1. Introduction

We consider the problem of valuing a real option, a derivative providing the right to undertake in a capital investment project, or in general, to invest in a given real asset within a specified time period. More details about real options in investment are provided in

Dixit and Pindyck (

1994). We begin with the formalism developed in

Grasselli (

2011); the results in the current manuscript are based on the numerical model presented in this reference. The distinguishing characteristics of the Grasselli approach were that it enabled the real option to be valued in an

incomplete market, within a

finite time horizon.

In an incomplete market, the time-varying value of the real project under consideration is

not perfectly correlated to a traded financial asset (or a stock market index), so that the option value cannot be fully hedged. Thus, its value depends to a degree on the investor’s (or the implied market) risk preferences. The finite time horizon, (or investment period) meant that the option value and the minimum project value at which its exercised both depend on the time until expiry. In

Grasselli (

2011), an exponential utility function is used to model the investor’s risk preferences, following work by

Hugonnier and Morellec (

2007) and

Henderson (

2007) (which utilised an infinite time horizon). A binomial tree model in the manner of Cox, Ross and Rubenstein

Cox et al. (

1979) is used for computational calculations.

For the purposes of the current manuscript, we incorporate two extensions into the numerical model. In Grasselli’s work, the risk-aversion coefficient , the parameter of the investor’s utility function, is constant over the lifetime of the project, and applied to the discounted monetary units at each backward induction step on the binomial tree. It implicitly assumes that the “inflation rate” applied to the nominal monetary amounts to which the investor assigns a fixed utility level over time, is equal to the risk-free interest rate. This may not be the case.

Extending this idea further, some recent literature has stated that a constant risk-aversion coefficient is unrealistic and may introduce substantial decision biases to the optimal strategies.

Thaler (

1981) shows that there exists some empirical evidence about dynamic inconsistencies in the discount factors.

Loewenstein and Prelec (

1992) studies the time-inconsistency when making decisions and provides an economic explanation.

Yong (

2012) derives optimal strategies for time-inconsistent optimal control problems based on the method of Hamilton-Jacob-Bellmen equations.

Zhao et al. (

2014) analyzed the optimal dividend payment strategies under the assumption of time-inconsistent preferences. Some related work about time-inconsistent preferences includes

Ainslie (

1992);

Grenadier and Wang (

2007) and

Chen et al. (

2014).

To reflect the time-inconsistency in the decision making process, we suggest that the project inflation rate, , may better characterise the investor’s time-dependent risk preferences (than the risk-free rate). Regardless, our first extension is introduce a new parameter, i, which characterises the investor’s implicit inflation rate. Then, we replace the coefficient with a time-varying substitute, , which decays exponentially (with time t) at a rate determined by the difference between i and the risk-free rate r.

The second extension is to introduce a jump-diffusion component into the model. It is well known that the Black-Scholes model fails to capture the volatility smiles and fat tails that have been observed in financial markets since the late 1980s. Since then, much work has sought to overcome its drawbacks. Jump-diffusion models are among one of the most popular alternative models because of their advantage in describing the short-run behaviour of security prices.

Kou and Wang (

2004) studied exotic options under a double-exponential jump-diffusion model. A mixed-exponential jump-diffusion model is proposed in derivative pricing in

Cai and Kou (

2011). Work related to jump-diffusion models includes

Merton (

1976),

Pham (

1997),

Song et al. (

2006) and

Bonis et al. (

2009). For our purpose, the justification is that the estimated value of the project is likely to not vary in a continuous manner according to geometric Brownian motion, but instead, to be subject to a number of intermittent adjustments (jumps), reflecting new information about project profitability or viability. The jump-diffusion process (or jump process) may be treated as uncorrelated with the performance of the traded asset (or index). Therefore, we treat it as a component of the non-hedgeable source of fluctuations in the project-value process.

In this work, we utilise a double-exponential distribution to represent the logarithm of the jump magnitude, with the number of jumps occurring up to a given time following a Poisson process. Compared with the double-exponential distribution adopted in

Kou and Wang (

2004), the parameters of the jump process were subject to an important restriction: incorporation of this process into the project-value process should not alter the drift or volatility of the latter. This is for two reasons. First and most importantly, it permits us to control for these dominant low-order effects (drift, volatility), which can be modified through the other parameters of the project-value process. (We can isolate the higher-order effects that are unique to the jump-diffusion model.) The second reason is that it permits us to represent the process with fewer free parameters. To apply the jump process on the binomial tree, we represented the double-exponential distribution in discrete form, using an approach by

Luceño (

1999) in order to match both the low-order moments and the cumulative distribution function of the continuous random variable to reasonable accuracy.

In the subsequent sections of this manuscript, we describe our modifications to the Grasselli algorithm, and present and discuss some numerical results highlighting their effects. Because of its importance in investor decision making, we follow Grasselli and his predecessors in emphasising the option’s exercise threshold value, the minimum project value (at any time) for which the option should be exercised immediately. We also afford significance to the time value of the option, the difference between its current value and the maximum of its immediate exercise value or zero. We present colour maps of this quantity vs. both time and project value. We compare different cases according to the values they assign to the option when the project value is “at the money”.

The structure of the remainder of this manuscript is as follows. In

Section 2, we provide a general mathematical model for the random processes describing the project and stock price movements (

Section 2.1), and present our representation of the investor’s time-dependent utility function (

Section 2.2). The specific form of the jump process, based on a double-exponential jump distribution, is given in

Section 3. In its three constituent sections, we present, respectively: the jump distribution itself, including parameter limitations; the backwards induction step on our multinomial tree; and the method for discretising the jump distribution.

Section 4 follows by providing more detailed specifics of the numerical algorithm we used in our calculation, including the justification for the selection of numerical parameters. We provide some results of the simulation in

Section 5, highlighting the different issues we raise in the manuscript.

Section 5.1 demonstrates the significance of the time dependence of the investor utility function, and

Section 5.2 the effect of varying inflation. In both preceding cases, jump diffusion is not incorporated into the model, in order to target these alternative effects. Instead, it is investigated in

Section 5.3, which shows the effects of varying all of its major parameters. Our conclusions are summarised in

Section 6.

2. Model Description

2.1. Fundamentals of the Model

We consider a market in which there are two liquidly traded assets, a stock (index) with value at time t, and a riskless bond, with value , for which .

There also exists a project, whose value at time t is represented by , which is not traded. However, a real option exists, which, at the option-holder’s choice, may be exercised at any time t satisfying , where the upper limit T is the finite stopping time of the project. If exercised at time t, the option provides an immediate payoff of , where is the time-dependent strike price, a deterministic function of time defined in the option contract.

We assume that

obeys geometric Brownian motion, and that the random process for

is Markovian and time-homogeneous. As in

Grasselli (

2011), it is partially correlated with

. In our case, however, it is not restricted to following geometric Brownian motion. The quantities

and

are assumed to be increasing exponentially with time, with continuous compounding rates

r and

, respectively. The rate

r is the risk-free interest rate, and

is an inflation rate that is specified in the terms of the contract. Quite possibly

.

