Economic Policy Uncertainty and Cryptocurrency Market as a Risk Management Avenue: A Systematic Review

1

Department of Management Sciences, Comsats University Islamabad, Islamabad 45550, Pakistan

2

Department of Mechanical Engineering Technology, College of Industrial Technology, King Mongkut’s University of Technology North Bangkok, Wongsawang, Bangsue, Bangkok 10800, Thailand

3

Department of Occupational Therapy, Faculty of Associated Medical Sciences, Chiang Mai University, Chiang Mai 50200, Thailand

4

Faculty of Nursing, HRH Princess Chulabhorn College of Medical Science, Chulabhorn Royal Academy, Bangkok 10210, Thailand

5

Asia-Australia Business College, Liaoning University, Shenyang 110036, China

*

Author to whom correspondence should be addressed.

Risks 2021, 9(9), 163; https://doi.org/10.3390/risks9090163

Submission received: 10 August 2021

/

Revised: 1 September 2021

/

Accepted: 4 September 2021

/

Published: 7 September 2021

(This article belongs to the Special Issue Cryptocurrencies and Risk Management)

Abstract

:Cryptocurrency literature is increasing rapidly nowadays. Particularly, the role of the cryptocurrency market as a risk management avenue has got the attention of researchers. However, it is an immature asset class and requires gaps in current literature for future research directions. This research provides a systematic review of the vast range empirical literature based on the cryptocurrency market as a risk management avenue against economic policy uncertainty (EPU). The review discovers that cryptocurrencies have mixed connectedness patterns with all national EPU therefore, the risk mitigation ability varies from country to country. The review finds that heterogeneous correlation patterns are due to the dependence of EPU on the policies and decisions usually taken by regulatory authorities of a particular country. Additionally, heterogeneous EPU requires heterogeneous solutions to deal with stock market volatility and economic policy uncertainty in different economies. Likewise, the divergent protocol and administration of currencies in the crypto market consequently vicissitudes the hedging and diversification performance against each economy. Many research lines can benefit investors, policymakers, fund managers, or portfolio managers. Therefore, the authors suggested future research avenues in terms of topics, data frequency, and methodologies.

1. Introduction

The current focus of researchers is upon exploring a suitable shelter to shield investments, because the current financially integrated world is more sensitive toward economic policy risk than ever before. Interestingly, no such pandemic and higher uncertain event (including Spanish Flu, Global Financial Crisis, European Debt Crisis) had ever degraded the stock market and plunged EPU as much as COVID-19 continues to tumble. The swelled economic policy uncertainty often restricts investment flow due to a fear factor that prevails in investors for investment loss, often termed as risk-aversion behavior. Therefore, the importance of risk mitigation avenues attracts investors and fund managers during financial crisis, turmoil periods or higher uncertain periods like the COVID-19 pandemic.

Modern day economists and financial experts have pinned COVID-19 as more hazardous and unpredictable toward eco-financial structures. The global infection has harmed individual investors, institutional investors. The current financial and economic crisis lingers as a controversial topic among investors and scholars around the globe (Abdelrhim et al. 2020; Awan et al. 2021; Baker et al. 2020; Haq et al. 2021; Haq and Awan 2020). Understanding the notion of uncertainties and risks (either micro, macro-economic, financial, or other security-specific) is a predominant feature in financial markets. Investors around the world are worried about the effectiveness of risk management and avenues utilized to mitigate it (Haq et al. 2021). Investors are risk-averse and avoid loss, hence are always looking forward to diminish the potential uncertainties in their investments. Economic policy uncertainty has connectedness with financial and economic distress (Baker et al. 2013, 2016, 2020; Davis 2016; Rubbaniy et al. 2021). While talking about the global financial crisis, the Eurozone serial crisis, and other events of higher uncertainty (Baker et al. 2016) argued that fears and worries about policy uncertainty intensified in awakening a sharp economic downfall between 2008–2009.

Particularly, in higher periods of economic uncertainty, either investors restrict their investments, wait for current conditions to be settled down, or look to find suitable strategies to mitigate uncertainty around the globe. Interestingly, the cryptocurrency market appeared as a risk management tool for the domestic and international investors of stock and commodity markets around the globe, particularly during the period of higher uncertain events (Akhtaruzzaman et al. 2021a, 2021b; Al Mamun et al. 2020; Ariefianto 2020; Bouri et al. 2017a, 2017b, 2020b, 2017c, 2017d, 2018; Bouri and Gupta 2019; Cheema et al. 2020; Chen et al. 2021; Colon et al. 2021; Demir et al. 2018; Fang et al. 2020; Fasanya et al. 2021; Haq et al. 2021; Hasan et al. 2021; Jiang et al. 2021; Kalyvas et al. 2020; Nguyen 2020; Koumba et al. 2020; Kyriazis 2021; Lucey et al. 2021; Matkovskyy et al. 2020; Mokni et al. 2020; Nie et al. 2020; Papadamou et al. 2021; Park and Chai 2020; Paule-Vianez et al. 2020; Wang et al. 2019b; Qin et al. 2021; Raheem 2021; Rubbaniy et al. 2021; Wang et al. 2019a; Wu et al. 2019, 2021; Cheng and Yen 2020; Yen and Cheng 2021). Therefore, the current COVID-19 crisis could lead towards a slower economic and financial recovery, as after the global financial crisis (Baker et al. 2016; Davis 2016). Economic policy uncertainty has appeared as a crucial predictor of volatility in the cryptocurrency market (Bouri and Gupta 2019; Chen et al. 2021; Colon et al. 2021; Fang et al. 2020). However, the presence of cryptocurrency in current era may lead to hedging and mitigating of risk for investors during and in the recovery phase of COVID-19 crisis. Thus ample risk management avenues are alive in the shape of cryptocurrencies (Abdelrhim et al. 2020). It is therefore important to conduct a systematic review to validate the risk management role of cryptocurrency market and open potential research avenues for future research—the core purpose of the systematic review. Moreover, to answer: can cryptocurrencies act as hedge and safe-haven in focused studies throughout the world or not?

This systemic literature review contributes to the literature in several ways. Firstly, it critically evaluates the findings of previous studies related to the diversification, hedging, and safe haven strands and highlights several limitations. Secondly, it highlights potential avenues for future research in terms of topics, data frequency, and research methodologies. Thirdly, it contributes to the literature of hedging, safe haven, and diversification role of cryptocurrency currencies for economic policy uncertainty.

The remainder of the review paper is organized as follows. Section 2 is the development of cryptocurrency market and EPU index. Section 3 explains cryptocurrencies as risk management avenues for economic policy uncertainty. Section 4 suggests future avenues for further research and concludes the paper.

2. Material and Methods

The study is a systematic review of previous economic policy uncertainty and cryptocurrency market related research. This review exclusively focused on exploring the role of cryptocurrencies for economic policy uncertainty. Authors considered two widely considered databases, Scopus and Web of Sciences, for published articles selection during the period. Risk management literature of cryptocurrencies is increasing rapidly, because investors are analyzing different risk management strategies during COVID-19. Therefore, this research used snowballing sampling process as depicted in Figure 1.

The motivation was taken from (Awan et al. 2021; Geissdoerfer et al. 2017) and adapted for screening process as illustrated in flow chart of Figure 1. The process was based on three steps. The first step was managing the systematic literature search. For initial screening purpose, criteria were defined earlier. The initial criteria comprise that these terms (“hedge”, “safe-haven”, “diversification”, “cryptocurrency market”, “cryptocurrencies”, “EPU” or “economic policy uncertainty”, and “global economic policy uncertainty”) must be present in the paper. These terms were screened while searching the papers in title, abstract, and keywords of published articles. The papers which were duplicated were removed initially and screened out 204 published papers. Afterward the defined criteria were applied. Consequently 111 articles were excluded while screening the criteria in abstract and title. As a result, 93 research papers were retrieved. Afterward, criteria were applied on full-text research articles, which led to exclusion of 49 research articles in total, 34 articles due to full-text and 15 articles due to data extraction problems. Finally, 44 published research articles between 2017 to 2021 were selected for systematic review.

3. Review of Related Research

3.1. Development of Cryptocurrency Market

Money as a payment system has a rich background. Several incredible evolutions have occurred in history, from barter to precious metals, paper money, plastic money, and credit cards, and now to the mega-evolution of cryptocurrency. The inception of cryptocurrencies was to resolve uncertainties and distrust due to unprophetic fluctuations in financial systems (Wang et al. 2019a). The evolution of cryptocurrencies has become increasingly popular among investors, economists, and financial analysts. In this inclusive debate Lucey et al. (2021) have introduced cryptocurrency policy risk. Cryptocurrencies are changing financial systems and financial markets through the medium of exchange which is cashless into a new financial era. The biggest example, Petro (asset-backed) an oil and mineral resources backed (state-owned) cryptocurrency in Venezuela is clear evidence for evolution to continue to find its successive direction (Balli et al. 2019). The announcement of KODAK Coin by Eastman Kodak USA tech company in 2018 sharply plunged the share price of Kodak from $3 US dollar to $12 US dollar within a week. Moreover, the prices and volatility of Kodak, Bitcoin, and DJIA are found highly correlated using dynamic conditional correlation generalized autoregressive conditional heteroscedasticity (DCC-GARCH model) (Corbet et al. 2019b). Therefore, having cryptocurrency with stable purchasing power can be useful for speculative purpose in political-economic turmoil (Harwick 2016).

