Impact of Fintech on Bank Risk-Taking: Evidence from China

Abstract

1. Introduction

2. Literature Review

3. Theoretical Analysis and Research Hypothesis

3.1. Theoretical Analysis

3.2. The Model

3.3. Research Hypotheses

4. Data, Variables, and Models

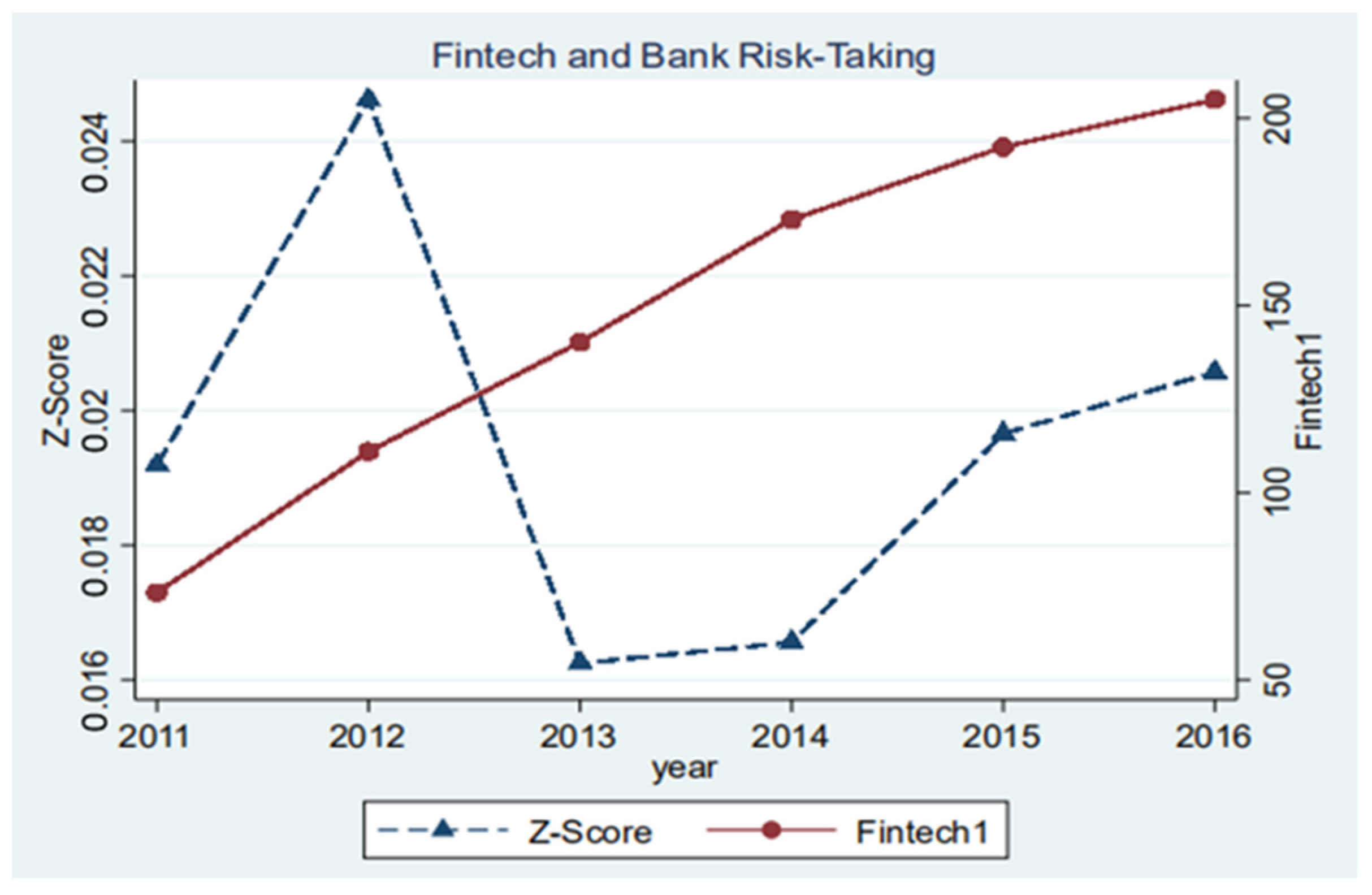

4.1. Samples and Data Sources

4.2. Definition and Measurement of Variables

4.2.1. Core Variables

4.2.2. Control Variable

4.2.3. Mediation Variable

4.2.4. Instrument Variable

4.2.5. Descriptive Analysis

5. Benchmark Model Setting

6. Empirical Results Analysis

6.1. Benchmark Regression Results

6.2. Endogenous Inspection

6.3. Robustness Test

7. Further Analysis

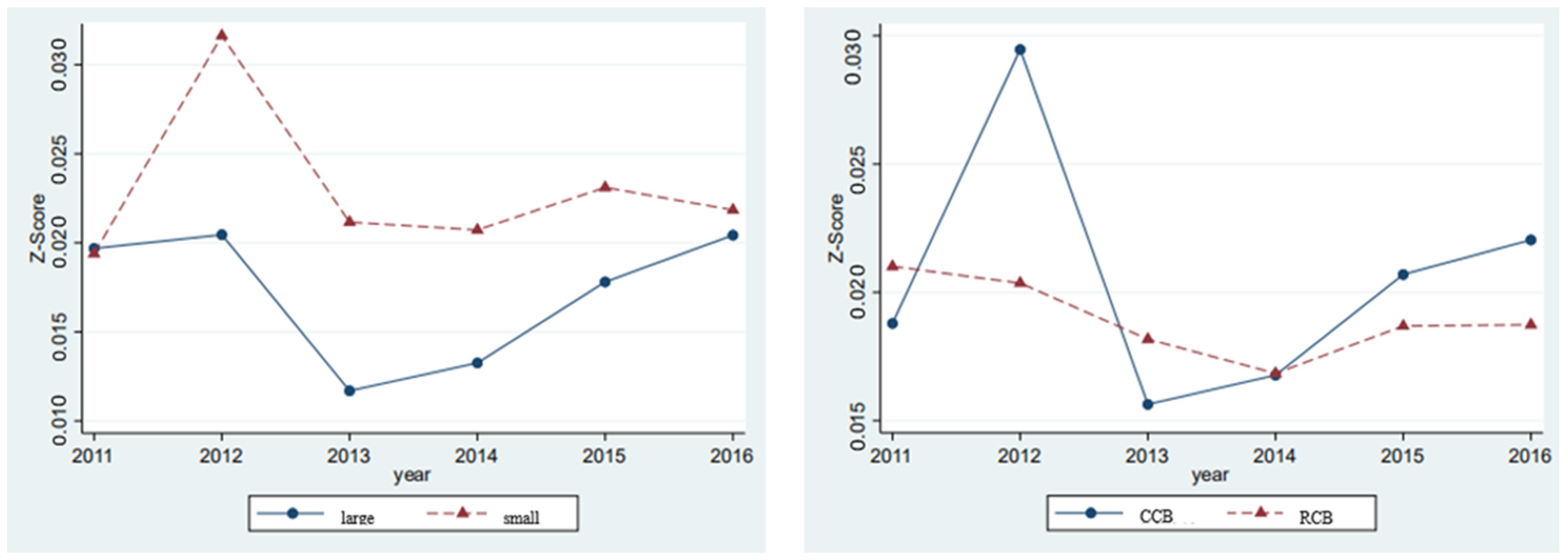

7.1. Heterogeneity Test

7.1.1. Regional Development Differences

7.1.2. Heterogeneity of Bank Size

7.1.3. Heterogeneity Analysis Based on the Banking System

7.2. Mechanism Inspection

7.2.1. Based on the Intermediary Effect Test within the Bank

7.2.2. Based on the Intermediary Effect Test Outside the Bank

8. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Describing Data

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Symbol | Variable Calculation Method |

|---|---|---|---|

| Bank data used in the explained variable | The return on total assets | ROA | From Wind Economic Database |

| The ratio of capital to assets | CAR | From Wind Economic Database | |

| The standard deviation of the return on total assets | SDROA | From Wind Economic Database | |

| Bank data used in the Intermediary variables | Management ability | Governance | ln (governance fees) |

