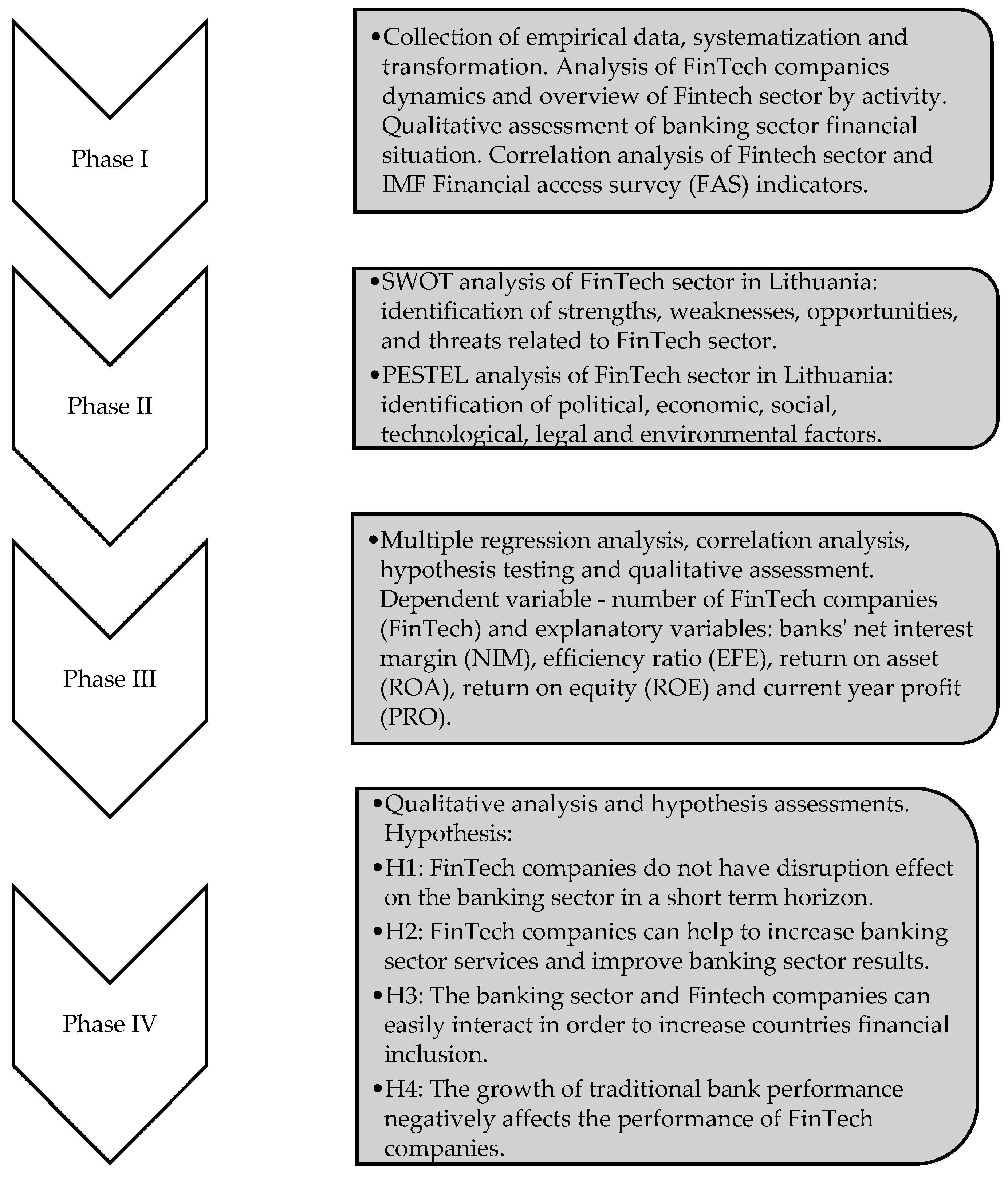

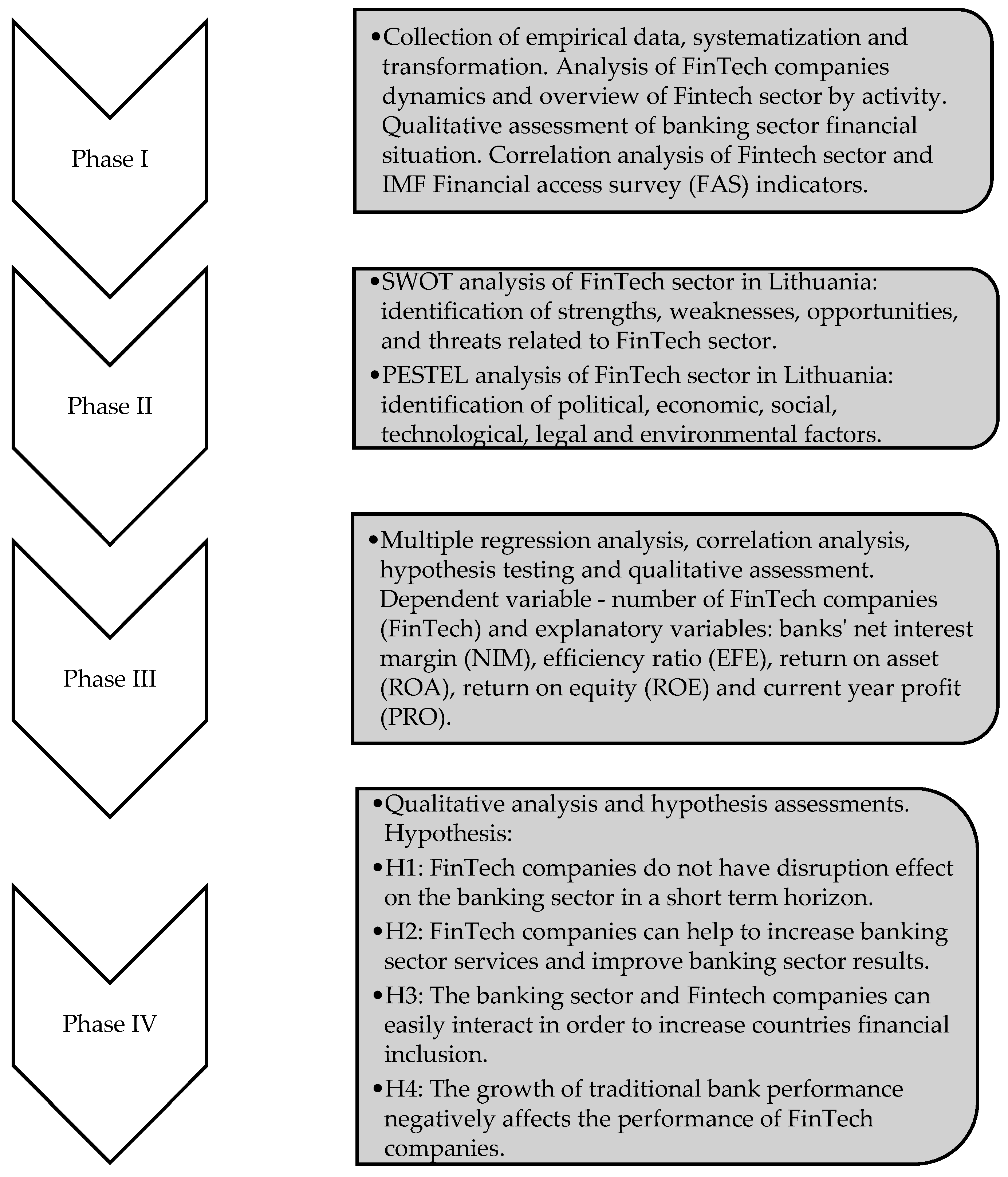

In this part we analyzed tendencies in the financial technology sector and the interaction with the banking sector using correlation and multiple regression analysis. From the qualitative approach side we used SWOT and PESTEL analysis.

4.1. Tendencies in Lithuanian FinTech Sector and Interaction with Banking Sector

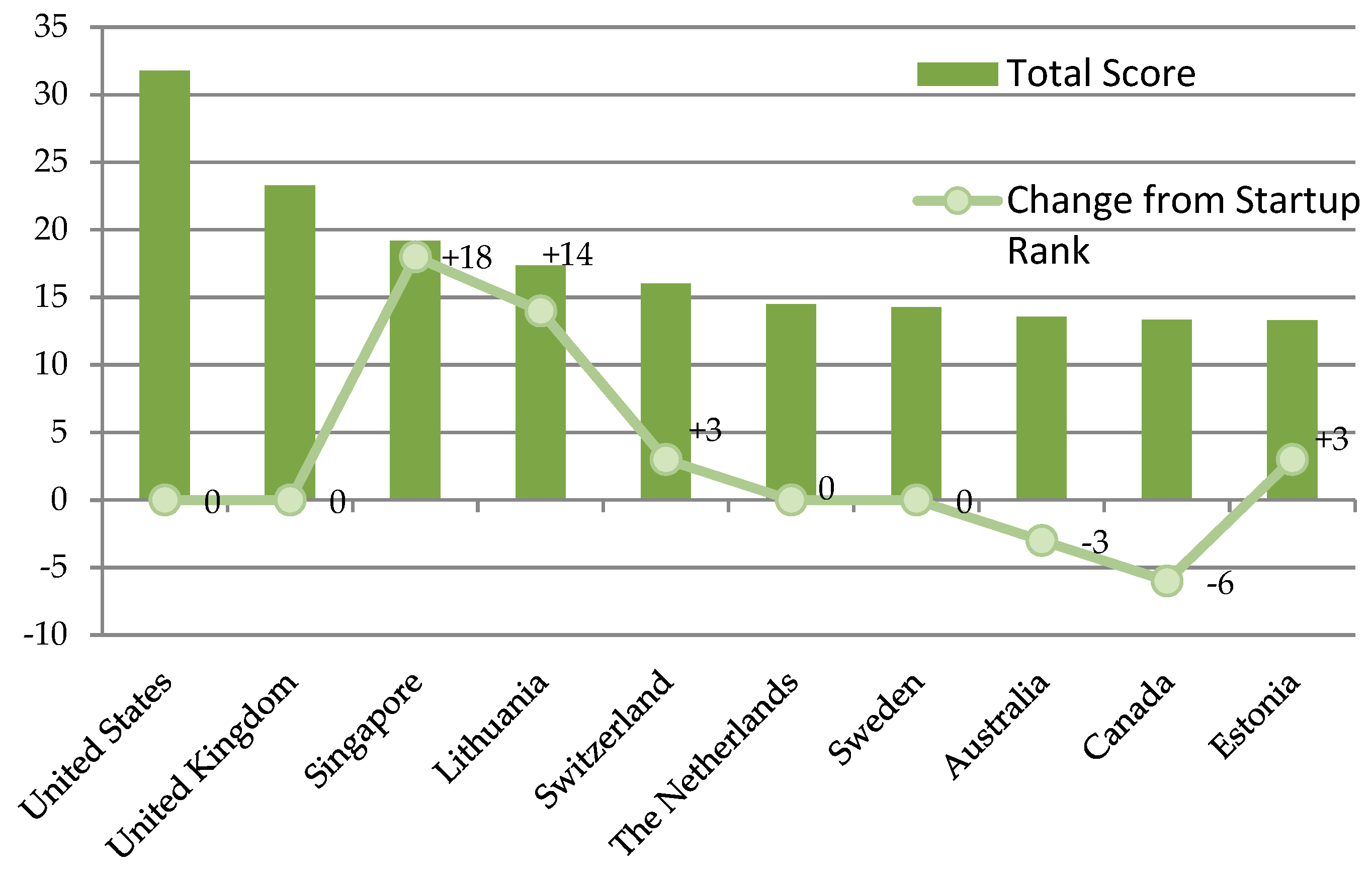

For our case study analysis we chose Lithuania because it is a small country with a high grade of FinTech sector expansion. Lithuania’s position in the Global Fintech Ranking is #4. For such a small country it is a great achievement (

Figure 2).

We would like to stress that lately Lithuania has made a big improvement in FinTech sector having changed its position in the Global FinTech ranking by 14 points.

