Tail Conditional Expectations Based on Kumaraswamy Dispersion Models

Abstract

:1. Introduction

2. TCE Formula Based on Univariate Kumaraswamy Distribution

3. Portfolio Risk Evaluation with TCE for Non-Negative Independent Losses

- and are independent.

4. TCE for Dependent Bivariate Kumaraswamy Distributions

4.1. The Dirichlet Bivariate Kumaraswamy Model

4.2. The Libby–Novick–Jones–Olkin–Liu Bivariate Kumaraswamy Model

5. Copula-Based Conditional Tail Expectation for Kumaraswamy Dispersion Models

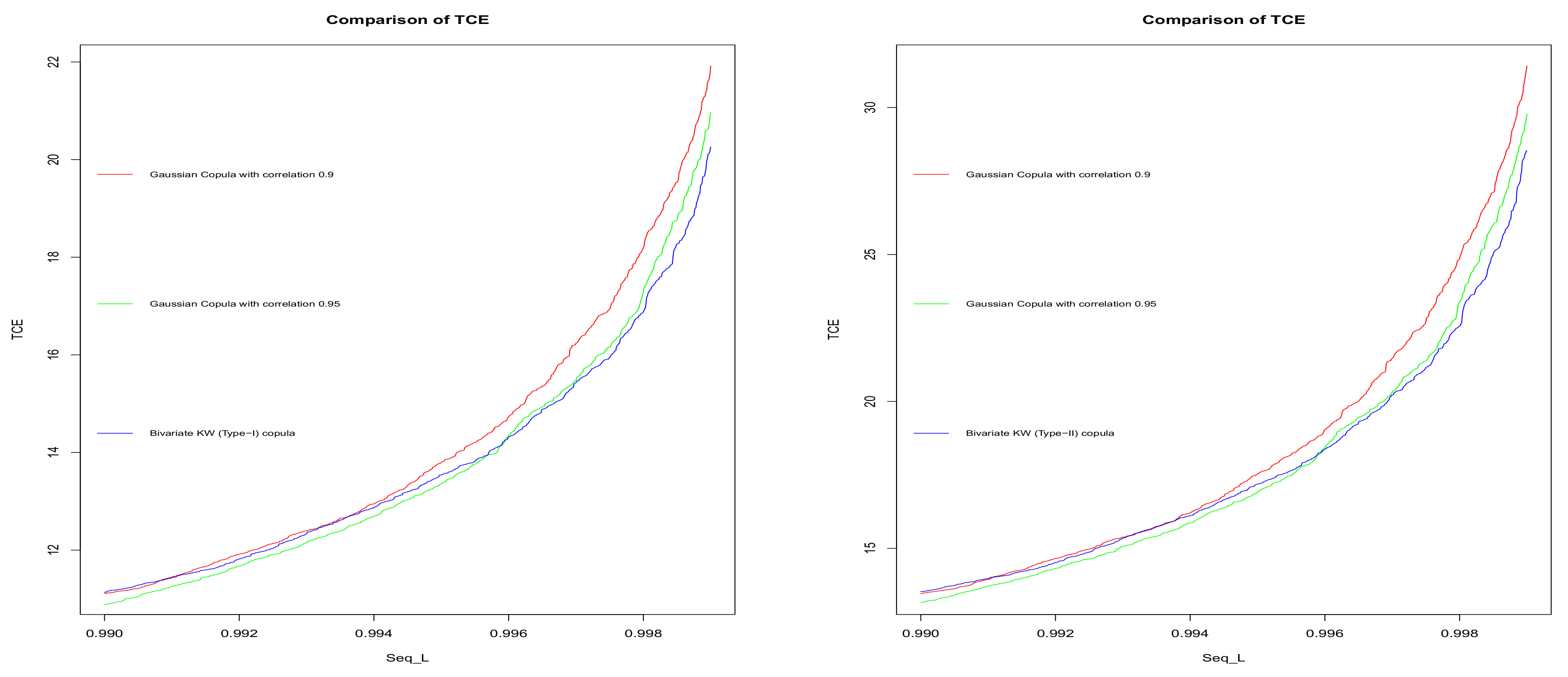

6. Application

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | 1 | 0.8649 | 0.5893 | 0.3231 |

| SMI | 0.8649 | 1 | 0.4529 | 0.8524 |

| CAC | 0.5893 | 0.4529 | 1 | 0.6372 |

| FTSE | 0.3231 | 0.8524 | 0.6372 | 1 |

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | — | 19.4533 | 25.6072 | 26.1129 |

| SMI | 29.4561 | — | 23.4038 | 22.6875 |

| CAC | 34.6823 | 18.6045 | — | 28.5331 |

| FTSE | 32.5709 | 27.4533 | 26.7138 | — |

References

- Artzner, P.; Delbaen, F.; Eber, J.M.; Heath, D. Coherent Measures of Risk. Math. Financ. 1999, 9, 203–228. [Google Scholar] [CrossRef]

