1. Introduction

OECD [

1] examined cross-country financial literacy levels across 30 countries using financial knowledge, financial attitude, and financial behavior as a combined measure of financial literacy. It was found that overall financial literacy levels are low. According to cross-country evidence provided by [

2], the financial literacy rates among adults are at least 65% in countries such as Australia, Canada, Denmark, Finland, Germany, Israel, The Netherlands, Norway, Sweden, and the United Kingdom, whereas they are only 25% or less in South Asia. In contrast, some countries in South Asia have the lowest financial literacy levels, where only a quarter of adults or fewer are financially literate.

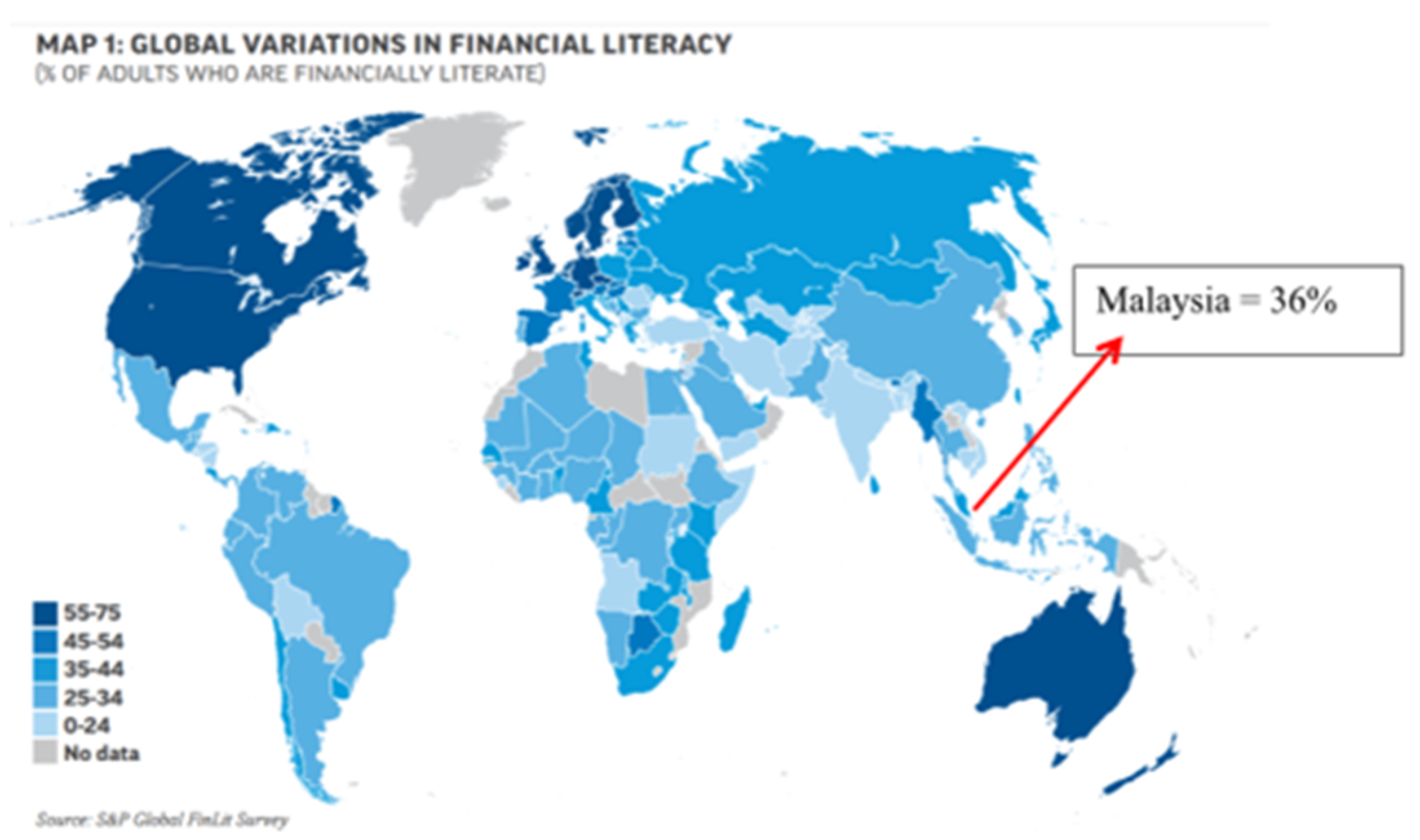

Globally, financial literacy has become one of the major financial management concerns in many countries. The authors in [

2] illustrated the financial literacy breakdown to demonstrate the literacy scores among countries, as shown in

Figure 1. The finding shows that Malaysia has produced an average score of 36% from all countries, indicating that financial illiteracy is prevalent in many countries, including Malaysia.

