Modeling the Yield Curve of BRICS Countries: Parametric vs. Machine Learning Techniques

Abstract

:1. Introduction

2. Methodology

2.1. The Five Factor De Rezende–Ferreira Model

- For each market we define the sets = of maturities with and equal to the sets cardinality. In particular, is the lower bound of () and corresponds to the first available maturity of the market, while the upper bound is, at the same time, the lower bound of , that is and it is equal to the straddling maturity between the short and medium–term period. Finally, the upper bound of () is the longest observed maturity. In our study we set = 30 years, as in general there aren’t any bonds traded for longer maturities in the analyzed markets. Values in and ranges between corresponding lower/upper values by proper step sizes and . As the step size can affect the overall performance of the procedure, we tried various step sizes in the range [0.25, 0.75] for and [0.25, 1] for . After extensive simulations we set and .

- For each maturity in the sets and we estimated the parameters and that maximize the medium term component:In this way we get as many curves as the number of maturities.

- For each time t in the time horizon of length T and for every maturity , keep constant and vary to estimate by OLS different array sets ; choose then the set associated to the lowest Sum of Squared Residuals (SSR):with and being the observed and fitted spot rates respectively.

- Repeat Step 3 for all so that there are as many sets of optimal parameters as the values. Then, select the set with the lowest SSR and fit the yield curve at the desired time t:

- Repeat Steps 3–4 for each time t, to get the set of T yield curves fitting and the related time series for all the model parameters.

