Designing an Intelligent Scoring System for Crediting Manufacturers and Importers of Goods in Industry 4.0

,

,  , , , and

, , , and

Abstract

:1. Introduction

- ▪

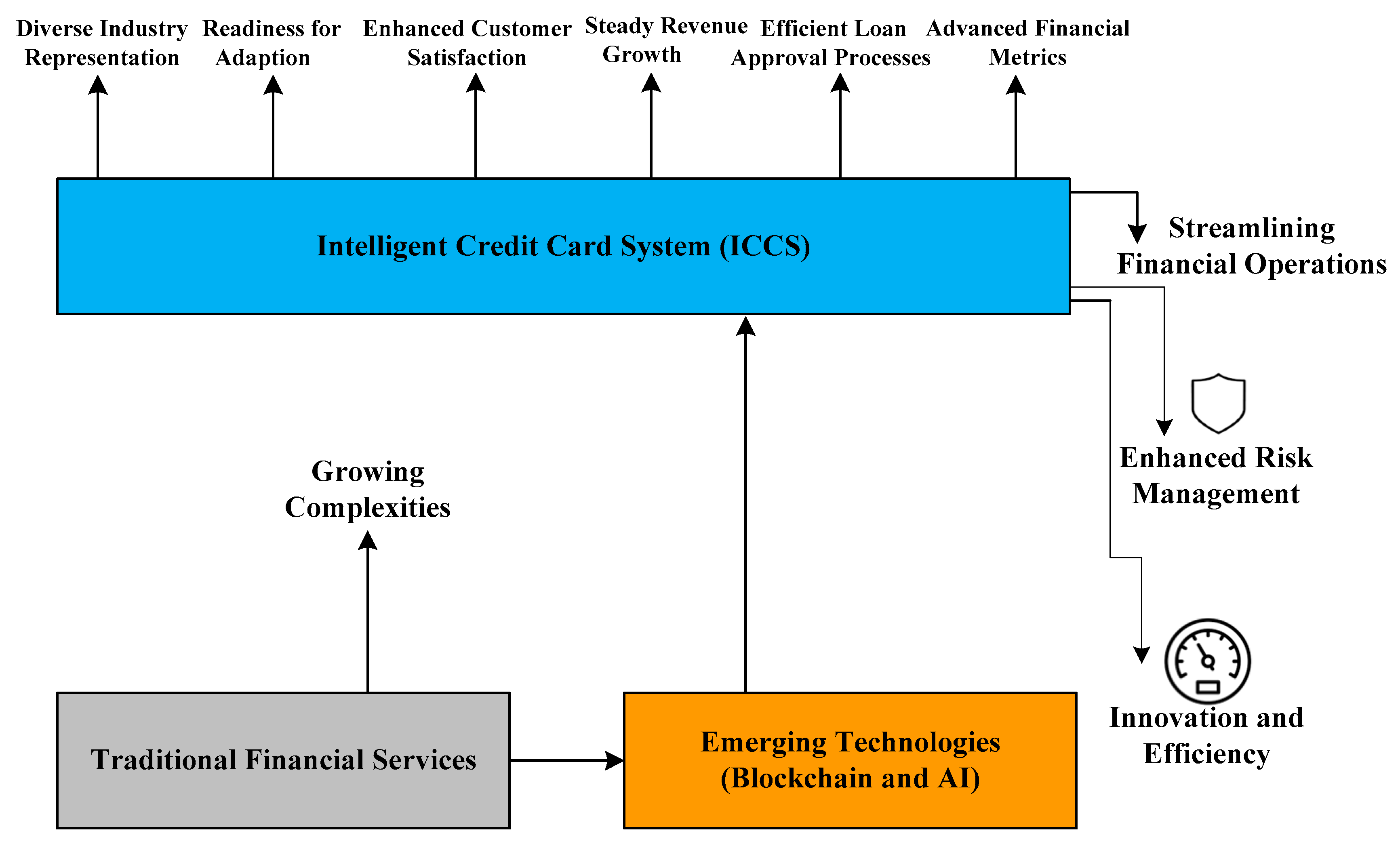

- The proposed study sheds light on the potential for advanced technologies like blockchain and AI to significantly enhance financial performance metrics, including credit scores, loan approval rates, default rates, revenue growth, and customer satisfaction. These findings underscore the transformative capabilities of modern financial systems.

- ▪

- This research highlights the potential of the intelligent credit card system to enhance the precision of credit assessments, which is of paramount importance to credit-dependent industries.

- ▪

- Efficient loan-approval processes are introduced that reveal the positive influence of blockchain and AI integration on loan approval efficiency, presenting practical insights for expediting and streamlining financial workflows in the manufacturing and importing sectors.

