Corporate Social Responsibility as an Alternative Approach to Financial Risk Management: Advantages for Sustainable Development

Abstract

:1. Introduction

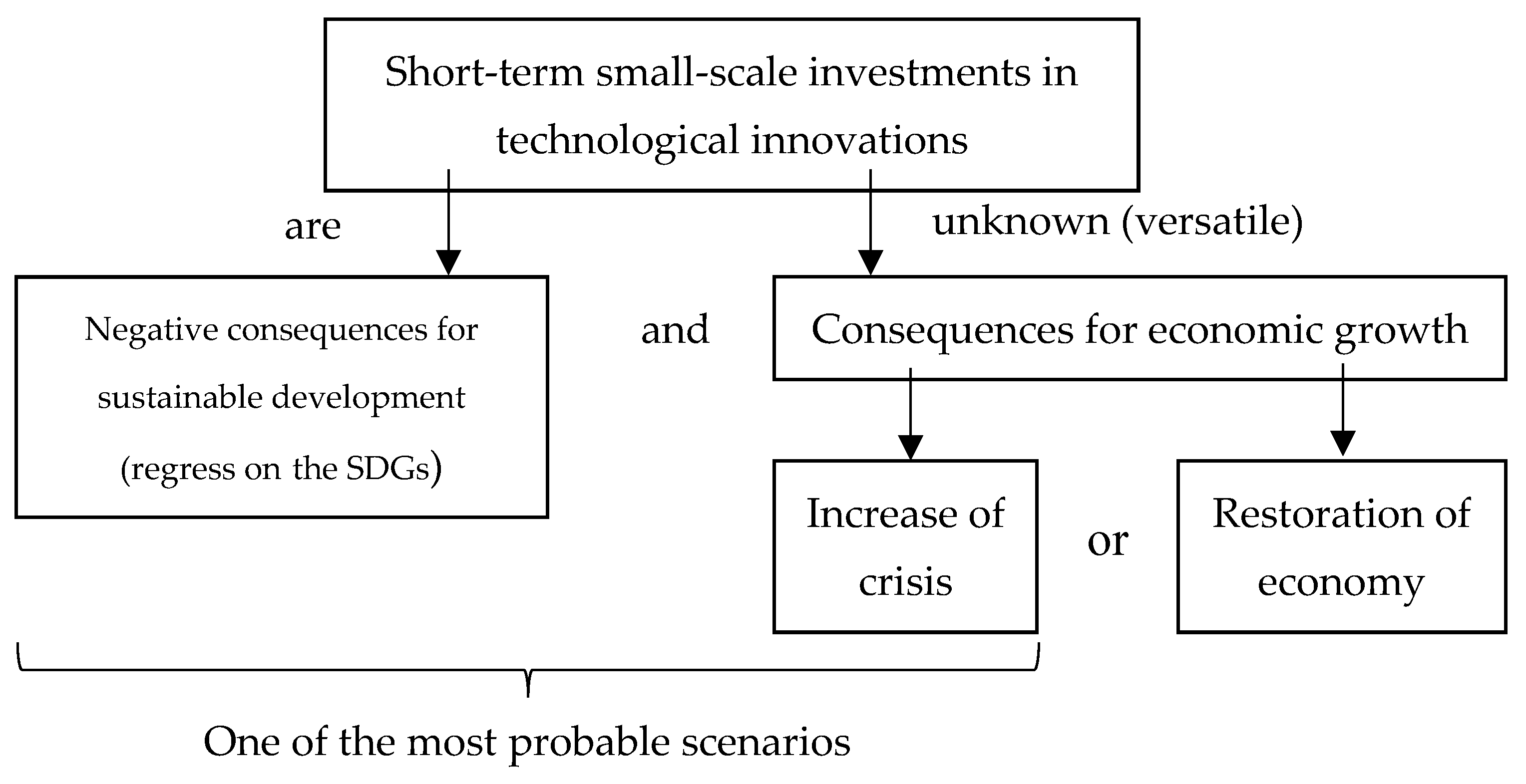

- −

- Identifying the level of the financial risk of companies, measuring and discovering the differences in its connection with the commercial and responsible investments;

- −

- Modeling the dependence of effectiveness of investments on commercial and responsible investments;

- −

- Performing a scenario analysis of the alternatives of financial risk management of companies in 2021 through the increase in the effectiveness of investments based on the optimization of investment flows.

2. Literature Review

- −

- preference is given to venture investments in technological innovations since they have the highest potential to increase the rate of economic growth (Conti et al. 2019; Frimpong et al. 2021);

- −

- it is expedient to place commercial (not supported by corporate social responsibility) investments since corporate social responsibility reduces the effectiveness of investments (reduces companies’ profitability because they are connected to additional expenditures) (Di Persio et al. 2021; Szemere et al. 2021);

- −

- Financial risks are high a priori amid a crisis and cannot be reduced. That is why the period of investing is short, because, first, there is a need for a quick effect for the economy in the form of increasing its growth rate and restoration after the crisis. Second, long-term investments are not profitable for investors due to the uncertainty of the perspectives of receiving a return on capital employed. Long-term investments (peculiar for infrastructural projects)—are a “market gap”, which is overcome through government financing of infrastructural projects (Cristiana 2021; Swishchuk 2021);

- −

- Investment projects are of a small scale since investors do not possess large financial resources and/or reduce financial risks through the diversification of the investment portfolio (implementation of several small-scale investment projects instead of one large project) (Batóg and Batóg 2021; Bouri et al. 2021);

- −

- Under the crisis conditions, the role of investments in stimulating sustainable development is focused on support for the implementation of SDG 8 (in the narrow treatment, limited by economic growth) and SDG 9 (in the narrow treatment, limited by industrialization and innovations) (Chen 2021; Kang 2020; Kurniatama et al. 2021).