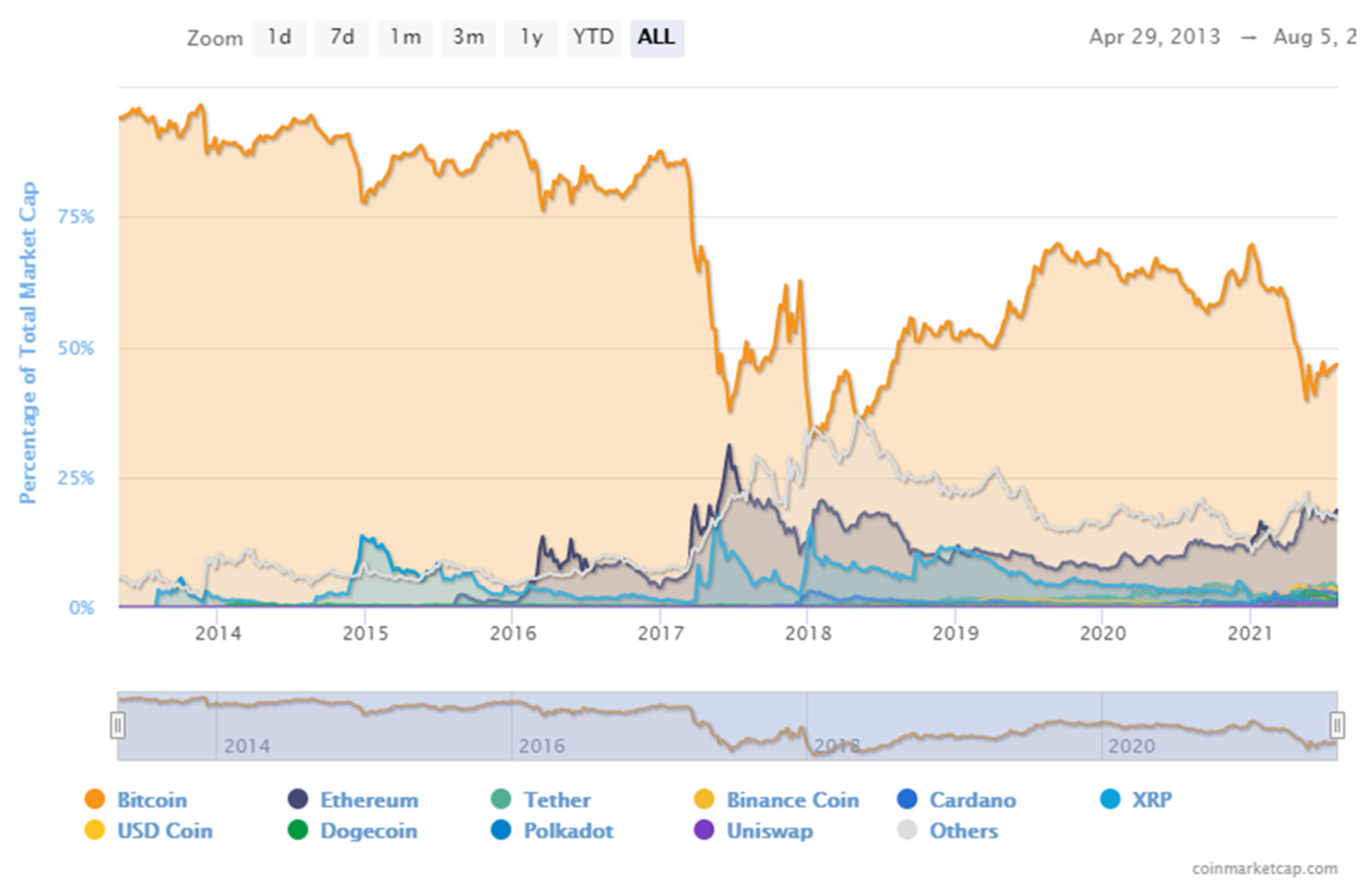

Cryptocurrency can be defined as digital coins which are openly available to everyone directly independent from financial regulatory authorities, sovereign governments, and controlled by the sophisticated peer to peer system of cryptography electronically based on blockchain technology (Demir et al. 2018; Fang et al. 2019; Khaldi et al. 2019; Koumba et al. 2020). A peer-to-peer electronic system introduced by (Nakamoto 2008) who formed the first-ever digital currency called Bitcoin in 2009 (Koumba et al. 2020). Unquestionably, the future of modern finance may rely on the technology of blockchain due to enormous advantages (Corbet et al. 2019a). Interestingly, the consideration of most investors has changed from Bitcoin to other emerging cryptocurrencies, resulting in the dominance of Bitcoin dropping. In 2014, Bitcoin held 88% of share in total market however 63% at present, as depicted in Figure 2 (CoinMarketCap 2020). In cryptocurrencies, Bitcoin is considered as a safe-haven against the economic policy uncertainty (EPU) and rich in literature with a strong empirical and theoretical background. Bitcoin dominance as a safe-haven will be decreased in the future. Moreover, the Bitcoin shocks are long-lived but are not dominant in respect to other currencies, even the largest in cryptocurrency market (Corbet et al. 2018a; Katsiampa et al. 2019). Therefore, this demonstrates the shortage of the empirical research on the risk management role of other cryptocurrencies.

3.2. EPU Index as a Risk Measure

Many risk measures have been utilized by researchers during the last two decades (Rubbaniy et al. 2021), the oldest being the standard deviation between asset prices and returns. CBOE developed VIX in 2006 and has a negative relationship with SandP 500 index consequently to employ long-term exposure offsetting (Al-Thaqeb and Ghanim 2019). Economic policy uncertainty becoming progressively worse introduced another measure survey by FRBP1. However, the recent debates on measuring economic policy uncertainty are around newspaper-based indexes and Internet search-based indexes, while Bitcoin was found to hedge against both indices (Bouri and Gupta 2019). More recent studies have proposed different indices to measure economic uncertainty, political uncertainty, and sentiment portion of uncertainty—most of them are text-based indexes, capturing news and journals using textual analysis (Da et al. 2015; Hassan et al. 2019; Julio and Yook 2012; Manela and Moreira 2016; Scotti 2016). All of these indexes were used only to measure specific kinds of uncertainty but found acceptable. Indexes hold few limitations, for instance they are complex in nature, not easy to use nor replicated in other countries of the world, not available publicly, and not useful for long-term measurement uncertainty as also highlighted (Al-Thaqeb and Ghanim 2019). Therefore, many scholars constructed and introduced EPU indexes for their countries as illustrated in Table 1.

The foundations developed by the prior studies converted by (Baker et al. 2016) into a strong and more useful single index proxy for 12 countries including the USA consist of policies, economic indicators, sentiment portion of uncertainty, and news elements altogether. EPU index of (Baker et al. 2016) has now expanded incredibly from 12 to 26 countries.

The Global Economic Uncertainty Index is also available with similar indicators of countries from different regions, based on these 21 countries. This index captures those countries which contribute heavily to overall global output based on PPP-adjusted and market exchange rate of 71% and 80% respectively. Moreover, global EPU is classified into further version PPP-adjusted and current price GDP measures (Baker et al. 2016). Yu and Song (2018) argued that the concept of global economic policy uncertainty has been derived from the Economic Policy Uncertainty Index of (Baker et al. 2016). The global policy uncertainty index is constructed with a weighted average of developed economies and highly correlated with the financial crisis and other recent events (Al-Thaqeb and Ghanim 2019). A similar nature of policy uncertainty index has been recently introduced (Lucey et al. 2021), which demonstrates the acceptability of the idea behind EPU construction. In overview, the EPU index constructed by Baker et al. (2016) has been a widely accepted measure for economic policy risk around the globe and it has been cited 5936 times during the last five years.

Newspapers can be the best platform of the general public (either household, investors or companies, government) for the emotional expression of uncertainty (Caporaley et al. 2019). The index of each country relies on the textual analysis of leading newspapers and the monthly count of a few specific and relevant terms applied in articles published in the newspaper. The index of each economy is based on these three terms (“Uncertainty” or “Uncertain” and “Economic” or “Economy”) must be in the article while one of these terms has to be found (“Congress”, “Deficit”, “Federal Reserves”, “Legislation”, “Regulation”, “White House”). The construction of the EPU index is explicitly based on the aggregate aim of who will take the economics decision, what decisions will be taken, and when (Baker et al. 2016). Moreover, the effects of the economic decisions by the governments is considered. News, taxes, and policies are the factors also considered to build an index for each economy.

3.3. Cryptocurrencies as Risk Management Avenue for Economic Policy Uncertainty

3.3.1. Role of Cryptocurrencies for Country EPUs

A successful hedging strategy needs to observe the correlation structure (Evans and Archer 1968; Kristjanpoller and Bouri 2019). The understanding of economic policy uncertainty patterns can be a helping hand for investors to redesign their portfolio, adding cryptocurrencies to evade potential loss (Cheng and Yen 2020). Otherwise, the uncertain economic policies can restrict investment flow (Kido 2016). A study (Koumba et al. 2020) has considered Ethereum while utilizing D-Vine Pair-Copula method to establish the basis of hedging aptitude for other digital currencies. (Koumba et al. 2020) found Ethereum was more highly correlated with US EPU compared to Ripple and Bitcoin. Thus, the aptness of Ethereum as hedge against EPU of the United States of America has only been studied.

Table 2 illustrates characteristics of 44 considered studies in tabular form. The characteristics were classified under eight sections or headings such as Title, Authors and Year, Reason, Employed Methodology, Frequency, Data Source, Data Coverage, and Findings. These sections can easily give an idea about the focused studies. Figure 3 demonstrates the coverage of data or the duration of data in 44 focused studies. There are relatively few papers which have investigated the safe-haven properties of cryptocurrencies considering COVID-19 data. Many studies have taken data from 2010 onwards. Figure 4 represents the percentage of Bitcoin nodes around globe considering top 20 countries. The graph demonstrates that top three countries (USA, Germany, and France) have more than half of the world’s Bitcoin nodes. USA is a leading holder of Bitcoin nodes around the world. Bitcoin nodes are also increasing in European countries, as several European countries are currently in the top 20 countries with Bitcoin nodes.

