1. Introduction

The payments industry has historically been characterized by the presence of network effects, high fixed costs, and economies of scale [

1]. Payment systems and remittances are considered the backbone of the financial sector, fostering economic growth and financial development by reducing systemic and settlement risks, facilitating proper liquidity management, and creating effective monetary policy [

2]. Payment systems are of central importance for supporting financial inclusion; a transaction account allows people to make and receive payments in a cost-effective way [

3]. Today, the global payments landscape is experiencing fundamental change [

4], driven by the emergence of new technology and business methods, the rise of new economic powers, and changes in the global currency landscape [

5]. A payment nowadays is viewed as something more than just the settlement of a transaction or the movement of funds. The broader commercial, retail, investment and public sector environments are taken into account, and the payment-related activities (such as investment decisions, trade-related financing and risk mitigation, the cross-border movement of wages and pensions, and more) make up the basis on which payment system providers develop better propositions [

6,

7,

8]. Innovative payment methods introduced by non-banking players are increasingly changing the reality of traditional payment systems [

9]. Even though the global payments business is already vast, it is expected to continue to expand under the influence of a number of factors and trends, some of which are having an impact at this very moment [

6]. Global demographics are affecting the payments landscape by redistributing financial resources across borders. Fast-growing markets in Asia, Africa, and elsewhere are developing their own payment propositions and systems, including for e-commerce [

10], especially since inflation in these regions significantly contributes to financial development in the short and long term [

11]. In this respect, international remittances, especially to developing countries, represent another developing source of global payment flows requiring the development of systems to serve them [

12].

The transformation of the global payment system takes place in a segmented manner [

13]. Revision of the competitive environment, arrival of non-traditional suppliers on the market, development of new solutions and strategic alliances, and increasingly observed convergence all applies to products and solutions related to payments and technology platforms and clearing opportunities that are becoming more global [

14]. With the emergence of a young tech-savvy generation, the expectations of retail and commercial customers for payments are becoming more and more consistent. They put forward more demands for convenience, security and flexibility of payments with the use of the most recent technologies [

4]. What is more, today, consumer preferences are changing due to the convenience of contactless cards and mobile payments [

15,

16].

Notwithstanding the above, commercial banks can be key traditional market players. The central factors influencing competitive advantages of traditional payment service providers embrace competitive product prices, easy access to services, range of services offered, quality of service and management, and e-marketing innovativeness [

17]. Indeed, the banking sector can now remain competitive in the payment system market if it responds quickly enough and takes advantage of the opportunities on offer in the global payments business [

18]. Thus, the development of information and communication technologies is central to payment innovation in the 21st century.

The fact that competition is a complex concept and therefore cannot be directly observed has led to the development of many approaches to its assessment [

19]. To a large extent, assessment of the competition in the banking industry has a long tradition. Early research in this field focused on the relationship between market structure and performance, or the structure–conduct–performance paradigm [

20,

21]. However, some authors raised serious doubts about its reliability, which stimulated the development of non-structural measures of competition, like the Lerner index, the conjectural variation model, the Panzar–Rosse model and the Boone indicator [

22,

23]. To assess the factors of competition and stability in the financial services market, many of them propose applying the Fuzzy Delphi Method (FDM) and the Interpretive Structural Modeling (ISM) approach [

24]. On the other hand, while some researchers may prefer one model over the other, there is still no consensus on the best measure to assess competition. Different indicators of competition do not provide the same conclusions. A significant drawback of most approaches is their complexity and the need to collect a large amount of data. For this particular reason, such assessment can only be carried out by narrow specialists.

Thus, the main gap in the existing literature is considered to be the lack of simple approaches in determining the factors affecting the global competition of payment systems to study it as a qualitative phenomenon. The article formulates the following research questions (RQ): RQ1: “What are the current trends of competition in the global market of payment systems?”; RQ2: “What are the promising trends and the role of financial technology (FinTech) in the global competition of payment systems?”; RQ3: “What groups of factors influence the competitiveness of the payment system today?” RQ4: “How are the factors of global competition of payment systems interpreted by active payment market participants?”.

The central aim of this study was to test a simple and interesting economic-mathematical approach to interpret the relevant factors affecting the global competition of payment systems. This was expected to enable the examination of the qualitative phenomenon of competition in the global payment system market through quantitative interdisciplinary approaches. As additional research goals, the authors focused on identifying and analyzing the current global payment system market’s competitive trends and investigated the perception of the introduction of FinTech innovations by new market players as a decisive factor in payment systems’ competitiveness.

