probab. 2009, 41, 495–522. [Google Scholar] [CrossRef]

- Cheung, E.C.K. A generalized penalty function in Sparre–Andersen risk models with surplus-dependent premium. Insur. Math. Econ. 2011, 48, 384–397. [Google Scholar] [CrossRef][Green Version]

- Cheung, E.C.K. Moments of discounted aggregate claim costs until ruin in a Sparre–Andersen risk model with general interclaim times. Insur. Math. Econ. 2013, 53, 343–354. [Google Scholar] [CrossRef]

- Cheung, E.C.K.; Woo, J.K. On the discounted aggregate claim costs until ruin in dependent Sparre–Andersen risk processes. Scand. Actuar. J. 2016, 2016, 63–91. [Google Scholar] [CrossRef]

- Cheung, E.C.K.; Feng, R. A unified analysis of claim costs up to ruin in a Markovian arrival risk process. Insur. Math. Econ. 2013, 53, 98–109. [Google Scholar] [CrossRef]

- Wang, H.C.; Li, N.X. On the Gerber–Shiu function with random discount rate. Commun. Stat. Theory Methods 2017, 46, 210–220. [Google Scholar] [CrossRef]

- Wang, W.Y.; Zhang, Z.M. Computing the Gerber–Shiu function by frame duality projection. Scand. Actuar. J. 2019, 2019, 291–307. [Google Scholar] [CrossRef]

- Egidio dos Reis, A.D. On the moments of ruin and recovery times. Insur. Math. Econ. 2000, 27, 331–343. [Google Scholar] [CrossRef]

- Lin, X.S.; Willmot, G.E. The moments of the time of ruin, the surplus before ruin, and the deficit at ruin. Insur. Math. Econ. 2000, 27, 19–44. [Google Scholar] [CrossRef]

- Drekic, S.; Willmot, G.E. On the moments of the time of ruin with applications to phase-type claims. N. Am. Actuar. J. 2005, 9, 17–30. [Google Scholar] [CrossRef]

- Pitts, S.M.; Politis, K. Approximations for the moments of ruin time in the compound Poisson model. Insur. Math. Econ. 2008, 42, 668–679. [Google Scholar] [CrossRef]

- Yu, K.; Ren, J.; Stanford, D.A. The moments of the time of ruin in Markovian risk models. N. Am. Actuar. J. 2010, 14, 464–471. [Google Scholar] [CrossRef]

- Lee, W.Y.; Willmot, G.E. On the moments of the time to ruin in dependent Sparre–Andersen models with emphasis on Coxian interclaim times. Insur. Math. Econ. 2014, 59, 1–10. [Google Scholar] [CrossRef]

- Lee, W.Y.; Willmot, G.E. The moments of the time to ruin in dependent Sparre–Andersen models with Coxian claim sizes. Scand. Actuar. J. 2016, 2016, 550–564. [Google Scholar] [CrossRef]

- Schmidli, H. Extended Gerber–Shiu functions in a risk model with interest. Insur. Math. Econ. 2015, 61, 271–275. [Google Scholar] [CrossRef]

- Deng, Y.C.; Liu, J.; Huang, Y.; Li, M.; Zhou, J.M. On a discrete interaction risk model with delayed claims and stochastic incomes under random discount rates. Commun. Stat. Theory Methods 2018, 47, 5867–5883. [Google Scholar] [CrossRef]

- Li, S.M.; Lu, Y. On the generalized Gerber–Shiu function for surplus processes with interest. Insur. Math. Econ. 2013, 52, 127–134. [Google Scholar] [CrossRef]

- Dickson, D.C.M.; Hipp, C. On the time to ruin for Erlang (2) risk processes. Insur. Math. Econ. 2001, 29, 333–344. [Google Scholar] [CrossRef]

- Li, S.M.; Garrido, J. On ruin for the Erlang(n) risk process. Insur. Math. Econ. 2004, 34, 391–408. [Google Scholar] [CrossRef]

- Gerber, H.U.; Shiu, E.S.W. On the time value of ruin. N. Am. Actuar. J. 1998, 2, 48–72. [Google Scholar] [CrossRef]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ruan, J.; Yu, W.; Song, K.; Sun, Y.; Huang, Y.; Yu, X. A Note on a Generalized Gerber–Shiu Discounted Penalty Function for a Compound Poisson Risk Model. Mathematics 2019, 7, 891. https://doi.org/10.3390/math7100891

Ruan J, Yu W, Song K, Sun Y, Huang Y, Yu X. A Note on a Generalized Gerber–Shiu Discounted Penalty Function for a Compound Poisson Risk Model. Mathematics. 2019; 7(10):891. https://doi.org/10.3390/math7100891

Chicago/Turabian StyleRuan, Jiechang, Wenguang Yu, Ke Song, Yihan Sun, Yujuan Huang, and Xinliang Yu. 2019. "A Note on a Generalized Gerber–Shiu Discounted Penalty Function for a Compound Poisson Risk Model" Mathematics 7, no. 10: 891. https://doi.org/10.3390/math7100891

APA StyleRuan, J., Yu, W., Song, K., Sun, Y., Huang, Y., & Yu, X. (2019). A Note on a Generalized Gerber–Shiu Discounted Penalty Function for a Compound Poisson Risk Model. Mathematics, 7(10), 891. https://doi.org/10.3390/math7100891