1. Introduction

Risk preferences play a vital role in a wide range of decision-making spheres, including economic, social, and political decisions, among others (

Ertac 2020). Economics and psychology in particular use risk preferences to predict human behavior, which can be exhibited through financial decisions and livelihood choices. In essence, risk preferences are a mediating factor of an individual’s risk tolerance behavior. In a bid to understand the risk preferences of individuals, researchers have elicited risk preferences using surveys and experimental approaches (

Charness et al. 2013;

Jaspersen et al. 2020;

Linciano and Soccorso 2012). There is a need to critically evaluate if subjects exhibit consistent risk attitudes in situations where different methods of gathering risk preferences are applied. Some of the methods used by researchers to elicit risk preferences from subjects include incentivized multiple price list (MPL), prospect theory tasks, balloon analogue risk task (BART), single choice of how to apportion between a safe and risk asset, single choice between gambles and non-incentivized questionnaires such as the great risk question (GRQ) (

Charness et al. 2013;

Jaspersen et al. 2020;

Kahneman and Tversky 1979).

The use of a questionnaire (GRQ) to elicit perceived willingness to take a financial risk (PWTFR) can be easily applied to large groups of subjects in surveys since the costs of collecting the data are lower when compared to the use of an incentivized risk preference experiment (

Dohmen et al. 2011;

Lusardi and Mitchell 2011). When subjects respond to the GRQ, they reflect on their individual risk preference experiences, which may be current or historical risk perceptions. They evaluate themselves usually on a Likert scale, where they rank their risk preferences(

Kalra Sahi 2017). Eliciting risk preferences by way of GRQ is subjective as one may reference themselves using their internal standard and may be heavily influenced by psychological biases (

Jaspersen et al. 2020). However, if individuals can reveal their subjective wellbeing by providing their true life experience, then the data collected by way of surveys can provide a true representation of one’s risk preference choices.

On the other hand, eliciting risk preferences by way of experiments can involve people being asked to make choices on lotteries with different risk profiles that have a probability of winning a true monetary value. The multiple price list (MPL) method is one of the popular methods that has been used by researchers to experimentally elicit risk preferences (

Charness et al. 2013;

Andersen et al. 2008). In this method, subjects are asked to make choices on one of two lotteries with different risk levels (see,

Holt and Laury 2002). In some MPL experiments, subjects are incentivized by being paid the true value of their choices as a way of encouraging them to exhibit their truthful risk preferences. In the same vein, experimentally elicited risk preferences can be heavily influenced by psychological (cognitive, emotional, etc.) biases. The presence of high- and low-risk lotteries in an experimental task means that subjects may be required to apply their numeracy skills, which may further give rise to cognitive biases. Biases that are inherent within subjects can affect their ability to maximize their utility, resulting in their risk preference choices deviating from rational economic theory predictions. This study does not investigate biases that may arise when subjects make risk preference choices, nor does it examine the superiority of particular risk-preference-eliciting methods. The paper investigates whether subjects made consistent and stable risk preference choices when they provide the risk preference choices experimentally and by way of the GRQ.

Overwhelming evidence suggests that financial literacy assists individuals to achieve better life outcomes (

Lusardi and Mitchell 2014;

Hastings et al. 2013;

Kurowski 2021). Minimum financial capabilities required by individuals to benefit from financial literacy include numeracy, which makes them understand the concept of interest and compounding interest, implications of inflation on investments and incomes as well as comprehending risk diversification (

Lusardi 2019). What is also not clear is how financial literacy interacts with risk preferences in the realization of life outcomes. There is evidence that suggests that financial literacy reduces risk attitude inconsistency (

Gizem Korkmaz et al. 2009;

Anderson and Mellor 2009). One may want to know if financial literacy helps individuals to better understand their risk preferences by comparing risk preferences that are elicited experimentally against those collected by way of the general risk question.

