1. Introduction

Two key innovations, brought by the Solvency II directive in insurance, are the introduction of the market consistent framework for the valuation of assets and liabilities and the definition of risk-based principles for the assessment of the Capital Requirement. In this context, the quantification of losses on an annual time horizon at a given confidence level is a crucial element in determining the requirement. Each company must decide whether to adopt the standard approach or to use its own (partial or full) internal model, which has to be approved by the local supervisory authority. Furthermore, several sources of risk are involved in the valuation process; measuring the dependence between them is also a crucial point.

In this framework, we focus on demographic profit and we provide a stochastic model to quantify the capital requirement for both mortality and longevity risk. In the literature, several papers have dealt with this topic. In particular,

Olivieri and Pitacco (

2008) design a framework for a market-consistent analysis of the life-annuity portfolio. The authors link the traditional approach to a risk-neutral valuation assessing the cost of capital for longevity risk and measuring the amount of target capital for mortality and longevity risk.

Hari et al. (

2008) analyse the relevance of longevity risk for the solvency position of annuity portfolios distinguishing between micro and macro-longevity risks.

Stevens et al. (

2010) quantify the value of annuity liabilities and of the related longevity risk capital requirement by applying the classical Lee–Carter model to estimate the uncertainty of future survival probabilities.

Bauer and Ha (

2015) propose an approach for the calculation of the required risk capital based on least-squares regression and Monte Carlo simulations.

Savelli and Clemente (

2013) provide an approach based on risk theory to evaluate the capital requirement for mortality and longevity risk in a local accounting framework.

Boonen (

2017) examines the consequences for a life insurance company of a calibration of longevity and financial risks by using the expected shortfall instead of value-at-risk. Furthermore, the notion of market-consistent valuation of insurance liabilities has been investigated recently by several authors (

Pelsser and Stadje 2014;

Dhaene et al. 2017) and the analyses have also been extended to a dynamic multi-period setting (

Barigou et al. 2019).

Dahl (

2004) model mortality intensity as a stochastic process and quantify mortality risk by capturing the importance of time dependency and uncertainty. This paper contributes to the existing literature, proposing a different approach for modelling the capital requirement for mortality and longevity risk. We adapt the well-known gain and loss decomposition (

Bacinello 1986) to a Solvency II framework, providing a closed formula for the random variable demographic profit and loss of a life insurance company. We show that this general formula holds for different non-participating life insurance contracts and we analytically split it into several elements in order to emphasize the main key drivers. To the best of our knowledge, a closed formula is not already available in the literature in a market-consistent framework. Additionally, it is noteworthy that, although our aim is not to forecast future mortality rates, the proposed approach is also consistent with the application of mortality models.

In particular, we assume a portfolio of non-participating life insurance policies composed by several cohorts of contracts, where in each cohort all the policyholders have the same characteristics (e.g., age, gender etc.) and the only element of distinction is represented by the sums insured. Hence, policyholders in the same cohort are assumed to be independent and identically distributed (i.i.d.), with the exception of the insured sums. It is noteworthy that the aggregation between different cohorts is not considered here as well as the possible presence of derivative contracts. Therefore, further research will concern the aggregation of several cohorts and portfolios composed of different contracts in order to catch the effects of both dependencies and natural hedging (see, e.g.,

Cox and Lin 2007).

Through this model, we prove the analytical decomposition of the expected demographic profit/loss, highlighting main drivers. Additionally, we assess the distribution via Monte Carlo simulations and we identify a Solvency Capital Requirement compliant with Solvency II. Furthermore, we assure that the model accurately reflects different sources of profit as requested by the requirements set by the Solvency II Directive (

European Parliament and Council 2015, art. 123). In addition, a numerical section is presented to apply the proposed approach to alternative life insurance policies; here, we focus on the risk identified in

Shen and Sherris (

2018) as idiosyncratic risk.

The remainder of this paper is organized as follows.

Section 2 exploits the traditional Homans formula, based on local Generally Accepted Accounting Principles (GAAP), adapting it to a market consistent context.

Section 3 focuses on the random variable demographic profit, also providing a decomposition of this random variable useful for profit and loss composition.

Section 4 presents the algebra underlying the model and the proof of a recursive formula that supports the results.

Section 5 presents some simplified examples to emphasize the main key drivers. In

Section 6, we assess our proposal by developing detailed case studies based on a real portfolio composed by different non-participating life insurance contracts. In particular, the main results confirm the effectiveness of the model in measuring the capital requirement and assessing the different components that affect the demographic results. In

Section 7, we propose the conclusions of our paper.

2. Technical Profit and Gain/Loss Decomposition in a Solvency II Framework

In this section, we provide a formula for the random variable (r.v.) technical profit of a life insurance company. In particular, we define it in a market consistent framework according to the definition of technical liabilities given by the Solvency II regulation. Furthermore, we prove that a gain and loss decomposition is possible in order to emphasize the main profit components. The decomposition is developed in a similar fashion to the well-known decomposition provided by Homans (

Bacinello 1986;

Savelli and Clemente 2013) in a local accounting framework.

First of all we specify that, consistent with the provisions of Solvency II (

European Parliament and Council 2015,

2021), our purpose is to evaluate the capital requirement on an annual time horizon, therefore the stochastic variables will be those evaluated in

since the valuation instant coincides with

t.

