1. Introduction

Since the 1980s, asset co-movement has attracted the attention of financial researchers (see the pioneer paper of Meese and Rogoff [

1]). Co-movement plays a critical role for asset allocation, portfolio diversification or risk management, and its causes have been studied from many points of view. Some authors found that it depends on market information capitalized in asset prices (Roll [

2]; Katsiampa [

3]). Others attributed the co-movement to market order flows and order type (Domowitz et al. [

4]). Byrne et al. [

5] concluded that global inflation explains most of the global yield co-movement. Some researchers also considered that co-movement is affected by variables that reflect different institutional aspects, such as international macroeconomic policy (Parsley and Popper [

6]). Other groups attributed the co-movement to market proximity (Edwards and Susmel [

7] or Lee [

8]).

In this paper, we focus on the growing interest in the study of the co-movement of volatility, as its movement affects financial assets in various ways, exerting a great influence on risk management, portfolio selection, pricing of derivatives and for setting regulatory policy.

The pioneer paper of Hamao et al. [

9] documented the existence of price volatility effects across Japanese, London and New York financial markets. The authors found that the spillover effects are only significant in the case of the Japanese market. Recently, Susmel and Engle [

10] examined the timing of mean and volatility spillovers between New York and London equity markets. The authors reported no evidence of significant volatility spillovers.

Fleming et al. [

11] used a simple model of speculative trading to study the role of information in creating volatility linkages between markets. In the same line, Dávila and Parlatore [

12] found that when prices are uninformative, there is a positive (negative) co-movement between price informativeness and price volatility, and they concluded that stocks with more volatility prices are likely to be less informative, and vice versa.

Edwards and Susmel [

7] provided evidence of significant volatility co-movement across financial markets in the emerging nations. The authors found evidence that these connections go beyond geographical proximity.

Jondeau and Rockinger [

13] reported evidence of covariability of volatility between five stock-index returns and six foreign-exchange returns sampled at a daily frequency. The authors concluded that extreme realizations tend to occur simultaneously on different markets.

Gabudean [

14] examined the difference in volatility behavior between a stock that is part of an index and one that is not. The author found that volatilities co-move more after a stock becomes part of the index, mainly at hourly frequency and less at a daily one. Calvet et al. [

15] found strong patterns in volatility co-movement between currencies. Volatility components tend to have high correlation when their durations are similar, and low correlations otherwise.

Lee [

8] studied the volatility spillover effect within six Asian countries for the period from 1985 to 2004, finding that there are significant volatility spillover effects between them. Modi et al. [

16] used various alternative techniques for recognizing co-movement resulting among the selected developed stock markets and the emerging stock markets of the world. These authors found that all the markets showed positive average daily returns and that there was considerable volatility in the correlations between the eight stock markets over time. Regarding the co-movement between markets, it was concluded that the eight stock markets are fragmented into two major components.

Chen et al. [

17] reported evidence of a common time varying volatility factor in the United Kingdom, Singapore and Australia. In the same line Zhang and Ding [

18] analyzed the volatility co-movements in different commodity futures markets, finding that various volatility measures of commodity return share a common trend, which can be interpreted as a common market volatility factor. Apparently, liquidity is an important transmission channel for volatility shocks.

Bašta and Molnár [

19] showed that the implied volatility of VIX index and the implied volatility of the oil market are highly correlated. The authors also found that the correlation between the stock and oil market volatility is time-varying and depends on the time scale. Using vector autoregressive models–multivariate generalized autoregressive conditional heteroscedastic models (VAR-MGARCH), Huang and Wang [

20] investigated the systemic importance of the volatility spillover.

Katsiampa [

3] investigated the volatility dynamics of Bitcoin and Ether, finding that the volatility of the two cryptocurrencies is responsive to major news. Fernandez-Aviles et al. [

21] did not find clear co-movement patterns in volatility of commodity markets in extreme financial episodes worldwide.