3. Materials and Methods

3.1. Methods and Instruments

The present study is based on the analysis of data collected through a survey of FinTech companies offering payment services to customers of traditional payment institutions.

Descriptive statistics for numeric variables obtained in SPSS Statistics was used in evaluating the potential of using FinTech solutions to improve the competitiveness of payment systems. The association between variables was assessed using the Stata software package.

Since the study benefited from an ordinal measurement scale, the median value (MD) was used as a measure of central tendency and the interquartile range (IQR) as a measure of statistical dispersion. In cases when elements could be grouped, the reliability of internal consistency was measured using Cronbach’s alpha (α) (0.82). The Friedman test, a nonparametric test for comparing more than two related samples, was applied to rank-order the measures. Differences between the studied groups were determined via posteriori comparison. The comparison of the absolute values of the severity of shifts in one direction or another was carried out using the Wilcoxon test, used to compare the absolute values of differences. The issue of multiple comparisons arising in the posteriori test was eliminated through Bonferroni correction, the simplest and the most popular approach for correcting type 1 errors. The Wald test was employed to assess constraints on statistical parameters. The Pearson’s r correlation was used to determine whether there was a linear relationship between the two variables.

3.2. Study Population

The sample of FinTech representatives was generated in 2019 using LinkedIn. The choice of this platform can be explained by its focus on finding and establishing business contacts. LinkedIn is a network of more than 500 million professionals representing 150 industries from 200 countries around the world, which actually meets the requirements for the respondents to be engaged in business, as well as for their geographical diversification. The choice of LinkedIn was also dictated by the fact that it has many representatives of emerging companies that are active in their segment and tend to respond quickly to the changing competitive environment.