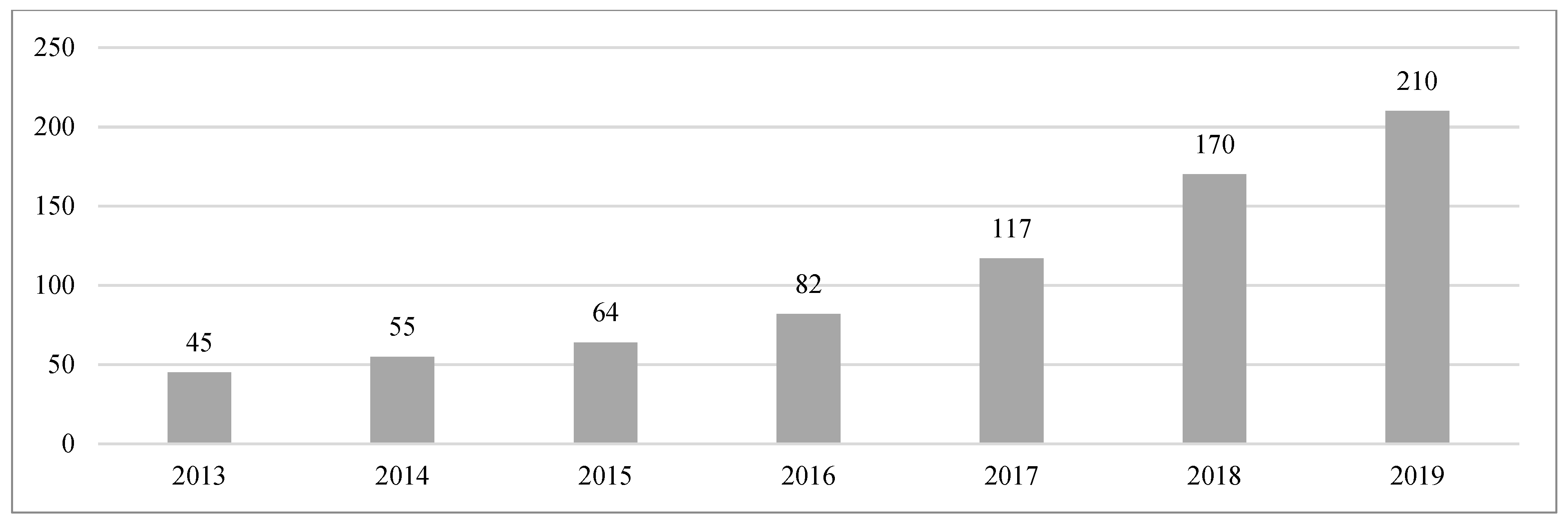

Since 2013 the number of FinTech companies emerging in Lithuania has been increasing. In 2013, the first official number of new FinTech companies was announced. In the same year, it was recorded that 45 financial technology companies were established in Lithuania. In 2014, the number of financial technologies reached only 55, in 2016 there were already 82 companies, and at the end of 2018, there were as many as 170 FinTech companies. On average, the annual percentage change over the whole period was almost 30% (see

Figure 3 for exact numbers of every year) (

Verslo žinios 2019).