The random variable technical profit

is defined as the difference of two terms. The first one is the sum of the complete technical provisions

,

2 and the gross earned premiums

, net of expenses

and surrenders

accumulated at the actual financial return rate

3. The second term in Equation (

1) is the sum of total claim costs

and the complete technical provisions stored at the end of the year

. It is noteworthy that we consider with the r.v.

different non-participating life insurance policies (i.e., as specified later, this r.v. could be equal to zero or to the total lump sums paid in the case of death or survival according to the kind of benefit covered by the insurance policy).

With the introduction of the Solvency II framework (

European Parliament and Council 2021), the previous formula has to be adapted to consider the market consistent valuation of assets and liabilities. Referring only to non-hedgeable liabilities, these are calculated as the sum of Best Estimate and Risk Margin (see Art. 77 of Directive 2009/138/EC). Hence, we can rewrite Equation (

1) as:

It should be pointed out that the Risk Margin is not considered since the purpose of this model is to identify a Solvency Capital Requirement consistent with the legislation and, therefore, with the Delegated Acts. Indeed, Delegated Regulation (

European Parliament and Council 2015) assumes that the worst case scenario does not change the amount of Risk Margin included in the technical provisions. Therefore, the inclusion of this aforementioned component in Equation (

2) when the formula is used for risk capital purposes is not in line with the constraints introduced by the regulation and could inappropriately affect the comparison with the standard formula requirement. Similarly to the well-known results regarding the decomposition of the classical Homans formula, we prove in the

Appendix A the five components of the technical profit formula in a stochastic context. Our main interest is to focus on the first and the second components, respectively the demographic and financial profit and loss. Using rate-based expressions

4 instead of amounts (therefore switching from uppercase letters to lowercase ones), we can define the demographic profit (loss) as:

where

is the rate of best estimate based on the risk-free curve available at time

t and realistic demographic assumptions

at time

t,

is the premium rate,

,

and

are expense loading coefficients for acquisition, management and collection costs, respectively. The term

is the difference between the amount of the sums insured

in time

t and surrenders

;

is the first order financial rate (i.e., the technical rate assumed in the premium assessment). Similarly the reserve at the end of the year is computed as the product of sums insured

and the best estimate rate

based on financial

and demographic

assumptions in force at time

. It is noteworthy that Equation (

3) also allows to analyse the effects of a possible change in the demographic technical base in

. From a qualitative point of view, demographic risk is defined as the possibility of suffering losses because of a variation in the effective mortality of the cohort of policyholders. Since we deal with policyholders that have the same characteristics within the same cohort, we assume that the probabilities of death of the entities are the same and the demographic evolution of the single policyholder is independent from the others (i.e., policyholders are i.i.d.). The only difference between them is represented by the insured sum. We point out that, although a change in value of risk-free rates is considered in the evaluation of capital requirement related to interest risk, a model oriented to highlight the valuation concerning the bridge between the Local GAAP Technical Provisions and the market consistent valuation of Solvency II Best Estimate, must consider the effect of risk-free rates component. The best estimates involved in the valuation (see Equation (

3)) depend on risk-free rates. Additionally, considering

, it is possible to find a capital requirement framework in line with the proposal made in the Quantitative Impact Study n.2, carried out in may 2006 for the preparation of final SCR standard formula, where a closed notation was provided for both mortality and longevity risk.

A peculiar mention must be given also to another profit component, the so-called financial profit, which is necessary to explain some key aspects of the model. It is defined as follows:

where

is the r.v. that describes the rate of return of invested assets and

is a specific penalization coefficient applied in case of surrender (see

Appendix A for details on the formula). As expected, the sign of this component depends on the relation between the effective investment rate and the technical rate guaranteed to the policyholders. For the sake of brevity, the other profit components are reported in

Appendix A, in particular that for expenses, for lapses and a residual margin. As proved, the sum of these five components gives back the whole technical profit (see Equation (

2)).

3. The Demographic Profit and Its Factorisation

Given the gain and loss decomposition provided in the previous section, we now focus only on the demographic component (see Equation (

3)). Indeed, modelling this random variable, we are able to assess the capital requirement for mortality or longevity risk. After some simple manipulations, it is possible to rewrite Equation (

3) as follows:

where

is the complete sum-at-risk rate at time

and

is the first-order annual death probability,

is the complete reserve rate based on a first order basis. The sum-at-risk are here defined “complete” since complete reserve rate is considered (i.e., including expenses reserves); they can be negative, as in pure endowment and annuities cases. This formula is based on the following relation that describes the evolution of the sums insured over time:

where

is the amount of sums insured eliminated in case of death.

5 In Equation (

5), we assume that the best estimates in

t and in

are calculated on the same realistic demographic assumptions. Therefore, we simplify the notation using

q instead of

and

. Since the assessment is carried out on a one-year time span, it makes sense to consider that, within such a short period of time, the insurer does not change its demographic expectations. However, it is possible to evaluate the additional effect on the demographic profit of a one-year change of the second-order demographic assumptions.

6It is worth pointing out that the first term in Equation (

5), here denoted as

:

represents the demographic profit in a local accounting framework (

Savelli and Clemente 2013).

Additionally, it is interesting to separately highlight the effects of risk-free rates volatility and demographic trends. In this regard, we provide the following decomposition:

where

is the demographic profit given by the differences between the first order financial rate

and the risk-free rate curve. The term

instead measures the demographic profit originated by the differences between first-order and second-order death probabilities (

and

q, respectively). To provide this decomposition and to define the second and the third term in Equation (

8), we denote with

the expected present value of future cash-flows evaluated at time

t and compute by using first-order discount rates

and second-order death probabilities

q. In other words, this amount differs from

only in terms of discounting factors.