Most recent studies have considered several cryptocurrencies for hedging for national EPUs, and Bitcoin has been well-versed. While measuring future volatility of cryptocurrencies like Bitcoin, Litecoin, and Ripple using (Wang and Yen 2019) regression framework, (Cheng and Yen 2020) discussed Chinese EPU as more sensitive toward predicting the volatility of Bitcoin and Litecoin while other national EPUs like United States of America, Korea, and Japan were unable to predict their future EPU. Finally, cryptocurrencies (Bitcoin and Litecoin) can be used to hedge national EPU. Another recent research by (Cheng and Yen 2020) applied the (Newey and West 1987) predictive regression model to examine whether the EPU predicts the monthly return of cryptocurrencies.

The intelligent duo kept a similar sample data set, except for the addition of Ethereum whose data unavailability issue restricted the timeframe to three years and four months. While closing the conversation (Cheng and Yen 2020) argued, the single Chinese EPU index can predict the returns. Therefore, the useful information that economic policy uncertainty indices contain enhances the power in predicting both return and volatility in cryptocurrencies like Bitcoin (Qin et al. 2021). In contrast, the volatility of cryptocurrencies is not driven by financial and economic factors of a single economy but by global business cycle and REAI (Real Economic Activities Index) (Demir et al. 2018). Anyway, the core concern is to explore risk management patterns in cryptocurrencies but these studies need to be mentioned as they provide implications for risk mitigation (Demir et al. 2018). The spillover effect of the economic policy uncertainty of the US toward Bitcoin was found to be minor which is negligible (Wang et al. 2019a). The application of Multivariate Quantile Model and Granger Causality validated the performance of Bitcoin as diversifier or safe-haven against unexpected EPU extreme shocks.

While examining the properties of Bitcoin (Wu et al. 2019) employed GARCH and Quantile Model with dummy variables, discovering that it does not prove to hedge the economic policy risk of the USA in normal conditions. Moreover, in extreme market conditions, whether higher or lower or extreme bullish and bearish trends, the ability to be as hedger or safe-haven is weak, but can be used for diversification or risk mitigation intent.

Another recent study by (Shaikh 2020) documented the estimation of Quantile regression and Ordinary Least Square methods to portray the behavior among Bitcoin returns and EPU (USA, UK, China, Japan, and Hong Kong), Global EPU, monetary policy uncertainty (MPU), VIX2, and SPX3 and Bitcoin returns. Results confirmed that Bitcoin can perform as safe-haven and hedge against market uncertainty, particularly returns of Bitcoin are more reactive to economic policy uncertainty of United States, Japan, and China. All-inclusive, the association among Bitcoin returns and the uncertainty and fear of equity market is negative (Shaikh 2020) however other cryptocurrencies and economic policy uncertainty are overlooked to take into account. Purposefully, our research aims to study the undiscovered phenomena of other cryptocurrencies to ensure whether the losing dominance of Bitcoin (Corbet et al. 2018b; Katsiampa et al. 2019) in the cryptocurrency market unlocks the abilities of other uppermost cryptocurrencies Bitcoin, Ethereum, XRP, Bitcoin Cash, and Litecoin). (Kalyvas et al. 2020) documented the behavioral aspect of Bitcoin investors and Bitcoin price crash uncertainty with economic policy uncertainty. Particularly, the association of Bitcoin price crash risk and economic policy uncertainty demonstrated a strong negative correlation pattern. While considering this, Bitcoin can be considered as a hedge against economic policy uncertainty because of its inverse or volatility correlations. (Bouri et al. 2020b) analyzed the hedging ability of Bitcoin against trade and economic policy uncertainties. They employed the realized volatility and linear regression on monthly values and confirmed that Bitcoin can be used as a hedge against trade and economic uncertainties. Therefore, ample opportunities exist in cryptocurrencies to hedge EPU and trade uncertainty.

Several studies have demonstrated short term volatility and return of cryptocurrencies, however (Fang et al. 2020) investigated the long term relationship of cryptocurrency market with implied volatility using GARCH-MIDAS model. They found a strong negative impact of NVIX on the uncertainty or volatility of the cryptocurrency market. Interestingly, they documented that uncertainty in human perception has much stronger influence on cryptocurrencies than that of economic fundamentals. (Park and Chai 2020) captured the effect of information asymmetry on investment in cryptocurrency market using probability of informed trading and Vector Error Correction model. They found that the investor’s decision making is based on sentiment rather than information about cryptocurrencies. Likewise, (Nie et al. 2020) analyzed the importance of investors’ perception of the US stock market and how it influences the volatility of the cryptocurrencies market. When investors are optimistic about the US stock market it decreases the change in trade volume of cryptocurrencies and volatility plunges when investors are pessimistic about US stock market. (Ariefianto 2020) investigated whether cryptocurrency was really a financial asset class or not, using monthly data of Bitcoin as a sample. They employed multiple regression and error correction models and found the notion of cryptocurrency as financial asset is spurious. The business model and technological development of Bitcoin is still open for improvement. (Al Mamun et al. 2020) investigated the dynamic impact of geopolitical and economic policy uncertainty on the correlation patterns of several financial stocks and commodity assets with Bitcoin using DCC-GJR-GARCH. Moreover, they gauged the impact of these factors on Bitcoin risk premium and volatility. Results confirmed that EPU and GPU hold strong impact during unfavorable economic and financial periods.

(Papadamou et al. 2021) explored the non-linear linkage between economic policy uncertainty during the bullish and bearish trends (market sentiment). They employed non-parametric quantile and Granger Causality test and found that EPU index positively correlated with several cryptocurrencies in bull market, and even larger number of currencies correlated to bear market.

(Colon et al. 2021) examined the effect of political and economic uncertainties on the cryptocurrency market using OLS regression model. The results of monthly data confirmed that cryptocurrencies are a strong hedge against GPU and weak against EPU during bullish trend. Economic policy uncertainty is a very crucial factor to determine the returns of cryptocurrencies. (Nguyen 2020) proposed a conditional beta and uncertainty factor in cryptocurrency pricing model using two-pass regression approach. They found that a conditional beta is better than an unconditional beta. (Matkovskyy et al. 2020) studied the influence of economic policy uncertainty on the linkage between conventional assets and Bitcoin based on daily and monthly data. They employed EWMA Models and GAS Model and found Bitcoin to be a hedging instrument against US EPU. (Cheema et al. 2020) investigated the impact of economic policy uncertainty on return prediction of cryptocurrencies in countries which have highest Bitcoin nodes around the globe—Figure 4 portrays a picture of Bitcoin nodes. They employed multiple methodologies (OLS, Multivariate Augmented regression, and Quantile regression) and concluded that EPU has stronger predictive ability over Bitcoin returns in long-run (6-months and 12-months) than short-run (1-month). Moreover, Bitcoin may not be considered as a hedge or safe-haven against financial assets. (Paule-Vianez et al. 2020) investigated the influence of economic policy uncertainty on Bitcoin returns and volatility to determine its safe-haven and hedge properties. They employed linear regression with OLS and concluded that Bitcoin acts as a safe-haven and means of exchange. They clarified that Bitcoin is not a speculative asset but is a safe-haven. (Wu et al. 2021) examined the impact of economic policy uncertainty (Twitter-based uncertainty measure) on top four cryptocurrencies and found a significant causality between cryptocurrencies and cryptocurrencies. Using the Rolling Window approach and Granger Causality test, they found a positive association between Twitter-based uncertainty, VIX, and Cryptocurrencies. Thus, Bitcoin can be used as a hedge against the VIX shocks. (Mokni et al. 2020) examined how EPU influence the dynamic correlation between US stock market and Bitcoin conditional volatility. They employed DCC-EGARCH to capture the dynamic moments and found EPU has negative effect on the correlation between US stocks and Bitcoin. Moreover, the presence of Bitcoin in portfolio works as a diversifier with US stocks.

The current debate is on the policy uncertainty of the cryptocurrency market itself (Lucey et al. 2021). Therefore, scholars should use cryptocurrency policy uncertainty for further investigation. In 2021 (Hasan et al. 2021) investigated the impact of cryptocurrency policy uncertainty on Bitcoin and gold using OLS, Quantile regression, and Quantile on Quantile regression. They found that Bitcoin is not a hedge nor a safe haven, but Gold is a traditional hedge.

(Wu et al. 2021) has analyzed the impact of economic policy uncertainty on the top four cryptocurrencies using the Granger Causality test, and found that Bitcoin, Ripple, and Ethereum act as a hedge against EPU shocks. Another study (Mokni 2021) shows the impact of economic policy uncertainty on Bitcoin considering the top 10 countries where Bitcoin nodes are higher. They found that EPU improves Bitcoin returns in most of the countries where Bitcoin nodes are higher using symmetric and asymmetric causality quantiles. A new study by (Lucey et al. 2021) has introduced a new policy uncertainty index based on (Baker et al. 2016) methodology and found a positive correlation between cryptocurrency policy uncertainty and economic policy uncertainty. A study used (Jiang et al. 2021) Quantile cross-spectral regression to estimate the connectedness between cryptocurrencies and economic policy uncertainty during COVID-19. They found that Bitcoin and XRP are the most appropriate hedge against high-EPU. On the contrary, in the case of low or moderate EPU, cryptocurrencies are not a suitable hedge. Likewise, new research by (Kyriazis 2021) has analyzed a relationship between digital and EPU and explored hedging, safe-haven, and diversifier properties using the ARCH model. They found that Litecoin and Ethereum are diversifiers for Bitcoin and Bitcoin is a safe haven and hedge for EPU.

In the same line (Fasanya et al. 2021) have investigated the connectedness among EPU, precious metals, and Bitcoin using a non-parametric quantile approach. They found that both precious metals and Bitcoin do not act as a hedge or safe haven. Moreover, (Chen et al. 2021) have explored the EPU and Bitcoin returns during COVID-19 using the Predictive Model (OLS-GQS generalized quantile regression). They concluded that Bitcoin is a hedge for EPU risk during the pandemic times. Similarly, (Foglia and Dai 2021) have investigated the cryptocurrency and policy uncertainty relationship and predictive ability of EPU for cryptocurrency returns using time-varying parameter vector autoregression. They found that EPU predicts cryptocurrency uncertainty and is thus a suitable hedge. Another recent paper by (Colon et al. 2021) uncovered the impact of EPU on the cryptocurrency market using simple OLS regression on monthly values. The findings suggested strong and weak hedge, and safe-haven EPU and geopolitical risk. Another interesting piece of research has recently been published by (Rubbaniy et al. 2021) considering the COVID-19 episode and safe-haven properties of crypto-assets for EPU. They found that cryptocurrencies are safe-haven non-financial risk proxies, however they are not a hedge for financial proxies during COVID-19. In a similar objective, a study investigated the relationship between Bitcoin and EPU using the OLS regression model through daily data. They concluded that Bitcoin acts as a safe haven during COVID-19.