According to the

Agency for Science (

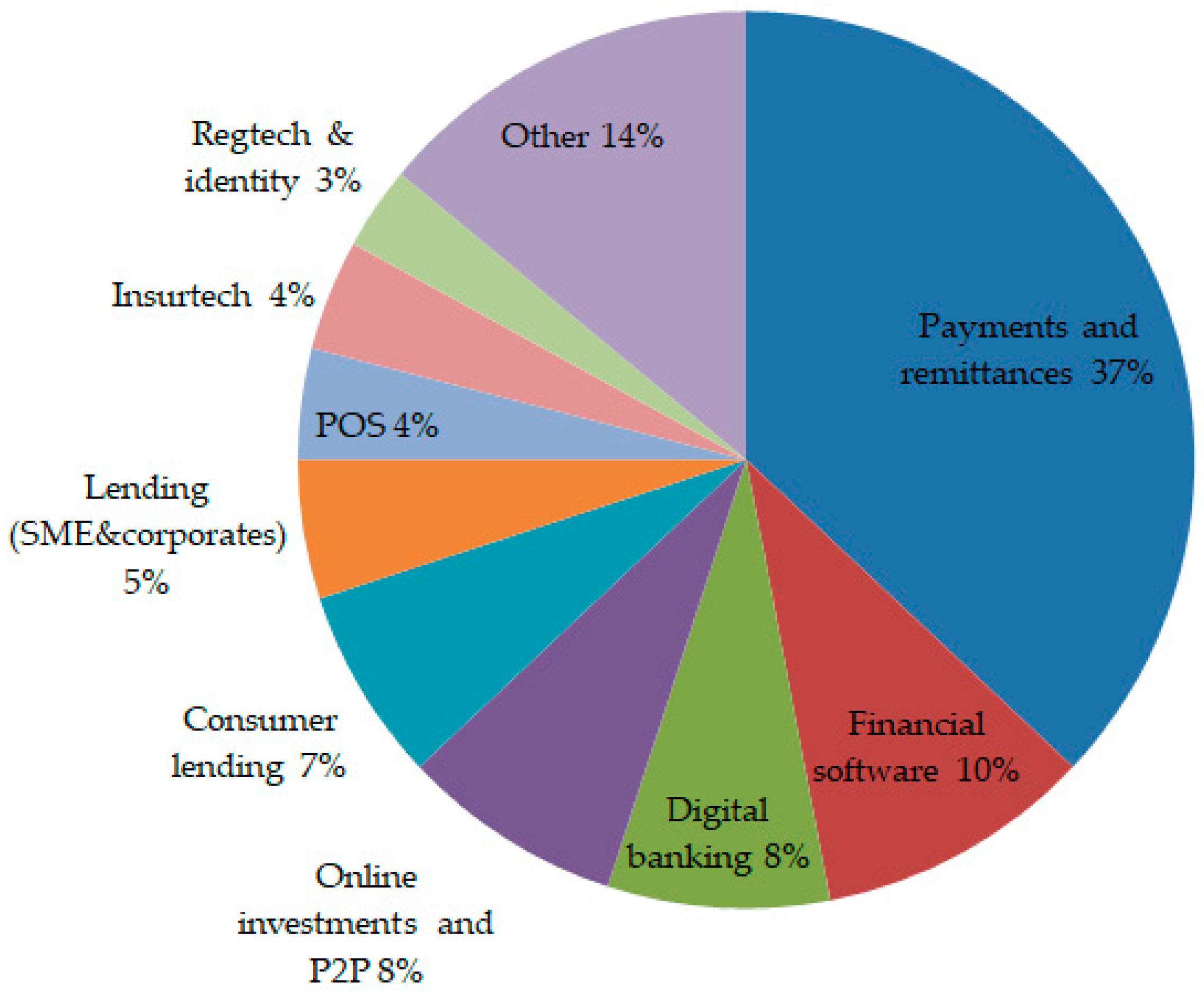

2019), Lithuania is widely recognized as one of the most attractive countries for EU FinTech start-ups, as in 2018 it issued 45 e-money institution licenses, ranking Lithuania second in Europe and second only to the United Kingdom. Number of licensed FinTech companies in Lithuania. Compared to 2017, it increased by 69% (from 87 to 113). According to the investment attractiveness rating (2019), in 2019 Lithuania was ranked 11th out of 190 countries. In 2019, the FinTech sector was also successful, with 210 companies involved in the development of financial technology. Looking at the variety of services Lithuanian FinTech sector is mostly focused on payments and remittances (

Figure 4).

We started the analysis of interaction using the main descriptive statistics parameters (

Table 1).

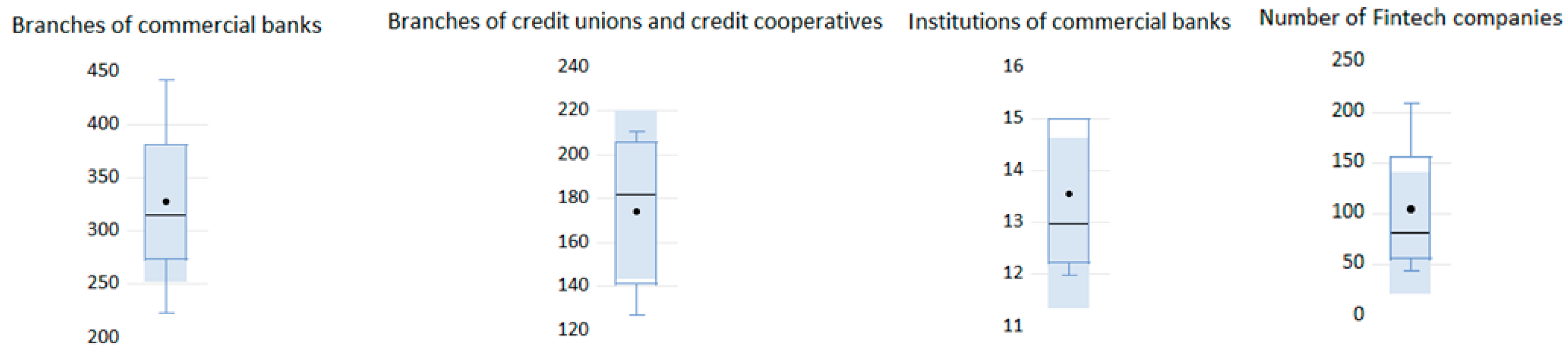

The most intensive growth of Fintech companies was fixed during the period of 2017–2018. It would be interesting to compare those figures with the financial inclusion data. For that reason, we have taken IMF Financial Access Survey (FAS) indicators in order to check if there are any relations between FAS indicators and the growth of FinTech companies.

Looking at the

Table 2 we can see that there was a strong negative correlation between the number of FinTech companies and branches of commercial banks and branches of credit unions and credit cooperatives. It means that the more FinTech companies we had in Lithuania the less branches of commercial banks and credit unions and credit cooperatives we had. From the first glance it could be interpreted that FinTech companies had a negative effect on banks, credit unions and credit cooperatives development but it was not true. Lots of banking and credit union services were becoming online, so people were encouraged to use the Internet instead of going to the physical branches. Banks were also seeking to optimize their activity by giving the priority to online banking so there was no need for so many branches. The latter fact is the explanation for why the number of branches of commercial banks, branches of credit unions and credit cooperatives was decreasing.

The same situation occurred between automated teller machines and the number of FinTech companies. However, the most interesting thing was that the correlation between institutions of commercial banks and FinTech companies was very low. Knowing the specifics of the Lithuanian banking sector and the fact that commercial banks try to reach higher efficiency by trying to focus clients on internet services, the decreasing tendency of ATM and branches had nothing in common with FinTech sector expansion. We would like to point the fact that statistical numbers must be explained using qualitative explanations as well.

The tendencies of FAS indicators in the period of 2013–2019 can be seen in

Figure 5.

By comparing some points of commissions of banking and FinTech services (

Table 3) we would like to pay attention to two aspects. Firstly, we agree that some banking services which were provided by FinTech companies were much cheaper, but this fact did not indicate that all bank clients would start using FinTech companies’ services. We must consider the whole package of services because it was much more convenient to have the biggest part of financial services at one provider. So having that in mind, we would like to point that FinTech companies could create competition but did not have enough power to take the biggest majority of clients from banking sector.