One of the main concerns among Malaysians is the low financial literacy issue caused by financial illiteracy. In connection with this issue, a survey by Bank Negara Malaysia (BNM) exposed that three out of four Malaysians find it difficult to raise even RM1000 for an emergency. Furthermore, 9 out of every 10 Malaysian households have no emergency funds, besides having significant debts [

3].

According to [

4], young Malaysians possess poor financial knowledge, which causes them to be heavily in debt [

5]. Furthermore, less than a quarter of people have any kind of investment to help them financially. The survey also showed that a majority of Malaysians tend to spend money for instant gratification instead of planning for the long term. This can be seen when only 40% of Malaysians considered themselves as financially ready for retirement, despite the steadily increasing life expectancy of Malaysians. Most people in Malaysia have insufficient information on the importance of having strong finances, including retirement savings, to avoid long-term financial commitment. Therefore, it is important to investigate the level of financial literacy among Malaysians.

The aim of this paper is to explore different dimensions and factors of financial literacy in Malaysian working adults. This study would generate items to measure the construct in this study using an appropriate quantitative approach.

2. Literature Review

Financial literacy typically refers to a capacity to use a knowledge of finance and to be able to use it to make wise decisions for oneself [

6]. More specifically, it refers to the abilities and information that enable people to make wise financial decisions [

7]. According to [

8], the capacity to comprehend and utilize financial matters is known as financial literacy. A person’s ability to manage their finances and to prevent future large debt obligations will be aided by their understanding of financial literacy.

Financial literacy is formed with two types of measures, objective and subjective [

9]. Objective financial literacy can be measured through questions related to various financial issues such as interest rates, inflation, and the time value of money [

10]. The “Big Three” [

11] are three questions about compound interest, inflation, and risk diversification developed by [

12] to create a measure of financial literacy on an objective measure. The authors in [

13] measured financial literacy by asking basic questions related to knowledge about numeracy (interest), compound interest, inflation, and risk diversification.

Consumers can handle their financial affairs autonomously if they have a basic understanding of financial concepts and the capacity to apply their numeracy abilities in a financial environment. They will react appropriately to news and events that could affect their financial situation [

14]. Financial inclusion, financial development, and ultimately financial stability are all thought to benefit from financial literacy [

15]. In addition, financially smart investors are also more likely to divide their money over numerous projects in order to diversify risk [

16]. According to [

17], better financial decision-making is supported by increased financial capability and literacy. Thus, this facilitates better management and planning of life events, including retirement, housing purchases, and education. These planning elements must become a top priority and one of the key factors influencing financial stability.

Exploratory Factor Analysis

Typically, in social science studies, there are two main classes of factor analysis: Exploratory Factor Analysis (EFA) and Confirmatory Factor Analysis (CFA). Prior to doing the subsequent CFA, the EFA is conducted first [

18]. In general, EFA is heuristic. EFA has been one of the statistical techniques that is used the most frequently, particularly in social science research. Research suggests that the EFA technique produces more precise results when multiple measurable variables that are either endogenous or exogenous constructs in the analysis are used to represent each common factor [

19,

20]. In addition, EFA outlines the fundamental relationship among the studied variables and cannot be measured directly, but is represented as a group of items [

21]. According to [

22], EFA is used when the number of factors included in a set of variables is unclear.

As the name implies, EFA is exploratory, and researchers have no assumptions regarding the quantity or kind of variables. That is, it enables the researchers to investigate the key dimensions in order to develop a theory or model from a sizable collection of latent constructs, frequently represented by a set of items. Principal component analysis (PCA), which is utilized for data reduction in EFA, does not distinguish between common and unique variance [

23]. As advised by [

24], in the EFA technique, the value is suppressed at the threshold of 0.60 or higher once the EFA procedure is implemented. It is suggested that the high factor loading is a crucial signal. Moreover, EFA proposes the factor loading into the same component, in addition to minimizing the number of variables used in this investigation. Indicators included in the same component demonstrate that this outer loading aims to represent the measurement model. This component will be used in structural equation modeling after the researchers complete the EFA technique (SEM).

