Controlling Waste and Carbon Emission for a Sustainable Closed-Loop Supply Chain Management under a Cap-and-Trade Strategy

Abstract

:1. Introduction

2. Literature Review

3. Problem Definition, Notation, and Assumptions

3.1. Problem Definition

3.2. Notation

3.3. Assumptions

- All players of the CLSCM are in a cooperation and the power of each player is the same. No game strategy is considered for the symmetric power of the SC players. This study elaborates on a coordination policy for the cost minimization. The demand and production rates are deterministic with . Thus, shortage is not allowed for this model.

- Constant and variable shipment carbon emission costs are introduced for the SSMD policy. This study adopts the variable shipment and carbon emission costs depending on the container quantity and distance between players.

- To help alleviate global warming due to carbon emissions, a CAPT strategy is considered by the retailer for a definite period in which it can sell or buy carbon credit regarding its own carbon emissions quantity to help control carbon emission (Hua et al. [32]).

- Two kinds of goods (newish from raw materials and remanufactured from collected used goods) are produced. The retailer and end customer bare a similar cost for both. It is further assumed that the manufacturing cost is larger than the remanufacturing cost, which is larger than the raw material price for remanufacturing used products, i.e., .

- A fraction of the total demand D is collected by 3PL as recyclable goods, and it is obtained that is the fraction of collected products that are defective after inspection, which are fully used for landfill, where . A two-stage inspection policy is performed by 3PL before the delivery of products to the manufacturer. At the time of inspection, inspectors may wrongly reject a faultless product as faulty, which is defined as a Type I error, and may wrongly accept a faulty product as faultless, which is defined as a Type II error (Sarkar and Saren [38]). Hence, two kinds of inspection errors may occur during human inspection.

- The manufacturer’s manufacturing/remanufacturing capacity is unlimited and both remanufactured and newly finished products have the same quality and price. The players use same type container for the delivery of products (Sarkar et al. [16]). The container number is considered as an integer. Collection, shipping, inspection, and delivery of the used products to the manufacturer are all the responsibility of 3PL. It is assumed that the random variables , , , are mutually independent and each pursues the same distribution (uniform) in this model.

4. Model Formulation

4.1. Manufacturer’s Model

4.1.1. Manufacturer’s Ordering Cost

4.1.2. Setup Cost of the Manufacturer

4.1.3. Manufacturer’s Holding Cost

Manufacturer’s Holding Cost for Newly Made Products

Manufacturer’s Holding Cost for Collected Used Products

4.1.4. Shipment Cost of the Manufacturer

4.1.5. Carbon Emission Cost

4.1.6. Manufacturing Cost of the Manufacturer

4.1.7. Remanufacturing Cost of the Manufacturer

4.1.8. Raw Material Price for Remanufacturing

4.1.9. Buying Price for Raw Materials at the Manufacturer

4.1.10. Manufacturer’s Total Cost per Production Run

4.2. Retailer’s Model

4.2.1. Retailer’s Ordering Cost

4.2.2. Retailer’s Holding Cost

4.2.3. Buying Price of Finished Products of the Retailer

4.2.4. Carbon Emission Cost Linked to the Replenishment Order

4.2.5. Carbon Emission Cost due to the Inventory of the Retailer

4.2.6. Total Cost Related to Retailer

4.3. 3PL’s Model

4.3.1. 3PL’s Collection Cost

4.3.2. Setup Cost of 3PL

4.3.3. 3PL’s Holding Cost

4.3.4. Inspection Cost

4.3.5. Landfill Cost of 3PL

4.3.6. Price Discounts

4.3.7. Shipment Cost During Delivery to the Manufacturer

4.3.8. Carbon Emission Cost During Dispatch to the Manufacturer

4.3.9. Inspection Error

Type I Error

Type II Error

4.3.10. Total Cost of 3PL per Cycle

4.4. Total Cost of CLSC per Cycle

4.5. Solution Methodology

MHGS Algorithm

- Step 1.

- Obtain shipment numbers and is found by using a linear search method. Put all parametric data and obtain the optimal value of shipment numbersand assume the manufacturer and 3PL have a clear-cut shipment numbers.