It is easy to show that

is defined as:

and the third component in Equation (

8) is:

It is interesting to note that is strictly related to the difference between the best estimate and the expected present value of future cash-flows . In particular, we have a positive value if this difference, accumulated at the technical rate , is greater than the analogous difference computed at time . It must be noted that the difference only depends on the difference between the risk-free rates at time t and the technical rate . For instance, a sudden and substantial change in value of the risk-free curve entails a jump in greater than the jump in t.

We also recall that we are focusing here only on the demographic profit. Hence, the whole effect of the risk-free rate curve on the technical profit can be assessed by also considering the financial profit. However, this point goes beyond the scope of the paper that is to quantify the capital requirement for mortality or longevity risk.

The term

depends instead on the difference between the expected present value

and the technical provisions defined according to local accounting rules. Both values are computed with the same discounting rate

, but using a different life table (second-order and first-order, respectively). It must be pointed out that the sign of

is mainly related to the comparison between the term

, accumulated at the technical rate

, and the same difference evaluated at time

. We have indeed that the last term in Equation (

10) usually has a very low weight and hence a low effect on the sign of

.

Now, we focus on the expected demographic profit (i.e.,

) and we prove (see

Section 4) that when

, we have:

since

This result shows that in case the second-order life table chosen by the insurance company is stable in the period

, the sign of the average demographic profit depends mainly on the differences between the risk-free curve and first-order financial rate. In particular, by Equation (

9), we can also rewrite the mean as (when

):

On the basis of Equation (

13), it easy to show that (see

Section 4):

if, at time

t, the one-year spot rate is equal to

.

It is worth pointing out that, at the inception of the contract (i.e., when

), by Equation (

13) the expected value of the demographic profit also depends on the differences between first-order and second-order life tables.

5. The Profit Formation

We focus in this section on the expected demographic profit considering two non-participating life insurance contracts: a pure endowment and a term insurance. We consider these two policies because their combination allows us to obtain other traditional policies issued in the insurance market. As is well-known, an Endowment contract coincides with the sum of a Pure Endowment

7 and a Term Insurance

8 with the same maturity and same sums insured, and an Annuity can be defined as the sum of several Pure Endowments with different maturities and a Term Insurance with variable insured sums is a slight adjustment of the classical Term Insurance. Hence, previous formulas can be used as a basis for evaluating the different kinds of contracts previously mentioned.

We consider a cohort of policyholders, whose main characteristics are summarized in

Table 1. We start from a simplified application that allows us to provide additional insights. In particular, for the sake of simplicity, we assume a flat risk free-rates constant over time and we neglect the effect of expenses. Additionally, we are assuming that the risk-free rates are equal to the technical rate

guaranteed to the policyholder. We have instead that the insurance company priced contracts assuming first-order death probabilities

equal to

of the death probabilities given by the ISTAT2016 population life table. In this first analysis, we assume that the observed mortality follows rates given by the ISTAT2016 population life table. In other words, a prudential pricing has been applied by the insurance company and, hence, a demographic profit is expected. In this regard, we compare in

