The Dynamics of Profitability among Salmon Farmers—A Highly Volatile and Highly Profitable Sector

Abstract

:1. Introduction

2. Theory

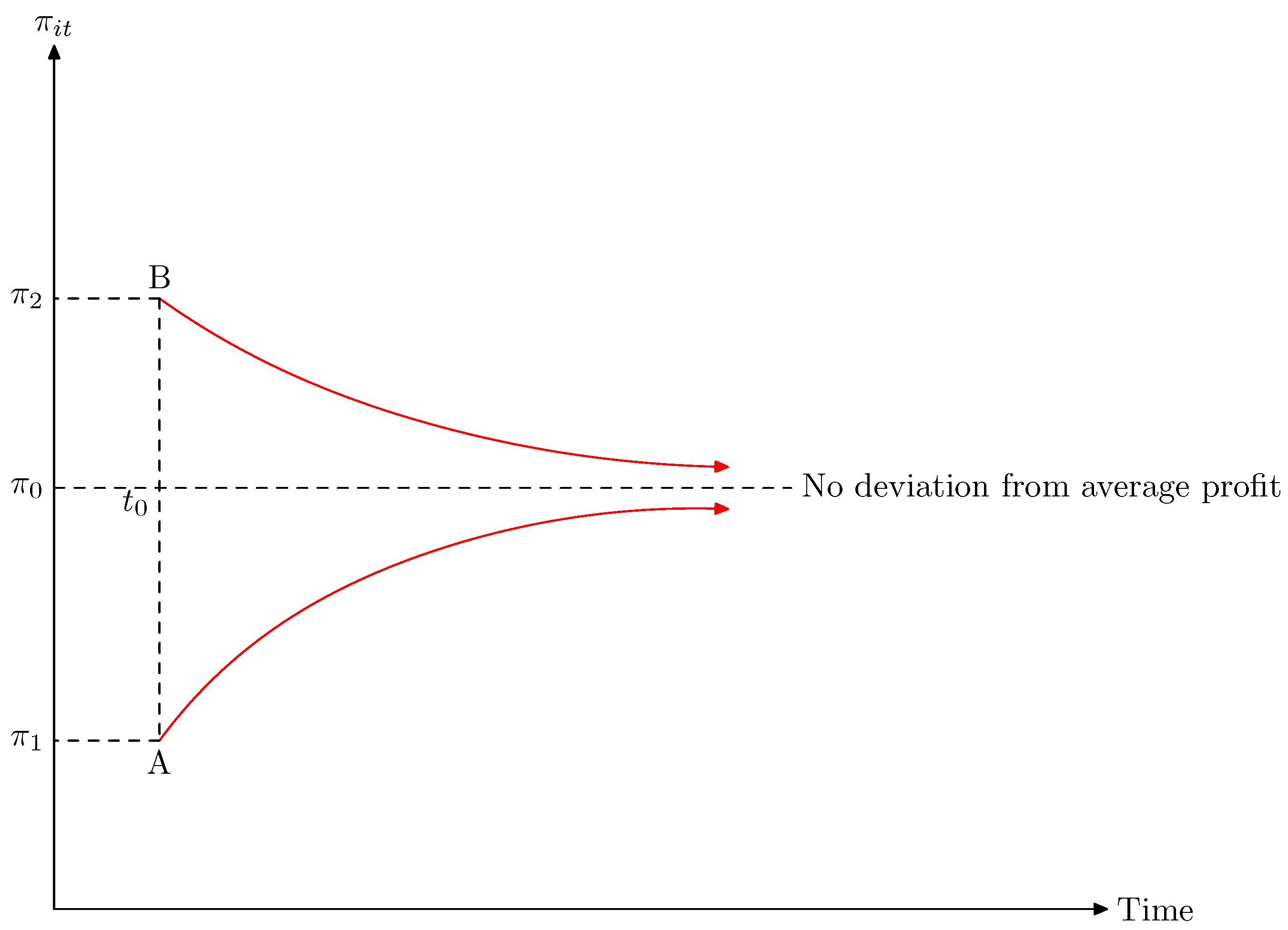

2.1. The Persistence of Profit (PoP)

2.2. Law of Proportionate Effect (LPE)

3. Research Questions

- Research Question:

- Research question 1 is described in Equation (2) and asks: What is the degree of profit persistence for the Norwegian salmon farming industry?