In a different perspective, Zheng et al. [

22] proposed a dynamic conditional correlation-mixed data sample (DCCMIDAS) model to analyze the contagion between the business cycle and financial volatility. Wang and Guo [

23] used a DCC-MGARCH model to study the stock market volatility co-movement of China and other G20 members, finding that the performance and influencing factors of co- movement are time varying.

Recently, Liu and Jiang [

24] have introduced a propagation dynamics model, called WSI mode, based on the classical discrete virus propagation mechanism, to study the volatility co-movement through different market indexes. Qiaoa et al. [

25] used wavelet coherence and the correlation network to examine the co-movement relationship among representative cryptocurrencies from the perspectives of returns and volatility. These authors reported evidence of co-movement and hedging effects.

To document co-movement, financial literature has proposed different variations of ARCH [

10,

17] and GARCH models [

13]. Other approaches have been the GARCH-M model [

9], the GMM model [

11], the SWARCH model [

7], the Multiplicative Error models (MEM) [

14], the Markov-Switching Multifractal (MSM) [

15], the bivariate Diagonal BEKK model [

3], the DCC-MGARCH model [

23], the DCCMIDAS model [

22] or the VAR-MGARCH model. More complex methods were introduced by Baštaa and Molnár [

19] where the authors used a Continuous Wavelet Transform, Lee [

8] where Bivariate Vector Autoregression-Generalized Autoregressive Conditional Heteroskedasticity Model is used, Fernandez-Aviles et al. [

21] where the authors proposed a combined ES-MDS procedure, the wavelet coherence analysis of Qiaoa et al. [

25] and the WSI model introduced by Liu and Jiang [

24].

In this paper, we propose to look at the co-movement in volatility from a different approach based on a function of physical particle systems and the previous works of Clara Rahola et al. [

26], Sánchez Granero et al. [

27], Puertas et al. [

28] and López García et al. [

29]. Unlike previous literature, this paper looks to several aspects of the volatility co-movement among the stocks of the same market and region. First, we study the volatility co-movement dynamically over time. This allows us to detect those periods of time when the volatility co-movement is higher or lower, and we can try to identify the source of the co-movement. Then, we focus on the volatility and log-price co-movement of stocks with similar volatility. We find that this co-movement is higher than the full market co-movement. In addition, an inverse relationship between co-movement and volatility is found. This is a pattern that repeats most of the years. Moreover, by repeating the calculation subtracting the market, we find that almost all the volatility and log-price co-movement is explained by the market. Finally, we study the co-movement between stocks of different volatilities. The analogy with physical systems allows us to conclude that most of the co-movement is originated by herding, with uncorrelated motion around the market. In crisis periods, however, a higher degree of co-movement beyond the market can be identified.

2. Methodology

In order to study co-movement, we borrow the analysis of physical many-body systems and adapt it to the financial markets. It is well known that the movement of assets can be described, as a first approach, with Brownian motion, initially developed for suspended particles or macromolecules in a solvent [

30]. The most simple system showing Brownian motion is hard particles, without any internal degrees of freedom, realized experimentally as sub-micrometer particles suspended in water or other solvents, generally known as colloidal systems [

31]. These can be directly observed through the microscope allowing direct access to their time-resolved positions. Our approach from physics considers a portfolio as if it were a system of many bodies [

28], using the index to represent a characteristic point that characterizes the whole system, such as the center of mass. Following the classical mechanics of multi-body systems, internal forces only affect the relative motion of a body with respect to the center of mass, so a proper estimate of co-motion due to interactions, within a physical approach, can only be made by subtracting the center of mass (or index). However, we are also interested here in the co-movement of the full market, without subtracting the center of mass.

Cooperative motion in colloids has been studied in connection to vitrification. Upon cooling down the system, its dynamic slows down significantly until the structural relaxation time scale becomes larger than the observational time scale, and the system becomes effectively a solid; it is said to have crossed the glass transition, or vitrified. Cooperative motions appear then as a route for relaxing the density or temperature fluctuations, when single particle dynamics is hindered [

32]. In fluids, on the other hand, collective motions are negligible as single particle diffusion is enough to relax these functions. Several parameters have been devised for accessing these collective motions [

33,

34], which have been used to study the co-movement in stocks [

28].