- ▪

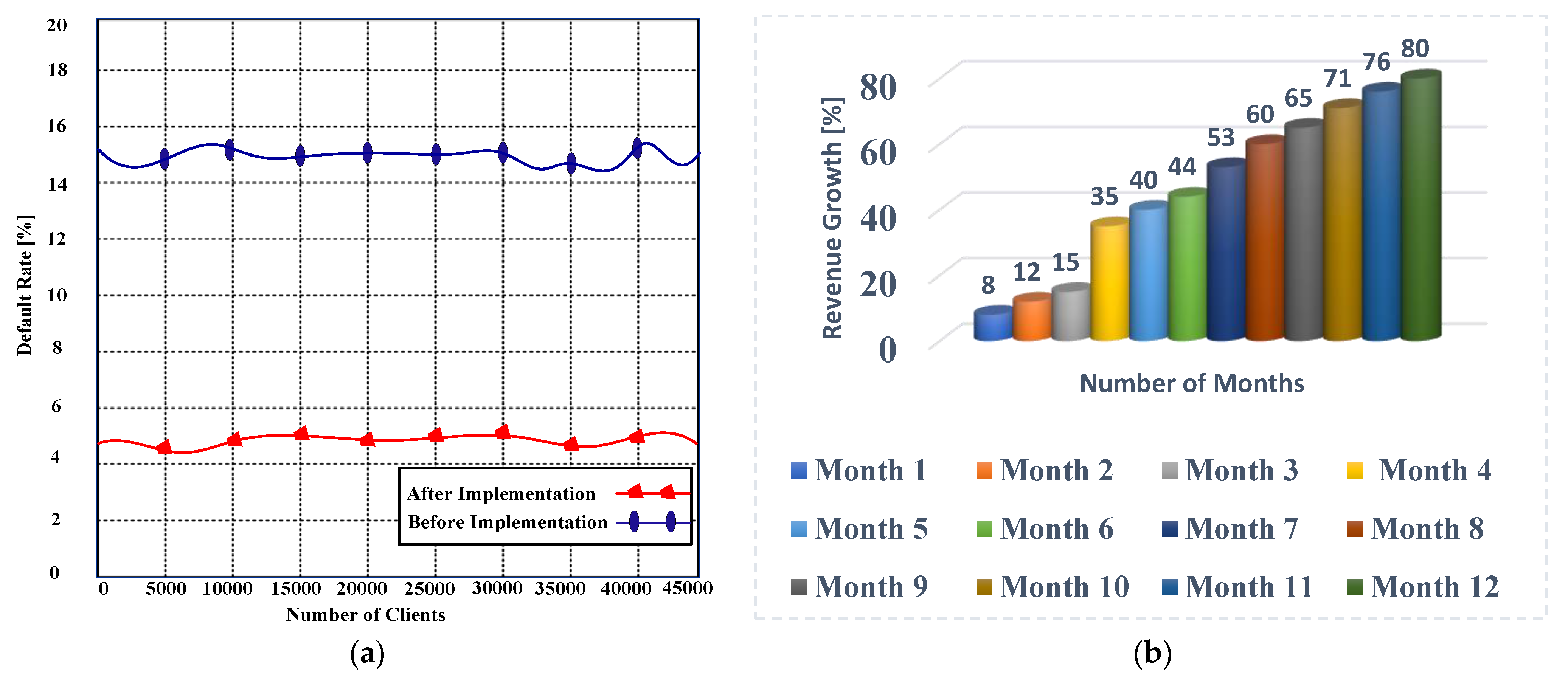

- A risk mitigation component is introduced that shows that the system effectively reduces default rates, which is crucial for ensuring the stability of financial operations. This mitigation of credit risks has the potential to reduce financial losses for manufacturers and importers.

- ▪

- Steady revenue growth is employed that demonstrates how the upward trajectory in revenue growth signifies the long-term financial benefits of implementing advanced technologies in financial systems. This finding provides a roadmap for achieving sustained financial prosperity.

- ▪

- An enhanced customer satisfaction metric is used to highlight the system’s role in building stronger customer relationships, which can lead to increased business growth and brand loyalty.

- ▪

- Readiness for adoption is used to reveal the readiness of a significant portion of participants to embrace innovative technology in their respective industries. This readiness underscores the potential for the rapid adoption and integration of advanced financial systems.