3. Method and Data

- −

- Investment in energy with private participation (Ienerg);

- −

- Investment in water and sanitation with private participation (Iwater);

- −

- Investment in transport with private participation (Itransp);

- −

- Domestic private health expenditure (Ihealth) per capita, PPP (current international $) (World Bank 2021a).

4. Results

Determining the level of the financial risk of companies, measuring and revealing the differences in its connection with the commercial and responsible investments

Modeling the Dependence of the Effectiveness of Investments on Commercial and Responsible Investments

Scenario Analysis of the Alternatives of Financial Risk Management of Companies in 2021 through an Increase in the Effectiveness of Investments Based on the Optimization of Investment Flows

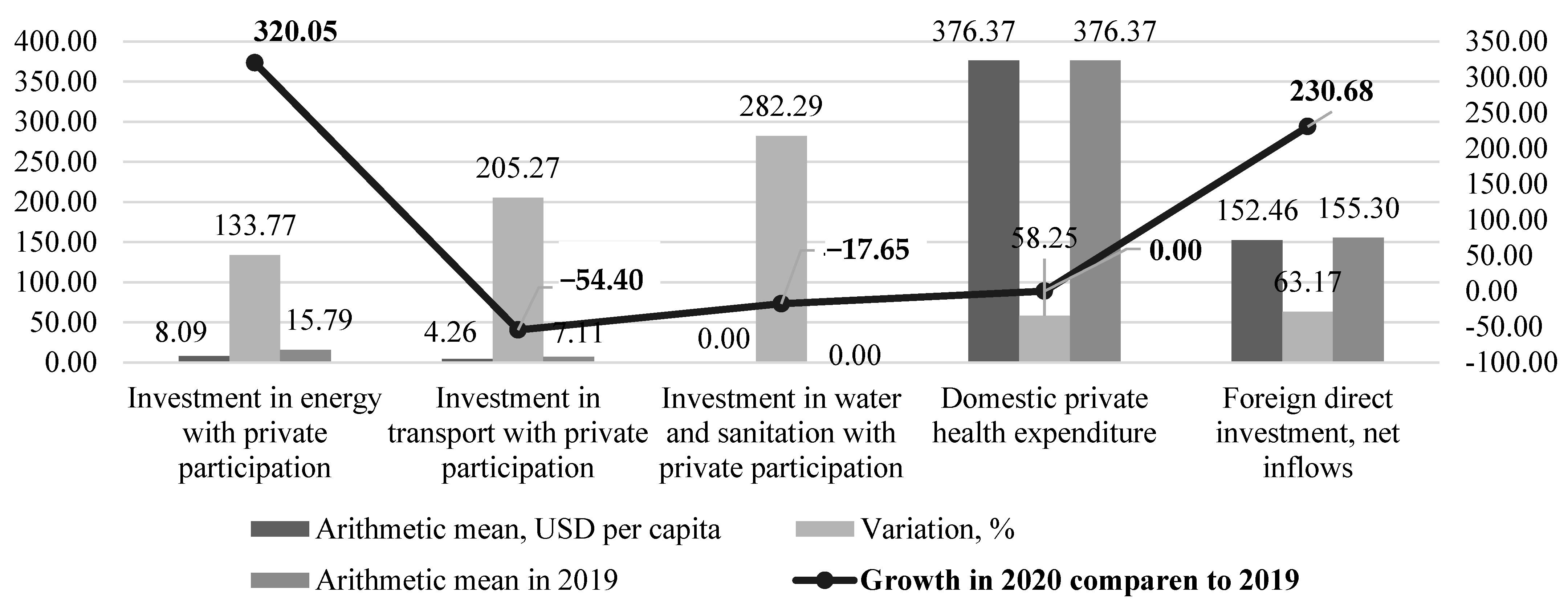

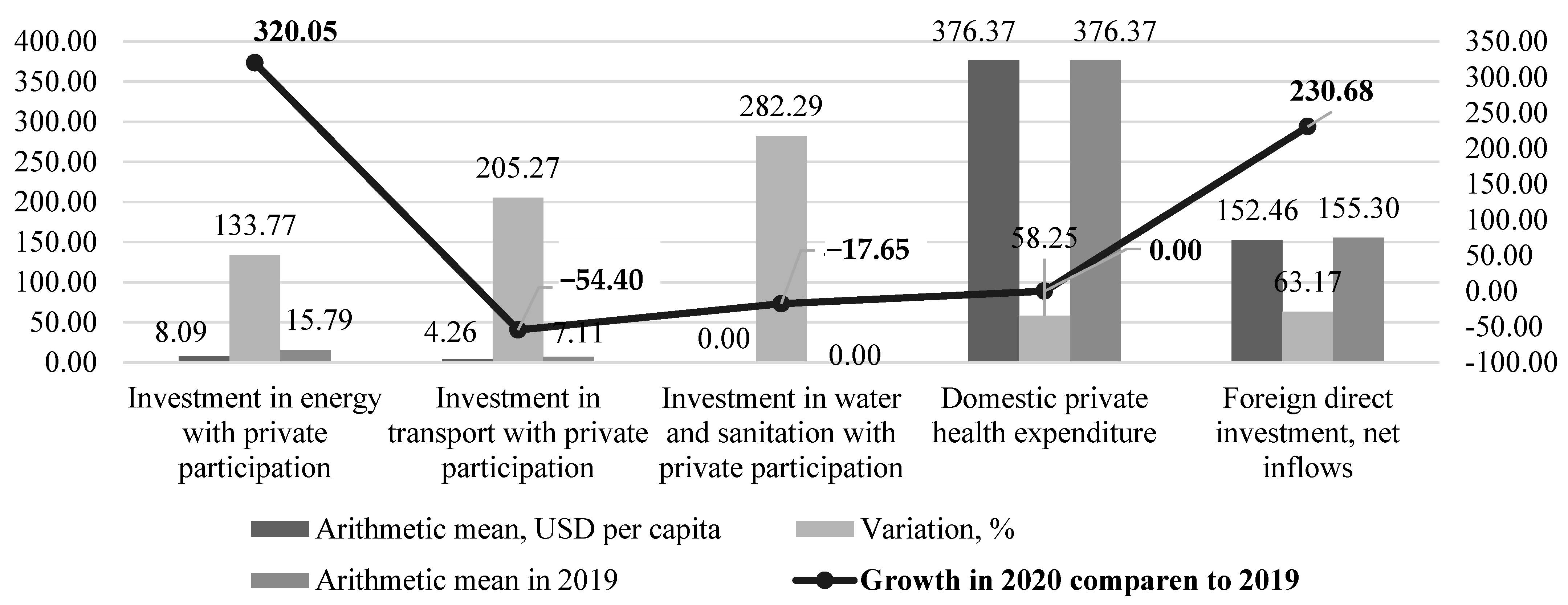

- −

- Increase in investments in transport by 0.73%: from USD 4.26 per capita to USD 4.30 per capita;

- −

- Increase in investments in water and sanitation by 2.68%: from USD 0.0012 per capita to USD 0.0012079 per capita;

- −

- Increase in investments in healthcare by 5.13%: from USD 376.37 per capita to USD 395.69 per capita.

5. Discussion

- −

- Preference is given to investments based on the mechanism of public-private partnership since the participation of the government ensures the co-financing of investment projects and the distribution of risks between the partners. Public-private partnership also guarantees high demand for products that are received as a result of implementing the investment projects since it envisages the implementation of projects that are in high demand in society. This is the difference between the obtained results and the existing literature (Conti et al. 2019; Frimpong et al. 2021);

- −

- It is expedient to make social—supported by corporate social responsibility—investments since its raises the effectiveness of investments (increases the profitability of companies). This is the difference between the obtained results and the existing literature (Di Persio et al. 2021; Szemere et al. 2021);

- −