Based on this analysis, three functions were proposed in [

29] to monitor cooperative dynamics in financial systems using the log-price. As the results applying the different functions were very similar, it has been decided to use the

function in this work, as it was the one that provided more information in the research of co-movement in [

29]. This function is defined as follows:

where

is the variable under study (log-price,

, or volatility,

, in this work) of asset

i at time

t,

. The summation runs over all pairs of assets

i,

j, excluding

.

is the average of

over time origins

t.

compares the change of variable y for stocks i and j in the time interval , averaging the product of changes for all pairs of particles. The function thus reaches values from to 1. When the values are close to 0 it means that there is no co-movement; if they are greater than 0 it means that the assets are moving in the same direction; if, on the contrary, the results are less than 0, it means that the assets are moving in the opposite direction. Furthermore, following the analogy with physical systems, we consider the center of mass of the system as the average position, . This index is affected only by external forces and represents a particular point in the system.

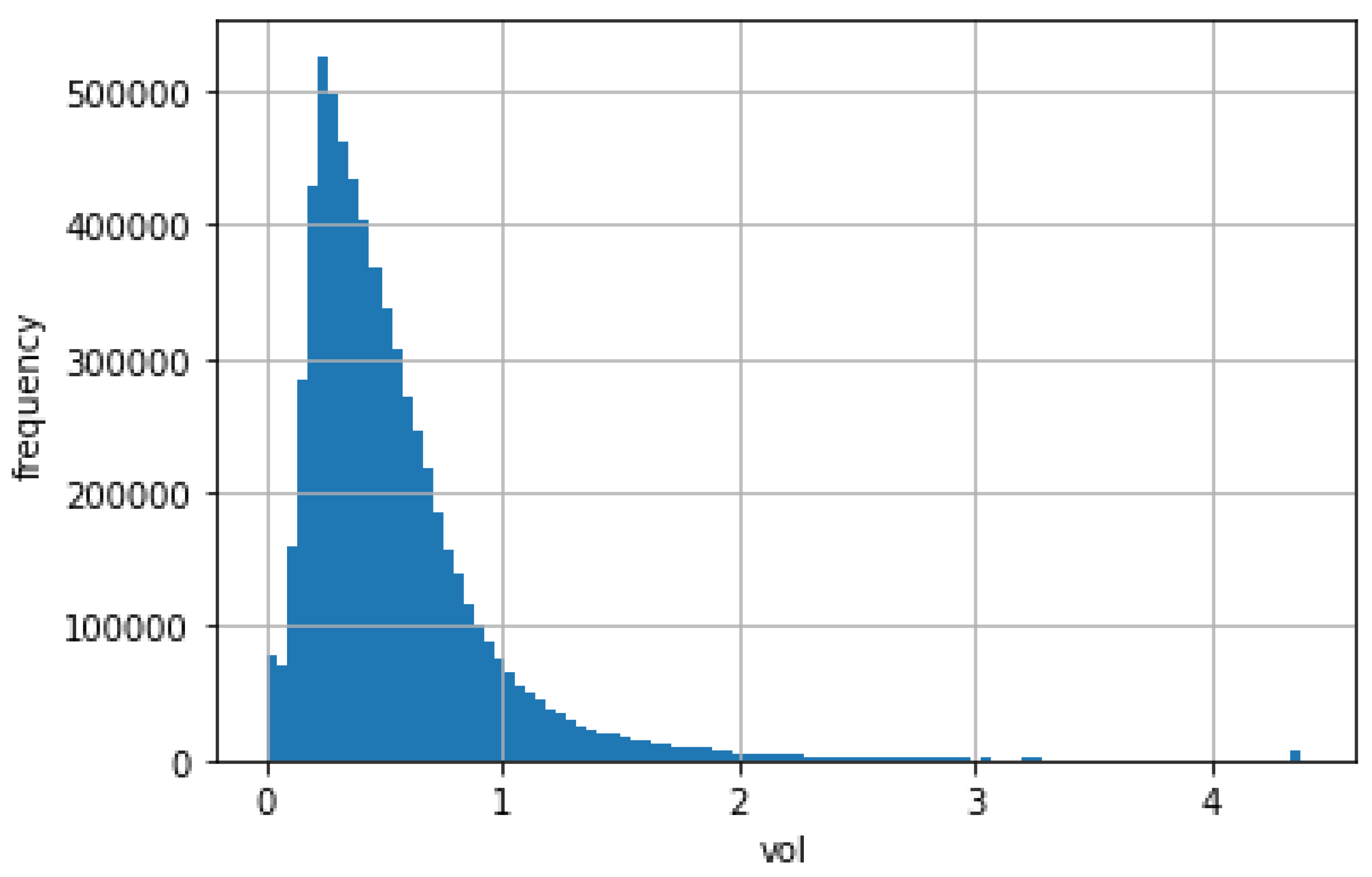

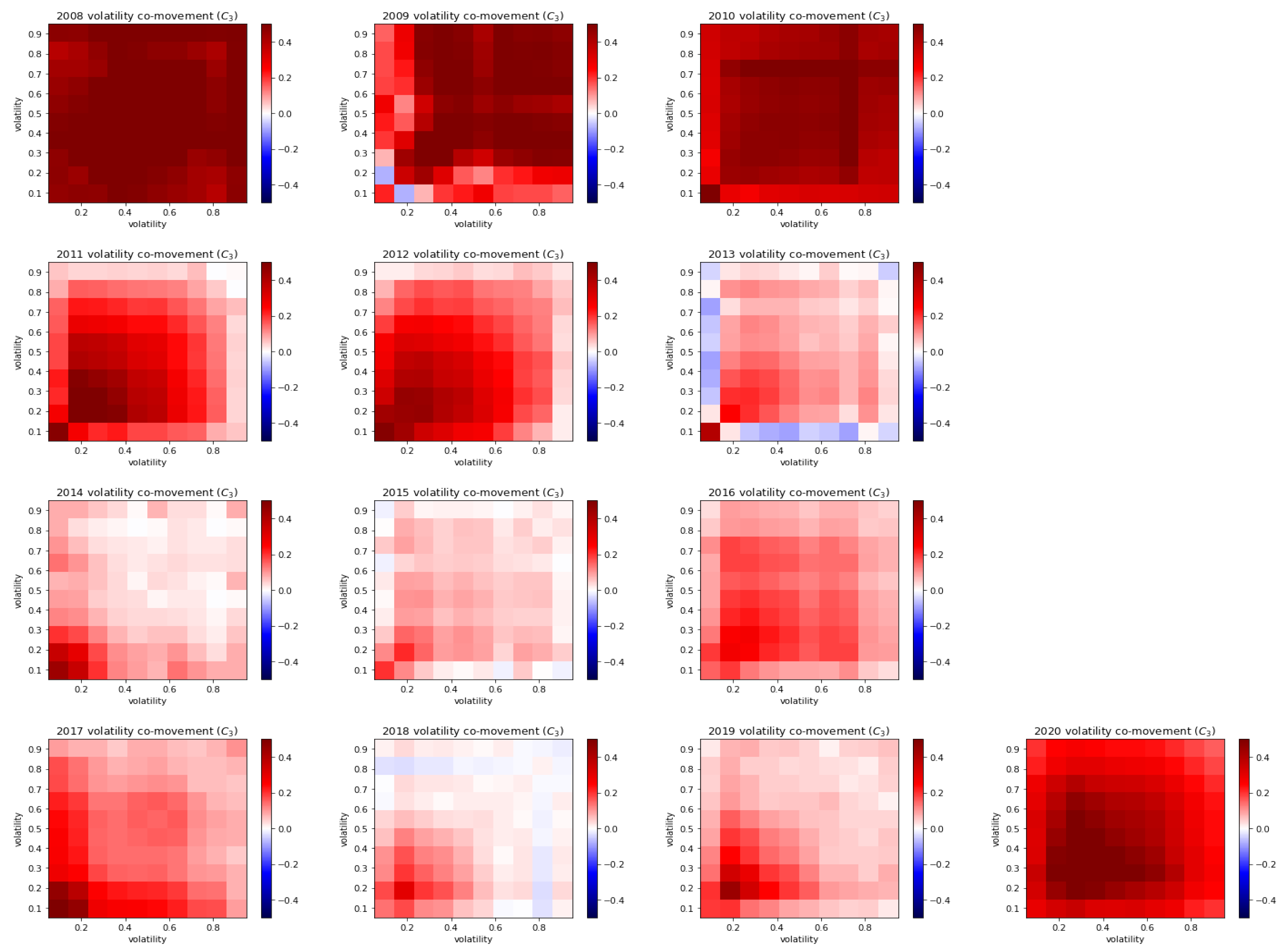

In this work, a set of 3577 American shares for the period from 2008 to 2020, sampled daily, has been used. The volatility of stock i at time t, , is calculated as the standard deviation of the log-returns of one year (250 trading days) ending at t. Other values of the time interval provide qualitatively similar results.