- Panjer, H.H.; Jing, J. Solvency and Capital Allocation. Research Report 01-14; Institute of Insurance and Pension Research, University of Waterloo: Waterloo, ON, Canada, 2001. [Google Scholar]

- Landsman, Z.; Valdez, E. Tail Conditional Expectation for Exponential Dispersion Models. ASTIN Bull. J. IAA 2005, 35, 189–209. [Google Scholar] [CrossRef] [Green Version]

- Arnold, B.C.; Ghosh, I. Bivariate beta and Kumaraswamy Models developed using the Arnold-Ng bivariate beta distribution. Revstat Stat. J. 2017, 5, 223–250. [Google Scholar]

- Landsman, Z.; Valdez, E. Tail Conditional Expectation for Elliptical Distributions. N. Am. Actuar. J. 2003, 7, 55–71. [Google Scholar] [CrossRef] [Green Version]

- Furman, E.; Kuznetsov, A.; Su, J.; Zitikis, R. Tail dependence of the Gaussian copula revisited. Insur. Math. Econ. 2016, 69, 97–103. [Google Scholar] [CrossRef] [Green Version]

- Arnold, B.C.; Ghosh, I. Some alternative Bivariate Kumaraswamy models. Commun. Stat. Theory Methods 2017, 46, 9335–9354. [Google Scholar] [CrossRef]

- Lin, F.; Peng, L.; Xie, J.; Yang, J. Stochastic distortion and its transformed copula. Insur. Math. Econ. 2018, 79, 148–166. [Google Scholar] [CrossRef]

- Brahim, B.; Fatah, B.; Djabrane, Y. Copula conditional tail expectation for multivariate financial risks. Arab. J. Math. Sci. 2018, 24, 82–100. [Google Scholar] [CrossRef]

- Brahimi, B. Involving copula functions in conditional tail expectation. arXiv 2012, arXiv:1205.4345. [Google Scholar]

- Ouyang, Z.-S.; Liao, H.; Yang, X.-Q. Modeling dependence based on mixture copulas and its application in risk management. Appl. Math. J. Chin. Univ. 2009, 24, 393–401. [Google Scholar] [CrossRef]

- Ghosh, I.; Ray, S. Some alternative bivariate Kumaraswamy type distributions via copula with application in risk management. J. Stat. Theory Pract. 2016, 10, 693–706. [Google Scholar] [CrossRef]

- Ghosh, I. Bivariate Kumaraswamy Models via Modified FGM Copulas: Properties and Applications. J. Risk Financ. Manag. 2017, 10, 19. [Google Scholar] [CrossRef] [Green Version]

- Nelder, J.A.; Wedderburn, R.W. Generalized linear models. J. R. Stat. Soc. Ser. A 1972, 135, 370–384. [Google Scholar] [CrossRef]

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | 1 | 0.4052 | 0.4374 | 0.3706 |

| SMI | 0.4052 | 1 | 0.3791 | 0.3924 |

| CAC | 0.4374 | 0.3791 | 1 | 0.4076 |

| FTSE | 0.3706 | 0.3924 | 0.4076 | 1 |

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | ∞ | 0.3422 | 0.4251 | 0.0789 |

| SMI | 0.3422 | ∞ | 0.7425 | 0.4786 |

| CAC | 0.4251 | 0.7425 | ∞ | 0.5491 |

| FTSE | 1.0789 | 0.4786 | 0.5491 | ∞ |

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | ∞ | 0.5672 | 0.3827 | 0.1874 |

| SMI | 0.5672 | ∞ | 1.5275 | 0.6847 |

| CAC | 0.3827 | 0.5275 | ∞ | 0.1945 |

| FTSE | 0.1874 | 0.6847 | 0.1945 | ∞ |

| Variable | DAX | SMI | CAC | FTSE |

|---|---|---|---|---|

| DAX | — | 19.4533 | 17.6087 | 21.9731 |

| SMI | 14.2812 | — | 23.4038 | 17.7486 |

| CAC | 18.6328 | 18.6045 | — | 20.2132 |

| FTSE | 14.5709 | 13.7593 | 22.4079 | — |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ghosh, I.; Marques, F.J. Tail Conditional Expectations Based on Kumaraswamy Dispersion Models. Mathematics 2021, 9, 1478. https://doi.org/10.3390/math9131478

Ghosh I, Marques FJ. Tail Conditional Expectations Based on Kumaraswamy Dispersion Models. Mathematics. 2021; 9(13):1478. https://doi.org/10.3390/math9131478

Chicago/Turabian StyleGhosh, Indranil, and Filipe J. Marques. 2021. "Tail Conditional Expectations Based on Kumaraswamy Dispersion Models" Mathematics 9, no. 13: 1478. https://doi.org/10.3390/math9131478

APA StyleGhosh, I., & Marques, F. J. (2021). Tail Conditional Expectations Based on Kumaraswamy Dispersion Models. Mathematics, 9(13), 1478. https://doi.org/10.3390/math9131478