| Bank competition intensity | HHI | Regional Herfindahl index | |

| Household propensity to save | PSaving | Total savings of local residents/district population | |

| Bank data used in the core explanatory variable | Capital adequacy ratio | CAR | Net bank capital/risk-weighted assets × 100 |

| Capital adequacy ratio | CAR | Net bank capital/risk-weighted assets × 100 | |

| Net operating margin | Netprf | Net profit/operating revenues × 100 | |

| Cost-to-income ratio | CIR | Operating cost/operating revenue × 100 | |

| Proportion of non-interest income | NIRR | Non-interest income/operating revenue × 100 | |

| Proportion of non-interest income | NIRR | Non-interest income/operating revenue × 100 | |

| Liquidity of funds | SAR | Bank balance/total bank assets × 100 |

Appendix B. Symbols and Their Meaning

| Symbol | Meaning | |

|---|---|---|

| Symbol | Total wealth | |

| Remanufacturer’s recovery cost | ||

| represents intermediary agency, b represents a large-scale intermediary agency s represents a small-scale intermediary agency | ||

| The number of asset managers The number of Robo-Advisors The number of traditional managers | ||

| The return of intermediaries investing on technology | ||

| fixed cost, | ||

| the relationship cost of working with a household, | ||

| is the fee paid to the investment manager | ||

| the net profit of any intermediary, | ||

| The return of robot advisors have access to the investment technology | ||

| The fixed entry cost of Robo-Advisors | ||

| the net profit of any intermediary | ||

| Num | The index to measure the intensity of competition | |

| pro | The index to measure the intensity of competition |

Appendix C. Robustness Test

| The Type of Robustness Test | Practice in the Text | The Reason |

|---|---|---|

| Variable substitution method | Replace the explained variable with SDROA | There are many ways to measure a variable, in order to enhance the reliability of the conclusion. We replace the dependent variable and independent variable respectively to verify the robustness of the results of this paper. |

| Replace the core explanatory variable with Fintech 2 | ||

| Change sample size | Remove the bank whose registered place is the municipality | Because the existence of extreme values in the sample will affect our results. Therefore, in the robustness test, we need to eliminate individual outliers, or select the most suitable sample for our research purposes in the sample to test whether our conclusions are still robust. |

Appendix D. Stata Measurement Software

| The Name of Software | The Advantage of Stata | Data Characteristics |

|---|---|---|

| Stata | Stata is a package that many beginners and power users like because it is both easy to learn and yet very powerful; Stata has numerous powerful yet very simple data management commands that allows you to perform complex manipulations of your data with ease; The greatest strengths of Stata are probably in regression (it has very easy to use regression diagnostic tools) | This article has many variables and complex data, it is more convenient to use Stata to perform regression. |

Appendix E. Wald Test

| Explained Variable | F-Value | p-Value |

|---|---|---|

| Z-Score | 15.55 | 0.0000 |

| SDROA | 30.58 | 0.0018 |

| Explained Variable | F-Value | p-Value |

|---|---|---|

| Z-Score | 15.56 | 0.0000 |

| SDROA | 29.66 | 0.0018 |

References

- Acharya, Ram N., and Albert Kagan. 2004. Community Banks and Internet Commerce. Journal of Internet Commerce 3: 23–30. [Google Scholar] [CrossRef]

- Allen, Franklin, and Douglas Gale. 2000. Financial Contagion. Journal of Political Economy 1: 1–33. [Google Scholar] [CrossRef]

- Beltratti, Andrea, and René M. Stulz. 2009. Why Did Some Banks Perform Better During the Credit Crisis? A Cross-Country Study of the Impact of Governance and Regulation; National Bureau of Economic Research Working Paper 15180. National Bureau of Economic Research. Available online: https://www.nber.org/papers/w15180 (accessed on 13 February 2021).