The effect of the non-zero riskless interest rate can be removed by expressing , , , and , in discounted coordinates, to yield S, V, B, and I, respectively. That is, we divide the former quantities by the common numeraire . Letting be the arrival time of the n-th jump, then is the number of jumps up to time t, a Poisson counting process. Let be a jump process representing the sum of jumps, which are denoted by , with arrival rate and jump size density distribution . That is .

The discounted quantities obey the following rules (

Grasselli 2011, Equation (1)):

We also assume that (by appropriately selecting both monetary units and the bond size at time ), and require that the parameters , satisfy the condition .

The random processes , and (the last-mentioned two being Brownian motions) are assumed to be independent, so that, in particular, the random components of and are only dependent on each other through , with the correlation term indicating the magnitude of this dependence. The terms represent the drifts of , , respectively, and positive , represent their volatilities.

In

Grasselli (

2011),

evolved in time according to geometric Brownian motion, that is,

was equal to zero. The more general form of

permits us to incorporate other models of project-value movements, such as jump diffusion, into the formulation. Equation (2) is expressed in terms of

, rather than

, to permit the choice of distribution for

to be incorporated into the multinomial tree we develop in

Section 3.2 without modification, since the tree utilises a logarithmic scale for

. The mean and variance of

are selected to be equal to those of

and

. That is,

,

. This is to ensure that the parameter

is meaningful as a measure of volatility. The correction terms

in Equation (2) are necessary to ensure that

represents the drift of

, regardless of the value of

.

The market is incomplete, since it is not possible to replicate the variations of the value of the project by merely dynamically trading the stock and the bond. Thus, there will not be a unique arbitrage-free price for the real option. In order to calculate a price, the option holder’s risk preferences must be taken into account. We represent the risk preferences by a utility function

; the potential investor will seek to maximise their expected utility at any given time. The subscript

t represents the possible explicit time-dependence of the utility function, an idea we develop in

Section 2.2.

Based on this formulation, the value of the option at any time t can be expressed . The parameter W represents the investor’s total wealth at time t, which may influence their risk preferences, given the utility function. Our aim is to calculate the quantity D using backwards induction on the multinomial tree.

The fact that

is independent of

, guarantees that, at a given time

t, the option price

does not depend on the current value of

. This is because for any dynamic trading strategy, the quantity

will be equal to the incremental proportional change in the total investor wealth invested in the stock, regardless of the price of an individual unit of stock. Thus, as in

Grasselli (

2011), a one-dimensional tree is sufficient to calculate

D. Also, we may write

, suppressing the notation indicating the explicit dependence on

W.

2.2. Time-Dependence of the Exponential Utility Function

The calculation of the option value is considerably simplified if we adopt an exponential utility function . This is due to the fact that an investor whose utility can be described in this way exhibits constant absolute risk aversion, with risk aversion parameter . As such, the initial value of the investor’s total wealth, , is irrelevant in determining the option price D.

We have incorporated time-dependence into the utility function for two reasons. Firstly, the monetary values x we shall use in our calculation will be represented in terms of their present values at time 0, according to discount rate r. However, at any time t, when an investor is making a decision about whether to exercise the option, the quantities of money considered will be in terms of their undiscounted values at time t. Therefore, the factor should be appropriately scaled in order to reverse the discounting effect.

The second reason why time-dependence should be incorporated into the utility function is that the investor’s risk preferences may change over time. We denote by i the inflation rate that applies to monetary values over time to which the investor assigns a fixed utility level. Its effect on is to impart an exponential decay factor at rate i. This corrects the product for the fact that x is expressed in nominal, not real monetary units.

Thus, in order that the utility function captures both of these time-dependent effects, correction for discounting, and the investor’s implicit inflation considerations, then:

where

is the risk-aversion parameter at time 0.

Note that in

Grasselli (

2011), a constant value

is used at all times. In terms of Equation (

5), this would imply that

, that is, an investor’s relative risk treatment of different monetary amounts would vary in accordance with the risk-free rate

r. In practice, it may be more likely that

better describes the investor’s behaviour: their risk-attitude towards the real value of a project remains stable over time. We shall compare the two cases in our subsequent calculations.

3. Jump-Diffusion Model

3.1. Distribution of the Jump Process

We specify a form for the jump process

. The jumps occur according to a Poisson process with rate

, and with the following properties. In a short interval

,

We assume that

is distributed according to a double-exponential distribution demonstrated in

Kou and Wang (

2004), with parameters

, so that its probability density function:

Thus, the random process

is characterised by the four parameters

and

. However, if these parameters are allowed to vary freely, their selection may introduce additional volatility into the project value, a parameter that we wish to control for as noted in the Introduction. Instead, volatility (and drift) can be modified through the parameters

,

in Equation (2). Thus, we restrict the parameters of

, matching the first and second moments of the random variables

and

, for all

t. As a result, the volatility of

will not depend on

. The drift of

was already controlled by the correction terms (in Equation (2)), described in

Section 2.1. However, matching the first moments of the random variables provides first-order correction. Given these restrictions, we may characterise

in terms of two free parameters instead of four. They are

and

. The other original parameters can be expressed in terms of

and

as follows:

Finally, the parameter

is related to the skewness

, the scaled third moment of

, according to the equation:

3.2. Setup of the Multinomial Tree

The multinomial tree is set up in a similar manner to that of

Grasselli (

2011). We define the time step to be

. Then consider a single step, from time

t to time

. We wish to calculate the value of the option

, given a particular current value for the project,

, and the values of the option for all project values at time

.

Following (

Grasselli 2011, Equation (29)), we let the ordered pair

evolve over a time step as follows:

where the random variable

is a discrete approximation of the random variable

. This will approximate the evolution of the random process to order

.

The values

apply the binary “up-down”, “high-low” factors to

S and

V, and the probabilities

associated with the four options (two binary choices) are similar to their respective values derived in (

Grasselli 2011, Equations (46)–(51)). However, they must be corrected to take into account the fact that the volatility

is partially allocated to the jump-diffusion term in Equation (2).

Based on the actual stock price

and project value

, up to the order

, we work with the increments relating up to down and high to low,

where

u and

h are multipliers on the stock price for an up move and a down move, respectively.

Following the procedure in

Grasselli (

2011), we work with the logarithms of the geometric Brownian motions of

and

, i.e.,

and

respectively, to simplify the calculation. Under the condition that there is no jump in the project value during the time step, we match the mean and covariance matrix for the discrete-time process on the binomial tree with increments

with those of the continuous-time process

up the order

. Denoting

,

, we have (

Grasselli 2011, Equations (38)–(42)):

where:

Solving this linear system, we obtain the unique solution:

where

In Equation (

10), we disregard the effect of the factors

h and

ℓ in cases when a jump occurs, because they have negligible relative impact when

is small. Also, we have not absorbed the correction terms (from Equation (2)) into the definition of

, so as to show their explicit impact on the preceding equations.

One important note is that when we generate the tree on a logarithmic scale, the increment size for the discretisation is set by the value . If approaches 1, this quantity will tend to zero, making the computation numerically intractable. It means that the random fluctuations in project value are almost entirely determined by the jump process, which is independent of the stock price. Thus, we choose an arbitrary upper bound of when performing our calculations.