Studies have confirmed that imparting non-cognitive skills such as human capital to individuals can help to alter preferences, suggesting that preferences can be flexible and malleable (

Ertac 2020). Furthermore, the theory of planned behaviour contends that knowledge interacts with attitudes, preferences, and norms to mold individual behavior (

Ajzen 2011). Financial knowledge is viewed as a human capital aspect that assists individuals to beneficially handle finances. In addition, financial literacy is the knowledge and capability to handle financial issues which includes aspects of numeracy that can require cognitive skills to provide solutions. Cognitive skills have been found to be essential in determining risk preferences in some studies (

Lührmann et al. 2018). In addition, low cognitive skills are associated with heuristic responses by individuals (

Binswanger and Salm 2017). Some studies suggest that preferences are permanent and can be identified at early stages in children (

Castillo et al. 2018). Others confirm that individual preferences can change as one grows older, suggesting that age compounded with experience and knowledge can influence preference choices (

Alan et al. 2020). Preferences can significantly differ by gender, involvement in decision making, the size of the household and the level of income that one is holding, among other factors (

Ertac 2020;

Haushofer and Fehr 2014).

The questions that usually arise are: can GRQ be a proxy of incentivized revealed risk preferences (IRRP) when eliciting risk preferences? Are subjects’ risk preference choices elicited by IRRP and GRQ methods stable? Are risk preferences flexible or permanent? Do human capital aspects such as financial literacy play a role in risk preference choice consistency? This study’s theoretical framework is nested in the Theory Comparison approach applied in the health sector studies (

Möller and Marsh 2013). The research compares an economics theory method of eliciting risk preference choices (IRRP) against a psychology theory method of gathering risk preference rankings (PWTFR) (

Hertwig et al. 2019). Theory comparison can help to examine if constructs can be captured differently or similarly using different approaches or if theories view the same constructs differently (

Nigg et al. 2002). Comparing PWTFR and IRRP methods can assist in designing guides to intervention which can help subjects to maintain their behaviour change over time. It is important to note that moderators, that is, minority status such as gender and many other individual characteristics, can variedly influence the effectiveness and outcomes of the methods under investigation. If observed variances between methods of eliciting risk preferences cannot be explained by the instruments under comparison, this can necessitate the development of new approaches of gathering data.

Informed by the theory comparison approach, the study seeks to test the following bi-directional hypothesis:

Hypothesis 1 (H1). PWTFR choices are positively and significantly correlate with IRRP choices.

Hypothesis 2 (H2). PWTFR mean choices are equal to IRRP mean choices.

Hypothesis 3 (H3). Financial literacy and individual characteristics influence PWTFR and IRRP choices.

Hypothesis 4 (H4). Financial literacy and individual characteristics influence the variance between PWTFR and IRRP choices.

This study examines the stability of risk preferences of subjects elicited using two different methods, namely: self-reported perceived willingness to take financial risk in investment (PWTFR) an equivalent to the general risk question (GRQ) and incentivized revealed risk preference (IRRP) choices elicited by way of multiple price list (MPL) tasks (

Andersen et al. 2008;

Mudzingiri 2019;

Holt and Laury 2002). The research further explores whether financial literacy helps subjects to make consistent risk preference choices between the two methods used to gather data. Stability of risk preferences collected by the two different methods is important in the following ways: firstly, if PWTFR can predict IRRP, the cost of eliciting risk preference from individuals will be lowered by merely asking the GRQ (PWTFR); secondly, if individuals understand their financial risk attitudes, researchers can easily predict their financial behaviour; thirdly, the study can provide insights into the effect of incentives in eliciting risk preferences. Fourthly, investigating whether human capital skills, such as financial literacy, can bridge the gap between PWTFR and IRRP can help researchers to understand the role of financial literacy on individual risk preferences.

This study is arranged as follows: the next section of the research focuses on the methodology, followed by sections exploring the model specification and results. The final section is dedicated to the conclusion.