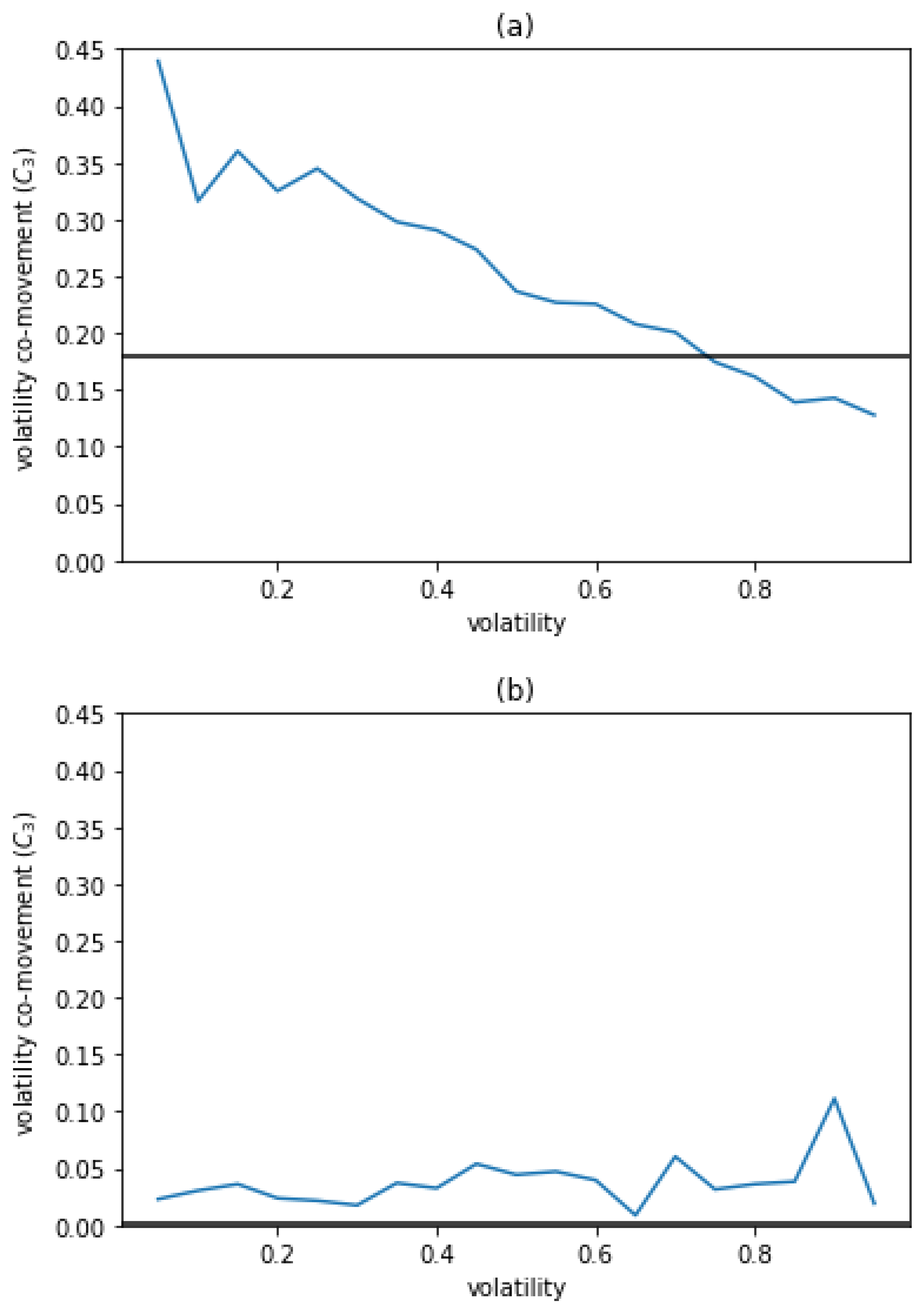

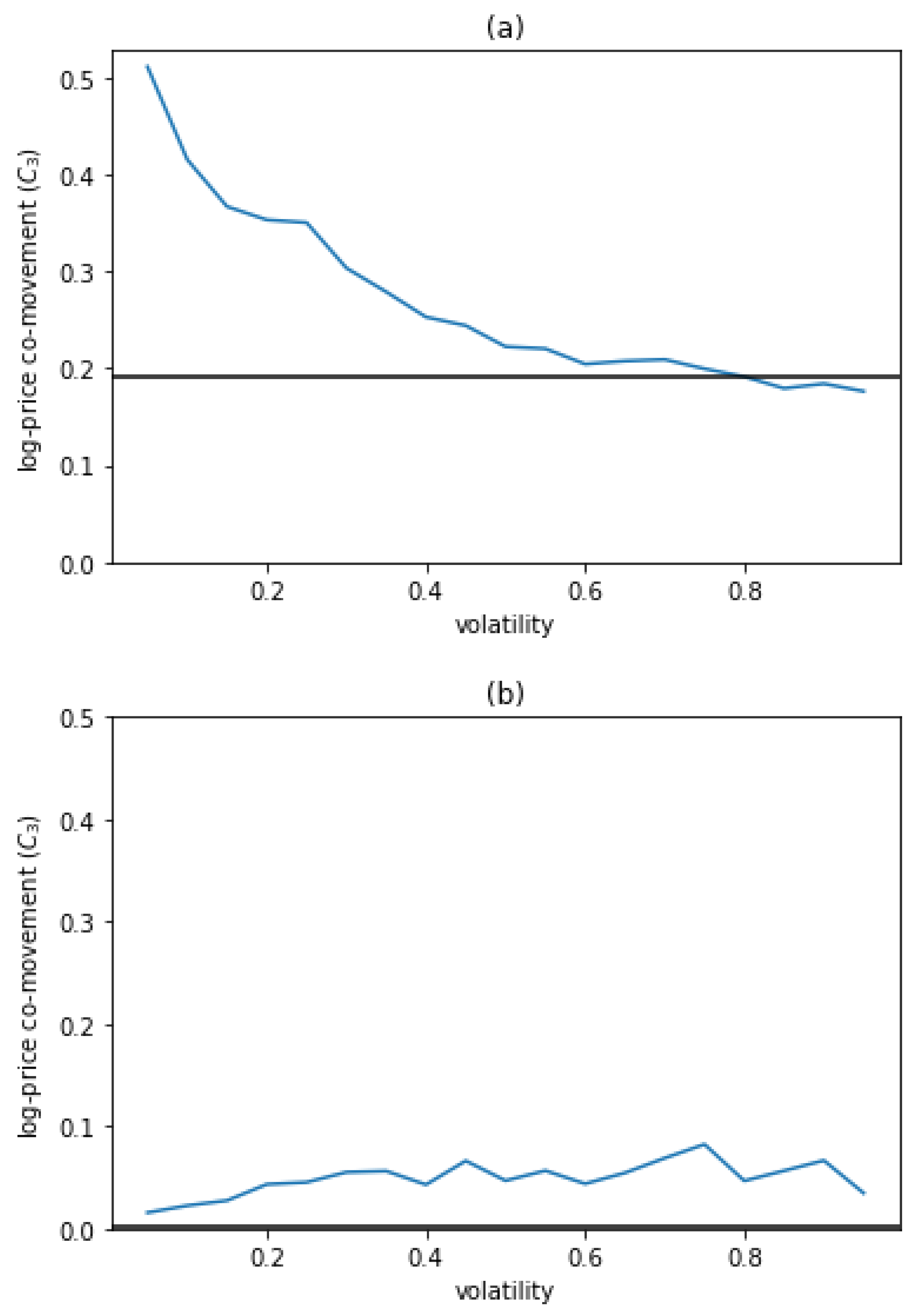

The calculations of and are performed with the bare data and with . This can serve then to identify the origin of co-movement: if it disappears when the motion of the center of mass is subtracted, there are no important dynamic correlations between individual stocks; on the other hand, if it remains after the center of mass is subtracted, it indicates the existence of dynamic correlations among stocks or groups of stocks.

It must be noted that, different from other techniques in the literature, the present method allows us to analyze the whole set of stocks in a given market, or a particular subset.

