Abstract

Auditing stands to be a strong enforcement mechanism in bringing tax compliance, safeguards public revenue and is strongly influenced by communication between auditors and audited taxpayers. This present work studied the opinions of auditors of the auditing body of the Public Revenue Research and Assurance Services (Y.E.D.D.E.) in order to investigate the communication between them and the taxpayers in the context of the preventive audit. Primary research was conducted. Findings from previous research were utilized and a questionnaire was used to collect primary data. The survey was conducted all over Greece by randomly sampling 120 auditors. This study provides useful insights for policymakers and implies that investigating the causes of taxpayers’ aggressiveness, providing lifelong education to auditors, enhancing collaboration between auditors and the fairness and efficiency of the tax system would have a beneficial effect on the communication between tax auditors and taxpayers and thus on tax compliance.

1. Introduction

Tax evasion is an issue of the utmost importance as it is linked to the economic development of a country, the possibility of implementing investments and even competition. The treatment and fight against it are performed through audit services, the operation and existence of which constitute an important parameter for ensuring fiscal stability [1]. Through audit services and the implementation of tax audits, it is possible to achieve the regulation of the tax system, the harmonization of taxpayers with the current legislative framework, the cultivation of tax awareness, the detection of violations and the institutionalization of a framework of rules and standards in which citizens are invited to adapt [2].

The extent to which the tax audits of audit agencies and their staff are effective is a related issue. This is true because carrying out a tax audit is not a simple process and can be determined and influenced by various factors. The purpose of this article is to investigate the preventive tax audit and to study its individual dimensions from the auditors’ aspect. More specifically, the opinions of the auditors of the Public Revenue Investigation and Assurance Service (Y.E.D.D.E.) in Greece concerning the communication between auditors and taxpayers, the execution of the audit work and the factors that affect the effectiveness of the audit work are examined.

The surveys that have been carried out in recent years in Greece in which the opinions of auditors are investigated are limited [3,4]. There are dimensions of the issue that have not received widespread attention, resulting in research gaps. Moreover, tax evasion is an important problem that remains unsolved despite the interventions made at the state level, and the need to investigate parameters related to it is essential. Understanding the relationship between taxpayers and auditors can contribute to a better treatment of tax evasion and the shadow economy in general [5,6].

The rest of this paper proceeds as follows. Section 2 consists of the theoretical framework. Section 3 describes the data and the research methodology. Section 4 presents the results. Section 5 develops the discussion of the results. Section 6 concludes. Finally, Section 7 refers to the limitations and suggestions for future research.

2. Literature Review

2.1. The Framework of the Tax Audit

2.1.1. Tax Audit and Compliance

Individuals and firms are taxed in various ways. Corporations constitute the greatest extent of the core of the economy and their action is rewarding as it contributes to the development of the country at an economic level. It is important that any society that wants to be called healthy and efficient is governed by efficient tax systems. Efficiency is a concept for the assurance in which a tax audit plays a decisive role [7].

A tax audit is a process in which public audit services examine whether a taxpayer correctly declares their income and, in general, their assets. Tax audits emphasize the accuracy of declarations and aim to investigate whether the income or assets are honestly declared by a taxpayer [2].

Tax compliance is a concept inextricably linked to tax audits. Tax compliance refers to the adaptation of taxpayers to the current tax system and to the way in which taxpayers manage their income and assets. The extent to which tax compliance is ensured is very important, as hundreds of tax violations and cases of tax evasion are recorded every day, indicating that the Greek tax system works inefficiently. A country’s tax system is characterized as efficient and citizens’ tax compliance is achieved when there is no need for tax audits, when taxpayers’ assets are correctly declared and when their tax obligations are covered in time [8]. Finally, the framework of the concepts of tax compliance and tax audit is overshadowed by principles such as the effective cooperation between taxpayers and the State.

2.1.2. The Preventive Tax Audit

There are three types of tax audits, which are [3]:

- Preventive tax audit;

- Regular tax audit;

- Temporary tax audit.

The role of a preventive audit is special because it has a preventive nature and contributes to the prevention of tax evasion and the strengthening of tax compliance. This audit emphasizes the Greek Accounting Standards (HAS) and the extent to which they are correctly applied. It is short in duration and can be performed at any time during a fiscal year. Its application can be done within the facilities of an organization and outside its internal environment, if deemed necessary, to detect tax evasion.

