COVID-19 Interruptions and SMEs Heterogeneity: Evidence from Poland

College of Finance, University of Economics in Katowice, 40-287 Katowice, Poland

*

Author to whom correspondence should be addressed.

Risks 2021, 9(9), 161; https://doi.org/10.3390/risks9090161

Submission received: 7 July 2021

/

Revised: 13 August 2021

/

Accepted: 19 August 2021

/

Published: 1 September 2021

(This article belongs to the Special Issue Financial Risk Management in SMEs)

Abstract

:This study contributes to the emerging stream of the literature on the COVID-19-related risks and their impact on businesses’ performance. The growing evidence within is, however, missing the uniqueness of country-level settings, as well as lacking the voice of SMEs solely. The extant literature provides some evidence on SMEs’ vulnerabilities to the crisis, but it commonly compares SMEs with large firms. To cover this gap, the main aim of this study is to analyze the perception of COVID-19 interruptions by various groups of Polish SMEs. Thus, this work adds primarily by revising the perceptions of COVID-19 risks, given the heterogeneity of SMEs if we consider their size, age, legal form of organization and status of a family firm. Based on the survey results on SMEs operating in Poland, we employ ANOVA and k-means ranks to provide strong evidence that COVID-19’s impact was perceived as more interruptive by micro and very young firms, as well as by the firms that perform as sole proprietorships. We have also found evidence that family firms do not differ from non-family ones in the perceptions of COVID-19 impacts.

1. Introduction

We are currently observing the severe and unprecedented interruptions caused by the COVID-19 outbreak. It is first and foremost a human tragedy. However, it is also having a growing adverse impact on the economy. In 2020 the global economy experienced the deepest recession since the end of World War II, with a 4.3% contraction in the global real GDP (World Bank 2021). Although the global economic situation is expected to recover in 2021, it will remain below pre-pandemic trends for a prolonged period. Thus, severe economic downturns are expected across the globe in the forthcoming years. Mechanisms underlying these downturns are complex and multidimensional; thus, it is imperative to understand the factors that make some firms and organizations more resilient to the COVID-19 crisis than others.

It is beyond doubt that the impact of COVID-19 on businesses’ performance is longitudinal (Gourinchas et al. 2021). Moreover, the COVID-19 crisis is expected to evolve irregularly, with partial recovery in some areas accompanied by worsening recoveries in others and periodic relapses, thus making the business environment turbulent in the longer run (Qiu 2020). Juergensen et al. (2020) distinguished between the immediate effects of lockdowns and the long-term implications for businesses, including SMEs and global value chains. Currently, businesses suffer from the lockdown and stay-at-home policies, which influence demand and consequently revenues (for the majority of companies a downward trend is observed) and impose higher costs on all businesses (due to the absence of workers, a necessity to implement safety measures, disruptions in the supply chain, or urgent need of the digitization of processes, etc.). However, these losses will translate further into long-term consequences, including price instability, higher cost of capital, demand restructuring, etc., which will reshape the business landscape. Thus, although shortly after the pandemic outbreak some branches enjoyed an increase in sales—whereas others a tremendous decline in sales—most businesses are or will be to some extent exposed to negative COVID-19 impacts.

Given the catastrophic dimension of COVID-19, the economic literature on COVID-19’s impacts is rapidly expanding (Amore et al. 2021; Bartik et al. 2020b; Beninger and Francis 2021; De Massis and Rondi 2020; Didier et al. 2021; Gu et al. 2020; Juergensen et al. 2020; Kraus et al. 2020; De Vito and Gómez 2020; Bognini et al. 2020). However, our study connects with the works that address the multidimensionality of the COVID-19 impact and the businesses’ resilience capabilities (on the micro and macro level), from a variety of angles. Shortly after the COVID-19 outbreak some initiatives to monitor the pandemic’s impact on the business community were launched. Several global surveys were conducted by the leading international institutions, to analyze the COVID-19 impact on the business interruption and bankruptcy risk from a business community standpoint (PwC 2020; Deloitte 2020; Mercer 2020; IRM 2020). These “barometers” offer some evidence on the most problematic COVID-19 risks and anxieties, such as the absence of the workers, the destabilization of the distribution channels, the related anxieties over the ability to continue production, the worries regarding the continuity of sales or the burden of additional costs that may appear while adapting to the new reality. However, these monitoring initiatives are designed to control the problem from a global perspective; thus, they miss the uniqueness of country-level settings. Moreover, the voice of the SMEs is lost in these monitoring endeavors.

Facing this evident gap in a more in-depth SME-oriented perspective, we designed our study to contribute to the emerging debate of COVID-19’s impacts, by providing some country-level evidence (Poland) on the importance of the heterogeneity of SMEs’ experience of the consequences of the pandemic. On the route to transition, policies were implemented to enable Poland to access foreign markets, attract foreign capital, and integrate itself deeply into cross-border supply chains. Currently, Poland is the only European economy recognized as one of 10 big emerging markets (BEM). However, similar to other transition economies, Poland is more vulnerable to shocks than the developed economies (Furceri and Zdzienicka 2011; Myant and Drahokoupil 2012). Pandemic-driven crises may thus cause bankruptcies among Polish enterprises and destabilize supply chains for a wide variety of products and services across Europe, since Polish enterprises are vital links in those chains. Early warnings on possible patterns of interruptions are thus highly desired.

A focus on the SME sector is motivated by the fact that SMEs’ uniqueness is lost in the existing COVID-19 monitoring endeavors, while this sector is of particular importance to the economy. In Poland SMEs represent 99.8% of all enterprises, they produce about 50% of GDP and they give employment to more than 67% of the Polish workforce (European Commission 2019). At the same time, SMEs are more vulnerable to distress as they have lower capital reserves and fewer assets in comparison to larger firms (Eggers 2020). It was found that the level of financial fragility among small businesses in the USA is high and that limited levels of cash on hand readily explain why COVID-19-driven layoffs and shutdowns have been so prevalent (Bartik et al. 2020a). On the other hand, small size and flexibility allow SMEs to explore new opportunities (Davidsson 2017; Myant and Drahokoupil 2012) and develop emergent strategies for sustainable business operations.

Our study contributes mainly by providing a structured view of SMEs’ experience of COVID-19’s impact by accounting for heterogeneity among SMEs. More specifically, the aim of our work is to explore whether in Poland SMEs with different characteristics exhibit different levels of sensitivity to the interruptions presented by COVID-19. First of all, the SMEs are not homogenous if we consider business size. This sector incorporates micro, small and medium-sized firms and accounting for size could be important, as it drives the availability of resources. Further, the SMEs are not homogenous in age. Older companies are more experienced, have larger networks and are perceived as more credible by their stakeholders. Next, the SMEs are not homogenous if we consider their legal form. In this respect, our attention is drawn to the differences in the possible legal forms of SMEs and the related owners’ financial responsibilities for the business’ collapse. The difference in legal form may significantly shape the owners’ perception of risks and losses caused by COVID-19, because losses may hit private property often also shared with other family members. To some extent perception of interruption seems also to be related to the family businesses where not only the owner but also the entire family’s income depends on the firm’s stability. Thus, we also controlled for differences among family and non-family firms.

In a methodological context, this study presents and discusses the results of a survey, which was conducted on a random sample of firms operating in Poland, in Jan–Feb 2021. At that time, Poland had witnessed the hit of the two pandemic waves, so the surveyed businesses were no longer under the first (shocking) impression of the COVID-19 interruptions. In addition, the Polish SMEs were eligible to benefit from government and institutional measures implemented in response to COVID-19 (e.g., direct financial aid, tax reliefs, or credit holidays) (KPMG 2020). Thus, the survey was conducted at a time when Polish SMEs had managed to familiarize themselves with the COVID-19-related risks, they increased their awareness of direct and indirect impacts and in many cases, and they were forced to redesign their business models to be more resilient. Interestingly, the results of our study have indicated that these unique SME features (size, age, legal form and the related ownership aspects) are related to differences in the perception of COVID-19 interruptions. Overall, we have found that family and non-family businesses differed significantly only with workforce-related interruptions and the ability to continue production. The businesses of varying size, age and legal form differed significantly with the perception of the remainder of COVID-19 interruptions considered in this study (continuity of sales, liquidity, accessibility to funds and bankruptcy threat).

The remainder of this work is organized as follows. In the second section, we develop our hypotheses, by addressing the prior evidence on SMEs’ ability to manage the crisis. In the third section, we explain the research design and method, and in the fourth section, we present the results. In the fifth section we discuss our findings. The final section concludes.

2. Literature Review and Hypothesis Development

The COVID-19 pandemic outbreak is undoubtedly a catastrophic and destabilizing event that tests businesses’ resilience capabilities. The literature on COVID-19 shock and resilience is still evolving. In the stream of the literature relevant to this work, there is some first evidence on large and publicly listed firms (e.g., Acharya and Steffen 2020; Cheema-Fox et al. 2021; De Vito and Gómez 2020), as well as on SMEs (e.g., Cepel et al. 2020; Nurunnabi 2020; or Chudziński et al. 2020). However, there is a significant number of pre-COVID-19 works that revise SMEs’ resilience to various types of shock and provide rich evidence on SMEs’ vulnerability and agility in comparison to larger firms. In hypothesis development, we draw from this stream of the literature and their theoretical foundations. In particular, the existing literature on SMEs resilience follows the resource-based view and the related organizational flexibility (dynamic capabilities) and slack holdings. Somers (2009) pointed that organizational flexibility is essential for the preparation, response to and recovery from any turbulence that a business may face in its operating activities. Similarly, Gilbert (2005) and Denis (2011) found that firms fail when threatened with discontinuous changes due to resource scarcity or rigidity. Thus, to develop the theoretical background of our study we briefly refer to these concepts and review prior empirical evidence within (including the very recent COVID-19-related works), to address the specific features of SMEs and the discussion on what makes them more or less vulnerable to turbulence. In light of this evidence, we develop our research hypotheses.