4. Conclusions

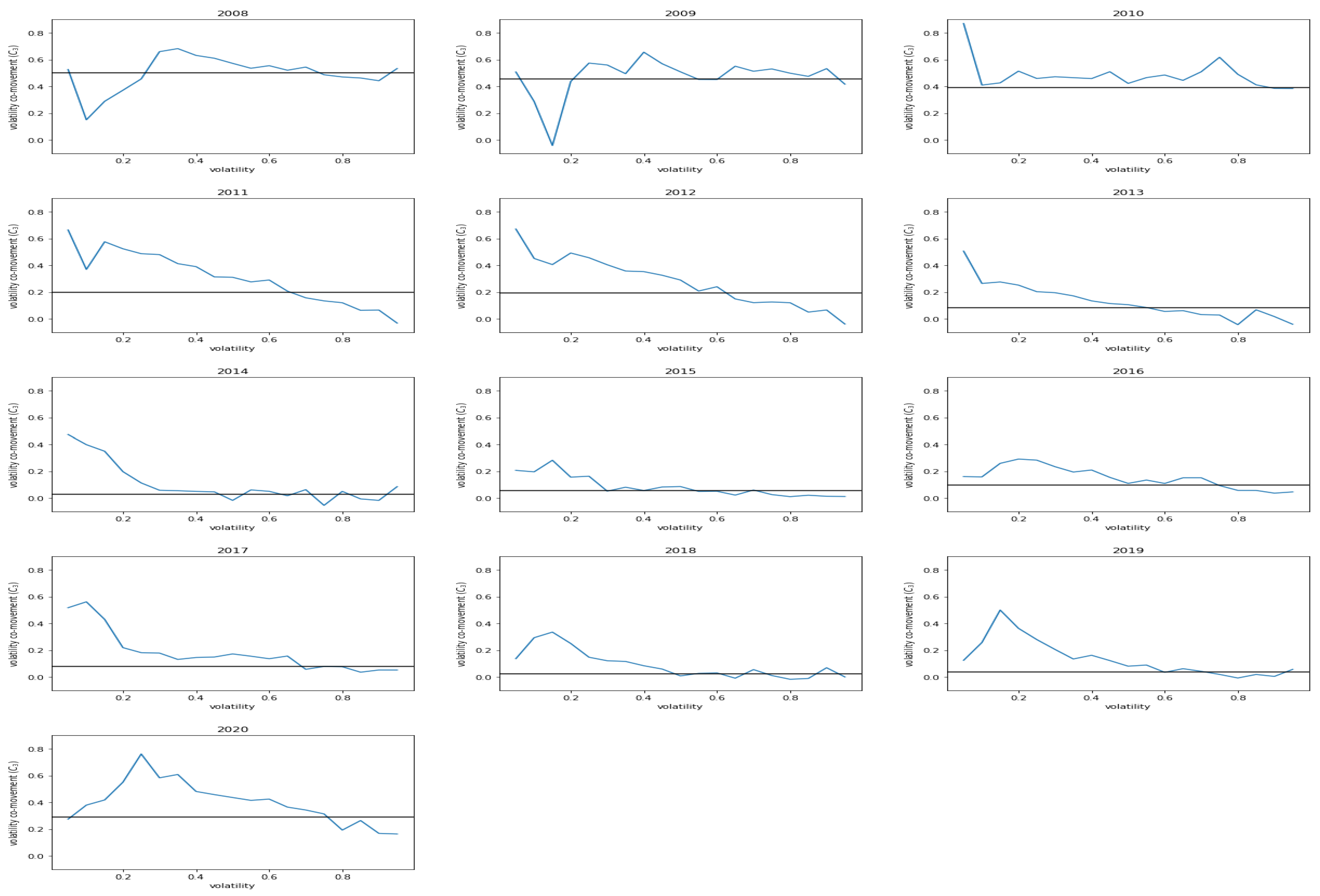

In this paper we use a function borrowed from the analysis of cooperative dynamics in physical systems of colloidal particles to study the co-movement in the volatility of stocks within a single market. A total of 3577 American shares, sampled daily from 2008 to 2020, are analyzed. The period includes the financial crisis in 2008–2010, and COVID19 crisis in 2020. We focus on the co-movement in two main factors: volatility and market. The contribution to the total co-movement from different stocks is classified according to the stock volatility. The methodology allows us to identify the origin of the co-movement and conclude if it is caused by an external agent or correlation among stocks.

Globally, stocks with low volatility have a greater volatility and log-price co-movement than the general market co-movement. In addition, co-movement between stocks of similar volatility is typically larger than co-movement between stocks of different volatility. Negative co-movement is found, in some years, between stocks of very different volatility.

Interpreting this analysis within the background of many-body physics, the market index is defined as the average over all stocks, similar to the center of mass. We study, thus, the volatility (and log-price) co-movement after subtracting the market. The results for the co-movement are very close to zero in both cases, indicating that the market explains the general co-movement to a great extent. These results are similar to those reported by Lopez-Garcia et al. [

29] for the log-price co-movement. Our results also show that the market factor is highly significant, as Lopez-Garcia et al. [

37] suggested, for asset pricing and portfolio risk and indicates that dynamic correlations between stocks are rare, but relevant only in selected periods, mainly the crisis.

On the other hand, it is observed that both volatility and log-price co-movement of the general market are much higher during crisis periods. Similar results are shown by Trinidad et al. [

36] or Tseng et al. [