- BIS. 2019. Annual Economic Report: Promoting Global Monetary and Financial Stability. Printed in Switzerland, Werner Druck & Medien AG, Basel. Basel: BIS. [Google Scholar]

- Buchak, Greg, Gregor Matvos, Tomasz Piskorski, and Amit Seru. 2018. Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks. Journal of Financial Economics 130: 453–83. [Google Scholar] [CrossRef]

- Chen, Mark A., Qinxi Wu, and Baozhong Yang. 2019. How Valuable Is Fintech Innovation? The Review of Financial Studies 32: 2062–106. [Google Scholar] [CrossRef]

- Claessens, Stijn, M. Ayhan Kose, and Marco E. Terrones. 2012. How do business and financial cycles interact? Journal of International Economics 87: 178–90. [Google Scholar] [CrossRef]

- Dapp, Thomas F. 2014. Fintech: The digital (r)evolution in the financial sector. Deutsche Bank Research 11: 1–39. [Google Scholar]

- Fang, Yi, Shengmin Zhao, and Xiaowen Xie. 2012. Analysis of Banking Risk Assurance of Monetary Policy: Concurrently Discussing the Coordination of Monetary Policy and Macro-prudential Policy. Management World 11: 9–19. [Google Scholar]

- FSB (Financial Stability Board). 2017. Fintech. Research Report. Available online: https://www.fsb.org/work-of-the-fsb/financial-innovation-and-structural-change/fintech/ (accessed on 3 May 2021).

- Gomber, Peter, Robert J. Kauffman, Chris Parker, and Bruce W. Weber. 2018. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. Journal of Management Information Systems 35: 220–65. [Google Scholar] [CrossRef]

- Gu, Haifeng, and Lixiang Yang. 2018. Internet Finance and Banking Risk-taking: Based on evidence from the Chinese banking industry. World Economy 10: 75–100. [Google Scholar]

- Guellec, Dominique, and Caroline Paunov. 2017. Digital Innovation and the Distribution of Income. NBER Working Paper 23987. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Guo, Ye, and Chen Liang. 2016. Blockchain application and outlook in the banking industry. Financial Innovation 24: 1–12. [Google Scholar] [CrossRef]

- Shen, Yue, and Guo Pin. 2015. Internet Finance, Technology Spillover and Total Factor Productivity of Commercial Banks. Finance Research 3: 160–75. [Google Scholar]

- Guo, Pin, and Yue Shen. 2019. Internet Finance, Deposit Competition and Banking Risk-taking. Financial Research 8: 58–76. [Google Scholar]

- Guo, Feng, Jingyi Wang, Fang Wang, Tao Kong, Xun Zhang, and Zhiyun Cheng. 2019. Measurement of China’s Digital Inclusive Financial Development: Index Compilation and Spatial Features. China Economic Quarterly 19: 1401–1418. [Google Scholar]

- Huang, Yiping, and Zhuo Huang. 2018. Digital Finance Development in China: Present and Future. Economics 4: 1489–502. [Google Scholar]

- Jakšič, Marko, and Marinč Matej. 2019. Relationship banking and information technology: The role of artificial intelligence and Fintech. Risk Management 21: 1–18. [Google Scholar] [CrossRef]

- Julapa, Jagtiani, and Catharine Lemieux. 2018. Do Fintech Lenders penetrate areas that are underserved by tradition banks? Journal of Economics and Business 100: 43–54. [Google Scholar]

- Kou, Zonglai, and Xueyue Liu. 2017. China City and Industry Innovation Report 2017; Shanghai: Industrial Development Research Center of Fudan University. Available online: http://www.cbnri.org/news/5389402.html (accessed on 5 January 2021).

- Lapavitsas, Costas, and Paulo L. Dos Santos. 2008. Globalization and Contemporary Banking: On the Impact of New Technology. Contributions to Political Economy 27: 31–56. [Google Scholar] [CrossRef]

- Li, Chuntao, Xuwen Yan, Min Song, and Wei Yang. 2020. Fintech and Enterprise Innovation: Evidence from NEEQ Listed Companies. China Industrial Economy 1: 81–98. [Google Scholar]

- Liu, Liya, Minghui Li, Sha Sun, and Jinqiang Yang. 2014. Research on The Relationship Between Net Interest Margin and Non Interest Income of China’s Banking Industry. Economic Research 49: 110–24. [Google Scholar]

- Ma, Yong, and Zhen Li. 2019. Liquidity and Banking Risk-taking: Empirical Evidence from China’s Banking Industry. Finance and Trade Economy 7: 67–81. [Google Scholar]