2.1. Size

First of all, larger companies are entrusted with more resources than smaller ones, and larger firms enjoy a greater degree of slack resources (as measured in absolute terms), which are the key to agility. Slack resources are broadly defined as the excess of resources currently available on-demand (Cyert and March 1963; Nohira and Gulati 1996; Mishina et al. 2004). Slack resources serve corporate flexibility because in times of crisis they can be mobilized to absorb, inflict, or respond to turbulence (or shocks), allowing a firm to re-align with the changing environment (George 2005; Sanchez 1995; Dai and Kittilaksanawong 2014). In particular, the financial slack is relevant, as it safeguards the financial liquidity position. Some recent works have addressed this problem by revising the liquidity and equity shortfalls’ magnitude in the case of COVID-19, including the SME perspective (McGeever et al. 2020; Demmou et al. 2020; Carletti et al. 2020; Gourinchas et al. 2020; Cepel et al. 2020; Nurunnabi 2020). Additionally, very recently, Beninger and Francis (2021) have pointed out the importance of various types of slack resources to SMEs’ resilience in crisis. Overall, the lower slack holdings are perceived as the key reason behind the greater vulnerability of SMEs to any shock (Eggers 2020).

On the contrary, SMEs are perceived as less vulnerable to crisis if we consider their agility and flexibility to respond to a shock (Eggers 2020). The related evidence within is confirmed in various dimensions. Foss and Saebi (2017) concluded in their meta-analysis that the dynamic capabilities in managing a business model and the related processes lead to better monitoring of internal and external risks and uncertainties, anticipating potential consequences, and implementing actions. Smaller size and simpler organizational structure allow SMEs to modify quickly (Antony et al. 2008; Burnard and Bhamra 2011) and grow faster both in stable times and in crisis (Bartz and Winkler 2016). In addition, smaller firms are closer to the decision-makers and to their customers, as well as to other stakeholders (Eggers et al. 2012). This in turn provides them with quicker market information that can help them recover and adapt to a shock (Eggers 2020).

Overall, the brief review of the key points that are addressed in the existing literature on SMEs’ vulnerability to shocks leads to the conclusion that there are clearly identifiable advantages and disadvantages of SMEs, as compared to large firms. However, this evidence is missing the heterogeneity of SMEs in the context of business size, as we have in this group micro firms, small firms and medium-sized ones. Thus, we posit that amongst the SMEs as a group, we may observe differences in the vulnerability to COVID-19 shock (and the related interruptions), given the discrepancies in SME size. As the majority of evidence compares smaller firms with larger ones, among the SMEs we expect to detect some differences between the micro firms (as the smallest ones) and the small and medium-sized ones. Thus, our first hypothesis is as follows:

Hypothesis 1 (H1).

COVID-19 interruptions are perceived as more severe by micro firms.

2.2. Age

The literature also provides some interesting evidence on the resilience capabilities if we consider businesses’ age, as associated with the number of years of their market performance. In this aspect, we refer to “liability of newness” (Freeman et al. 1983), which means that new organizations face a greater risk of failure than older ones. The reasons behind this are the lack of established business models, low level of legitimacy or dependence on cooperation with strangers (Eggers 2020). The latter aspect (cooperation with strangers) refers to the importance of social capital, which is developed by firms over time; thus, more mature firms enjoy some benefits within this dimension. Pal et al. (2014) stated that social capital is one of the important building blocks of resilience capabilities. Social capital is developed and maintained through stakeholder relations (Maak 2007; Cots 2011), which may allow for more frequent, timely, and accurate information-sharing and problem-solving activities (Matos and Silvestre 2013). In this respect, more mature firms that operate on the market for a longer period of time are able to strengthen their social capital, and this could be supportive while facing any disturbances or turbulence in operating performance. There is some empirical evidence that SMEs’ survival and recovery from crisis is significantly dependent on their social capital. Torres et al. (2019) provide empirical evidence that small businesses that received benefits derived from social capital during the recovery from Hurricane Katrina were more likely to be economically resilient. Canhoto and Wei (2021) in their qualitative study focused on the hospitality industry in the COVID-19 outbreak found that through close relations with stakeholders, a business owner benefited from the social partners’ knowledge and from mapping their interests, and by taking these into consideration while developing recovery strategies. There is also some evidence that directly links businesses’ age with survival or growth in times of crisis, identifying visible disadvantages of younger firms. Bartz and Winkler (2016) demonstrated that during crisis younger firms show significantly lower growth than their respective peers. Facing this evidence, we posit that younger firms, as those facing the “liability of newness”, are more prone to negative COVID-19 impacts. Thus, our second hypothesis is as follows:

Hypothesis 2 (H2).

COVID-19 interruptions are perceived as more severe by younger firms.

2.3. Legal Form of the Business’ Operation

SMEs are also not homogenous if we consider the legal form of the businesses’ organization. The legal form is a specific feature of any firm that influences the liability of the owners, the tax status and the access to external funds. In firms organized as unlimited liability entities, the owners are liable up to the amount of their entire financial wealth. In other words, the firm owners’ bear the unlimited and ultimate financial responsibility for the business failure, while the owners of limited liability firms typically bear only the risk of losing the equity invested in the firm. Horvath and Woywode (2005) suggested that risk aversion is a key factor in choosing the liability status by the owners of the firms. The tax rate differences and cost of capital differences are less important in this context. They also found that limited liability firms are less likely to fail in total but more likely to fail by bankruptcy when they do fail. Additionally, they proved that limited liability firms are more likely to experience positive growth, in comparison to unlimited liability firms. However, this growth potential is linked to the risk-taking behavior of limited liability firms. As Hansmann and Kraakman (1991) stated, limited liability is acknowledged to create incentives for excessive risk-taking by permitting firms to avoid the full costs of their activities. Gollier et al. (1997) analyzed limited liability firms and their risk-taking behavior and proved that the optimal exposure to risk of the limited liability firm is always larger than under full liability. The literature evidence suggests that the differences in risk aversion stemming from the legal form of organization and the related limited or unlimited owners’ financial responsibility for the business collapse could be related to the perception of COVID-19 as more or less interruptive. The firms with limited liability may enjoy the advantage of holding (private) resources outside the firm and the owners may access these resources easily, if needed. Firms of unlimited liability may not hold this advantage and thus, feel more constrained while facing the tensions. Thus, in our third hypothesis, we posit that:

Hypothesis 3 (H3).

COVID-19 interruptions are perceived as more severe by firms that operate in legal forms that incorporate unlimited owners’ liability.

2.4. Family Ownership

It is very common that SMEs perform as family firms. Overall, there is rich evidence that family firms behave differently to non-family firms and that family firms remain more long-term oriented, less risk-taking (more conservative) and less concerned about the growth rate (Habbershon et al. 2003; Lubatkin et al. 2007; Kraus et al. 2020; Soluk et al. 2021). The existing literature evidence on how family firms differ from non-family ones if we consider the impact of crisis provides ambiguous results.

One stream of studies suggests that family firms perform better during crises than non-family firms. Amore et al. (2021) found out that Italian firms with controlling family shareholders fared significantly better than other firms during the COVID-19 pandemic. This effect is particularly strong for firms in which a family is both the controlling shareholder and holds the CEO position. Arregle et al. (2007) suggested that the presence of a family in the business is assumed to ensure stable and trusting long-lasting relationships with external and internal actors, accruing distinctive social capital. Additionally, Salvato et al. (2020) proved that the superior resilience of family firms was linked to the ability to seize posttraumatic entrepreneurial opportunities for recovery and growth.

On the other hand, Vlados et al. (2021) suggested that in economies where most firms are family-owned, there is a risk of poor management and problematic strategic and technological comprehension, which may undermine an economy’s ability to overcome economic crises through innovative and entrepreneurial thinking and adaptability. Soluk et al. (2021) found that an exogenous shock (such as COVID-19) further reinforces the family firms’ resource constraints and the family’s fear of losing their socioemotional wealth. Family-centered non-economic goals and ensuring preservation of socioemotional wealth are regarded as the primary drivers of decision-making in family businesses (De Massis and Rondi 2020). De Massis and Rondi (2020) stated also that COVID-19 and its aftermath are triggering challenges that, although potentially affecting any business, are particularly salient for family businesses. In this respect, it seems that family and non-family firms may differ in their perceptions of COVID-19’s impact. Thus, our fourth hypothesis is as follows:

Hypothesis 4 (H4).

COVID-19 interruptions are perceived as more severe by family firms.

3. Research Design and Method

3.1. Survey Design

The first cases of COVID-19 infections were officially confirmed in Poland on 4 March 2020, which was shortly after followed by the lockdown. The release of restrictions was a gradual procedure, and at the beginning of June 2020 businesses re-opened, although obliged to implement the required safety measures. Unfortunately, shortly after this the second wave of the pandemic was announced in October 2020 and the restrictions lasted till January 2021. In April 2021, despite the extensive vaccination program, Poland was facing the third wave of the pandemic (even more tragic concerning the number of infected and dead due to COVID-19) accompanied by severe restrictions and another period of economic lockdown. Thus, many businesses have already been closed for over a year with short periods of regular operating activity.

The prolonged disturbances of operating performance have led to the worsening of the macroeconomic conditions in Poland, as well as to the deterioration of the financial results of Polish enterprises. According to the macroeconomic data after the third quarter of 2020, there was a decrease in GDP (at 4.6%), private consumption (at 4.2%) and investments (at 10.6%), as compared to the results for the same period in 2019. In September 2020 the unemployment rate was 6.1% and the CPI increased by 3.6% (as compared to the previous year) (Ministerstwo Rozwoju 2020). On average, the Polish companies were affected by a decrease in sales revenues (at 5.3%), a decrease in EBIT (at 3.7%) and reduced investment activity (at 7%). The observed reduction in revenues was the greatest in 12 years and was primarily driven by the decrease in export (−10.6%) and domestic market sales (−3.7%) (Pekao 2020). The worsening of the financial results led to serious consequences including insolvency and bankruptcy. The total number of insolvencies of Polish enterprises in 2020 amounted to 1243 cases and was 22% higher as compared to 2019. The highest increase in the number of insolvencies was observed in services (at 54%), retail trade (at 39%) and transport (at 36%). As for the legal forms, it should be noted that 57% of simplified insolvency procedures concerned sole proprietorships (Coface 2021).