- Step 2.

- Capacity of single container , cycle length are obtained.

- Step 2.1.

- Put .

- Step 2.2.

- Evaluate from Equation (36).

- Step 3.

- Calculate the total cost from Equation (33). is an optimum solution for fixed .

- Step 4.

- Put and perform Step 2.2 and 3. If , reiterate Step 2 and then go to Step 3, if not go to Step 5.

- Step 5.

- Put . is the global optimal solution.

5. Numerical Experiment

5.1. Special Case 1: Model without a CAPT Strategy for the Retailer

5.2. Special Case 2: Model without Reverse Logistics

5.3. Special Case 3: Model without Variable Transportation and Carbon Emission

6. Sensitivity Analysis

- If the setup cost of the manufacturer for setting up the production infrastructure, ordering costs , relating to manufacturer and retailer, setup cost per setup, and the collection cost of 3PL are all increased, the total cost increases in that situation. Due to the reductions in the setup cost, ordering cost, and collection cost by 25% or 50%, infeasible results are obtained. These parameters moderately affect the models.

- The manufacturer’s holding costs for newly finished products and collected used products, retailer’s and 3PL’s holding costs and are not sensitive in this study. For negative as well as positive percent changes of the holding cost, the results are similar in magnitude to the total cost. Thus, for both changes, an equilibrium situation is observed in both directions.