3.3.2. Role of Cryptocurrencies for Global EPU

The focus in previous studies was to explore economic policy uncertainty alongside gold and cryptocurrencies. Moreover, the focal point was whether Bitcoin or other cryptocurrencies act as hedge for EPU in a same manner as gold does. Therefore, the current discussion provides an overview of earlier research. Interestingly, the relevance of the cryptocurrency market with global economic policy uncertainty has been investigated (Parino et al. 2018) since the inception of Bitcoin’s financial system (Murphy et al. 2015). New studies relating to practices of stable coins as safe-haven and hedge against the largest cryptocurrencies (Hoang and Baur 2020) and (Baur and Hoang 2020) demonstrate the empirical worth of cryptocurrencies. Even cryptocurrency’s hedging and safe-haven abilities have been tested with each other (Beneki et al. 2019). As the traditional hedge gold has been challenged by Bitcoin against global economic policy uncertainty, do other cryptocurrencies also behave against Global EPU as hedger, safe-haven, or diversifier? Until 2019, 74.3% of ninety studies on cryptocurrency have taken Bitcoin for investigative analysis (Corbet et al. 2019b). Thus, empirical foundations of cryptocurrencies other than Bitcoin have been discriminated against and under-studied for analysis concerning hedge or risk management tools (Corbet et al. 2019b).

Recent research discovered that when the price of Bitcoin surges it causes a decline in the price of gold, thus a clear sign of undermining the historical hedging aptitude of the gold. However, the same pattern has been found for gold against Bitcoin, therefore, both can be used as an alternative not in a competition against the global EPU in bearish and bullish market sentiment (Su et al. 2020) while both of them mitigate the risk prevailing in the financial system. Qualities of being utilized as safe-haven and importantly, store of value, often feature Bitcoin as identical to gold (Baur and Hoang 2020). The strong medium of exchange and the store of value often put cryptocurrencies in-between Gold and US Dollars for portfolio diversification, safe-haven, and ideal choice risk-averse investors in the market discovered firstly by (Dyhrberg 2015b). Bitcoin cannot always be considered a hedge against Global EPU because the prices and volatility of Bitcoin are also determined by external (EPU and GEPU) and Bitcoin specific factors (cyber-attacks and speculative bubbles) (Qin et al. 2021). Apart from the associated risk, investors must consider cryptocurrencies like Bitcoin for attractive benefits (Bouri et al. 2018).

Global economic policy uncertainty influences the uncertainty of Bitcoin slightly, thus weak effect on hedging could lead investors to restrict their hedging outcomes (Fang et al. 2019). Findings of DCC-MIDAS validate Bitcoin as a hedge under particular timeframe, and Global EPU effect positively on the correlation of Bitcoin with commodities and equities, however, negatively on Bitcoin-Bonds (Fang et al. 2019). (Wang et al. 2019b) added that Bitcoin were not workable as a hedge against 30 well-known international indices. Earlier, industrial stocks of different emerging markets found negatively correlated with GEPU hence can be added for the diversification in cross-industry portfolios (Donadelli and Persha 2014) concluded using DCC-GARCH and Rolling Window framework. Additionally, Bitcoin has been found as safe-haven against the Global Financial Stress Index for two months during the European Debt and Cypriot Banking Crisis (Bouri et al. 2018) using Copula-based modeling.

Moreover, risk management and diversification abilities of Gold (Wu et al. 2019) and Bitcoin cannot be disregarded due to recent empirical evidence. Although, financial securities of emerging markets, the traditional hedger (gold), and Bitcoin have potential to be utilized for mitigating global economic policy uncertainty and risk in other traditional financial assets equities (Bouri et al. 2017a), bonds and energy commodities are an immense cause of global economic policy risk (Bouri et al. 2017b, 2017c). But, interestingly in a manner, Bitcoin has come to be seen as a complementary use with gold (Baur and Hoang 2020; Dyhrberg 2015a; Su et al. 2020), therefore the other cryptocurrencies’ behavior must be studied. The volatility of cryptocurrencies driven by the global business cycle (Demir et al. 2018) and global economic policy uncertainty has a close relationship with the global business cycle, thus, the pattern of GEPU has to be thoroughly analyzed to exploit diversification benefits. Global economic policy uncertainty unlocks the ample need to study the risk management power of other cryptocurrencies. The foundation of crude oil, gold, and US dollar related to the hedging potentials are clear in the literature. Bitcoin’s character is also identical to these commodities and currencies. However, the similar understood characteristics held by the other cryptocurrencies (Bouri et al. 2020b; Koki et al. 2019; Kristjanpoller and Bouri 2019) opens ample opportunities for researchers to explore the risk mitigation properties in several other cryptocurrencies. Research moves around the analysis of the traditional ability of gold and Bitcoin as hedge and diversifier during higher global economic unrest or higher GEPU. However, our research aims to study the undiscovered phenomena of other cryptocurrencies to ensure whether the losing dominance of Bitcoin (Corbet et al. 2018a; Katsiampa et al. 2019) in cryptocurrency market unlocks the abilities of other uppermost cryptocurrencies like Bitcoin, Ethereum, XRP, Bitcoin Cash, and Litecoin.

Previous selected studies have investigated several data frequencies from cryptocurrencies and economic policy uncertainty as illustrated in Table 3.

The data for crypto assets is available in several frequencies such as intra-day, daily, weekly, monthly, and semi-annually. However, EPU data is available in daily and monthly frequencies. In this review paper, daily frequency of data is coming up as the most investigated data frequency where 56.82% (25) of focused studies preferred daily frequency. The monthly frequency came as second most used data frequency with 28.89% (13) of total studies. Very few studies have explored other data frequencies such as daily-intra-day, monthly-daily, daily-weekly, and weekly. These findings demonstrate that less studies have used monthly and other combination of mixed-frequency or mixed-sampling data between cryptocurrencies and economic policy uncertainty. Therefore, all findings of previous research based on daily data might have produced spurious results because the economic policy uncertainty is a macro-economic variable and cryptocurrencies are a short-term and high frequency variable. Therefore, more studies are called for on monthly time series between these variables.

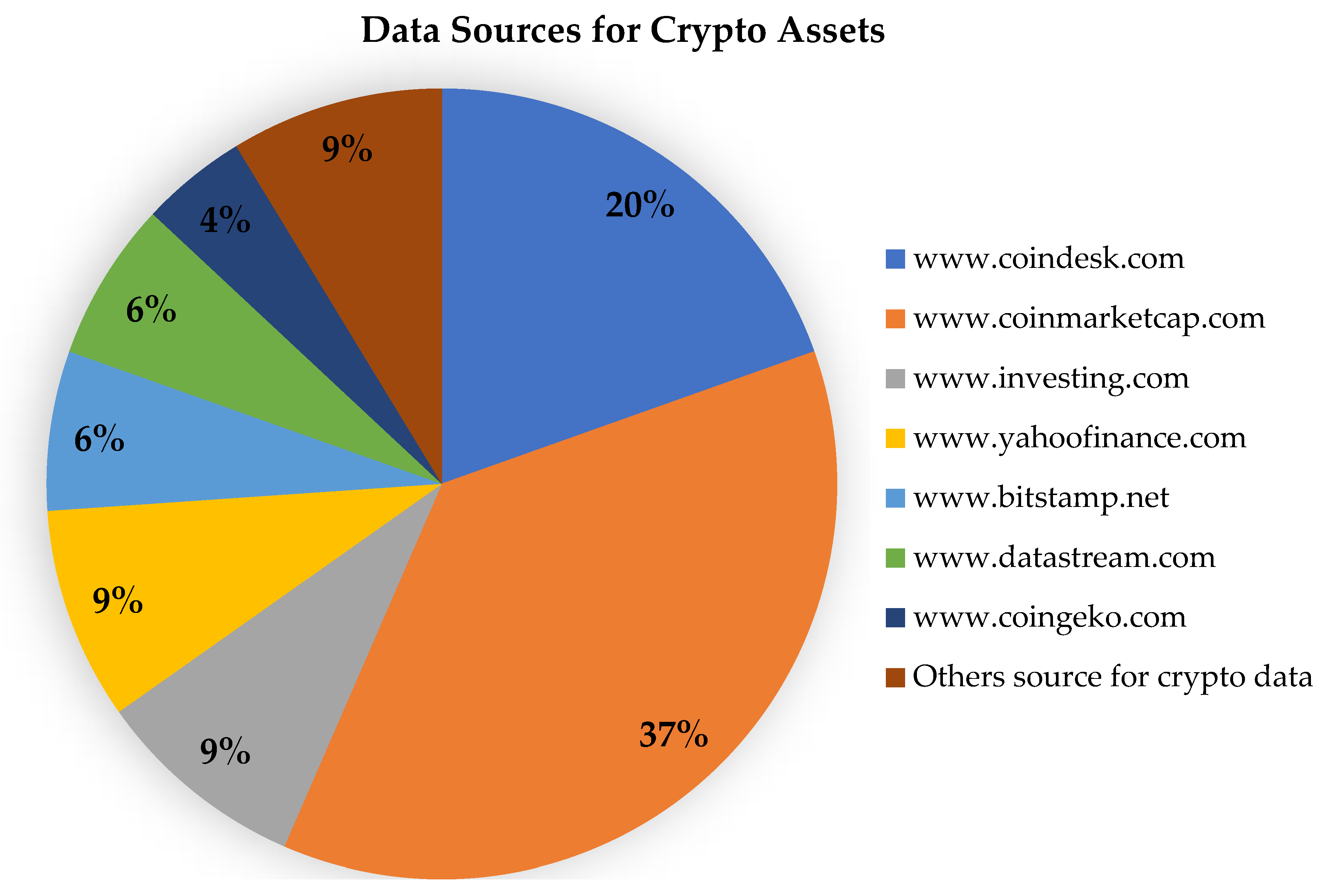

This systematic analysis discovered frequent sources for crypto data used in selected studies. As illustrated in Table 4 and Figure 5. The most frequent source employed for data retrieving in selected studies was www.coinmarketcap.com, where 36.36% (16) of total studies (44) have considered this source. This is due to its data availability and public access to users. The second frequent source was www.coindesk.com, as used by 9 studies that comprise 20.45% of total sampled papers in current review. There were several sources such as www.investing.com and www.yahoofinance.com that were used by 4 (9.09%) studies for each. Other sources were www.bitstamp.net, www.datastream.com, and www.coingeko.com. Moreover, to measure economic policy uncertainty or economic policy risk all studies retrieved the data from www.policyuncertainty.com.