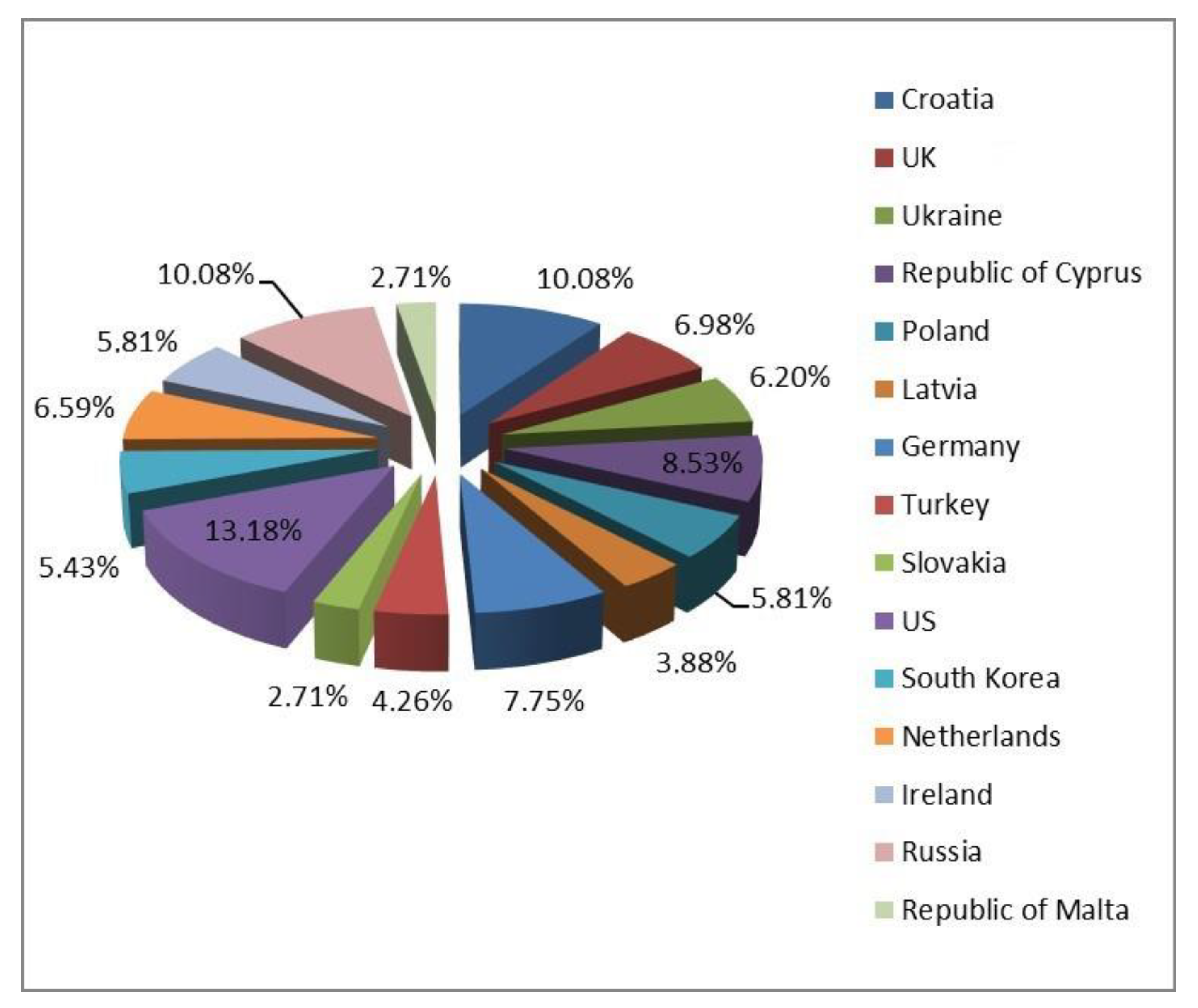

When selecting the study respondents, the key factor was having at least three years of experience in FinTech (both in startups and mature companies like Cake, Sthaler, WorldRemit, or Klarna) and experience in developing payment systems for large non-traditional players, e.g., Amazon, Apple, or Samsung. In total, an e-mail invitation asking to participate in an online survey and providing a link to the questionnaire was sent to 320 candidates. Of them, 271 responded positively, and 258 completed the questionnaire they had been sent. The distribution of respondents by region is depicted in

Figure 5.

The need to balance the composition of the respondents led to the organization of an additional survey. With the help of the LinkedIn social network, representatives of FinTech companies from the Asia-Pacific region, as well as from the Gulf countries and African states, were found and invited to become the study respondents. Thus, invitations to be enrolled in the survey (it was held in an online mode) were sent to 287 individuals. Positive responses were collected from 262 potential respondents, though completed questionnaires were received from only 246 of them (

n = 246). The results of additional sampling are presented in

Figure 6.

Hence, the final sample consisted of 504 individuals from 28 countries.

3.3. Study Design

Summarizing the existing theoretical framework allowed us to identify four main categories of factors, which, within the current research, were defined as exerting the most substantial influence on the competitiveness of the payment system [

13,

49,

65,

66,

67,

68]:

- −

Costs, involved in implementing and maintaining availability solutions.

- −

Service channels, which refers to innovations in products and services that allow for better communication, marketing and sales, as well as the development of new proportions, fueling the competition.

- −

Privacy and Security, implying that technology must ensure that client’s personal information and data of transactions are stored securely, privacy is maintained, and risks are reduced.

- −

Quality and Efficiency, which refers to the use of technology as a means of improving the quality of service and efficiency of payments.

In the survey, respondents were asked to enter the country in which their company is located and rank their perceptions of whether FinTech innovations facilitate the gain of a competitive advantage. Respondents were asked to rank the impact of FinTech innovations on the competitiveness of the payment systems using a 5-point Likert scale [

69], ranging from ‘1’ (FinTech innovation is perceived to have a negative impact on the competitiveness), to ‘5’ (FinTech innovation is perceived to have a positive impact on the competitiveness). The following items were designed to assess the importance of those factors above to competitiveness: ‘Costs’, ‘Service channels’, ‘Privacy and Security’, and ‘Quality and Efficiency’. Each of these items was on a 5-point Likert scale, ranging from ‘1’ (no importance) to ‘5’ (high importance).

As regards the study design, all participants were told that participation in the survey was voluntary. The sample thus includes representatives of FinTech companies who expressed a desire to contribute to modernizing the methodological apparatus for identifying factors of the payment system global competitiveness. As a result, this study draws on data not subjected to the authors’ interpretation and preliminary statistical processing by government services and commercial agencies. Hence, the involvement of FinTech representatives made it possible to improve the objectivity of the study.

