1. Introduction

Insurance premiums are typically calculated based on the expected loss, with an added loading depending on distributional properties of the risk (the expected value principle, variance principle, utility premium, etc.). An alternative to these static premium principles is to consider the premium as a dynamic control variable of the insurance company, as suggested in

Asmussen et al. (

2013) and

Thøgersen (

2016). In this approach, the individual customer’s problem of deciding whether or not to insure at any given premium offered is modelled explicitly, and the premium is chosen optimally by the insurance company, balancing the resulting portfolio size against revenue per customer in order to minimize ruin probability. The analysis is based on the diffusion approximation to a standard Cramér-Lundberg risk process, extended to allow investment in a risk-free asset. In

Asmussen et al. (

2019), this idea is extended to a situation where insurance companies compete against each other, and Nash equilibria in premium controls of the resulting stochastic differential game are determined under suitable conditions. However, in some cases, no Nash equilibrium exists.

In the present paper, we present a parallel to this analysis dealing with product differentiation, with insurance companies offering different deductibles, and accounting for the possibility of Stackelberg equilibria. Two insurance companies compete against each other such that one company is the leader, choosing its premium first, and the other company is the follower, choosing its premium in response to the leader’s. The setting is slightly modified relative to that in

Asmussen et al. (

2019), in that we do not consider search and switching costs when modelling the customer’s choice between insurance products. Our main contributions are, first, to establish the existence of Stackelberg equilibrium under suitable conditions on this strategic game between insurance companies, and to identify the restrictions under which this reduces to the special case of Nash equilibrium. To our best knowledge, this adds at least the following new features to the literature on game theory in insurance: an example of Stackelberg equilibrium in premium controls; a finding of dependence of optimal premiums on reserves; and an occurrence of the phenomenon of adverse selection in a stochastic differential game between insurance companies, i.e., a lower premium charged increases portfolio size but leaves the average customer riskier to the company.

In the literature following

Taylor (

1986), the individual insurance company is frequently modelled as setting its premium in response to the aggregate insurance market, without explicitly considering the analogous behavior of the other companies constituting this market and the resulting strategic interactions. Examples include

Taylor (

1987) on marginal expense rates,

Emms and Haberman (

2005) generalizing the deterministic discrete-time analysis of Taylor to a stochastic continuous-time model,

Pantelous and Passalidou (

2013,

2015) using stochastic demand functions in discrete time, and

Emms (

2007) and

Emms et al. (

2007), adopting stochastic processes for the market average premium and demand conditions in continuous time.

Pantelous and Passalidou (

2017) recently found the optimal premium to depend on the company’s reserve in a competitive environment in the sense of this literature, but, again, this is not explicitly a game-theoretic equilibrium in the sense of Nash or Stackelberg, which is where we obtain dependence on reserves.

Game-theoretic aspects arise if the other insurers in the market in fact do react to the policy of the individual insurer, with the latter explicitly taking this into account in setting its policy. Market reaction to the individual insurer’s premium is considered by

Emms (

2011). Explicit games between insurance companies have been studied using non-cooperative game theory, where Cournot games involve volume controls, see, e.g.,

Powers et al. (

1998), whereas premium controls correspond to Bertrand games, e.g., the one-period games in

Polborn (

1998) and

Dutang et al. (

2013), who note that one aspect missing in their analysis is adverse selection among policyholders—our analysis includes this.

Emms (

2012) and

Boonen et al. (

2018) do consider continuous-time differential games in premium controls, but again based on

Taylor (

1986) type demand functions of own and market average premium.

Boonen et al. (

2018) in addition present a continuous-time extension of a one-period aggregate game of

Wu and Pantelous (

2017), involving a price elasticity of demand or market power parameter, and the individual insurer’s payoff depending on own premium and an aggregate of market premiums. The models are deterministic and open-loop Nash equilibria are determined. In contrast, rather than assuming demand functions, we model the customer’s choice of where to insure directly and find closed-loop or feedback Nash and Stackelberg equilibria in the resulting continuous-time strategic stochastic differential game between insurance companies. The roles of product differentiation via deductibles, adverse selection, and separating equilibrium in our solution are reminiscent of

Rothschild and Stiglitz (

1976), one of the first applications of game theory to competition in insurance premiums.

Besides competition in premiums, game theory has found several other applications in insurance, starting with

Borch (

1962) on risk transfer.

Zeng (

2010),

Taksar and Zeng (

2011), and

Jin et al. (

2013) consider Nash equilibria of stochastic differential games between insurance companies in reinsurance strategies. The analysis has been extended to non-zero sum games and additional investment controls by

Bensoussan et al. (

2014), nonlinear risk processes by

Meng et al. (

2015), ambiguity-aversion by

Pun and Wong (

2016), and insurance companies with different levels of trust in information by

Yan et al. (

2017). Stackelberg-type equilibria of stochastic differential games have been studied in

Lin et al. (

2012), where an insurance company selects an investment strategy while the market (or nature) selects a worst-case probability scenario, and in

Chen and Shen (

2018), where the game is between insurer and reinsurer, but not as here in a game between insurance companies. For some more remote references, see

Asmussen et al. (

2019). Stackelberg games were introduced by

von Stackelberg (

1934), and the theory of stochastic differential Stackelberg games is considered by

Yong (

2002),

Bensoussan et al. (

2015), and

Shi et al. (

2016).

Premium competition between insurance companies is likely to arise because the premium charged may affect both portfolio size and revenue per customer. Without market frictions or product differentiation, it might be expected that all customers would simply insure at the company offering the lowest premium. However, this may not be the case in the presence of market frictions. Thus, when choosing which insurance company to contact, customers may face different costs of search and switching, transportation, or information acquisition, or they may simply exhibit differences in preferences. Search frictions have been studied in economics by

Diamond (

1982),

Mortensen (

1982),

Mortensen and Pissarides (

1994), and others.