4. Conclusions

In this study, a systematic analysis was conducted on the basis of recently published cryptocurrency and economic policy uncertainty research nexus from January 2017 to December 2021. We document that the risk management ability of cryptocurrencies has vastly analyzed and accepted mixed patterns in research during the last five years. Several authors demonstrated that these cryptocurrencies act as hedge against economic policy risk. In current strand, several studies concluded that cryptocurrencies act as hedge and safe haven (Bouri et al. 2017b, 2017c, 2017d, 2019, 2020a; Bouri and Gupta 2019; Chen et al. 2021; Cheng and Yen 2020; Colon et al. 2021; Fang et al. 2020; Fasanya et al. 2021; Jiang et al. 2021; Kalyvas et al. 2020; Koumba et al. 2020; Kyriazis 2021; Matkovskyy et al. 2020; Mokni 2021; Mokni et al. 2020; Papadamou et al. 2021; Paule-Vianez et al. 2020; Wang et al. 2019b; Raheem 2021; Rubbaniy et al. 2021; Wu et al. 2019, 2021; Cheng and Yen 2020; Yen and Cheng 2021). In contrast, cryptocurrencies do not act as hedge or safe-haven for economic policy uncertainty (Cheema et al. 2020; Fasanya et al. 2021; Hasan et al. 2021; Jiang et al. 2021; Lucey et al. 2021; Wu et al. 2019). Moreover, economic policy uncertainty predicts the cryptocurrency market volatility and returns (Al Mamun et al. 2020; Bouri et al. 2018; Demir et al. 2018; Fang et al. 2019; Foglia and Dai 2021; Papadamou et al. 2021; Qin et al. 2021; Shaikh 2020). Sometimes, there is no such association and predictiveness between cryptocurrency and economic policy uncertainty (Bouri et al. 2017a; Wang et al. 2019a), and crypto trading is usually based on market sentiment rather than information (Nie et al. 2020; Park and Chai 2020). Therefore, the hedging and safe-haven properties are well accepted against economic policy uncertainty and investors should add cryptocurrencies to shield their investments. However, the findings imply that investors should be aware and have enough information of where they want to hedge economic policy risk and when (Mokni 2021) because economic policy uncertainty has a heterogenous pattern in each economy due to independent nature and dependence on government policies and regulations. This may remove the risk mitigation ability in cryptocurrencies thus investors should keen to understand where and when they use cryptocurrencies to mitigate policy risk. Although cryptocurrencies are well-versed as risk mitigation tool, the existence of cryptocurrency and blockchain is still immature, but they do potentially hold ample prospect to grow in future, as according to (Corbet et al. 2019b), who argued that the cryptocurrency market is not yet as developed as stock exchanges worldwide. Additionally, several attacks on cryptocurrency market and legalization issues have signaled cryptocurrency market as an immature area in finance. Therefore, notion of cryptocurrency as financial asset is spurious (Ariefianto 2020). Cryptocurrencies differ from traditional financial assets due to: (i) no association with higher regulatory authorities or decentralized nature, (ii) infinitely divisible, (iii) not collateralized (backed by the economy, asset, or firm) but securitized by an algorithm. However, some interesting features of cryptocurrencies are: lower cost of a transaction, direct peer to peer or one to one transaction, and independence from the involvement of the government of the state. Due to these features, several economies around the world have imposed a ban on cryptocurrency trading. It will take some time for the cryptocurrency market to be as established and well-organized as stock markets. Findings of previous research suggest that policymakers should work on blockchain development and controlling system in cryptocurrency market to ensure minimum volatility transition and hacking on cryptos market. Our key findings depict that there are several literature and knowledge gaps in cryptocurrency and economic policy uncertainty literature. Thus, we highlighted several research gaps in terms of topics or objectives, methodology and data coverage and frequency.

Future Research Avenues

This review paper provides a comprehensive outlook of cryptocurrencies as risk management tool in the current era. At the same time, this paper provides several future research pathways for young scholars in three classes, topics or objectives, methodology, data coverage, and frequency, illustrated in Table 5. This table indicates potential gaps in the current literature. After reviewing the literature from the last five years, future lines of research are proposed by the authors for further investigation.

Generally, previous studies in literature have considered DDC GARCH to capture the dynamic correlation patterns as illustrated in Table 2. Very few studies used other financial and econometric models such as quantile regression, quantiles model and granger causality, D-vine copula, rolling window, ordinary least square, and multiple regression. Few studies considered the predictive role of economic policy uncertainty to prices and returns of cryptocurrency market. Regarding the accuracy of DCC multivariate GARCH model, it cannot capture the frequency of correlation over time, however other cavities are discussed in literature (Caporin and McAleer 2013). Therefore, future studies are recommended to consider the Wavelet approaches to capture the correlation with frequency and time. Moreover, other methodological approaches, such as non-parametric models are suggested to estimate further economic policy uncertainty and cryptocurrency. Previous research also seems more focused to GARCH family, however future research should consider the copula family to capture the dependence. Moreover, more studies are required to generalize the findings of previous studies with new econometric and financial models. The application of neural networks on current topics can be another methodological contribution.

In terms of data frequency, 56.82% of total studies focused on daily values of economic policy uncertainty and cryptocurrency currencies as illustrated in Table 3. This may lead to spurious connectedness and correlation outcomes because the EPU is a macroeconomic variable and estimation through daily value is not appropriate (Cheng and Yen 2020). Therefore, more research is called for to estimate the weekly, monthly, quarterly, and semiannual values of EPU and cryptocurrency currencies. DCC-MIDAS is suggested to capture the mixed frequency. Moreover, intra-day values of cryptocurrencies are available and future scholars should focus on intraday values of cryptocurrencies with monthly values of EPU in DCC-MIDAS methodology. Cryptocurrency is the latest financial asset with data available since 2013, and even top capped cryptocurrencies have been introduced recently, so considering annual data is not possible for estimation. Additionally, cryptocurrencies are a high frequency variable and investor use them for speculative purposes. Therefore, short-term and long-term safe-haven and hedging properties are called for to investigate in coming research.

Cryptocurrency as a risk management tool has not yet been well-versed due to its recent inception and hype. Additionally, very few countries have legalized cryptocurrency trading, which means that it is a less explored area in literature (Corbet et al. 2019b). There are enormous topics based on an several risk management objectives. This study offers new topics of interests for further investigation. Most studies have considered the hedging role of cryptocurrency for speculative purpose. Additionally, several studies have been based on risk management role against EPU. The role of cryptocurrencies as shielding the volatility of green and sustainable financial assets such green bonds (Haq et al. 2021), clean energy stocks, EGS stocks has been ignored. Likewise, the linkage of EPU with metals such as precious metals, national indexes of rare earth metals, individual rare earth metals. As for the data availability issue of EPU, more research can be done on constructing EPU indexes for other countries therefore most research avenues can be opened. Table 1 illustrates the currently available EPU national indices. Daily indexes are available for China, USA, and UK only, and production and consumption of rare earth elements is mainly based on these countries. Future research has potential to extend this line of research. Interestingly, a recent downfall in cryptocurrency prices during COVID-19 could wipe out the risk management ability of cryptocurrencies for policy risk. Thus, more research is required in the current strand. Significantly, the economic policy uncertainty index is available for almost all those economies which have higher percentage of Bitcoin nodes around the world, as illustrated in Figure 4. Therefore, future scholars should adapt new financial and econometric methodologies to better portray the current picture. Investors should analyze the past behavior of cryptocurrencies during crisis episode and in recovery phase and are advised to obtain short-term and long-term risk management benefits during, and post, COVID-19 crisis.

Author Contributions

Conceptualization, I.U.H.; methodology, I.U.H. and C.H.; software, A.M. and S.C.; validation, A.M., S.C. and C.H.; formal analysis, I.U.H.; investigation, I.U.H.; resources, A.M. and S.C.; data curation, W.S. and S.C.; writing—original draft preparation, I.U.H.; writing—review and editing, I.U.H., A.M. and S.C.; visualization, W.S.; supervision, C.H.; project administration, I.U.H. and C.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research is purely managed by authors, no funding was provided by any funding agency.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to extend their sincere appreciation to anonymous reviewers.