2.1.3. Purpose of Preventive Audit

A preventive audit aims to [9,10,11,12]:

- Verify the correct application of tax provisions;

- Verify the fulfillment of the tax obligations of the taxpayers, as they derive from the relevant tax provisions;

- Verify compliance with the prescribed accounting records (books) and issuance of the appropriate tax data when business transactions are carried out;

- Investigate the validity of complaints and, in general, information with which delinquent behavior of taxpayers is reported;

- Fight against tax evasion through the imputation of the prescribed violations upon detection of taxpayers’ delinquent behavior;

- Strengthen taxpayer compliance through the presence of the Tax Administration’s audit bodies at various points of business activity (e.g., public markets), particularly during festive periods and periods of intense trading activity.

2.2. Preventive Tax Audit and Communication

When carrying out tax audits, whether they are preventive or in another form, it is necessary to meet various conditions [13]. One of them concerns the existence of a good and acceptable communication framework between the auditors and the taxpayers, as auditees. Communication is a dimension of effective work execution, which is not limited to the moment of the audit but precedes it as it relates to the working conditions, the prevailing situation in which the auditors are employed, the climate of communication and cooperation between employees, etc. The execution of a project, let alone its effectiveness, is based on the concept of a team, on group action and on the ability of different people, with different points of view, perceptions and life attitudes, to communicate effectively, cooperate and be guided by common goals and shared visions. It is argued that the achievement of the goals of an organization or a group is the result of effective and healthy interaction between its members [14].

Examining the dimension of communication internally, it is necessary to refer to the fact that members of public service, such as the members of the Y.E.D.D.E., have the elements of a good listener [15]. It is a necessary condition that the members understand the objectives of the service, understand its vision, take care of the development and maintenance of healthy interpersonal relationships, show respect and appreciation to their colleagues and that there is mutual support between the members. It is considered appropriate to underline that the characteristics of effective communication mentioned above do not only concern the relationship between members but are also found throughout the hierarchy (e.g., the relationship between executives and supervisors, the relationship between executives and managers, etc.).

By the aspect of taxpayers, the concept of communication concerns them equally to a significant extent. During the interaction of a civil servant with a citizen, a form of communication develops, the quality of which is also determined by the attitude of the citizen. Their attitude can be positive or negative, and this can be determined by the perceptions of the citizen, their culture, their mentality, the way they have learned to think, the perceived image of the public sector, the behavior of the employee (for example if they are arrogant, bossy or friendly), the way the official is able to convey effective messages and the skills they to direct the citizen [16]. Both the personality of the citizen and the personality of the official are equally important to the communication between them, and the possibility that the communication is not good is possible at any time as the result has not so much to do with personal issues as with the situation of the issue [14].

3. Research Methodology

3.1. Purpose and Research Questions

The purpose of this paper.

In this present paper, the interest is focused on the communication of the auditors of Y.E.D.D.E. with the taxpayers in the context of the preventive audit. The main pillar around which the research is developed concerns not only the concept of a preventive audit, but also the dimensions, such as the communication between the auditors and the audited, the effectiveness of the execution of the audit work, the conditions under which the preventive audit is carried out and the factors that contribute to its effectiveness. This research examines the above issues from the point of view of the auditors of Y.E.D.D.E. Based on the above, the research questions are as follows:

- What is the opinion of the auditors of Y.E.D.D.E. about the communication framework that exists between them and the taxpayers during the performance of preventive audits?

- What is the opinion of the auditors of Y.E.D.D.E. about the effectiveness of performing preventive audits and the factors that make it difficult?

- What is the opinion of the auditors of Y.E.D.D.E. on the ways in which the effectiveness of preventive audits can be improved?

3.2. Research Method

Given the needs of this research, quantitative research was chosen and the questionnaire method was used. The use of the quantitative method allows for information to be searched, collected and processed quickly. Furthermore, in quantitative research, the respondents do not have the obligation to devote much time away from their availability, resulting in the fact that the recording of their opinions is performed immediately and without fatigue. Finally, quantitative research enables a researcher to quickly process data so that conclusions can be drawn about the wider population to which a sample belongs [17,18]. More specifically, a questionnaire was constructed that was then digitized and sent to the respondents. The questionnaire was distributed via e-mail and via the Facebook social network.

3.3. Description of Respondents

The research sample consisted of 120 out of 233 auditors of Y.E.D.D.E. who come from different geographical parts of the country. More specifically, the sample is made up of Y.E.D.D.E. from the cities of Thessaloniki, Athens, Patras and Heraklion. Every respondent who participated in the survey had the same chances to participate in it and no restrictions were placed on factors such as gender, age, education, experience, etc.