The parameter

, the “below-equilibrium rate-of-return shortfall”, is defined in

Grasselli (

2011) as the difference between the value of

related to the capital asset pricing model (CAPM) equilibrium and the actual value of

. It satisfies the equation:

which we maintain even though

encompasses the volatility associated with the jump-diffusion component of the project-value process.

We permit the discrete random variable

to take on the values:

with probabilities:

respectively. The increment size for the discretisation

is set by the value

. That is, each of the

values (

to

n) must be a multiple of

, so that the tree recombines. The procedure we use for selecting the

and

parameters is provided in the following section.

We calculate the discounted option

continuation value . That is, the value of the option to the investor at time

t, if they do

not choose to exercise it then, following the derivation in (

Grasselli 2011, Equation (35)), is equal to:

In this equation,

where

represents the discounted value of the option.

Finally, we calculated the discounted option value

D, at time

t, project value

. It is equal to the

maximum of the continuation value and the

immediate exercise value,

. That is,

where

The preceding equations permit backwards induction to be performed on the tree.

3.3. Discretisation of the Random Variables

We now consider the selection of the parameters

and

, that is, the probability distribution of the discretisation of

. In order to achieve this, we utilise an approach explained in

Luceño (

1999). Given two integer parameters—

M,

N—the method provides a recursive algorithm for generating a discrete approximation to a given continuous distribution, with the following three properties. Firstly, the two distributions share the same low-order moments up to moment

. Secondly, their distribution functions (CDFs) coincide at at least

points. Thirdly, the discrete distribution takes on

different values, that is,

. For computational efficiency, it is preferable to keep the product

as small as possible, without sacrificing the accuracy of the approximation.

In implementing the approach, we selected M bands containing equal probability weight. That is, the points where the two distributions coincided corresponded to their 0, , -th percentiles. In fact, the approach guarantees that exactly discrete values occur between any pair of these successive percentiles.

In selecting values for M, N, note that the choice guarantees that the three moment parameters—mean, variance, skewness—necessary to define a double-exponential distribution are preserved in the discretised form. We believe that, given an upper restriction for n, there is greater utility in increasing the parameter M, rather than selecting a value of N greater than 2. The discrete CDF will converge uniformly to the continuous CDF through the increasing number of coincident points, at equally spaced probability weights.

Finally, given , we have chosen M by acknowledging the trade-off between computational speed and the accuracy of the approximation. There is another consideration: following implicitly from the allocation of two discrete points for each of M bands, the maximum value of selected by the algorithm will increase as M does. For the simplest case if , then , respectively. By choosing a smaller value of M, we can reduce the size of the arrays we need to store in order to perform the backwards induction step of the process. This consideration is of greater significance when we have skewed distributions, with long tails in one direction. For example, if and , then , respectively.

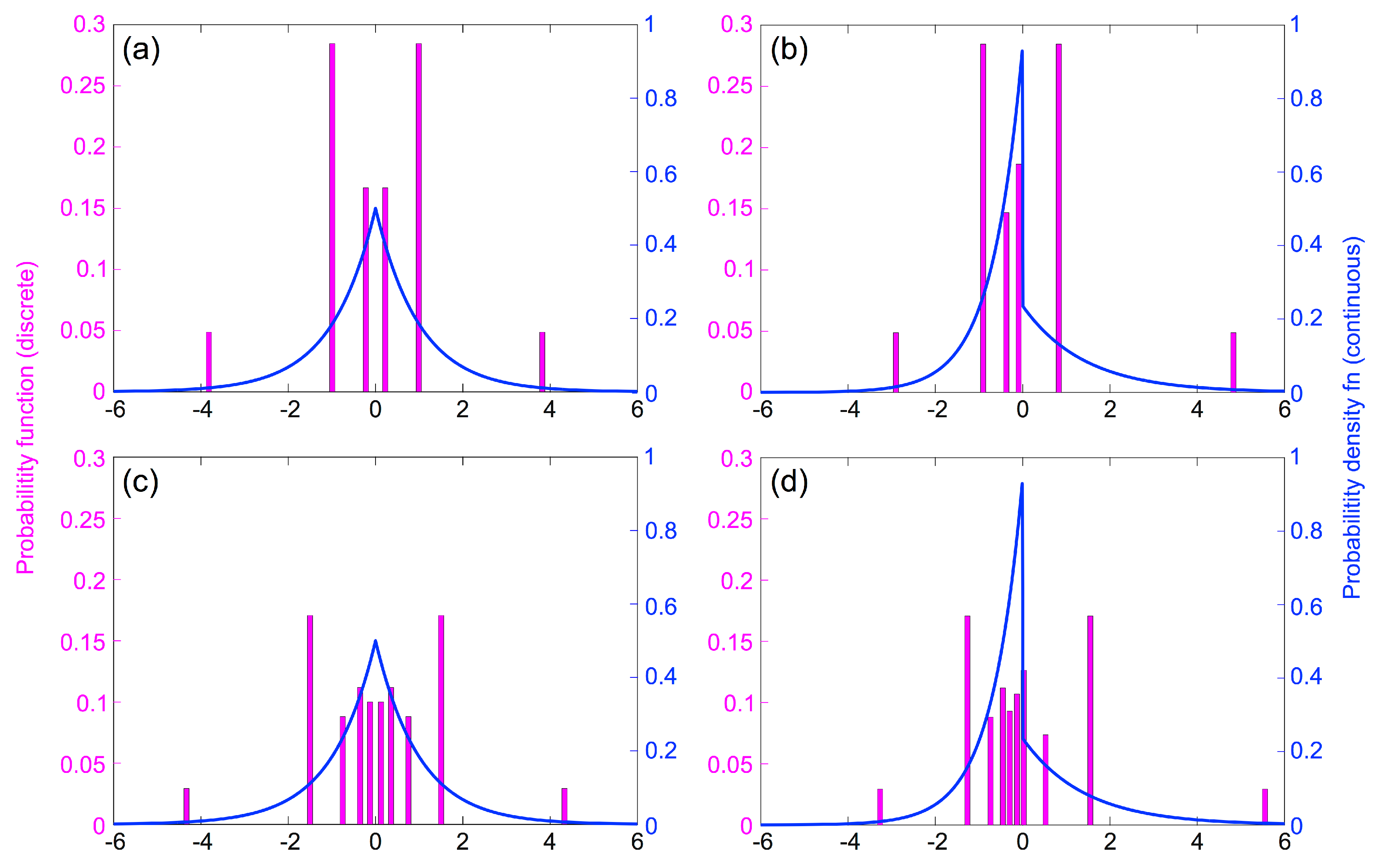

Comparison between the continuous and discrete-approximation density functions, for these two cases (

), for

, are illustrated in

Figure 1. In

Figure 1a,b, two discrete values occur below the 33.3

rd percentile and above the 66.7

th percentile of the respective continuous distributions. For

Figure 1c,d, the percentiles are the 20

th, 80

th respectively. Thus, the most extreme values for the

case are more extreme than those for the

case (consistent with the earlier statements about

), but they have lower weight.

Based on these considerations, we believe that

is a suitable compromise for providing both accuracy and computational efficiency. Some additional numerical analysis is provided in

Section 5.3.1.