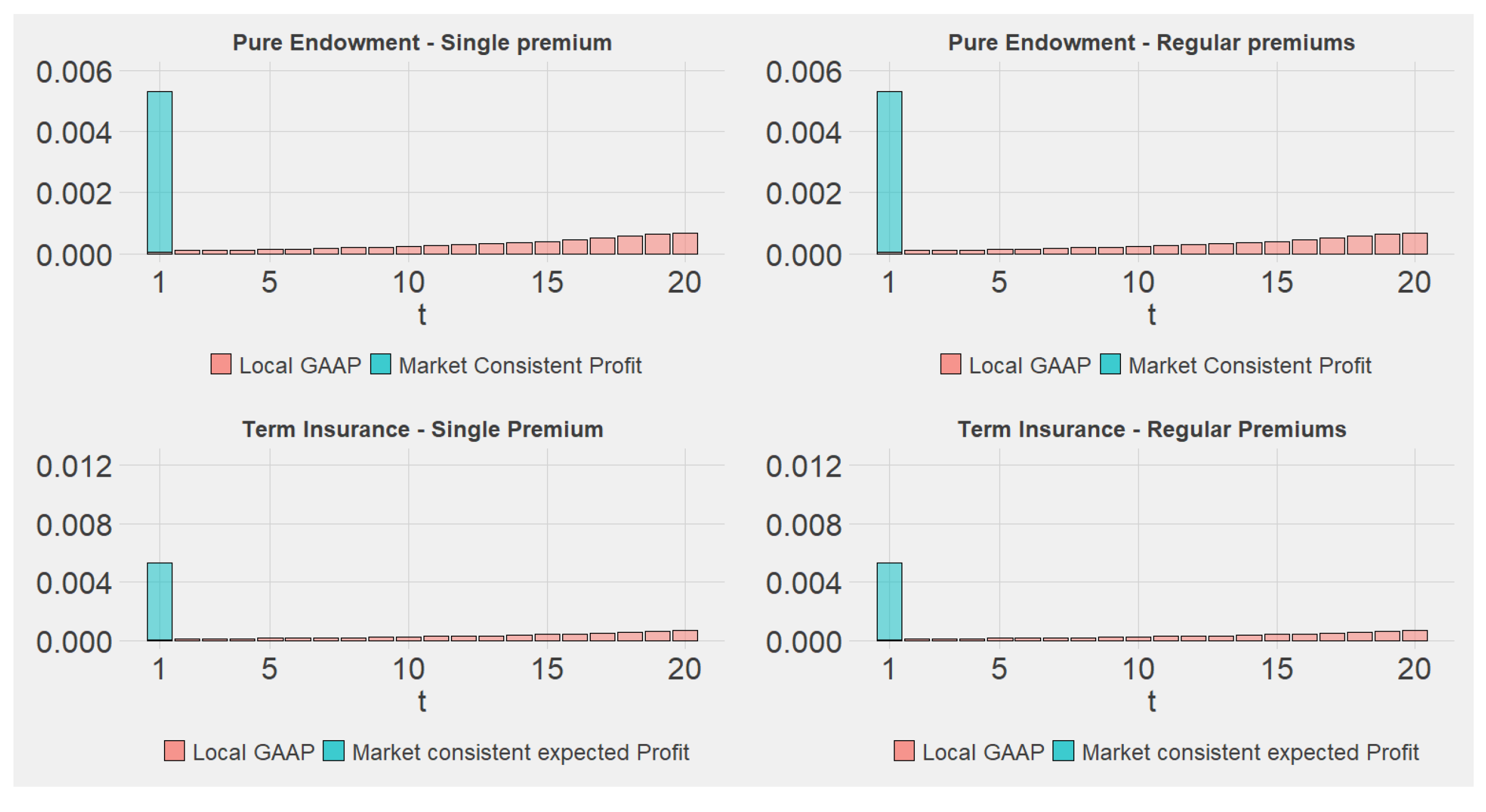

Figure 1 how the profit is released over time in either a market-consistent or a local accounting framework.

We emphasize that the stochastic evolution of the cohort implies deviations from 0 of the r.v. demographic profit. The comparison shows how these fluctuations impact differently in a Local GAAP context and in a market consistent context (see Theorem 2). In a local accounting framework (i.e., see

, Equation (

7)), the expected profit varies over time, depending on the trend of the sum-at-risk, the implicit safety loading and the effects of mortality. As expected, in a market consistent context, because of unlocked technical bases, the expected profit (i.e.,

) occurs when the difference between the technical bases and realistic assumptions is revealed, while only the unexpected profit linked to the idiosyncratic risk of the mortality rates occurs over time. In particular, at the inception of the contract, we notice the effect of the difference between first-order basis (used for premium assessment) and second-order basis (used for the market-consistent valuation of technical provisions). In other words, implicit safety loadings are released as a technical profit at the end of the first year.

From year 2 to the end of the contract, we observe that

is equal to 0. We are indeed assuming that risk-free rates are constant and equal to first-order technical rate

and that the realistic assumptions used for best estimate valuation are kept unchanged over time by the company: these results derive from Theorem (1) and Theorem (2) of

Section 4.

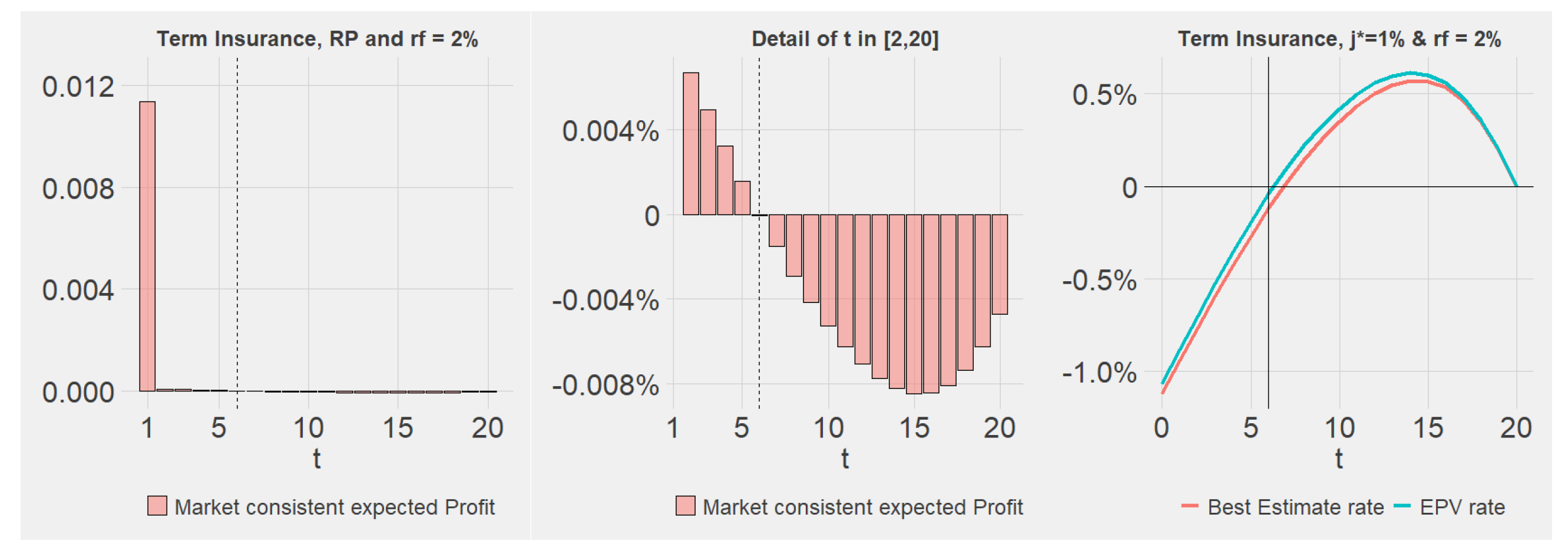

The same analysis has been also applied to term insurance contracts. In this case, we maintain the same assumptions reported in

Table 1, but we assume that premiums have been computed using an ISTAT2014 life table, while insureds die at the same rates used for the pure endowment portfolio; therefore, also in this case we have an implicit safety loading.

