Abstract

In recent years, cryptocurrencies have received substantial attention from investors, researchers and the media due to their volatile behaviour and potential for high returns. This interest has led to an expanding body of research aimed at predicting cryptocurrency prices, which are notably influenced by a wide array of technical, sentimental, and legal factors. This paper reviews scholarly content from 2014 to 2024, employing a systematic approach to explore advanced quantitative methods for cryptocurrency price prediction. It encompasses a broad spectrum of predictive models, from early statistical analyses to sophisticated machine and deep learning algorithms. Notably, this review identifies and discusses the integration of emerging technologies such as Transformers and hybrid deep learning models, which offer new avenues for enhancing prediction accuracy and practical applicability in real-world scenarios. By thoroughly investigating various methodologies and parameters influencing cryptocurrency price predictions, including market sentiment, technical indicators, and blockchain features, this review highlights the field’s complexity and rapid evolution. The analysis identifies significant research gaps and under-explored areas, providing a foundational guideline for future studies. These guidelines aim to connect theoretical advancements with practical, profit-driven applications in cryptocurrency trading, ensuring that future research is both innovative and applicable.

1. Introduction

Modern financial systems are based on fiat money, which is known to have many advantages due to its divisibility, durability, transferability, and scarcity [1]. However, there are also disadvantages, including: centralised government control of currency, which can lead to various problems such as hyperinflation and income inequality [2]; the vulnerability of ledgers that can be manipulated and violated; and the way in which money is transacted, which requires the involvement of a trusted third party [3].

These problems were addressed with the introduction of Blockchain technology, by Satoshi Nakamoto in October 2008 which was underpinned by the world’s first successful, digital currency (cryptocurrency), namely, Bitcoin [4,5]. Bitcoin was created in order to solve the “double-spending” problem, which has affected all attempts to create an electronic version of cash since the Internet’s creation [6].

Until the invention of cryptocurrency, it was impossible for two parties to transact electronically without employing the service of a central, third party or a trusted intermediary [7,8]. Cryptocurrencies are an application of blockchain technology in which peer-to-peer online transactions are possible without the involvement of a third party or intermediary financial institutions, such as banks [3,9]. These instruments have an advantage over traditional centralised methods as they provide integrity, anonymity, immutability and decentralisation [4,8]. Based on the uniqueness of this financial instrument, it has gained a lot of attention from businesses, consumers, investors and traders [10].

Cryptocurrencies have experienced a huge rise in popularity over recent years, largely due to the lure of rapid investment returns (that result from high price volatility) and the influence of key social media actors (such as Elon Musk and interest in Dogecoin and Shiba Inu [11]). Many investors and institutions have heavily invested in cryptocurrencies, but the market has proven to be much less stable than traditional equity markets. It has demonstrated significantly higher volatility compared to traditional equity markets, a characteristic well-documented in the literature. For instance, Bouri et al. [12] (2021) provide empirical evidence that the price volatility of cryptocurrencies far exceeds that of conventional stocks, reflecting their nascent and speculative nature. The cryptocurrency market is affected by many technical, sentimental and legal factors leading to volatility [4,13], and as a result, many day traders have turned their attention to cryptocurrencies to capitalise on the extreme volatility compared with traditional equities (such as stocks, indices, forex etc.) [14,15,16].

Despite fundamental differences between cryptocurrencies and traditional equities—such as the absence of physical assets or central regulation—investors often approach cryptocurrency markets similarly to conventional equities. Cryptocurrencies were the first digital assets managed by asset managers; thus, they possess distinct characteristics and their behaviour as an asset class is still in the process of being understood [15]. Nonetheless, investors frequently employ similar trading strategies used in traditional markets, applying both fundamental and technical analysis to forecast future prices over varying time horizons, based on the intrinsic properties of each asset and historical market data. This behaviour is critically examined by Gandal et al. (2018) [17], who argue that attraction to cryptocurrencies among investors may stem from perceived parallels in market mechanics, despite the fundamental discrepancies in the underlying factors that drive price dynamics.

Besides catching the attention of investors and traders, cryptocurrency market prediction has also led many researchers to investigate the various factors that can influence price fluctuations. These researchers explore the myriad factors influencing price volatility, thereby transforming market research into an interdisciplinary domain. This domain not only encompasses economics, but also integrates computational and data sciences, fostering the development of sophisticated algorithmic models for data analysis, designed to deliver precise and reliable price forecasts.

Scope and Objectives

The complex cryptocurrency market is influenced by a large number of factors wherein the prediction of future market dynamics is relatively challenging [18,19]. In light of emerging technologies and the volatile nature of the cryptocurrency market, this review significantly advances the field by systematically collating and synthesising current methodologies and by introducing a nuanced understanding of the interaction between various predictive models and market dynamics from diverse aspects. Specifically, this research contributes to the existing literature in the following ways:

- Comprehensive Parameter Analysis: Beyond simply identifying common parameters key influential parameters that have been considered for algorithmic methods used in cryptocurrency price prediction, this review includes an exploration of less-studied parameters, offering insights into their underutilised potential.

- Methodological Innovation: By examining state-of-the-art methodologies, this review highlights the evolution of predictive models from basic statistical approaches to sophisticated machine learning and deep learning techniques. It critically assesses the applicability of these models in real-world market scenarios, and a novel evaluation on how they utilise the various data sources available; and

- Future Research Directions: Based on the identified shortcomings, research challenges and gaps in the literature, this review proposes research avenues to help guide future research directions.

This survey serves a crucial role in addressing existing gaps in the understanding of cryptocurrency price prediction. By systematically reviewing the current state of research, a comprehensive overview of the methodologies and influential parameters utilised is provided. This survey not only consolidates existing knowledge but also serves as a guide for future research endeavours in the dynamic field of cryptocurrency markets. Recognising the unique challenges posed by technical, sentimental, and legal factors, this survey aims to assist researchers and practitioners in navigating these complexities and developing more robust predictive models.

While previous works have demonstrated success in predicting traditional stock markets, the unique characteristics of cryptocurrency markets demand novel approaches [20]. The technical, sentimental, and legal factors contributing to cryptocurrency market instability have spurred diverse prediction methods, ranging from traditional regression analyses to sentiment analyses using social media and news media [21,22,23,24,25,26,27,28,29]. More recently, machine and deep learning techniques have gained traction for cryptocurrency price prediction, showcasing varying degrees of success in cryptocurrency price prediction.

In this work, a comprehensive review of recent literature relating to cryptocurrency price prediction is undertaken. In Section 2, the methodology for the identification of papers is outlined—specifically: paper selection; duplicate removal; and filtering of results. Section 3 identifies and groups key influential parameters used in cryptocurrency price prediction, and Section 4 discusses the various data analysis methods used, highlighting how they leverage available parameters. Finally, in Section 5, this review identifies and discusses both well-addressed and under-researched areas in cryptocurrency price prediction, aiming to guide future research endeavour in this dynamic and evolving field.

2. Methodology

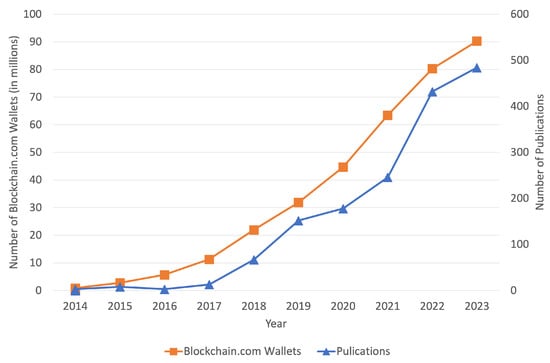

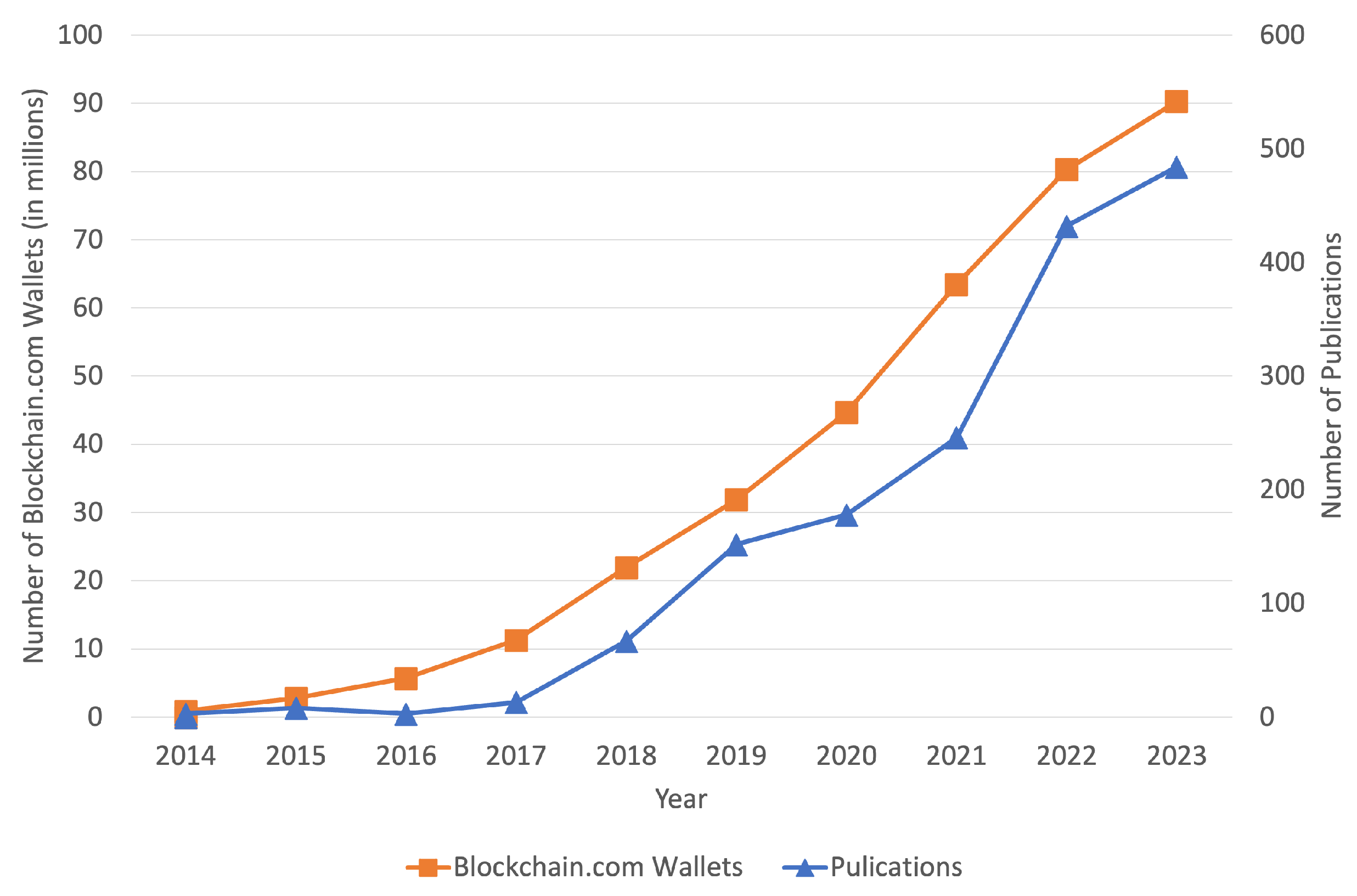

Given the relatively recent surge in both user engagement and scholarly investigation surrounding cryptocurrency price prediction, as evidenced in Figure 1, coupled with the significant fluctuations in cryptocurrency values (with some experiencing a decline of over 90%), this review meticulously compiles relevant literature spanning from February 2014 to the final literature extraction at 1 May 2024. The start year, 2014, is critical as it marks the emergence of significant altcoins like Ethereum, which expanded the landscape beyond Bitcoin, thus increasing market maturation. This year also coincides with the first scholarly articles which utilise meticulously selected keywords associated with cryptocurrency price prediction that (which will be discussed in the next section), establishing a practical boundary to encapsulate significant technological advancements and regulatory changes that continued to shape market dynamics [13]. By examining scholarly content from this defined period, this research aims to offer a comprehensive assessment of the theoretical underpinnings and the evolution in the domain of cryptocurrency price prediction, substantiating the choice of this study’s timeframe.