3. Methodology

To achieve the research objectives, this study used a cross-sectional research design to create a valid and reliable measure for the Financial Literacy construct, particularly in the working adult context. The participants in this study were school educators in Kelantan, Malaysia, and 100 randomly selected school educators were used as the sample. Data were collected through a structured questionnaire and analyzed using Exploratory Factor Analysis (EFA) to establish the rotated component analysis used for significant items in the model.

To determine the suitable Financial Literacy measures among working adults in Malaysia, the researchers developed a structured questionnaire that comprised 15 items, which were measured using a 10-point interval scale, from “1 = Strongly Disagree” to “10 = Strongly Agree”. The measurement of financial literacy was adopted and adapted from [

25,

26,

27].

4. Results

Calculating the coefficient alpha allows one to assess how reliable a scale is. Therefore, the reliability of the study’s items was assessed using the conventional Cronbach’s alpha approach. Based on suggestions by [

28], a more favorable coefficient alpha is above 0.70, as stated by [

29]. He states that Cronbach’s alpha is a consistent coefficient, indicating that the relationships among the item sets are proportionally correlated. In addition, in his opinion, a reliability value below 0.70 is considered a weak model. Moreover, the 15 items in the questionnaire have a Cronbach’s alpha value of 0.819, demonstrating the suitability and reliability of the Financial Literacy construct items in measuring the response.

4.1. Kaiser–Meyer–Olkin (KMO) and Bartlett’s Test of Sphericity

The researchers conducted EFA using principal component analysis with the varimax rotation method on 100 datasets to evaluate and purify the scale items, and to separate which items should be classified in the same components. According to [

30], a Kaiser–Meyer–Olkin (KMO) value of greater than 0.50 is used to purify the measurement items. However, this study used factor loadings above 0.60, so that only the remaining high factor loading can be processed for the subsequent step. In this case, the KMO value of 0.868 is excellent, as it exceeds the recommended value of 0.6. Additionally, the value of Bartlett’s Test of Sphericity must be less than 0.05 (

p-value < 0.05) for factor analysis to be acceptable. The Bartlett’s Test significance value for the present study is 0.000, which meets the required significance value of less than 0.05 [

31,

32].

Both Bartlett’s Test of Sphericity is significant (

p-value < 0.05) and the sampling adequacy by Kaiser–Meyer–Olkin (KMO) is excellent, since it exceeded the required value of 0.6. The authors in [

33] suggested that the data are adequate to proceed further with the data reduction procedure in EFA [

34].

The total variance explained is also an extraction process of the items, to reduce them into a manageable number before further analysis. In this process, components with eigenvalues exceeding 1.0 are extracted into different components [

35]. The outcome showed that the EFA process produced three components based on a computed Eigenvalue of greater than 1.0. The eigenvalues ranged between 2.866 and 2.105. Meanwhile, the variance explained for component 1 is 26.051%, for component 2 is 24.205%, and for component 3 is 19.134. This construct’s measurement yields a total explained variance of 69.390%. Given that it surpasses the required minimum of 60%, the total variance explained is acceptable [

36]. This indicates that the items are grouped into three dimensions with a total explained variance of 69.390%, which would be considered for further analysis.

4.2. Scree Plot

The Exploratory Factor Analysis (EFA) was employed for data analysis, to determine the number of components of the Financial Literacy construct. As illustrate in

Figure 2, the screen plot has identified three factors, while three factors have also been identified based on the initial eigenvalues and the total variance explained.

4.3. Component Matrix

According to [

31], the rotated component matrix was examined, and only items with a factor loading of above 0.6 were retained for further analysis.

Table 1 presents the three dimensions or components that emerged, and their respective items resulting from the EFA procedure. The factor loading for every item should be greater than 0.6 in order to be retained, since it indicates the usefulness of items in measuring the particular construct [

34,

35]. As a result,

Table 2 shows all 11 retained items, which will be considered for further analysis under the three dimensions of the Financial Literacy construct.

Next, the researchers constructed the latent variables for each variable, based on the EFA report. In this study, financial literacy is a second-order construct, measured by the following three components, namely numeracy, time money value, and inflation. Finally, the researchers computed Cronbach’s alpha using the internal reliability statistics test as presented in

Table 3. Cronbach’s alpha (α) was used to measure the internal consistency reliability of the selected items in measuring the construct. The value of Cronbach’s alpha should be greater than 0.7 for the items to achieve Internal Reliability [

31].