We also were required to round the

values for which the discrete distribution is defined to the nearest multiple of

. For small

, the error introduced at this step will often be negligible, but we address the issue in more detail in

Section 5.1.

4. Numerical Calculation

We proceed by listing the input parameters of the calculation. The fundamental parameters are

T,

,

,

,

,

,

,

,

i,

r,

,

(or

),

and the numerical parameters are

,

M,

N. The parameter

can be calculated using Equation (

11).

Next, we must decide upon the sizes of the arrays (multinomial trees). The number of columns is set by T, , and is equal to . The set of times is . The number of rows is set by considering the maximum and minimum values of V for which the option price is calculated, say , , respectively. We recall that V represents the value of the project at any given time, discounted at the risk-free rate to its present value at time .

The range of values of

V, from

to

, must be sufficiently broad so as not to affect the result of the simulation. Their influence on the calculation is through Equation (

12), in which a weighted sum of the option values at time

is required in the calculation of the

continuation value of the option at time

t. Suppose

is the

maximum discounted exercise threshold over the interval

. That is, for any time

, if the discounted project values exceeds

, we are guaranteed to exercise the option immediately, and we do not need to calculate the continuation value (or apply Equation (

12)). Then

need be no greater than

, according to the definition of

. Of course,

is not necessarily known precisely in advance of performing the calculation, however, a reasonable upper bound can be specified by adding a small margin to its value in known cases (for example, the

case).

The value of need only be chosen so that the option value is near-zero, with reasonable tolerance, when the discounted project value lower than this value, at all times t. Such a value can be determined by trial and error, using the case , and then applied to more general cases as required.

Once

,

are specified, the discrete values of

V are evenly spaced on a logarithmic scale, with increment

. Thus, the number of rows is:

where the “floor” notation indicates rounding down to the nearest integer.

We next generate the arrays. Firstly, we define the column vector

of values of

V, as follows:

where the superscript

T represents matrix transpose, and the exponentiation operator is applied to each element individually.

Next, we consider the matrix of option values, , which has dimensions . Each row corresponds to a different value of the project value; each column to a different time step.

The rightmost column, column

, corresponds to time

T. At this time, the option has no continuation value, and its value is equal to its exercise value (both discounted to time

), so that (

Grasselli 2011, Equation (53)):

where

is an

vector with all entries equal to

, and the notation on the left-hand side represents the

-th column of

.

Next, backward induction is applied to columns

in this order. To do so, Equation (

12) is applied point by point to the values in the vector

. For calculation efficiency, in calculating the entry

, corresponding to column

j of the array, we only need to be concerned with values of

that are below the exercise threshold for the column, noting that this is not known precisely in advance for each value of

j. For higher values of

, the discounted option value is equal to the immediate exercise value.

However, the calculation for may make reference to out-of-bound entries of the vector , if V is particularly low (near ). Note that appropriate selection of should avoid this problem in the high-V case. This is due to the limited range of project values for which the option continuation value is calculated, as explained in the previous paragraph. In the low case, we may substitute zero for out-of-bound values, which should be appropriate according to the selection of .

The discounted immediate exercise value of the option at the

j-th column is given by the vector:

and is permitted to be negative.

The discounted option value vector , where the maximum operation is performed element by element. The exercise threshold is the value for which . This threshold may be calculated using linear interpolation, given the two vectors. Then

The backward-induction operations can be performed on a column-by-column basis (instead of an element by element basis), using a convolution operation to implement Equation (

12) step, applied to the denominators of the arguments of the log functions. This is useful from the perspective of calculation efficiency, especially given the few values for

required in our discretisation approach.

Finally, for display purposes, we have chosen to re-scale the array so that each row corresponds to a constant undiscounted project value, rather than a constant discounted value. (The discounting step is a mathematical convenience introduced at the start of the calculation, to the somewhat arbitrary choice of time .) Noting that the (vertical) project-value scale is expressed in logarithmic units, this is achieved by translating each column in the array by the appropriate amount to reverse the effect of discounting. Interpolation is used to deal with translations of fractional units of . The figures presented in the next section are adjusted in this way. Similarly, the option values displayed in the figures are in undiscounted values, calculated by multiplying the discounted option values D, by .

The process allows us to calculate option exercise threshold at each point in time, the option value for every combination of project value and time. The option value can be split into time value and money value, and it is convenient to display the former in the figures. The value of the option when “at the money” is also plot against time. It may be calculated by interpolation from the derived array , and considered along with the exercise threshold (at time ) as a means of comparing the results when the input parameters are modified.

5. Simulation Results

We performed numerical calculations using Matlab 2016a on a PC with an Intel (R) Core (TM) i7-6700HQ CPU @ 2.60 GHz, and 16 GB RAM, on Windows 10 (64-bit).

We utilised the following parameters, unless stated otherwise, following

Grasselli (

2011). Fundamental parameters:

;

;

;

;

;

;

;

. The selected numerical parameter

was usually chosen to be 0.0005, with exceptions noted in the text where applicable.

5.1. Time-Dependent Utility Function

In the first instance, we set

, so that there is no jump-diffusion component to the project price movements.