Data analysis was performed with SPSS Statistics 29.

Given the needs of the research, eight new variables based on the existing literature and previous studies [3,4] were created, and the results are listed below in Table 1:

Table 1.

Reliability index results.

For each set of propositions corresponding to the eight above, new variables were tested for reliability with the help of Cronbach’s α index. The indicators are very satisfactory and show that all propositions are related to each other, characterized by consistency and internal coherence and are able to measure what they were used for. Therefore, the tool used is considered very reliable for data collection.

4. Results

4.1. Demographics

A total of 120 auditors employed in the services of Y.E.D.D.E. participated in the research. The demographic characteristics of the respondents are summarized in Table 2.

Table 2.

Demographics.

4.2. Auditor-Taxpayer Interaction During an Audit

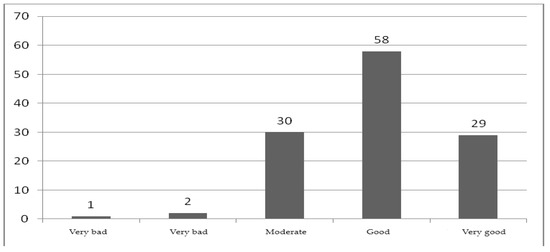

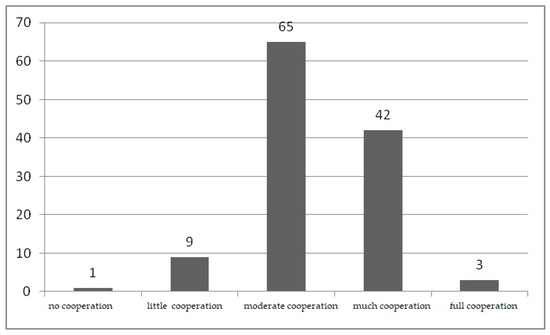

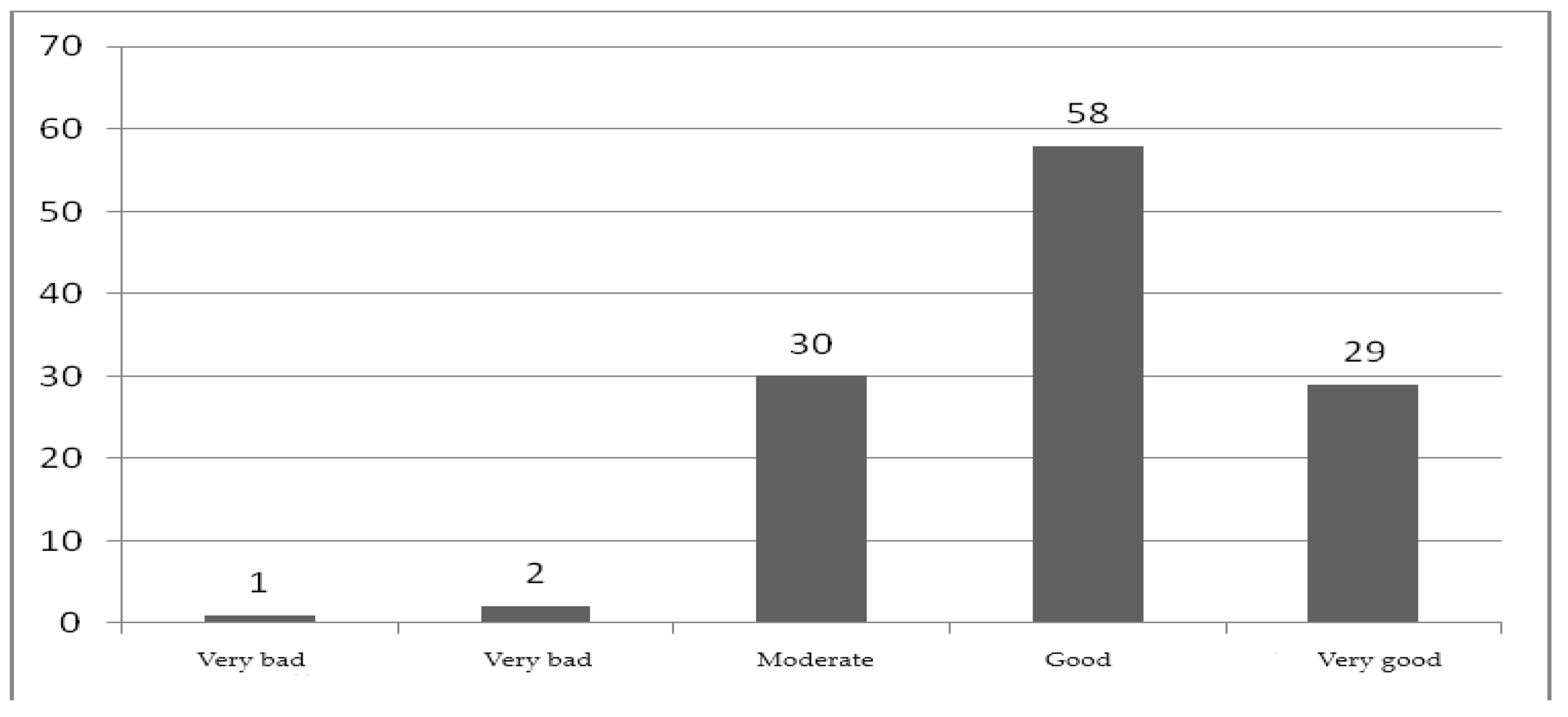

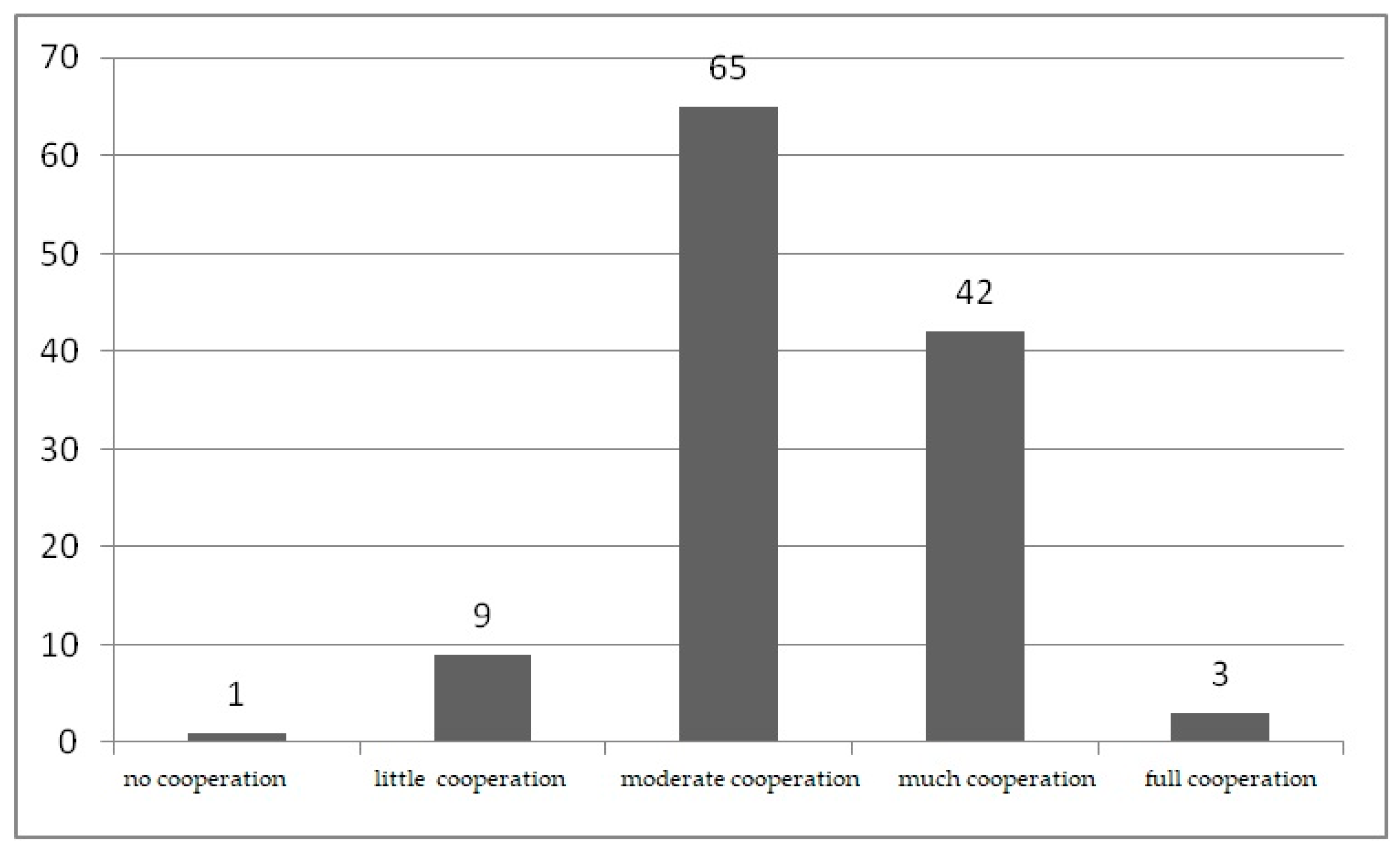

In this part, the following aspects were examined: auditors’ opinions about their communication with taxpayers during an on-site audit, auditors’ opinions about their cooperation with taxpayers when they are subject to an audit and the factors influencing communication and the emotions generated during the audit. The results are listed below in Figure 1 and Figure 2 and Table 3 and Table 4:

Figure 1.

Auditors’ opinions about their communication with taxpayers during an on-site audit.

Figure 2.

Cooperation with taxpayers when they are subject to an audit.

Table 3.

Factors influencing communication.

Table 4.

Emotions generated during the audit.