5. Conclusions

The present study contributes to the measurement of the Financial Literacy construct, particularly among school teachers in Kelantan, Malaysia. The EFA results of this study produced a structure that extracts three dimensions of the Financial Literacy construct, which are numeracy, time money value, and inflation. These dimensions can be measured using the 11 items developed in this study. This is because all of the reliability measures for the three dimensions showed a high Cronbach’s alpha value, hence meeting Bartlett’s Test achievements (significant), acceptable KMO values (>0.6), and factor loadings exceeding the minimum threshold of 0.6. This reflects that the items are applicable in this study [

36].

This study adds an important survey instrument to the literature that will help to measure the financial literacy dimensions. Without a proper definition and dimension available for financial literacy, there is a need for the present study to explore and examine the reliability of the Financial Literacy construct for working adults in the Malaysian context. Thus, using the final validated version of this dimension will be useful for future research. The finding of this study can be applied to the structural model in future research, and could benefit applied researchers who are interested in financial literacy research.

Author Contributions

Conceptualization, J.B.; methodology, J.B. and F.A.M.N.; investigation, J.B. and W.M.W.M.; validation, J.B., F.A.M.N., W.M.W.M. and M.M.; formal analysis, J.B.; writing—original draft preparation, J.B., F.A.M.N., W.M.W.M. and M.M.; writing—review and editing, J.B., F.A.M.N., W.M.W.M. and M.M.; supervision, J.B.; project administration, J.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

This research was partially supported by Universiti Teknologi MARA Kelantan Branch, Malaysia.

Conflicts of Interest

The authors declare no conflict of interest.

References

- OECD. OECD/INFE International Survey of Adult Financial Literacy Competencies. 2016. Available online: https://www-oecd-org.ezaccess.library.uitm.edu.my/finance/oecd-infe-survey-adult-financial-literacy-competencies.htm (accessed on 5 March 2020).

- Klapper, L.; Lusardi, A.; Van Oudheusden, P. Financial Literacy Around the World; World Bank: Washington, DC, USA, 2015. [Google Scholar]

- Ngui, N. Malaysians Are Borrowing Too Much, Not Saving Enough, The Star Online (30 August 2016). Available online: https://www.thestar.com.my/business/businessnews/2016/08/30/khazanah-malaysians-borrowing-too-much/ (accessed on 12 January 2018).

- Asian Institute of Finance, Finance Matters: Understanding Gen Y- Bridging the Gap of Malaysian Millennials. 2015. Available online: https://www.aif.org.my/clients/aif_d01/assets/multimediaMS/publication/Finance_Matters_Understaning_Gen_Y_Bridging_the_Knowledge_Gap_of_Malaysias_Millennials.pdf (accessed on 7 February 2019).

- Murugiah, L. The level of understanding and strategies to enhance financial literacy among Malaysians. Int. J. Econ. Financ. Issues 2016, 6, 130–139. [Google Scholar]

- Hogarth, J.M. Financial Literacy and Family and Consumer Sciences. J. Fam. Consum. Sci. 2002, 94, 15–28. [Google Scholar]

- Norman, A.S. Importance of financial education in making informed decision on spending. J. Econ. Int. Financ. 2010, 2, 199–207. [Google Scholar]

- Remund, D.L. Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Allgood, S.; Walstad, W.B. The effects of perceived and actual financial literacy on financial behaviors. Econ. Inq. 2016, 54, 675–697. [Google Scholar] [CrossRef]

- Khan, M.N.; Rothwell, D.W.; Cherney, K.; Sussman, T. Understanding the financial knowledge gap: A new dimension of inequality in later life. J. Gerontol. Soc. Work 2017, 60, 487–503. [Google Scholar] [CrossRef] [PubMed]

- Agnew, J.R.; Bateman, H.; Thorp, S. Financial literacy and retirement planning in Australian. Numeracy 2013, 6, 7. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial literacy and retirement planning in the United States. J. Pension Econ. Financ. 2011, 10, 509–525. [Google Scholar] [CrossRef]

- Hasler, A.; Lusardi, A. The Gender Gap in Financial Literacy: A Global Perspective; Global Financial Literacy Excellence Center, The George Washington University School of Business: Washington, DC, USA, 2017. [Google Scholar]

- Morgan, P.J.; Trinh, L.Q. Determinants and impacts of financial literacy in Cambodia and Viet Nam. J. Risk Financ. Manag. 2019, 12, 19. [Google Scholar] [CrossRef]

- Ramakrishnan, D. Financial Literacy-The Demand Side of Financial Inclusion. 2011. Available online: https://ssrn.com/abstract=1958417 (accessed on 22 April 2019).