Figure 1.

Number of Blockchain.com cryptocurrency wallets and research publications related to cryptocurrency price prediction (publication data is retrieved from the SCOPUS database) (data as of final literature extraction at 1 May 2024).

The sources for this compilation were rigorously selected from peer-reviewed academic works featured in renowned online databases, namely SCOPUS, Elsevier (Science Direct), IEEE Xplore, and the ACM Digital Library. These databases were chosen in order to: (1) gain a broad overview of research on this topic, as can be provided by the largest database of peer-reviewed literature, SCOPUS (2) access detailed and high-quality articles from diverse aspects through Elsevier (Science Direct); and (3) obtain literature specifically from the computer science domain through IEEE Xplore and ACM Digital Library.

Figure 1 not only illustrates the increase in user engagement but also distinctly showcases the year-on-year changes in the volume of research publications within this field. This visualisation underscores a growing academic interest in cryptocurrency price prediction, reflecting the evolving nature and significance of this research area.

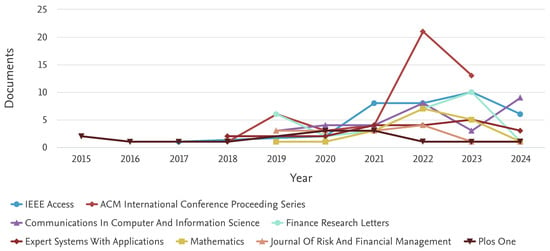

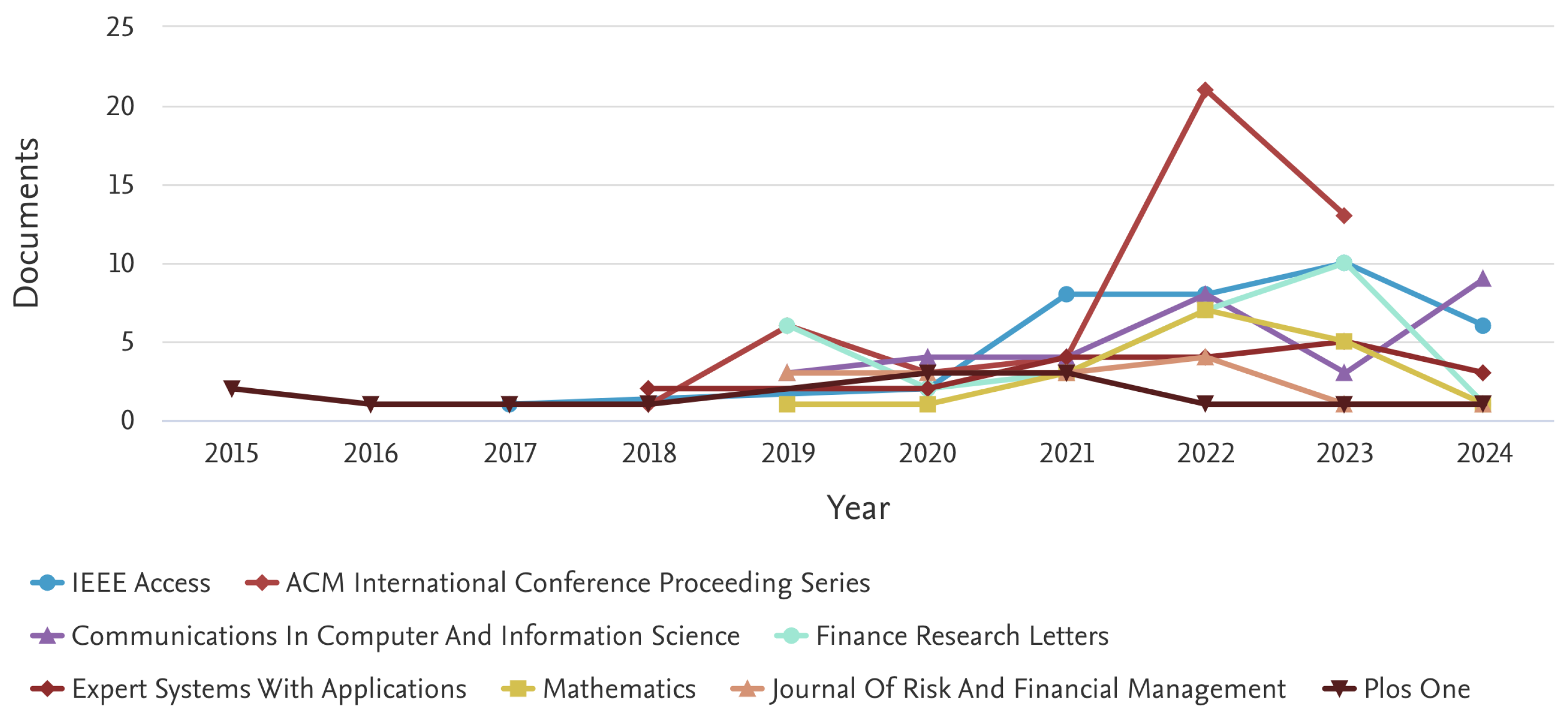

Additionally, Figure 2 includes an analysis summarising the distribution of papers across various academic journals per year. This breakdown provides insights into the diversity of publication outlets and the interdisciplinary nature of the field, reflecting its relevance across multiple academic disciplines–particularly computer science and economics.

Figure 2.

Annual Distribution of Cryptocurrency Price Prediction Publications Across Various Academic Journals (publication data is retrieved from the SCOPUS database) (data as of final literature extraction at 1 May 2024).

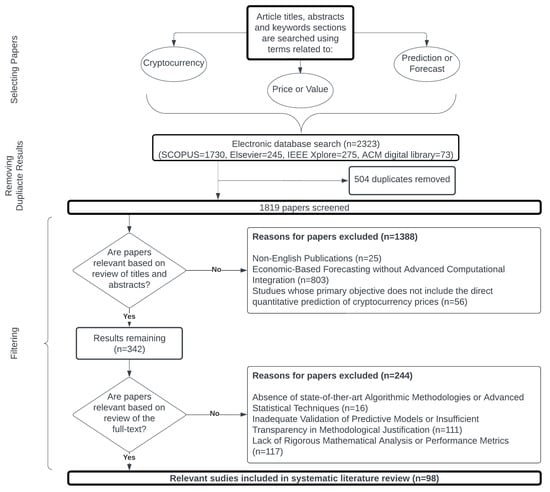

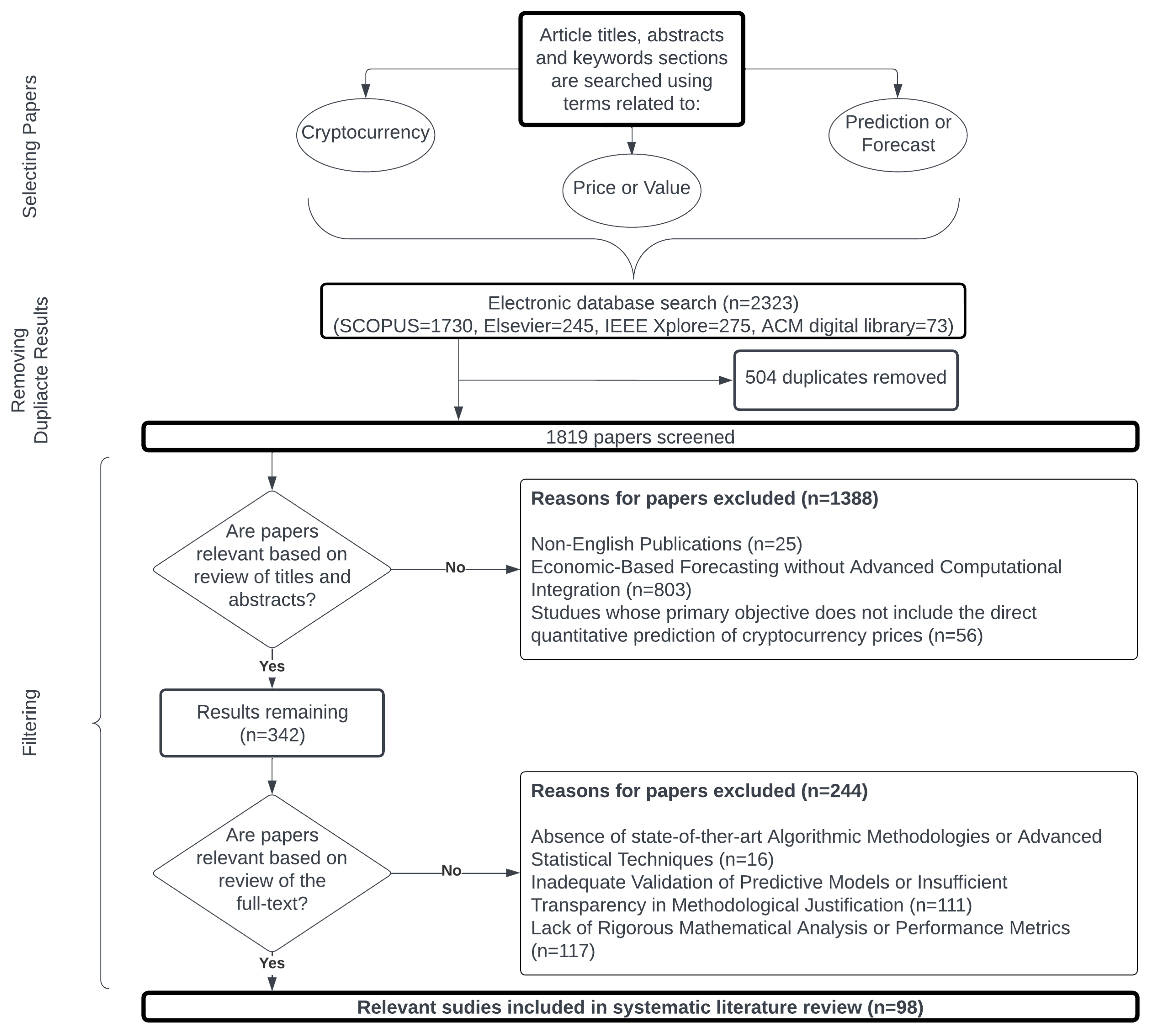

Figure 3 presents an overview of the review process. The 3-step process was meticulously designed to ensure the inclusion of papers that rigorously apply sophisticated, quantitative methods for cryptocurrency price prediction. Initially, papers were selected using a set of predefined keywords. Subsequent steps included the removal of duplicates and a detailed filtering process. This filtering specifically excluded papers that did not focus on advanced quantitative methods or state-of-the-art models, or those that failed to provide rigorous mathematical analyses and outcomes, ensuring the inclusion of only the most relevant and scientifically robust studies. Each step is explained in detail in the following sub-sections.