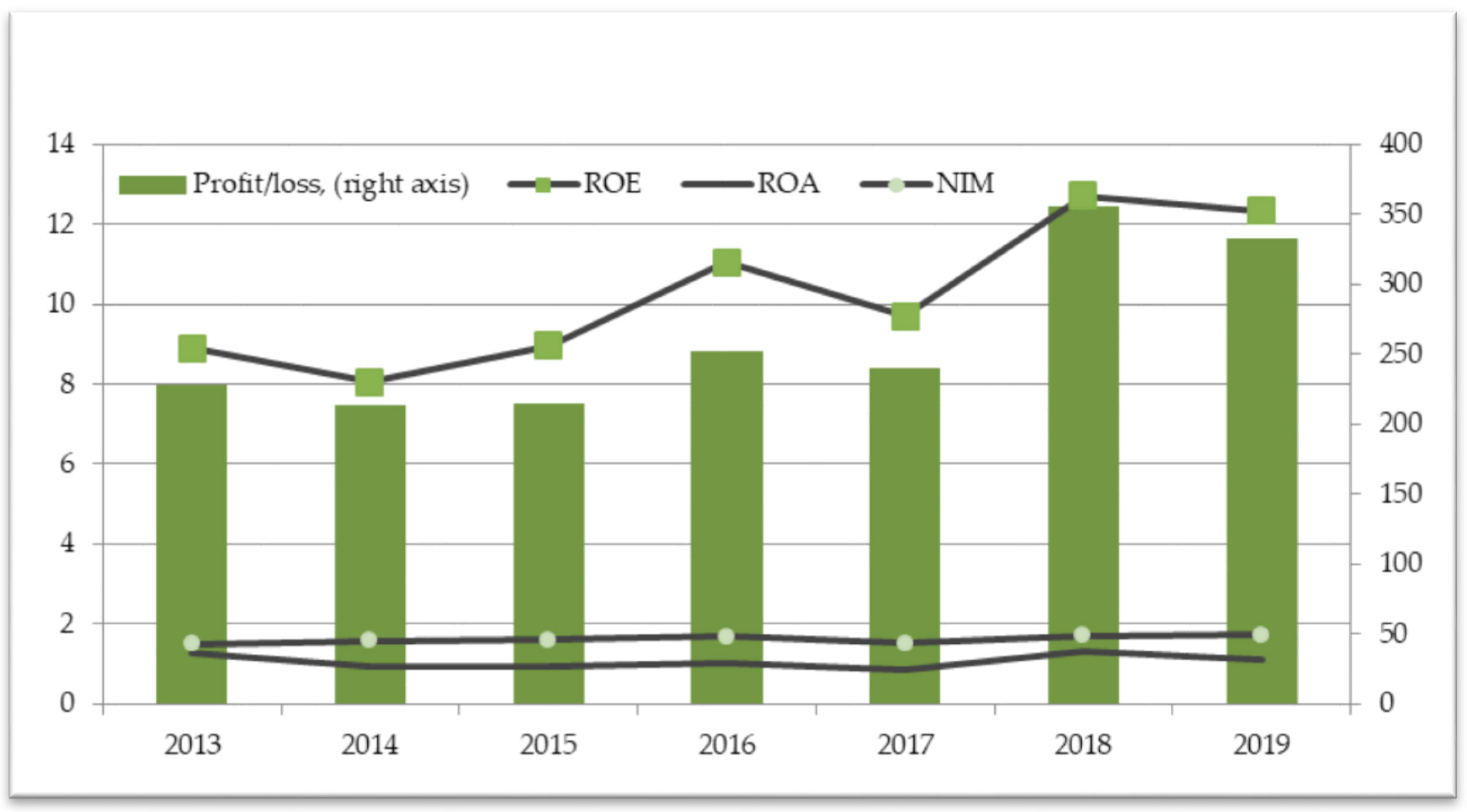

In order to analyze the interaction between FinTech companies and banking sector we had to research the main tendencies of financial activity of Lithuanian banking sector in the period of 2013–2019 (

Figure 6).

In the period of 2013–2019 we can see that the profit of Lithuanian banking sector was quite volatile while the intensity of FinTech growth was increasing in every year (

Table 4).

After the analysis of banking sector activity we noticed that in the period when the growth of Fintech companies was at the highest level banking sector demonstrated the highest profit and great profitability ratios (

Table 5). So, we would like to support the hypothesis H1 that FinTech companies did not have a disruption effect on the banking sector in a short-term horizon.

Net interest margin in banking sector of Lithuania (

Table 6) increased almost every year which means that commercial banks had lots of opportunities to earn more because they had a good monetary policy transmission channel and a cheap source of money.

We can point that the efficiency ratio of Lithuanian banking sector (

Table 7) was one of the highest in Europe but analyzing 2013–2019 period we saw a decreasing trend.

The influence of the banking sector on FinTech companies in recent times has indeed been the subject of interest of many scholars and entrepreneurs. Researchers from other countries are conducting research to find out what the future holds for these two similar service providers. A study by

Phan et al. (

2019) on the impact of the FinTech sector on the banking sector in Indonesia revealed that “FinTech has a negative impact on banking operations and is likely to push traditional banks out of the peak of popularity in the future”. However, we do not want to support those findings in Lithuania as we saw a different situation in a short-term horizon. Taking into account all those statistical data, correlations and financial ratio analysis we would like to conclude and support our hypothesis H2 that FinTech companies can help to increase banking sector services and improve banking sector results. We think that bigger competition in financial sector forces banks to take more efficient decisions and take actions in order to attract more clients and to reach higher quality of their services.

All in all we support our hypothesis H3 that the banking sector and FinTech companies can easily interact in order to increase countries financial inclusion. Bank of Lithuania, as a central bank, supports not only FinTech sector but also creates opportunities for new commercial banks to start their activity in the country. So by increasing competition in the financial market we can achieve higher results of financial inclusion in the country.

Taking into account everything what has been mentioned we reject the hypothesis H4 that the growth of traditional bank performance negatively affects the performance of FinTech companies.

4.2. SWOT and PESTEL Analysis of FinTech Sector

FinTech valuation issues are very relevant nowadays because this sector is evolving at a rapid speed and making strong influence on finance sector, economy and our lives. First of all it is essential to be more familiar with FinTech business model in order to understand possible impact on the banking sector. The author

Roberto Moro Visconti (

2020) in his article about FinTech valuation issues paid a lot of attention to SWOT and PESTLE analysis. Another author

Stephan Hoppe (

2018) in his book “The Rise of FinTech. Threats and Opportunities for the German Retail Banking Market” presented SWOT analysis as a suitable tool for FinTech sector.