- During crises, financial risks could be reduced through the optimization of the investment portfolio. That is why long-term investments are allowed and are the most preferable (peculiar for infrastructural projects), for the perspectives of receiving a return on capital employed are most favorable. This is the difference between the obtained results and the existing literature (Cristiana 2021; Swishchuk 2021);

- −

- Investment projects are of large scale since it is preferable to concentrate investments on the most profitable responsible investments (it is necessary to refuse the diversification of the investment portfolio). This is the difference between the obtained results and the existing literature (Batóg and Batóg 2021; Bouri et al. 2021);

- −

- Amid a crisis, investments in responsible innovations are most perspective, for they have the largest potential for an increase in market capitalization. The role of investments in stimulating sustainable development has several aspects and includes the support for the implementation of SDG 7 (during investment in energy), SDG 11 (during investment in transport and logistics), SDG 6 (during investment in water and sanitation), SDG 3 (during investment in healthcare), SDG 8 (in the wide treatment, which covers not only economic growth but also decent work), and SDG 9 (in the wide treatment, which covers not only industry and innovations but also infrastructure). This is the difference between the obtained results and the existing literature (Chen 2021; Kang 2020; Kurniatama et al. 2021).

6. Conclusions

- −

- It is expedient to support investments in renewable energy sources during a crisis: expenditures for energy resources grow, and this is a problem, while the decarbonization of the economy is necessary for preventing future epidemics and pandemics;

- −

- Investments in transport are important to support the continued work of the key sectors of the economy even under the conditions of social distancing and economic limitations;

- −

- Investments in healthcare are critically important during the pandemic;

- −

- Investments in water and sanitation supplement them since they raise the level of hygiene and allow for fighting the current pandemic and preventing future epidemics and pandemics.