From the individual firm’s perspective, the ultimate impact of the COVID-19 risk and the related interruptions will be inevitably reflected in the accounting-based figures. If compared to prior operating performance and financial position, clear conclusions on the true and financially measurable COVID-19 impact could be drawn. However, it seems that in the meantime we are able to capture the COVID-19 interruptive power by running dedicated surveys. Inspired by the COVID-19 barometer surveys (Deloitte 2020; PwC 2020) and given the gap in capturing the country-specific settings and uniqueness of SMEs, we designed a survey composed of several sections, where the central issue was the COVID-19 impact. The remaining sections of the surveys addressed the SMEs’ business features, as well as their risk and corporate governance characteristics. However, in this paper, we report only the interruptive power of COVID-19 and the business features addressed above (size, age, and legal form that determines the owner’s financial responsibility for business failure).

The data collection was supported by a professional research agency (located at the University of Economics in Katowice), which supervised the proper survey design and ran the pilot study. Given the pandemic restrictions, the survey was distributed online, among 5005 randomly selected SME businesses, located in Poland. In return, we received 627 surveys; however, 89 were rejected as not conforming to the criteria of SMEs (the purged companies had 250 or more people). The response rate was 12.53%, which is very satisfactory given the online survey. Nevertheless, our results could be potentially biased, as firms may tend to hide the true dimension of the COVID-19 impacts, and the personal attitudes of the respondents (e.g., optimistic or pessimistic views) could be influential on the evaluation of difficulties. Moreover, firms suffering more COVID-19 difficulties could pay less attention to responding to the survey. However, we believe that the design of the survey (with a relatively short set of questions) and the professionalism of the research agency helped to limit this bias.

The survey was distributed among the respondents in January–February 2021. At that time, Poland had just completed the second wave of the COVID-19 hit, which was very dramatic, and the second phase of the lockdown restrictions. Thus, it could be assumed that businesses had been already familiarized with the COVID-19 impact on their performance. In other words, the surveyed firms were able to evaluate the real COVID-19 impacts more reasonably and less emotionally, in comparison to the state of anxiety that accompanied the first COVID-19 wave and lockdown.

While designing our study we decided to focus only on the selected COVID-19 impacts that were inspired by the former COVID-19 monitoring surveys and are also relatively intuitive if we imagine the business continuity interruptions following the fortuitous events. First of all, we included in our survey the set of questions that was directly tied to the nature of the disease. In this respect, we asked our respondents about the interruptions caused by the limited availability of workers, which was a natural consequence of the growing number of infections and imposed quarantines (following the evidence of, e.g., Moyo 2020 or Chudziński et al. 2020). We also asked the respondents about the interruptions caused by the additional burden of cost due to the implementation of the required safety measures (e.g., disinfection or the measures of workers’ protection).

The survey incorporated also a set of questions that were driven by financial performance-related aspects, induced by the lockdown or the changing economic conditions. More specifically, we asked the respondents about the impact on supply chains, ability to sustain continuity of production and sales. We also considered the possible worsening of the financial liquidity and the potentially limited accessibility of funds, as these aspects have been confirmed as relevant in the recent studies (De Vito and Gómez 2020; Chudziński et al. 2020).

With regard to each of these factors, the respondents were asked to answer the question “Did the COVID-19 pandemic results in difficulties in the following aspects of the firm’s performance?” For each interruptive factor listed in this question, the respondents were asked to answer by using the 7-point Likert scale, ranging from 1 (strongly disagree) to 7 (strongly agree). Additionally, we added one general question to control how far surveyed SMEs felt that COVID-19 threatens their survival, using the same scale for answers. In Table 1 we provide details concerning the questions asked in the first section of the survey.

3.2. Sample Composition: Businesses Characteristics

The sample characteristics and the related variables we controlled in our study are outlined in Table 2. Our sample was relatively balanced if we consider the size of the surveyed firms. Small firms (with 10–49 workers) composed 39% of our sample, followed by 34% of micro firms (with employment up to 9 persons) and 27% of medium firms (employing 50–249 persons). The sample was also relatively balanced if we consider the age of the firms. Nearly 16% of the respondents were in their infancy, in operation for up to 5 years, and 25% of the respondents declared to have been operating for between 6 and 10 years. Altogether, the young firms composed 41.5% of the sample. In our further analysis, we controlled the firms in infancy and the young firms as separated groups (AGE_1) and as one group (AGE_2). The firms with 11 to 20 years of market operation composed 35% of our sample and were classified as intermediate. Finally, 24% of respondents were classified as mature firms, operating for 21 years or more.

Our sample was also controlled with reference to the legal form of business organization to draw conclusions on the owners’ financial responsibility. The sample was balanced if we consider the percentage of firms that perform in legal forms that impose unlimited legal liability and the related full owner’s financial responsibility (49.4%) and those where this responsibility is isolated (limited liability) (50.6%). More specifically, as the firms of limited liability, we classified the firms that perform as limited liability companies (LLC); all others were classified as non-LLCs. This dichotomous approach was controlled as the first criterion of the owner’s financial responsibility (OWN_1). However, the firms classified as those of full owner’s financial responsibility (non-LLC) were not homogenous, if we consider the legal form of their organization. More specifically, the majority of non-LLCs operated as sole proprietorships (SP) and composed 36% of our sample. There were 14% of non-LLCs that operated as partnerships but with the unlimited financial responsibility of the owners (so-called civil law partnerships, hereafter CP). Thus, in our analysis, we additionally controlled for this expanded classification of the owner’s financial responsibility (OWN_2). Finally, 31% of our respondents declared to run a family business.

In Appendix A we provide the contingencies between the firm characteristics of our sample. Overall, between all categories of interest (size, age, legal form and family ownership) we observed statistically significant contingencies (as confirmed with Pearson’s chi-squared tests), with the exception of firm’s age and family ownership. This was not surprising, however, given the natural routes of business growth—the newly established firms commonly begin to operate as sole proprietorships and tend to change the legal form of operation to a partnership, as they grow in size over time. This pattern is confirmed in our sample, as for instance we observe that among the micro firms there were 72.1% infants, 68.7% operating as sole proprietors, and 52.7% declared to be family firms. In addition, nearly 55% of the family firms in our sample operate as sole proprietors.

3.3. Method

At the first stage of the empirical investigations, we incorporated analysis of variance (ANOVA) to test whether there are statistically significant differences in the perception of the COVID-19 interruptions between the groups of companies, given their business characteristics (Size, AGE_1, AGE_2, OWN_1, OWN_2 and FAM). As our variables are not normally distributed (see Appendix B), we applied the non-parametric ANOVA (Kruskal–Wallis test). Further, to capture the consolidated effect of the COVID-19 impacts, we clustered the firms by applying the k-means clustering algorithm. Overall, the k-means rank method gives freedom to define the number of clusters and is useful in classifying the objects by their means. K-means clustering minimizes within-cluster variances (squared Euclidean distances, to obtain the intergroup homogeneity) (Everitt et al. 2011). To optimize the number of clusters in our analysis, we controlled the group means of the COVID-19 interruptive factors, to identify the clusters of low, moderate and high COVID-19 impact. To add robustness to our results, we controlled the aggregated COVID-19 impact to capture which business characteristics emerged to be relevant.

4. Results

4.1. The COVID-19 Interruptions and Business Characteristics

In Table 3 we present the summary of the results of non-parametric ANOVA, to highlight the interesting pattern that emerges from the analysis of the differences between the COVID-19 interruptions, given the business characteristics of interest. In our discussion of these findings, we will refer to the graphical illustration of mean ranks of COVID-19 impacts presented in Figure 1, Figure 2, Figure 3, Figure 4 and Figure 5, for each business characteristic related variable subject to this study. We will also address the most relevant message behind the pair-wise comparisons for the Kruskal–Wallis test, which is presented in Appendix B.