Figure 3.

Flowchart of the identification and selection of relevant papers.

2.1. Paper Selection

In the first step, sets of keywords pertinent to cryptocurrency price prediction were carefully selected to encompass a comprehensive range of terms relevant to modern cryptocurrency markets and their dynamics. These were utilised to conduct searches across the aforementioned databases to capture the essence of computational and predictive approaches in cryptocurrency price prediction. These keywords included: [“cryptocurrency” OR “cryptocurrencies” OR (“crypto” AND “currency” ) OR “stablecoin” OR “altcoin” OR (“digital” AND (“coins” OR “coin”)) OR (“digital” AND (“currencies” OR “currency”)) OR (“digital” AND (“tokens” OR “token”)) OR “Bitcoin” OR “Ethereum”], combined with the relevant terms [“price” OR “value” OR “valuation” OR “worth”] AND [“prediction” OR “predicting” OR “predict” OR “predicted” OR “forecast” OR “forecasting” OR “forecasted”]. This selection aimed to capture the essence of computational and predictive approaches specifically tailored to cryptocurrencies, and so it is important to clarify that terms such as ”NFT” and “CBDC” were deliberately excluded due to their distinct market behaviours and the nascent nature of their trading environments. While NFTs and cryptocurrencies often are associated with one another, the exclusion of NFTs is justified by their primary market function as collectibles or art pieces, which does not align with the typical trading dynamics and liquidity found in traditional cryptocurrency markets, and are often not traded frequently enough to generate reliable predictive models based on quantitative analysis. Similarly, CBDCs were excluded due to their regulatory and central bank-backed nature, which fundamentally differs from decentralised cryptocurrencies and their pricing dynamics. CBDCs are heavily by monetary policy rather than market speculation, and therefore may potentially require prediction approaches that focus on regulatory impacts rather than purely market-driven factors. Including these would necessitate a distinct analytical framework that focuses on regulatory impacts and cultural valuation, which falls outside the scope of this review.

This keyword selection process was crucial for initially identifying studies that potentially align with our rigorous review criteria. All of these terms were searched within the article title, abstract or keywords sections, ensuring that the initial pool of papers was relevant and comprehensive. The search returned 1730 results from Scopus, 245 results from Elsevier (Science Direct), 275 results from IEEE Xplore and 73 results from ACM digital library, for a total of 2323 results which were last retrieved and updated on 1 May 2024.

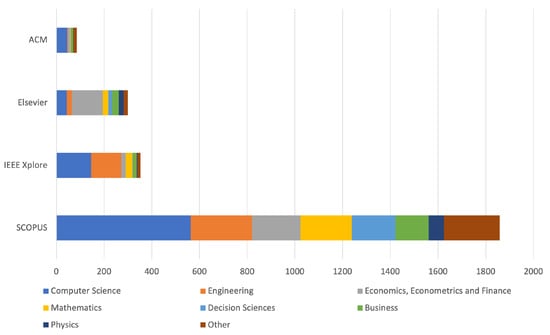

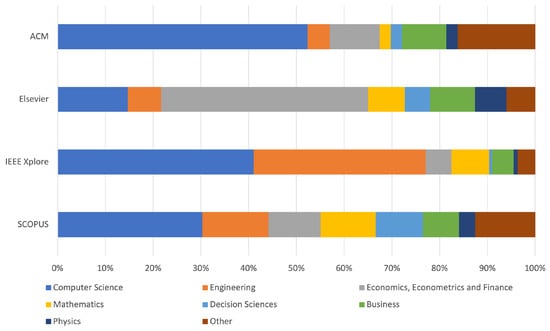

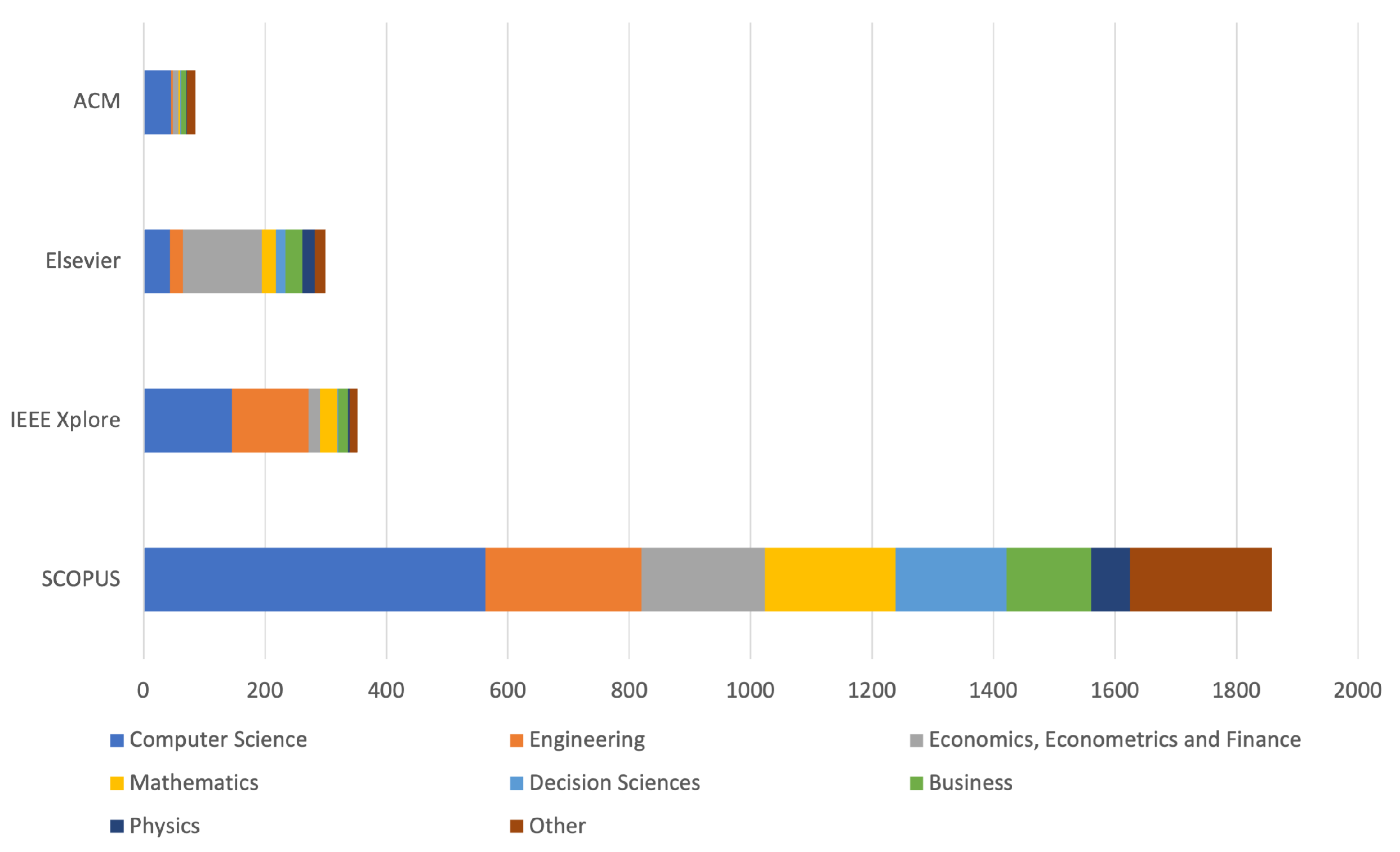

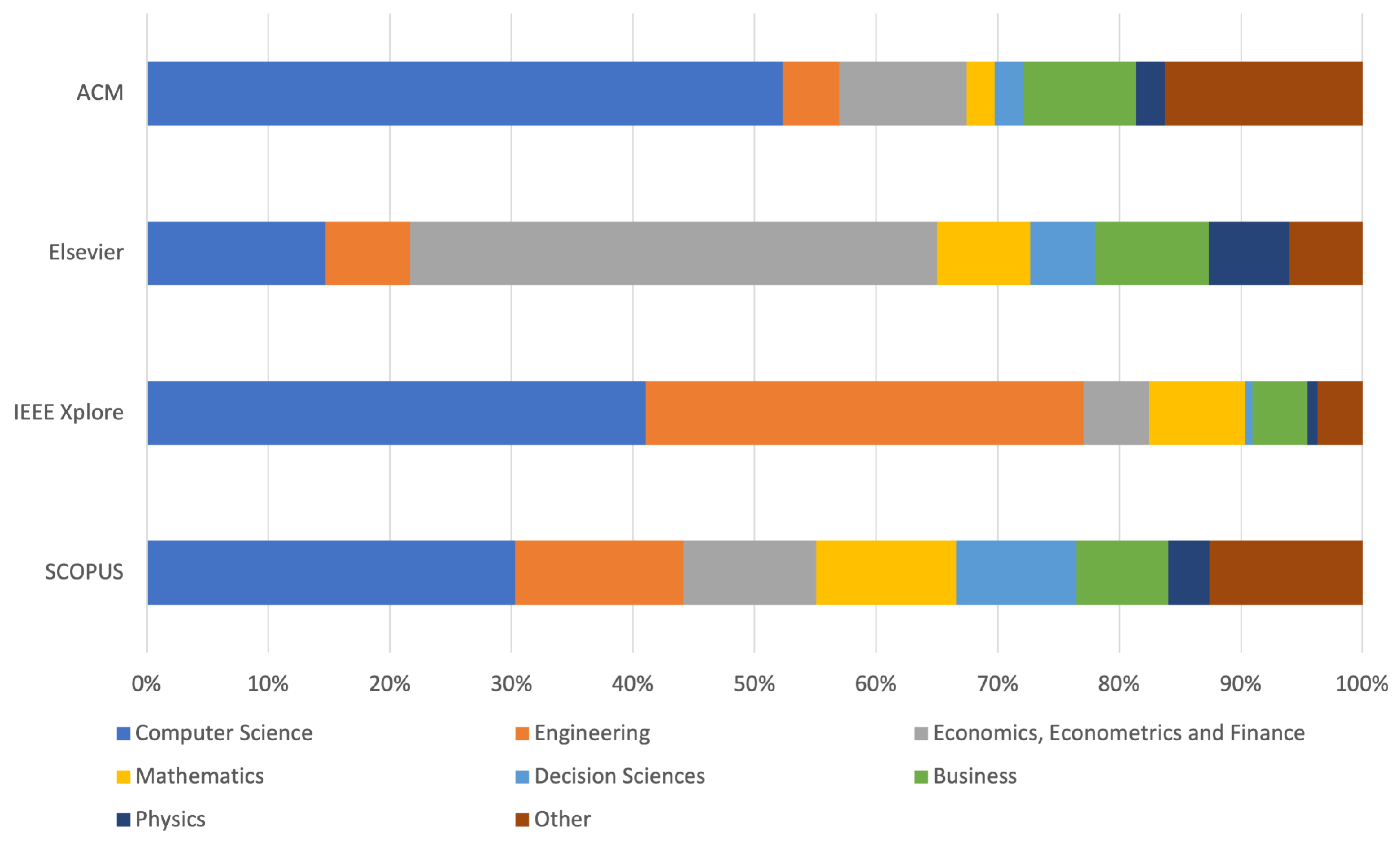

Figure 4 shows the absolute number of results retrieved from each database, grouped by subject area. Figure 5 displays the grouping as a percentage for each database. If the journal or conference where a paper is published is associated If the journal or conference where a paper is published is associated with multiple disciplines, it counts for all disciplines. As can be seen in the figures, the main field of focus for Scopus, IEEE Xplore and ACM digital library is computer science, whereas the main subject area for the Elsevier database is economics, econometrics and finance. Other major subject areas among all the databases include engineering, mathematics and business.