Citta et al. (

2018) in their research used SWOT analysis for FinTech companies in Indonesia as well. In practice PESTLE analysis is often considered together with SWOT analysis in order to identify and properly values the ecosystem of FinTech sector. So, we chose that methodological approach to analyze the FinTech sector in Lithuania.

In order to better understand the FinTech sector and its impact on the banking sector, it is appropriate to conduct a SWOT analysis of the financial technology industry, which will reveal FinTech’s strengths, weaknesses, opportunities and threats (

Table 8). The scientific literature presents a number of strengths, weaknesses, opportunities and threats in the financial technology industry, the most important of which are listed in the table below.

As many as six strengths were singled out in the FinTech sector. According to

Acar and Citak (

2019), compared to traditional financial institutions, financial technology start-ups provided better quality services because they focused on a narrower range of services. Such companies tended to operate at a lower price than traditional financial institutions, so they could offer a higher quality of the services provided to customers at a relatively low price.

The availability of services, according to

Nicoletti (

2017), allowed consumers to increase efficiency, modernize financial infrastructure, enable more effective risk management, and expand access to financial services in a variety of areas, including lending, payments, personal finance, remittances, and home insurance.

Financial technologies facilitated and simplified complex processes such as the provision of finance.

Romānova and Kudinska (

2016), write that FinTech allows lending even remotely without causing physical inconvenience to conventional banking institutions and their protracted processes.

The next strength was openness and transparency. According to

Zavolokina et al. (

2016), this industry demonstrates significantly more openness and transparency in its transactions in the financial sector, thus gaining customer confidence, entering the market, and becoming a full part of it.

As FinTech has become increasingly popular, profitable and interesting sector, its benefits have been seen not only by customers and investors, but also by national governments (

Philippon 2016). In order to boost economic growth, countries need to invest in promising innovations, and one of them is certainly financial technology. Therefore, national governments are encouraging the development of FinTech, while also seeing the potential to boost the country’s economic growth.

The financial technology sector, with its many strengths, also had its weaknesses. The first weakness was the regulatory rigor;

Anagnastopoulos (

2018) writes that regulation of the FinTech sector is very strict, and over time, it becomes even stricter. This attitude of regulators was caused, among other things, by the global financial crisis of 2008, when trust, which was a bridge between people and financial service providers, collapsed.

These days, the focus is also on the privacy of personal information that users provide online. With the entry into force of the Data Protection Act, great importance is attached to the protection of the data of customers, employees and other related persons. The risk of fraud or financial risk associated with users who do not fully understand new financial products is also considered a weakness in financial technology. Ensuring data privacy and mitigating risks in the sector, according to

McKinsey and Co (

2016), are very relevant areas of activity in the FinTech sector and are among the weaknesses of this sector, as a lot of resources are needed to mitigate these risks.

FinTech is considered to be an infinitely promising industry with many opportunities, including the exploitation of the blockchain concept. This means that with the development of innovative and technology-based financial services, great potential is visible for the use of blockchains.

CB Insights (

2019) presented 55 major industries that could be heavily influenced and fundamentally changed by blockchain adaptation, including not only banking but also the country’s infrastructure, communications, medicine, education, and more.

The FinTech industry makes a significant contribution to facilitating access for natural persons to official financial systems such as stock exchanges, derivatives markets and other financial instruments markets.

The next opportunity was risk reduction (

Shao et al. 2020). FinTech could offer risk mitigation solutions to key risk anxiety factors, such as the Know Your Customer (KYC) policy, or eliminate the need for the banking sector altogether. FinTech companies have developed a lot of various solutions for regulatory aspects, especially the security issues. So, those solutions can help to easy the use of KYC policy not only for FinTech companies but also for banking sector as well. With the help of technologies, nowadays we have a rapid growth of electronic and mobile KYC. FinTech companies can help to create more automated KYC policy. There is no need for everyone to have internal methods of KYC policy because it can be outsourced to KYC providers. We think that FinTech companies can play here a key role and provide banks KYC policy services.

Falling prices for online services and increasing mobile and smartphone penetration in small and developing countries also provide an excellent opportunity to use FinTech to promote financial inclusion among the approximately two billion people who do not have access to official financial services (

Scott et al. 2017).

The banking sector is very deeply rooted, and 10 years ago it seemed that it would not face any competition until the wave of popularity of financial technology came and now every traditional financial institution is struggling with start-ups for a place in the financial services market. However, FinTech and the traditional banking sector do not always need to compete, they can also complement each other and learn from each other by forming new partnerships to deliver financial services efficiently, a study by

Accenture (

2015) has shown.

The last opportunity is an attractive labor market. New solutions create the need for new competences, especially in traditional banking. This opens opportunities for FinTech industry professionals—the development of services increases the need for compliance, regulatory and financial policy experts, and the growing popularity of mobile wallets will open the door for many start-ups and IT companies for programmers and mobile application developers, UX/UI designers, and big data analysts.

Although there are fewer threats than opportunities, they should not be questioned. One of the most frequently mentioned threats in the scientific literature is cybercrime: hacking or data protection inadequacies, which can severely damage the integrity of the entire financial system (

Arner et al. 2015). This is perhaps the main reason why some central banks are reluctant to cooperate with financial technologies. Many small and developing countries lack the capacity and infrastructure to ensure cybersecurity. There are also concerns that many start-ups are too focused on the rapid delivery of their product, without paying due attention to security measures.

The next threat is unfavorable regulation. Since, according to

Anagnastopoulos (

2018), financial technology is a relatively new thing, regulatory work is ongoing to this day. Regulation varies from country to country, taking into account different risks, data provision and other important aspects. However, in developing countries, where the regulatory framework for FinTech is still being developed, there is a significant risk that regulation may be very unfavorable to entrepreneurs, which will prevent them from competing with traditional financial institutions.

Abuse of financial technologies is also not new. In the absence of proper regulation, readily available financing can lead to risky behaviors such as over-borrowing and high accumulation of personal debt. There are also some legitimate concerns about market competition. Several new entrants can quickly expand and have a huge monopoly power. On the other hand, too many market participants providing similar services may also distort the market and make supervision more difficult.

The last threat was ageing population. Today’s financial technology companies target a young, well-off person. However, this generation will also age over time and it is difficult to predict how well it will be prepared to continue to adopt all the innovations that are being developed.