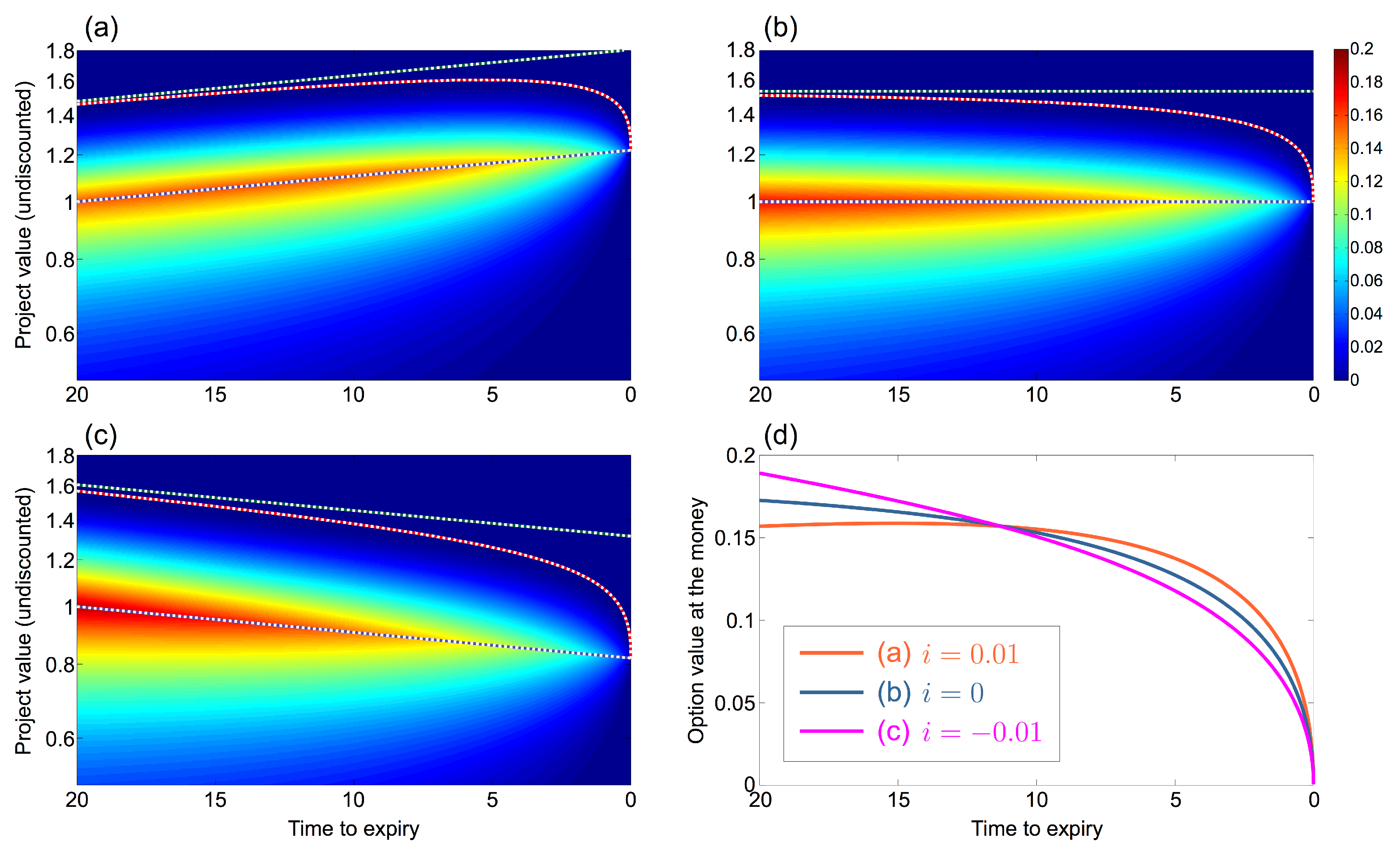

Figure 2 shows the difference between the cases where

and

. The vertical axis represents the undiscounted project value,

, plotted on a logarithmic scale. The horizontal axis is shown on a reverse scale indicating time to expiry. Thus, actual time

t runs from left to right, beginning at

. This is explicitly indicated in

Figure 2d.

The colour scale in the two-dimensional array represents the undiscounted time value of the option, which is greatest when the option is approximately at the money. For each panel of the figure, the blue dotted line indicates time/project-value combinations for which the option is at the money. Since the inflation rate , this is a horizontal line at project value 1. The green dotted line, drawn parallel to the blue line, represents (at time ) the exercise threshold in the limit . Finally, the red dotted line represents the exercise threshold throughout the lifetime of the option, above which the time value of the option is zero.

In the top row, for which

,

Figure 2a, for which

, is identical to the rightmost region of the

Figure 2b (

). This is because, in the absence of inflation (in either the option contract or the option-holder’s preferences), the situation faced by the option-holder 10 time units prior to expiry does not depend on the value of

T. The red curves are strictly increasing as time to expiry increases, that is, looking from right to left, representing the corresponding increasing benefit of holding the option.

In the case

(lower row of

Figure 2), once again, the red curve lies strictly below the green line at time

, representing the greater value of an option with a longer time to expiry. However, in this case, specifically in

Figure 2d, the decision threshold (red curve) is not necessarily decreasing over the lifetime of the option. This surprising effect is due to the fact that the option-contract-specific inflation rate,

, is lower than the investor’s implied inflation rate,

i. Thus, for large values of

t, the option-holder is less risk-averse with respect to monetary values equal to the strike price, so is more likely to delay exercising the option. Just as the exercise threshold increases over the life of the option, similarly, the option value at the money increases prior to decreasing to zero at expiry.

To avoid this counterintuitive result, we believe it is more sensible and realistic to adopt the approach that , so that both at-the-money option value and the exercise threshold are decreasing functions of time. If a known alternative effective inflation rate can be assigned to the investor, this value should be used instead.

The calculation times (in seconds) for the backwards induction step (i.e., generating the two-dimensional arrays) are provided in the figure caption. They are the averaged results of three trials in each case. These times are clearly dependent on the sizes of the arrays. The values are almost four times as large as the values, due to the additional computational resources required to progressively update the larger arrays.

5.2. Inflation Effects

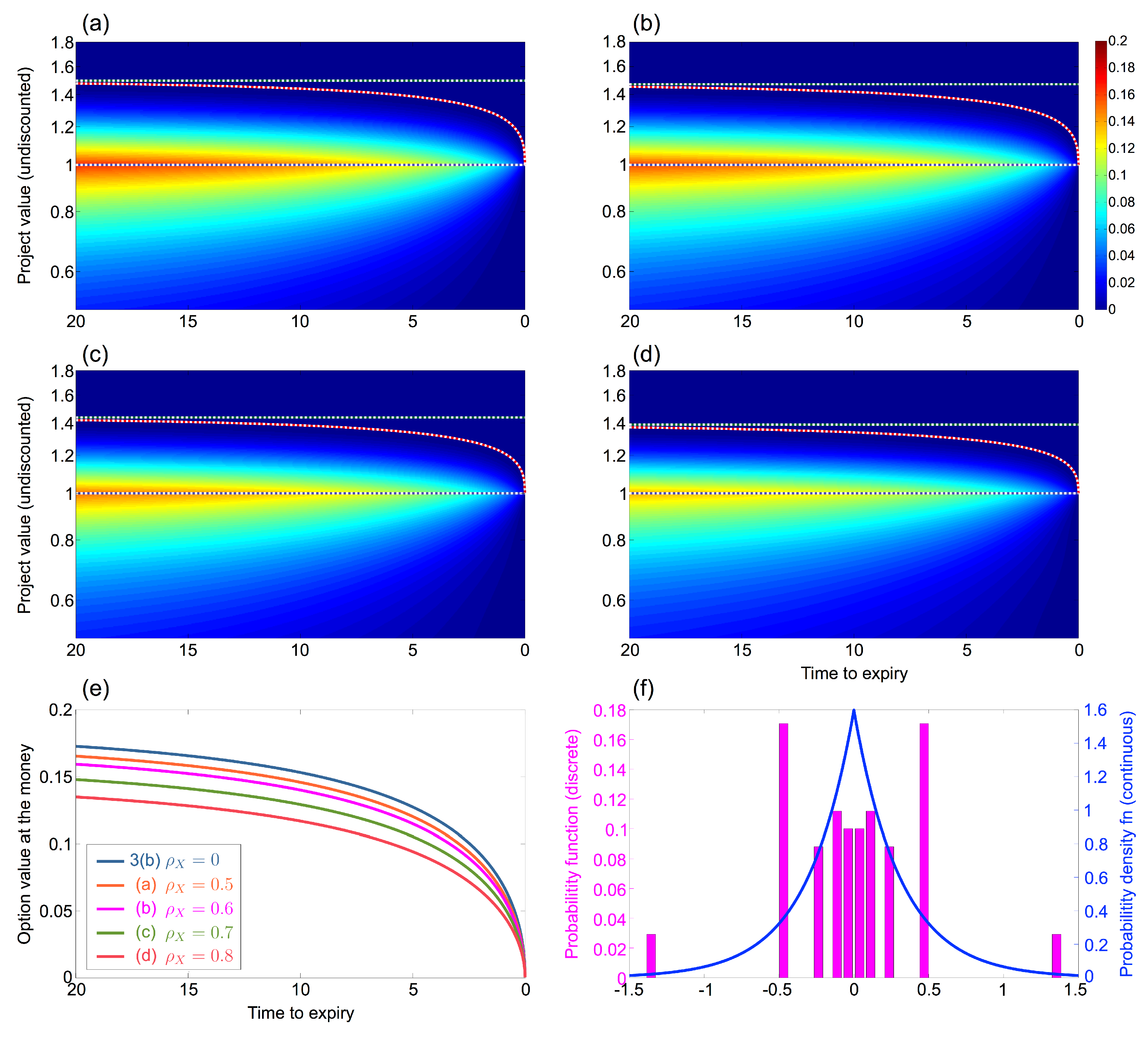

Given

, we consider the effect as this parameter is varied.