3.4. Limitations

Some decisions made regarding the research procedure make it impossible to use the goodness-of-fit test to evaluate whether distributions differ significantly from each other with respect to the geographic groups. In addition, the Bonferroni correction used to solve the issue of multiple comparisons could increase the risk of generating type 2 errors (false negatives).

Another source of possible uncertainty is the lack of the ability to form a research sample based on the share of FinTech companies’ distribution across countries. The impossibility of such an approach to be realized in an adequate form is explained by a rather substantial part of the shadow economy in many states, which would actually have made the FinTech share present with large errors in advance. Another limitation is associated with the voluntary nature of the survey, which did not allow an extensive range of countries.

3.5. Ethics

The respondents were guaranteed non-disclosure of personal and professional data. When filling out the questionnaire, respondents were told that they would indicate only the country of the company’s origin, and that no personal data or details about the company would be taken. Each questionnaire was assigned a number.

5. Discussion

The global payments landscape is in a state of transformation. Banks and other financial institutions cannot afford to leave non-bank payment platforms and solutions out of account. Banks and other payment service providers seeking to make a profit must be aware of competitive dynamics that redefine the payments market to ensure that their propositions align with customer expectations and needs [

70]. Otherwise, the appealing payment options such as PayPal, Google Wallet, Bitcoin, Facebook and M-Pesa will take over [

3]. It is confirmed that in order to win the competition for payments, it is necessary to develop new forms of partnerships with modern technological financial companies [

2] and adapt to the requirements of a new generation of customers. As a result of the survey, the theses of earlier works have been confirmed, testifying that players in the global payment market should become more flexible, use the latest technologies to develop cross-product offers and develop market strategies, which correspond to the needs and nature of the payment space in each market, actively focusing on fast-growing segments [

6], because the modern perception of competitiveness is primarily related to safe and effective satisfaction of consumer demands.