PESTEL analysis provides an overview of external factors affecting the FinTech sector in Lithuania by analysing them according to political, economic, social, technical, legal factors.

Political factors:

Favorable conditions for development in Lithuania are created for FinTech start-ups, which the

Bank of Lithuania (

2020) provides on its website: “Development of a regulatory and supervisory ecosystem favorable to FinTech’s activities and promotion of innovations in the financial system is one of the strategic directions of the Bank of Lithuania. Together with other state institutions, the Bank of Lithuania seeks to create such a FinTech environment that would attract new companies and encourage them to develop new products in Lithuania.”

Privacy and security issues arising from technological development.

Degerli (

2019) writes that in the financial sector, cyber-attacks are 300 times more common than in any other industry. This threat brings about new political changes that may lead to changes in regulation in the future and, more precisely, to tighten up regulation;

The financial technology industry successfully meets the needs of customers, which has a positive impact on the public recognition of FinTech, which is conducive to the country’s image in the political arena (

Ministry of Finance website news,

2020);

According to

Invest in Lithuania (

2019), Lithuania is friendly to the FinTech sector in terms of regulation, infrastructure, innovation opportunities, state support and general support.

Economic factors:

Very large sums are invested in the FinTech sector and more and more contracts are made every year (

Schueffel 2016);

Local financial services can become global financial services due to government subsidies due to their positive impact on the country’s economy (

Ministry of Finance 2020);

In cases where banks sometimes lack funds, FinTech companies are investing in new financial services that are replacing the current payroll system;

Due to industrial fragmentation, banks’ profit margins are declining (

Phan et al. 2019);

At present, the greater share of the profits earned by banks is made up of profits from operations. Blockchain is a system that can automatically make it safer and cheaper. Banks will lose huge profits when this online system becomes global and up and starts operating. This does not have a particular impact on the asset management industry, but has a huge impact on banks in general.

Social factors:

As a result of mergers and acquisitions (M&A) transactions, which, according to

Phan et al. 2019, have recently increased between banks and FinTech companies, the cultures of start-ups and prosperous companies often do not coincide;

Customer confidence in traditional institutions is declining due to: high prices, slowness, lack of transparency, lack of good user experience (UX/UI), lack of convenient mobile apps, poor customer service and credit crunch (

Anand and Mantrala 2019);

As other apps, which are not necessarily financial technology apps, are better tailored to consumers, customer expectations create a need for innovative products and services in the financial world;

The society has more confidence in FinTech companies than traditional institutions for better quality of service, service diversity and easy access (

Thakor 2019).

Technological factors:

Due to large direct investments in research and development, significant changes are taking place in industry (

Invest in Lithuania 2019);

Difficulties arise in trying to protect intellectual property through the technological development of companies;

Technological development is faster than consumer access to technological solutions;

User interfaces are still overused based on the needs of companies rather than the needs of customers;

Smartphone apps are changing the way customers use banking services;

Increasing competition and technological progress encourage traditional financial institutions to improve their systems (

Anagnastopoulos 2018);

The current range of financial services is mainly related to: payments, micro/P2P/P2B lending, crowdfunding, crowd investing, online commerce and personal finance management (

Invest in Lithuania 2019).

Environmental factors:

Legal factors:

Local policy does not allow the quick and easy acquisition of licenses for start-ups (

Bank of Lithuania 2020);

Patents and invention licenses facilitate the functioning of slow market entities;

To ensure the security of personal information and money, consumers need specific safety rules for financial services;

Trends in the digitalization of industry require advanced authentication and secure access tools and the adaptation of biometric data (

Invest in Lithuania 2019).

The results of SWOT and PESTEL analyses have shown that the FinTech sector in Lithuania is just beginning to show its potential, which means that a lot of capital is being invested in this industry and a huge growth is expected. Lately we could see a rapid growth in FinTech sector and we hope it will continue.