Figure 4.

Disciplines reflected in documents relative to each database considered (data as of final literature extraction at 1 May 2024).

Figure 5.

Disciplines reflected in documents relative to each database considered by percentage (data as of final literature extraction at 1 May 2024).

2.2. Duplicate Removal

The second step of the review process required removing the overlapping results between each of the databases. There was a reasonable amount of overlap given the similarities between the top disciplines, journals/conferences and authors that were present among all the databases. After removing 504 duplicates, there were a total of 1819 unique results across all databases i.e., a total of 89 results were found in addition to the 1730 results from the SCOPUS database.

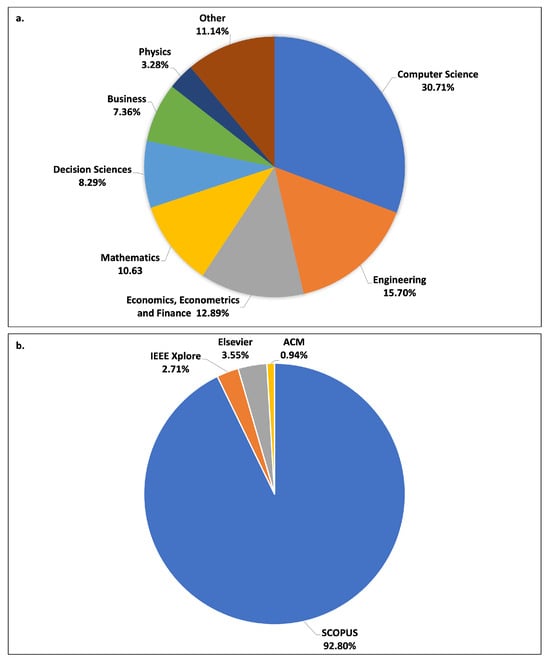

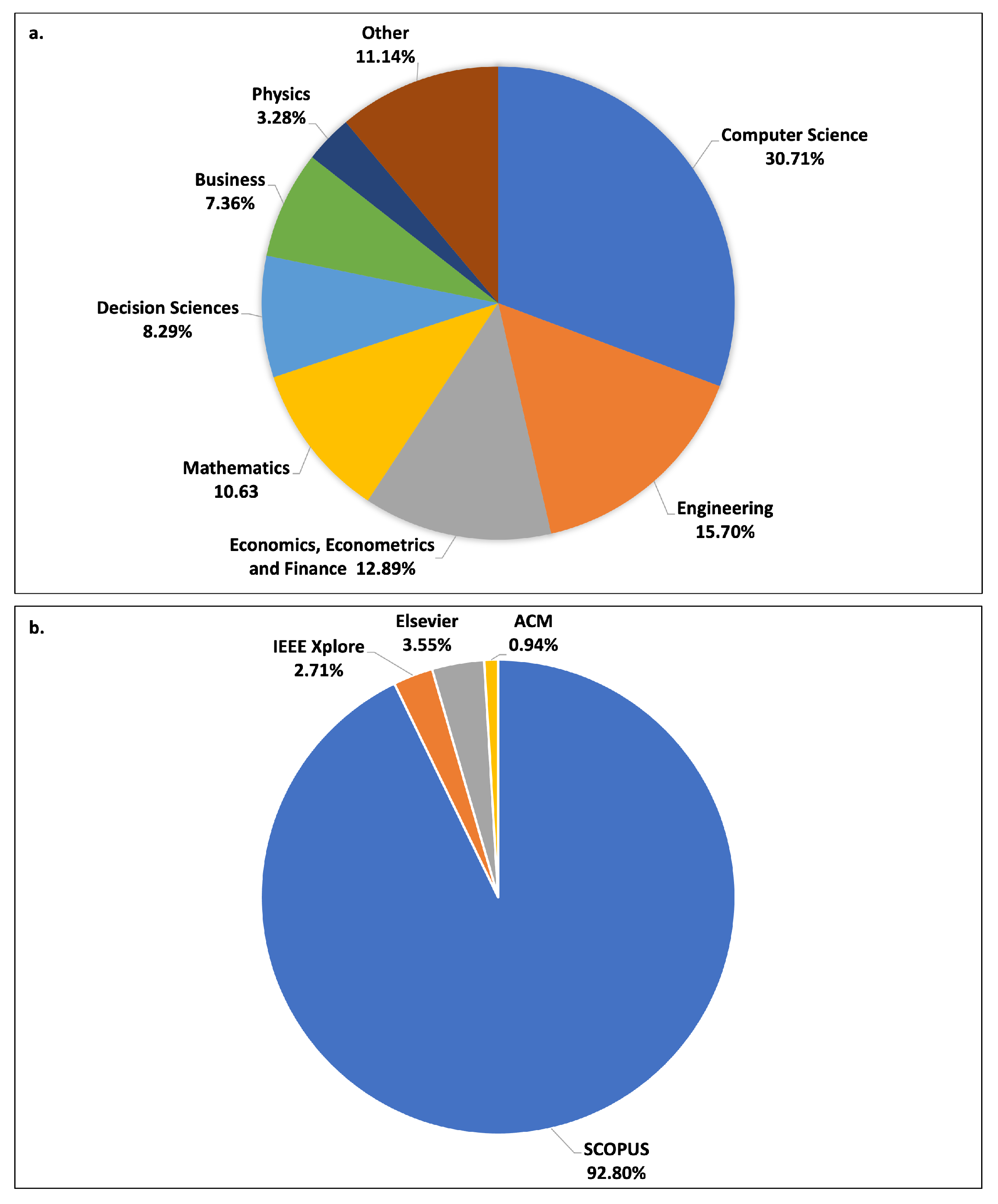

Figure 6a shows the distribution of papers across disciplines after removal of duplicates. If the journal or conference where a paper is published is associated with multiple disciplines, it counts for all disciplines. The four main disciplines were identified as: computer science; engineering; economics, econometrics and finance; and mathematics. It can be seen that the computer science discipline dominates the field, accounting for 30.71% of publications, whereas the economics, econometrics and finance discipline accounts for less than half of the dominating field’s publications at 12.89%—even though the papers from databases specific to computer science (26 from IEEE Xplore, 9 from ACM Digital Library; see Figure 6b) make up only 3.65% of the corpus. This indicates that the prediction of cryptocurrency markets is now a task considered by computer and data scientists more than economists. The top four leading journals were IEEE Access, Finance Research Letters, Expert Systems With Applications and PLoS ONE.

Figure 6.

(a) Disciplines reflected in journals and conferences as publication outlets, (b) Distribution of results across databases (data as of final literature extraction at 1 May 2024).

Considering that most of the results for research in this field have been provided by SCOPUS; the significant amount of overlapping results between SCOPUS and the other databases; and the similarities between the top disciplines, journals/conferences and authors that were present among all the databases—it could be deemed sufficient to use solely the SCOPUS database for practitioners or researchers in this field with limited time or resources available.

2.3. Results Filtering

The final step involved filtering the remaining, unique results by applying appropriate conditions and parameters. An intricate filtering process where the remaining, unique results were scrutinised based on rigorous conditions and parameters detailed below.

This process was essential to ensure that only studies utilising advanced quantitative methods specifically aligned with computer science approaches to cryptocurrency price prediction, and presents relevant and substantial mathematical outcomes were included:

- Language and Scope: This review specifically targets studies that utilise algorithmic methodologies such as state-of-the-art computational techniques (including machine learning, deep learning, etc.), and other advanced statistical techniques capable of handling large dataset and extracting predictive insights from complex market dynamics. Studies not written in English, or primarily employing traditional economic or financial models without integration of these advanced state-of-the-art techniques were excluded.

- Relevance to Cryptocurrency Price Prediction: Studies were also excluded that did not directly aim to predict cryptocurrency prices through quantitative models. For instance, papers primarily using traditional or theoretical economic analysis or financial forecasting models, without empirical testing or incorporating advanced computational techniques, were not considered.

- Methodological Rigor: Studies lacking in rigorous mathematical analysis evident from either the absence of rigorous statistical analysis or failure to report essential performance metrics like accuracy, precision, recall, or mean squared error were excluded. Additionally, studies that do not provide proper validation methods for their predictive models or fail to describe their methodologies transparently were also excluded. It was crucial that included studies demonstrated substantial mathematical outcomes with sufficient validation or justifications of there methods used, that contribute directly to the field of cryptocurrency price prediction.

For an example of an excluded study is the work by Pirgaip et al. [30] titled ’Bitcoin Market Price Analysis and an Empirical Comparison with Main Currencies, Commodities, Securities and Altcoins’. Despite its relevance, it was ultimately excluded because it focused primarily on co-integration and causality analysis and did not meet the criteria of integrating these methods within a broader computational framework. Such studies, while valuable, did not meet the review’s criterion of contributing directly through predictive modelling. This decision highlights our rigorous standards for inclusion, focusing on studies that not only have relevance to cryptocurrency price prediction, but also use sophisticated models and has a strong mathematical foundation.

Upon review of the titles and abstracts, the exclusion process rigorously applied the criteria established above to filter out unsuitable studies. Specifically, papers not written in English and those approaching the subject from a purely economic perspective, rather than a computational one, were immediately discarded. Further, any studies that did not employ methodologies directly relevant to the quantitative prediction of cryptocurrency prices were also eliminated. This meticulous screening process resulted in the exclusion of 1389 papers, narrowing the field to 341 potentially relevant studies.