It is worth pointing out the higher expected demographic profit with respect to a pure endowment portfolio and a different behaviour at time 1 between regular and single premiums (see

Figure 1, top). A higher profit is here realised when a single premium is charged because of greater values of the implicit safety loading.

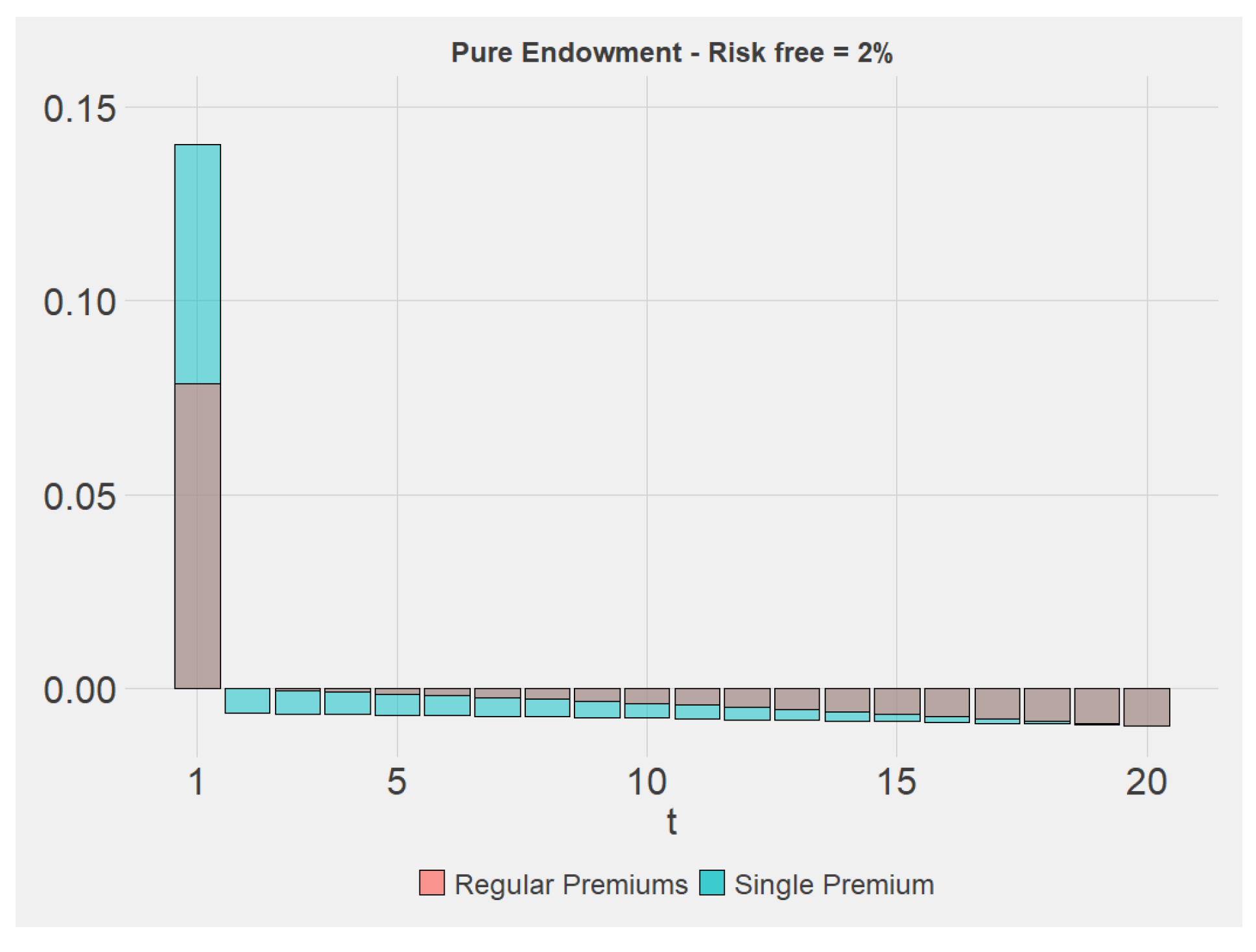

10Previous examples assumed a full coincidence between technical rates and risk-free rates. The advantage is the fact that demographic profit is not affected by the behaviour of financial rates. We analyse now the effects of alternative risk-free rates and we focus only on the expected profit evaluated in a market-consistent framework.

Figure 2, left hand-side, reports the pattern of the expected profit for a pure endowment. In this case, the same assumptions of

Table 1 have been considered, but constant spot risk-free rates equal to

are assumed. Higher risk-free rates lead to an increase of the initial profit due to a lower technical provision at the end of the year because of higher discounting effects.

11 A lower increase is observed in the case of regular premiums because also future cash-in (premiums) are discounted at higher rates.