4.3. Multiple Regression Analysis and Qualitative Assessment

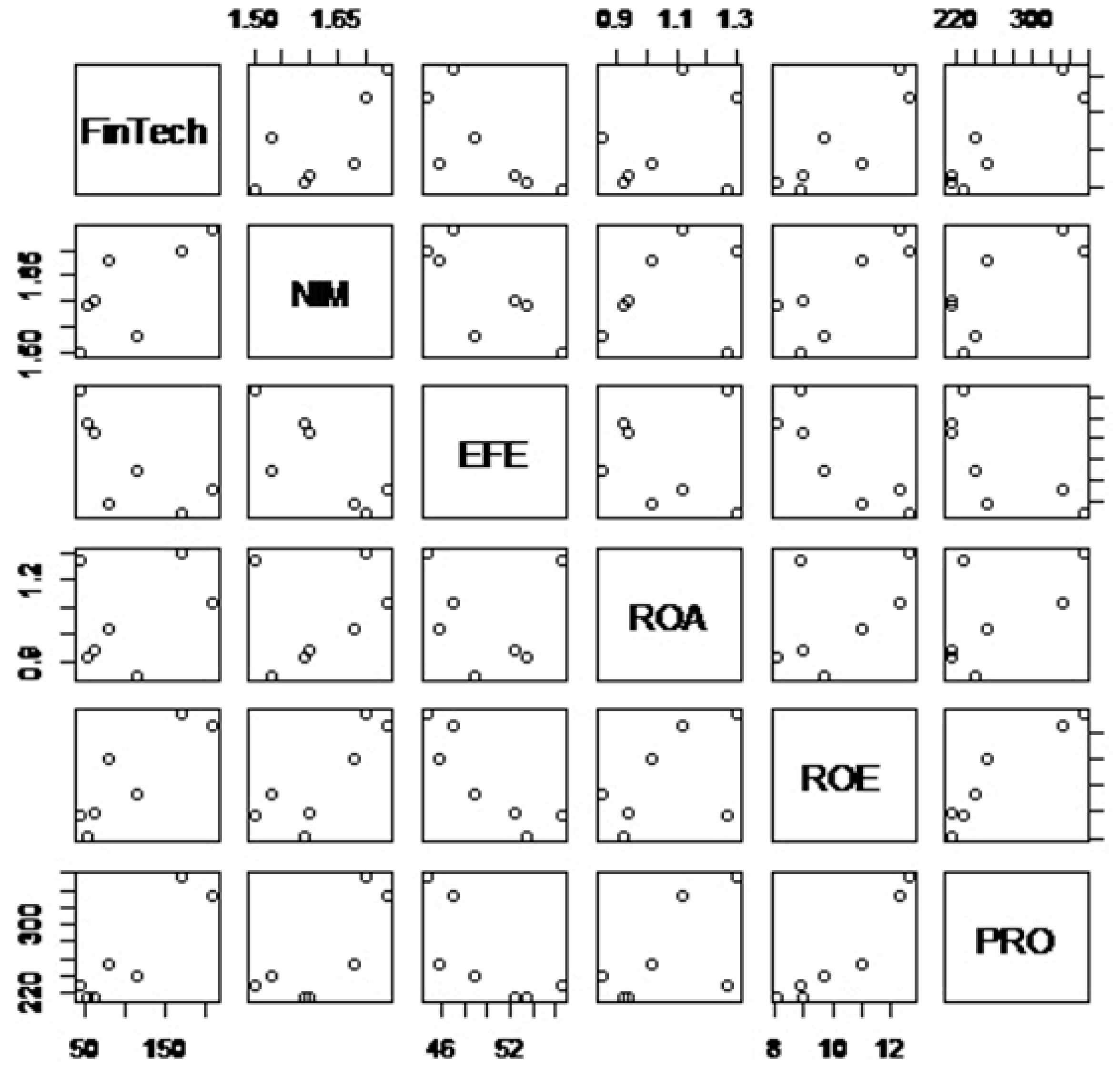

In order to clarify the relationship between the number of Lithuanian FinTech companies and the banking sector in the country, a multiple regression analysis was carried out. The following indicators were selected for the study: the dependent variable—number of FinTech companies (FinTech) and explanatory variables—banks’ net interest margin (NIM), efficiency ratio (EFE), return on assets (ROA), return on equity (ROE) and current year profit (PRO). It was investigated how the explanatory variables NIM, EFE, ROA, ROE, and PRO make way for the dependent variable FinTech.

First of all we did Spearman’s rank correlation because of short time series (

Table 9 and

Table 10).

Table 9 shows that correlation between variables is quite high in almost all cases. The biggest correlation we have noticed between number of Fintech companies and banking sector ROE. It is very interesting to point that the correlation is positive and it means that there is a strong positive relation but of course we cannot say anything about causality.

We checked the hypothesis for every variable: —correlation coefficient is equal to zero. According to test results we have that with the level of significance α = 0.05, the is rejected only in case of ROA, but in other cases we support .

All the results of dispersion of our variables can be seen in

Figure 7.

In the next step we made a regression analysis. Firstly, we would like to stress, that in a regression analysis we used quite a small number of observations, because of public data about FinTech companies’ limitations. Our limited regression analysis results should be interpreted together with SWOT and PESTEL analysis and other qualitative practical assessment.

Starting our quite limited regression analysis, firstly, we checked the null hypothesis about linearity of regression. The

p value 0.04418 was less then α = 0.05 so we reject the hypothesis that regression was not linear. Because our data set was very small we used adjusted coefficient of determination which was equal to 0.9852. The latter results indicated that 98.5% of data dispersion could be explained by linear regression. Regression analysis showed that standard regression error was 7.642 (

Table 11).

Before creating multiple linear regression we determined the dependent variable (number of FinTech companies) and checked if the data were stationary. For that purpose we used unit root test: Augmented Dickey–Fuller (ADF) test and tested for unit root in level. Null hypothesis for that test was: the FinTech dependent variable has a unit root. The results of the test are shown in the table below (

Table 12).

The results of ADF test showed that FinTech companies’ data were non-stationary so we tried the same test for the 1st difference. The results are defined in

Table 13.

Table 13 results showed that 1st difference data of FinTech companies were stationary.

At that step of our research, we got multiple linear regression:

From Formula (1) we can see that variables EFE and NIM had a negative effect on the expansion of FinTech sector while ROE and PRO had a positive effect. From the other side we had to pay attention that some variables had interconnection. Because of our small data set we had to refuse to use one independent variable. We selected ROE and refused to include ROA in multiple linear regression.

We also checked the significance of every parameter. Results are placed in

Table 14.

From the results in

Table 14 we see that all parameters of our model were not statistically significant. Because of that we created a new regression model and used just two variables which had the lowest p-value during our first try. Those variables were (PRO) and (NIM). The results of new regression are placed in

Table 15.

The obtained p-value wasless than the significance level α = 0.05 and equal to 0.003007, therefore the hypothesis about the nonlinearity of the regression was rejected. The coefficient of adjusted determination is 0.965278, which means that 96.53% of the dispersion could be explained by linear regression. Multiple regression analysis showed that the standard regression error was 3.33.

It can be seen from

Table 16 above that with a significance level of α = 0.05, all model parameters were statistically significant. Regression equation:

Looking just at the quantitative assessment from this regression analysis it can be concluded that a profitable activity of banks had a positive effect on FinTech companies and changes in banking sector net interest margin have negative effect. Valuing that using qualitative assessment we could point that profitable activity of banking sector attracted more FinTech companies to enter the financial sector and to provide services similar to banking sector ones.

As our data set was quite small, we would like not to focus on quantitative analysis a lot but pay more attention to qualitative assessment and broad tendencies. We understand that most new companies of FinTech are focused not to lending but to payment systems so the factor of NIM is not so important for them. We also think that tendencies in banking sector do not have strong effect on FinTech companies’ development and growth. From qualitative analysis we have noticed that regulatory environment is among the most important issues for FinTech companies. So for further research, we would like to go into more details trying to identify how big the impact of regulatory institutions on FinTech development is.

For further research we would recommend to repeat this research after some time having larger sample of observations in order to get more accurate results of regression analysis and it would be interesting to value the impact of COVID-19 pandemic on the interaction between banking sector and financial technology companies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}