Conflicts of Interest

The authors declare no conflict of interest.

| 1 | FRBP stands for Federal Reserve Bank of Philadelphia who proposed another measure for policy uncertainty exhibited USA’s economic uncertainty worsening in recent past (Al-Thaqeb and Ghanim 2019). |

| 2 | VIX stands for Volatility Index formed by CBOE (Chicago Boards Options Exchange). |

| 3 | SPX is the abbreviation of (Standard and Poor Index); both are considered as fear-gauge. |

References

- Abdelrhim, Mansour, Abdullah Elsayed, Mahmoud Mohamed, and Mahmoud Farouh. 2020. Investment Opportunities in The Time Of (COVID-19) Spread: The Case of Cryptocurrencies and Metals Markets. SSRN Electronic Journal, 1–19. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021a. Financial contagion during COVID–19 crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Akhtaruzzaman, Md, Sabri Boubaker, Brian M. Lucey, and Ahmet Sensoy. 2021b. Is gold a hedge or a safe-haven asset in the COVID–19 crisis? Economic Modelling 102: 105588. [Google Scholar] [CrossRef]

- Al Mamun, Md, Gazi Salah Uddin, Muhammad Tahir Suleman, and Sang Hoon Kang. 2020. Geopolitical risk, uncertainty and Bitcoin investment. Physica A: Statistical Mechanics and Its Applications 540: 123107. [Google Scholar] [CrossRef]

- Algaba, Andres, Samuel Borms, Kris Boudt, and Jeroen Van Pelt. 2020. The Economic Policy Uncertainty Index for Flanders, Wallonia and Belgium. SSRN Electronic Journal, 1–13. [Google Scholar] [CrossRef]

- Al-Thaqeb, Saud Asaad, and Barrak Ghanim Algharabali. 2019. The Journal of Economic Asymmetries Economic policy uncertainty: A literature review. The Journal of Economic Asymmetries 20: e00133. [Google Scholar] [CrossRef]

- Arbatli, Elif C., Steven J. Davis, Arata Ito, and Naoko Miake. 2019. Policy Uncertainty in Japan. Tokyo: National Bureau of Economic Research. [Google Scholar]

- Ariefianto, Moch Doddy. 2020. Assessing qualification of crypto currency as a financial assets: A case study on Bitcoin. Paper presented at International Conference on Information Management and Technology (ICIMTech), Bandung, Indonesia, August 13–14; pp. 934–39. [Google Scholar] [CrossRef]

- Armelius, Hanna, Isaiah Hull, and Hanna Stenbacka Köhler. 2017. The timing of uncertainty shocks in a small open economy. Economics Letters 155: 31–34. [Google Scholar] [CrossRef] [Green Version]

- Awan, Tahir Mumtaz, Muhammad Shoaib Khan, Inzamam Ul Haq, and Sarwat Kazmi. 2021. Oil and stock markets volatility during pandemic times: A review of G7 countries. Green Finance 3: 15–27. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic policy uncertainty. The Quarterly Journal of Economics 131: 1–52. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, and Xiaoxi Wang. 2013. “Economic Policy Uncertainty in China”. unpublished paper. University of Chicago. [Google Scholar]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The Unprecedented Stock Market Reaction to COVID-19: Vol. Covid Econ. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Balli, Faruk, Anne de Bruin, Md Iftekhar Hasan Chowdhury, and Muhammad Abubakr Naeem. 2019. Connectedness of cryptocurrencies and prevailing uncertainties. Applied Economics Letters 27: 1316–22. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Lai T. Hoang. 2020. A crypto safe haven against Bitcoin. Finance Research Letters 38: 101431. [Google Scholar] [CrossRef]

- Beneki, Christina, Alexandros Koulis, Nikolaos A. Kyriazis, and Stephanos Papadamou. 2019. Research in International Business and Finance Investigating volatility transmission and hedging properties between Bitcoin and Ethereum. Research in International Business and Finance 48: 219–27. [Google Scholar] [CrossRef]

- Bouri, Elie, and Rangan Gupta. 2019. Predicting Bitcoin returns: Comparing the roles of newspaper- and internet search-based measures of uncertainty. Finance Research Letters 38: 101398. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Brian Lucey, and David Roubaud. 2019. Cryptocurrencies and the downside risk in equity investments. Finance Research Letters 33: 101211. [Google Scholar] [CrossRef]

- Bouri, Elie, Georges Azzi, and Anne Haubo Dyhrberg. 2017a. On the return-volatility relationship in the Bitcoin market around the price crash of 2013. Economics 11: 1–17. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Naji Jalkh, Peter Molnár, and David Roubaud. 2017b. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017c. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, Aviral Kumar Tiwari, and David Roubaud. 2017d. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Finance Research Letters 23: 87–95. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Rangan Gupta, Chi Keung Marco Lau, David Roubaud, and Shixuan Wang. 2018. Bitcoin and Global Financial Stress: A Copula-Based Approach to Dependence and Causality-in-Quantiles. The Quarterly Review of Economics and Finance 69: 297–307. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Konstantinos Gkillas, and Rangan Gupta. 2020a. Trade uncertainties and the hedging abilities of Bitcoin. Economic Notes 49: 1–10. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2020b. Cryptocurrencies as hedges and safe-havens for US equity sectors. Quarterly Review of Economics and Finance 75: 294–307. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, Menelaos Karanasos, and Stavroula Yfanti. 2019. Macro-Financial Linkages in the High- Frequency Domain: The Effects of Uncertainty on Realized Volatility. Social Science Research Network, Working Paper 1922. Available online: https://www.econstor.eu/bitstream/10419/215002/1/cesifo1wp8000.pdf (accessed on 7 September 2021).

- Caporin, Massimiliano, and Michael McAleer. 2013. Ten things you should know about the dynamic conditional correlation representation. Econometrics 1: 115–26. [Google Scholar] [CrossRef] [Green Version]

- Cerda, Rodrigo, Alvaro Silva, and José Tomás Valente. 2018. Impact of economic uncertainty in a small open economy: The case of Chile. Applied Economics 50: 2894–908. [Google Scholar] [CrossRef]

- Cheema, Muhammad A., Kenneth Szulczuk, and Elie Bouri. 2020. Predicting Cryptocurrency Returns Based on Economic Policy Uncertainty: A Multicountry Analysis Using Linear and Quantile-Based Models. SSRN Electronic Journal, 1–34. [Google Scholar] [CrossRef]

- Chen, Tiejun, Chi Keung Marco Lau, Sadaf Cheema, and Chun Kwong Koo. 2021. Economic Policy Uncertainty in China and Bitcoin Returns: Evidence From the COVID-19 Period. Frontiers in Public Health 9: 1–7. [Google Scholar] [CrossRef]

- Cheng, Hui-Pei, and Kuang-Chieh Yen. 2020. The relationship between the economic policy uncertainty and the cryptocurrency market. Finance Research Letters 35: 101308. [Google Scholar] [CrossRef]

- Choudhary, M. Ali, Farooq Pasha, and Mohsin Waheed. 2020. Measuring Economic Policy Uncertainty in Pakistan. Available online: https://mpra.ub.uni-muenchen.de/100013/1/MPRA_paper_100013.pdf (accessed on 7 September 2021).

- CoinMarketCap. 2020. Percentage of Total Market Capitalization (Dominance). Available online: https://coinmarketcap.com/charts/#dominance-percentage (accessed on 5 August 2021).

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2021. The effect of political and economic uncertainty on the cryptocurrency market. Finance Research Letters 39: 101621. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018a. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2018b. Datestamping the Bitcoin and Ethereum bubbles. Finance Research Letters 26: 81–88. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019a. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2019b. KODAKCoin: A blockchain revolution or exploiting a potential cryptocurrency bubble? Applied Economics Letters 21: 518–24. [Google Scholar] [CrossRef]

- Da, Zhi, Joseph Engelberg, and Pengjie Gao. 2015. The sum of all FEARS investor sentiment and asset prices. Review of Financial Studies 28: 1–32. [Google Scholar] [CrossRef] [Green Version]

- Davis, Steven J. 2016. An Index of Global Economic Policy Uncertainity. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Demir, Ender, Giray Gozgor, Chi Keung Marco Lau, and Samuel A. Vigne. 2018. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters 26: 145–49. [Google Scholar] [CrossRef] [Green Version]

- Donadelli, Michael, and Lauren Persha. 2014. Understanding emerging market equity riskpremia: Industries, governance andmacroeconomic policy uncertainty. Research in International Business and Finance 30: 284–309. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2015a. Hedging capabilities of Bitcoin is it the virtual gold? Finance Research Letters 16: 139–44. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, Anne Haubo. 2015b. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef] [Green Version]

- Evans, John L., and Stephen H. Archer. 1968. Diversification and the Reduction of Dispersion: An Empirical Analysis. The Journal of Finance 23: 761–67. [Google Scholar]

- Fang, Libing, Elie Bouri, Rangan Gupta, and David Roubaud. 2019. Does global economic uncertainty matter for the volatility and hedging effectiveness of Bitcoin? International Review of Financial Analysis 61: 29–36. [Google Scholar] [CrossRef]

- Fang, Tong, Zhi Su, and Libo Yin. 2020. Economic fundamentals or investor perceptions? The role of uncertainty in predicting long-term cryptocurrency volatility. International Review of Financial Analysis 71: 101566. [Google Scholar] [CrossRef]

- Fasanya, Ismail O., Johnson A. Oliyide, Oluwasegun B. Adekoya, and Taofeek Agbatogun. 2021. How does economic policy uncertainty connect with the dynamic spillovers between precious metals and Bitcoin markets? Resources Policy 72: 102077. [Google Scholar] [CrossRef]

- Foglia, Matteo, and Peng-Fei Dai. 2021. “Ubiquitous uncertainties”: Spillovers across economic policy uncertainty and cryptocurrency uncertainty indices. Journal of Asian Business and Economic Studies. [Google Scholar] [CrossRef]

- Geissdoerfer, Martin, Paulo Savaget, Nancy M.P. Bocken, and Erik Jan Hultink. 2017. The Circular Economy—A new sustainability paradigm? Journal of Cleaner Production 143: 757–68. [Google Scholar] [CrossRef] [Green Version]

- Ghirelli, Corinna, Javier J. Pérez, and Alberto Urtasun. 2019. A new economic policy uncertainty index for Spain. Economics Letters 182: 64–67. [Google Scholar] [CrossRef] [Green Version]

- Gil, Mauricio, and Daniel Silva. 2018. Economic Policy Uncertainty Indices for Colombia. In Deutch Bank Research. Available online: http://www.policyuncertainty.com/methodology.html (accessed on 7 September 2021).