Brown and Goolsbee (

2002) studied the effect of internet search on life insurance premiums in US data. Information frictions have been modelled as differences in the cost of obtaining information, e.g., by

Salop and Stiglitz (

1977). In

Asmussen et al. (

2019) we study premium competition between insurance companies in the presence of market frictions. In the present paper, we consider instead product differentiation, and for simplicity abstract from market frictions. With the leading example of car insurance in mind, product differentiation may come in several forms. Here, we focus on different deductibles. Other possibilities would be bonus-malus systems, see

Denuit et al. (

2007), or proportional compensation in deductibles, similar to reinsurance arrangements, see

Albrecher et al. (

2017).

We consider the case of two insurance companies, referred to as and . We allow for product differentiation by letting offer an insurance contract with fixed deductible for a premium , . The deductible measures the quality of the insurance product, so the company offering the lower deductible will be able to charge a higher premium.

We assume that there is a financial market consisting of a single risk-free asset with dynamics , where r is the risk-free interest rate. All excess wealth of customers and reserve of insurers is invested in this asset. There are N customers in the insurance market. We assume that all customers must insure at either or and focus the analysis on the choice between the two companies. This involves several characteristics of both customer and insurance product. We pay special attention to product differentiation and customer risk.

The characteristics of an individual customer are unknown to the insurance companies, but their probability distribution known. Based on this distribution, the companies can determine the expected portfolio sizes and average claim frequencies in their portfolios as functions of the premiums offered. The gross premium rate of is then , and the aggregate claim frequency is .

Let

be the initial reserve of company

i. For given premiums

, the reserve of

is governed by the dynamics

where

and

are independent Wiener processes, and

The random variable

Z represents claim sizes, assumed to be independent and identically distributed. Thus, (

1) can be considered as a diffusion approximation to the Cramér-Lundberg process extended to the case where the insurance companies have access to investment in a risk-free asset. Such diffusion approximations have been used widely, based on the arguments of

Iglehart (

1969).

The aim is to derive value functions for the insurance companies, and determine game-theoretic equilibria. We consider here what we call push-pull competition. We assume that the largest company in terms of initial capital, , selects its premium to try to push the small company away, while the small company tries to pull closer to the large company. For and the leader choosing its premium first, we derive conditions for a Stackelberg equilibrium. The stronger feature of a Nash equilibrium may also occur, and we give conditions for that, but our numerical examples indicate that Stackelberg is the more typical case. Subsequently, for completeness, we briefly sketch the solution in the opposite case, . The claim frequencies of individual customers are considered random to the insurance company, and we obtain explicit solutions for equilibrium premiums in the case of gamma-distributed claim frequencies.

The structure of the paper is as follows. In

Section 2 we analyze the customer’s problem. We proceed to portfolio characteristics in

Section 3. In

Section 4, we use the portfolio characteristics to find the strategies of

and

. In

Section 5, we obtain explicit solutions in the case of gamma-distributed claim frequencies, and provide numerical examples.

Section 6 concludes. Some calculations and proofs are deferred to

Appendix A.

2. Customer’s Problem

The customer has access to the risk-free asset paying interest at rate

r. This is the customer’s only source of income, and he/she invests all his/her wealth in this. The customer is exposed to a risk

, modelled as a compound Poisson process

, where

is a Poisson process with claim frequency

, and

are the claim sizes, assumed to be independent of

. The customer will then reduce this risk by buying insurance. If the customer insures at

, then he/she will continuously pay the premium

, and in return have the claim sizes reduced to at most

. The wealth of the customer

when insuring at company

i thus has dynamics

where

is the compound Poisson process

, and

the customer’s initial wealth.

We here use similar evaluation criteria and subsequent arguments as in

Thøgersen (

2016), which we refer to for a more exhaustive treatment. The first step is to realize that the expected present discounted wealth when insuring at

can be evaluated as

where

is a subjective discount rate. If the customer were risk-neutral, he/she would simply choose the insurance company generating maximum expected present discounted wealth. Thus, he/she would prefer

over

if

However, an existence criterion for the insurance industry is that customers are risk averse, and this requires modification of (

2). If

, the customer will be facing an excess claim size risk when insuring at the company with the higher deductible. Let this additional (or reduced) risk be denoted

when insuring at

rather than

. Please note that

corresponds to the last factor in (

2), and is positive if

, and vice versa. Let

denote the risk aversion of the customer. By standard arguments of insurance, due to the risk aversion, the customer will be willing to pay a fee to avoid the additional risk. We will take this into account by introducing a personal safety loading

that the customer is willing to pay to avoid the excess risk present when

. This is incorporated in (

2) by multiplying the excess risk by

. The more risk averse the customer, the higher the safety loading, i.e.,

is non-negative and increasing in

, with

. Thus, including risk aversion, the customer will prefer

over

if

and conversely,

over

if

In the next section, we use these relations to evaluate the portfolio sizes and average claim frequencies of the respective companies. We remark, however, at this place that in

Asmussen et al. (

2019) we have presented an in part more sophisticated approach to the customer’s problem involving a finite decision horizon with varying interpretations, but for the sake of simplicity, we have not pursued this aspect here.

4. The Strategies of the insurance Companies—Push and Pull

We now consider the optimization problems of the insurance companies. A control

is a set

of premium strategies where

denote the premiums set by the companies at time

t. As in much of stochastic control theory, we will only consider Markovian (also called feedback) strategies

, meaning that

only depend on the current value

of the difference

between the corresponding controlled reserve processes

. That is, we can write

,

for suitable functions

. Since the (uncontrolled) reserves have the dynamics (

1), this makes

a diffusion process,

where

and

is again a Wiener process. Without loss of generality, we take

, i.e.,

is the large company and

the small. The large company seeks to maximize the reserve difference (to

push the competitor further away), while the small company seeks to minimize the same (to

pull closer to the competitor), each taking the current reserve difference as the state variable. The optimality criterion is to consider a fixed interval

with

and let

Then the large company chooses to maximize the probability to exit at the upper boundary, and the small chooses to minimize , or equivalently to maximize the probability to exit at the lower boundary.