A detailed assessment of the full texts of these remaining articles was then conducted to ensure their strict alignment with the core focus of this review, based on the inclusion criteria above. This focus was specifically defined as research utilising sophisticated, state-of-the-art computational techniques, with proper validation methods for their predictive models or offer transparency in their methodological justification, and demonstrating mathematical rigor with substantial results. Only papers that rigorously met these stringent standards for rigor and relevance were retained. This critical phase of the review process led to the exclusion of 248 papers, ultimately selecting 93 studies that comprehensively satisfied all the specified inclusion criteria and were thus included in the final analysis of literature.

2.4. Initial Review

Having established the corpus of papers for this survey, relevant information can now be synthesised. Various elements are considered among the reviewed papers which can be categorised as: parameters; prediction algorithms; cryptocurrencies; and time frames considered for prediction [31,32,33,34,35,36].

The literature considers various parameters that may influence the price of cryptocurrencies. The types of parameters considered include previous price and volume, technical indicators such as moving averages and Bollinger bands, semantic data from Twitter and financial news media, and features of the block-chain such as transaction fees and miners’ revenue. These are utilised in a range of prediction models (primarily machine and deep learning algorithms) and include: regression analyses; Naïve Bayes; support vector machines (SVM’s); random forests; autoregressive integrated moving average (ARIMA); autoregressive integrated moving average with exogenous variables (ARIMAX); deep neural network (DNN); recurrent neural network (RNN); convolutional neural networks (CNN); gated recurrent units (GRU); long short-term memory networks (LSTM); convolutional long short-term memory networks (ConvLSTM); LSTM and GRU based hybrid deep learning model (LSTM-GRU); and multi-scale residual convolutional neural network (MRC) and LSTM based hybrid deep learning model (MRC-LSTM). More details and relevant references can be found in Table 1.

Table 1.

Variety of elements considered in the reviewed literature.

In the literature, there is a diverse focus on cryptocurrencies for price prediction, encompassing not only widely recognised ones with high market capitalisation like Bitcoin, Ethereum, and Litecoin but also lesser-known, lower market cap cryptocurrencies such as Zcash and Dash. This comprehensive approach allows for a broad understanding of the market dynamics across different tiers of cryptocurrencies. The research spans a variety of time frames, from minute-to-minute fluctuations to weekly trends, and even incorporates years’ worth of data for more in-depth analysis. The frequency of studies per cryptocurrency is revealing: Bitcoin emerges as the most extensively studied cryptocurrency, featuring in approximately 79% of the research papers. Ethereum also garners considerable attention, being the focus of about 32% of studies. Other cryptocurrencies like Monero, Ripple, Dash, and Zcash each constitute about 4.3% to 6.4% of the research, highlighting a growing interest in a diverse range of digital currencies. It’s important to note that these percentages are not mutually exclusive, as some studies explore multiple cryptocurrencies, leading to overlaps in the distribution. This data, along with a detailed breakdown of the time frames and methodologies used, are systematically organised in Table 1. Studies covering multiple cryptocurrencies are accounted for in each relevant category, offering a comprehensive view of the research landscape. Additionally, for a detailed overview of some of these studies, Table 2 provides comprehensive annotations on various aspects of classic literature in this field.

Table 2.

Detailed annotations of classic literature in cryptocurrency price prediction.

The diverse methodologies and focus areas outlined in Table 2 underscore the complexity and multifaceted nature of cryptocurrency price prediction research. Based on the analysis of the content and attention of the reviewed literature, only specific influential parameters that have shown to be prevalent, reliable and significant in current state-of-the-art methodologies will be considered in the following analysis of the reviewed literature. The insights from the analysis are then compiled and research gaps and under-addressed areas in the literature are identified and discussed, which forms the main contribution of this review.

3. Influential Parameters for Cryptocurrency Price Prediction

This section describes the most important influential parameters that are utilised for the price prediction of cryptocurrencies with the most success, it elaborates on how they are used in the process of building a prediction model, and what combinations of parameters are employed. A variety of parameters have been mentioned in the literature, however, some of these have shown to be less significant in price prediction analysis. Some noteworthy factors that have been considered for this task with less prevalence and significance in previous works include: relating Bitcoin price and search engines [53], and implementing the relation of a cryptocurrency with other financial indicators such gold, S&P 500 index, USD and other cryptocurrencies [3,4,20,33,50,51,52,53,122]. Of the reviewed literature, four parameters have been identified as the most influential for cryptocurrency price prediction. They include: previous price and volume data; technical indicators (simple and exponential moving averages); blockchain features (including transaction fees and miners revenue); and social media sentiment. In the following subsections, these parameters are covered in more detail.

3.1. Price and Volume

As can be seen in Table 1, the majority of papers selected for this review have considered previous price and/or volume in their analysis, which indicates that these have been the most prominent parameters used in cryptocurrency price prediction. This includes average, opening, closing, high and low prices, and trading volumes across many time frames. This comes as no surprise, as price action is the foundation of technical analysis which most traders of any financial instrument (stocks, forex, cryptocurrencies etc.) use every day [123]. Highlighting key price support and resistance areas, identifying certain price patterns that often play out in predictable ways, and using various technical indicators, which are used to influence trading decisions in technical analysis, are all based on the previous price (and volume) of these financial instruments.

Studies that have used previous price and/or volume as parameters have employed either statistical analysis techniques, such as regression analyses or Granger causality [21,24,25,26,27,28,41,42,43,46], as well as more advanced machine and deep learning methods. Some benefits of using this parameter in cryptocurrency prediction analysis include its relevancy, the sufficiently large quantity of data available on multiple time frames, and the ability for this parameter to be easily extracted from cryptocurrency exchanges. Shortcoming of utilisation of these parameters is related to fact that on variety of exchanges (e.g., Binance or CoinSpot) the price and volume values can vary depending on the exchange considered, which may create slight inaccuracies in the price prediction analysis.

3.2. Technical Indicators

As mentioned above, technical analysis is a widely used method for price prediction among day traders [123]. Within this analysis, various day trading tools called technical indicators are employed, which can be used for price prediction. Some of these include various moving averages, Bollinger bands, relative strength index (RSI), Fibonacci studies and a plethora of others. In addition to these indicators, technical analysis also considers certain price patterns (for example: cup and handle; double bottom/top; and ascending and descending triangles or wedges) that are referred to as subjective technical analysis methods, since these price patterns are not precisely defined. This can be seen in Figure 7 (https://www.tradingview.com/chart/BTCUSDT/Adx5wasL-Fitting-patterns-to-your-bias/?amp, accessed on 19 June 2024) which gives a visual representation of how the same price chart can be interpreted as a variety of different price patterns. A consequence of this is that a particular conclusion derived from this subjective method reflects the individual interpretations of the analyst applying the method [124]. Therefore, price patterns are not considered for price prediction as widely in the literature as the objective, technical indicators, which have calculated, quantitative values derived from previous prices.

Figure 7.

Ambiguous price charts which can be interpreted as a variety of price patterns.

As can be seen in Table 1, only 5 of the considered papers have utilised this parameter, which is surprising given its wide use in day trading. However, the studies considering this parameter have all been published in recent years (from 2018) indicating that this is an emerging area requiring more research and greater focus. Similar to price and volume, the benefits of using technical indicators include its relevancy and the sufficiently large quantity of data available, across multiple time frames, which can be easily extracted from cryptocurrency exchanges. A particular limitation in using technical indicators is the number of insignificant indicators that could be considered which do not correlate with price changes. It is therefore important to first determine which indicators correlate with cryptocurrency price changes to know which of these to consider in cryptocurrency price prediction analysis.

3.3. Blockchain Features

In addition, and in contrast, to traditional financial markets, cryptocurrencies may also be influenced by blockchain information. These blockchain features consist of statistics related to the blockchain of each cryptocurrency. They include features such as total number of circulating coins, transaction fees, miners revenue, transaction rate per second and a range of other blockchain features (which can be found at https://www.blockchain.com/explorer/charts#block, accessed on 1 May 2024). As can be seen in Table 1, only 5 papers have considered blockchain features, however, given that these features are unique to cryptocurrency markets, they still require more research and greater focus.

The benefits of using this parameter are its relevancy and ability for the data of these features to be easily extracted. Similar to technical indicators, given the range of blockchain features which may affect cryptocurrency price, determining which of these have a strong correlation with changes in price (and which do not) will benefit traders, investors and researchers to make more informed decisions in cryptocurrency price prediction analysis.

3.4. Social Media Sentiment

Sentiment analysis of social media posts is a widely used parameter for cryptocurrency price prediction. A large number of studies have been carried out to study the relationship between social media sentiment and cryptocurrency prices, as shown in Table 1. This analysis is one of the most prominent parameters used in cryptocurrency price prediction due to its direct measurement of public opinion and speculative atmosphere surrounding digital currencies [125].

The primary platforms of focus are Twitter and Reddit, both of which are valuable sources of real-time public sentiment [126,127]. The benefits of using social media sentiment include the ease of data extraction via Twitter and Reddit APIs, and the availability of a vast amount of user-generated content on Reddit that reflects diverse viewpoints and is indicative of community-driven market movements.

- Examples of data extraction include:

- Twitter: Tweets containing specific keywords or hashtags, tweets posted by certain influential users or institutions, and tweets posted by users with a specific minimum or maximum number of followers. Some previous works have also extracted data by using keywords and hashtags relating to specific equities or equity markets, for example, Kilimci [22] used “BitcoinDollar”, “BitcoinUSD”, “BTCDollar”, “BTCUSD” for the extraction of Bitcoin related tweets. Others have used posts that contain explicit statements of the user’s mood states, for example, Bollen et al. [27] used posts with the expressions “I feel”, “I am feeling”, “I don’t feel”, “I’m”. These data points can be leveraged to gauge market sentiment and predict potential price movements based on the emotional tone and public reactions to market events or news [21,22,23,24,26,27,28,29,35,36,42,50,61,103,106,107,109,110,111,112,113].

- Reddit: Analysis of comments and posts in both general and specific cryptocurrency-related subreddits. This involves tracking the frequency and sentiment of posts about specific cryptocurrencies or the overall cryptocurrency market as a whole, and examining the community engagement that follows specific and general market-related events. For instance, the subreddit r/Bitcoin frequently features discussions that reflect user sentiments ranging from bullish to bearish, which correlate with market movements [114]. During specific events like regulatory announcements or technological advancements (e.g., Bitcoin halving), the increase in posting frequency and shift in sentiment can be significant indicators of market. Additionally subreddits such as r/CryptoCurrency and r/Bitcoin are pivotal in gathering collective investor sentiment, such as threads discussing new ICOs or tokens may serve as early indicators of market interest or skepticism [114,115,116,117].

Based on the extracted, relevant data from these essential social media data sources, researchers can use natural language processing, or sentiment analysis tools to analyse the sentiment expressed in these posts and comments, quantify it, and correlate it with price movements in the cryptocurrency market [114].

Limitations of this parameter include the presence of noisy, irrelevant, or sarcastic and biased opinions which can affect the true expression of public sentiment and cause inaccuracies in the data. Furthermore, the sentiment expressed on these platforms can be extremely volatile, reacting rapidly to market changes or news, thus requiring sophisticated filtering techniques to distinguish meaningful signals from mere noise [128].