- Research Questions:

- (2a) Does Gibrat’s Law hold for the Norwegian salmon-farming industry? (Equation (5)).

- (2b) Will failure or success be maintained the next period? (Equation (5)).

- Research Questions:

- (3a) Is there a correlation between profitability and firm-specific factors?

- (3b) Does including business-specific characteristics of the sector have an impact on the level of profit persistency?

4. Methodology and Data

4.1. The Sample

4.2. The Models

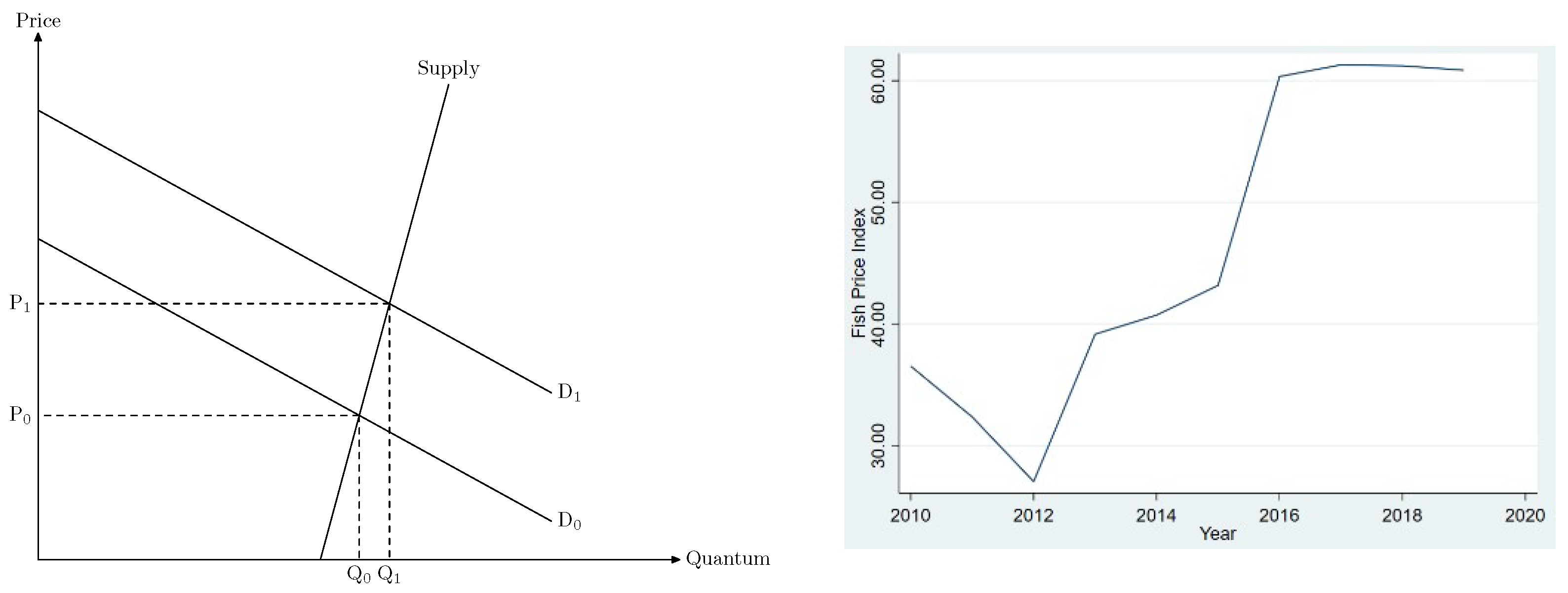

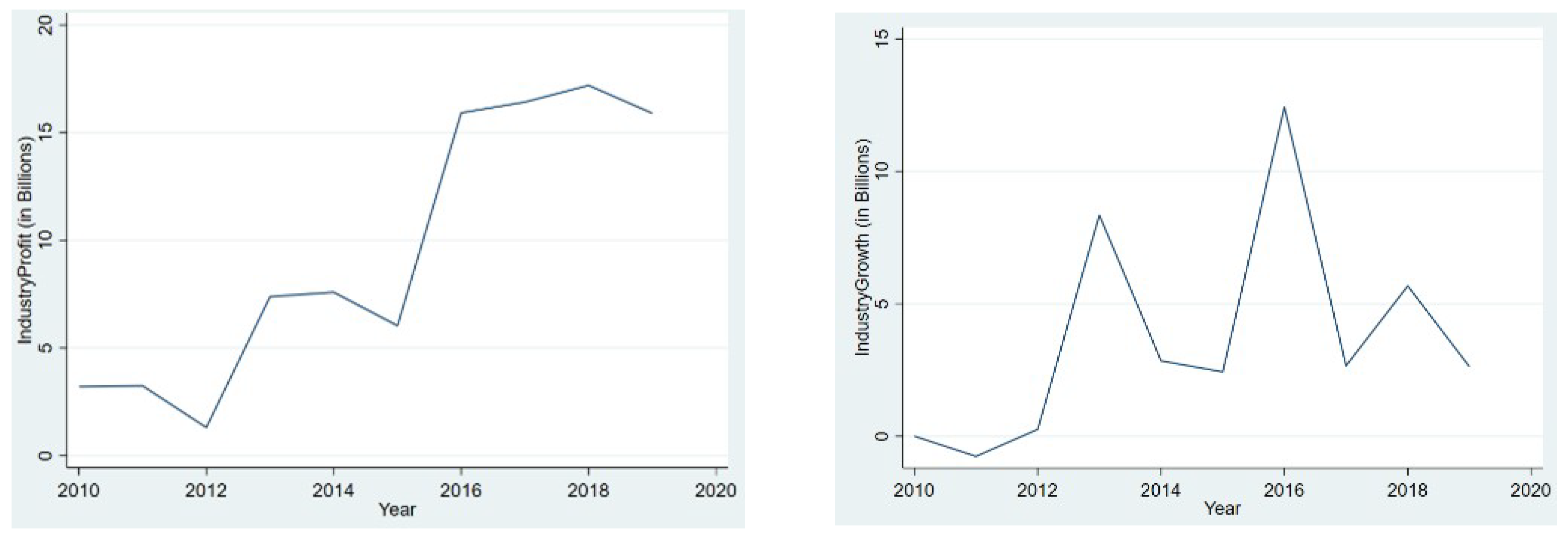

- The volatility in production due to illnesses in the salmon stock.

- The volatility in demand due to exchange-rate fluctuations.

- How the high profitability of the industry is distributed in face of the firms’ challenges with instability.