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adamoglou, Xanthippe, Vasiliki Kounnou, and Dimitris Kyrkilis. 2022. US Foreign Direct Investments in the Eurozone: A Distance Analysis in View of Global Crisis. Evidence from the Manufacturing Sector. Palgrave Studies of Cross-Disciplinary Business Research. In Association with EuroMed Academy of Business. Cham: Palgrave Macmillan, pp. 17–39. [Google Scholar] [CrossRef]

- Alashbaieva, Nursulu, Dametken Turekulova, Asemgul Kapenova, Aliya Zhunusova, and Raikhan Sutbayeva. 2021. Management of the company’s investment projects in anti-crisis management and their impact on the environment. Journal of Environmental Management and Tourism 12: 1914–29. [Google Scholar] [CrossRef]

- Ambrocio, Gene, and Tae-Seok Jang. 2021. The Impact of the Global Financial Crisis on Investment in Finland and South Korea. Journal of Business Cycle Research 17: 321–37. [Google Scholar] [CrossRef]

- Anwar, Muhammad Bashar, Gord Stephen, Sourabh Dalvi, Bethany Frew, Sean Ericson, Maxwell Brown, and Mark O’Malley. 2022. Modeling investment decisions from heterogeneous firms under imperfect information and risk in wholesale electricity markets. Applied Energy 306: 117908. [Google Scholar] [CrossRef]

- Batóg, Barbara, and Jacek Batóg. 2021. Regional government revenue forecasting: Risk factors of investment financing. Risks 9: 210. [Google Scholar] [CrossRef]

- Becchetti, Leonardo, Rocco Ciciretti, Ambrogio Dalò, and Stefano Herzel. 2015. Socially responsible and conventional investment funds: Performance comparison and the global financial crisis. Applied Economics 47: 2541–62. [Google Scholar] [CrossRef]

- Bendall, Helen, and Alan Fraser Stent. 2006. ROA Valuation of Risks in Commercialisation of New HSC Designs and Technology. London: International Conference High Speed Craft—ACV’s, WIG’s and Hydrofoils, pp. 151–62. [Google Scholar]

- Bianchi, Benedetta, Vahagn Galstyan, and Valerie Herzberg. 2022. Global risk and portfolio flows to emerging markets: Evidence from irish-resident investment funds. Journal of International Money and Finance 123: 102600. [Google Scholar] [CrossRef]

- Bilbao-Terol, Amelia, Mar Arenas-Parra, Veronica Cañal-Fernández, and Celia Bilbao-Terol. 2016. Multi-criteria decision making for choosing socially responsible investment within a behavioral portfolio theory framework: A new way of investing into a crisis environment. Annals of Operations Research 247: 549–80. [Google Scholar] [CrossRef]

- Bouri, Elie, Riza Demirer, Rangan Gupta, and Jacobus Nel. 2021. Covid-19 pandemic and investor herding in international stock markets. Risks 9: 168. [Google Scholar] [CrossRef]

- Chen, Bingyao. 2021. Public–private partnership infrastructure investment and sustainable economic development: An empirical study based on efficiency evaluation and spatial spillover in China. Sustainability 13: 8146. [Google Scholar] [CrossRef]

- Chiang, Thomas. 2021. Geopolitical risk, economic policy uncertainty and asset returns in Chinese financial markets. China Finance Review International 11: 474–501. [Google Scholar] [CrossRef]

- Conti, Annamaria, Nishant Dass, Francesco Di Lorenzo, and Stuart Graham. 2019. Venture capital investment strategies under financing constraints: Evidence from the 2008 financial crisis. Research Policy 48: 799–812. [Google Scholar] [CrossRef]

- Cristiana, Tudor. 2021. Investors’ trading activity and information asymmetry: Evidence from the Romanian stock market. Risks 9: 149. [Google Scholar] [CrossRef]

- Cristiano, Carlo, Marioa Cristina Marcuzzo, and Eleonora Sanfilippo. 2018. Taming the great depression: Keynes’s personal investments in the US stock market, 1931–39. Economia Politica 35: 13–40. [Google Scholar] [CrossRef]

- Di Persio, Luca, Matteo Garbelli, and Kai Wallbaum. 2021. Forward-looking volatility estimation for risk-managed investment strategies during the covid-19 crisis. Risks 9: 33. [Google Scholar] [CrossRef]

- Falato, Antonio, Itay Goldstein, and Ali Hortaçsu. 2021. Financial fragility in the COVID-19 crisis: The case of investment funds in corporate bond markets. Journal of Monetary Economics 123: 35–52. [Google Scholar] [CrossRef]

- Flammer, Caroline, and Ioannis Ioannou. 2021. Strategic management during the financial crisis: How firms adjust their strategic investments in response to credit market disruptions. Strategic Management Journal 42: 1275–98. [Google Scholar] [CrossRef]

- Forbes. 2022. Global 2000 in 2020–2021. Available online: https://www.forbes.com/lists/global2000/ (accessed on 16 December 2021).