3. Empirical Model Specification

Before estimating regression analysis, the study provided descriptive statistics, performed row and column cross tabulations of risk preference choices, carried paired t-test analysis and provided partial correlation analysis.

A cross-sectional ordinary least squares (OLS) regression model investigating factors associated with PWTFR rankings was specified as follows (

Ghaddar et al. 2008):

where

stands for GRQ responses made by individual

i,

is a constant representing other factors that were not included in the model,

represents variable of interest ‘financial literacy score’ of individual

i,

is the coefficient of financial literacy score,

represents control variables gender (female), age, geographical location (urban), income, financial decision status (whether one is a non-financial decision maker, joint-financial decision maker or main-financial decision maker) and number of family members in one’s household (household size).

, is the coefficient of particular control variable and

is the stochastic error term. The time-invariant variables

and

were also included in all the regression models specified below (see,

Table 2).

The study specified a random effect (RE) panel regression model for the IRRP choices made by the subjects (

Borenstein et al. 2010).

is the time-variant sum of safe choice made by individual

i at time

t;

is the risk preference task completed by individual

i at time

t and

is the coefficient of

T. Subjects completed the four

IRRP tasks one after the other. Therefore, time

t = 1, …, 4, the time period in which the

MPL tasks were completed. The research further calculated the absolute difference between the total number of safe choices an individual made on the

IRRP and

PWTFR choices. The absolute gap between

PWTFR and the

IRRP is referred to as the ‘risk tolerance gap’ in this study. The research specified the following risk tolerance gap model:

is a time-variant absolute difference between

PWTFR and

IRRP choices. The variables

PWTFR,

IRRP, risk tolerance gap, financial literacy, income and household size were presented in natural logarithms in the regression analysis. The random effect panel regressions controlled for

IRRP task-specific characteristics. To determine the appropriateness of the panel regression models used in the study, the Hausman and the Breusch Pagan Lagrange Multiplier tests were used (

Pesaran 2016). The tests supported the use of a random effect panel regression over the fixed effect model. STATA 16 was used to analyze the data.

3.1. Descriptive Statistics

A total of about 53% of the 193 subjects that participated in the research were female, about 70% resided in urban centres, the average age was about 22 years, the average income was about ZAR1 605, and the average number of family members in a household was about five. The total average of IRRP choices were 4.70 compared to 4.38 for PWTFR rankings. The average financial literacy score was 40%, showing that the subjects had low financial literacy, although they were pursuing an undergraduate Bachelor of Commerce degree and the average risk tolerance gap for the subjects was 13.3 (see

Table 3).