Figure 3 presents plots in the manner of

Figure 2, for the cases (a)

, (b)

, and (c)

. The parameter

, and all other parameters are as given at the beginning of this section. In each case, the (red) exercise threshold curve approaches the (blue) at-the-money line as time

t increases, a consequence of the two inflation parameters being equal.

The at-the-money option value at time is greatest when , and least when . This is because the option is more likely to be “in the money” at any point in the future, if inflation (as specified in the option contract) is lower (or negative). Similarly, the exercise threshold increases for decreasing .

However, the at-the-money option value decreases much more sharply with time

t as inflation decreases, as shown in

Figure 3d, so that eventually (towards the right of the panel), the order of the three curves is reversed. This effect can be ascribed to the fact that the actual monetary values on the at-the-money line increase/decrease according to inflation/deflation, which will contribute a scaling effect to the option value. In fact, the curve for the positive-inflation case is actually increasing with

t for a subset of its domain (low values of

t).

The reported calculation times, provided in

Figure 3 caption, are consistent with the values provided in

Figure 2, given

T. The slight differences between them are due to the different maximum and minimum values of

V (and hence the sizes of the arrays) for the different cases (and random variation).

5.3. Incorporation of Jump Diffusion into the Project Value

We now restrict ourselves to the case

in order to compare the results as the jump-diffusion parameters are varied. This permits us to avoid the issues described in the previous sections, including the scaling issue that occurred when the project value at the money varied over the lifetime of the option. The results are presented in successive figures. As noted in

Section 3.3, we used the values

,

to perform the calculations.

5.3.1. Effect of Varying the Parameter

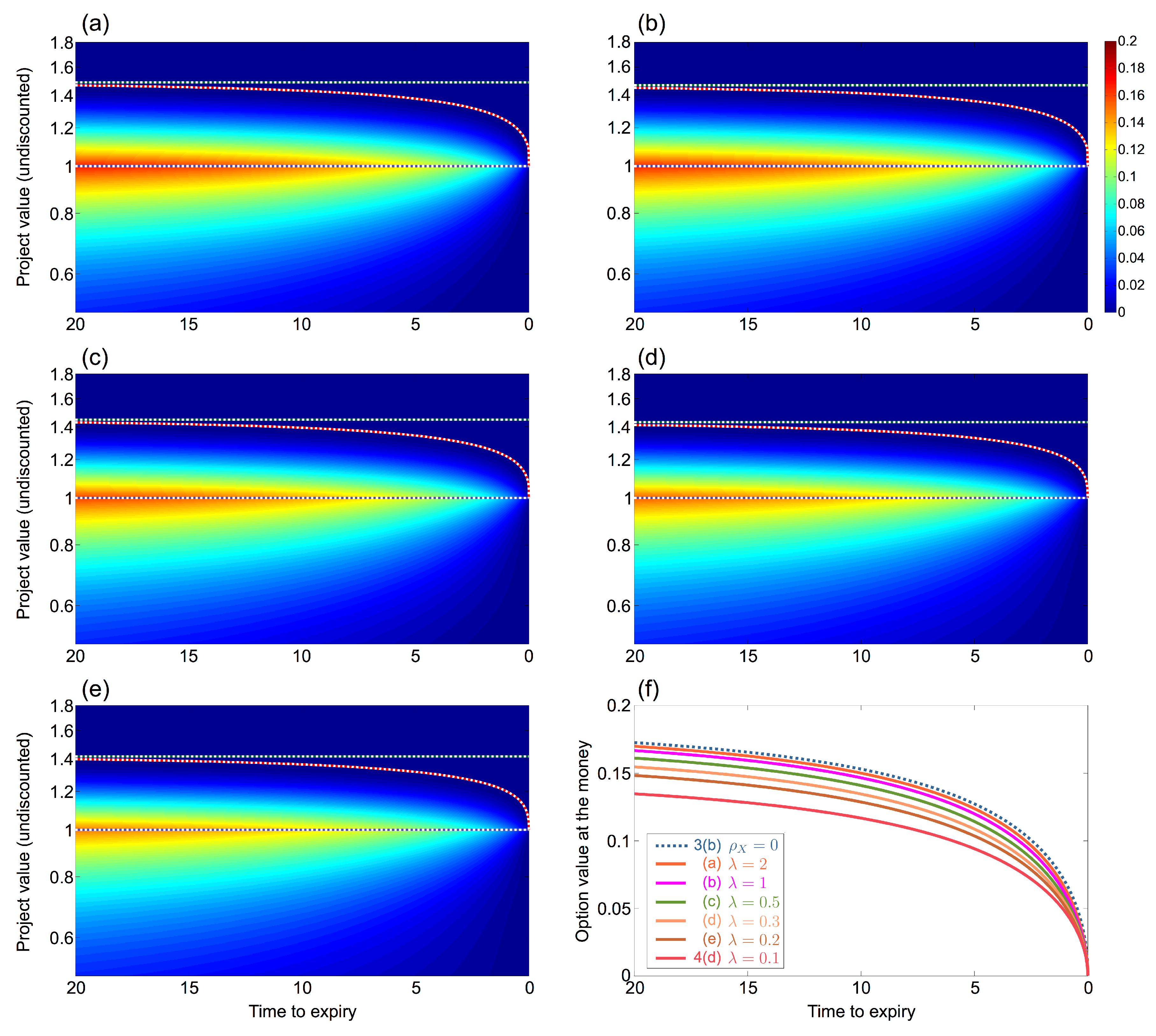

In

Figure 4, a jump-diffusion model is presented with the parameters

. The latter parameter choice means that upwards and downwards jumps are equally likely. Results are displayed for different values of

. [The ratio

is the relative contribution by variance of the jump-diffusion component to the project-value fluctuations that are independent of the stock index movements.]

Despite the fact that we have controlled for the drift and volatility of the project-value process, the net effect of introducing jump diffusion into the model is to reduce the option value and exercise threshold, as indicated in the figure. The risk-averse investor responds negatively to the possibility of extreme changes in project value, valuing the option less and being more likely to exercise it early, if the other parameters are held stable.

Figure 4e shows that the relative option values for different

cases remain stable over the option’s lifetime, and

Figure 4f presents a comparison between the continuous double-exponential probability density function and its discrete approximation. Up to rounding of the

values, the discrete and continuous cumulative distribution functions match at the quintiles of the latter, and the first three moments agree. Due to the symmetry about the origin for the case

, the distributions also have equal medians.