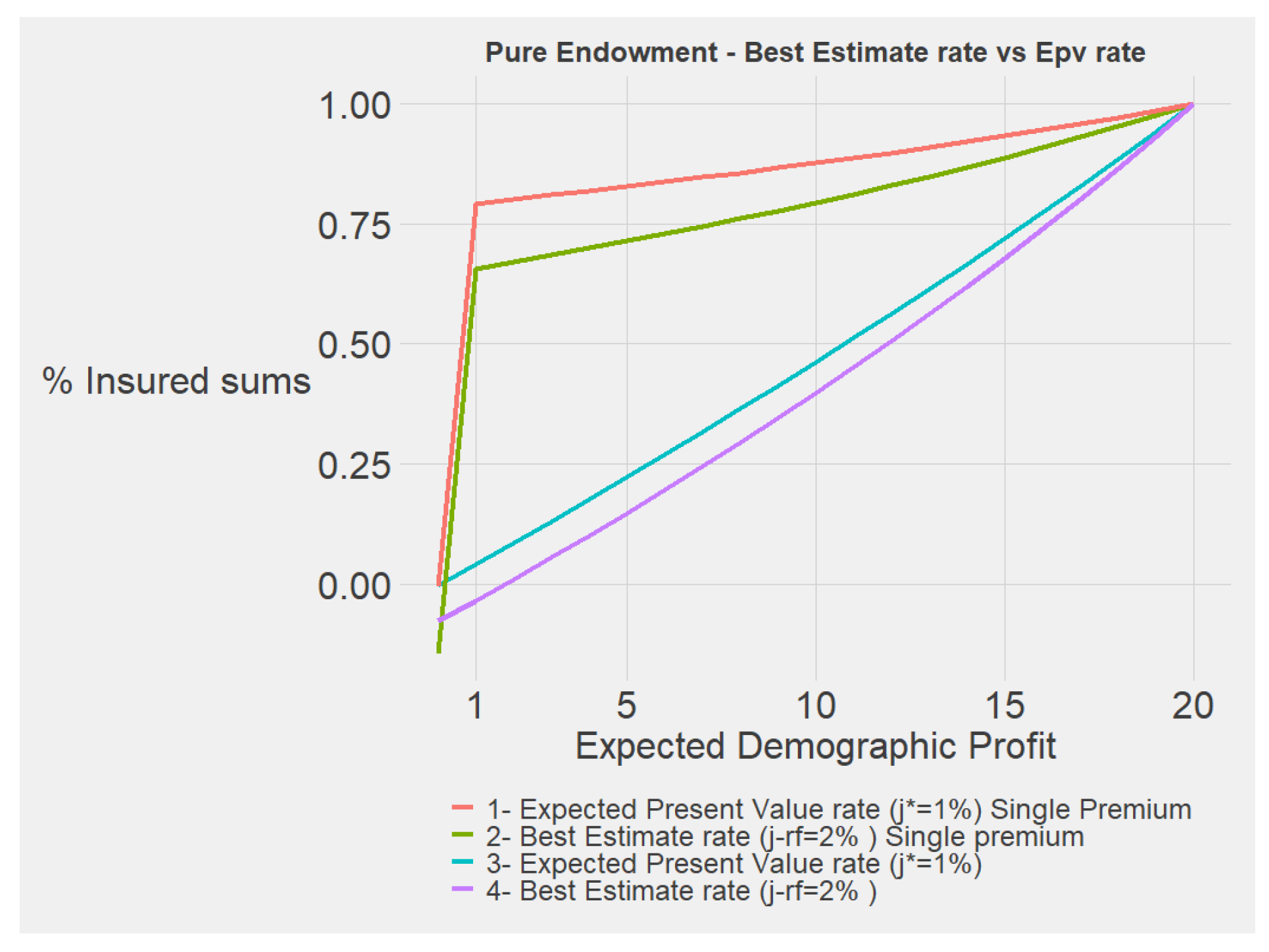

Following periods, namely for

, are instead characterized by expected losses. This behaviour can be explained by Equation (

9). As shown in

Figure 3, the reserve jump

is negative and is accumulated at a rate

. This amount is higher than the term

. The same result can also be explained by Equation (

13), where, under the assumption that the best estimates at time

t and

are positive, we have an expected loss if

is smaller than the spot rate

.