Remark 1. The feedback assumption implies that this is equivalent to maximizing (minimizing) for all .

Given that deductibles are different, one of the firms offers a product of higher quality (lower deductible) than the other. Therefore, the sequence of the game matters, and so a Stackelberg game is considered, where the companies compete sequentially. The sequence of the game is that at any time t

The insurance company with the better product (i.e., lower deductible) is the leader and thus plays first.

The insurance company with the lower quality product is the follower, and plays second, instantly after observing the leader’s choice.

If

(the smallest firm) is the leader and

the follower (i.e.,

), then a Stackelberg equilibrium is defined as a strategy pair

satisfying

where

. This case,

, is relevant when the company offering the lower deductible is not able to attract sufficiently many high-risk customers (who need this extra protection) to become the largest company. We briefly discuss the opposite case below, in Remark 6.

The Stackelberg equilibrium concept involves backward induction. First, the optimal response of the follower is determined as a reaction function. Next, the leader inserts the reaction function of the follower into its optimization problem, and solves for the best first move. As the game evolves in continuous time, the reserve difference changes. At each instant, each firm reconsiders its strategy, taking the running reserve difference as the state variable, and taking into account the future strategies of both companies, as long as the reserve difference remains in

. The criteria for a Stackelberg equilibrium are less strict than the ones for the more common Nash equilibrium, defined as a strategy pair

satisfying

i.e., neither firm has an incentive to deviate from its strategy unilaterally. We later specify the specific (second order) criteria for our solution for both types of equilibrium.

We next quote from

Asmussen et al. (

2019) some results that will allow replacing optimization problems in the space of functions

by the more elementary problem of pointwise maximization/minimization of the real-valued ratio

between the drift and variance of the reserve difference process in (

10).

Lemma 1. Let be bounded and measurable functions on an interval such that and let be defined on a suitable probability space such that W is a standard Brownian motion andfor some . Define further ,and . Then: (i) .

(ii) For a given function κ on and a given , let denote the r.h.s. in (i). Then implies .

By slight abuse of notation, define

To ease notation here and in the following subsections, we use the notation

for partial derivatives, where the number of primes indicates the number of times the function is differentiated, and the subscript specifies with respect to which variable.

1Now consider the resulting drift and variance of the reserves in (1), focusing on the case

. Writing

and

, it follows from (1) and

Section 3 that the drift and variance for the reserve of

can be written as

and for

,

with

y given by (

6). These expressions show that the denominator

in (

15) depends on the controls

because so does

y and

implies

(if

then

reduces to

). Therefore, we need to optimize over the entire

function (

15) and not just the difference in drifts

as in

Asmussen et al. (

2019).

From (

6), by lowering the premium

,

(with a high deductible in their product) can increase

y and thereby portfolio size

, for given

, but at the expense of simultaneously increasing average claim rate

, leaving the combined effect on the drift

in (

1) of sign that may go either way in general. Thus, there is a tradeoff, reflecting the adverse selection problem, cf.

Rothschild and Stiglitz (

1976), i.e., lowering the premium brings more but riskier customers. In contrast, by lowering its premium

for given

,

(offering the lower deductible) can lower

y and thereby simultaneously increase portfolio size

and reduce average claim rate

, but the combined effect on the drift of the reserve difference in (

10) is nevertheless of ambiguous sign, and further modelling indeed required.

By (i) of Lemma 1,

takes the form

, and combination of (ii) of the lemma and Remark 1 allows characterizing a Stackelberg equilibrium with

as the leader and

the follower. It shows that the optimization problem is local: We can just consider maximization or minimization of

separately at each

. This yields Proposition 1 below, in which we find the explicit (local) conditions for a Stackelberg equilibrium in (

11) in terms of the function

from (

15). For a solution to exist, the maximizing company should be facing a (locally, at least) concave problem structure, and the minimizing company a convex one. Existence cannot be guaranteed in general, but needs to be verified when considering a specific distribution of

A, and hence a specific

. For the standard assumption of a gamma-distributed heterogeneity, we see in

Section 5 that an equilibrium does in fact exist and is unique. Although multiple solutions do not occur in this example, they cannot be excluded in general, so that the equilibrium may not be unique. The approach with backward induction should be the same, though giving a set of solutions. As multiple equilibria do not arise in the gamma case, we do not discuss them in more depth, except noting that uniqueness is guaranteed if the (local) concavity and convexity properties exploited in the following proposition extend globally.

For a fixed , write for the optimal premium for given follows a strategy with premium at level .

Proposition 1. In a Stackelberg equilibrium , the optimal set , of premiums at level δ is a solution toThe first order conditions for areand the second order conditions arewhere is the Hessian of . Proof. Condition (

16) follows from the definition of Stackelberg equilibrium, see (

11), and the local character of the problem discussed above. Choosing the best

given

means that

takes

as

, so

satisfies

The problem

is facing is then to minimize

so

is the zero of the function

At a Stackelberg equilibrium we have

. We therefore get

and the second order condition

means

Now (20) implies that the first term in (22) vanishes, and using (20) again, we arrive at (

17). Furthermore, differentiating (20) gives

and thus

in (23) vanishes. So does the second term, by (20), and hence (23) reduces to

where the first equality follows from (24). Combination with (21) produces (

19). □

Corollary 1. If, in addition to (18), the premiums in (16) satisfythen furthermore meets the conditions of a Nash equilibrium. It is clear from Proposition 1 and Corollary 1 that the Stackelberg equilibrium concept is more general than Nash equilibrium. In particular, by (

18) and (25), the diagonal entries of the relevant Hessian are of opposite sign in Nash equilibrium, so (

19) is automatic. Furthermore, since (

18) and (

19) are the general conditions for a (local) saddlepoint of

, any saddlepoint of this function gives rise to a (local) Stackelberg equilibrium. Geometrically, such a saddlepoint need not be parallel to the axes corresponding to the controls (premiums). In case the cross-partial

(equivalently, the policy of

does not depend on that of

at the optimum), then the saddlepoint is parallel to the axes and, indeed, gives rise to a (local) Nash equilibrium. Again, the conditions are only necessary, whereas sufficient conditions would involve global concavity/convexity.