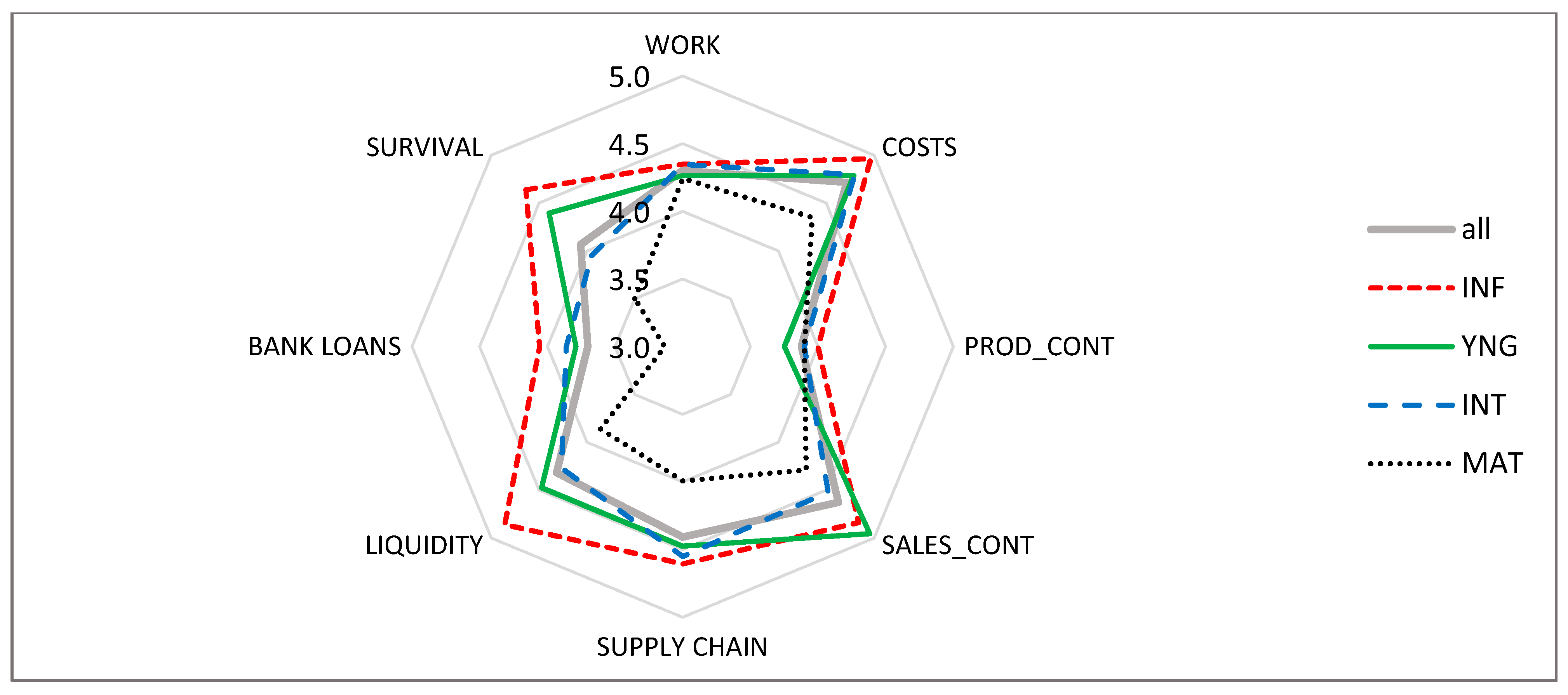

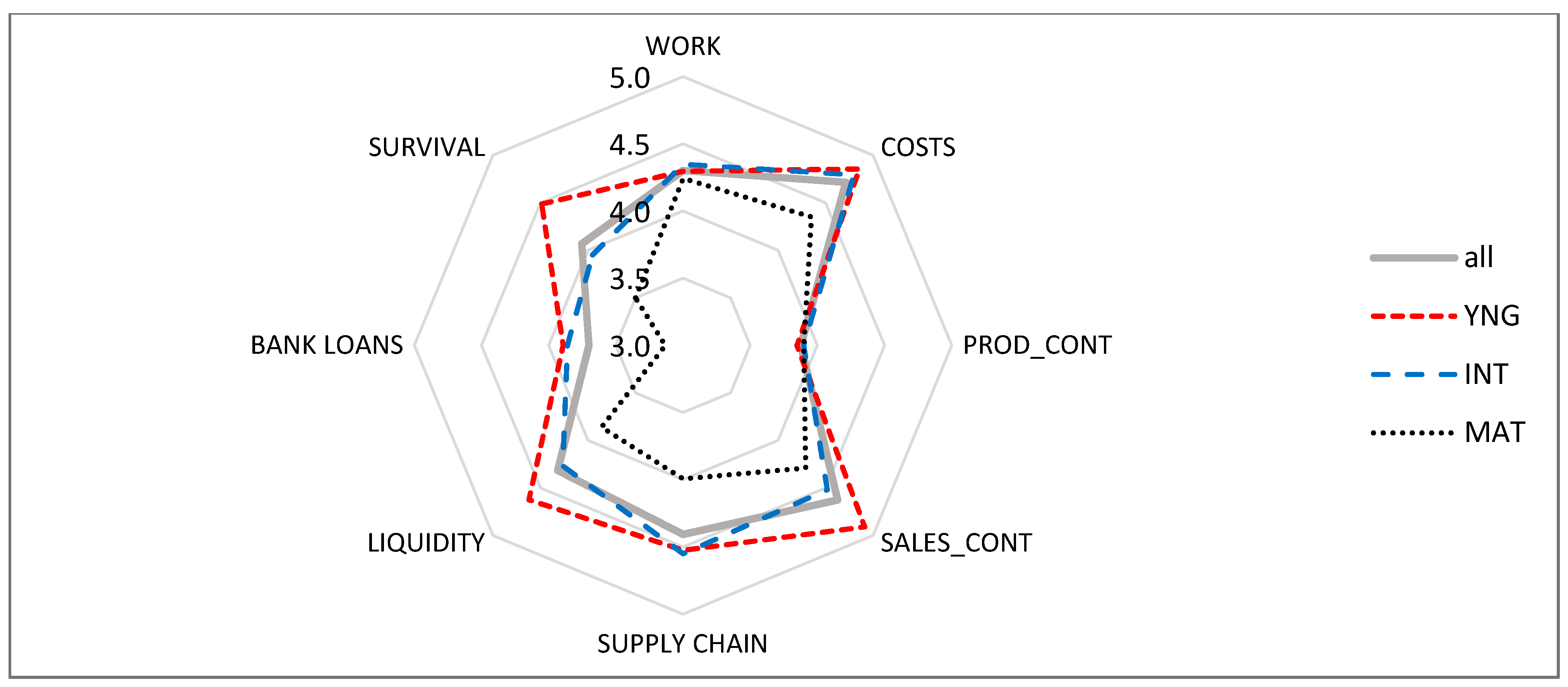

We find evidence that the size is influential on the perception of the COVID-19 interruptions related to the increase in operating costs, ability to continue sales, worsening of financial liquidity, access to bank loans and the overall threat for the business survival. Data provided in Figure 1 indicate that micro firms perceived these interruptions as more severe in comparison to the small and medium-sized firms, and the pair-wise comparisons confirm these differences to be statistically significant. We do not find evidence that the interruptions related to the limited accessibility of workers, ability to continue production and supply chain problems were statistically significant, which suggests that these channels of interruption have equally influenced companies, regardless of their size. Data provided in Figure 1 indicate that these interruptions were evaluated by the respondents as close to the mean ranks.

We also find evidence that age is influential on the perception of the COVID-19 impact in a similar vein as in the case of the business size, except for supply chain problems, which were found to be statistically significant as well. The pair-wise comparisons indicate that these differences are statistically significant if we compare very young firms (up to 10 years of operation or firms in their infancy with up to 5 years of operation) and the mature firms that operate for 21 years or more. Data presented in Figure 2 graphically illustrate the mean ranks assigned to COVID-19-related interruptions among the firms within the four criteria of age (AGE_1). The firms in infancy (up to 5 years) have evaluated these interruptions as more severe than the young firms, except for continuity of sales, which was perceived as more problematic in young firms than in the infant ones.

Data provided in Figure 3 illustrate the mean ranks assigned to COVID-19-related interruptions among the firms within the three criteria of age (AGE_3). This visualization clearly communicates that the very young firms perceived the inability to continue sales, worsening of liquidity and the overall threat to their survival as much more severe than the remaining two age groups. The data in Figure 2 and Figure 3 illustrate also that the mature firms evaluated the interruptions related to lower accessibility of bank loans and the overall threat to the business survival as much lower, in comparison to the intermediate and young firms. We find no statistical significance for the interruptions in the accessibility of workers and the abilities to continue production, which suggests that firms of different ages perceived these issues as of similar impact. The graphical illustration presented in Figure 2 and Figure 5 indicates that these interruptions were relatively comparable with c.a. 4.3 mean rank for accessibility of workers and c.a. 3.8 for continuity of production.

We also find evidence that the firms of different owners’ financial responsibility (and the related legal form of operation) vary with the perceptions of the COVID-19-related interruptions manifested by the increase in costs, ability to continue sales, worsening of financial liquidity, limited access to bank loans and the overall threat to the business survival. The pair-wise comparisons indicate that these differences are statistically significant between LLCs and non-LLCs, which is illustrated in Figure 4 and Figure 5. Overall, non-LLCs assigned visibly higher ranks to these channels of COVID-19 interruptions in comparison to LLCs, with the highest impact being the increase in operating costs. Interestingly, we find that there are also statistically significant differences in the perception of these issues if we compare the two groups of non-LLCs where the owners’ liability is not limited, namely between sole proprietorships and partnerships based on civil law regulations. This evidence suggests that the businesses operating as partnerships (regardless of the effect of limited or unlimited responsibilities of the owners) perceived the cost, sales or financial situation-related COVID-19 interruptions as of lower impact. We find no statistical differences for the accessibility of workers, continuity of sales and destabilization in supply chains, which suggests that these interruptions are perceived as of equal impact regardless of the legal form of businesses organization. However, supply chain problems and accessibility of workers were on average assigned higher scores (of c.a. 4.4 and 4.3, respectively), in comparison to the ability to continue production (with mean ranks of c.a. 3.8).

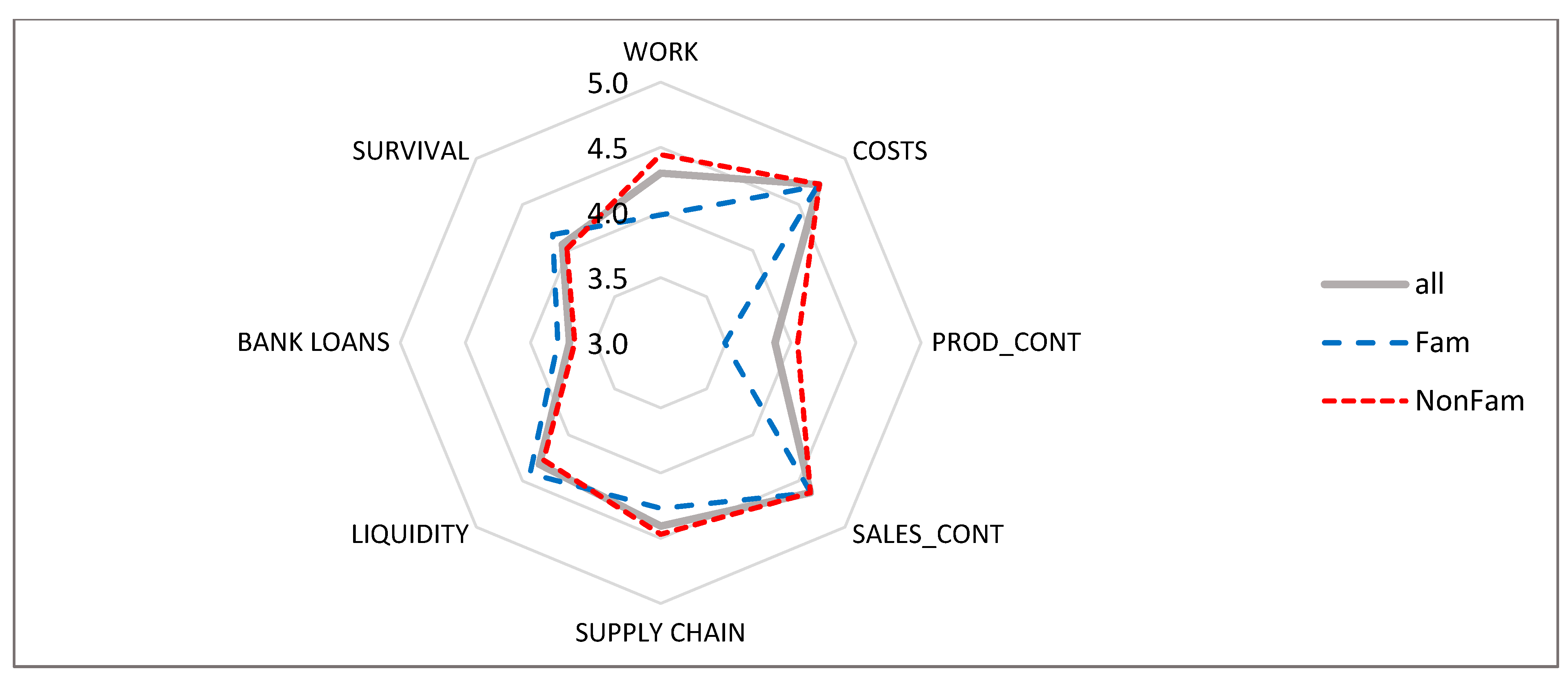

Finally, we study the differences in the perception of the COVID-19 interruptions between family and non-family businesses. Interestingly, family businesses differ statistically significantly from non-family ones only if we consider the accessibility of workers and the ability to continue production. Data provided in Figure 6 clearly indicate that these COVID-19-related interruptions were perceived as of greater impact in the non-family businesses. This is an interesting observation that suggests that family businesses are less dependent on the external workforce and thus, the ability to continue production is more manageable. Noticeably, family businesses assigned on average the lowest ranks to these two interruption channels, in comparison to the mean ranks for other interruptions considered in this study. We find no statistically significant differences for the remaining types of interruptions, which suggests that these have an equal impact on family and non-family firms.