Paper Organization

2. Related Work

3. Research Methodology

3.1. Data Collection Methods

3.2. Data Analysis Method

3.3. Data Calculation Model

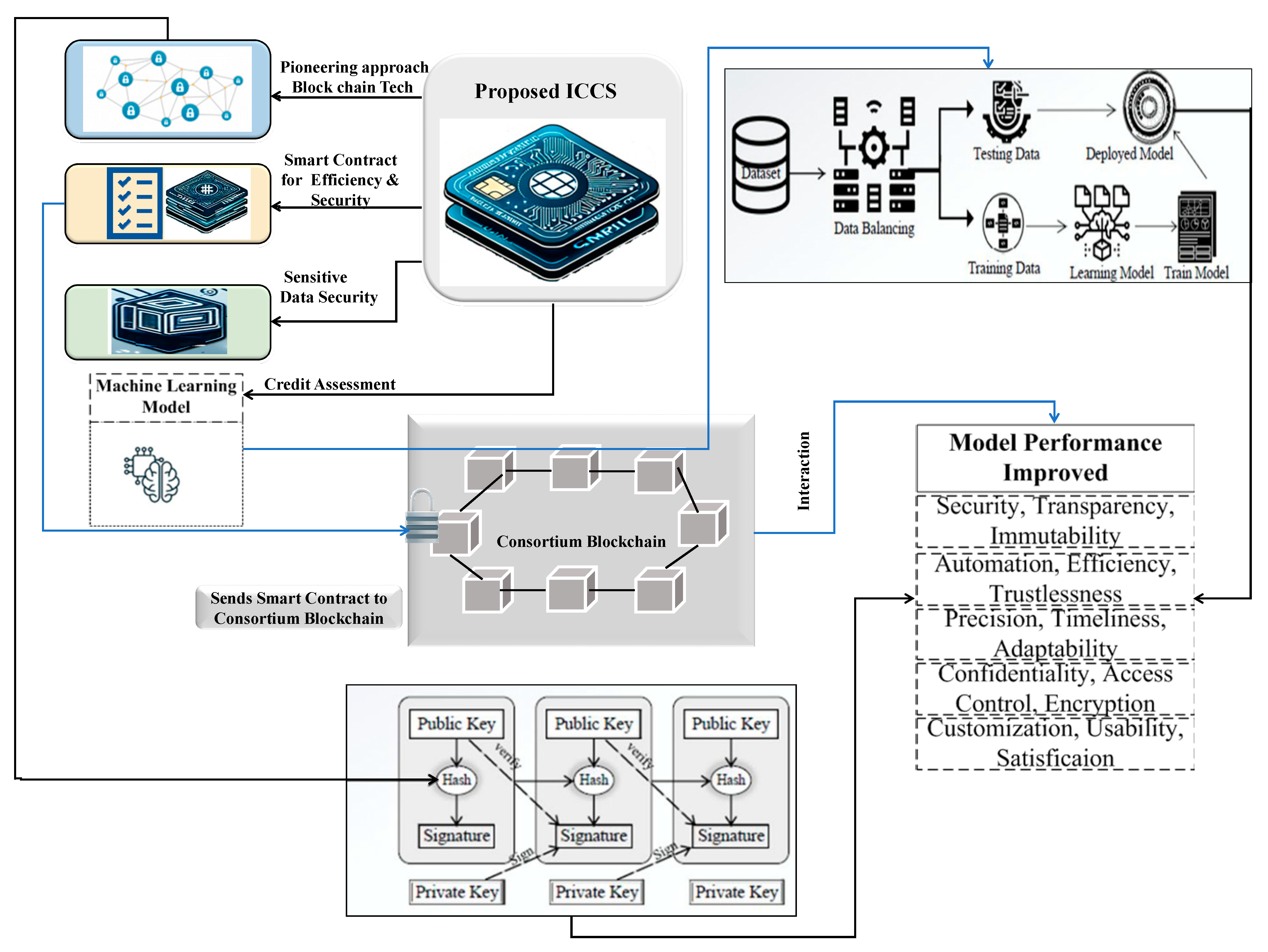

4. Proposed Method for the Intelligent Credit Card System

4.1. Blockchain-Based Security in Credit Cards

4.1.1. Security Distribution for Unassailable Transactions

4.1.2. Safeguarding Sensitive Financial Data

4.1.3. Financial Transformation Using Smart Contracts

4.1.4. Fostering Trust and Accountability Process

| Algorithm 1: Securing commodities using consortium blockchain technology |

|

5. Testing Process with Experimental Setup and Results

5.1. Testing Process

5.2. Experimental Setup

5.3. Results

- ▪

- Predicative credit risk forecasting;

- ▪

- Fraud detection;

- ▪

- Credit assessment accuracy;

- ▪

- Loan approval rate comparison;

- ▪

- Default rate reduction;

- ▪

- Monthly revenue growth trend.