- Marcus, Alan J. 1984. Deregulation and bank financial policy. Journal of Banking & Finance 8: 557–65. [Google Scholar]

- Mishkin, Fredric S., and Philip E. Strahan. 1999. Global financial instability: Framework, events, issues. Journal of Economic Perspectives 13: 193–201. [Google Scholar] [CrossRef]

- Petter, Gottschalk, and Geoff Dean. 2009. A review of organised crime in electronic finance. International Journal of Electronic Finance 3: 46–63. [Google Scholar]

- Philippon, Thomas. 2015. The Fintech Opportunity; National Bureau of Economic Research Working Paper. Cambridge: National Bureau of Economic Research. Available online: http://www.nber.org/papers/w22476 (accessed on 5 March 2021).

- Philippon, Thomas. 2019. On Fintech and Financial Inclusion. NBER Working Paper. Available online: https://www.nber.org/papers/w26330 (accessed on 13 January 2021).

- Pi, Tianlei, and Tie Zhao. 2014. Internet Finance: Category, revolution and Prospect. Finance & Economics 6: 22–30. [Google Scholar]

- Pierri, Nicola, and Yannick Timmer. 2020. Tech in Fin before Fintech: Blessing or Curse for Financial Stability? International Monetary Fund Working Paper 8067. International Monetary Fund. Available online: https://ssrn.com/abstract=3623873 (accessed on 14 March 2021).

- Qiu, Han, Yiping Huang, and Yang Ji. 2018. The Impact of Fintech on Traditional Banking Behaviors: From the Perspective of Internet Finance. Financial Research 11: 17–29. [Google Scholar]

- Roger, Lagunoff, and Stacey L. Schreft. 1999. Financial Fragility with rational and irrational Exuberance. Journal of Money, Credit and Banking 31: 531–60. [Google Scholar]

- Inna, Romānova, and Marina Kudinska. 2016. Banking and Fintech: A Challenge or Opportunity? In Contemporary Issues in Finance: Current Challenges from Across. Bingley: Emerald Group Publishing Limited. [Google Scholar]

- Schumpeter, Joseph Alois. 1912. Theorie Der Wirtschaftlichen Entwicklung. München und Leipzig: Duncker & Humblot. [Google Scholar]

- Sheng, Tianxiang, and Conglai Fan. 2020. Financial Science and Technology, Optimal Banking Market Structure and Credit Supply of Small and Micro Enterprises. Financial Research 6: 114–32. [Google Scholar]

- Shi, Bingzhan, and Xiangyi Jin. 2019. Attention disposition, Internet Search and International Trade. Economic Research Journal 54: 71–86. [Google Scholar]

- Song, Min, Peng Zhou, and Haitao Si. 2021. Fintech and firm total factor productivity: A perspective of “enabling” and credit rationing. China Industrial Economics 4: 138–55. [Google Scholar]

- Wang, Xun, and Anders Johansson. 2013. Financial Repression and Economic Structural Transformation. Economic Research 1: 54–67. [Google Scholar]

- Xie, Ping, and Chuanwei Zou. 2012. Research on Internet Finance Model. Financial Research 12: 11–22. [Google Scholar]

- Xu, Mingdong, and Xuebin Chen. 2012. Monetary environment, basic adequacy ratio and risk taking of commercial banks. Financial Research 7: 48–62. [Google Scholar] [CrossRef]

- Yao, Ting, and Liangrong Song. 2020. The Impact of Financial Technology on The Risk of Commercial Banks and Its Heterogeneity. Journal of Yunnan University of Finance and Economics 36: 53–63. [Google Scholar]

- Zhang, Xuelan, and Dexu He. 2012. Monetary Policy Position and Bank Risk-taking: An Empirical Study Based on Chinese Banking Industry. Economic Research 5: 31–44. [Google Scholar]