4.2. Consolidated COVID-19 Effect

The next stage of our empirical analysis assumed the application of clustering (k-means method) to classify firms by the intensity of COVID-19 interruptions stemming from the consolidated view of the interruptive factors considered in our survey. The application of k-means clustering has led to the reasonable distinction of three clusters of interruptions: high, moderate and low. In Table 4 we provide the results of clustering.

In Table 5 we report the results of non-parametric ANOVA to detect the statistical significance of the differences between the clusters of low, moderate and high COVID-19 interruptions and the business characteristics considered in this work. We provide also information on the results of pair-wise comparisons and the mean ranks of the Kruskal–Wallis test. First of all, we find that there are statistically significant differences in the overall evaluation of the COVID-19 interruptions for firms of different ages and owners’ financial responsibility. The mean ranks of the Kruskal–Wallis test indicate that in the cluster of low COVID-19 interruptions there were the more mature firms, the firms that perform as LLCs and the small firms that employ 49–250 workers (although this effect is not statistically significant).

To confirm the observed interdependencies, we additionally performed linear multiple regression analysis. Our dependent variable was a summary of the scores assigned by each respondent to particular COVID-19 impacts considered in this study (COVID-19 score), and as independent variables we employed SIZE, AGE_1, OWN_2, and FAM. The results are reported in Appendix B, Table 3. Although the R-squared is low (0.053), the coefficients are statistically significant for age and ownership ( and , respectively). The negative signs confirm that the overall COVID-19 impact is perceived as lower by more mature firms and the firms that operate with a greater level of limited liability. The size effect and family business effects are not significant, consistent with ANOVA results.

5. Discussion

This study was designed to report the impact of COVID-19 on SMEs’ performance, given their unique business-specific characteristics and controlling isolated country settings. Our first hypothesis stated that COVID-19 interruptions are perceived as more severe by micro firms. This hypothesis finds some support if we consider particular channels of interruptions. Micro firms differed significantly from small and medium-sized firms if we consider their perceptions of the severity of interruptions caused by an increase in costs, continuity of sales, worsening of financial liquidity, accessibility of bank loans and the overall threat to their survival. However, there were no statistically significant differences between small and medium-sized firms. It clearly suggests that micro firms perceived these COVID-19 impacts as more severe and, in this regard, confirms prior evidence of greater vulnerabilities of smaller firms to a shock (Eggers 2020). However, if we consider the aggregated/consolidated impact of COVID-19 (all factors together) there is a weak significance (at 10%) of the evidence that firms classified as high/moderate/low differ with the size.

Our second hypothesis stated that COVID-19 interruptions are perceived as more severe by younger firms. This hypothesis found strong support in our survey. First of all, we observed statistically significant differences between the firms in infancy (up to 5 years of operation) or young ones (6–10 years of operation) and the mature firms (21 years or more) with regard to financial issues: worsening of financial liquidity, lowered accessibility of bank loans or overall threat of the survival (bankruptcy threat). A slightly less statistically significant effect was observed in the interruptions related to the increase in costs, continuity of sales and supply chains. Given the consolidated effect of COVID-19 impacts, we found that the firms of low, moderate and high COVID-19 impact differed significantly if we consider a firm’s age. In particular, we found that firms classified as those of lower COVID-19 impact were the more mature ones. This evidence confirms the effect of “liability of newness” (Freeman et al. 1983) and the related greater exposure to risk and interruptions in smaller firms.

Our third hypothesis stated that COVID-19-related interruptions are perceived as more severe by the firms in which owners hold unlimited financial responsibility for the collapse of their businesses. This hypothesis also found strong evidence. First of all, given the particular factors of COVID-19 interruptions, there were statistically significant differences between firms of limited (LLCs) and unlimited liability (non-LLCs) if we consider additional costs, continuity of sales, worsening of liquidity, lower accessibility of bank loans and overall threat to business survival. The analysis of Kruskal–Wallis test mean ranks indicated that the perception of these problems was much lower in LLCs as compared to non-LLCs. Interestingly, we also found that sole proprietorships (which belong to non-LLCs) declared to be more exposed to the COVID-19 impacts. Similar conclusions could be drawn if we look at the consolidated impact of COVID-19 interruptions. In the cluster of firms of low impact, the LLCs were prevalent at a statistically significant level. This supports the former evidence that the legal form of organization and the related limited or unlimited owners’ financial responsibility for the business collapse is related to the perception of the risks induced by external shocks (Hansmann and Kraakman 1991; Gollier et al. 1997).

Our fourth hypothesis stated that COVID-19 interruptions are perceived as more severe by family firms. However, this hypothesis found no support and provides empirical evidence that does not support the view that family firms differ from non-family ones if the crisis or resilience to shock is considered, which is contrary to the findings of a more et al. (2021), Salvato et al. (2020), and Soluk et al. (2021). First, we observed that statistically significant differences were confirmed between family and non-family firms only in the case of the perception of limited availability of workers and ability to continue production. The remaining channels of COVID-19 interruptions impacted family and non-family businesses in a similar vein. These findings were confirmed with consolidated COVID-19 impacts, as the differences between the clusters of low, moderate and high interruptions for family and non-family firms were found to be statistically insignificant.

6. Conclusions

6.1. Practical Implications

In this work, we studied several channels of COVID-19 interruptions from the perspective of SMEs operating in Poland. We considered here several aspects that were confirmed as relevant in the prior COVID-19 monitoring surveys and stem from the direct impact of the disease (availability of workers or supply chain destabilization due to lockdown restrictions), as well as the less direct impact that is induced by consumer behavior (e.g., continuity of sales) or the worsening of businesses’ financial liquidity or emerging financial constraints (accessibility of bank loans). Our study was motivated primarily by the lack of COVID-19 monitoring studies considering SMEs exclusively and focusing on SMEs’ heterogeneity in particular.

In the practical dimension, our study provides some evidence that could be relevant to policy-makers. First of all, we have demonstrated that the SME sector lacks homogeneity in the perceptions of COVID-19 impacts. This suggests that interventions and supportive schemes need to consider the individual features of particular firms, rather than considering purely their size. Second, our study indicates that the examined firms differed in their perceptions of COVID-19’s impacts, depending on the problem-oriented perspective. This evidence suggests that the surveyed SMEs were concerned about additional costs that will impact their financial performance and financial standing. At the same time, the surveyed firms were concerned about liquidity shortfalls and the bankruptcy threat. The access to external funding (that could help to sustain liquidity shortfalls) is dependent on a firm’s performance. Thus, it seems that in practical terms the enhancement of external funding opportunities for SMEs should be the subject of intervention, to remove existing financial constraints and dismiss the waves of bankruptcy among SMEs.

6.2. Further Works

Our study also leads to several important observations and related paths of the possible further investigations. First of all, the impact of COVID-19 on family firms needs a deeper revision. Our study has found strong evidence that only two out of eight interruptive factors were differently perceived by family and non-family businesses. At the same time, these factors were statistically insignificant given the business size, age or owner’s financial responsibility, as driven by the legal form of the business. It suggests that family firms may have a different perception of the COVID-19 impacts and related anxieties. Possibly, other corporate governance-related features of SMEs may emerge as informative as well. In this respect, further works could shed some light on the importance of the roles and duties of board members, their strategic thinking, or implemented control mechanisms.

Secondly, further inquiries are needed to confirm the strong evidence for the age effect, as well as the size effect. The former literature on the impact of the crisis on SMEs has indicated that size matters. However, our evidence suggests that the pandemic as the cause of the crisis could differ from other possible economic crises the SMEs may face. Moreover, this study suggests that the consideration of different “sizes” of SMEs could be influential on crisis perception and, possibly, the related resilience capabilities. Finally, the country settings (and the related institutional settings) could be influential on the perception of pandemic-related anxieties.

In our study, we did not control for the industry, which is one of its important limitations. However, reliable control of this factor could be difficult in online surveys. It seems that inquiries focused on the single-sector level will bring more substantial results. One of the questions included in our survey was designed to control for the overall COVID-19-related threat (the question on threats to survival). Additionally, we assumed that COVID-19 was interruptive to some extent for each business, although some businesses suffered more, while others encountered some opportunities (given the scope of their performance).

Finally, we have found that the perceptions of the impact of financially driven factors (worsening of liquidity, lower availability of bank loans and overall threat of bankruptcy) were strongly statistically significant if we consider firms’ size, age and owners’ financial responsibility. This suggests that further studies need to revise these aspects more in-depth. In particular, given that our study was conducted at the peak of the second wave of the pandemic in Poland and the second phase of lockdown, this evidence could indicate the first symptoms of worsening of a firm’s financial situation. In particular, the research on micro firms is relevant, as these were found in our study to be more exposed to the consequences of COVID-19 interruptions. Further works could contribute significantly to this debate, by examining the symptoms of the liquidity constraints, monitoring the signals of bankruptcy threat, or the overall worsening of financial position, both from the micro and macro perspective.