Heuristically, because the premium controls of the companies are equally powerful and act in opposite directions, they should split customers evenly. This is formalized in the next proposition.

Proposition 2. In Stackelberg equilibrium, and share the market equally, i.e., .

Proof. Suppressing

for notational convenience, let

and

denote the numerator and denominator, respectively, of

in (

15). Simple calculations show that the partial derivatives satisfy the relations

with

y from (

6). Following Proposition 1, we find the first order condition for

,

which can be reduced to

From this equation, the optimal response function

is deduced. Similarly, the first order condition for

can be reduced to

Using the relation (26) between the partial derivatives yields

which in combination with (27) yields

. Hence, in Stackelberg equilibrium

y should be the median of

A, and from (

7),

. □

5. Gamma-Distributed Claim Frequencies

For modelling purposes, we assume that the claim frequencies are distributed according to

, with c.d.f.

where

are the Gamma function, and the lower resp. upper incomplete Gamma function. The gamma distribution is standard for modelling unobserved heterogeneity in a Poissonian setting (in insurance, a classical case is credibility theory, see

Bühlmann and Gisler (

2006); in general Bayesian modelling, the gamma has the role of a conjugate prior greatly facilitating calculations, see

Robert (

2007)). However, the outline calculations can easily be paralleled for other distributions, though the amount of analytic details may be considerable.

The portfolio characteristics (

7)–(

9) can then be written explicitly as

if

and

which, as explained in

Section 3, is equivalent to

and

.

Theorem 1. Assume that , and let denote the median of . Then a Stackelberg equilibrium exists atwhereprovidedandwith Remark 2. As we discussed in

Asmussen et al. (

2019), there are arguments that motivate to remove condition (31) of non-negative premiums or to tighten it to premiums never below net levels

. However, since

now depends on

y from (

6) and hence on premiums unlike in the Nash equilibrium occurring there, this route leads to an implicit condition and is not pursued further here. See; however, the discussion following (37) below.

Proof. Using the portfolio characteristics (28) and the notation from the proof of Proposition 2, we can write the numerator of the criterion to be optimized (

15) as

using the relations

and

. Similarly, for the denominator,

The derivatives of the incomplete Gamma functions are

and by the definition (

6) of

y, we have

. Hence,

and

have partial derivatives

confirming (26) in this case. By Proposition 2,

y must be the median of the gamma distribution, namely, the value

that solves

. From the definition (

6) of

y it then follows that

is chosen to satisfy

Thus, when evaluated at

, the optimal response by

is

. We may now evaluate the expressions

Substitute these into (27) and solve for

to get

The second order conditions, (

18) and (

19), are verified in

Appendix A such that the first order conditions yield the types of optima desired.

We have without loss of generality assumed that

, i.e., by (

6),

charges the highest premium. This is reasonable because it offers the best product (

). Indeed, there cannot be an equilibrium in the region

, since here, the criterion to be optimized would be

, which is decreasing in

. Since

seeks to minimize, it would increase

until again

. □

Corollary 2. If, in addition to (32), the premiums in (29) satisfythen furthermore meets the conditions of a Nash equilibrium. Proof. Follows from Corollary 1 and calculations in the

Appendix A. □

Remark 3. The median is not analytically available, but can be solved for numerically.

Banneheka and Ekanayake (

2009) argue that the median for

can be approximated as

. Further to this, note that by scaling properties of the gamma distribution,

is the median of a

distribution. Evidently, equilibrium premiums scale in proportion to

a.

Remark 4. If , the gamma distribution reduces to the exponential with parameter and median . In this case, the expressions for equilibrium premiums simplify to Remark 5. Without product differentiation, , premiums coincide, . With product differentiation, the difference between equilibrium premiums is increasing in excess risk and safety loading .

Remark 6. In case , i.e., the large firm offers the highest-quality insurance product (lowest deductible), then for a gamma-distributed claim frequency, the criterion to be optimized is by symmetry insteadIn this case, will be the leader of the Stackelberg game, and the follower. Recall here that because we have . The same approach as in the proof of Theorem 1 then yields the equilibrium We have again that , (this follows as in the proof of Proposition 2 and as in that case does not depend on the assumption of gamma-distributed heterogeneity). The case is relevant if the company offering best protection (lowest deductible) and therefore charging highest premiums is able to more than cover the extra cost associated with the high-risk customers willing to pay such higher premiums, and thus become the largest company.

Returning to Theorem 1 and the discussion of how the Stackelberg equilibrium evolves over time, note that due to interest rates, the strategy of the leader (here,

, with strategy

) changes in an affine fashion with

. Although

indicates the difference in initial reserves, the companies may reoptimize at any point in time. The game is repeated every instant, and each new equilibrium in the feedback version of the game takes the same form, with premiums set as in Theorem 1, and

the running difference in reserves. As functions of

, the Stackelberg equilibrium premiums,

and

, remain time-invariant. In game-theoretic terms, the equilibrium is time-consistent. Furthermore, the portfolio characteristics actually remain constant through time. The reason is that the difference between premiums,

, clearly is constant over time, not dependent on the reserve difference

, and by

Section 3, portfolio sizes and average claim frequencies for the companies only depend on the difference in premiums.