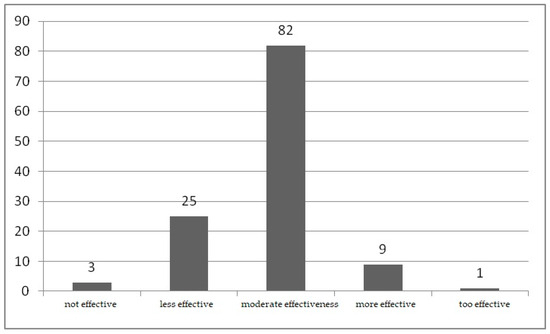

4.3. Effectiveness of Tax Audit Systems

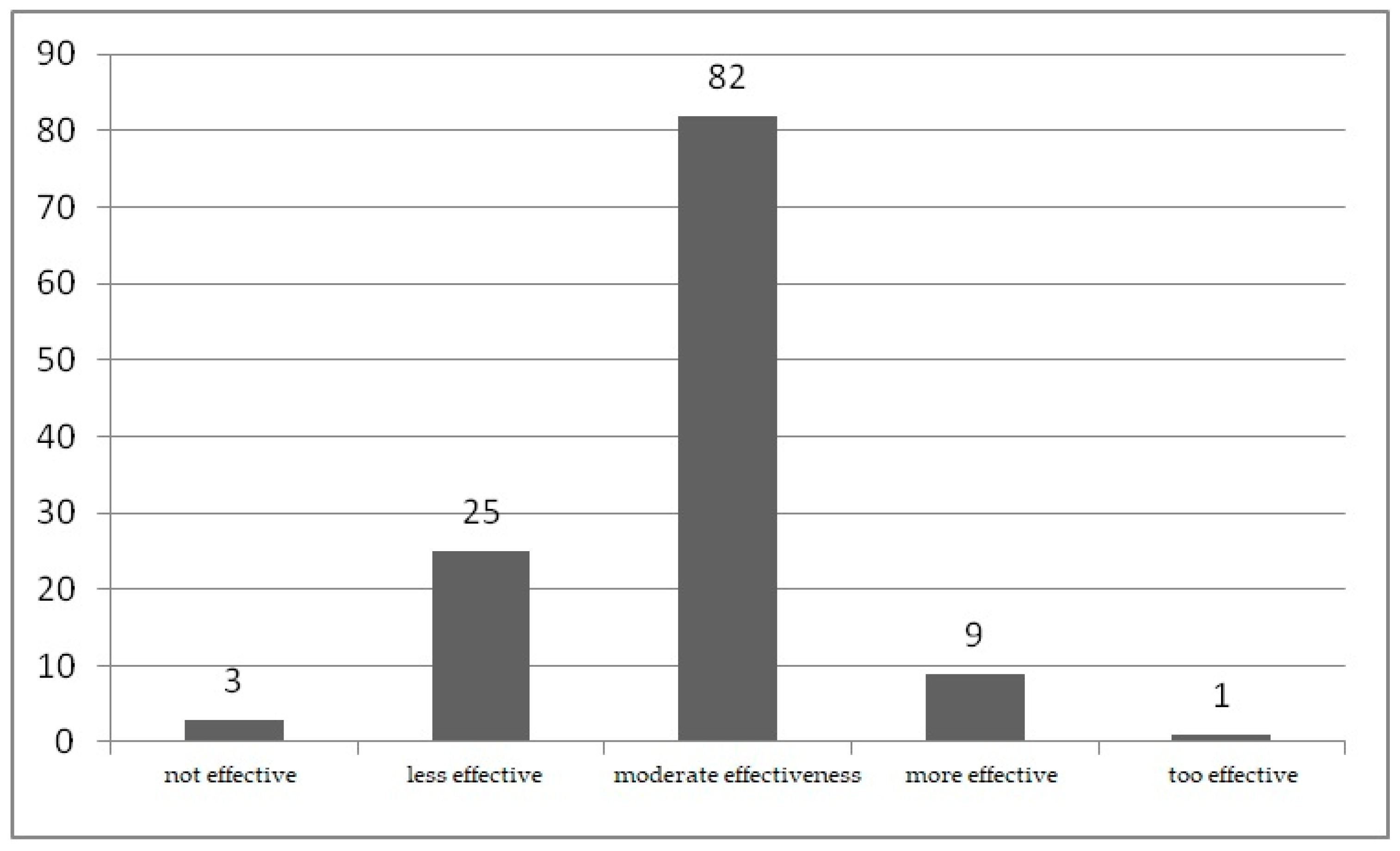

Most respondents responded moderately to the effectiveness of tax audit systems, as can be seen from the results listed in Figure 3.

Figure 3.

Effectiveness of tax audit systems.

The effectiveness of the execution of the audit work can be affected by several factors, as reflected in Table 5.

Table 5.

Factors affecting the execution of the audit work.

4.4. Facilitation of the Audit Process

The work of auditors can be influenced by various factors, and the role played by the attitude and characteristics of the auditees is decisive. With reference to the characteristics, it can be seen from the following data that they can exert a great influence on the control process and facilitate it to a very significant extent, as summarized in Table 6.

Table 6.

Characteristics of audited citizens that may facilitate the audit process.

The work of auditors is inevitably influenced by various factors, and taxpayers play a special role in this. However, there are now factors that can influence the audit work and contribute to improving its effectiveness. For the needs of the research, 10 different factors were examined in terms of their influence, as showcased in Table 7.

Table 7.

Factors that can improve the effectiveness of the auditors’ work.

4.5. CorrelationResults

The eight new variables created were correlated with two quantitative demographic variables, age and work experience. It is observed that empathy is not statistically significantly related to age and work experience (p > 0.05). Age and work experience are not statistically significantly related to the positive emotions experienced during inspections (p > 0.05). Work experience is not statistically significantly related to the negative emotions experienced during inspections (p > 0.05), but there is a statistically significant, negative and weak relationship with age (p < 0.05, r = −0.199).

Furthermore, age and years of service are not related to a statistically significant degree with the influencing factors of the effectiveness of conducting audits (p > 0.05), the influence of audited characteristics on auditors (p > 0.05), audited characteristics that facilitate the process audit (p > 0.05) or the factors to improve the effectiveness of an audit project. These results are presented in Table 8.