- Haq, Inzamam Ul, and Tahir Mumtaz Awan. 2020. Impact of e-banking service quality on e-loyalty in pandemic times through interplay of e-satisfaction. Vilakshan XIMB Journal of Management 17: 39–55. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul, Supat Chupradit, and Chunhui Huo. 2021. Do Green Bonds Act as a Hedge or a Safe Haven against Economic Policy Uncertainty? Evidence from the USA and China. International Journal of Financial Studies 9: 40. [Google Scholar] [CrossRef]

- Hardouvelis, Gikas A., Georgios Karalas, Dimitrios Karanastasis, and Panagiotis Samartzis. 2018. Economic Policy Uncertainty, Political Uncertainty and the Greek Economic Crisis. SSRN Electronic Journal. [Google Scholar] [CrossRef] [Green Version]

- Harwick, C. 2016. Cryptocurrency and the problem of intermediation. Independent Review 20: 569–88. [Google Scholar] [CrossRef]

- Hasan, Md Bokhtiar, M. Kabir Hassan, Zulkefly Abdul Karim, and Md Mamunur Rashid. 2021. Exploring the hedge and safe haven properties of cryptocurrency in policy uncertainty. Finance Research Letters, 102272. [Google Scholar] [CrossRef]

- Hassan, Tarek A., Stephan Hollander, Laurence Van Lent, and Ahmed Tahoun. 2019. Firm-level political risk: Measurement and effects. Quarterly Journal of Economics 134: 2135–202. [Google Scholar] [CrossRef] [Green Version]

- Hoang, Lai T., and Dirk G. Baur. 2020. How Stable Are Stablecoins? SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Jiang, Yonghong, Lanxin Wu, Gengyu Tian, and He Nie. 2021. Do cryptocurrencies hedge against EPU and the equity market volatility during COVID-19?—New evidence from quantile coherency analysis. Journal of International Financial Markets, Institutions and Money 72: 101324. [Google Scholar] [CrossRef]

- Julio, Brandon, and Youngsuk Yook. 2012. Political uncertainty and corporate investment cycles. Journal of Finance 67: 45–83. [Google Scholar] [CrossRef]

- Kalyvas, Antonios, Panayiotis Papakyriakou, Athanasios Sakkas, and Andrew Urquhart. 2020. What drives Bitcoin’s price crash risk? Economics Letters 191: 108777. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019. High frequency volatility co-movements in cryptocurrency markets. Journal of International Financial Markets, Institutions and Money 62: 35–52. [Google Scholar] [CrossRef]

- Khaldi, Rohaifa, Abdellatif El Afia, and Raddouane Chiheb. 2019. Forecasting of BTC volatility: Comparative study between parametric and nonparametric models. Progress in Artificial Intelligence 8: 511–23. [Google Scholar] [CrossRef]

- Kido, Yosuke. 2016. On the link between the US economic policy uncertainty and. Economics Letters 144: 49–52. [Google Scholar] [CrossRef]

- Koki, Constandina, Stefanos Leonardos, and Georgios Piliouras. 2019. A Peek into the Unobservable: Hidden States and Bayesian Inference for the Bitcoin and Ether Price Series. arXiv arXiv:1909.10957. [Google Scholar]

- Koumba, Ur, Calvin Mudzingiri, and Jules Mba. 2020. Does uncertainty predict cryptocurrency returns? A copula-based approach. Macroeconomics and Finance in Emerging Market Economies 13: 67–88. [Google Scholar] [CrossRef]

- Kristjanpoller, Werner, and Elie Bouri. 2019. Asymmetric multifractal cross-correlations between the main world currencies and the main cryptocurrencies. Physica A: Statistical Mechanics and Its Applications 523: 1057–71. [Google Scholar] [CrossRef]

- Kroese, Lars, Suzanne Kok, and Jante Parlevliet. 2015. Beleidsonzekerheid in nederland. Economisch Statistiche Berichten 4715: 464–67. [Google Scholar]

- Kyriazis, Nikolaos A. 2021. The nexus of sophisticated digital assets with economic policy uncertainty: A survey of empirical findings and an empirical investigation. Sustainability 13: 5383. [Google Scholar] [CrossRef]

- Lucey, Brian M., Samuel A. Vigne, Larisa Yarovaya, and Yizhi Wang. 2021. The cryptocurrency uncertainty index. Finance Research Letters 10: 102147. [Google Scholar] [CrossRef]

- Luk, Paul, Michael Cheng, Philip Ng, and Ken Wong. 2017. Economic Policy Uncertainty Spillovers in Small Open Economies: The Case of Hong Kong. Pacific Economic Review 25: 21–46. [Google Scholar] [CrossRef]

- Manela, Asaf, and Alan Moreira. 2016. News implied volatility and disaster concerns. Journal of Financial Economics 123: 137–62. [Google Scholar] [CrossRef]

- Matkovskyy, Roman, Akanksha Jalan, and Michael Dowling. 2020. Effects of economic policy uncertainty shocks on the interdependence between Bitcoin and traditional financial markets. Quarterly Review of Economics and Finance 77: 150–55. [Google Scholar] [CrossRef]

- Mokni, Khaled. 2021. When, where, and how economic policy uncertainty predicts Bitcoin returns and volatility? A quantiles-based analysis. Quarterly Review of Economics and Finance 80: 65–73. [Google Scholar] [CrossRef]

- Mokni, Khaled, Ahdi Noomen Ajmi, Elie Bouri, and Xuan Vinh Vo. 2020. Economic policy uncertainty and the Bitcoin-US stock nexus. Journal of Multinational Financial Management 58: 1–13. [Google Scholar] [CrossRef]

- Murphy, Edward V., M. Maureen Murphy, and Michael V. Seitzinger. 2015. Bitcoi: Questions, Answers, and Analysis of Legal Issues; Washington, DC: Congressional Research Service.

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Journal for General Philosophy of Science 39: 53–67. [Google Scholar] [CrossRef]

- Newey, Whitney K., and Kenneth D. West. 1987. Hypothesis Testing with Efficient Method of Moments Estimation. International Economic Review 28: 777. [Google Scholar] [CrossRef]

- Nguyen, Khanh Q. 2020. Conditional Beta and Uncertainty Factor in the Cryptocurrency Pricing Model. arXiv arXiv:2010.12736. [Google Scholar]

- Nie, Wei-Ying, Hui-Pei Cheng, and Kuang-Chieh Yen. 2020. Investor Sentiment and the Cryptocurrency Market Investor Sentiment and the Cryptocurrency Market. Empirical Economics Letters 19: 1254–62. [Google Scholar]

- Papadamou, Stephanos, Nikolaos A. Kyriazis, and Panayiotis G. Tzeremes. 2021. Non-linear causal linkages of EPU and gold with major cryptocurrencies during bull and bear markets. North American Journal of Economics and Finance 56: 101343. [Google Scholar] [CrossRef]

- Parino, Francesco, Mariano G. Beiró, and Laetitia Gauvin. 2018. Analysis of the Bitcoin blockchain: Socio-economic factors behind the adoption. EPJ Data Science 7: 38. [Google Scholar] [CrossRef]

- Park, Minjung, and Sangmi Chai. 2020. The Effect of Information Asymmetry on Investment Behavior in Cryptocurrency Market. Proceedings of the 53rd Hawaii International Conference on System Sciences 3: 4043–52. [Google Scholar] [CrossRef] [Green Version]

- Paule-Vianez, Jessica, Camilo Prado-Román, and Raúl Gómez-Martínez. 2020. Economic policy uncertainty and Bitcoin. Is Bitcoin a safe-haven asset? European Journal of Management and Business Economics 29: 347–63. [Google Scholar] [CrossRef] [Green Version]

- Qin, Meng, Chi-Wei Su, and Ran Tao. 2021. Bitcoin: A new basket for eggs? Economic Modelling, February 94: 896–907. [Google Scholar] [CrossRef]

- Raheem, Ibrahim D. 2021. COVID-19 pandemic and the safe haven property of Bitcoin. Quarterly Review of Economics and Finance 81: 370–75. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, and Aristeidis Samitas. 2021. Are Cryptos Safe-Haven Assets during COVID-19? Evidence from Wavelet Coherence Analysis. Emerging Markets Finance and Trade 57: 1741–56. [Google Scholar] [CrossRef]

- Scotti, Chiara. 2016. Surprise and uncertainty indexes: Real-time aggregation. Journal of Monetary Economics 82: 1–19. [Google Scholar] [CrossRef] [Green Version]

- Shaikh, Imlak. 2020. Policy uncertainty and Bitcoin returns. Borsa Istanbul Review 20: 257–68. [Google Scholar] [CrossRef]

- Sorić, Petar, and Ivana Lolić. 2017. Economic uncertainty and its impact on the Croatian economy. Public Sector Economics 41: 443–77. [Google Scholar] [CrossRef]

- Su, Chi-Wei, Meng Qin, Ran Tao, and Xiaoyan Zhang. 2020. Is the status of gold threatened by Bitcoin? Economic Research-Ekonomska Istrazivanja 33: 420–37. [Google Scholar] [CrossRef]

- Wang, Gang-Jin, Chi Xie, Danyan Wen, and Longfeng Zhao. 2019a. When Bitcoin meets economic policy uncertainty (EPU): Measuring risk spillover effect from EPU to Bitcoin. Finance Research Letters 31: 489–97. [Google Scholar] [CrossRef]

- Wang, Pengfei, Wei Zhang, Xiao Li, and Dehua Shen. 2019b. Is cryptocurrency a hedge or a safe haven for international indices? A comprehensive and dynamic perspective. Finance Research Letters Journal 31: 1–18. [Google Scholar] [CrossRef]

- Wang, Yaw-Huei, and Kuang-Chieh Yen. 2019. The information content of the implied volatility term structure on future returns. European Financial Management 25: 380–406. [Google Scholar] [CrossRef]

- Wu, Shan, Mu Tong, Zhongyi Yang, and Abdelkader Derbali. 2019. Does gold or Bitcoin hedge economic policy uncertainty? Finance Research Letters 31: 171–78. [Google Scholar] [CrossRef]

- Wu, Wanshan, Aviral Kumar Tiwari, Giray Gozgor, and Huang Leping. 2021. Does economic policy uncertainty affect cryptocurrency markets? Evidence from Twitter-based uncertainty measures. Research in International Business and Finance 58: 101478. [Google Scholar] [CrossRef]

- Yen, Kuang-Chieh, and Hui-Pei Cheng. 2021. Economic policy uncertainty and cryptocurrency volatility. Finance Research Letters 38: 101428. [Google Scholar] [CrossRef]

- Yu, Miao, and Jinguo Song. 2018. Volatility forecasting: Global economic policy uncertainty and regime switching. Physica A: Statistical Mechanics and Its Applications 511: 316–23. [Google Scholar] [CrossRef]

- Zalla, Ryan. 2017. Economic Policy Uncertainty in Ireland. Atlantic Economic Journal 45: 269–71. [Google Scholar] [CrossRef]

Figure 1.