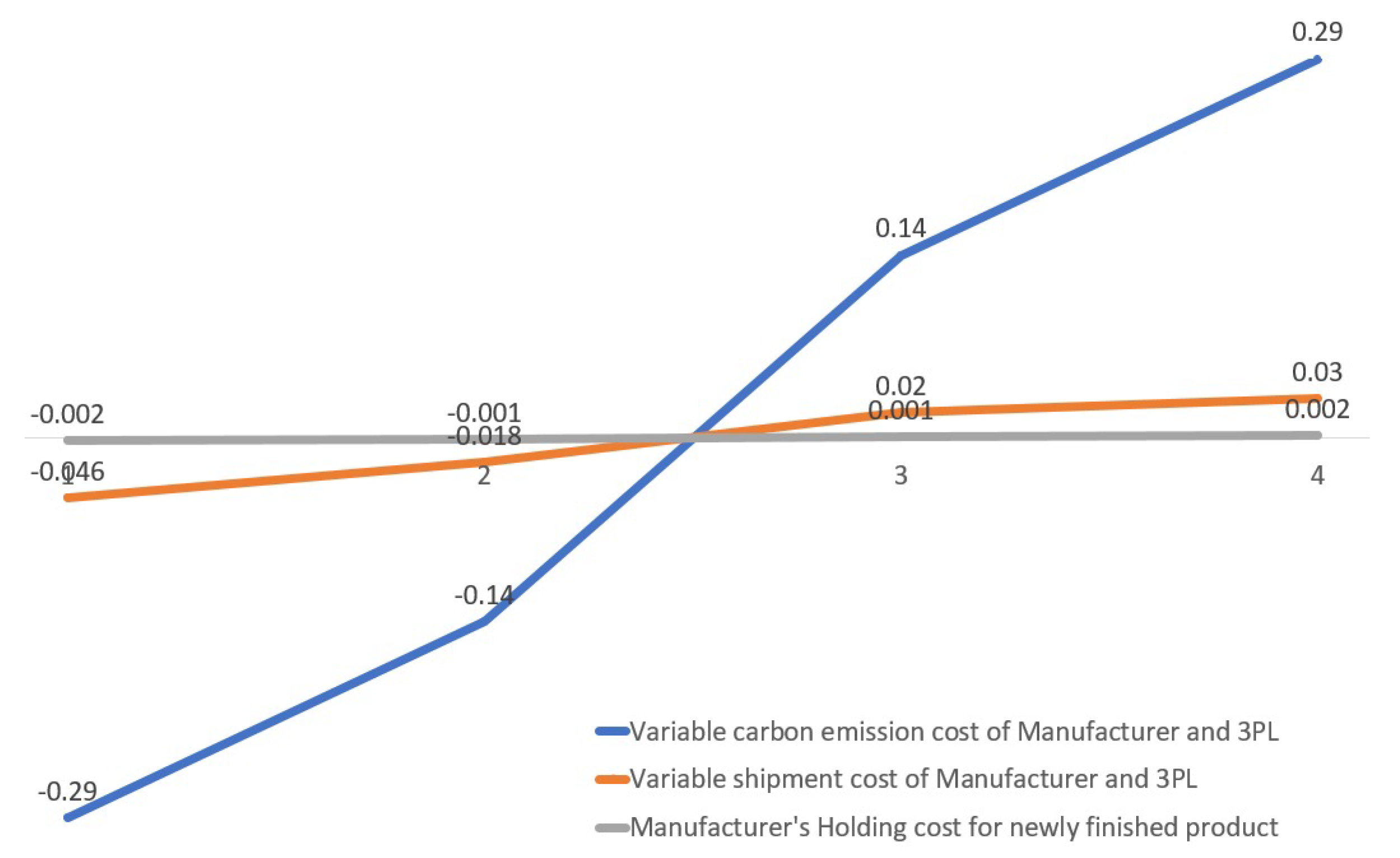

- If the fixed shipment cost of the CLSCM model per shipment F and fixed carbon emission costs and per shipment for manufacturer and 3PL are increased by 50% and 25%, respectively, then the expected total cost increases. For decreases of and by 50% and F by 25% or more, infeasible results are obtained. Therefore, it can be concluded that these parameters moderately affect the system. Again, The expected total cost increases or decreases according as the shipment cost per container per unit distance increases or decreases.

- If the carbon emission cost and per container per unit distance are increased/decreased, then the expected total cost for the CLSCM model increases/decreases, respectively. The total cost maintains a position of equilibrium and these parameters moderately affect the system.

- It is observed that for percentage increases in the manufacturer’s production cost and buying price of raw materials of the manufacturer , the changes in total cost is infeasible. If the production cost and buying price of raw materials decreases by 25% or 50%, the total cost decreases. Thus, these parameters are more sensitive.

- If the raw material’s price for remanufacturing and the remanufacturing cost of the manufacturer increase, then the total cost increases. Decreasing these parameters by 25% or 50% leads to infeasible results. Thus, these are sensitive parameters. Again, if the carbon price c of the retailer decreases, then the total cost increases which is a fully different scenario compared to previous parameters. But due to the increment of this parameter by 25% or 50%, an infeasible result is obtained. If less carbon cost is needed, it is very simple for any CLSC to offset total cost.

- The buying price is the most significant and sensitive parameter for this model. This model considers newly finished and finished products both. Therefore, this cost is very effective and it is clear from sensitivity analysis that if the buying price of finished product of retailer decreases by 50%, then the optimal cost decreases by 28.76%.

- The total cost of CLSCM is increased if per-unit inspection cost is increased. Here, it is noticed that if the parameter is decreased by 25% or more, an infeasible result is obtained. Again, if the variable inspection cost per container increases, then the expected total cost increases. If the parameters decreases by 25% or more, an infeasible result is obtained. Therefore, it is not possible to decrease the inspection cost by 25% or more.

- The landfill cost , price discounts , cost of wrongly rejecting good items , and cost of wrongly accepting faulty items are the least sensitive parameters in this model. For positive/negative change of each parameter, an equilibrium situation is arrived.

7. Implications and Managerial Insights

- From sensitive analysis, it is evident that if the carbon price of the retailer decreases, the total cost is increased. This is because the retailer uses a CAPT mechanism (in which they can sell the extra carbon credit).

- It is observed that if the buying cost of newish/remanufactured products is at a minimum, the total cost is at a minimum. Therefore, industry managers can easily make decisions considering these findings. Here, each of the random variables (like return rate of used goods, defective rate of collected used products and also the random variables presenting Type I and Type II errors) follow the uniform distributions, from which the global minimum expense can be calculate by the industry easily.

8. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| SSC | sustainable supply chain |

| EOL | end-of-life |

| CLSCM | closed-loop supply chain management |

| SSMD | single-setup multi-delivery |

| SC | supply chain |

| SCM | supply chain management |

| CAPT | cap-and-trade |

| GSCM | green supply chain management |

| RL | reverse logistics |

| RLSC | reverse logistics supply chain |

| VMIP | vendor-managed-inventory policy |

| 3PL | third party logistics |

Appendix A

Appendix B

References

- Tayyab, M.; Jemai, J.; Lim, H.; Sarkar, B. A sustainable development framework for a cleaner multi-item multi-stage textile production system with a process improvement initiative. J. Clean. Prod. 2020, 246, 119055. [Google Scholar] [CrossRef]

- Tiwari, S.; Ahmed, W.; Sarkar, B. Sustainable ordering policies for non-instantaneous deteriorating items under carbon emission and multi-trade-credit-policies. J. Clean. Prod. 2019, 240, 118183. [Google Scholar] [CrossRef]

- Cárdenas-Barrón, L.E.; González-Velardeb, J.L.; Treviño-Garza, G.; Garza-Nuñeza, D. Heuristic algorithm based on reduce and optimize approach for a selective and periodic inventory routing problem in a waste vegetable oil collection environment. Int. J. Prod. Econ. 2019, 211, 44–59. [Google Scholar] [CrossRef]

- Cárdenas-Barrón, L.E.; Sana, S.S. A production-inventory model for a two-echelon supply chain when demand is dependent on sales teams’ initiatives. Int. J. Prod. Econ. 2014, 155, 249–258. [Google Scholar] [CrossRef]

- Taleizadeh, A.A.; Noori-daryan, M.; Cárdenas-Barrón, L.E. Joint optimization of price, replenishment frequency, replenishment cycle and production rate in vendor managed inventory system with deteriorating items. Int. J. Prod. Econ. 2015, 155, 285–295. [Google Scholar] [CrossRef]

- Hota, S.K.; Sarkar, B.; Ghosh, S.K. Effects of unequal lot size and variable transportation in unreliable supply chain management. Mathematics 2020, 8, 357. [Google Scholar] [CrossRef] [Green Version]

- Daryanto, Y.; Wee, H.M.; Widyadana, G.A. Low carbon supply chain coordination for imperfect quality deteriorating items. Mathematics 2019, 7, 234. [Google Scholar] [CrossRef] [Green Version]

- Mishra, U.; Wu, J.Z.; Sarkar, B. A sustainable production-inventory model for a controllable carbon emissions rate under shortages. J. Clean. Prod. 2020, 256, 120268. [Google Scholar] [CrossRef]

- Ullah, M.; Sarkar, B. Recovery-channel selection in a hybrid manufacturing-remanufacturing production model with RFID and product quality. Int. J. Prod. Econ. 2020, 219, 360–374. [Google Scholar] [CrossRef]

- Taleizadeh, A.A.; Soleymanfar, V.R.; Govindan, K. Sustainable economic production quantity models for inventory systems with shortage. J. Clean. Prod. 2018, 174, 1011–1020. [Google Scholar] [CrossRef]

- Ahamed, W.; Sarkar, B. Management of next-generation energy using a triple bottom line approach under a supply chain framework. Resour. Conserv. Recyc. 2019, 150, 104431. [Google Scholar] [CrossRef]

- Sarkar, B.; Tayyab, M.; Kim, N.; Habib, M.S. Optimal production delivery policies for supplier and manufacturer in a constrained closed-loop supply chain for returnable transport packaging through metaheuristic approach. Comp. Indus. Eng. 2019, 135, 987–1003. [Google Scholar] [CrossRef]

- Sarkar, B.; Majumdar, A. Integrated vendor–buyer supply chain model with vendor’s setup cost reduction. App. Math. Comp. 2013, 224, 362–371. [Google Scholar] [CrossRef]

- Sarkar, B. A production-inventory model with probabilistic deterioration in two-echelon supply chain management. App. Math. Mod. 2013, 37, 3138–3151. [Google Scholar] [CrossRef]