- Zhang, Yilin, Yifu Lin, and Qiang Gong. 2019. Enterprise Scale, Bank Scale and Optimal Banking Industry Structure—Based on The Perspective of New Structural Economics. Management World 3: 31–47. [Google Scholar]

| 1 | This article introduces the cross-multiplying terms of internet penetration and financial technology development to examine the moderating effect of regional internet penetration on the correlation between financial technology and bank risk. |

| 2 | This paper also uses one-stage lag independent variable to weaken the endogenous problem. Due to space limitations, we will not go into details. |

| Variable Type | Variable Name | Variable Symbol | Variable Meaning |

|---|---|---|---|

| Explained variable | Z | Z-Score | ln (Z + 1) |

| Volatility of return on assets | SDROA | ln (SDROA + 1) | |

| Core explanatory variable | Fintech level | Fintech 1 | ln (the coverage breadth dimension of regional digital finance index) |

| Fintech 2 | Refer to Li et al. (2020) | ||

| Instrumental variable | Urban innovation index | Innovation | Refer to Kou and Liu (2017) |

| Intermediary variables | Net interest margin | NIM | Net interest income/average interest-bearing assets × 100 |

| Management ability | Governance | ln (governance fees) | |

| Bank competition intensity | HHI | Regional Herfindahl index | |

| Household propensity to save | PSaving | Total savings of local residents/district population | |

| Bank-level control variables | Bank size | Size | ln (total bank assets) |

| Asset-liability ratio | DAR | Total bank liabilities/total bank assets × 100 | |

| Capital adequacy ratio | CAR | Net bank capital/risk-weighted assets × 100 | |

| Net operating margin | Netprf | Net profit/operating revenues × 100 | |

| Cost-to-income ratio | CIR | Operating cost/operating revenue × 100 | |

| Proportion of non-interest income | NIRR | Non-interest income/operating revenue × 100 | |

| Liquidity of funds | SAR | Bank balance/total bank assets × 100 | |

| City-level control variables | Level of economic development | PGDP | ln(GDP per capita) |

| Degree of financial development | FinDev | (Total regional deposits + total regional loans)/total wages of all employees | |

| Macro-level control variables | Monetary Policy Trend | M2 | Broad money growth rate |

| Variable Name | Average | Standard Deviation | Median | Minimum | Maximum | Observed Value |

|---|---|---|---|---|---|---|

| Z-Score | 0.019 | 0.025 | 0.015 | 0.001 | 0.613 | 898 |

| SDROA | 0.002 | 0.002 | 0.001 | 0.000 | 0.026 | 904 |

| Fintech 1 | 4.925 | 0.434 | 5.034 | 2.692 | 5.515 | 930 |

| Fintech 2 | 3.210 | 1.460 | 3.260 | 0.000 | 15.78 | 909 |

| Innovation | 42.56 | 93.66 | 13.72 | 0.099 | 1061 | 930 |

| Internet | 0.274 | 0.203 | 0.214 | 0.018 | 1.386 | 930 |

| NIM | 3.275 | 1.227 | 3.100 | −0.040 | 13.42 | 899 |

| Governance | 2.407 | 0.093 | 2.411 | 2.128 | 2.640 | 902 |

| HHI | 0.114 | 0.040 | 0.106 | 0.055 | 0.250 | 930 |

| PSaving | 5.690 | 3.761 | 4.759 | 0.949 | 24.29 | 930 |

| Size | 15.69 | 1.225 | 15.70 | 12.13 | 19.17 | 926 |

| DAR | 92.19 | 2.518 | 92.58 | 58.04 | 96.99 | 926 |

| CAR | 14.32 | 14.80 | 13.16 | 5.550 | 446.0 | 890 |

| Netprf | 33.74 | 9.642 | 34.45 | −56.89 | 56.43 | 923 |

| CIR | 33.48 | 7.653 | 32.92 | 14.83 | 152.9 | 921 |

| NIRR | 17.69 | 16.76 | 12.15 | −5.340 | 101.6 | 900 |

| SAR | 73.81 | 11.18 | 74.64 | 33.26 | 101.5 | 924 |

| PGDP | 1.906 | 0.666 | 1.833 | −1.905 | 3.525 | 930 |

| (1) Random Effect | (2) Individual Fixed Effect | (3) Time-Fixed Effect | (4) Two-Way Fixed Effect | |