Author Contributions

Conceptualization, M.W.-K.; methodology, M.W.-K., software, M.W.-K., formal analysis, J.B., A.D. and M.W.-K.; writing—original draft preparation, J.B., A.D. and M.W.-K., writing—review and editing, J.B., A.D. and M.W.-K.; supervision, M.W.-K.; project administration, M.W.-K. All authors have read and agreed to the published version of the manuscript.

Funding

The APC was funded by the University of Economics in Katowice.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data archived by the authors.

Acknowledgments

We gratefully acknowledge the three anonymous Reviewers and the participants of the 2nd Accounting and Accountability in Emerging Economies (AAEE) Conference (28–30 June 2021) for the insightful comments on this study.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Contingencies between the examined firm characteristics.

| SIZE | |||||||||||

| Micro | Small | Medium | in Total | ||||||||

| N | % | N | % | N | % | N | % | ||||

| AGE_1 | infant | 62 | 72.1% | 21 | 24.4% | 3 | 3.5% | 86 | 100% | ||

| X2: 129.390 *** | young | 59 | 43.1% | 61 | 44.5% | 17 | 12.4% | 137 | 100% | ||

| Cont.: 0.440 *** | itermediate | 47 | 25.1% | 78 | 41.7% | 62 | 33.2% | 187 | 100% | ||

| mature | 14 | 10.9% | 48 | 37.5% | 66 | 51.6% | 128 | 100% | |||

| In total | 182 | 33.8% | 208 | 38.7% | 148 | 27.5% | 538 | 100% | |||

| OWN_1 | SP | 134 | 68.7% | 52 | 26.7% | 9 | 4.6% | 195 | 100% | ||

| X2: 193.328 *** | LCC | 20 | 7.5% | 118 | 44.4% | 128 | 48.1% | 266 | 100% | ||

| Cont.: 0.514 *** | CP | 28 | 36.4% | 38 | 49.4% | 11 | 14.3% | 77 | 100% | ||

| In total | 182 | 33.8% | 208 | 38.7% | 148 | 27.5% | 538 | 100% | |||

| FAM | family | 88 | 52.7% | 56 | 33.5% | 23 | 13.8% | 167 | 100% | ||

| X2: 43.738 *** | non-family | 94 | 25.3% | 152 | 41.0% | 125 | 33.7% | 371 | 100% | ||

| Cont.: 0.247 *** | In total | 182 | 33.8% | 208 | 38.7% | 148 | 27.5% | 538 | 100% | ||

| AGE_1 | |||||||||||

| Infant | Young | Intermediate | Mature | in Total | |||||||

| N | % | N | % | N | % | N | % | N | % | ||

| OWN_1 | SP | 59 | 30.3% | 66 | 33.8% | 55 | 28.2% | 15 | 7.7% | 195 | 100% |

| X2: 76.817 *** | LCC | 15 | 5.6% | 51 | 19.2% | 106 | 39.8% | 94 | 35.3% | 266 | 100% |

| Cont.: 0.353 *** | CP | 12 | 15.6% | 20 | 26.0% | 26 | 33.8% | 19 | 24.7% | 77 | 100% |

| In total | 86 | 16.0% | 137 | 25.5% | 187 | 34.8% | 128 | 23.8% | 538 | 100% | |

| FAM | family | 29 | 17.4% | 42 | 25.1% | 66 | 39.5% | 30 | 18.0% | 167 | 100% |

| X2: 5.335 | non-family | 57 | 15.4% | 95 | 25.6% | 121 | 32.6% | 98 | 26.4% | 371 | 100% |

| Cont.: 0.099 | In total | 86 | 16.0% | 137 | 25.5% | 187 | 34.8% | 128 | 23.8% | 538 | 100% |

| OWN_1 | |||||||||||

| SP | LCC | CP | in Total | ||||||||

| N | % | N | % | N | % | N | % | ||||

| FAM | family | 91 | 54.5% | 41 | 24.6% | 35 | 21.0% | 167 | 100% | ||

| X2: 60.026 *** | non-family | 104 | 28.0% | 225 | 60.6% | 42 | 11.3% | 371 | 100% | ||

| Cont.: 0.317 *** | In total | 195 | 36.2% | 266 | 49.4% | 77 | 14.3% | 538 | 100% | ||

Notes: X2 denotes the statistics of Pearson’s chi-squared test; Cont. denotes the values of contingency ratios between the variables; statistically significant at *** α = 0.001; the names of the variables and the related explanation—see in Table 2.

Appendix B

Table A2.

Tests of normality distribution.

| Variables | Kołmogorov–Smirnov | Shapiro–Wilk | ||||

|---|---|---|---|---|---|---|

| Statistic | df | Sig. | Statistic | df | Sig. | |

| WORK | 0.192 | 538 | 0.000 | 0.917 | 538 | 0.000 |

| COSTS | 0.194 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| PROD_CONT | 0.152 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| SALES_CONT | 0.177 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| SUPPLY CHAIN | 0.189 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| LIQUIDITY | 0.167 | 538 | 0.000 | 0.925 | 538 | 0.000 |

| BANK LOANS | 0.168 | 538 | 0.000 | 0.936 | 538 | 0.000 |

| SURVIVAL | 0.193 | 538 | 0.000 | 0.929 | 538 | 0.000 |

Table A3.

Pair-wise comparisons for Kruskal–Wallis test.

| Variables | WORK | COSTS | PROD _CONT | SALES _CONT | SUPPLY CHAIN | LIQ | BANK LOANS | SURV |

|---|---|---|---|---|---|---|---|---|

| SIZE | 0.188 | 0.000 *** | 0.411 | 0.001 ** | 0.644 | 0.000 *** | 0.002 ** | 0.000 *** |

| small-medium | 1.000 | 1.000 | 0.058 | 0.156 | 0.162 | |||

| small-micro | 0.000 *** | 0.004 ** | 0.000 *** | 0.001 ** | 0.000 ** | |||

| medium-micro | 0.006 ** | 0.009 ** | 0.000 *** | 0.211 | 0.001 ** | |||

| AGE_1 | 0.970 | 0.021 * | 0.823 | 0.017 * | 0.012 * | 0.000 *** | 0.000 *** | 0.000 *** |

| mat-young | 0.237 | 0.032 * | 0.108 | 0.017 * | 0.000 *** | 0.000 *** | ||

| mat-interm | 0.082 | 1.000 | 0.024 * | 0.189 | 0.000 *** | 0.071 | ||

| mat-inf | 0.027* | 0.132 | 0.034 * | 0.000 *** | 0.000 *** | 0.000 *** | ||

| young-interm | 1.000 | 0.269 | 1.000 | 1.000 | 1.000 | 0.059 | ||

| young-inf | 1.000 | 1.000 | 1.000 | 0.611 | 1.000 | 1.000 | ||

| interm-inf | 1.000 | 0.722 | 1.000 | 0.048 * | 1.000 | 0.009 ** | ||

| AGE_2 | 0.924 | 0.013 * | 0.925 | 0.006 ** | 0.005 ** | 0.000 *** | 0.000 *** | 0.000 *** |

| mat-interm | 0.041 * | 0.924 | 0.012 * | 0.095 | 0.000 *** | 0.036 | ||

| mat-young | 0.016 * | 0.008 ** | 0.009 ** | 0.000 *** | 0.000 *** | 0.000 *** | ||

| interm-young | 1.000 | 0.087 ** | 1.000 | 0.109 | 1.000 | 0.002 ** | ||

| OWN_1 | 0.283 | 0.000 *** | 0.252 | 0.001 ** | 0.385 | 0.000 *** | 0.000 *** | 0.000 *** |

| OWN_2 | 0.326 | 0.000 *** | 0.266 | 0.002 ** | 0.077 | 0.000 *** | 0.000 *** | 0.000 *** |

| LLC-CP | 1.000 | 0.735 | 0.623 | 0.544 | 1.000 | |||

| LLC-SP | 0.000 *** | 0.001 ** | 0.000 *** | 0.000 *** | 0.000 *** | |||

| CP-SP | 0.008 ** | 0.511 | 0.003 ** | 0.020 * | 0.000 *** | |||

| FAM | 0.004 ** | 0.858 | 0.001 ** | 0.83 | 0.196 | 0.378 | 0.308 | 0.366 |

Notes: statistically significant at: *** α = 0.001; ** α = 0.01; * α = 0.05.

Table A4.

OLS regression results for consolidated COVID-19 effect.

| st.err | t | Sig. | ||

|---|---|---|---|---|

| Intercept | 43.271 *** | 2.024 | 21.377 | 0.000 |

| SIZE | −1.074 | 0.662 | −1.622 | 0.105 |

| AGE_1 | −0.960 * | 0.483 | −1.988 | 0.047 |

| OWN_2 | −1.865 ** | 0.676 | −2.758 | 0.006 |

| FAM | 1.395 | 0.957 | 1.457 | 0.146 |

| R-squared = 0.053 Adj. R-squared = 0.046 F = 7.403 *** | ||||

Notes: dependent variable COVID-19 score (summary of the scores assigned by each respondent to the particular COVID-19 impacts); statistically significant at *** α = 0.001; ** α = 0.01; * α = 0.05.