5.3.1. Predictive Credit Risk Forecasting

5.3.2. Fraud Detection

5.3.3. Credit Assessment Accuracy

5.3.4. Loan Approval Rate Comparison

5.3.5. Default Rate Reduction

5.3.6. Monthly Revenue Growth Trend

6. Summary

6.1. Conclusions

6.2. Future Research Direction

6.3. Research Limitations and Challenges

6.4. Research Implications

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| Acronyms | Full Form |

| ICCS | intelligent credit card system |

| VAE | variational automatic coding |

| AI | artificial intelligence |

| ML | machine learning |

| UI | user interface |

| DPO | data protection officer |

| GDPR | general data protection regulation |

| CCPA | California Consumer Privacy Act |

| EEA | European Economic Area |

| DeFi | Decentralized Finance |

| RegTech | regulatory technology |

| CBDCs | central bank digital currencies |

| ERP | Enterprise Resource Planning |

References

- Taherdoost, H. Fintech: Emerging trends and the future of finance. Financ. Technol. DeFi A Revisit Digit. Financ. Revolut. 2023, 29–39. [Google Scholar] [CrossRef]

- Üçoğlu, D. Blockchain technology and future banking: Opportunities and challenges. Appl. Chall. Oppor. Blockchain Technol. Bank. Insur. 2022, 43–68. [Google Scholar] [CrossRef]

- Fernández, A. Artificial intelligence in financial services. Banco Esp. Artic. 2019, 3, 19. [Google Scholar] [CrossRef]

- Sadok, H.; Sakka, F.; Maknouzi, M.E.H.E.; McMillan, D. Artificial intelligence and bank credit analysis: A review. Cogent Econ. Financ. 2022, 10, 2023262. [Google Scholar] [CrossRef]

- Wang, Y.; Su, Z.; Zhang, N.; Xing, R.; Liu, D.; Luan, T.H.; Shen, X. A survey on metaverse: Fundamentals, security, and privacy. IEEE Commun. Surv. Tutor. 2022, 25, 319–352. [Google Scholar] [CrossRef]

- Nalgozhina, N.; Razaque, A.; Raissa, U.; Yoo, J. Developing Robotic Process Automation to Efficiently Integrate Long-Term Business Process Management. Technologies 2023, 11, 164. [Google Scholar] [CrossRef]

- Tingfei, H.; Guangquan, C.; Kuihua, H. Using variational auto encoding in credit card fraud detection. IEEE Access 2020, 8, 149841–149853. [Google Scholar] [CrossRef]

- Rao, P.; Kumar, S.; Chavan, M.; Lim, W.M. A systematic literature review on SME financing: Trends and future directions. J. Small Bus. Manag. 2023, 61, 1247–1277. [Google Scholar] [CrossRef]

- Patel, R.; Migliavacca, M.; Oriani, M.E. Blockchain in banking and finance: A bibliometric review. Res. Int. Bus. Financ. 2022, 62, 101718. [Google Scholar] [CrossRef]

- An, Y.J.; Choi, P.M.S.; Huang, S.H. Blockchain, cryptocurrency, and artificial intelligence in finance. In Fintech with Artificial Intelligence, Big Data, and Blockchain; Singapore: Singapore, 2021; pp. 1–34. [Google Scholar]

- Zetzsche, D.A.; Arner, D.W.; Buckley, R.P. Decentralized finance (defi). J. Financ. Regul. 2020, 6, 172–203. [Google Scholar] [CrossRef]

- Truby, J.; Brown, R.; Dahdal, A. Banking on AI: Mandating a proactive approach to AI regulation in the financial sector. Law Financial Mark. Rev. 2020, 14, 110–120. [Google Scholar] [CrossRef]

- Jaiwant, S.V. Artificial intelligence and personalized banking. In Handbook of Research on Innovative Management Using AI in Industry 5.0; IGI Global: Hershey, PA, USA, 2022; pp. 74–87. [Google Scholar]

- Ahmad, T.; Zhu, H.; Zhang, D.; Tariq, R.; Bassam, A.; Ullah, F.; AlGhamdi, A.S.; Alshamrani, S.S. Energetics Systems and artificial intelligence: Applications of industry 4.0. Energy Rep. 2022, 8, 334–361. [Google Scholar] [CrossRef]

- Wan, L.; Eyers, D.; Zhang, H. Evaluating the Impact of Network Latency on the Safety of Blockchain Transactions. In Proceedings of the 2019 IEEE International Conference on Blockchain (Blockchain), Atlanta, GA, USA, 14–17 July 2019; pp. 194–201. [Google Scholar]

- Yu, K.-P.; Tan, L.; Aloqaily, M.; Yang, H.; Jararweh, Y. Blockchain-Enhanced Data Sharing With Traceable and Direct Revocation in IIoT. IEEE Trans. Ind. Inform. 2021, 17, 7669–7678. [Google Scholar] [CrossRef]