Table 8.

Results of Speraman’s rho correlations.

5. Discussion

5.1. Auditor-Taxpayer Communication

The analysis of the results showed that, from the auditors’ perspective, the communication between them and taxpayers is good (M.O. = 3.93) and respondents expressed significantly positive views on this issue. The positive views recorded on this issue are an indication that auditors interact effectively with taxpayers and are able to exchange information with them that is necessary to complete audits. The data showed that the same is not true for the quality of cooperation between auditors and taxpayers when the latter are subject to an audit (M.O. = 3.31). This shows that taxpayers may have a high intention to communicate with the auditors, but when they are asked to cooperate with them, obstacles emerge that undermine the outcome of the audits to some extent. An auditor’s personality is the most important factor that can influence the communication framework between auditors and taxpayers. To the same extent, the climate prevailing between colleagues who carry out the audit together was highlighted, while the leadership skills of the auditor and their knowledge background play an important role. The communication context is not determined so much by whether the auditor is male or female, by the auditor’s appearance or by the number of auditors conducting the audit.

According to the auditors, the effectiveness of a tax audit is also determined by the personality characteristics of the auditors. It should be emphasized that the effectiveness of a tax audit requires that the auditors, when conducting an audit, communicate effectively with each other and that there is a good and positive atmosphere, a good relationship and effective interaction. Furthermore, it seems necessary for an auditor to have leadership skills, motivation, values and self-confidence; and to focus on achieving results; to be characterized by emotional intelligence, discipline, persistence, motivation, decision-making skills, support and coordination skills. It is important to have thinking, communication and management skills and to be governed by characteristics such as consistency, authenticity and reliability. Finally, the effectiveness of a tax audit is also determined by the auditor’s knowledge.