References supporting the inclusion of Reddit along with Twitter for sentiment analysis in cryptocurrency contexts have shown that both platforms significantly influence and reflect cryptocurrency market dynamics. Studies such as by Kim et al. [115] and Serafini et al. [26] have highlighted the predictive power of combined social media data from these platforms in understanding and forecasting cryptocurrency volatility and price changes.

- Methodological Considerations for Social Media Sentiment Data:

Recent changes in data access policies on major social media platforms have significant implications for sentiment analysis, particularly with respect to cryptocurrency price prediction. Historically, Twitter has been a primary source for real-time public sentiment data (as is evident in the literature), widely used due to the accessibility of its API. However, under the new ownership of Elon Musk, Twitter has introduced substantial restrictions on API access, limiting the amount and type of data that can be freely extracted by researchers and developers. These restrictions not only reduce the volume of data available but also potentially increase the costs associated with accessing detailed data necessary for robust sentiment analysis [129,130].

In contrast, Reddit continues to offer relatively open access to its data, making it an increasingly valuable resource for researchers analysing the impact of community-driven discussions on cryptocurrency markets. Reddit’s API provides extensive access to historical and real-time posts across numerous cryptocurrency focused communities, where diverse viewpoints and market reactions are prominently shared and discussed [131,132].

Given these developments, it is advisable for researchers to consider the implications of these changes in their methodology sections, and potentially to pivot towards more accessible platforms like Reddit for conducting sentiment analysis. This shift might also necessitate a revaluation of the tools and approaches used to collect and analyse social media data, ensuring that research remains feasible and relevant under the evolving data access landscape [133].

3.5. Summary of Influential Parameters Used

Overall, in the majority of recent relevant studies, the main influential parameters used for price prediction of cryptocurrencies include previous price and volume, technical indicators, blockchain features, and social media sentiment (notably from Twitter and Reddit). Table 3 summarises the benefits and challenges of using each of these parameters as identified in the reviewed papers. Additionally, recent advances in deep learning, such as Transformers–introduced in the paper “Attention is All You Need” by Vaswani et al. [134] in 2017–have shown promise in capturing complex dependencies [19]. While not yet widely documented in the existing cryptocurrency prediction literature, the application of Transformers could potentially enhance feature extraction from time-series data, suggesting a promising avenue for future research. Determining the best selection of these parameters, as variables for cryptocurrency price prediction and applying the most appropriate methodologies, should therefore be given careful attention in this area of research.

Table 3.

Data sources considered in the reviewed literature.

4. Recent Methodologies Employed

This section discusses the various state-of-the-art machine learning, deep learning and hybrid (also called ensemble) deep learning methods employed and proposed in studies focused on cryptocurrency price prediction, as shown in Table 1. Many researchers have implemented these methodologies for forecasting cryptocurrency prices and have achieved impressive results for both long- and short-term data, as detailed in the following subsections.

4.1. Machine Learning Based Prediction

Machine learning algorithms are quite beneficial to use in prediction analyses as they easily identify trends and patterns, however, they are subject to overfitting and underfitting data, leading to a poor generalisation to other data. Maden et al. (2015) [40] developed a custom algorithm utilising random forests, SVMs, and generalised linear models to predict the directional changes in Bitcoin prices over daily and 10-minute intervals. Using closing price data as well as 16 features of the Bitcoin blockchain, the algorithm was able to predict the sign of the price change with an accuracy of 98.7% for the daily time interval, and a 50–55% accuracy for the 10 min time interval for the binomial generalised linear model (GLM), indicating that this model is slightly better than random probability for shorter time frames [40]. In 2015, Colianni et al. employed Naïve Bayes, logistic regression, and SVM’s to analyse Social Media data for hourly Bitcoin price predictions [21]. Bernoulli Naïve Bayes achieved the highest accuracy among text classification algorithms, recording an hourly prediction accuracy of 76.23% [21]. Chen et al. implemented both machine learning-based algorithms, such as linear regression, Naïve Bayes, SVM’s, random forests, ARIMA; and deep learning-based models including RNN and neural networks, to predict the price changes in Ethereum [43]. The best result was achieved by using ARIMA, which yielded a 61.17% accuracy for price prediction [43].

Similar to [21], later in [42], Lamon et al. also utilised Naïve Bayes, logistic regression, and SVM’s to predict the prices of Bitcoin, Ethereum, and Litecoin by considering semantic content from social media platforms and news media. Then Velankar et al. considered the daily price of Bitcoin to predict its future prices by applying more normalisation techniques on the dataset [44]. Forecasting was performed by implementing the machine learning methods random forest and Bayesian models by considering five features which consisted of block size, total volume, daily high and low prices, number of transactions, and trading volume. Further, in [24], 5 regression algorithms and 11 classification algorithms are used for the price prediction of Bitcoin by using previous price changes and social media sentiment as input features. Naïve Bayes algorithm and random forest classification was found as the two methods with the best accuracy by implementing the net sentiment score with accuracies of 89.65% and 85.78% respectively [24].

In [26], the authors also made use of social media sentiment using the lexicon-based sentiment analysis tool VADER (for Valence Aware Dictionary for sEntiment Reasoning) as described by [135]. Two models used for Bitcoin time-series predictions were compared, namely ARIMAX and LSTM-RNN, by using previous Bitcoin price and sentiment as the only two input features. Results show that ARIMAX outperformed the LSTM-RNN by achieving a lower mean square error (MSE), demonstrating that a more complex model is not always the best method to use for price prediction [26]. In [22], Kilimci makes use of social media sentiment in deep learning and word embedding models for estimating the direction of Bitcoin price. The results show that the use of the FastText model (a word embedding model) outperforms all other models with an accuracy of 89.13% to predict the direction of Bitcoin price.

4.2. Deep Learning Based Prediction

In addition to machine learning algorithms, there are also various existing works on deep learning-based forecasting models. Deep learning approaches are profoundly accurate when compared to classical machine learning models, due to their superior ability to identify complex patterns which is highly beneficial in prediction analyses [136]. The use of architectures such as RNNs, LSTMs, and CNNs has been prevalent, as these models are capable of learning from extensive historical data and capturing non-linear relationships in price movements.

Tan et al. conducts a comparative study of various methods in their ability to predict the price of Bitcoin [41]. By using the daily open, close, high and low prices and daily volume, the LSTM model was shown to have a significantly higher accuracy in predicting the closing price of Bitcoin with a root-mean-square error (RMSE) of 33.7091, followed by SVM, ARIMA and Bayesian regression with RMSE’s of 288.0618, 439.98 and 461.9379 respectively. Another comparative study was also conducted by Ji et al. [39] in which they compared various state-of-the-art deep learning methods: DNN; deep neural rejection (DNR); LSTM; CNN; and various combinations of these for Bitcoin price prediction [39]. Using daily, closing Bitcoin prices as well as a total of 29 features of the Bitcoin blockchain, the paper concluded that, for regression problems, LSTM slightly outperformed the other models, whereas for classification problems, DNN slightly outperformed the other models [39].

The LSTM network, and its variant, are used in [45] where the possible applicability in the prediction of various cryptocurrencies is reported. Tandon et al. [46] also utilised the LSTM model along with the 10-fold cross-validation for predicting the daily prices of Bitcoin [46]. Compared to machine learning and regression methods, the results showed a significantly lower mean absolute error (MAE) with a value of 0.0043 s [46]. In [33], Aggarwal et al. considered various Bitcoin and social factors for Bitcoin price prediction purposes. A comparative study of various deep learning models was conducted, and it was concluded that LSTM showed the best result among those considered.

Albariqi et al. proposes a multilayer perceptron (MLP) and the recurrent neural network-based scheme to predict the price of Bitcoin price for short and long time windows, 2–60 days [119]. By using data from Bitcoin’s blockchain, it was shown that the MLP outperformed RNN, displaying the greatest accuracy, precision and recall for both scenarios. More recently, in 2021, Buzcu et al. [103] combines both sentiment analysis—calculated by FinBERT (a state-of-the-art financial sentiment analysis model) and LSTM (given its robustness when it comes to text classification)—and technical analysis, specifically the moving average convergence/divergence (MACD) indicator, and only places buy or sell orders if these two entities both agree on a bull or bear market [103]. The proposed model achieves a 34.02% return on investment (ROI) which outperforms simply buying and holding Bitcoin, which has a 28.25% ROI, beating the market by 5.77% over a 2-month period [103]. The authors suggest that the results indicate that by combining both qualitative (textual and sentimental data) and quantitative (technical indicators) data, it may be a master strategy that is able to beat the market [103]—however, this work was conducted during a bull market and only one technical indicator was used. Belcastro et al. [99] propose a methodology for enhancing cryptocurrency price forecasting by integrating machine learning with social media and market data. Their approach combines statistical, text analytics, and deep learning techniques to create a trading recommendation algorithm that analyzes the correlation between social media activity and price fluctuations. The methodology demonstrates significant profitability, especially with influential meme coins, achieving an average gain of 194% without transaction fees and 117% with fees, showcasing the effectiveness of their integrated approach [99].

In later studies, Shamshad et al. [82] propose a Predictive Analytics System employing a combination multiple advanced machine learning and deep learning algorithms including ARIMA, SVM, and various LSTM configurations, to predict the price of a variety cryptocurrencies over a ten-day period. Their empirical results indicate that ARIMA outperforms other models in accuracy, providing a reliable method for market analysts to forecast cryptocurrency prices with confidence [82]. Kumar et al. [85] explore the application of a LSTM-based Recurrent Neural Network to predict Bitcoin prices. Using a historical dataset, their approach involves intensive model training and optimisation, concluding that LSTM networks, through detailed analysis of past price data, can accurately forecast future Bitcoin prices, offering a viable tool for trading strategies [85]. Mahfooz et al. [93] combine LSTM and Facebook Prophet models with external economic indicators such as interest rates and recession probabilities to forecast Bitcoin prices. The study demonstrates that integrating these exogenous variables significantly improves predictive accuracy, offering a sophisticated model for financial analysts and investors focusing on cryptocurrency [93].

Building on the success of these existing deep learning models, the introduction of Transformers may represent the next evolution in predictive models. Known for their groundbreaking performance in various domains, particularly natural language processing [134], Transformers offer promising prospects for cryptocurrency price prediction. Unlike traditional RNNs or even their evolved form, LSTMs, which process data sequentially, Transformers can handle multiple data points of a time series in parallel. This ability significantly enhances computational efficiency and model responsiveness, crucial for adapting to the volatile cryptocurrency market. Recent studies leveraging Transformers in cryptocurrency predictions illustrate their potential, such as in Singh and Bhat [137], who explore a transformer-based neural network for Ethereum price forecasting, highlighting its superiority in handling cross-currency correlations and market sentiment analysis. Penmetsa et al. [138] demonstrate how multi-headed self-attention mechanisms can enhance the prediction accuracy for cryptocurrencies like Bitcoin and Ethereum. Sridhar et al. [139] employ a multi-feature Transformer model to predict price fluctuations by integrating various market indicators, showing a significant improvement over traditional models. Liu [66] discusses the application of Transformers to predict Bitcoin prices using time-series data, emphasising their ability to capture complex patterns that escape other predictive models. Herremans and Martens [61] present a comparative study of Transformers against standard deep learning models, validating the former’s enhanced performance in cryptocurrency markets. As the field progresses, integrating Transformers with existing models could create systems that combine the strengths of both architectures, offering unprecedented predictive power and robustness in the face of market unpredictability, potentially setting new benchmarks for accuracy in cryptocurrency price prediction.