|---|---|---|---|---|

| Fintech 1 | −0.00419 ** | −0.00977 *** | −0.0141 *** | −0.0102 * |

| (−2.39) | (−3.40) | (−3.15) | (−1.76) | |

| Size | −0.00233 *** | 0.00524 * | −0.00222 *** | 0.00504 |

| (−3.29) | (1.68) | (−3.21) | (1.26) | |

| DAR | 0.00113 *** | 0.00101 *** | 0.00111 *** | 0.000994 ** |

| (4.31) | (2.70) | (4.26) | (2.48) | |

| CAR | 0.000105 *** | 0.000136 *** | 0.000108 *** | 0.000134 *** |

| (3.34) | (4.21) | (3.44) | (4.04) | |

| Netprf | −0.000402 *** | −0.000452 *** | −0.000389 *** | −0.000455 *** |

| (−7.27) | (−4.85) | (−6.85) | (−4.61) | |

| CIR | −0.000129 ** | −0.0000276 | −0.000109 * | −0.0000292 |

| (−1.98) | (−0.22) | (−1.64) | (−0.22) | |

| NIRR | 0.0000638 ** | 0.0000711 * | 0.0000516 ** | 0.0000709 * |

| (2.45) | (1.85) | (1.97) | (1.84) | |

| SAR | −0.000182 *** | −0.000108 | −0.000158 *** | −0.0000972 |

| (−3.58) | (−1.15) | (−3.12) | (−1.03) | |

| PGDP | −0.00180 * | −0.00257 | −0.000612 | −0.00281 |

| (−1.93) | (−1.23) | (−0.59) | (−1.33) | |

| FinDev | 0.000192 *** | 0.000144 | 0.000195 *** | 0.000117 |

| (3.30) | (1.54) | (3.25) | (1.21) | |

| M2 | −0.000268 | 0.000322 | −0.00487 *** | −0.000635 |

| (−0.56) | (0.87) | (−2.97) | (−0.22) | |

| _cons | 0.00226 | −0.0915 | 0.102 ** | −0.0724 |

| (0.08) | (−1.51) | (2.28) | (−0.68) | |

| Observations | 846 | 846 | 846 | 846 |

| R2 | 0.148 | 0.161 | 0.164 | 0.176 |

| Variable Name | Variable Symbol | |

|---|---|---|

| Dependent variable | Z | Z-Score |

| Exogenous variables | Urban innovation index | Innovation |

| Endogenous variables | Fintech level | Fintech 1 |

| Bank-level control variables | Size, DAR, CAR, Netprf, CIR, NIRR, SAR | |

| City-level control variables | PGDP, FinDev | |

| Macro-level control variables | M2 | |

| Instrumental variable | Urban innovation index | Innovation |

| (1) Z-Score | (2) Fintech 1 | (3) Z-Score | |

|---|---|---|---|

| Innovation | −0.0000258 | 0.0019945 *** | |

| (−0.77) | (5.94) | ||

| Fintech 1_hat | −0.0169861 ** | ||

| (−2.11) | |||

| observations | 846 | 846 | 846 |

| R2 | 0.487 | 0.623 | 0.115 |

| (1) Random Effect | (2) Individual Fixed Effect | (3) Time-Fixed Effect | (4) Two-Way Fixed Effect | |

|---|---|---|---|---|

| Fintech 1 | −0.000451 ** | −0.000779 ** | −0.00186 *** | −0.00146 ** |

| (−2.04) | (−1.97) | (−3.28) | (−2.07) | |

| observations | 847 | 847 | 847 | 847 |

| R2 | 0.272 | 0.283 | 0.289 | 0.303 |

| (1) Random Effect | (2) Individual Fixed Effect | (3) Time-Fixed Effect | (4) Two-Way Fixed Effect | |

|---|---|---|---|---|

| Fintech 2 | −0.00108 ** | −0.00154 * | −0.00113 ** | −0.00102 |

| (−2.22) | (−1.87) | (−2.03) | (−1.13) | |

| observations | 828 | 828 | 828 | 828 |

| R2 | 0.154 | 0.158 | 0.174 | 0.184 |

| (1) Random Effects | (2) Individual Fixed Effect | (3) Time-Fixed Effect | (4) Two-Way Fixed Effect | |