Numerical Illustration

We have aimed for examples with parameters that are somehow realistic in car insurance, taking the time unit as a year and the monetary unit as one €. For gamma-distributed unobserved heterogeneity there are some studies (see

Bichsel (

1964)) with

b very close to 1, so for the sake of illustration, we take

. Furthermore, an average claim frequency of order 0.05–0.10 is common in Western countries, so we took

. A gamma(0.1,1)-distribution has median

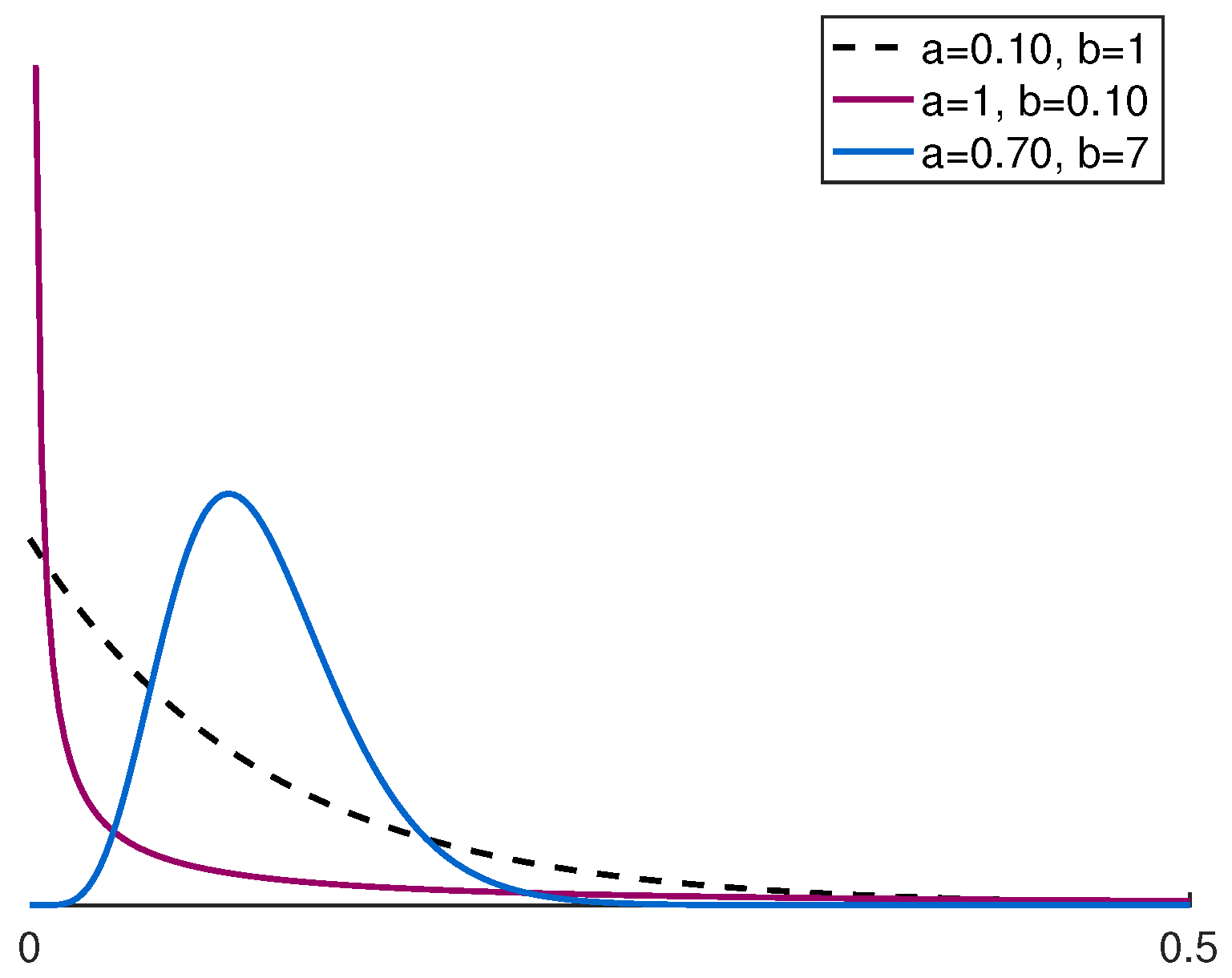

. Examples of gamma-distributed claim frequencies across customers are illustrated in

Figure 1 for different values of the parameters

a and

b. The combinations of parameters are chosen to maintain an average claim frequency of 0.1.

Assuming for simplicity that the claim sizes are exponentially distributed with parameter