- Bonyuet, D. Overview and impact of blockchain on auditing. Int. J. Digit. Account. Res. 2020, 20, 31–43. [Google Scholar] [CrossRef]

- Kalsoom, T.; Ahmed, S.; Rafi-ul-Shan, P.M.; Azmat, M.; Akhtar, P.; Pervez, Z.; Ur-Rehman, M. Impact of IOT on Manufacturing Industry 4.0: A new triangular systematic review. Sustainability 2021, 13, 12506. [Google Scholar] [CrossRef]

- Ahmed, S.; Kalsoom, T.; Ramzan, N.; Pervez, Z.; Azmat, M.; Zeb, B.; Rehman, M.U. Towards Supply Chain Visibility Using Internet of Things: A Dyadic Analysis Review. Sensors 2021, 21, 4158. [Google Scholar] [CrossRef]

- Azmat, M.; Thanou, E. Blockchain-Enabled Smart Contract Architecture in Supply Chain Design. In Blockchain Driven Supply Chain Management: A Multi-Dimensional Perspective; Springer Nature Singapore: Singapore, 2023; pp. 1–14. [Google Scholar]

- Azmat, M.; Ahmed, S.; Mubarik, M.S. Supply chain resilience in the fourth industrial revolution. In Supply Chain Resilience: Insights from Theory and Practice; Springer International Publishing: Cham, Switzerland, 2022; pp. 149–163. [Google Scholar]

- Chen, J.; Cai, T.; He, W.; Chen, L.; Zhao, G.; Zou, W.; Guo, L. A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry. Entropy 2020, 22, 95. [Google Scholar] [CrossRef]

- Smith, S.S. Blockchain, Artificial Intelligence and Financial Services: Implications and Applications for Finance and Accounting Professionals; Springer Nature: Berlin, Germany, 2019. [Google Scholar]

- Bui, T.-D.; Tsai, F.M.; Tseng, M.-L.; Tan, R.R.; Yu, K.D.S.; Lim, M.K. Sustainable supply chain management towards disruption and organizational ambidexterity: A data driven analysis. Sustain. Prod. Consum. 2021, 26, 373–410. [Google Scholar] [CrossRef]

- Zhang, J.; Thomas, C.; FragaLamas, P.; Fernández-Caramés, T.M. Deploying blockchain technology in the supply chain. In Computer Security Threats; Thomas, C., Fraga-Lamas, P., Fernández-Caramés, T.M., Eds.; Books on Demand GmbH: Norderstedt, Germany, 2019; p. 57. [Google Scholar]

- Cao, Z.; Shi, X. A systematic literature review of entrepreneurial ecosystems in advanced and emerging economies. Small Bus. Econ. 2021, 57, 75–110. [Google Scholar] [CrossRef]

- Rashid; Al-Mamun, A.; Roudaki, H.; Yasser, Q.R. An Overview of Corporate Fraud and its Prevention Approach. Australas. Account. Bus. Finance J. 2022, 16, 101–118. [Google Scholar] [CrossRef]

- Ahmad Naqishbandi, T.; Syed Mohammed, E.; Venkatesan, S.; Sonya, A.; Cengiz, K.; Banday, Y. Secure Blockchain-Based Mental Healthcare Framework:—A Paradigm Shift from Traditional to Advanced Analytics. In Quantum and Blockchain for Modern Computing Systems: Vision and Advancements: Quantum and Blockchain Technologies: Current Trends and Challenges; Springer International Publishing: Cham, Switzerland, 2022; pp. 341–364. [Google Scholar]

- Yang, F.; Qiao, Y.; Huang, C.; Wang, S.; Wang, X. An automatic credit scoring strategy (ACSS) using memetic evolutionary algorithm and neural architecture search. Appl. Soft Comput. 2021, 113, 107871. [Google Scholar] [CrossRef]

- Jameaba, M. Digitalization, Emerging Technologies, and Financial Stability: Challenges and Opportunities for the Indonesian Banking Industry and Beyond; Qeios: London, UK, 2022. [Google Scholar]

- Haleem, A.; Javaid, M.; Singh, R.P.; Suman, R.; Rab, S. Blockchain technology applications in healthcare: An overview. Int. J. Intell. Netw. 2021, 2, 130–139. [Google Scholar] [CrossRef]

- Süzen, A.A.; Duman, B. Blockchain-Based Secure Credit Card Storage System for E-Commerce. Sak. Univ. J. Comput. Inf. Sci. 2021, 4, 204–215. [Google Scholar] [CrossRef]

- Mohanty, D.; VorugantI, N.K.; Patel, C.; Manglani, T. Implementing Blockchain Technology for Fraud Detection in Financial Management. BioGecko 2023, 12, 2. [Google Scholar]