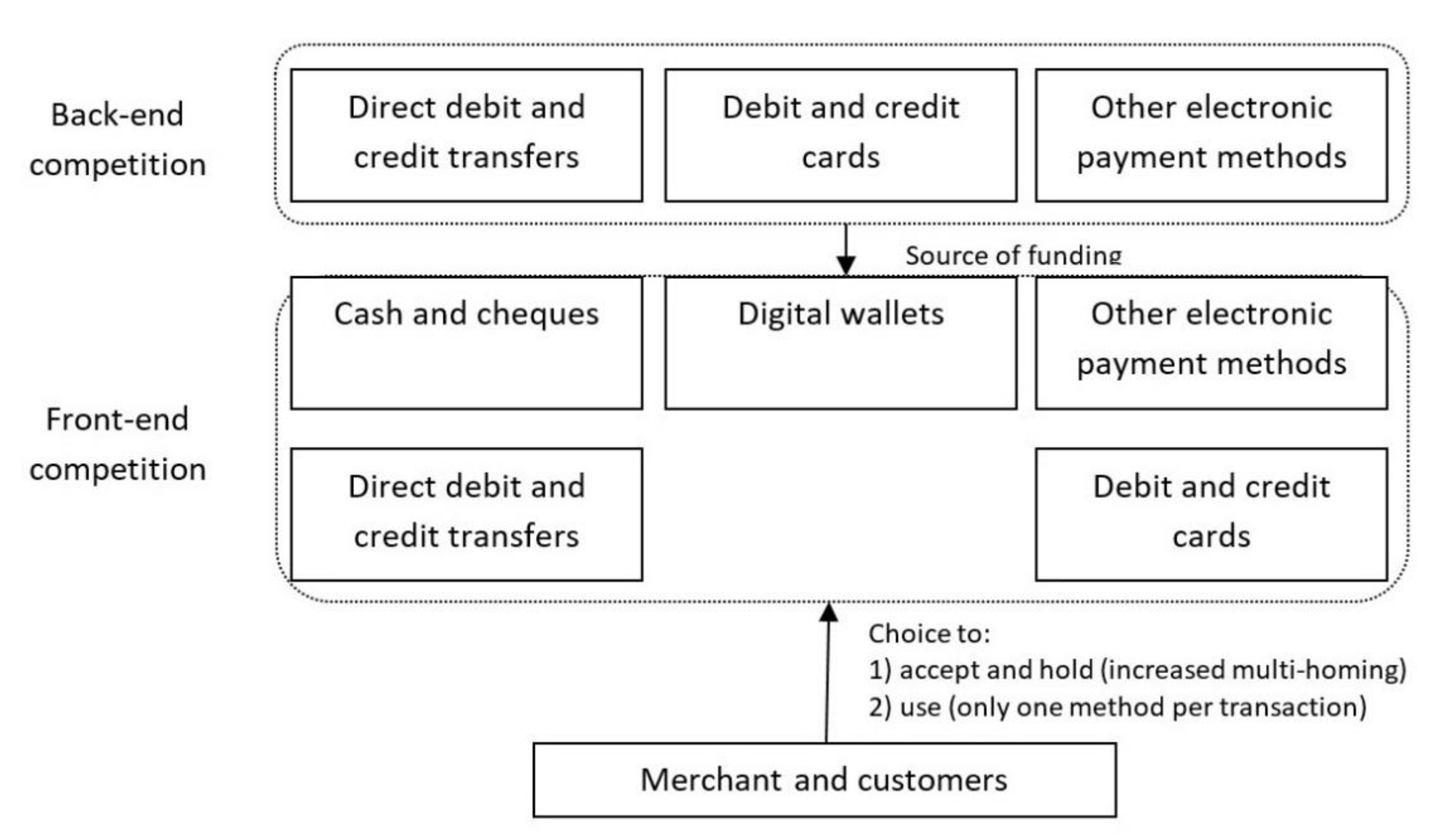

New entrants can compete successfully in the market if they leverage their existing customer bases (e.g., Apple) or if they introduce additional services based on the existing infrastructure (e.g., Klarna) [

26]. The competition between payment service providers is increasingly aggressive. Consumers are increasingly using more than one payment method, intensifying competition for payment methods, and the growth of digital wallet technology facilitates both front-end and back-end competition [

9]. The thesis that FinTech is now becoming an integral part of the payment industry is confirmed [

56], and the use of these innovations contributes to the competitiveness of payment systems [

65]. Qualitative analysis undercuts the need to develop and implement innovative payment options and identify potential drivers of competitiveness in the payment market [

71]. The results of this study are consistent with the view that the main factors affecting the competitiveness of the payment system are technological costs, service channels, privacy and security, quality and efficiency of service [

72]. Moreover, unlike studies that have placed the main emphasis on the competitiveness of payment innovations based on user confidence in FinTech [

63], in this case the results are confirmed and reveal that the greatest statistical significance is in the implementation and maintenance costs factors as well as user satisfaction [

59,

68].

6. Conclusions

The present work evidences the success of approbation of an interesting economic and mathematical approach to interpreting the perception of (1) new global payment market entrants, (2) the impact of FinTech innovations on the companies’ competitiveness, and (3) a quantitative assessment of the top-used quality-related competition trends. The analysis of survey results suggests that the perception of the payment system’s competitiveness is largely associated with low technology costs and efficient customer satisfaction. At the same time, factors such as high quality and efficiency of the payment product or service, high speed of transactions, security, privacy, and low risk are also perceived as important. In general, the use of FinTech innovations is expected to improve the competitiveness of payment systems (M = 4.32).

From the analysis of the ordered logistic regression results, the examined factors collectively explain almost half of the variation in perceptions (Pseudo R-Squared = 0.4886). Variables that yield statistically significant coefficients are ‘implementation costs’ (z = 1.74), ‘maintenance and servicing costs’ (z = 3.30), and ‘customer satisfaction’ (z = 3.15). The analysis of correlations indicates that the perception of FinTech innovations is that they determine the competitiveness of payment systems.

The study has some limitations, which include decisions made about the research procedure—they make it difficult to use the criterion of agreement to assess differences in the distribution across geographic groups. The lack of opportunity to form a research sample based on FinTech companies’ distribution by country should be perceived as a source of possible uncertainty. In the future, it would be interesting to study the perception of global payment system competitiveness factors, taking into account the regional aspect of financial companies’ operations.

Nevertheless, the study managed to analyze the perception of FinTech innovation implementation by new market participants and offer a simple economic-mathematical approach to the interpretation of factors affecting the global competition of payment systems. The approach is recommended when developing a competitive market strategy for FinTech companies wishing to achieve a high competitive position.

The findings obtained may be of interest to specialists and researchers dealing with the dynamics of competition in the global payment business, payment innovations, or the convergence and transformation of the payment industry. The proposed approach is also expected to contribute to the development of interdisciplinarity and expand the range of contact points of the journal’s readership from related fields.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}