3.2. Perceived Willingness to Take Financial Risk for All Subjects

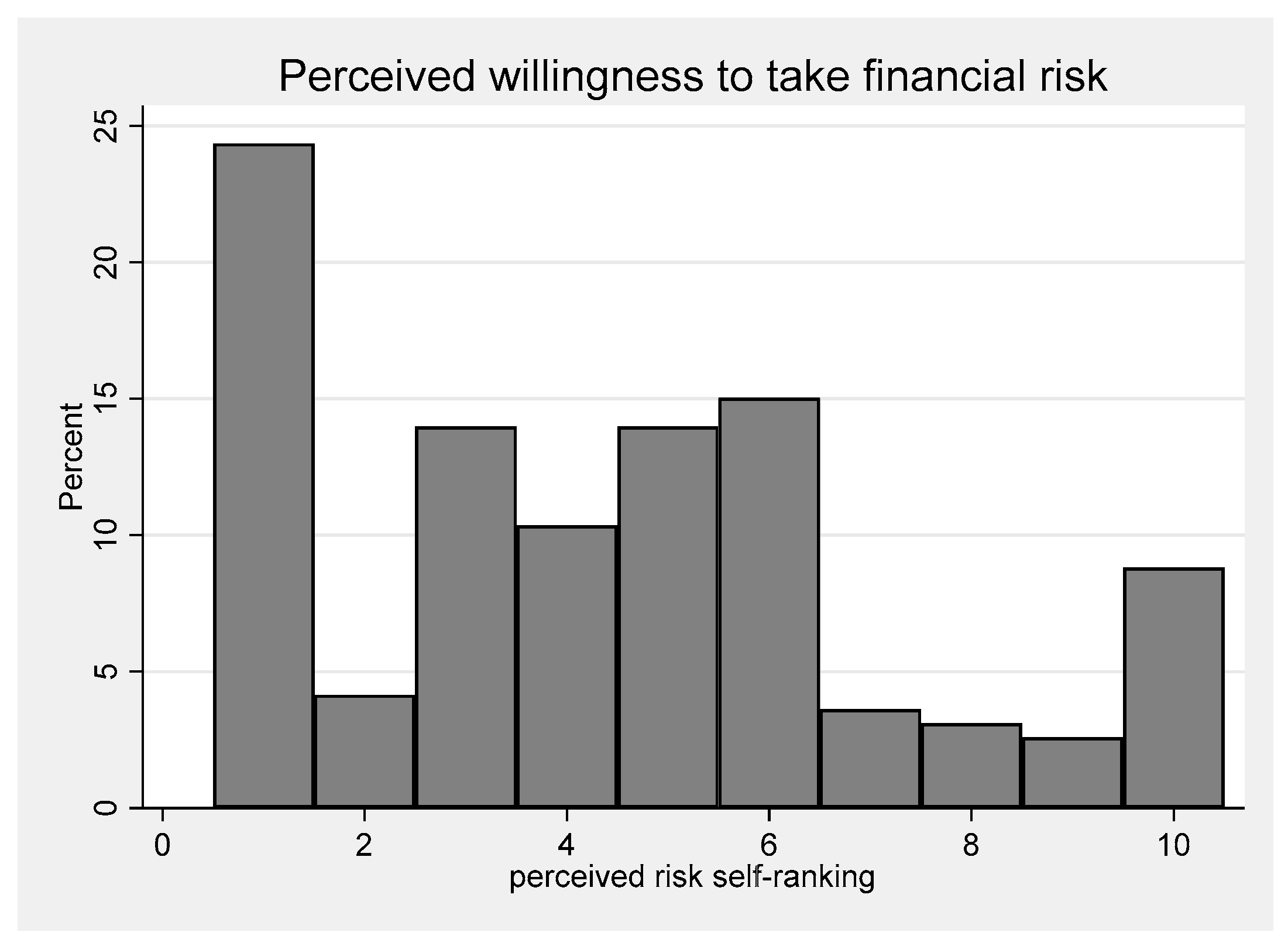

In the study, the subjects were asked to rank their willingness to take financial risk in their investments.

Figure 1 shows that the majority of the subjects indicated that they were highly willing to take financial risk (bar graph 1, about 24% of the sample). The respondents exhibited a tendency to anchor their choices at the extremes of risk loving and at the middle. The majority of the subjects perceived themselves as risk-seeking people. The way subjects rank their PWTFR shows that the responses are concentrated around either ‘highly risk-seeking’, ‘risk-neutral’, or ‘highly risk-averse’.