- Mapa Mudiyanselage, C.; Perera, P.; Grandhi, S. A Blockchain-Based Model for the Prevention of Superannuation Fraud: A Study of Australian Super Funds. Appl. Sci. 2023, 13, 9949. [Google Scholar] [CrossRef]

- Chen, Y.; Bellavitis, C. Blockchain disruption and decentralized finance: The rise of decentralized business models. J. Bus. Ventur. Insights 2020, 13, e00151. [Google Scholar] [CrossRef]

- Kamran, R.; Khan, N.; Sundarakani, B. Blockchain technology development and implementation for global logistics operations: A reference model perspective. J. Glob. Oper. Strat. Sourc. 2021, 14, 360–382. [Google Scholar] [CrossRef]

- Hewa, T.M.; Hu, Y.; Liyanage, M.; Kanhare, S.S.; Ylianttila, M. Survey on Blockchain-Based Smart Contracts: Technical Aspects and Future Research. IEEE Access 2021, 9, 87643–87662. [Google Scholar] [CrossRef]

- Sunny, J.; Undralla, N.; Pillai, V.M. Supply chain transparency through blockchain-based traceability: An overview with demonstration. Comput. Ind. Eng. 2020, 150, 106895. [Google Scholar] [CrossRef]

- Saheed, Y.K.; Baba, U.A.; Raji, M.A. Big Data Analytics for Credit Card Fraud Detection Using Supervised Machine Learning Models. In Big Data Analytics in the Insurance Market; Emerald Publishing Limited: Bradford, UK, 2022; pp. 31–56. [Google Scholar]

- Gandomi, A.H.; Chen, F.; Abualigah, L. Machine Learning Technologies for Big Data Analytics. Electronics 2022, 11, 421. [Google Scholar] [CrossRef]

- Zhou, T.; Zhang, F.; Shao, K.; Li, K.; Huang, W.; Luo, J.; Hao, J. Cooperative multi-agent transfer learning with level-adaptive credit assignment. arXiv 2021, arXiv:2106.00517. [Google Scholar]

- Shen, H.; Kurshan, E. Deep Q-network-based adaptive alert threshold selection policy for payment fraud systems in retail banking. In Proceedings of the First ACM International Conference on AI in Finance, New York, NY, USA, 15–16 October 2020; pp. 1–7. [Google Scholar] [CrossRef]

- Cirqueira, D.; Helfert, M.; Bezbradica, M. Towards design principles for user-centric explainable AI in fraud detection. In International Conference on Human-Computer Interaction; Springer International Publishing: Cham, Switzerland, 2021; pp. 21–40. [Google Scholar]

- Najjar, L.J. Advances in e-commerce user interface design. In Human Interface and the Management of Information. Interacting with Information: Symposium on Human Interface 2011, Held as Part of HCI International 2011, Orlando, FL, USA, July 9–14, 2011, Proceedings, Part II; Springer: Berlin/Heidelberg, Germany, 2011; pp. 292–300. [Google Scholar]

- Chatzimparmpas, A.; Martins, R.M.; Jusufi, I.; Kucher, K.; Rossi, F.; Kerren, A. The State of the Art in Enhancing Trust in Machine Learning Models with the Use of Visualizations. Comput. Graph. Forum 2020, 39, 713–756. [Google Scholar] [CrossRef]

- Choi, J. Modeling the intergrated customer loyalty program on blockchain technology by using credit card. Int. J. Future Revolut. Comput. Sci. Commun. Eng. 2018, 4, 388–391. [Google Scholar]

- Balagolla, E.M.S.W.; Fernando, W.P.C.; Rathnayake, R.M.N.S.; Wijesekera, M.J.M.R.P.; Senarathne, A.N.; Abeywardhana, K.Y. Credit card fraud prevention using blockchain. In Proceedings of the 2021 6th International Conference for Convergence in Technology (I2CT), Maharashtra, India, 2–4 April 2021; pp. 1–8. [Google Scholar]

- Cherif, A.; Badhib, A.; Ammar, H.; Alshehri, S.; Kalkatawi, M.; Imine, A. Credit card fraud detection in the era of disruptive technologies: A systematic review. J. King Saud Univ.-Comput. Inf. Sci. 2022, 35, 145–174. [Google Scholar] [CrossRef]

- Baliker, C.; Baza, M.; Alourani, A.; Alshehri, A.; Alshahrani, H.; Choo, K.K.R. On the Applications of Blockchain in FinTech: Advancements and Opportunities. IEEE Trans. Eng. Manag. 2024, 71, 5669–5690. [Google Scholar] [CrossRef]