References

- Acharya, Viral, and Sascha Steffen. 2020. The risk of being a fallen angel and the corporate dash for cash in the midst of COVID. The Review of Corporate Finance Studies 9: 430–71. [Google Scholar] [CrossRef]

- Amore, Mario Daniele, Fabio Quarato, and Valerio Pelucco. 2021. Family Ownership during the COVID-19 Pandemic. SSRN Electronic Journal 1–38. [Google Scholar] [CrossRef]

- Antony, Jiju, Maneesh Kumar, and Ashraf Labib. 2008. Gearing Six Sigma into UK manufacturing SMEs: Results from a pilot study. Journal of the Operational Research Society 59: 482–93. [Google Scholar] [CrossRef]

- Arregle, Jean-Luc, Michael. A. Hitt, David G. Sirmon, and Philippe Very. 2007. The development of organizational social capital: Attributes of family firms. Journal of Management Studies 44: 73–95. [Google Scholar] [CrossRef]

- Bartik, Alexander W., Marianne Bertrand, Zoë B. Cullen, Edward L. Glaeser, Michael Luca, and Chirstopher T. Stanton. 2020a. How Are Small Businesses Adjusting to COVID-19? Early Evidence from a Survey (No. w26989). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Bartik, Alexander. W., Marianne Bertrand, Zoë B. Cullen, Edward L. Glaeser, Michael Luca, and Chirstopher T. Stanton. 2020b. The impact of COVID-19 on small business outcomes and expectations. Proceedings of the National Academy of Sciences 117: 17656–66. [Google Scholar] [CrossRef]

- Bartz, Wiebke, and Adalbert Winkler. 2016. Flexible or fragile? The growth performance of small and young businesses during the global financial crisis—Evidence from Germany. Journal of Business Venturing 31: 196–215. [Google Scholar] [CrossRef]

- Beninger, Stefanie, and June N. Francis. 2021. Resources for Business Resilience in a COVID-19 World: A Community-Centric Approach. Business Horizons 1–28. [Google Scholar] [CrossRef]

- Bognini, Paola, Małgorzata Iwanicz-Drozdowska, Oliviero Roggi, and Viktor Elliot. 2020. Global Report on Business Continuity Planning and Management (BCP/BCM). Survey Results. Available online: https://ssrn.com/abstract=3764401 (accessed on 1 July 2021).

- Burnard, Kevin, and Ran Bhamra. 2011. Organisational resilience: Development of a conceptual framework for organisational responses. International Journal of Production Research 49: 5581–99. [Google Scholar] [CrossRef]

- Canhoto, Anna, and Liyuan Wei. 2021. Stakeholders of the World, Unite!: Hospitality in the time of COVID-19. International Journal of Hospitality Management 102922. [Google Scholar] [CrossRef]

- Carletti, Elena, Tommaso Oliviero, Marco Pagano, Loriana Pelizzon, and Marti G. Subrahmanyam. 2020. The COVID-19 shock and equity shortfall: Firm-level evidence from Italy. The Review of Corporate Finance Studies 9: 534–68. [Google Scholar] [CrossRef]

- Cepel, Martin, Beata Gavurova, Jan Dvorsky, and Jaroslav Belas. 2020. The impact of the COVID-19 crisis on the perception of business risk in the SME segment. Journal of International Studies 13: 248–63. [Google Scholar] [CrossRef] [PubMed]

- Cheema-Fox, Alex, Bridget LaPerla, George Serafeim, and Hui Wang. 2021. Corporate Resilience and Response during COVID-19. Harward Business School Working Paper No 20-108. Available online: https://www.hbs.edu/ris/Publication%20Files/20-108_6f241583-89ac-4d2f-b5ba-a78a4a17babb.pdf (accessed on 1 July 2021).

- Chudziński, Paweł, Szymon Cyfert, Wojcieh Dyduch, and Maciej Zastempowski. 2020. Projekt Sur(vir)val: Czynniki przetrwania przedsiębiorstw w warunkach koronakryzysu. E-mentor 5: 34–44. [Google Scholar] [CrossRef]

- Coface. 2021. Raport Roczny Coface: Niewypłacalności firm w Polsce w 2020 Roku. Available online: http://img.go.coface.com/Web/COFACE/%7B635f800d-875e-49d9-96b9-c9eff82dff87%7D_Niewyplacalnosci_w_Polsce_w_2020_ROCZNY_Raport_Coface_ok.pdf (accessed on 1 July 2021).

- Cots, Elisabet Garriga. 2011. Stakeholder social capital: A new approach to stakeholder theory. Business Ethics: A European Review 20: 328–41. [Google Scholar] [CrossRef]

- Cyert, Richard M., and James G. March. 1963. A Behavioral Theory of the Firm. Hoboken: Prentice Hall. [Google Scholar]

- Dai, Weiqi, and Wiboon Kittilaksanawong. 2014. How are different slack resources translated into firm growth? Evidence from China. International Business Research 7: 1–12. [Google Scholar] [CrossRef] [Green Version]

- Davidsson, Per. 2017. Opportunities, propensities, and misgivings: Some closing comments. Journal of Business Venturing Insights 8: 123–24. [Google Scholar] [CrossRef] [Green Version]

- De Massis, Alfredo, and Emanuela Rondi. 2020. COVID-19 and the Future of Family Business Research. Journal of Management Studies 57: 1727–31. [Google Scholar] [CrossRef]

- De Vito, Antonio, and Juan-Pedro Gómez. 2020. Estimating the COVID-19 cash crunch: Global evidence and policy. Journal of Accounting and Public Policy 39: 106741. [Google Scholar] [CrossRef]

- Deloitte. 2020. Deloitte Global Cost and Enterprise Transformation Survey. Available online: https://www2.deloitte.com/us/en/pages/about-deloitte/articles/press-releases/deloitte-covid-19-survey-shifts-cost-strategies.html (accessed on 5 October 2020).

- Demmou, Lilas, Guido Franco, Sara Calligaris, and Dennis Dlugosch. 2020. Corporate Sector Vulnerabilities during the COVID-19 Outbreak: Assessment and Policy Responses. VoxEU. org. May 23. Available online: https://voxeu.org/article/corporate-sector-vulnerabilities-during-covid-19-outbrea (accessed on 1 July 2021).

- Denis, David J. 2011. Financial flexibility and corporate liquidity. Journal of Corporate Finance 17: 667–74. [Google Scholar] [CrossRef]

- Didier, Tatiana, Fuderico Huneeus, Mauricio Larrain, and Sergio Schmukler. 2021. Financing Firms in Hibernation during the COVID-19 Pandemic. Journal of Financial Stability 53: 1–14. [Google Scholar] [CrossRef]

- Eggers, Fabian. 2020. Masters of disasters? Challenges and opportunities for SMEs in times of crisis. Journal of Business Research 116: 199–208. [Google Scholar] [CrossRef]

- Eggers, Fabian, David J. Hansen, and Amy E. Davis. 2012. Examining the relationship between customer and entrepreneurial orientation on nascent firms’ marketing strategy. International Entrepreneurship and Management Journal 8: 203–22. [Google Scholar] [CrossRef]

- European Commission. 2019. 219 SBA Fact Sheet Poland. Available online: https://ec.europa.eu/docsroom/documents/38662/attachments/22/translations/en/renditions/native (accessed on 1 July 2021).

- Everitt, Brian S., Sabine Landau, Morven Lesse, and Daniel Stahl. 2011. Cluster Analysis, 5th ed. Chichester: John Wiley and Sons. [Google Scholar]

- Foss, Nicola J., and Tina Saebi. 2017. Fifteen years of research on business model innovation: How far have we come, and where should we go? Journal of Management 43: 200–27. [Google Scholar] [CrossRef] [Green Version]

- Freeman, John, Glenn R. Carroll, and Michael T. Hannan. 1983. The Liability of Newness: Age Dependence in Organizational Death Rates. American Sociological Review 48: 692–710. [Google Scholar] [CrossRef]

- Furceri, Davide, and Aleksandra Zdzienicka. 2011. The real effect of financial crises in the European transition economies1. Economics of Transition 19: 1–25. [Google Scholar] [CrossRef] [Green Version]

- George, Gerard. 2005. Slack resources and the performance of privately held firms. Academy of Management Journal 48: 661–76. [Google Scholar] [CrossRef]

- Gilbert, Clark G. 2005. Unbundling the structure of inertia: Resource versus routine rigidity. Academy of Management Journal 48: 741–63. [Google Scholar] [CrossRef] [Green Version]

- Gollier, Christian, Pierre-François F. Koehl, and Jean-Charles Rochet. 1997. Risk-Taking Behavior with Limited Liability and Risk Aversion. The Journal of Risk and Insurance 64: 347. [Google Scholar] [CrossRef]

- Gourinchas, Pierre-Olivier, Sebnem Kalemli-Özcan, Veronika Penciakova, and Nick Sander. 2020. COVID-19 and SME failures. National Bureau of Economic Research Working Paper No. 27877. Available online: https://www.nber.org/papers/w27877 (accessed on 1 July 2021). [CrossRef]

- Gourinchas, Pierre-Olivier, Sebnem Kalemli-Özcan, Veronika Penciakova, and Nick Sander. 2021. COVID-19 and SMEs: 2021 “Time Bomb”? National Bureau of Economic Research Working Paper No. 28418. Available online: https://www.nber.org/papers/w28418 (accessed on 1 July 2021).

- Gu, Xin, Shan Ying, Weiqiang Zhang, and Yewei Tao. 2020. How Do Firms Respond to COVID-19? First Evidence from Suzhou, China. Emerging Markets Finance and Trade 56: 2181–97. [Google Scholar] [CrossRef]

- Habbershon, Timothy G., Mary Williams, and Ian MacMillan. 2003. A Unified systems perspective of family firm performance. Journal of Business Venturing 18: 451–65. [Google Scholar] [CrossRef]

- Hansmann, Henry, and Reinier Kraakman. 1991. Toward Unlimited Shareholder Liability for Corporate Torts. The Yale Law Journal 100: 1879. [Google Scholar] [CrossRef] [Green Version]

- Horvath, Michael, and Michael J. Woywode. 2005. Entrepreneurs and the Choice of Limited Liability. Journal of Institutional and Theoretical Economics 161: 681. [Google Scholar] [CrossRef]

- IRM. 2020. COVID–19 Global Risk Management Response. Institute of Risk Management. Available online: https://www.theirm.org/media/8903/irm-covid-response-survey-initial-report-final.pdf (accessed on 25 October 2020).

- Juergensen, Jill, Jose Guimón, and Rajneesh Narula. 2020. European SMEs amidst the COVID-19 crisis: Assessing impact and policy responses. Journal of Industrial and Business Economics 47: 499–510. [Google Scholar] [CrossRef]

- KPMG. 2020. Poland. Government and Institution Measures in Response to COVID-19. September 30. Available online: https://home.kpmg/xx/en/home/insights/2020/04/poland-government-and-institution-measures-in-response-to-covid.html (accessed on 10 August 2021).