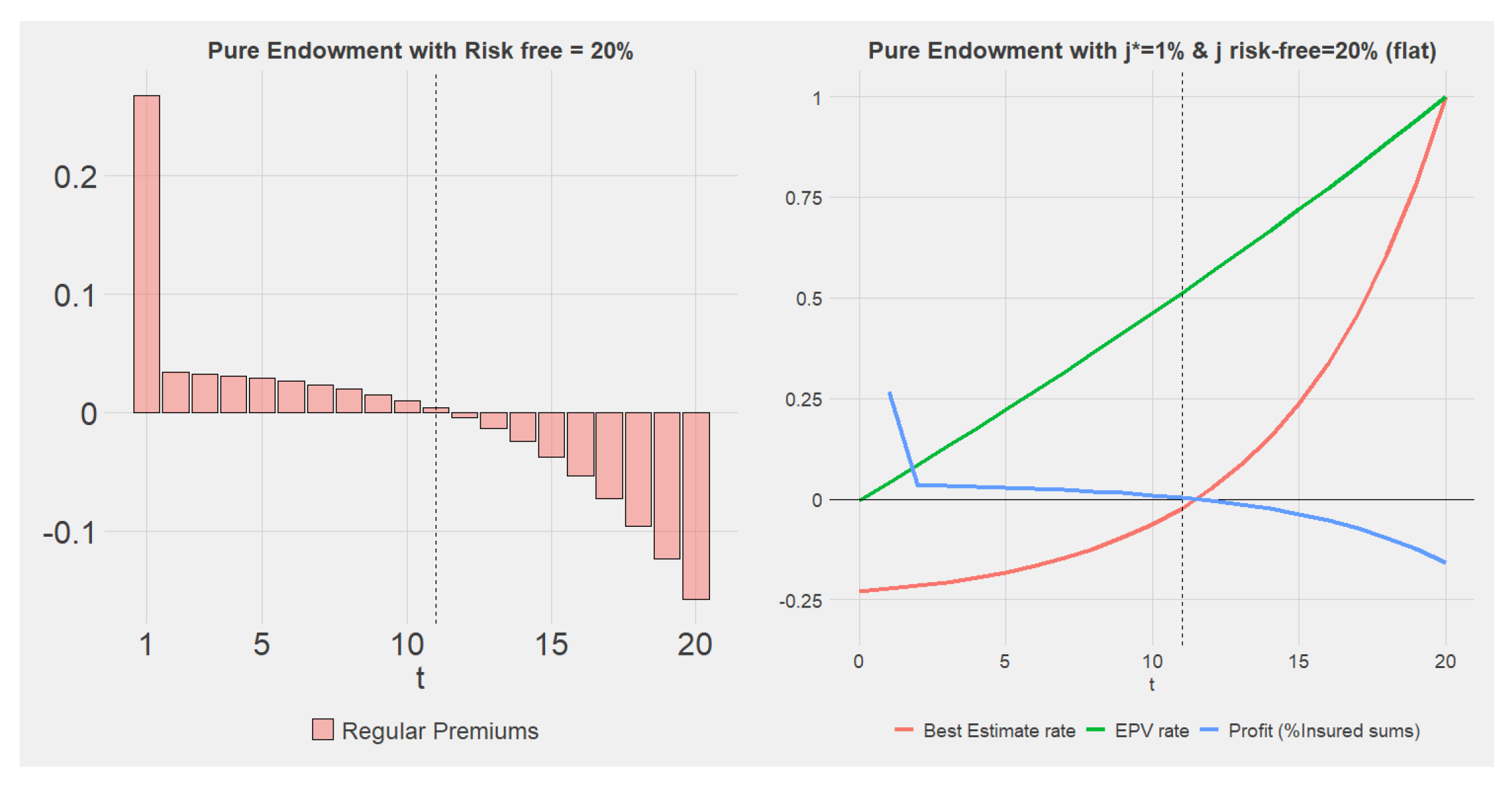

It is also interesting to note that in case of a negative best estimate we have an opposite result. In

Figure 4, we consider again a pure endowment with the same characteristics but we assume an extraordinarily large flat rate equal to

. It could be noticed that, in line with Equation (

13), in time periods in which

is negative, a positive expected profit is observed (see

in

Figure 4).

In

Figure 5, we report the behaviour of the expected profit in case of either a regular and a single premium for the term insurance. Policyholder and contract characteristics are the same reported in

Table 1 and the risk-free rate is equal to

. Results confirm a consistent behaviour independent of the kind of policy considered.

However, because of the lower best estimate rate, the effect of financial rates is less relevant when a term insurance contract is considered.

Finally, in this section, the analysis has been developed assuming a constant risk-free rate for all maturities. However, considering the case of a risk-free curve, similar comments follow from Equations (

9) and (

13) based on the comparison between the technical rate

and the forward rates for each period

.

Before presenting the next section, it is emphasized that, for a particularly young insurance company, the strictly one year vision can lead to incorrect and partial results, indeed if the Solvency Capital Requirement were calculated over a three-year time horizon, the results would be the opposite.

6. The Application of the Model to Non-Participating Life Policies

In this section, we analyse the behaviour of our model in terms of volatility and capital requirement by developing a detailed case study. We consider a portfolio characterized by three non-participating insurance policies: a Pure Endowment, an Endowment and a Term Insurance. To this end, we are able to catch how the different characteristics of the contracts can affect the demographic profit distribution and the related capital requirement.

In

Table 2, we summarize the general characteristics (age and contractual duration of the policy) and the expense loadings. For the sake of comparability, we assume that different policies have been underwritten by policyholders with the same characteristics. Furthermore, the sums insured at time 0,

, are calculated as the sum of the individual sums insured of each policyholder:

where

is the number of policyholders in

.

The risk-free rate curve used is the one provided by EIOPA for the Euro area (at the end of 2015); we preferred to use a curve calibrated in a quiet period, which does not present particular types of stress. We have chosen the one without volatility adjustment. Demographic technical bases are summarized in

Table 3 and are different for each policy because the goal is to highlight specific profit creation considering a realistic rating process.

Consequently, for the Endowment and the Term Insurance with positive sum-at-risk, the pricing is carried out with the ISTAT2014 demographic table. Pure Endowment, characterized by a negative sum-at-risk, has been priced multiplied by the death probabilities, derived by ISTAT2016 life tables, by a coefficient between and that depends on the age of the policyholder. The effective mortality of all portfolios is instead described by the ISTAT2016 table. We are obviously aware that second-order mortality can be affected by self-selection or medical-selection (e.g., in term insurance products to identify calibrated risks). Similarly, term insurance and endowment policies are usually priced using a different life table. To assure a greater comparison between results we considered in this numerical analysis similar technical bases for different policies. The results can be easily adapted to the case of a higher customization of life tables.

It is also noteworthy that future mortality rates can be obviously obtained using forecasting models (as, for instance, the Lee–Carter model). However, the main comments described in this section also hold in the case of projected second-order life tables.