2.2. Feed Forward Neural Networks

3. Empirical Analysis

3.1. Data

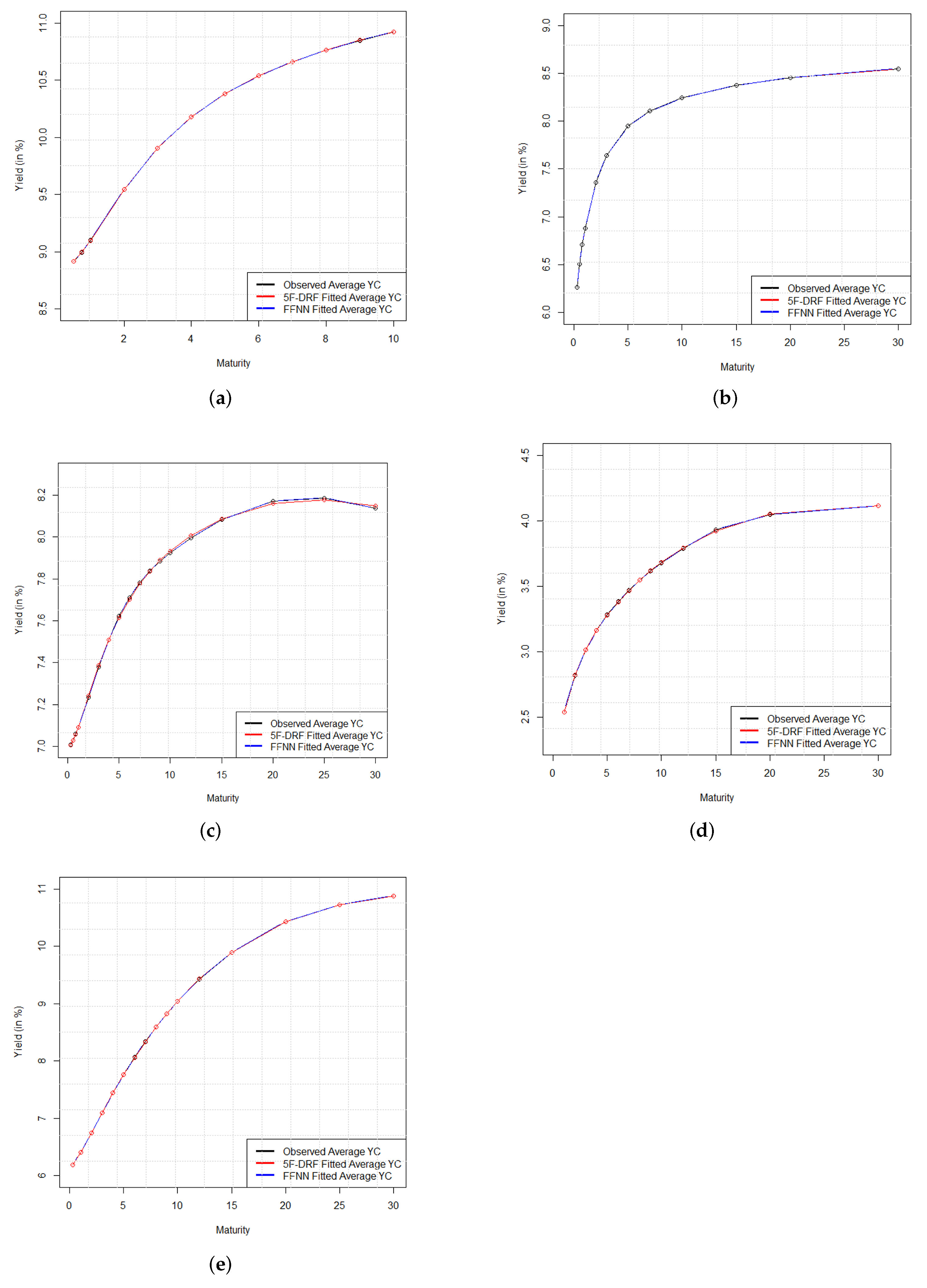

3.2. Comparison of the 5F-DRF and FFNN Models Fitting Performances

- (a) FFNNs perform better than the 5F–DRF model for in sample fitting of the yield curve of the BRICS countries.

- (b) The reason of (a) is in a better adaptability of the FFNN to both internal and external shocks.

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| BRICS | Brazil, Russia, India, China, South Africa |

| ANN | Artificial Neural Network |

| FFNN | Feed–Forward Neural Network |

| 5F-DRF | Dynamic De Rezende–Ferreira Five Factor Model |

| BPA | Backpropagation Algorithm |

References

- Bekiros, Stelios, and Christos Avdoulas. 2020. Revisiting the Dynamic Linkages of Treasury Bond Yields for the BRICS: A Forecasting Analysis. Forecasting 2: 102–29. [Google Scholar] [CrossRef]

- Caldeira, João Frois, Guilherme V. Moura, and Marcelo S. Portugal. 2010. Efficient Yield Curve Estimation and Forecasting in Brazil. Revista Economia 11: 27–51. [Google Scholar]

- Caldeira, João Frois, Rangan Gupta, Muhammad Tahir Suleman, and Hudson S. Torrent. 2020. Forecasting the Term Structure of Interest Rates of the BRICS: Evidence from a Nonparametric Functional Data Analysis. Emerging Markets Finance and Trade, 1–18. [Google Scholar] [CrossRef]

- Castello, Oleksandr, and Marina Resta. 2019. DeRezende.Ferreira: Zero Coupon Yield Curve Modelling. R Package Version 0.1.0. Genova: Department of Economics and Business Studies, University of Genova. [Google Scholar]

- Chakroun, Fatma, and Fathi Abid. 2014. A Methodology to Estimate the Interest Rate Yield Curve in Illiquid Market: The Tunisian Case. Journal of Emerging Market Finance 13: 305–33. [Google Scholar] [CrossRef]

- de Boyrie, Maria E., and Ivelina Pavlova. 2016. Dynamic interdependence of sovereign credit default swaps in BRICS and MIST countries. Applied Economics 48: 563–75. [Google Scholar] [CrossRef]

- De Rezende, Rafael Barros, and Mauro S. Ferreira. 2008. Modeling and Forecasting the Brazilian Term Structure of Interest Rates by an Extended Nelson-Siegel Class of Models: A Quantile Autoregression Approach. Resreport, Escola Brasileira de Economia e Finanças. Available online: http://bibliotecadigital.fgv.br/ocs/index.php/sbe/EBE08/paper/download/521/13 (accessed on 8 May 2021).