5. Findings and Discussion

5.1. Research Question 1 (PoP)

5.2. Research Question 2 (LPE)

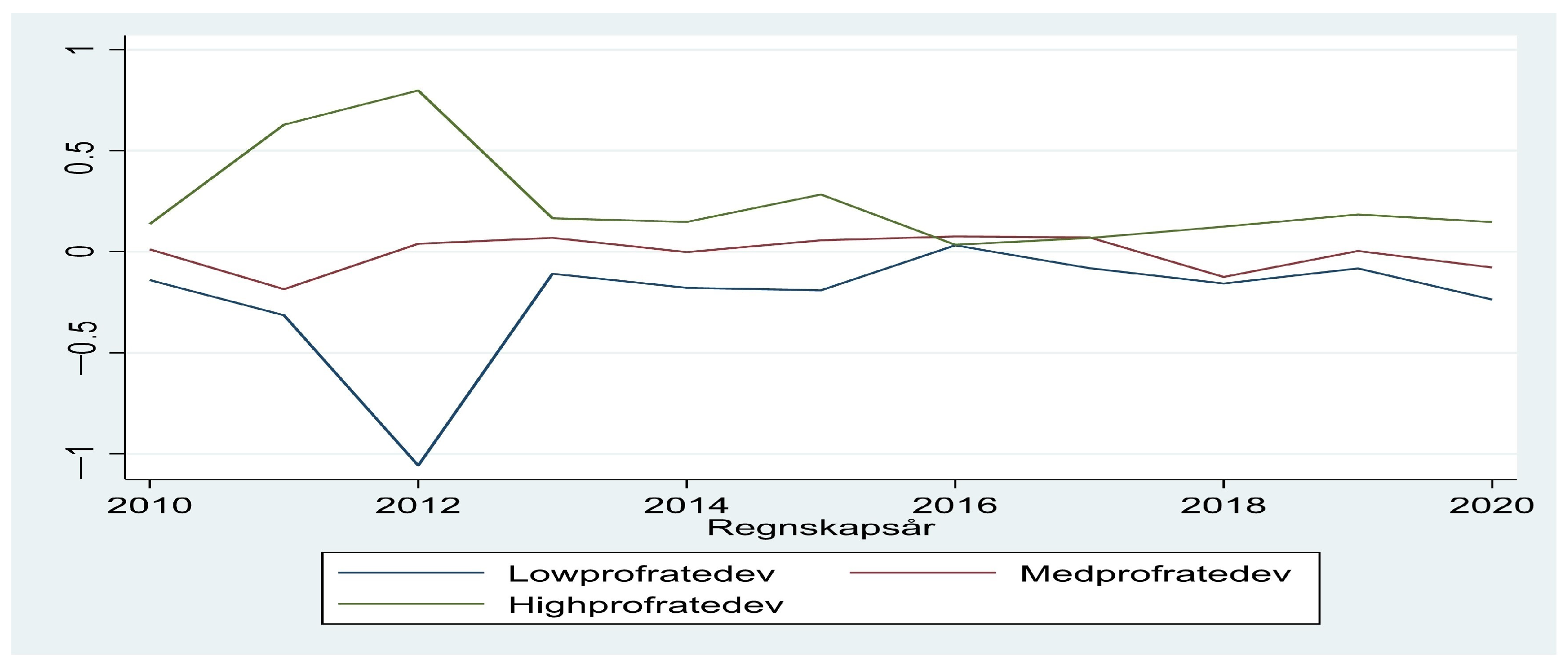

5.3. Research Question 3: Firm-Specific Factors and Profitability

6. Conclusions, Further Research, and Limitation

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Hersoug, B. Why and how to regulate Norwegian salmon production?—The history of Maximum Allowable Biomass (MAB). Aquaculture 2021, 545, 737144. [Google Scholar] [CrossRef]

- Iversen, A.; Asche, F.; Hermansen, Ø; Nystøyl, R. Production cost and competitiveness in major salmon farming countries 2003–2018. Aquaculture 2020, 522, 735089. [Google Scholar] [CrossRef]

- Available online: https://fishpool.eu/fish-pool-european-buyers-index/ (accessed on 11 March 2022).

- Dennis, S.N.; Taranin, V. The Complexity of Reaching Further Production Growth in the Norwegian Salmon Farming Industry: A Two-Pronged APPROACH to qualitatively Evaluating Technological Development. Master’s Thesis, Norwegian School of Economics, Bergen, Norway, 2020. [Google Scholar]

- Misund, B.; Nygård, R. Big fish: Valuation of the world’s largest salmon farming companies. Mar. Resour. Econ. 2018, 33, 245–261. [Google Scholar] [CrossRef] [Green Version]

- Asche, F.; Sikveland, M.; Zhang, D. Profitability in Norwegian salmon farming: The impact of firm size and price variability. Aquac. Econ. Manag. 2018, 22, 306–317. [Google Scholar] [CrossRef]

- Asche, F.; Oglend, A. The relationship between input-factor and output prices in commodity industries: The case of Norwegian salmon aquaculture. J. Commod. Mark. 2016, 1, 35–47. [Google Scholar] [CrossRef]

- Asche, F.; Oglend, A.; Tveteras, S. Regime shifts in the fish meal/soybean meal price ratio. J. Agric. Econ. 2013, 64, 97–111. [Google Scholar] [CrossRef]

- Grefsrud, E.S.; Svås, T.; Glover, K.; Husa, V.; Hansen, P.K.; Samuelsen, O.B.; Stien, L.H. Risikorapport Norsk Fiskeoppdrett 2019-Miljøeffekter av Lakseoppdrett. Fisken og havet. 2019. Available online: https://imr.brage.unit.no/imr-xmlui/handle/11250/2640589 (accessed on 11 March 2022). (In Norwegian).