- Kraus, Sascha, Thomas Clauss, Matthias Breier, Johanna Gast, Alessandro Zardini, and Victor Tiberius. 2020. The economics of COVID-19: Initial empirical evidence on how family firms in five European countries cope with the corona crisis. International Journal of Entrepreneurial Behavior & Research 26: 1067–92. [Google Scholar] [CrossRef]

- Lubatkin, Michael H., Yan Ling, and William S. Schulze. 2007. An Organizational Justice-Based View of Self-Control and Agency Costs in Family Firms. Journal of Management Studies 44: 955–71. [Google Scholar] [CrossRef]

- Maak, Thomas. 2007. Responsible leadership, stakeholder engagement, and the emergence of social capital. Journal of Business Ethics 74: 329–43. [Google Scholar] [CrossRef] [Green Version]

- Matos, Stelvia, and Bruno S. Silvestre. 2013. Managing stakeholder relations when developing sustainable business models: The case of the Brazilian energy sector. Journal of Cleaner Production 45: 61–73. [Google Scholar] [CrossRef]

- McGeever, Niall, John McQuinn, and Samantha Myers. 2020. SME Liquidity Needs during the COVID-19 Shock (No. 2/FS/20). Dublin: Central Bank of Ireland. [Google Scholar]

- Mercer. 2020. Globally, How Are Companies Adapting to the COVID-19 Business and Workforce Environment? Available online: https://app.keysurvey.com/reportmodule/REPORT2/report/41488264/41196046/59f27889c1eafb1ba976d193e88cb690?Dir=&Enc_Dir=60e929fb&av=IxnIBAm77ac%3D&afterVoting=888b4feadd76&msig=32162cb48db989d5d550fdc13ba64dc0 (accessed on 15 October 2020).

- Ministerstwo Rozwoju. 2020. Podstawowe Wskaźniki Makroekonomiczne, Polska, Wrzesień 2020. Available online: https://www.gov.pl/attachment/bc0e9744-1fdf-475c-a137-d141df473769 (accessed on 1 July 2021).

- Mishina, Yuri, Timothy G. Pollock, and Joseph F. Porac. 2004. Are more resources always better for growth? Resource stickiness in market and product expansion. Strategic Management Journal 25: 1179–97. [Google Scholar] [CrossRef]

- Moyo, Nggabutho. 2020. Antecedents of employee disengagement amid COVID-19 pandemic. Polish Journal of Management Studies 22: 323–34. [Google Scholar] [CrossRef]

- Myant, Martin, and Jan Drahokoupil. 2012. International Integration, Varieties of Capitalism and Resilience to Crisis in Transition Economies. Europe-Asia Studies 64: 1–33. [Google Scholar] [CrossRef]

- Nohira, Nitin, and Ranjay Gulati. 1996. Is slack good or bad for innovation? Academy of Management Journal 39: 1245–64. [Google Scholar] [CrossRef] [Green Version]

- Nurunnabi, Mohammad. 2020. Recovery planning and resilience of SMEs during the COVID-19: Experience from Saudi Arabia. Journal of Accounting & Organizational Change 16: 643–53. [Google Scholar] [CrossRef]

- Pal, Rudrajeet, Hakan Torstensson, and Heikki Mattila. 2014. Antecedents of organizational resilience in economic crises—An empirical study of Swedish textile and clothing SMEs. International Journal of Production Economics 147: 410–28. [Google Scholar] [CrossRef]

- Pekao. 2020. Krajobraz po bitwie. Wyniki Sektora Przedsiębiorstw w Pierwszym Półroczu 2020 Roku–Najnowszy Raport Banku Pekao S.A. (The Landscape fter the Battle. Results of the Corporate Sector in the First Half of 2020-the Latest Report of Bank Pekao S. A. Available online: https://media.pekao.com.pl/pr/569211/krajobraz-po-bitwie-wyniki-sektora-przedsiebiorstw-w-pierwszym-polroczu-2020-roku-najnowszy-raport-banku-pekao-s-a (accessed on 15 October 2020).

- PwC. 2020. PwC Global COVID-19 CFO Pulse Report, June 2020. Available online: https://www.pwc.com/gx/en/issues/crisis-solutions/covid-19/global-cfo-pulse.html (accessed on 2 October 2020).

- Qiu, Joseph. 2020. Pandemic risk: Impact, modelling, and transfer. Risk Management and Insurance Review 23: 293–304. [Google Scholar] [CrossRef]

- Salvato, C., M. Sargiacomo, M. D. Amore, and A. Minichilli. 2020. Natural disasters as a source of entrepreneurial opportunity: Family business resilience after an earthquake. Strategic Entrepreneurship Journal 14: 594–615. [Google Scholar] [CrossRef]

- Sanchez, Ron. 1995. Strategic flexibility in product competition. Strategic Management Journal 16: 135–59. [Google Scholar] [CrossRef]

- Soluk, Jonas, Nadine Kammerlander, and Alfredo De Massis. 2021. Exogenous shocks and the adaptive capacity of family firms: Exploring behavioral changes and digital technologies in the COVID-19 pandemic. R&D Management, 1–17. [Google Scholar] [CrossRef]

- Somers, Scott. 2009. Measuring Resilience Potential: An Adaptive Strategy for Organizational Crisis Planning. Journal of Contingencies and Crisis Management 17: 12–23. [Google Scholar] [CrossRef]

- Torres, Ariana P., Maria I. Marshall, and Sandra Sydnor. 2019. Does social capital pay off? The case of small business resilience after Hurricane Katrina. Journal of Contingencies and Crisis Management 27: 168–81. [Google Scholar] [CrossRef]

- Vlados, Charis, Epaminondas Koronis, and Dimos Chatzinikolaou. 2021. Entrepreneurship and Crisis in Greece from a neo-Schumpeterian Perspective: A Suggestion to Stimulate the Development Process at the Local Level. Research in World Economy 12: 1. [Google Scholar] [CrossRef]

- World Bank. 2021. Global Economic Prospects. Available online: https://www.worldbank.org/en/publication/global-economic-prospects (accessed on 1 July 2021).

Figure 1.

Perception of the COVID-19 interruptions and business size.

Figure 2.

Perception of the COVID-19 interruptions and business age (AGE_1).

Figure 3.

Perception of the COVID-19 interruptions and business age (AGE_2).

Figure 4.

Perception of the COVID-19 interruptions and business organization form (OWN_1).

Figure 5.

Perception of the COVID-19 interruptions and business organization form (OWN_2).

Figure 6.

Perception of the COVID-19 interruptions in family and non-family businesses.

Table 1.

Survey design: questions on COVID-19 interruptions.

| Variable | Question |

|---|---|

| Did the COVID-19 pandemic result in difficulties in the following aspects of firm’s performance? | |

| WORKERS | limited accessibility of workers |

| COSTS | additional costs of the implementation of required safety measures |

| PROD_CONT | inability to continue production |

| SALES_CONT | inability to continue sales |

| SUPPLY CHAIN | delayed delivery of production components/materials, etc., or produced goods to the customers |

| LIQUIDITY | worsening of financial liquidity |

| BANK LOANS | limited accessibility of bank loans |

| SURVIVAL | The overall impact of COVID-19 threatened the survival of our company |

Notes: COVID-19 interruptions were evaluated by respondents on the 7-point Likert scale: 1—strongly disagree, 2—disagree, 3—somewhat disagree, 4—neither agree nor disagree; 5—somewhat agree; 6—agree; 7—strongly agree. Cronbach’s Alpha—0.865.

Table 2.

Sample composition and variables that explain businesses’ characteristics relevant to this study.

Table 2.

Sample composition and variables that explain businesses’ characteristics relevant to this study.

| Variable | N | % | |

|---|---|---|---|

| SIZE (by the number of employees) | |||

| micro | up to 9 persons | 182 | 33.8 |

| small | 10–49 persons | 208 | 38.7 |

| medium | 50–249 persons | 148 | 27.5 |

| AGE_1 (by the years of operation, four categories of firms’ age) | |||

| infant | (up to 5 years) | 86 | 16.0 |

| young | (6–10 years) | 137 | 25.5 |

| intermediate | (11–20 years) | 187 | 34.8 |

| mature | (21 years or more) | 128 | 23.8 |

| AGE_2 (by the years of operation, three categories of firms’ age) | |||

| young | up to 10 years | 223 | 41.5 |

| intermediate | (11–20 years) | 187 | 34.8 |

| mature | (21 years or more) | 128 | 23.8 |

| OWN_1 (by the owners’ responsibility, dichotomous) | |||

| LLC | limited, perform as limited liability companies | 266 | 49.4 |

| non-LLC | other than LLC, with unlimited owners’ responsibility | 272 | 50.6 |

| OWN_2 (owners’ responsibility, three categories) | |||

| LLC | limited, perform as limited liability companies | 266 | 49.4 |

| SP | unlimited, perform as sole proprietorship | 195 | 36.2 |

| CP | unlimited, perform as civil law partnerships | 77 | 14.3 |

| FAM (family business, as declared by the surveyed firms) | |||

| family | 167 | 31.0 | |

| non-family | 371 | 69.0 | |

| In total | 538 | 100 | |

Table 3.

Results of ANOVA (p-values of Kruskal–Wallis test).

| WORK | COSTS | PROD_CONT | SALES_CONT | SUPPLY CHAIN | LIQUIDITY | BANK LOANS | SURVIVAL | |

|---|---|---|---|---|---|---|---|---|

| SIZE | 0.188 | 0.000 *** | 0.411 | 0.001 ** | 0.644 | 0.000 *** | 0.002 ** | 0.000 *** |

| AGE_1 | 0.970 | 0.021 * | 0.823 | 0.017 * | 0.012 * | 0.000 *** | 0.000 *** | 0.000 *** |

| AGE_2 | 0.924 | 0.013 * | 0.925 | 0.006 ** | 0.005 ** | 0.000 *** | 0.000 *** | 0.000 *** |

| OWN_1 | 0.283 | 0.000 *** | 0.252 | 0.001 ** | 0.385 | 0.000 *** | 0.000 *** | 0.000 *** |

| OWN_2 | 0.326 | 0.000 *** | 0.266 | 0.002 ** | 0.077 | 0.000 *** | 0.000 *** | 0.000 *** |

| FAM | 0.004 ** | 0.858 | 0.001 ** | 0.830 | 0.196 | 0.378 | 0.308 | 0.366 |

Notes: statistically significant at: *** α = 0.001; ** α = 0.01; * α = 0.05. Sample N = 538.

Table 4.

Results of k-means clustering: clusters of high, moderate and low COVID-19 interruptions.