- Hashemi Joo, M.; Nishikawa, Y.; Dandapani, K. Cryptocurrency, a successful application of blockchain technology. Manag. Financ. 2020, 46, 715–733. [Google Scholar] [CrossRef]

- Mhlanga, D. Financial Inclusion in Emerging Economies: The Application of Machine Learning and Artificial Intelligence in Credit Risk Assessment. Int. J. Financial Stud. 2021, 9, 39. [Google Scholar] [CrossRef]

- Bussmann, N.; Giudici, P.; Marinelli, D.; Papenbrock, J. Explainable Machine Learning in Credit Risk Management. Comput. Econ. 2021, 57, 203–216. [Google Scholar] [CrossRef]

- Ji, Y.; Ma, Y. The robust maximum expert consensus model with risk aversion. Inf. Fusion 2023, 99, 101866. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Approaches | Proposed Solutions | Features/Characteristics | Limitations |

|---|---|---|---|

| Tingfei et al. [7] | The increasingly critical issue of credit card fraud is being analyzed and detected through the application of machine-learning techniques. | It suggests an oversampling strategy based on variational automatic coding (VAE) in conjunction with traditional deep learning methods. | The suggested approach is restricted to a publicly available credit card fraud dataset that includes purchases made by cardholders in Europe. Lacks customization for B2B use and is limited for small-scale financial operations. |

| Rao et al. [8] | Designed for transparency in the credit card system, especially in transaction details. | Focuses on transaction detail transparency for small business management. | Limited to real-time transaction for small- and medium-sized enterprises; does not cover the large financial operations. |

| Patel et al. [9] | Designed to offer a content analysis and bibliometric study of blockchain technology in banking and finance that are often inadequate for assessing unique financial profiles of manufacturers and importers. | Focuses on the effects on financial applications, regulation and cybersecurity, sustainable blockchain, and financial intermediation. | Limited to bibliometric review and content analysis of scholarly works addressing the causes, effects, and applications of blockchain-based technology adoption in various intricately linked sectors, especially focusing on banking and finance; insufficient data points for customized credit evaluation; and does not cover financial growth for manufacturers and importers |

| An et al. [10] | Developed with consideration for the benefits and drawbacks of using AI technology to asset management, lending platforms, and banking. | Explains the fundamentals of artificial intelligence (AI), blockchain, and cryptocurrencies, as well as how they are in to the financial industry. | Limited to central bank digital currency and decentralization and consensus, which are two ideas that are related to the benefits of blockchain applications. |

| Zetzsche et al. [11] | Designed for the FinTech and sustainable development goals in the digital transformation. | Supports the UN Sustainable Development Goals (SDGs), in the FinTech industry; and uses progressive approach to the development of the underlying infrastructure needed to enable the digital financial transformation. | Limited to FinTech and Sustainable Development Goals (SDGs) for the digital financial transformation. |

| Truby et al. [12] | Automation in credit-related transactions. | Designed for automated credit processes for credit transactions to reduce excessive administrative workload and controls on the unprecedented risks to consumers. | Limited to increased administrative overhead and financial stability for consumers. |

| Jaiwant [13] | Designed with AI in banks to improve client support and customers with a tailored experience. | Focuses on AI in banks to improve client support and providing customers with a tailored experience, mainly concentrating on the idea of AI in the banking industry and increased the effectiveness and success of IoT banking operations. | Limited to AI applications for banking sector in general and does not cover the industry at large and manufacturers and importers and credit assessment; and may not address financial needs. |

| Ahmed et al. [14] | AI models adapt to specific financial dynamics. | Improves efficiency of energy management usage and transparency in industry 4.0. | Limited to AI applications for energy and management in financial sector and does not cover manufacturers and importers. |

| Wan et al. [15] | Integrating blockchain enhances security and transparency | Examines network delay that affects the behavior of blockchain forks and protects transaction histories. | Limited to blockchain security for network latency and transactions. |

| Yu et al. [16] | Designed for blockchain-enhanced security access control system | Focuses on the tracking and revocation of malicious users and allows for revocability and traceability. | Limited to data encryption and decryption for enhanced data sharing. |

| Bonyuet [17] | Blockchain’s real-time transaction recording mitigates risks in auditing. | Enhances transparency and credit assessment, optimizing credit decisions. | Limited to blockchain and real-time transactions for auditing; does not cover complexities in implementation. |

| Kalsoom et al. [18] | Examines IoT’s impact on supply chain visibility and manufacturing. | Identifies key IoT technologies for supply chain visibility and their benefits and challenges. | Limited to IoT applications in manufacturing; does not directly address financial operations. |

| Ahmed et al. [19] | Addresses the need for resilience in business operations due to global challenges. | Aligns with the transformative potential of blockchain and AI in financial operations. | Focuses on strategic shifts in business practices; limited coverage of specific financial solutions. |