, then we additionally have that

for

, together with excess risk

Aiming for an average claim size of 5000 €, we choose

€. We consider a deductible for

of

of the average claim size, that is

. Similarly for

with

of the claim size giving

. Note in particularly that

. For these parameter values, we get

Assume further that there are

customers with identical personal safety loadings of

and that the risk-free interest rate is

. To get an indicator of the level of the reserves, we find a starting point,

R, based on a

Value at Risk (VaR) principle. As

N is rather large, the distribution of the sum

can be approximated by the normal distribution N

. Solving for the

R that satisfies

using the inverse of the N

cdf, yields

. Next,

is assumed to have a reserve somewhat more than

R, and

somewhat less. More specifically, we let

which leads to an initial reserve difference of

. Choosing e.g.,

we get a difference of

. Since the analytic results do not depend on the bounds on the reserve,

and

, their particular values do not matter, and we just need that the interval

contains the chosen

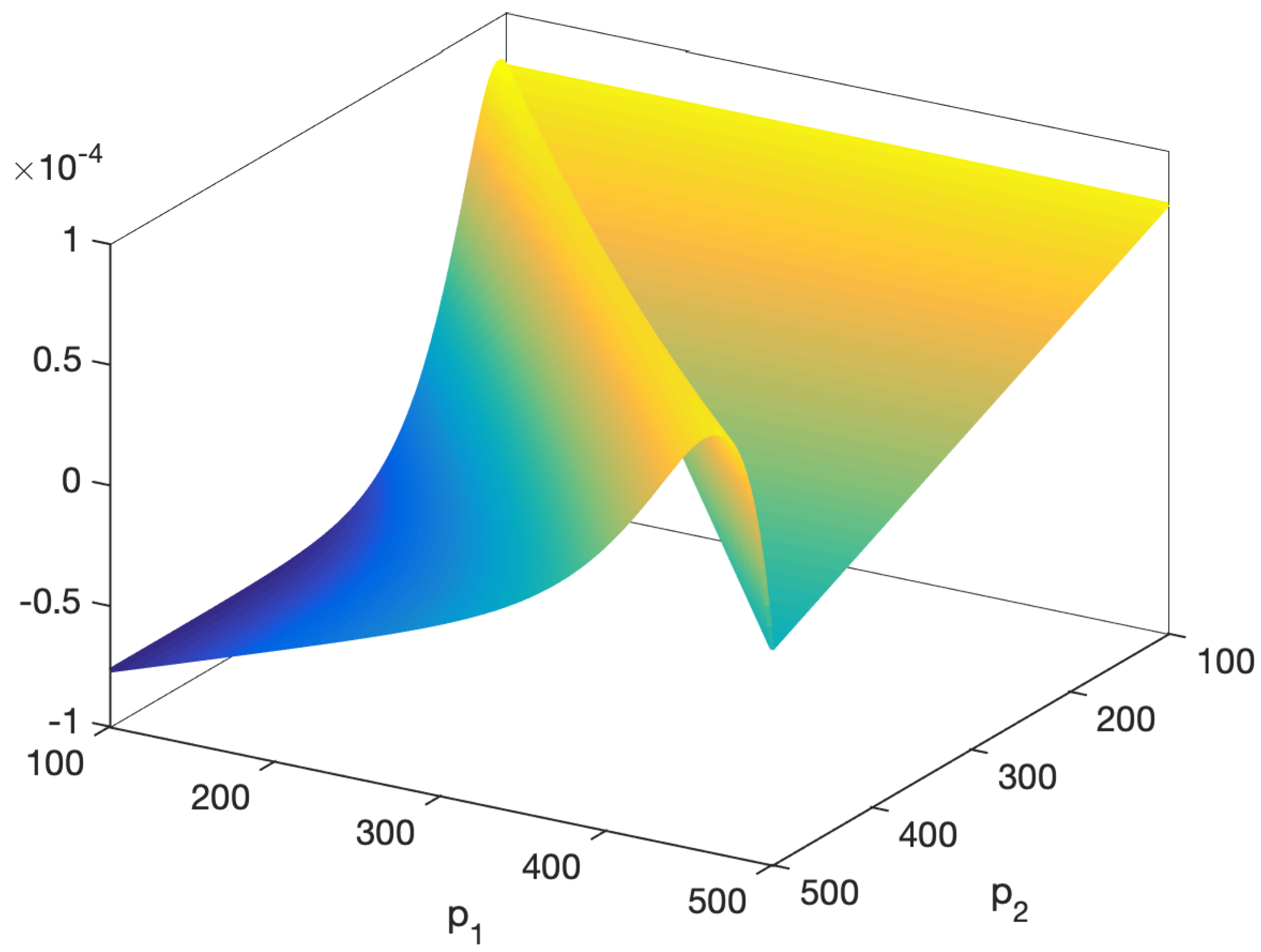

. Given this value, the graph of the criterion to be optimized,

, appears in

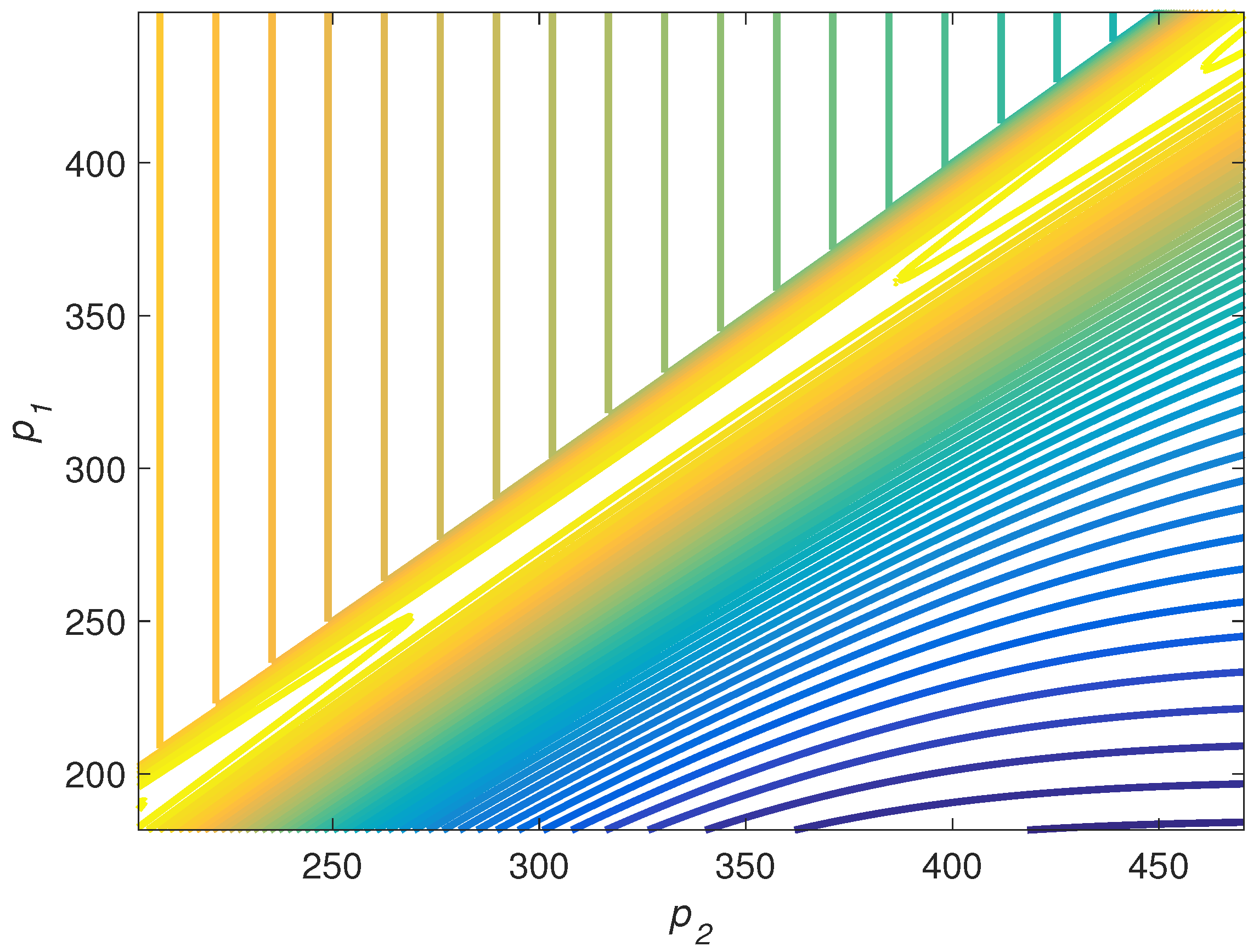

Figure 2, and the corresponding contour diagram in

Figure 3.

Recall that we here consider the case where

offers the better product (

) and chooses its premium

first. Given this,

maximizes by seeking toward the ridge that appears diagonally when choosing

. The market leader,

, takes this response function of

into account, and minimizes

along the ridge, by choice of