- Frimpong, Fauna Atta, Ellis Kofi Akwaa-Sekyi, and Ramon Saladrigues. 2021. Venture capital healthcare investments and health care sector growth: A panel data analysis of Europe. Borsa Istanbul Review 22: 388–99. [Google Scholar] [CrossRef]

- Frith, Karen. 2021. From COVID-19 Crisis to Digital Health Care Innovation. Nursing Education Perspectives 42: 264–66. [Google Scholar] [CrossRef]

- Gaies, Brahim, and Mahmoud-Sami Nabi. 2021. Banking crises and economic growth in developing countries: Why privileging foreign direct investment over external debt? Bulletin of Economic Research 73: 736–61. [Google Scholar] [CrossRef]

- Gavlovskaya, Galina V., and Azat N. Khakimov. 2022. Impact of the Covid-19 pandemic on the electronic industry in Russia. In Current Problems of the World Economy and International Trade. Bingley: Emerald Publishing Limited, vol. 42. [Google Scholar]

- Giuliani, Giovanni Amerigo. 2022. The uncertain path towards social investment in post-crisis Italy. Contemporary Italian Politics 14: 87–105. [Google Scholar] [CrossRef]

- Guggenberger, Tobias, Jannik Lockl, Maximilian Röglinger, Vincent Schlatt, Johannes Sedlmeir, Jens-Christian Stoetzer, Nils Urbach, and Fabiane Völter. 2021. Emerging Digital Technologies to Combat Future Crises: Learnings from COVID-19 to be Prepared for the Future. International Journal of Innovation and Technology Management 18: 2140002. [Google Scholar] [CrossRef]

- Guseva, Irina, Elena Kulikova, and Boris Rubtsov. 2019. Dialectics of the financial market category in the Russian economic science: From the Marx era to the digital economy. In Marx and Modernity: A Political and Economic Analysis of Social Systems Management. Charlotte: Information Age Publishing, pp. 401–10. [Google Scholar]

- Harvey, John. 2021. Testing Keynes’ aggregate investment function. Journal of Post Keynesian Economics. [Google Scholar] [CrossRef]

- Herrera-Cano, Carolina, and Maria Alejandra Gonzalez-Perez. 2016. Global Financial Crisis and the Emergence and Maturing of Socially Responsible Investments. Advances in Sustainability and Environmental Justice 18: 189–202. [Google Scholar] [CrossRef]

- Ilbahar, Esra, Cengiz Kahraman, and Selcuk Cebi. 2022. Risk assessment of renewable energy investments: A modified failure mode and effect analysis based on prospect theory and intuitionistic fuzzy AHP. Energy 239: 121907. [Google Scholar] [CrossRef]

- IMD. 2021. World Digital Competitiveness Ranking 2021. Available online: https://www.imd.org/globalassets/wcc/docs/release-2021/digital_2021.pdf (accessed on 16 December 2021).

- International Monetary Fund. 2021. World Economic Outlook Database: October 2021. Available online: https://www.imf.org/en/Publications/WEO/weo-database/2021/October (accessed on 16 December 2021).

- Juszczuk, Przemyslaw, Ignacy Kaliszewski, Janucz Miroforidis, and Dmitry Podkopaev. 2022. Expected mean return—Standard deviation efficient frontier approximation with low-cardinality portfolios in the presence of the risk-free asset. International Transactions in Operational Research. [Google Scholar] [CrossRef]

- Kang, Moon Young. 2020. Sustainable profit versus unsustainable growth: Are venture capital investments and governmental support medicines or poisons? Sustainability 12: 7773. [Google Scholar] [CrossRef]

- Keynes, John Maynard. 1998. The Collected Writings of John Maynard Keynes. In 30 Volume Hardback. Edited by E. Johnson, D. Moggridge and A. Robinson. Cambridge: Cambridge University Press. [Google Scholar]

- Kurniatama, Gandang Ardi, Robiyanto Robiyanto, Gatot Sasongko, and Andrian Dolriandra Huruta. 2021. Determinants of corporate social responsibility: Empirical evidence from sustainable and responsible investment index. Quality—Access to Success 22: 55–61. [Google Scholar]

- Lean, Hooi Hooi, and Fabio Pizzutilo. 2021. Performances and risk of socially responsible investments across regions during crisis. International Journal of Finance and Economics 26: 3556–68. [Google Scholar] [CrossRef]

- Leins, Stefan. 2020. ‘Responsible investment’: ESG and the post-crisis ethical order. Economy and Society 49: 71–91. [Google Scholar] [CrossRef]

- Li, Kai, Shao-Zhou Qi, Ya-Xue Yan, and Xiao-Ling Zhang. 2022. China’s ETS pilots: Program design, industry risk, and long-term investment. Advances in Climate Change Research 13: 82–96. [Google Scholar] [CrossRef]

- Ling, David, Chongyu Wang, and Tingyu Zhou. 2022. Asset productivity, local information diffusion, and commercial real estate returns. Real Estate Economics 50: 89–121. [Google Scholar] [CrossRef]

- Liu, Shenglong, and Penglong Zhang. 2022. Foreign Direct Investment and Air Pollution in China: Evidence from the Global Financial Crisis. Developing Economies 60: 30–61. [Google Scholar] [CrossRef]