5.2. Execution of Audit Work and Hindrance Factors

The realization and completion of the tax audit process inevitably presupposes the existence of an effective communication framework between the auditors and the taxpayers. In such a process, however, the factors are now influential, some to a lesser extent and others to a greater extent. One of them concerns the tax audit systems and the extent to which they operate effectively. According to the auditors studied, the tax audit systems are moderately effective (M.O. = 2.83); therefore, the existing systems undermine the effectiveness of their work. Tax systems lack efficiency because they are complex and because of the existence of many and difficult-to-understand laws that make the work of auditors difficult [16].

In addition to the systems used, the effectiveness of the execution of the audit work is cumulatively affected by additional factors, of particular importance being the heavy workload, complex legislation and constant changes and understaffing of the audit services. Reference is made to the insufficient training of auditors, the deadlines for the execution of audit work, the low fees, the problematic/insufficient computerization, the lack of equipment and the direct communication between taxpayers through social networking.

All the factors mentioned so far appeared to be highly influential, indicating that the audit agency under study should, cumulatively, emphasize a number of factors in order to become more effective, efficient and functional. Of particular interest is the fact that less influence on the effectiveness of conducting tax audits is caused by the stress experienced by auditors when conducting audits and resistance to audit by taxpayers. By studying the characteristics of taxpayers that influence auditors and the tax audit process, it was found that aggressive behavior by taxpayers can be very influential. There are additional traits such as rudeness and irony that appeared to moderately undermine the audit process and other traits such as arrogance, indecent appearance and distrust that undermined the audit process even less.

5.3. Improving the Effectiveness of Audit Work

In the last section, the opinions of the auditors were recorded regarding the characteristics of the taxpayers that can facilitate the audit process as well as other factors that can improve the effectiveness of the auditors’ work. Regarding the first issue, it was made clear that taxpayers play a crucial role and as part of their role they should provide meaningful and truthful information to the auditors. The effectiveness of the auditing work can be favored to the greatest extent through the continuous training of the auditors and also by the existence of a positive climate between colleagues-supervisors-subordinates. To the same extent as continuous training, the existence of a positive climate was recognized and this shows how important it is in the workplace of auditors to have a healthy climate among all members, regardless of hierarchy, so that auditors are motivated to work efficiently and effectively. Auditors, in order of priority, emphasize the equal and correct allocation of tasks, the targeting of cases with qualitative and quantitative criteria and the online interconnection of tax mechanisms with the digital platform myDATA in providing financial incentives, redesigning systems that correctly capture the flow of audit processes and implement necessary existing regulations and laws. Moreover, the recruitment of new staff to audit services and the integration of IT and communication technologies into the audit process were highlighted.

6. Conclusions

The main conclusions that emerged as far as it concerns the communication framework between auditors and taxpayers during the performance of preventive audits are that auditors’ communication with the taxpayers was assessed as good by the auditors, while taxpayers cooperate moderately with auditors. At the same time, the level of the empathy of auditors is high.

An auditor’s personality is the most basic factor affecting communication between auditors and taxpayers. Furthermore, auditors, while conducting an audit, experience positive and negative emotions to a small degree and outweigh the positive ones. Taxpayers’ aggressiveness during audits affects auditors to a great extent.

Finally, concerning the ways in which the effectiveness of preventive audits can be improved, we found that tax audit systems are moderately effective and that the effective performance of tax audits by auditors is mainly affected by the heavy workload. Moreover, the provision of essential and true information by taxpayers facilitates preventive audits and the efficiency of auditors’ work can be improved by the continuous training of the auditors.

7. Limitations and Suggestions for Future Research

All research is associated with limitations. This present research was limited mostly to the gender, age and working experience of the auditors. Other factors that could have been taken into account are their job description (e.g., if someone is a supervisor or not) or specific personality elements. This research was limited to investigating communication from the auditors’ side only. It would be of particular interest to examine the opinion and attitude of the other party, that is, the taxpayers. In this way, it will be possible to draw useful and more objective conclusions that will improve the quality and effectiveness of audits.

Therefore, an interesting area for future research would be to study the opinion of taxpayers and the way they perceive their communication with auditors. The research could also be extended to other agencies, such as the Labor Inspectorate, which carry out audit work to identify similarities and differences. Finally, it would be useful to carry out similar research in other countries to study the behavior of auditors and auditees and to what extent it resembles the findings of this present research in Greece.