Flow Diagram for screening and management process. Note: This diagram depicts the whole screening and selection process of related studies used in analyzing the current literature review.

Figure 1.

Flow Diagram for screening and management process. Note: This diagram depicts the whole screening and selection process of related studies used in analyzing the current literature review.

Figure 2.

Percentage of Total Market Capitalization (Dominance). Source: https://coinmarketcap.com/ (accessed on 5 August 2021). Note: This figure demonstrates the dominance of Bitcoin in the crypto market.

Figure 2.

Percentage of Total Market Capitalization (Dominance). Source: https://coinmarketcap.com/ (accessed on 5 August 2021). Note: This figure demonstrates the dominance of Bitcoin in the crypto market.

Figure 3.

Data coverage in years. Note: This figure portrays the data covered by previous research from 2010 to 2021, left side is indicating the author names and year of publication and black horizontal bars are indicating set data covered by studies in years.

Figure 3.

Data coverage in years. Note: This figure portrays the data covered by previous research from 2010 to 2021, left side is indicating the author names and year of publication and black horizontal bars are indicating set data covered by studies in years.

Figure 4.

Percentage of total Bitcoin nodes. Source: https://thenextweb.com/ (accessed on 1 September 2021). Note: This figure highlights countries with highest to lowest nodes around the globe. USA and Germany are the leader of Bitcoin node around the globe and including France they are holding over half of world Bitcoin nodes.

Figure 4.

Percentage of total Bitcoin nodes. Source: https://thenextweb.com/ (accessed on 1 September 2021). Note: This figure highlights countries with highest to lowest nodes around the globe. USA and Germany are the leader of Bitcoin node around the globe and including France they are holding over half of world Bitcoin nodes.

Figure 5.

This figure illustrates sources used by previous studies to retrieve the secondary data for cryptocurrencies. The most frequently used platform was www.coinmarketcap.com, covering around 37% of studies data collection source, and www.bitstamp.net is least employed source for cryptos data.

Figure 5.

This figure illustrates sources used by previous studies to retrieve the secondary data for cryptocurrencies. The most frequently used platform was www.coinmarketcap.com, covering around 37% of studies data collection source, and www.bitstamp.net is least employed source for cryptos data.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Available EPU Indices.

| Authors | EPU Index | |

|---|---|---|

| 1 | Baker et al. (2016) | USA, Brazil, Canada, Australia, France, India, Germany, United Kingdome, South Korea, Russia, Mexico, Italy, and Europe. |

| 2 | Algaba et al. (2020) | Belgium |

| 3 | Cerda et al. (2018) | Chile |

| 4 | Baker et al. (2013) | China |

| 5 | Gil and Silva (2018) | Columbia |

| 6 | Sorić and Lolić (2017) | Croatia |

| 7 | Hardouvelis et al. (2018) | Greece |

| 8 | Zalla (2017) | Ireland |

| 9 | Luk et al. (2017) | Hong Kong |

| 10 | Arbatli et al. (2019) | Japan |

| 11 | Kroese et al. (2015) | Netherlands |

| 12 | Choudhary et al. (2020) | Pakistan |

| 13 | Davis (2016) | Global and Singapore |

| 14 | Ghirelli et al. (2019) | Spain |

| 15 | Armelius et al. (2017) | Sweden |

Note: This table highlights that EPU index is available for 26 countries along with a global EPU index. Countries and authors with year of publication is mentioned in the table.

Table 2.

Key Characteristics of Included Research.

| No | Title | Authors & Year | Reason | Employed Methodology | Frequency | Data Source | Data Coverage | Findings |

|---|---|---|---|---|---|---|---|---|

| 1 | Policy uncertainty and Bitcoin returns | (Shaikh 2020) | Bitcoin returns and EPU, MPU and VIX | Quantile Regression and Marko Regime-Switching | Monthly/Daily | www.coindesk.com www.policyuncertainity.com | 2010–2018 | Bitcoin return’s responsiveness to EPU |

| 2 | Gold & Bitcoin as a hedge again EPU | (Wu et al. 2019) | Hedge and safe-haven | GARCH Model and Quantile Regression | Daily | www.investing.com www.policyuncertainity.com | 2012–2018 | Gold and Bitcoin are not strong hedge and safe-haven |

| 3 | Measuring risk spillover from EPU to Bitcoin | (Wang et al. 2019a) | Risk Spillover | Multivariate Quantiles Model & Granger Causality Test | Daily | www.coindesk.com www.policyuncertainity.com | 2010–2018 | Negligible risk spillover from EPU to Bitcoin |

| 4 | Does EPU predicts the Bitcoin returns. | (Demir et al. 2018) | Predictive Power of EPU on Bitcoin returns | OLS and QQ Regression | Daily | www.coindesk.com www.policyuncertainity.com | 2010–2017 | EPU holds strong Predictive power on Bitcoin Returns |

| 5 | Is Bitcoin a new egg in the basket? | (Qin et al. 2021) | Risk mitigation role of Bitcoin | Granger Causality Test | Monthly | www.yahoofinance.com www.policyuncertainity.com | 2010–2019 | Mixed (positive/negative) impact on Bitcoin returns |

| 6 | EPU and Cryptocurrency returns | (Cheng and Yen 2020) | Risk management and responsiveness | Predictive Regression Model | Daily | www.coinmarketcap.com www.policyuncertainity.com | 2014–2019 | Positive association between Chinese EPU and Cryptocurrency market |

| 7 | Uncertainty predict cryptocurrency returns | (Koumba et al. 2020) | EPU impact of Cryptocurrency returns in financial crisis Risk Management | D-Vine Copula | Daily | www.coingeko.com www.policyuncertainity.com | 2015–2018 | Ethereum is better hedge in cryptocurrency market |

| 8 | Cryptocurrency volatility, hedging effectiveness and EPU | (Fang et al. 2019) | Long-run global volatility hedging | GARCH-MIDAS | Monthly | www.coindesk.com www.policyuncertainity.com | 2010–2018 | EPU as a source of plunged volatility in Bitcoin market |

| 9 | Cryptocurrency and downsize risk | (Bouri et al. 2019) | Diversifier role of Bitcoin | DCC-GARCH Model | Daily | www.coinmarketcap.com www.datastream.com | 2015–2018 | Bitcoin, Ethereum and Litecoin are hedge. |

| 10 | Global financial stress and Bitcoin returns | (Bouri et al. 2018) | Bitcoin return Predictability | Copula based Model Granger Causality Cross-Quantilogram | Daily | www.coindesk.com | 2010–2017 | Right tail dependence between uncertainty and Bitcoin |

| 11 | Bitcoin and major stock indexes | (Bouri et al. 2017c) | Bitcoin as a hedge and safe0haven | DCC-GARCH Model | Daily/weekly | www.datastream.com | 2011–2015 | Strong safe-haven properties of Bitcoin in Asia |

| 12 | Linkage of Bitcoin and Commodities | (Bouri et al. 2017b) | Bitcoin as Hedge, Safe-haven and Diversifier | DCC-GARCH Model | Daily | www.coindesk.com | 2010–2015 | Hedge and safe-haven in Pre-Bitcoin price crash and diversifier in post-period |

| 13 | Bitcoin and Global EPU | (Bouri et al. 2017d) | Hedging properties of Bitcoin | Wavelet Quantile-on-Quantile approach | Daily | www.coindesk.com www.datastream.com | 2011–2016 | Bitcoin is a hedge against global uncertainty |

| 14 | Volatility and cryptocurrency return relationship | (Bouri et al. 2017a) | Co-Movements and hedging | Asymmetric GARCH Model | Daily | wwwbitstamp.com | 2011–2016 | No Asymmetric return volatility relationship |

| 15 | Predicting Bitcoin returns | (Bouri and Gupta 2019) | New-based and internet search-based EPU measures predictability | EGARCH | Monthly | www.cryptocompare.com www.policyuncertainty.com | 2010–2019 | Bitcoin works as hedge against both measures. |

| 16 | Bitcoin and international indices | (Wang et al. 2019b) | Hedge and safe-haven properties | DCC-GARCH | Daily | www.coinmarketcap.com | 2013–2018 | Cryptocurrencies are more safe-haven than a hedge |

| 17 | EPU and Bitcoin Investment | (Al Mamun et al. 2020) | Impact of EPU on securities correlation patterns | DCC-GJR-GARCH | Daily | www.coindesk.com | 2010–2016 | EPU and GPU hold strong impact during unfavorable economic and financial periods |

| 18 | Bitcoin prices crash and EPU association | (Kalyvas et al. 2020) | EPU risk hedging | NCSKEW & DUVOL | Daily/Intra-day | www.bitcoincharts.com | 2011–2018 | Bitcoin can hedge EPU risks |