- Jensen, B.B.; Brun, E.; Fineid, B.; Larssen, R.B.; Kristoffersen, A.B. Risk factors for cardiomyopathy syndrome (CMS) in Norwegian salmon farming. Dis. Aquat. Org. 2013, 107, 141–150. [Google Scholar] [CrossRef]

- Pincinato, R.B.; Asche, F.; Bleie, H.; Skrudl, A.; Stormoen, M. Factors influencing production loss in salmonid farming. Aquaculture 2021, 532, 736034. [Google Scholar] [CrossRef]

- Taranger, G.L.; Karlsen, Ø; Bannister, R.J.; Glover, K.A.; Husa, V.; Karlsbakk, E.; Svås, T. Risk assessment of the environmental impact of Norwegian Atlantic salmon farming. ICES J. Mar. Sci. 2015, 72, 997–1021. [Google Scholar] [CrossRef] [Green Version]

- Abolofia, J.; Asche, F.; Wilen, J.E. The cost of lice: Quantifying the impacts of parasitic sea lice on farmed salmon. Mar. Resour. Econ. 2017, 32, 329–349. [Google Scholar] [CrossRef]

- Overton, K.; Dempster, T.; Oppedal, F.; Kristiansen, T.S.; Gismervik, K.; Stien, L.H. Salmon lice treatments and salmon mortality in Norwegian aquaculture: A review. Rev. Aquac. 2019, 11, 1398–1417. [Google Scholar] [CrossRef] [Green Version]

- Dahl, R.E.; Yahya, M. Price volatility dynamics in aquaculture fish markets. Aquac. Econ. Manag. 2019, 23, 321–340. [Google Scholar] [CrossRef]

- Asche, F.; Misund, B.; Oglend, A. The case and cause of salmon price volatility. Mar. Resour. Econ. 2019, 34, 23–38. [Google Scholar] [CrossRef]

- Baldursson, I.A. Price Hedging in Salmon Farming: Is Price Hedging a Viable, Profit Inducing Option for Salmon Farming Companies? Ph.D. Dissertation, Bifröst University, Bifröst, Iceland, 2021. [Google Scholar]

- Luthman, O.; Jonell, M.; Troell, M. Governing the salmon farming industry: Comparison between national regulations and the ASC salmon standard. Mar. Policy 2019, 106, 103534. [Google Scholar] [CrossRef]

- Olaussen, J.O. Environmental problems and regulation in the aquaculture industry. Insights from Norway. Mar. Policy 2018, 98, 158–163. [Google Scholar] [CrossRef] [Green Version]

- Asche, F.; Sikvel, M. The behavior of operating earnings in the Norwegian salmon farming industry. Aquac. Econ. Manag. 2015, 19, 301–315. [Google Scholar] [CrossRef]

- Mueller, D.C. Profits in the Long Run; Cambridge University Press: Cambridge, UK, 1986. [Google Scholar]

- Gibrat, R. Les Inégalits Économiques; Sirey: Paris, France, 1931. [Google Scholar]

- Xie, J.; Kinnucan, H.W.; Myrl, Ø. Demand elasticities for farmed salmon in world trade. Eur. Rev. Agric. Econ. 2009, 36, 425–445. [Google Scholar] [CrossRef]

- Norges Offentlige Utredninger 2019: 18. Oslo 2019. Available online: https://www.regjeringen.no/contentassets/207ae51e0f6a44b6b65a2cec192105ed/no/pdfs/nou201920190018000dddpdfs.pdf (accessed on 6 April 2022).

- Gschwandtner, A. Evolution of profit persistence in the USA: Evidence from three periods. Manch. Sch. 2012, 80, 172–209. [Google Scholar] [CrossRef]

- Hirsch, S. Successful in the long run: A meta-regression analysis of persistent firm profits. J. Econ. Surv. 2018, 32, 23–49. [Google Scholar] [CrossRef]

- Bhangu, P.K. Persistence of profitability in top firms: Does it vary across sectors? Compet. Rev. 2020, 30, 269–287. [Google Scholar] [CrossRef]

- McKinsey Global Institute. The New Global Competition for Corporate Profits. 2015. Available online: https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/the-new-global-competition-for-corporate-profits (accessed on 11 March 2022).