- Cárdenas-Barrón, L.E.; Chung, K.J.; Treviño-Garza, G. Celebrating a century of the economic order quantity model in honor of Ford Whitman Harris. Int. J. Prod. Econ. 2014, 155, 1–7. [Google Scholar] [CrossRef]

- Sarkar, B.; Ullah, M.; Kim, N. Environmental and economic assessment of closed-loop supply chain with remanufacturing and returnable transport items. Comp. Indus. Eng. 2017, 111, 148–163. [Google Scholar] [CrossRef]

- Sarkar, B.; Omair, M.; Kim, N. A cooperative advertising collaboration policy in supply chain management under uncertain conditions. Appl. Sci. Comp. 2020, 88, 105948. [Google Scholar]

- Cárdenas-Barrón, L.E.; Sana, S.S. Multi-item EOQ inventory model in a two-layer supply chain while demand varies with promotional effort. App. Math. Mod. 2015, 39, 6725–6737. [Google Scholar] [CrossRef]

- Guide, V.D.R., Jr.; Van Wassenhove, L.N. The evolution of closed-loop supply chain research. Oper. Res. 2009, 57, 10–18. [Google Scholar] [CrossRef]

- Saxena, N.; Sarkar, B.; Singh, S.R. Selection of remanufacturing/production cycles with an alternative market: A perspective on waste management. J. Clean. Prod. 2020, 245, 118935. [Google Scholar] [CrossRef]

- Govindan, K.; Soleimani, H. A review of reverse logistics and closed-loop supply chains: A Journal of Cleaner Production focus. J. Clean. Prod. 2016, 142, 371–384. [Google Scholar] [CrossRef]

- Govindan, K.; Soleimani, H.; Kannan, D. Reverse logistics and closed-loop supply chain: A comprehensive review to explore the future. Eur. J. Oper. Res. 2015, 240, 603–626. [Google Scholar] [CrossRef] [Green Version]

- Shaharudin, M.R.; Govindan, K.; Zailani, S.; Tan, K.C. Managing product returns to achieve supply chain sustainability: An exploratory study and research propositions. J. Clean. Prod. 2015, 101, 1–15. [Google Scholar] [CrossRef]

- Huang, X.; Choi, S.M.; Ching, W.K.; Siu, T.K.; Huang, M. On supply chain coordination for false failure returns: A quantity discount contract approach. Int. J. Prod. Econ. 2011, 133, 634–644. [Google Scholar] [CrossRef]

- Heydari, J.; Govindan, K.; Jafari, A. Reverse and closed loop supply chain coordination by considering government role. Trans. Res. Part D 2017, 52, 379–398. [Google Scholar] [CrossRef]

- Govindan, K.; Popiuc, M.N. Reverse supply chain coordination by revenue sharing contract: A case for the personal computers industry. Eur. J. Oper. Res. 2014, 233, 326–336. [Google Scholar] [CrossRef]

- Konstantaras, I.; Skouri, K.; Jaber, M.Y. Lot sizing for a recoverable product with inspection and sorting. Comp. Indus. Eng. 2010, 58, 452–462. [Google Scholar] [CrossRef]

- Khouja, M. Optimizing inventory decisions in a multi-stage multi-customer supply chain. Trans. Res. Part E Log. Trans. Rev. 2003, 39, 193–208. [Google Scholar] [CrossRef]

- Cárdenas-Barrón, L.E. Optimizing inventory decisions in a multi-stage multi-customer supply chain: A note. Trans. Res. Part E Log. Trans. Rev. 2007, 43, 647–654. [Google Scholar] [CrossRef]

- Ertogral, K.; Darwish, M.; Ben-Daya, M. Production and shipment lot sizing in a vendor-buyer supply chain with transportation cost. Eur. J. Oper. Res. 2007, 176, 1592–1606. [Google Scholar] [CrossRef]

- Sarkar, B.; Ganguly, B.; Sarkar, M. Effect of variable transportation and carbon emission in a three-echelon supply chain model. Trans. Res. Part E Log. Trans. Rev. 2016, 91, 112–128. [Google Scholar] [CrossRef]