. The optimum provides the Stackelberg equilibrium, at the saddle point. However, in this case the saddle is located diagonally, not parallel to the axes, and there is no Nash equilibrium. In particular, given

,

would benefit from increasing

, moving away from the ridge (toward cooler colors in the figures). While this precludes Nash equilibrium, the analysis demonstrates that it is possible to obtain an equilibrium in finite premiums by having

commit to some

at the given

, then letting

respond, i.e., a Stackelberg equilibrium. This is also verified by the value

which tells us that condition (32) is satisfied, whereas (34) is not, as

, i.e., greater than

in this case.

From Theorem 1, we compute the Stackelberg equilibrium premiums

at the current reserve difference

. These are to be compared with the net premiums

so that pursuing solely the competition aspects would lead to a likely loss for

at the current reserve difference. This is not necessarily a paradox since the perspective of control and game theory is to focus solely on a one-eyed goal. Larger

means

is lagging more behind the large firm

, and this gives

greater incentive to compete for customers by lowering its premium, with

responding by letting premiums move in lockstep. Thus, in equilibrium,

always receives a higher premium than

, reflecting the higher quality product (lower deductible). This type of product is attractive to “bad” customers, that is, customers with high claim frequency, as seen in

Figure 4. These customers are expected to experience more losses than “good” customers, and are therefore willing to pay extra for better coverage, yielding a separating equilibrium, with customers’ choices revealing their type, as in

Rothschild and Stiglitz (

1976). Still,

may remain the smallest company, due to the higher risk of its customers.