| Azmat and Evanthia [20] | Blockchain’s role in transforming supply chains beyond financial transactions. | Enhances supply chain resilience and agility; applicable in contractual processes within supply chains. | Primarily focused on supply chain applications; limited discussion on direct financial operations impacts. |

| Azmat et al. [21] | Investigates blockchain’s impact on supply chain finance and contractual processes. | Highlights the potential of blockchain-enabled smart contracts in supply chain design. | Limited to supply chain finance and contractual processes; broader implications for financial operations not fully explored. |

| Chen et al. [22] | Integration of Blockchain and AI for Payment Processing | Efficient payment processing and real-time transaction tracking. | Limited to auto real industry and supply chain finance; does not cover interdisciplinary approach within the manufacturing and importing sectors. |

| Smith [23] | Demonstrates how blockchain’s secure data sharing can enhance the training of AI models for improved credit assessment. | Highlights the potential for smart contracts on blockchain to automate credit-related transactions, reducing administrative overhead. | Limited to the practical exploration of blockchain and AI integration in financial operations and administrative overhead and does not cover manufacturer and importers in Industry 5.0. |

| Our Solution | Designed for manufacturers and importers, addressing complex financial needs. | Designed with the capacity of cutting-edge technologies such as blockchain and AI to substantially elevate financial performance metrics. These encompass credit scores, loan approval rates, default rates, revenue growth, customer satisfaction, etc. | Limited to streamlining financial processes within the manufacturing and importing sectors through the integration of blockchain and AI, resulting in more efficient workflows. |

| Limitations | Concerns of Participants |

|---|---|

| Security concerns | 78% |

| High transaction fees | 78% |

| Limited transaction transparency | 56% |

| Lengthy payment processing | 42% |

| Complex credit assessment | 36% |

| Type of Participants | Adoption Intention (%) |

|---|---|

| Non-willing participants | 10% |

| Strongly willing participants | 42% |

| Undecided participants | 16% |

| Somewhat willing participants | 32% |

| Research Directions/Trends | Key Data |

|---|---|

| Decentralized credit networks | Access to diverse credit options; lower interest rates |

| Multi-Party Computation (MPC) | Enhanced privacy for credit assessments |

| Quantum-Safe Cryptography | Ensuring long-term data security |

| Hyper-Personalized Credit Solutions | Tailored credit options based on behavior |

| Predictive Financial Analytics | Real-time insights into financial trends |

| Regulatory Technology (RegTech) | Automated compliance with financial regulations |

| Cross-Blockchain Integration | Seamless integration for cross-border transactions |

| Central Bank Digital Currencies (CBDCs) | Simplifying cross-border trade and transactions |

| Sustainable Blockchain | Environmentally friendly blockchain solutions |

| Ethical AI | Fair and unbiased credit assessments |

| Category | Challenges |

|---|---|

| Integration with existing system | Legacy systems compatibility Data migration |

| User adoption | Change management Training and education User experience |

| Security and compliance | Regulatory compliance Security risks |

| Scalability | Handling increased volume |

| Cost management | Initial investment |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ali, M.; Razaque, A.; Yoo, J.; Kabievna, U.R.; Moldagulova, A.; Ryskhan, S.; Zhuldyz, K.; Kassymova, A. Designing an Intelligent Scoring System for Crediting Manufacturers and Importers of Goods in Industry 4.0. Logistics 2024, 8, 33. https://doi.org/10.3390/logistics8010033

Ali M, Razaque A, Yoo J, Kabievna UR, Moldagulova A, Ryskhan S, Zhuldyz K, Kassymova A. Designing an Intelligent Scoring System for Crediting Manufacturers and Importers of Goods in Industry 4.0. Logistics. 2024; 8(1):33. https://doi.org/10.3390/logistics8010033

Chicago/Turabian StyleAli, Mohsin, Abdul Razaque, Joon Yoo, Uskenbayeva Raissa Kabievna, Aiman Moldagulova, Satybaldiyeva Ryskhan, Kalpeyeva Zhuldyz, and Aizhan Kassymova. 2024. "Designing an Intelligent Scoring System for Crediting Manufacturers and Importers of Goods in Industry 4.0" Logistics 8, no. 1: 33. https://doi.org/10.3390/logistics8010033

APA StyleAli, M., Razaque, A., Yoo, J., Kabievna, U. R., Moldagulova, A., Ryskhan, S., Zhuldyz, K., & Kassymova, A. (2024). Designing an Intelligent Scoring System for Crediting Manufacturers and Importers of Goods in Industry 4.0. Logistics, 8(1), 33. https://doi.org/10.3390/logistics8010033