- Hua, G.; Cheng, T.C.E.; Wang, S. Managing carbon footprints in inventory management. Int. J. Prod. Econ. 2011, 132, 178–185. [Google Scholar] [CrossRef]

- Shaw, B.K.; Sangal, I.; Sarkar, B. Joint effects of carbon emission, deterioration, and multi-stage inspection policy in an integrated inventory model. In Optimization and Inventory Management; Shah, N., Mittal, M., Eds.; Springer: Singapore, 2020; pp. 195–208. [Google Scholar]

- Tiwari, S.; Ahmed, W.; Sarkar, B. Multi-item sustainable green production system under trade-credit and partial backordering. J. Clean. Prod. 2018, 204, 82–95. [Google Scholar] [CrossRef]

- Ahmed, W.; Sarkar, B. Impact of carbon emissions in a sustainable supply chain management for a second generation biofuel. J. Clean. Prod. 2018, 186, 807–820. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, W.; Liu, B. Manufacturing/remanufacturing decisions for a capital-constrained manufacturer considering carbon emission cap and trade. J. Clean. Prod. 2017, 140, 1118–1128. [Google Scholar] [CrossRef]

- Sarkar, B.; Saren, S.; Sinha, D.; Hur, S. Effect of unequal lot sizes, variable setup cost, and carbon emission cost in a supply chain model. Math. Prob. Eng. 2015, 469486. [Google Scholar] [CrossRef] [Green Version]

- Sarkar, B.; Saren, S. Product inspection policy for an imperfect production system with error and warranty cost. Eur. J. Oper. Res. 2016, 248, 263–271. [Google Scholar] [CrossRef]

- Kim, S.J.; Sarkar, B. Supply chain model with stochastic lead time, trade-credit financing, and transportation discounts. Mathematics 2017, 6465912. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author(s) | CLSCM and SSMD | Shipment | Environmental Effect | Reuse | Strategy |

|---|---|---|---|---|---|

| Cárdenas-Barrón and Sana [18] | — | Const. | — | — | Delay in payment |

| Daryanto et al. [7] | SSMD | Variable | CE, carbon tax | — | — |

| Hua et al. [32] | — | — | CE, carbon CAPT | — | — |

| Huang et al. [24] | SSMD | Const. | — | — | Quantity discount |

| Heydari et al. [25] | CLSCM | Const. | — | Remanuf- acturing | Price discount |

| Sarkar et al. [16] | CLSCM and SSMD | Variable | CE | Remanuf- acturing | — |

| Taleizadeh et al. [10] | — | — | CE | — | Shortage, back- ordering |

| Khouja et al. [28] | SSMD | Const. | — | — | — |

| Sarkar et al. [37] | SSMD | Variable | CE | Reworking | — |

| This model | CLSCM and SSMD | Variable | CE, carbon CAPT | LF | Price discount |

| Decision Variables | |

|---|---|

| replenishment cycle length (year) | |

| shipment numbers in a cycle for delivering the finished goods to the retailer via manufacturer (integer number) | |

| shipment numbers in a cycle for delivering the used goods to the manufacturer via 3PL (integer number) | |

| capacity of a single container (units) | |

| Dependent variable | |

| X | transfer quantity of carbon emissions (units) |

| Random variables | |

| collection rate of 3PL for the used products (units/cycle) | |

| fraction of collected products that are defective due to inspection and are used for landfill | |

| random variable presenting Type I error | |

| random variable presenting Type II error | |

| Parameters | |

| Q | retailer’s ordering quantity (units) |

| P | production rate per year (units/year) |

| D | rate of demand (units/year) |

| manufacturer’s unit production expense ($/unit) | |

| manufacturer’s holding cost to hold finished products ($/unit/unit time) | |

| manufacturer’s setup expense per setup ($/setup) | |

| manufacturer’s per-order ordering expense ($/order) | |

| buying price of raw material for manufacturing ($/unit) | |

| manufacturer’s remanufacturing cost ($/unit) | |

| manufacturer’s holding cost to hold used goods ($/unit/unit time) | |

| buying price of new/remanufactured products of the retailer ($/unit) | |

| retailer’s holding cost to hold finished goods ($/unit) | |

| retailer’s ordering cost per order ($/order) | |

| carbon emission quota (units/cycle) | |

| e | unit carbon emission linked to the replenishment order (unit) |

| w | unit variable carbon emission at the warehouse due to retailer’s inventory (unit) |