The calculation times provided in

Figure 4 are also provided as multiples of the

case, so that the computational cost of incorporating jump diffusion into the model is quantified. This cost comes about from two sources: firstly, the incorporation of the

n-term sums into Equation (

12), recalling that

; and secondly, the increased sizes of the arrays required when

is large (to accommodate larger jumps). The effect of the first source in isolation can be approximated by considering the low-

case. The additional computational burden is quite modest (relative computation time 1.3×). The value increases to 1.9× for the

case, for which the jumps are the dominant source of stochastic variation in the project value. This may be accounted for by the second source identified above; it reflects the concomitant increase in the array size.

We also use this scenario to compare the effects on the results and calculation time when the computation parameters

M and

N are modified. Firstly, we consider three cases for the pair

, as presented in

Table 1. Our choice of selected parameters provides similar exercise thresholds and option values at the money to those of the higher values

. However, the calculation times are only modestly greater than those of the

case, to within

the respective

calculation times. These observations suggest that our choice is a reasonable compromise between accuracy and computation speed.

5.3.2. Effect of Varying Jump Rate

Figure 5 illustrates the effect of modifying the parameter

, when other parameters are held constant. Note that if the jump rate is increased, but the drift and volatility remain constant, then the jump size must necessarily decrease. Also, according to the central limit theorem, as

increases indefinitely, the jump process should tend towards the Brownian motion process

. That is, the model should approach the case for which

. This observation is borne out in

Figure 5f. Beginning at the case

, from

Figure 4d, the option value curve rises steadily as

is increased to (a) 0.2, (b) 0.3, (c) 0.5, (d) 1, then (e) 2, ultimately approximating the case

from

Figure 3b. Again, the relative option value remains consistent over the entire time to expiry.

The differences in calculation times listed reflect the second source of costs mentioned in

Section 5.3.1, that is, different array sizes. The calculation times also reflect the first source (additional calculations per induction step), even for high values of

, when the result is similar to the case

. Given these considerations, the times listed are consistent with those of

Section 5.3.1.

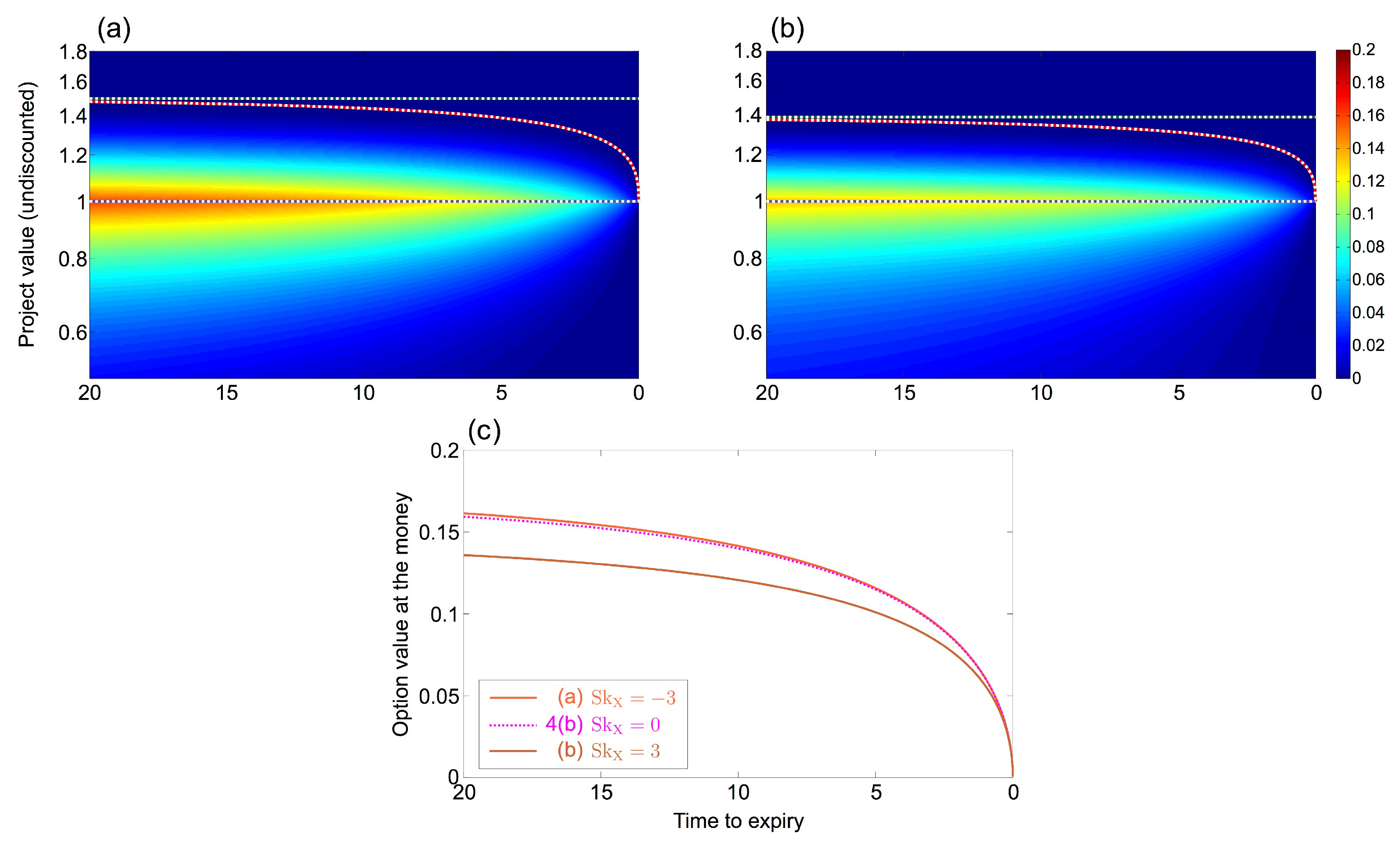

5.3.3. Effect of Varying Skewness

In

Figure 6, starting with the parameters used to generate

Figure 4b, we investigate the effect of modifying the skewness parameter

from the value 0 which has been utilised thus far.

We used the values

, 0 and 3, corresponding to

and 3.73 respectively. In

Figure 6c, we see that the largest at-the-money option value occurs when

(that is, 0.1614), with value falling to 0.1588 for zero skewness, and much further to 0.1359 for skewness +3. The asymmetry of this effect (about zero skewness) is due to the different characteristics of the upside and downside risks associated with jumps in the positive- and negative-skewness cases, noting that the value of an option lies in its ability to eliminate downside risk. Specifically, in the positive-skewness case, most jumps are downwards and small in magnitude, with a few being upwards and large in magnitude. However, these directions are reversed in the negative-skewness case. (We emphasise again that all effects must be understood in the context that drift and volatility are held constant in the project-value process.) In

Section 5.3.4, we will see that the effect of increasing

rapidly mitigates the limited-downside-risk issue associated with the positive-skewness case.