3.3. Incentivized Revealed Risk Preferences (IRRP)

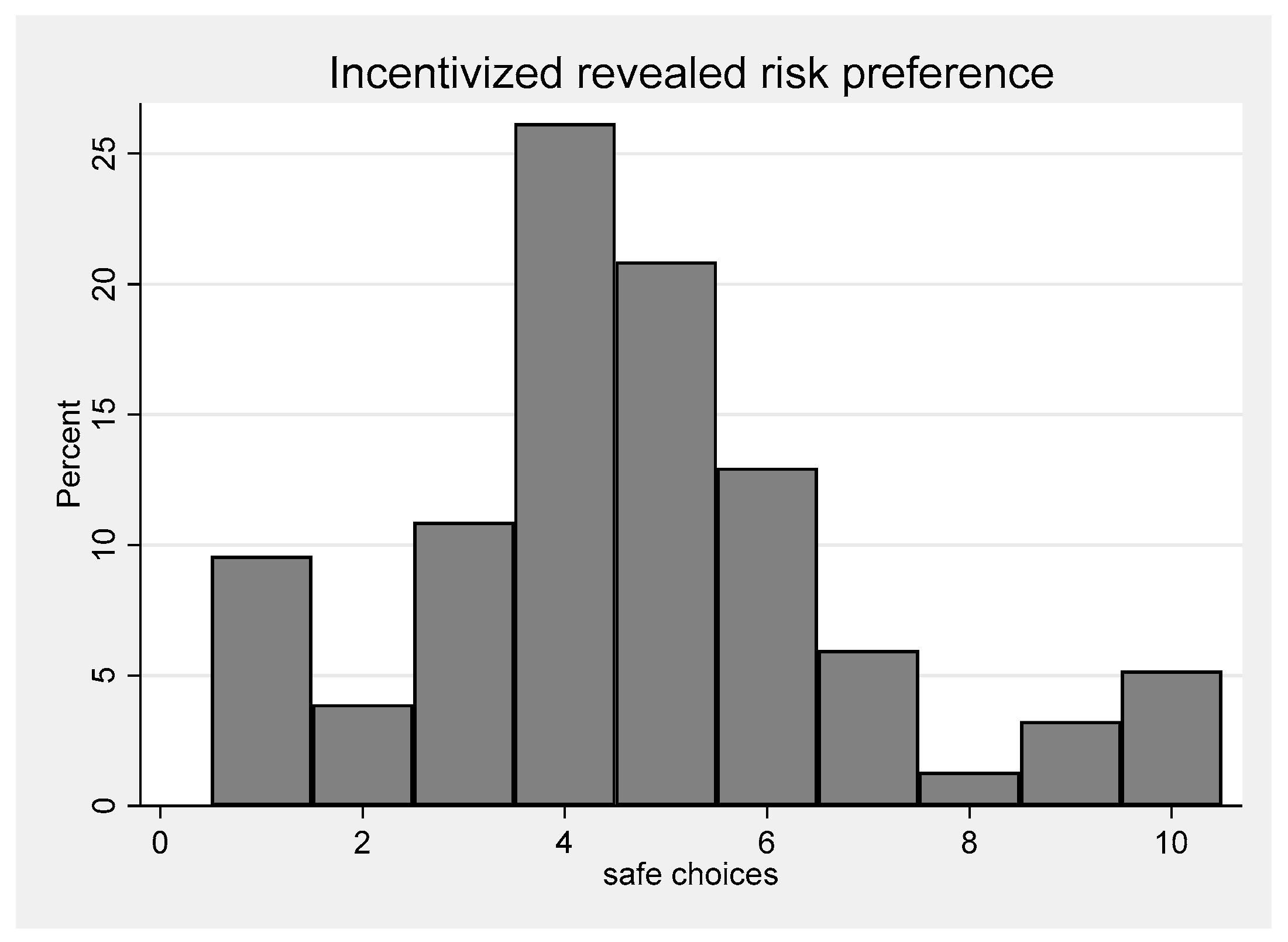

In the research, subjects completed four IRRP tasks.

Figure 2 shows aggregated safe choices for all the four tasks completed. The aggregated graph is fairly normally distributed. Making few safe choices (lottery A choices) is an exhibition of risk-seeking behavior while selecting a high number of safe choices reflects a risk aversion attitude. The majority of subjects made four (over 26%) and five (over 23%) safe choices showing risk neutrality on IRRP tasks. There are low rates of anchoring at the extreme for IRRP when compared to PWTFR. In the IRRP tasks, more subjects exhibit a risk neutrality attitude, suggesting that the presence of real monetary incentives in eliciting risk preferences could have caused subjects to be risk-averse or -neutral while in situations where there were no monetary incentives the subjects were more likely to be risk-loving/seeking.