| c | carbon price of the retailer ($/unit) |

| raw material price for remanufacturing paid by the manufacturer to 3PL ($/unit) | |

| collection cost of 3PL ($/unit) | |

| setup cost paid by 3PL per setup ($/setup) | |

| holding cost paid by 3PL to hold collected products ($/unit/unit time) | |

| inspection cost of 3PL ($/unit) | |

| variable inspection cost of 3PL container to deliver products to the manufacturer ($/container) | |

| landfill cost of 3PL ($/unit) | |

| price discount offered to the manufacturer by 3PL ($/unit) | |

| cost of wrongly accepting faulty items ($/unit) | |

| cost of wrongly rejecting faultless items ($/unit) | |

| F | fixed shipment cost of the CLSC ($/shipment) |

| shipment cost conferred by the manufacturer and 3PL per container per unit distance ($/container/km) | |

| distance of the retailer from manufacturer (kilometers) | |

| distance of the manufacturer from 3PL (kilometers) | |

| fixed carbon emission cost paid by manufacturer per shipment for the delivery of finished products ($/shipment) | |

| carbon emission cost paid by manufacturer per container at unit distance for the delivery of finished products ($/container/kilometer) | |

| fixed carbon emission cost paid by 3PL per shipment to deliver used products to the manufacturer ($/shipment) | |

| carbon emission cost paid by 3PL per container per unit distance to deliver used products to the manufacturer ($/container/kilometer) |

| Parameters for the Manufacturer | ||

| 200/setup | 120/order | 0.28/unit/unit time |

| 0.22/unit/ unit time | 452 units/year | 300/shipment |

| 2/shipment | 0.2/container/unit distance | 60 km |

| 60/unit | 45/unit | 144/unit |

| 0.01/container/ unit distance | 158/unit | |

| Parameters for the retailer | ||

| 140 units/year | 52/order | 0.2/unit |

| 720 units | 0.32/unit/unit time | 1.5 unit |

| 300/unit | 5816 units | |

| Parameters for the 3PL | ||

| 0.8 | 0.88 | 0.06 |

| 0.14 | 35/setup | 11.6/unit |

| 0.22/unit/unit time | .12/unit | 2/unit |

| .05/unit | 1/unit | 2/shipment |

| 0.2/container/ unit distance | 0.006 | 25 km |

| 0.014 | 0.02 | 0.06 |

| 0.01/unit | 0.023/unit | |

| Decision Variables | |||||

|---|---|---|---|---|---|

| Optimum Results | 4 | 3 | 0.25 | 4 | 73,021 |

| Decision Variables | |||||

|---|---|---|---|---|---|

| Optimal results under Special Case 1 | 2 | 2 | 0.96 | 4 | 73,375.7 |

| Optimal results under Special Case 2 | 2 | 0 | 0.84 | 4 | 73,328.9 |

| Optimal results under Special Case 3 | 4 | 3 | 0.69 | 4 | 72,629 |

| Parameters | Changes of Inputs (%) | Change of JTC (%) | Parameters | Changes of Inputs (%) | Changes of JTC (%) |