- Giotopoulos, I. Dynamics of firm profitability and growth: Do knowledge-intensive (business) services persistently outperform? Int. J. Econ. Bus. 2014, 21, 291–319. [Google Scholar] [CrossRef]

- Gschwandtner, A.; Hirsch, S. What drives firm profitability? A comparison of the US and EU food processing industry. Manch. Sch. 2018, 86, 390–416. [Google Scholar] [CrossRef] [Green Version]

- Opstad, L.; Idsø, J.; Valenta, R. The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway. Economies 2022, 10, 53. [Google Scholar] [CrossRef]

- Tschoegl, A.E. Size, growth, and transnationality among the world’s largest banks. J. Bus. 1983, 56, 187–201. [Google Scholar] [CrossRef]

- Valenta, R.; Idsø, J.; Opstad, L. Evidence of a threshold size for Norwegian campsites and its dynamic growth process implications—Does Gibrat’s law hold? Economies 2021, 9, 175. [Google Scholar] [CrossRef]

- Eriotis, N.P.; Frangouli, Z.; Ventoura-Neokosmides, Z. Profit margin and capital structure: An empirical relationship. J. Appl. Bus. Res. (JABR) 2002, 18. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, H.T.; Nguyen, A.H. The impact of capital structure on firm performance: Evidence from Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 97–105. [Google Scholar] [CrossRef]

- Yadav, I.S.; Pahi, D.; Gangakhedkar, R. The nexus between firm size, growth and profitability: New panel data evidence from Asia–Pacific markets. Eur. J. Manag. Bus. Econ. 2021, 31, 115–140. [Google Scholar] [CrossRef]

- Musah, A.; Gakpetor, E.D.; Pomaa, P. Financial management practices, firm growth and profitability of small and medium scale enterprises (SMEs). Inf. Manag. Bus. Rev. 2018, 10, 25–37. [Google Scholar] [CrossRef] [Green Version]

- Opstad, L.; Idsø, J.; Valenta, R. The degree of profit persistence in tourism industry. The case of Norwegian campsites. Int. J. Econ. Bus. Adm. 2021, 9, 140–155. [Google Scholar] [CrossRef]

- Zouaghi, F.; Hirsch, S.; Garcia, M.S. What drives firm profitability? A multilevel approach to the Spanish agri-food sector. In Proceedings of the 56th Annual Conference, Bonn, Germany, 28–30 September 2016. No. 873-2016-60917. [Google Scholar]

- Blundell, R.; Bond, S. Initial conditions and moment restrictions in dynamic panel data models. J. Econom. 1998, 87, 115–143. [Google Scholar] [CrossRef] [Green Version]

- Hirsch, S.; Gschwandtner, A. Profit persistence in the food industry: Evidence from five European countries. Eur. Rev. Agric. Econ. 2013, 40, 741–759. [Google Scholar] [CrossRef] [Green Version]

- Gschwandtner, A. Profit persistence in the ‘very’ long run: Evidence from survivors and exiters. Appl. Econ. 2005, 37, 793–806. [Google Scholar] [CrossRef]

- Harris, D.J. On the classical theory of competition. Camb. J. Econ. 1988, 12, 139–167. [Google Scholar] [CrossRef]

- Bahçe, S.; Eres, B. Components of differential profitability in a classical/Marxian theory of competition: A case study of Turkish manufacturing. In Alternative Theories of Competition; Routledge: London, UK, 2012; pp. 251–288. [Google Scholar]

- Rumelt, R.P. Towards a strategic theory of the firm. Compet. Strateg. Manag. 1984, 26, 556–570. [Google Scholar]

- Afrifa, G.A.; Padachi, K. Working capital level influence on SME profitability. J. Small Bus. Enterp. Dev. 2016, 23, 44–63. [Google Scholar] [CrossRef]

- Marris, R.; Maclean, I.; Bernau, S. The Economics of Capital Utilization; Macmillan: London, UK, 1964. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | St. Dev. | Min | Max |