The model is applied by means of Monte Carlo simulations. In particular, the number of deaths is simulated in a one-year time horizon by a Binomial distribution with parameters equal to the number of policyholders and the second-order death probability. To consider the variability of the sums insured, we extract the insured capital at the end of the year and the amounts paid in case of death by LogNormal distributions with mean and CV defined in

Table 2.

Another key element is the assessment of the Best Estimate rate at the end of the period. It is assumed that, on average, the spot rates at the end of the year will coincide with the forward rates inferable from the risk-free curve of spot rates at the beginning of the year. The volatility of risk-free rates is introduced through the use of a Vasicek model (

Vasicek 1977); particularly effective in case of negative risk-free rates for shorter maturities. Hence, the calibration of the Vašíček model is carried out for each policy and at each time point, requiring that the expected value of the best estimate rate, calculated at the end of the time span, coincides with the best estimate rate calculated with the forward rates implicit in the spot rate curve at the beginning of the time horizon. This method has been selected to eliminate the possibility of arbitrage. In this way, the expected present value in

t of the best estimate calculated from

, is equal to the expected present value in

of the best estimate (obviously calculated in

) since the spot rates in

coincide with the forward rates inferable from the spot curve available in

t. Given this constraint, valid alternatives, which consider the adjustment of the yield term, are the models proposed in (

Ho and Lee 1986;

Black et al. 1990). However, it is specified that, since the model is balanced on forward rates, the most important element is the sigma

multiplier of the infinitesimal increment of the Brownian Motion

as it is the parameter that directly influences the volatility of the risk-free rate curve.

The results of the stochastic model are presented. Two points must be highlighted:

For each policyholder, 10 million simulations have been made. Therefore, the results are particularly consistent, especially in terms of volatility;

12The total amount of the sums insured at the inception of the policy () is equal to approximately 1.5 billion euros. It is therefore noted that any Capital Requirement, in terms of magnitude, must be compared with the value just mentioned, although at first glance it may seem particularly high.

First of all,

Table 4 shows

13 the results of the simulation model applied at the inception of the contract (

) and with a one-year view to the portfolio of Pure Endowment policies.

It should be noted that the initial Best Estimate rate at the time

is negative (equal to −7.65%). Despite the significant contribution of the implicit safety demographic loading, the largest share of expected profit derives from the difference between the first order financial rate (

) and the discounting spot rate for longer maturities. For instance, the expected survival benefits paid to the policyholder at the end of the coverage are discounted by using a spot rate equal to 1.57%.

14Additionally, we have that the capital requirement, computed here using a value at risk at a 99.5% confidence level, is negative. We have indeed that the huge expected profit allows to cover adverse fluctuation of demographic assumption also in the worst case computed at the previously mentioned confidence level. A different situation is instead obtained, assumed to be at times

t = 10 and

t = 19, respectively. In

Table 4 we also report the main characteristics of profit distribution as well as the capital requirement computed on a one-year view at different time periods.

It is interesting to note that, after the first year of contract, where the expected profit at inception is accounted for, the risk-free forward rate higher than the technical rate leads to significant expected losses (in accordance to Equation (

13). This effect increases as the year progressively grows because forward rates grow over time. Because of this behaviour we have positive requirements in both periods.

In

Table 5, we provide results obtained applying the model in a local accounting framework. It is noteworthy that we observe that the standard deviation in

increases due to the greater volatility of risk-free rates, while in

only the strictly demographic volatility remains, because the only risk-free rate is known. As regards skewness, what happens is similar: in

and

the skewness deriving from the Vašíček model is the main driver, while in

only the skewness of the purely demographic component remains. With reference to the simulated SCR, it should be noted that the previous Solvency 0 and Solvency I regulations indicated 0.3% of positive sum-at-risk as a capital requirement for life underwriting risk without differentiations related to the characteristics of the insurance portfolio.

A similar analysis has been developed for an Endowment; we report in

Table 6 the main characteristics of the distribution of

and the SCR ratio according to the three time periods.

Table 7 summarizes analogous values computed in a local accounting framework.

Endowment contract shows similar results to the pure endowment case in terms of both expected profit and capital requirement ratio. The main differences can be noticed in the last year of the contract (). We have indeed that, given the fact that the payment of benefit is certain, we have no volatility and, hence, the capital requirement is only needed to face expected losses.

As well-known previous contracts are typically chosen for saving purposes and the financial profit is the key issue for an insurance company. Therefore, we investigate the behaviour of the demographic profit in the case of a term insurance, which is typically chosen by policyholders for risk-protection purposes. The main results are reported in

Table 8.

It is interesting to note that the expected gain accounted for in , although strictly greater than the expected losses of the subsequent periods, is lower than those of other policies (e.g., pure endowment, endowment). In this case, the very small volume of mathematical reserves ensures that expected losses and expected profits are very low. The previous comment is also explained by the fact that we are assuming the same first and second-order life tables in term insurance and endowment. On the other hand, despite the volatility of sums insured paid in the case of death, a lower ratio between the capital requirement and the sums insured is observed.

Comparing the results of the Term Insurance with those obtained in a Local GAAP context (see

Table 9), we observe that also in this case, the volatility in

and

is mainly driven by the volatility of the Vašíček model, while in

it remains only the volatility of the strictly demographic component. As in the case of the Pure Endowment, it is clearly observed that where the financial component is zero (in

the only spot rate is known), only the purely demographic skewness remains.

Finally, it should be noted that, despite the different nature of the alternative policies, a similar effect of the implicit forward rates is noticed both in terms of expected gains/losses, and in terms of capital requirement.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}