3.4. Cumulative Density Function for PWTFR and IRRP Choices

Figure 3 shows plotted risk preference choices made by the subjects across the two methods of eliciting risk preferences on a cumulative density function. Subjects were more risk loving when they responded to the PWTFR question than when they made choices in IRRP experimental tasks. This could be also due to the incentive effect provided in the IRRP approach and not provided in the PWTFR method.

5. Conclusions

The study findings cast some doubt on equating PWTFR to IRRP when researchers elicit risk preferences using surveys and MPL incentivized experiments. The t-test and regression analysis show that subjects risk preferences collected by way MPL experiment and the GRQ were unstable and inconsistent. PWTFR cannot always precisely predict IRRPs showing that what individuals say, cannot always precisely reflect what they do when faced with a risk preference dilemma. In addition, the study findings show that financial literacy significantly influences IRRP choices and the risk tolerance gap; however, financial literacy did not influence PWTFR, suggesting that incentives impact the way people make risk preferences.

The significant narrowing of the risk tolerance gap as financial literacy increases shows that the provision of financial literacy helps individuals to more precisely predict their risk preference attitudes. The results show that low financial literacy increases heuristic responses and inconsistency. In addition, the fact that an increase in financial literacy leads to an increase in selecting safe IRRP choices and the narrowing of the risk tolerance gap shows that the provision of financial literacy has the potential to change one’s risk preferences, showing that risk preferences are malleable and flexible. The provision of financial literacy impact risk preferences of individuals resulting in a particular financial behaviour being exhibited.

Gender differences significantly influence risk preference choices, especially in the PWTFR GRQ method. The risk tolerance gap widened when subjects were female, suggesting that female subjects are more likely to under/overstate their PWTFR when compared to their IRRP. Such behavior where the risk tolerance widens could have been influenced by the female child’s life challenges or other related biases.

The study also concluded that participation in financial decision-making significantly influenced risk preferences. Involving oneself in making financial decisions influences the day-to-day risk preference choices an individual makes, showing that some learning happens when one is involved in decision making. Other variables that significantly influenced PWTFR, IRRP and the risk tolerance gap are age and income. Age brings experience with it, which influences risk preferences. Individuals who were holding higher levels of income were associated with a low RT gap. This finding could mean that holding a higher amount of money by subjects could have influenced understanding financial risk and could have helped subjects to make more calculated choices. The tendency by subjects to anchor their PWTFR choices to the extremes and at the middle suggests that surveys eliciting risk preferences should use at most three responses instead of a 10-point Likert scale. The three responses should just elicit information showing whether a person is risk-seeking or -loving, risk-averse or risk-neutral.

The implications of this study to academics are that risk preferences elicited by GRQ are not always similar to those gathered by the IRRP method, especially if subjects have low levels of financial literacy. The variation in the choices made by subjects when collecting data using the two methods is minimal if data is collected from subjects with high financial literacy. Collecting data from a high financial literacy population sample using any of the two methods can provide more reliable data. On the social front, individual characteristics can influence the way subjects make their risk preference choices. The implication of this study to government is that imparting financial literacy to citizens helps them to better understand their financial risk profile.

The use of PWTFR and IRRP tasks has limitations in eliciting true risk preferences of subjects as the world is made up of a wide range of risk preferences that cannot be easily captured by the two instruments. The instruments at this study’s disposal cannot explain a wide range of risk preferences that individuals encounter in their daily life. Besides the shortfalls, the study initiates debate on ways to elicit individual preferences in the market and their stability. Spreading the study from the laboratory into a field experiment can provide a clearer understanding of whether IRRP can be matched to PWTFR. There is a need to investigate the effect of biases on making risk preference choices. Further studies can also investigate whether providing financial literacy has the potential to change individual risk preferences for a South African representative population.

{kind=link}

{kind=link}

{kind=link}