4.3. Hybrid Deep Learning Based Prediction

Since 2020, various hybrid (or ensemble) models have been proposed through the integration of several forecasting models to overcome the weaknesses of a single prediction model, which makes them extremley useful and beneficial in prediction analyses [3]—however, these methods are often highly complex and difficult to refine. In [102], Kelotra et al. proposes the Rider-monarch butterfly optimisation (MBO) based deep convolutional long short-term memory networks as a prediction system. Using 12 technical indicators as input features, the prediction performance of the MBO-ConvLSTM, upon visual inspection, appears to correspond with the actual price values to a reasonable significance. The proposed method produces the minimum MSE of 7.2487 and RMSE of 2.6923 [102]. Later, Kilimci et al. conducts a comparative study on various deep learning and hybrid deep learning models by using various previous pricing data and technical indicators for a total of 19 input features for each model [37]. The performance order of all models considered are concluded as: ConvLSTM, LSTM, CNN, CNN-LSTM, with mean absolute percentage error’s (MAPE’s) of 2.4076, 3.6479, 4.9474, 7.3124 respectively. The prediction performance of the best proposed model, ConvLSTM, upon visual inspection, corresponds with the actual values of the Bitcoin price to a very high degree for the test set time period (along with its impressive error statistics) [37].

In their study, Ali et al. [83] investigate the utility of an ensemble model combining CNN and GRU architectures to enhance the forecasting accuracy of cryptocurrency prices, especially in a high-volatility environment. Trained on a dataset spanning from 2015 to 2023, their model undergoes extensive hyperparameter tuning and validation, showing that the integration of CNN and GRU not only effectively captures the spatial-temporal dynamics but also achieves high predictive accuracy, making it a valuable tool for investors and analysts [83]. Sabeena et al. [111] present a comprehensive model integrating ARIMA with CNNs, using sentiment analysis and blockchain data to enhance cryptocurrency market predictions. This hybrid model combines real-time data integration and robust hyperparameter optimisation, resulting in a model that outperforms traditional methods, offering a nuanced approach to capturing market dynamics [111]. Guo et al. also proposes a novel approach which combines multi-scale residual convolutional (MRC) neural network and a long short-term memory network, called MRC-LSTM, to acquire effective features to learn trends and interaction of time series, for the price prediction of Bitcoin [38]. By using daily closing price of Bitcoin and 10 types of internal (Bitcoin trading data) and external (macroeconomic variables and investor attention) information that have an impact on the price of Bitcoin, it is concluded that MRC-LSTM significantly outperforms a variety of network structures [38]. Peng et al. [98] propose an innovative Attention-based CNN–LSTM model (ACLMC) to enhance high-frequency cryptocurrency trend prediction by combining data from different frequencies and multiple cryptocurrencies. Their model addresses the volatility issue in cryptocurrency markets by employing a stable triple trend labeling method, significantly reducing the number of trades compared to traditional methods. Through extensive experiments, they demonstrate that the ACLMC model improves financial metrics, showcasing better performance than several baseline models, and supports simultaneous multi-currency trading, thereby optimizing financial indicators and reducing investment risk [98]. Ladhari and Boubaker [97] explore Bitcoin price prediction using a novel hybrid deep learning approach that integrates Long Short-Term Memory (LSTM) networks with attention mechanisms, enhanced by gradient-specific optimization. This methodology leverages a comprehensive dataset of hourly Bitcoin prices from 2018 to 2024, aiming to improve prediction accuracy by focusing on significant data features and fine-tuning the learning process through gradient adjustments. Their findings demonstrate that this approach surpasses traditional models, providing a robust tool for analyzing the volatile cryptocurrency market [97].

In [3], Patel et al. proposed a LSTM and GRU based hybrid model to predict the prices of the two cryptocurrencies, Litecoin and Monero. Results show that the proposed scheme accurately predicts future prices with reasonable accuracy and outperforms LSTM for all prediction windows - 1-day, 3-day and 7-day [3]. In a similar study a year later, the previously proposed LSTM-GRU based hybrid model is now used by the same authors for the prediction of Litecoin and Zcash [4]. By focusing on the interrelationships of Litecoin and Zcash, the proposed model outperformed the state-of-the-art techniques, including the classical LSTM and GRU model, for the window sizes of 1-day, 3-days, 7-days, and 30-days, with impressive error statistics. Ramesh et al. [94] on the other hand, propose a Hybrid Oppositional Sparrow Search of Gravitational Search Algorithm (HOSS-GSA) for cryptocurrency price prediction. Their approach uses Resilient Stochastic Clustering to identify relevant features and reduce dimensionality, enhancing prediction accuracy. The study’s findings suggest that HOSS-GSA optimises model parameters effectively, providing a valuable tool for traders and analysts in a rapidly evolving cryptocurrency market [94]. In addition to the LSTM-GRU based model previously proposed, Politis et al. proposes an ensemble model of LSTM, GRU, and a temporal convolutional network (TSN) to to forecast the price of cryptocurrencies and apply it to the prediction of Ether, based on its historical price data [31]. Short- and long-term (1-day and 1-week) forecasts achieve accuracies of 84.2% and 78.9% respectively [31]. In a similar manner, Kim et al. proposed a LSTM and GRU system in order to predict the daily price changes of Bitcoin, Ethereum and Litecoin, based on historical price data [47].

4.4. Open-Source Contributions in Cryptocurrency Price Prediction Research

In addition to reviewing the methodologies and focus areas of cryptocurrency price prediction, the significance of open-source resources in advancing this field is recognised. The availability of code and datasets not only enables the verification and reproducibility of research findings but also encourages collaboration and innovation within the academic community. Table 4 has been included to highlight studies that generously made their code and datasets freely available, thereby contributing to the collective knowledge base.

Table 4.

Sample studies with freely available code and datasets.

Table 4 underscores the contributions these works make to the field of cryptocurrency price prediction and highlights the essence of open science. The act of sharing code and data facilitates the advancement of this domain, providing valuable assets for further investigation and innovation of predictive models. However, the apparent scarcity of open-source code and datasets in the literature, significantly impedes the ability of the scientific community to conduct replication and validation. Addressing this, by making more resources available, would not only enable a more comprehensive evaluation of predictive models but could also facilitate rapid progress within this domain.

4.5. Comparative Summary of Methodological Aspects

This subsection aims to provide a comparative analysis of various methodological aspects across the studies reviewed in Section 4. By examining performance evaluation indicators, programming languages, validation approaches, and other pertinent dimensions, we seek to offer a comprehensive overview that underscores the effectiveness and practicality of the different methodologies employed in cryptocurrency price prediction.

The studies reviewed exhibit a diverse array of performance evaluation indicators. Common metrics include accuracy, root mean square error (RMSE), mean absolute error (MAE), mean square error (MSE), mean absolute percent error, and precision. Python is the predominant programming language used, particularly for deep learning models, owing to its rich ecosystem of libraries such as TensorFlow and PyTorch. In contrast, R and MATLAB are more frequently utilised for novel statistical models.

To summarise the state-of-the-art methodologies employed to forecast the price of various cryptocurrencies, Table 5 lists the benefits and challenges of using each of these methodologies. Based on the analysis of the relevant papers, the various hybrid methods, employed and proposed, have shown to outperform prevailing machine and deep learning models with a high success rate, highlighting that hybrid deep learning models are the most appropriate and accurate models to use for cryptocurrency price prediction.

Table 5.

Methodologies considered in the reviewed literature.

5. Discussion

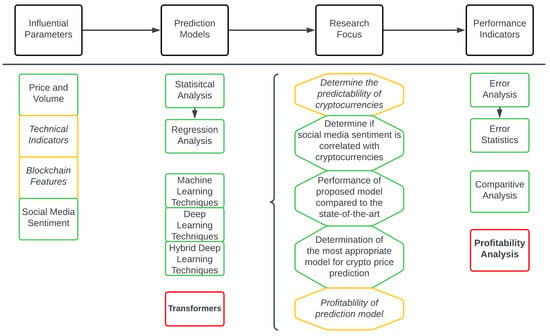

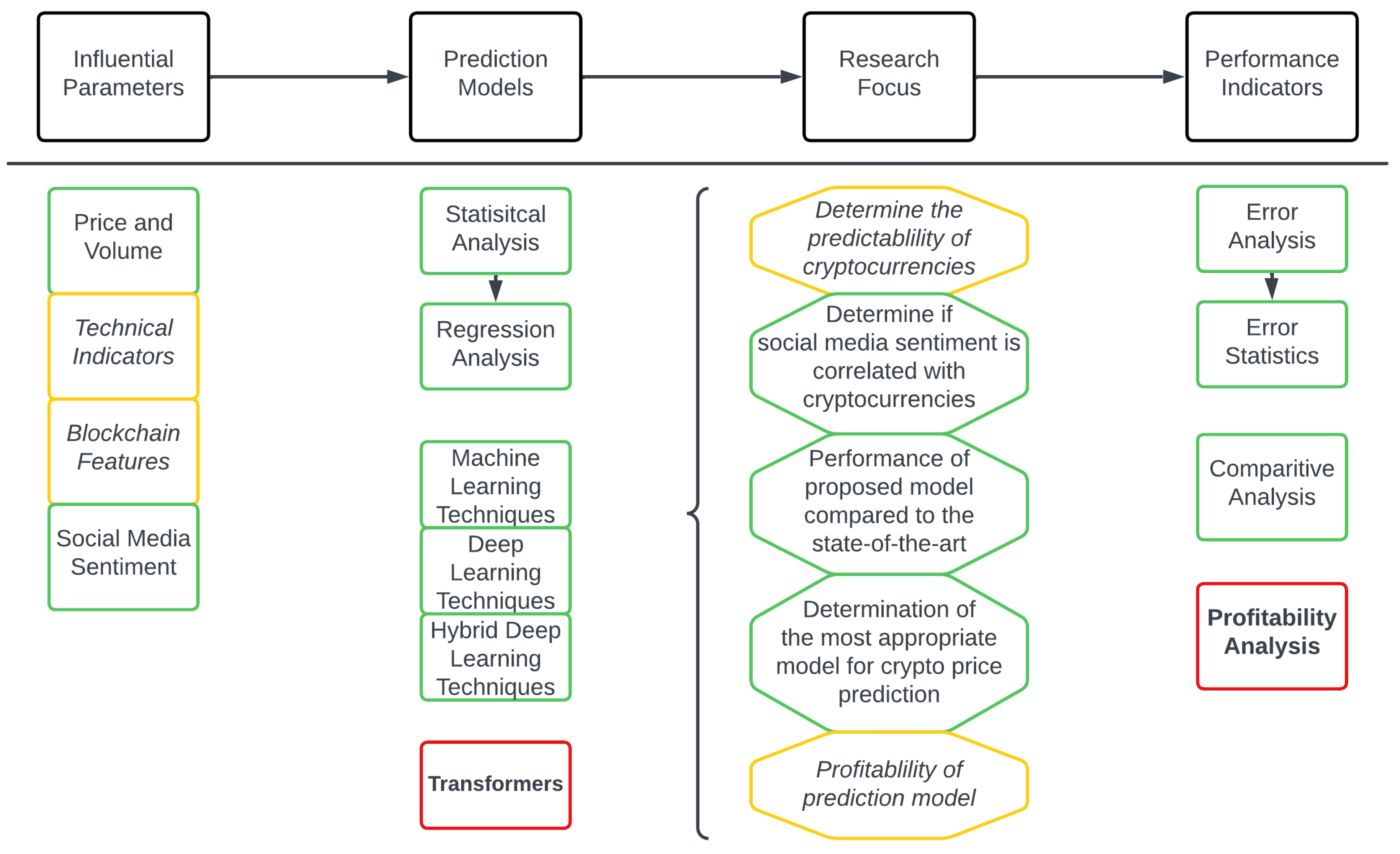

A compilation of insights derived from the review of the relevant literature in the domain of cryptocurrency price prediction is shown in Figure 8, which presents a conceptual framework to inform future research on this topic. The framework describes the influential parameters used in cryptocurrency price prediction, what models and methodologies are used in the research focuses, and the measures of performance employed. Based on the insights gained from this review, the elements of this framework were classified as follows: well-addressed (shown in green with regular font in Figure 8), requires more attention (orange and italics) and under-researched (red and bold), This framework therefore provides a visual representation of research gaps that have emerged from this review.