|---|---|---|---|---|

| Fintech 1 | −0.00969 *** | −0.0189 *** | −0.0286 *** | −0.0200 * |

| (−2.76) | (−2.88) | (−3.55) | (−1.67) | |

| observations | 786 | 786 | 786 | 786 |

| R2 | 0.491 | 0.509 | 0.501 | 0.532 |

| (1) Eastern Region | (2) Central Region | (3) Western Region | |

|---|---|---|---|

| Fintech 1 | −0.0116 ** | −0.0122 | −0.0348 ** |

| (−2.20) | (−0.94) | (−2.28) | |

| observations | 549 | 155 | 142 |

| Number of banks | 100 | 27 | 25 |

| R2 | 0.147 | 0.338 | 0.244 |

| (1) Provincial Capitals | (2) Non-Provincial Capital | |

|---|---|---|

| Fintech 1 | −0.0122 | −0.0147 ** |

| (−1.01) | (−2.54) | |

| observations | 233 | 553 |

| Number of banks | 41 | 101 |

| R2 | 0.403 | 0.101 |

| (1) Large-Scale | (2) Small-Scale | |

|---|---|---|

| Fintech 1 | −0.0086 *** | −0.0019 |

| (−3.73) | (−0.67) | |

| observations | 456 | 390 |

| Number of banks | 102 | 100 |

| R2 | 0.285 | 0.100 |

| (1) Urban Commercial Bank | (2) Rural Commercial Bank | |

|---|---|---|

| Fintech 1 | −0.0350 *** | −0.0236 ** |

| (−3.35) | (−2.15) | |

| observations | 589 | 257 |

| Number of banks | 101 | 51 |

| R2 | 0.518 | 0.302 |

| (1) Z-Score | (2) NIM | (3) Z-Score | (4) Z-Score | (5) Governance | (6) Z-Score | |

|---|---|---|---|---|---|---|

| Fintech 1 | −0.0249 *** | −0.463 * | −0.0240 *** | −0.00419 ** | 0.00903 *** | −0.00372 ** |

| (−3.15) | (−1.80) | (−3.00) | (−2.39) | (3.32) | (−2.13) | |

| NIM | 0.00170 * | |||||

| (1.73) | ||||||

| Governance | −0.0580 *** | |||||

| (−2.81) | ||||||

| observations | 846 | 848 | 837 | 846 | 860 | 845 |

| R2 | 0.499 | 0.627 | 0.501 | 0.148 | 0.734 | 0.163 |

| (1) Z-Score | (2) HHI | (3) Z-Score | (4) Z-Score | (5) PSaving | (6) Z-Score | |

|---|---|---|---|---|---|---|

| Fintech 1 | −0.0141 *** | −0.0182 *** | −0.0168 *** | −0.00419 ** | 1.441 *** | −0.0168 *** |

| (−3.15) | (−4.38) | (−3.58) | (−2.39) | (12.16) | (−3.59) | |

| HHI | −0.0268 * | |||||

| (1.67) | ||||||

| PSaving | 0.000557 * | |||||

| (1.85) | ||||||

| observations | 846 | 863 | 846 | 846 | 863 | 846 |

| R2 | 0.164 | 0.627 | 0.163 | 0.148 | 0.751 | 0.162 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Deng, L.; Lv, Y.; Liu, Y.; Zhao, Y. Impact of Fintech on Bank Risk-Taking: Evidence from China. Risks 2021, 9, 99. https://doi.org/10.3390/risks9050099

Deng L, Lv Y, Liu Y, Zhao Y. Impact of Fintech on Bank Risk-Taking: Evidence from China. Risks. 2021; 9(5):99. https://doi.org/10.3390/risks9050099

Chicago/Turabian StyleDeng, Liurui, Yongbin Lv, Ye Liu, and Yiwen Zhao. 2021. "Impact of Fintech on Bank Risk-Taking: Evidence from China" Risks 9, no. 5: 99. https://doi.org/10.3390/risks9050099

APA StyleDeng, L., Lv, Y., Liu, Y., & Zhao, Y. (2021). Impact of Fintech on Bank Risk-Taking: Evidence from China. Risks, 9(5), 99. https://doi.org/10.3390/risks9050099