- Nisticò, Sergio. 2020. Keynes’s investment theory as a micro-foundation for his grandchildren. Economics 14: 1–15. [Google Scholar] [CrossRef]

- Reboredo, Juan, Andrea Ugolini, and Javier Ojea-Ferreiro. 2022. Do green bonds de-risk investment in low-carbon stocks? Economic Modelling 108: 105765. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Nader Trabelsi, Aviral Kumar Tiwari, Emmanuel Joel Aikins Abakah, and Zhilun Jiao. 2021. Relationship between green investments, energy markets, and stock markets in the aftermath of the global financial crisis. Energy Economics 104: 105655. [Google Scholar] [CrossRef]

- Sharma, Gagan Deep, Aviral Kumar Tiwari, Gaurav Talan, and Mansi Jain. 2021. Revisiting the sustainable versus conventional investment dilemma in COVID-19 times. Energy Policy 156: 112467. [Google Scholar] [CrossRef]

- Sohibien, Gama Putra Danu, Lills Laome, Achmad Choiruddin, and Heri Kuswanto. 2022. COVID-19 Pandemic’s Impact on Return on Asset and Financing of Islamic Commercial Banks: Evidence from Indonesia. Sustainability 14: 1128. [Google Scholar] [CrossRef]

- Swishchuk, Anatoliy. 2021. Merton investment problems in finance and insurance for the hawkes-based models. Risks 9: 108. [Google Scholar] [CrossRef]

- Szemere, Tibor Pai, Monika Garai-Fodor, and Ágnes Csiszárik-Kocsir. 2021. Risk approach—Risk hierarchy or construction investment risks in the light of interim empiric primary research conclusions. Risks 9: 84. [Google Scholar] [CrossRef]

- UN. 2020. Sustainable Development Report 2020. The Sustainable Development Goals and Covid-19. Available online: https://www.sdgindex.org/reports/sustainable-development-report-2020/ (accessed on 16 December 2021).

- UN. 2021. Sustainable Development Report 2021. Available online: https://dashboards.sdgindex.org/rankings (accessed on 16 December 2021).

- Urbano, Eva, Victor Martinez-Viol, Konstantinos Kampouropoulos, and Luis Romeral. 2022. Risk assessment of energy investment in the industrial framework—Uncertainty and Sensitivity Analysis for energy design and operation optimisation. Energy 239: 121943. [Google Scholar] [CrossRef]

- Werge, Nicklas. 2021. Predicting risk-adjusted returns using an asset independent regime-switching model. Expert Systems with Applications 184: 115576. [Google Scholar] [CrossRef]

- Willems, Sofie, Jyutsna Rao, Sailee Bhambere, Dipu Patel, Yvonne Biggins, and Jessica Guite. 2021. Digital solutions to alleviate the burden on health systems during a public health care crisis: Covid-19 as an opportunity. JMIR mHealth and uHealth 9: e25021. [Google Scholar] [CrossRef]

- World Bank. 2021a. Domestic Private Health Expenditure Per Capita, PPP (Current International $). Available online: https://data.worldbank.org/indicator/SH.XPD.PVTD.PP.CD (accessed on 16 December 2021).

- World Bank. 2021b. Foreign Direct Investment, Net Inflows (BoP, Current US$). Available online: https://data.worldbank.org/indicator/BX.KLT.DINV.CD.WD (accessed on 16 December 2021).

- World Bank. 2021c. Investment in Energy with Private Participation (Current US$). Available online: https://data.worldbank.org/indicator/IE.PPI.ENGY.CD?view=chart (accessed on 16 December 2021).

- World Bank. 2021d. Investment in Transport with Private Participation (Current US$). Available online: https://data.worldbank.org/indicator/IE.PPI.TRAN.CD?view=chart (accessed on 16 December 2021).

- World Bank. 2021e. Investment in Water and Sanitation with Private Participation (Current US$). Available online: https://data.worldbank.org/indicator/IE.PPI.WATR.CD?view=chart (accessed on 16 December 2021).

- World Bank. 2021f. Market Capitalization of Listed Domestic Companies (Current US$). Available online: https://data.worldbank.org/indicator/CM.MKT.LCAP.CD?view=chart (accessed on 16 December 2021).

- World Bank. 2021g. Population, Total. Available online: https://data.worldbank.org/indicator/SP.POP.TOTL?view=chart (accessed on 16 December 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameters of Investments That Have to Ensure the Crisis Resolution | Manifestation of the Existing Approach to Financial Risk Management Amid the Economic Crisis |

|---|---|

| Mechanism of investing | venture investing |

| Object of investing | technological innovations |

| Type of investments | commercial investments |

| Period of investing | short-term |

| The scale of investment projects | small-scale investments |

| Supported SDGs within the investment projects | SDG 8 (economic growth) SDG 9 (industry, innovations) |

| Research Task | Research Method | Contribution to the Verification of the Hypothesis (Expected, Targeted Result, Which Is Necessary for Proving the Hypothesis) |

|---|---|---|

| 1. Determining the level of the financial risk of companies, measuring and discovering the differences in its connection with commercial and responsible investments | Horizontal analysis | Proving high financial risks |