- De Rezende, Rafael Barros, and Mauro S. Ferreira. 2013. Modeling and Forecasting the Yield Curve by an Extended Nelson-Siegel Class of Models: A Quantile Autoregression Approach. Journal of Forecasting 32: 111–23. [Google Scholar] [CrossRef]

- Dey, Ayon. 2016. Machine Learning Algorithms: A Review. International Journal of Computer Science and Information Technologies 7: 1174–79. [Google Scholar]

- Di Franco, Giovanni, and Michele Santurro. 2020. Machine learning, artificial neural networks and social research. Quality & Quantity 55: 1007–25. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Canlin Li. 2006. Forecasting the term structure of government bond yields. Journal of Econometrics 130: 337–64. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis, and Glenn Rudenbusch. 2017. Yield Curve Modeling and Forecasts. Princeton: Princeton University Press. [Google Scholar]

- El-Shagi, Makram, and Lunan Jiang. 2019. Efficient Dynamic Yield Curve Estimation in Emerging Financial Markets. CFDS Discussion Paper Series 2019/4; Kaifeng: Center for Financial Development and Stability at Henan University. [Google Scholar]

- Filipović, Damir. 2009. Term Structure Models. Berlin: Springer. [Google Scholar]

- Hess, Markus. 2020. A pure-jump mean-reverting short rate model. Modern Stochastics: Theory and Applications 7: 113–34. [Google Scholar] [CrossRef]

- Hornik, Kurt, Maxwell Stinchcombe, and Halbert White. 1989. Multilayer feedforward networks are universal approximators. Neural Networks 2: 359–66. [Google Scholar] [CrossRef]

- Lantz, Brett. 2019. Machine Learning with R: Expert Techniques for Predictive Modeling, 3rd ed. Birmingham: Packt Publishing. [Google Scholar]

- Lopez De Prado, Marcos. 2018. Advances in Financial Machine Learning. New York: Wiley. [Google Scholar]

- Pereda, Javier. 2009. Estimacion de la Curva de Rendimiento Cupon Cero para el Perú. Technical Report, Banco Central De Reserva Del Perú. Available online: https://www.bcrp.gob.pe/docs/Publicaciones/Revista-Estudios-Economicos/17/Estudios-Economicos-17-4.pdf (accessed on 28 January 2022).

- Posthaus, Achim. 2019. Yield Curve Fitting with Artificial Intelligence: A Comparison of Standard Fitting Methods with AI Algorithms. Journal of Computational Finance 22: 1–23. [Google Scholar] [CrossRef]

- Prasanna, Krishna, and Subramaniam Sowmya. 2017. Yield curve in India and its interactions with the US bond market. International Economics and Economic Policy 14: 353–75. [Google Scholar] [CrossRef]

- Rosadi, Dedi, Yoga Aji Nugraha, and Rahmawati Kusuma Dewi. 2011. Forecasting the Indonesian Government Securities Yield Curve Using Neural Networks and Vector Autoregressive Model. Technical Report. Yogyakarta: Department of Mathematics, Gadjah Mada University. [Google Scholar]

- Rumelhart, David E., Geoffrey E. Hinton, and Ronald J. Williams. 1986. Learning representations by back-propagating errors. Nature 323: 533–36. [Google Scholar] [CrossRef]

- Salisu, Afees A., Juncal Cuñado, Kazeem Isah, and Rangan Gupta. 2021. Stock markets and exchange rate behaviour of the BRICS. Journal of Forecasting 40: 1581–95. [Google Scholar] [CrossRef]

- Saunders, Anthony, and Marcia Cornett. 2014. Financial Markets and Institutions, 6th ed. New York: The McGraw-Hill/Irwin Series in Finance, Insurance, and Real Estate. [Google Scholar]