35]. In these periods, stocks with low volatility have a great co-movement, not only with other stocks with low volatility (that they have in general), but also with stocks with greater volatilities, resulting in different distributions of co-movement in crisis and stable periods. Studying the volatility distribution of the co-movement thus serves to identify and characterize crisis periods as well as provide further insight into the dynamics of stock markets.

Finally, the proposed method to study co-movement should be seen as a method to study the co-movement of the full market (or a subgroup of stocks) and can be used to study the influence of a factor or variable (in this paper we have used the volatility) in the log-price or volatility co-movement.

Our findings could also be helpful to approach other problems, such as portfolio diversification. We showed that stocks with low volatilities usually have a high degree of co-movement (both in log-price and volatility); thus, some questions arise with respect to the portfolio: Is a portfolio with stocks of low volatility riskier since they will have a high degree of co-movement? Is it better to construct a portfolio with stocks of different volatilities, as suggested by the fact that they will have a lower degree of co-movement? What about the risk of a portfolio of stocks with high volatility, which tend to have a lower degree of co-movement? These questions represent future promising research lines.

Another implication of our findings is that during crisis periods, the co-movement of the general market increases significantly, and the co-movement between stocks with different volatilities is very high, in comparison with the co-movement between stocks with different volatilities in other periods. Hence, a portfolio that can be considered well diversified in non-crisis periods will probably be much riskier during a crisis, since the diversification fails to work during crisis periods.

To conclude, another future research line is to study with the proposed method the co-movement of other asset pricing factors to see if stocks with a similar factor will have higher or lower co-movement than the general market.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}