| Correlation analysis | Proving a much larger contribution to the reduction in financial risk from responsible investments compared to commercial investments | |

| 2. Modelling the dependence of effectiveness of investments on commercial and responsible investments | Regression analysis | Substantiating the sustainable and key role of responsible investments on the increase in the effectiveness of companies’ investments compared to commercial investments |

| 3. Performing scenario analysis of the alternatives of financial risk management of companies in 2021 through the increase in the effectiveness of investments based on the optimization of investment flows | Scenario analysis with the help of the least-squares method | Demonstration of wide and flexible opportunities for preventing and managing financial risk in 2021 through the optimization of investment flows (an increase in responsible investments) |

| Determination | Investment in Energy with Private Participation | Investment in Transport with Private Participation | Investment in Water and Sanitation with Private Participation | Domestic Private Health Expenditure | Foreign Direct Investment, Net Inflows |

|---|---|---|---|---|---|

| Investment in energy with private participation | 1 | - | - | - | - |

| Investment in transport with private participation | 0.04 | 1 | - | - | - |

| Investment in water and sanitation with private participation | 0.21 | −0.14 | 1 | - | - |

| Domestic private health expenditure | 0.26 | −0.21 | −0.10 | 1 | - |

| Foreign direct investment, net inflows | 0.37 | 0.22 | −0.01 | 0.60 | 1 |

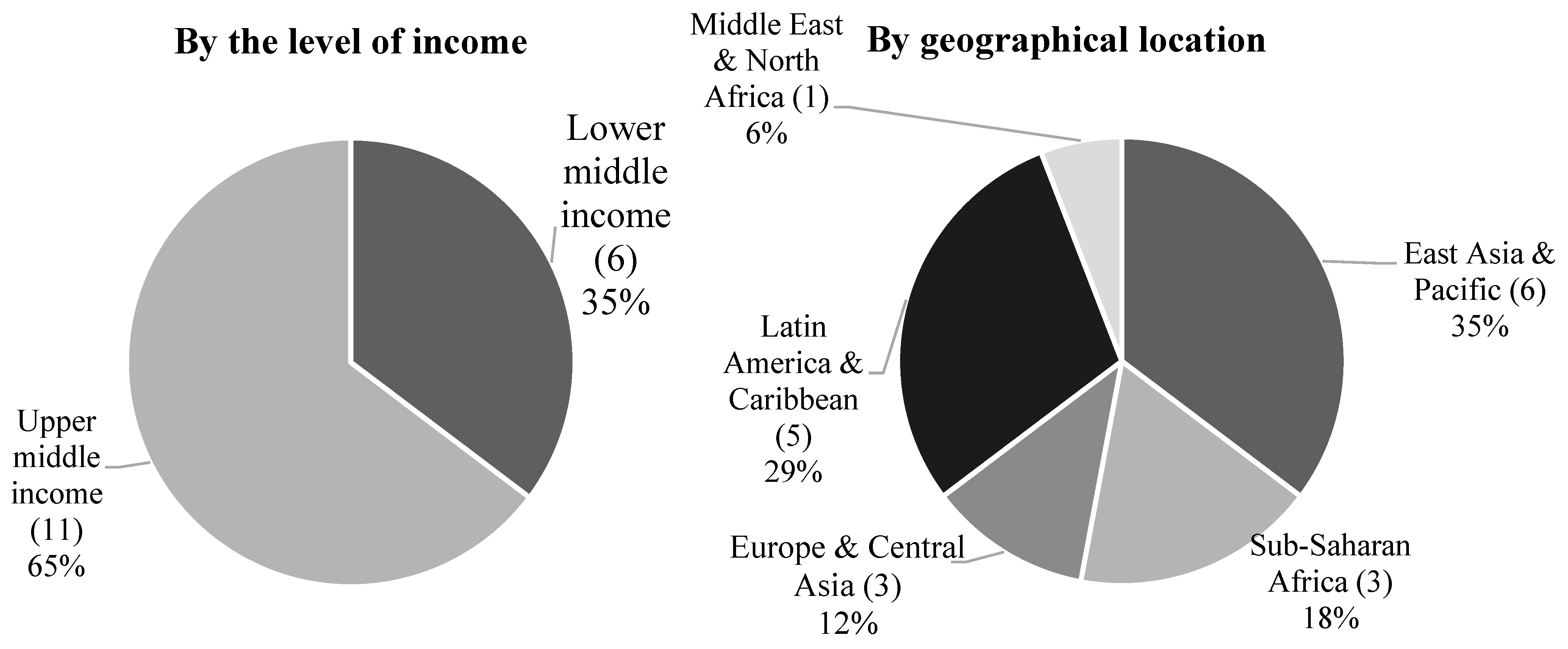

| Country Name | Company | ROA2020 | ROA2021 | Financial Risk % |

|---|---|---|---|---|

| Argentina | YPF | 0.03 | −0.04 | −259.81 |

| Brazil | Itaú Unibanco Holding | 0.02 | 0.01 | −43.75 |

| China | ICBC | 10.48 | 9.32 | −11.08 |

| Colombia | Ecopetrol | 0.10 | 0.01 | −88.46 |

| Egypt, Arab Rep, | Commercial International Bank | 0.03 | 0.02 | −18.22 |

| Indonesia | Bank Rakyat Indonesia (BRI) | 0.02 | 0.01 | −48.60 |

| Kazakhstan | Halyk Bank | 0.04 | 0.03 | −4.89 |

| Kenya | Safaricom | 0.30 | 0.32 | 9.41 |

| Malaysia | Maybank | 0.01 | 0.01 | −28.17 |

| Mexico | América Móvil | 0.04 | 0.03 | −32.57 |

| Nigeria | Zenith Bank | 0.03 | 0.03 | −8.95 |

| Peru | Credicorp | 0.02 | 0.00 | −93.95 |

| Philippines | SM Investments | 0.04 | 0.02 | −51.46 |

| South Africa | FirstRand | 0.02 | 0.01 | −57.33 |

| Thailand | PTT | 0.03 | 0.01 | −59.60 |

| Turkey | Isbank | 0.01 | 0.01 | −2.47 |

| Vietnam | Joint Stock Commercial Bank for Foreign Trade of Vietnam | 0.02 | 0.01 | −13.47 |

| Arithmetic mean, USD per capita | 0.66 | 0.58 | −47.85 | |

| Correlation with the risk % | 15.76 | 16.67 | 100.00 | |

| Regression statistics | Multiple R | 0.7961 |

| R-square | 0.6339 | |

| Adjusted R-square | 0.4675 | |

| Standard error | 1.6450 | |

| Observations | 17 | |

| Analysis of variance | F | 3.809132 |

| Significance F | 0.030109 | |

| Coefficients that specify the research model (1) | const | −0.34 |

| benerg | −0.08 | |