The optimal exercise threshold exhibits a similar dependence on skewness, being also asymmetric about the origin. The listed calculation times, comparable with the 4.48 s from

Figure 4b, tend to increase for greater values of skewness. This is due to different sizes of the required arrays (the second “source” of computational cost from

Section 5.3.1), due to the fact that a lower value of

must be selected if larger positive jumps are possible.

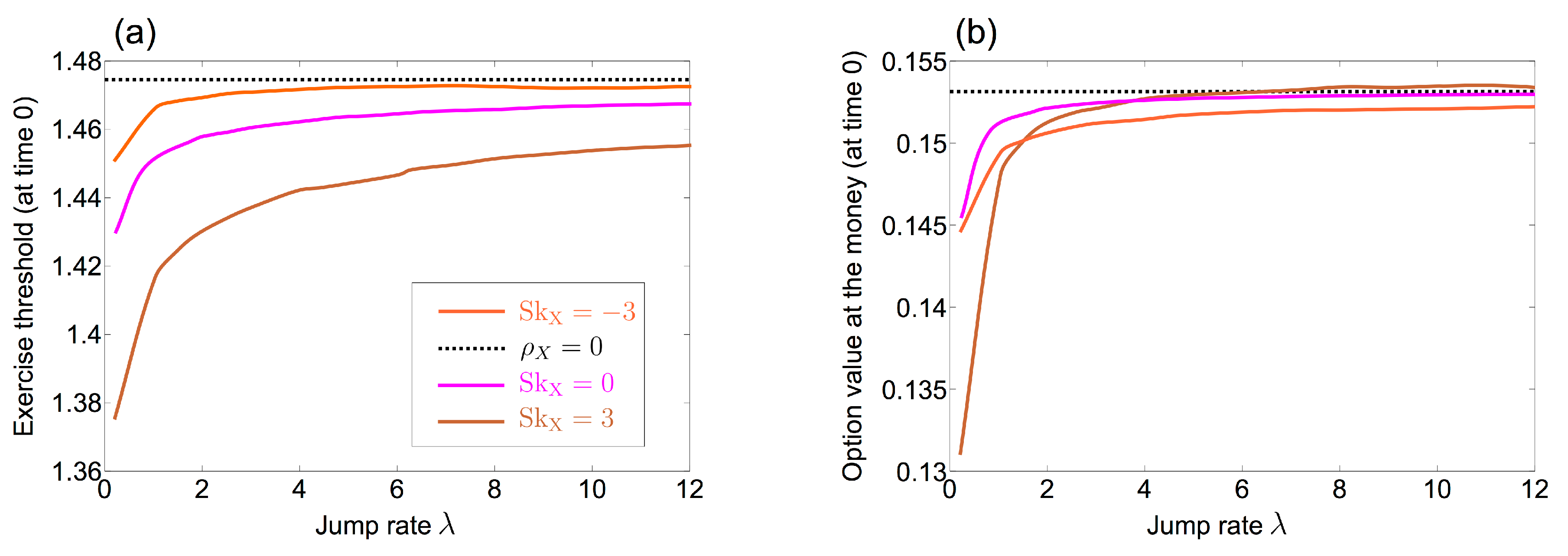

5.3.4. Further Investigation of , ,

In

Figure 7 and

Figure 8, we plot exercise threshold and option value at time

for a range of input parameters. For

Figure 7, we plot the variation of these quantities with jump rate

, for three different values of skewness

. We selected

,

, with all other parameters being equal to their values stated earlier.

The three coloured curves in the figure represent the different skewness levels. Their orderings for low values of

are consistent with the discussion of

Figure 6. Moreover, as observed with respect to

Figure 5, the curves should converge to the black dotted line (representing the case

) when

increases indefinitely. This is apparent in the plots, although there are still discernible discrepancies between the curves even when

, representing 120 expected jumps over the option lifetime.

Another significant observation in the option-value plot is that when

increases, the positive-skewness curve exceeds the zero- and negative-skewness curves and even apparently overshoots the large-

limit. (This observation does not hold for the exercise-threshold plot.) This can be explained in terms of the rapid mitigation of the issue implied in the discussion of

Figure 6, that the project-value jumps had limited downside risk, diminishing the option value. When a large number of jumps occur, then the potential cumulative effect of multiple downward jumps does constitute more significant downside risk when considering the project value. So the option will gain value as a result.

The small-scale fluctuations in the plotted curves are due to calculation noise, in particular, the rounding error associated with forcing the values of

to be multiples of

. This effect has been mitigated by selecting

for

Figure 7, as opposed to the value

used earlier. Also, the effect is only significant for large values of

(for which the jump size, compared to

, is relatively small). The curves have been smoothed, partly through the judicious choices of the discrete jump rates

for which they were calculated. For these reasons, particularly in

Figure 7b, the plotted values have limited reliability for large values of

. Finally, we note that the error is least when

, since in this case the first and third moments of the discrete distribution are guaranteed to be matched to those of the continuous distribution it is approximating (i.e., to zero).

For

Figure 8, we fix the value of

at 0.1 (and set

to 0.00025), and now plot the variation in exercise threshold and option value with skewness

. The trend observed in

Figure 4 is apparent: the plotted quantities decline with increasing

, and this is preserved over all values of skewness. Additionally, as discussed in relation to

Figure 6, the plotted quantities are asymmetric with respect to the sign (positive or negative) of the skewness. In particular, the low option value for large positive values of skewness is due to the fact that jumps are rare. (The expected number of jumps over the option’s lifetime is 1.) The optimum level of skewness, in terms of maximising option value, is negative, and becomes more so as

is increased.

6. Conclusions

In this manuscript, we have incorporated two extensions to the real-options approach of

Grasselli (

2011). In doing so, we have maintained its key characteristics: the finite time horizon; the partial correlation between the project value and tradable instruments; and the utilisation of the investor’s utility function.

In addition, we have incorporated the ability to model the investor’s implied inflation rate, which determines the time dependence of their utility function. This permits us to perform a more realistic model of the investor behaviour over time, specifically, that an investor’s risk preferences will tend to vary with inflation rather than the rate of interest.

Also, we have incorporated a jump-diffusion component into the value of the underlying project for which the option is written. In the most general case, the dominant effects of such a jump component would be the additional drift and volatility it imparted to the project value. Accordingly, we have limited the number of free parameters when defining our jump process, so as to control for these effects. The correction terms in Equation (2) also assist in this aim. As a result, we are able to examine the impact of the particular form of the double-exponential jump distribution, and the dependence of the option value and investor behaviour on the skewness of the jump process.

In the results we presented, the incorporation of a jump-diffusion component into the option price model tended to reduce both the exercise threshold and the option value. An apparent exception to this rule was shown in

Figure 7b, in which it was possible for the plotted option value under the jump process to exceed that in its absence. However, this applied only for extremely high jump rates, and was subject to numerical error.

We have been able to utilise a parsimonious approach for approximating the continuous double-exponential distribution using a discrete distribution, taking only a limited number of values over the binomial tree whose increments are determined by the non-jump components of the process. As such, the additional computational burden of incorporating the jump-diffusion extension is small. Indeed, we found calculation times were generally less than twice those required in the absence of jump diffusion, except for cases of extreme values of the parameters.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}