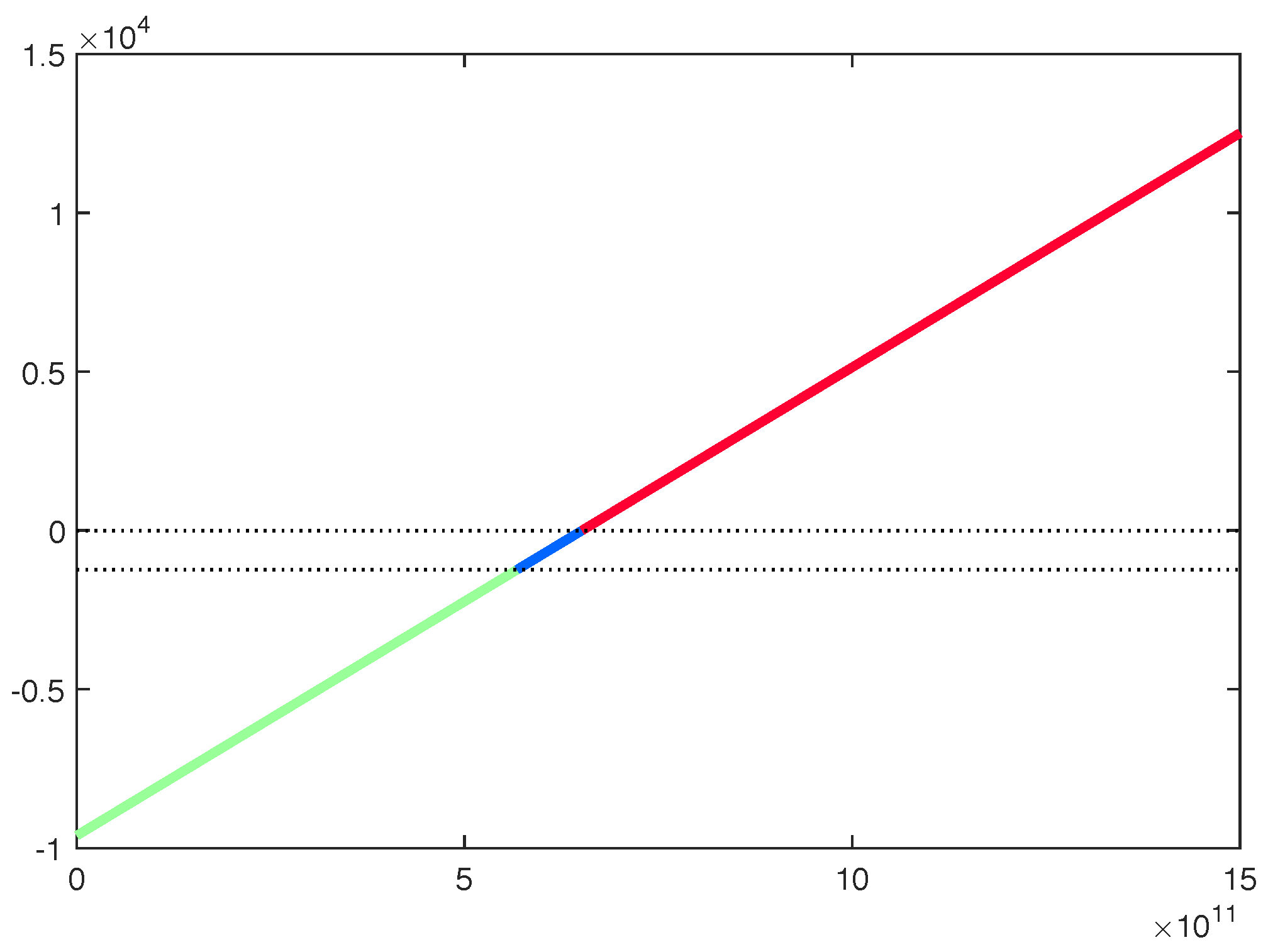

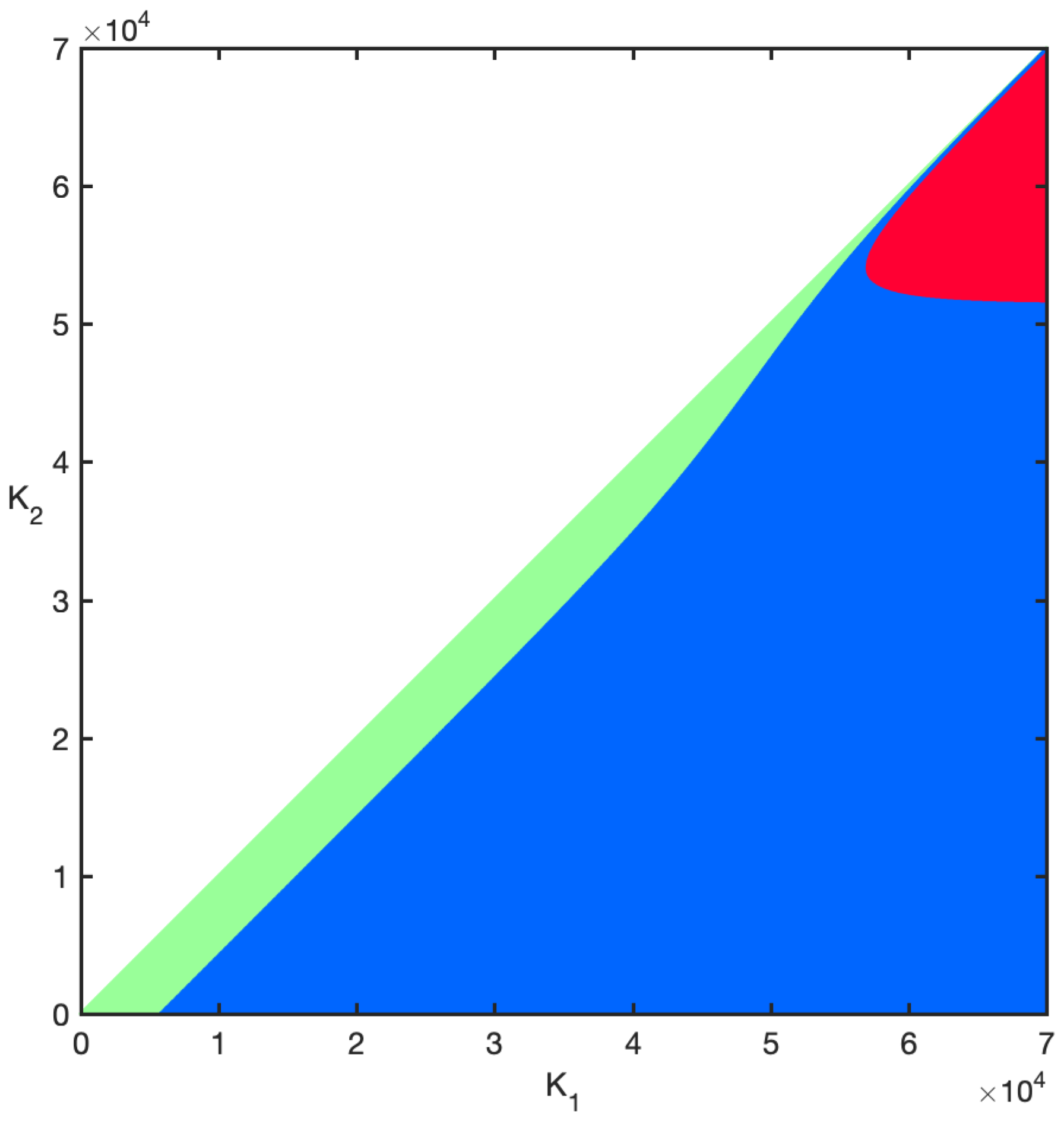

In

Figure 5 and

Figure 6, exhibiting aspects of D, we take a closer graphical look at the second order criteria. Starting with

Figure 5, we plot D as a function of

. All other parameters remain the same as above. Values for

for which

are plotted in green to indicate that the equilibrium is of Stackelberg type. Values that yield

, and hence equilibrium of Nash-type, are plotted in blue. Finally, the values plotted with red give

, which tells us that there is no equilibrium. Here we see that D is indeed a linearly increasing function of

, as it should be according to (30) and (33). Hence, for small

-values we get a Stackelberg equilibrium (green). For a small spectrum in the middle we get a Nash equilibrium (blue), and, finally, for large values of

there is no equilibrium. The same color codes are used in

Figure 6, which shows the color plateaus of

D, and not the actual values, as depending on the deductibles,

and

. As we restrict the analysis to the case where

, it is only the lower triangular part that is illustrated. For simultaneously large values (above

) of

and

, there appears an area (red) where there is no equilibrium. However,

is ten times the average claim size of 5000 and obviously an unrealistically large value of the deductibles. For

and

being close, i.e., along the diagonal, there is then an equilibrium of Stackelberg type (green area) for smaller values. Moving away from the diagonal, the equilibrium type will change from Stackelberg to Nash (blue area). However, in the most realistic region of deductibles

being below the mean claim size

it is always Stackelberg.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}