- Stuart, Rebecca. 2020. The term structure, leading indicators, and recessions: Evidence from Switzerland, 1974–2017. Swiss Journal of Economics and Statistics 156: 1–17. [Google Scholar] [CrossRef]

- Suimon, Yoshiyuki, Hiroki Sakaji, Kiyoshi Izumi, and Hiroyasu Matsushima. 2020. Autoencoder-Based Three-Factor Model for the Yield Curve of Japanese Government Bonds and a Trading Strategy. Journal of Risk and Financial Management 13: 82. [Google Scholar] [CrossRef]

- Ullah, Wali, and Khadija Malik Bari. 2018. The Term Structure of Government Bond Yields in an Emerging Market. Romanian Journal for Economic Forecasting 21: 5–28. [Google Scholar]

- Vela, Daniel. 2013. Forecasting Latin–American Yield Curves: An Artificial Neural Network Approach. Techreport 761. Colombia: Banco de la República. [Google Scholar]

- Wahlstrom, Ranik Raaen, Florentina Paraschiv, and Michael Schurle. 2021. A Comparative Analysis of Parsimonious Yield Curve Models with Focus on the Nelson-Siegel, Svensson and Bliss Versions. Computational Economics, 1–38. [Google Scholar] [CrossRef]

- Wilamowski, Bogdan M., and David Irwin. 2011. Intelligent Systems, 2nd ed. Boca Raton: CRC Press. [Google Scholar] [CrossRef]

- Zeb, Shumaila, and Abdul Rashid. 2019. Systemic risk in financial institutions of BRICS: Measurement and identification of firm-specific determinants. Risk Management 21: 243–64. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Period | N of Observations | Source | |

|---|---|---|---|---|

| Start | End | |||

| Brazil | 30/09/2011 | 30/12/2020 | 2128 | TRD |

| Russia | 04/01/2003 | 30/12/2020 | 4578 | CBR |

| India | 14/02/2012 | 30/12/2020 | 2185 | TRD |

| China | 24/01/2005 | 30/12/2020 | 3818 | TRD |

| South Africa | 18/02/2011 | 30/12/2020 | 2472 | TRD |

| Country | Hidden Layer | Input/Output Nodes | Hidden Nodes |

|---|---|---|---|

| Brazil | 1 | 12 | 9 |

| Russia | 1 | 12 | 13 |

| India | 1 | 18 | 10 |

| China | 1 | 14 | 11 |

| South Africa | 1 | 16 | 12 |

| Brazil | Russia | India | China | South Africa | |

|---|---|---|---|---|---|

| MSE | RMSE | ||||

|---|---|---|---|---|---|

| 5F-DRF | FFNN | 5F-DRF | FFNN | ||

| Brazil | Mean | ||||

| SD | |||||

| Min | |||||

| Max | |||||

| Russia | Mean | ||||

| SD | |||||

| Min | |||||

| Max | |||||

| India | Mean | ||||

| SD | |||||

| Min | |||||

| Max | |||||

| China | Mean | ||||

| SD | |||||

| Min | |||||

| Max | |||||

| S. Africa | Mean | ||||

| SD | |||||

| Min | |||||

| Max | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Castello, O.; Resta, M. Modeling the Yield Curve of BRICS Countries: Parametric vs. Machine Learning Techniques. Risks 2022, 10, 36. https://doi.org/10.3390/risks10020036

Castello O, Resta M. Modeling the Yield Curve of BRICS Countries: Parametric vs. Machine Learning Techniques. Risks. 2022; 10(2):36. https://doi.org/10.3390/risks10020036

Chicago/Turabian StyleCastello, Oleksandr, and Marina Resta. 2022. "Modeling the Yield Curve of BRICS Countries: Parametric vs. Machine Learning Techniques" Risks 10, no. 2: 36. https://doi.org/10.3390/risks10020036

APA StyleCastello, O., & Resta, M. (2022). Modeling the Yield Curve of BRICS Countries: Parametric vs. Machine Learning Techniques. Risks, 10(2), 36. https://doi.org/10.3390/risks10020036