|---|---|---|---|---|---|

| −50 | N.F. | −50 | −13.3 | ||

| −25 | N.F. | −25 | −6.3 | ||

| +25 | + 0.11 | +25 | N.F. | ||

| +50 | +0.17 | +50 | N.F. | ||

| −50 | N.F. | −50 | −4.6 | ||

| −25 | N.F. | −25 | −2.1 | ||

| +25 | + 0.08 | +25 | N.F. | ||

| +50 | +0.12 | +50 | N.F. | ||

| −50 | −0.002 | −50 | N.F. | ||

| −25 | −0.001 | −25 | N.F. | ||

| +25 | +0.001 | +25 | +0.66 | ||

| +50 | +0.002 | +50 | +.96 | ||

| −50 | −0.013 | −50 | N.F. | ||

| −25 | −0.007 | −25 | N.F. | ||

| +25 | +0.007 | +25 | +1.22 | ||

| +50 | +0.013 | +50 | +1.74 | ||

| F | −50 | N.F. | −50 | N.F. | |

| −25 | N.F. | −25 | N.F. | ||

| +25 | +0.43 | +25 | +0.04 | ||

| +50 | +0.62 | +50 | +0.07 | ||

| −50 | −0.046 | c | −50 | +0.04 | |

| −25 | −0.018 | −25 | +0.03 | ||

| +25 | +0.02 | +25 | N.F. | ||

| +50 | +0.03 | +50 | N.F. | ||

| −50 | N.F. | −50 | −0.004 | ||

| −25 | −0.01 | −25 | −0.002 | ||

| +25 | +0.001 | +25 | +0.002 | ||

| +50 | +0.018 | +50 | +0.004 | ||

| −50 | −0.29 | −50 | −28.76 | ||

| −25 | −0.14 | −25 | −14.38 | ||

| +25 | +0.14 | +25 | +14.38 | ||

| +50 | +0.29 | +50 | +28.76 | ||

| −50 | N.F. | −50 | 0.00 | ||

| −25 | N.F. | −25 | 0.00 | ||

| +25 | +0.033 | +25 | 0.00 | ||

| +50 | +0.055 | +50 | 0.00 | ||

| −50 | N.F. | −50 | N.F. | ||

| −25 | N.F. | −25 | −0.01 | ||

| +25 | + 0.334 | +25 | +0.01 | ||

| +50 | + 0.495 | +50 | +0.02 | ||

| −50 | −0.008 | −50 | −0.29 | ||

| −25 | −0.004 | −25 | −0.14 | ||

| +25 | +0.004 | +25 | +0.14 | ||

| +50 | +0.008 | +50 | +0.29 | ||

| −50 | N.F. | −50 | −0.00002 | ||

| −25 | N.F. | −25 | −0.00001 | ||

| +25 | +0.02 | +25 | +0.00001 | ||

| +50 | +0.03 | +50 | +0.00002 | ||

| −50 | −0.002 | −50 | −0.0007 | ||

| −25 | −0.0008 | −25 | −0.0004 | ||

| +25 | +0.0008 | +25 | +0.0004 | ||

| +50 | +0.002 | +50 | +0.0007 | ||

| −50 | N.F | ||||

| −25 | N.F. | ||||

| +25 | +0.05 | ||||

| +50 | +0.07 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mishra, M.; Hota, S.K.; Ghosh, S.K.; Sarkar, B. Controlling Waste and Carbon Emission for a Sustainable Closed-Loop Supply Chain Management under a Cap-and-Trade Strategy. Mathematics 2020, 8, 466. https://doi.org/10.3390/math8040466

Mishra M, Hota SK, Ghosh SK, Sarkar B. Controlling Waste and Carbon Emission for a Sustainable Closed-Loop Supply Chain Management under a Cap-and-Trade Strategy. Mathematics. 2020; 8(4):466. https://doi.org/10.3390/math8040466

Chicago/Turabian StyleMishra, Mowmita, Soumya Kanti Hota, Santanu Kumar Ghosh, and Biswajit Sarkar. 2020. "Controlling Waste and Carbon Emission for a Sustainable Closed-Loop Supply Chain Management under a Cap-and-Trade Strategy" Mathematics 8, no. 4: 466. https://doi.org/10.3390/math8040466

APA StyleMishra, M., Hota, S. K., Ghosh, S. K., & Sarkar, B. (2020). Controlling Waste and Carbon Emission for a Sustainable Closed-Loop Supply Chain Management under a Cap-and-Trade Strategy. Mathematics, 8(4), 466. https://doi.org/10.3390/math8040466