|---|---|---|---|---|

| Sales | 478,262.2 | 730,184.3 | 38,959.7 | 4,64,029.0 |

| Profit rate (%) | 24.53 | 7.7 | 8.06 | 54.55 |

| Market share (%) | 1.31 | 1.95 | 0.097 | 11.51 |

| Growth (%) | 17.30 | 10.56 | −19.37 | 61.58 |

| Debt rate (%) | 75.20 | 33.50 | 30.65 | 228.94 |

| Working capita1 (1) | 50.09 | 26.57 | 6.35 | 175.16 |

| Salary expenses (%) | 6.48 | 3.33 | 3.37 | 19.81 |

| Initial | Initial | Initial | ||

|---|---|---|---|---|

| Variables | All (1) | Low | Medium | High |

| (Group 1) | (Group 2) | (Group 3) | ||

| 0.074 ** | 0.002 | 0.035 | 0.092 * | |

| (0.030) | (0.049) | (0.058) | (0.051) | |

| Constant () | −0.240 *** | −0.206 *** | ||

| (0.017) | (0.031) | (0.029) | (0.036) | |

| Observations | 712 | 248 | 202 | 234 |

| Firms | 84 | 29 | 24 | 29 |

| Initial | Initial | Initial | ||

|---|---|---|---|---|

| All (1) | Low | Medium | High | |

| 0.227 |

| Initial | Initial | Initial | ||

|---|---|---|---|---|

| Variables | All (1) | Low | Medium | High |

| (Group 1) | (Group 2) | (Group 3) | ||

| 0.948 | 0.998 | 0.942 | 1.033 | |

| (0.038) | (0.056) | (0.052) | (0.051) | |

| MA | −0.567 *** | −0.590 *** | −0.523 *** | *** |

| (0.045) | (0.067) | (0.077) | (0.071) | |

| Constant | 0.762 *** | 0.159 *** | 0.859 *** | −0.289 *** |

| (0.478) | (0.700) | (0.641) | (0.625) | |

| Observations | 615 | 218 | 175 | 199 |

| Firms | 87 | 29 | 24 | 29 |

| Initial | Initial | Initial | ||

|---|---|---|---|---|

| Variables | All (1) | Low | Medium | High |

| (Group 1) | (Group 2) | (Group 3) | ||

| 0.112 *** | 0.203 *** | 0.031 | 0.095 * | |

| Market share | 0.301 | 5.711 | ||

| (4.28) | (8.362) | (4.883) | (5.223) | |

| Growthrate | 0.159 *** | 0.484 *** | 0.060 | |

| (0.053) | (0.088) | (0.090) | (0.095) | |

| Debtrate | ** | ** | ||

| (0.068) | (0.089) | (0.146) | (0.135) | |

| Working Capital | 0.171 | |||

| (0.088) | (0.139) | (0.137) | (0.129) | |

| Constant | 0.112 | 0.300 ** | ||

| (0.081) | (0.147) | (0.143) | (0.145) | |

| Observations | 615 | 218 | 175 | 199 |

| Firms | 87 | 29 | 24 | 29 |

| Initial | Initial | Initial | ||

|---|---|---|---|---|

| Variables | All (1) | Low | Medium | High |

| (Group 1) | (Group 2) | (Group 3) | ||

| 0.089 *** | 0.170 *** | 0.083 | ||

| (0.031) | (0.057) | (0.059) | (0.054) | |

| Market share | 1.251 | 2.138 | ||

| (3.969) | (8.072) | (4.899) | (5.284) | |

| Growth rate | 0.090 | 0.320 *** | 0.054 | |

| (0.055) | (0.096) | (0.093) | (0.095) | |

| Debt rate | 0.002 | 0.041 | 0.203 | |

| (0.076) | (0.105) | (0.148) | (0.137) | |

| Working capital | 0.111 | 0.380 | ||

| (0.097) | (0.144) | (0.134) | (0.169) | |

| Salary rate | *** | *** | *** | |

| (1.399) | (2.101) | (2.676) | (2.282) | |

| Constant | 0.292 *** | 0.231 | 0.324 * | 0.328 ** |

| (0.089) | (0.155) | (0.193) | (0.154) | |

| Observations | 615 | 218 | 175 | 199 |

| Firms | 87 | 29 | 24 | 29 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Opstad, L.; Idsø, J.; Valenta, R. The Dynamics of Profitability among Salmon Farmers—A Highly Volatile and Highly Profitable Sector. Fishes 2022, 7, 101. https://doi.org/10.3390/fishes7030101

Opstad L, Idsø J, Valenta R. The Dynamics of Profitability among Salmon Farmers—A Highly Volatile and Highly Profitable Sector. Fishes. 2022; 7(3):101. https://doi.org/10.3390/fishes7030101

Chicago/Turabian StyleOpstad, Leiv, Johannes Idsø, and Robin Valenta. 2022. "The Dynamics of Profitability among Salmon Farmers—A Highly Volatile and Highly Profitable Sector" Fishes 7, no. 3: 101. https://doi.org/10.3390/fishes7030101

APA StyleOpstad, L., Idsø, J., & Valenta, R. (2022). The Dynamics of Profitability among Salmon Farmers—A Highly Volatile and Highly Profitable Sector. Fishes, 7(3), 101. https://doi.org/10.3390/fishes7030101