- Abreu, M.; Mendes, V. Financial literacy and portfolio diversification. Quant. Financ. 2010, 10, 515–528. [Google Scholar] [CrossRef]

- Mahdzan, N.S.; Tabiani, S. The Impact of Financial Literacy on Individual Saving: An Exploratory Study in the Malaysian Context. Transform. Bus. Econ. 2013, 12, 4155. [Google Scholar]

- Afthanorhan, W.M.A.B.W.; Ahmad, S.; Mamat, I. Pooled confirmatory factor analysis (PCFA) using structural equation modeling on volunteerism program: A step-by-step approach. Int. J. Asian Soc. Sci. 2014, 4, 642–653. [Google Scholar]

- MacCallum, R.C.; Widaman, K.F.; Zhang, S.; Hong, S. Sample size in factor analysis. Psychol. Methods 1999, 4, 84. [Google Scholar] [CrossRef]

- Velicer, W.F.; Fava, J.L. Effects of variable and subject sampling on factor pattern recovery. Psychol. Methods 1998, 3, 231. [Google Scholar] [CrossRef]

- Hair, J.F.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Nayak, T.; Sahoo, C.K. Quality of work life and organizational performance: The mediating role of employee commitment. J. Health Manag. 2015, 17, 263–273. [Google Scholar] [CrossRef]

- Bentler, P.M.; Kano, Y. On the equivalence of factors and components. Multivar. Behav. Res. 1990, 25, 67–74. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed, a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Potrich, A.C.G.; Vieira, K.M.; Mendes-Da-Silva, W. Development of a financial literacy model for university students. Manag. Res. Rev. 2015, 39, 356–376. [Google Scholar] [CrossRef]

- Van Rooij, M.; Lusardi, A.; Alessie, R. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef]

- AKPK Financial Behaviour Survey 2018 (AFBeS’18). Financial Behaviour and State of Financial Well-being of Malaysian Working Adults. 2018. Available online: https://www.akpk.org.my/sites/default/files/AKPK_Financial%20Behaviour%20and%20State%20of%20Finanical%20Well-being%20of%20Malaysian%20Working%20Adult.pdf (accessed on 29 January 2021).

- Nunnally, J.C. An overview of psychological measurement. In Clinical Diagnosis of Mental Disorders; Wolman, B.B., Ed.; Springer: New York, NY, USA, 1978; pp. 97–146. [Google Scholar]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; Wiley: Hoboken, NJ, USA, 2010. [Google Scholar]

- Hair, J.F.; Wolfinbarger, M.F.; Ortinau, D.J.; Bush, R.P. Essentials of Marketing Research; McGraw-Hill/Higher Education: New York, NY, USA, 2008. [Google Scholar]

- Awang, Z. Structural Equation Modeling Using AMOS Graphic; Penerbit Universiti Teknologi MARA: Kuala Lumpur, Malaysia, 2012. [Google Scholar]

- Hoque, A.S.M.M.; Awang, Z.; Baharu, S.M.A.T.; Siddiqui, B.A. Upshot of Generation ‘Z’ Entrepreneurs’ E-lifestyle on Bangladeshi SME Performance in the Digital Era. Int. J. Entrep. Small Medium Enterp. (IJESME) 2018, 5, 97–118. [Google Scholar]

- Pallant, J. SPSS Survival Manual. A Step-by-Step Guide to Data Analysis Using SPSS, 4th ed.; Allen & Unwin: Crows Nest, Australia, 2011; Available online: www.allenandunwin.com/spss (accessed on 28 March 2021).

- Yahaya, T.; Idris, K.; Suandi, T.; Ismail, I. Adapting instruments and modifying statements: The confirmation method for the inventory and model for information sharing behavior using social media. Manag. Sci. Lett. 2018, 8, 271–282. [Google Scholar] [CrossRef]

- Awang, Z. SEM Made Simple: A Gentle Approach to Learning Structural Equation Modelling; MPWS Rich Resources: Bandar Baru Bangi, Malaysia, 2015. [Google Scholar]

- Awang, Z.; Afthanorhan, A.; Mamat, M.; Aimran, N. Modeling Structural Model for Higher Order Construct (HOC) using Marketing Model. World Appl. Sci. J. 2017, 35, 1434–1444. [Google Scholar]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}