| btransp | 0.04 | |

| bwater | 554.30 | |

| bhealth | 0.003 | |

| bforeign | −0.003 | |

| t-Stat at | const | −0.37 |

| benerg | −1.92 | |

| btransp | 0.76 | |

| bwater | 4.22 | |

| bhealth | 1.25 | |

| bforeign | −0.54 |

| Characteristics of the Scenario | The Base of Scenario Analysis | Scenarios of Financial Risk Management | |

|---|---|---|---|

| The Scenario of Reduction in the Financial Risk | The Scenario of Prevention of the Financial Risk | ||

| Investment in energy with private participation per capita (current US$) | 8.09 | 8.09 | 8.09 |

| unchanged | |||

| Investment in transport with private participation per capita (current US$) | 4.26 | 4.30 (+0.73%) | 4.26 |

| Investment in water and sanitation with private participation per capita (current US$) | 0.0012 | 0.0012079 (+2.68%) | 0.01 (+750%) |

| Domestic private health expenditure per capita, PPP (current international $) | 376.37 | 395.69 (+5.13%) | 376.37 |

| Foreign direct investment, net inflows per capita (BoP, current US$) | 152.46 | 152.46 | 152.46 |

| unchanged | |||

| ROA (Profit/Assets) | 0.58 | 0.66 (+14.37%) | 5.47 (+847.55%) |

| ∆ROA, % | −48% | 0% | 727.31% (+1515.23%) |

| Parameters of Investments That Are to Ensure the Overcoming of the Crisis | Manifestation in the Existing Approach to Financial Risk Management Amid the Economic Crisis | |||

|---|---|---|---|---|

| Mechanism of investing | public-private partnership | |||

| Type of investments | responsible investments | |||

| Period of investing | long-term | |||

| The scale of investment projects | large-scale investments | |||

| Object of investing | social and ecological innovations in infrastructure in the sphere | |||

| energy | transport and logistics | water and sanitation | healthcare | |

| SDGs that are supported within the investment projects | SDG 7 | SDG 11 | SDG 6 | SDG 3 |

| +SDG 9 (industry, innovation, and infrastructure) and +SDG 8 (decent work and economic growth) | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yankovskaya, V.V.; Mustafin, T.A.; Endovitsky, D.A.; Krivosheev, A.V. Corporate Social Responsibility as an Alternative Approach to Financial Risk Management: Advantages for Sustainable Development. Risks 2022, 10, 106. https://doi.org/10.3390/risks10050106

Yankovskaya VV, Mustafin TA, Endovitsky DA, Krivosheev AV. Corporate Social Responsibility as an Alternative Approach to Financial Risk Management: Advantages for Sustainable Development. Risks. 2022; 10(5):106. https://doi.org/10.3390/risks10050106

Chicago/Turabian StyleYankovskaya, Veronika V., Timur A. Mustafin, Dmitry A. Endovitsky, and Artem V. Krivosheev. 2022. "Corporate Social Responsibility as an Alternative Approach to Financial Risk Management: Advantages for Sustainable Development" Risks 10, no. 5: 106. https://doi.org/10.3390/risks10050106

APA StyleYankovskaya, V. V., Mustafin, T. A., Endovitsky, D. A., & Krivosheev, A. V. (2022). Corporate Social Responsibility as an Alternative Approach to Financial Risk Management: Advantages for Sustainable Development. Risks, 10(5), 106. https://doi.org/10.3390/risks10050106