Author Contributions

Conceptualization, A.V. and I.K.; methodology, A.V. and I.K.; software, A.V.; validation, A.V. and I.K.; resources, A.V. and I.K.; writing—original draft preparation, A.V. and I.S.; writing—review and editing, A.V., I.K., I.S., A.K. and T.M.; visualization, A.V and I.S.; supervision, I.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

All data are available upon request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Anastasiou, A.; Kalamara, E.; Kalligosfyris, C. Estimation of the size of tax evasion in Greece. Bull. Appl. Econ. 2020, 7, 97–107. [Google Scholar]

- Drogalas, G.; Sorros, I.; Karagiorgou, D.; Diavastis, I. Tax audit effectiveness in Greek firms: Tax auditors’ perceptions. J. Account. Tax. 2015, 7, 123–130. [Google Scholar]

- Vanas, I. Tax Audit and Its Contribution to Avoiding Tax Evasion: Views of Accountants and Tax Auditors. Master’s Thesis, Hellenic Open University, Patras, Greece, 2020. [Google Scholar]

- Kalamopoulou, M. Tax Audit Procedures: Views of Tax Auditors. Master’s Thesis, University of Macedonia, Thessaloniki, Greece, 2022. (In Greek). [Google Scholar]

- Alm, J.; Jackson, B.R.; McKee, M. Audit Information Dissemination, Taxpayer Communication, and Compliance Behavior, Andrew Young School of Policy Studies Research Paper Series Working Paper. 2006, pp. 6–44. Available online: https://ssrn.com/abstract=897348 (accessed on 5 March 2024).

- Alm, J. Measuring, Explaining, and Controlling Tax Evasion: Lessons from Theory, Experiments, and Field Studies; Working Paper 1213, Tulane Economics Working Paper Series; Springer: Berlin/Heidelberg, Germany, 2012; pp. 1–35. [Google Scholar]

- Ziaga, E.; Kiriakou, Κ. Tax audit procedure for unique entities according to the provisions of the Tax Procedure Code. (Law 4174/2013). Tax Insp. 2016, 794. (In Greek) [Google Scholar]

- See, P.A.; Pelagidis, T. Hypocritical to Suggest Greece Be Ejected from Eurozone. The Financial Times, 28 January 2010. [Google Scholar]

- Law 4308/2014 on Greek Accounting Standards, Related Regulations and Other Provisions. Available online: https://www.taxheaven.gr/law/4308/2014 (accessed on 1 March 2024). (In Greek).

- Law 4174/2013 on Tax Procedures and Other Provisions. Available online: https://www.taxheaven.gr/law/4174/2013 (accessed on 1 March 2024). (In Greek).

- Law 4172/2013 on Income Taxation, Urgent Measures to Implement Law 4046/2012, Law 4093/2012 and Law 4127/2013 and Other Provisions. Available online: https://www.taxheaven.gr/law/4172/2013 (accessed on 1 March 2024). (In Greek).

- Law 2859/2000 on the Sanction of the Value Added Tax Code. Available online: https://www.taxheaven.gr/law/2859/2000 (accessed on 1 March 2024). (In Greek).

- Hofmann, E.; Hoelzl, E.; Kirchler, E. Preconditions of Voluntary Tax Compliance: Knowledge and Evaluation of Taxation, Norms, Fairness and Motivation to Cooperate. J. Psychol. 2008, 216, 209–217. [Google Scholar] [CrossRef] [PubMed]

- Georgakopoulos, T. What Is the Extent of Tax Evasion in Greece? Who Are the Tax Evaders? And What Can Be Done to Combat the Problem? 2016. Available online: https://www.dianeosis.org/2016/06/tax_evasion_in_greece/ (accessed on 1 March 2024).

- Rajiani, I.; Musa, H.; Hardjono, B. Ability, Motivation and Opportunity as Determinants of Green Human Resources Management Innovation. Res. J. Bus. Manag. 2016, 10, 51–57. [Google Scholar] [CrossRef]

- Samanta, I.; Lamprakis, A. Modern leadership types and outcomes: The case of Greek public sector. Manag. J. Contemp. Manag. Issues 2018, 23, 173–191. [Google Scholar] [CrossRef]

- Choy, L. The strengths and weaknesses of research methodology: Comparison and complimentary between qualitative and quantitative approaches. IOSR J. Humanit. Soc. Sci. 2014, 19, 99–104. [Google Scholar] [CrossRef]

- Williams, C. Research methods. J. Bus. Econ. Res. 2007, 5, 65–72. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).