Figure 8.

Conceptual framework for research in cryptocurrency prediction.

5.1. Influential Parameters

Current research has underscored the significance of identifying parameters influencing cryptocurrency prices, with prevalent focus on the previous price, volume, and social media sentiment, particularly from platforms like Twitter and Reddit. The majority of the literature has mainly used the previous price as well as (in some cases) volume to predict future prices. The recurrent use of these parameters in prediction models suggests their importance. However, it is essential to acknowledge the potential limitations. The reliance on historical data assumes that past trends will repeat, overlooking potential market shifts. Moreover, the accuracy of historical price data and its ability to capture unforeseen events pose challenges.

Additionally, the attention drawn to social media sentiment is unsurprising, considering the considerable influence wielded by prominent figures, including Elon Musk. The documented impact of sentiment on cryptocurrency prices in various studies further underscores its significance in shaping market dynamics and their perceived importance in the development of predictive models. However, while social media sentiment provides valuable insights into market sentiment, its reliability and robustness must be critically examined. The recent excitement on social media around cryptocurrencies like Dogecoin, spurred by influential figures, raises concerns about the susceptibility of sentiment analysis to external influences. Potential biases and noise introduced through social media platforms pose challenges for robust prediction models.

Other parameters which were mildly addressed, but still require more attention, were technical indicators and blockchain features. This is surprising as the prevailing method used by day traders to predict future prices is technical analysis. Technical analysis, often relying on these technical indicators which have been shown to have the ability to influence price [37,48,49,63,91,102,103,104,105,106,107,108], is susceptible to subjective interpretation and can be influenced by market sentiment, leading to potential limitations in the use of this parameter.

Additionally, Blockchain features, though acknowledged for their unique influence on the cryptocurrency market, have been surprisingly under-addressed in the existing literature [32,39,40,44,84,106,111,119]. This oversight hinders a comprehensive understanding of their impact and introduces challenges in building accurate predictive models. One notable limitation lies in the variability of blockchain implementations across different cryptocurrencies, each with its own set of features and protocols. The lack of standardised metrics and uniformity complicates the analysis, making it challenging to derive generalised conclusions. Additionally, the reliability of data sources providing information on blockchain features becomes a critical concern. Inconsistencies in reporting transaction speeds, security measures, and consensus mechanisms may introduce noise into the predictive models, diminishing their accuracy. Furthermore, the dynamic nature of blockchain technologies, with frequent updates and forks, poses a challenge in maintaining up-to-date and relevant data.

5.2. Prediction Models

In the rapidly evolving field of cryptocurrency price prediction, researchers have leveraged a wide spectrum of models, from fundamental statistical analyses to sophisticated machine learning and deep learning algorithms. Early approaches often relied on methods like Granger causality and regression analyses, which provided initial insights into the understanding of the influence parameters affecting market trends. These statistical methods played a crucial role in laying the groundwork for more complex models, elucidating how various factors drive cryptocurrency prices.

While these statistical methods have been fundamental in understanding the influence of various parameters on cryptocurrency prices, as the field progressed, more advanced techniques began to dominate the research landscape. Prevailing methods in recent literature include complex forecasting models using machine and deep learning algorithms like Naïve Bayes, random forests, SVM as well as LSTM, CNN, GRU and RNN. These models, capable of learning from extensive historical data, significantly outperformed simpler statistical methods by capturing non-linear relationships within the data effectively.

In more recent years, the landscape of predictive models for financial markets, particularly in cryptocurrency price prediction, has shifted significantly towards even more robust methodologies. Until approximately 2019/2020, LSTM networks dominated this domain (see Table 1) due to their capacity to process not only individual data points but entire sequences of data, learning long-term dependencies crucial for accurate forecasting. The advent of hybrid deep learning models around 2020 marked a pivotal evolution in predictive technologies. State-of-the-art hybrid models like ConvLSTM, LSTM-GRU and MRC-LSTM emerged, combining the strengths of multiple deep learning approaches to enhance prediction accuracy. These hybrid models are well-documented in contemporary literature and have consistently demonstrated superior performance compared to traditional single-model approaches, particularly in handling the complex dynamics of cryptocurrency markets.

These hybrid methods have not only been compared to but also frequently outperformed LSTM networks in terms of accuracy and error statistics. This progression highlights a significant trend in the field: researchers are increasingly moving towards models that merge multiple deep learning techniques to achieve the highest prediction accuracies. For those seeking to advance the frontier of cryptocurrency price prediction, developing new hybrid models or optimising existing configurations, such as ConvLSTM, LSTM-GRU, and MRC-LSTM, represents a promising research direction.

The progression of deep learning in cryptocurrency prediction is also marked by the adoption of Transformers, which could represent the next step in enhancing cryptocurrency price prediction methodologies. Known for their groundbreaking performance in various domains, particularly natural language processing, Transformers offer promising prospects for handling time-series data for cryptocurrency markets. Unlike traditional RNNs or even their evolved form, LSTMs, which process data sequentially, Transformers can handle multiple data points of a time series in parallel. This ability significantly enhances computational efficiency and model responsiveness, crucial for adapting to the volatile cryptocurrency market. Additionally, the self-attention mechanism of Transformers allows them to assess the importance of different points within the time series dynamically, thereby potentially improving the accuracy and reliability of predictions. This model could address some of the intrinsic challenges faced by models or hybrid models which integrate RNNs and LSTMs, such as long dependency lags and sensitivity to input size variations.

The potential integration of Transformers with existing hybrid models suggests a promising research trajectory. This could lead to systems that offer unprecedented predictive power and robustness in the face of market unpredictability. Such advancements not only promise to refine prediction accuracy but also offer adaptability to real-world trading conditions, a crucial aspect that merits empirical validation. Additionally, making these models and datasets publicly available. In addition, it is recommended that researchers make these advanced models and their datasets publicly available (as many in the literature are not, see Table 4) to foster comprehensive evaluations and expedite advancements in the field.

A rigorous examination of these advanced models in real-world trading scenarios is imperative. While the literature frequently cites accuracy rates and error statistics, it often overlooks the performance of these models under actual market conditions. Bridging this gap is essential for understanding their practical utility in profit-driven scenarios. Making these models and datasets publicly accessible would considerably aid in this endeavour, allowing for a more thorough evaluation and potentially accelerating field advancements.

Evaluation of Model Accuracy and Reliability

A critical assessment of the accuracy and reliability of prediction models is essential to understanding their effectiveness in cryptocurrency price prediction. To facilitate this, a selection of highly cited papers has been organised in Table 6, to provide a comprehensive overview of key works in this domain. Table 6 summarises the methodologies and performance metrics of these key studies, serving as a concise reference for seminal contributions within the field.

Table 6.

Comparative analysis of prediction model performance metrics of selected key works in cryptocurrency price prediction.

Based on the comprehensive comparison of various prediction models presented in Table 6, it is evident that the field of cryptocurrency price prediction has evolved significantly, embracing diverse machine learning approaches and performance metrics. For instance, the early use of Bayesian Regression by Shah in 2014, focusing on historical price and volume, demonstrated a promising investment doubling in less than 60 days. This early success highlighted the potential of machine learning in cryptocurrency predictions. However, the evolution towards the more complex, deep learning models, indicates a shift towards more sophisticated approaches, due to the growth and advancement of machine learning platforms

Notably, LSTM models and its variants (in particular hybrid models such as LSTM-GRU) have gained prominence. The performance metrics, particularly RMSE and MAE, suggest these models achieve a fine balance between accuracy and computational efficiency. However, traditional performance metrics such as RMSE, MAPE, MSE, and MAE, while indicative of predictive power, don’t always reflect profitability or reliability in real-world trading, necessitating further investigation.

The reliability of a model extends beyond statistical accuracy to include performance stability under volatile market conditions and adaptability to new data. Even robust models like LSTM and its variants may falter during periods of high market volatility or unexpected events, which is a significant limitation. It is this understanding of each model’s performance in the face of real-world financial complexities, that will ultimately guide the development of more resilient and profitable trading strategies, taking into consideration a variety of influential parameters and performance metrics.

5.3. Research Focus

In this review, it has been shown that there are a variety of research focuses that have been considered in the literature. Most prevalent among these include focusing on: whether social media sentiment is correlated with cryptocurrency prices; the performance of a proposed model compared to state-of-the-art methods; and to determine the most appropriate (or accurate) model to use, among a certain selection, for cryptocurrency price prediction. All of these have been well-addressed in the literature, most of which with corroborating results across the various works.

Research requiring more attention should focus on the predictability of cryptocurrencies and profitability of the prediction models utilised. Given that cryptocurrency price prediction models aim to accurately predict future prices, it is a noticeable gap in the literature that the predictability of cryptocurrencies and in turn profitability of the models used is not as widely considered as determining the best prediction model and its accuracy.

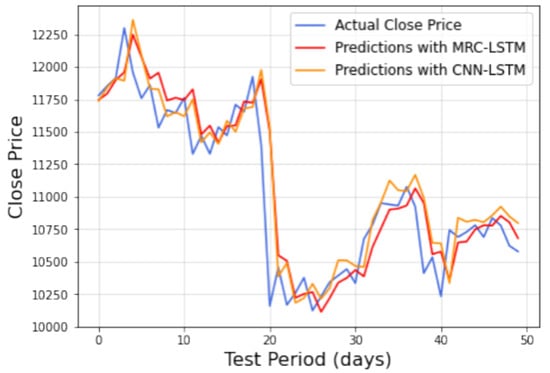

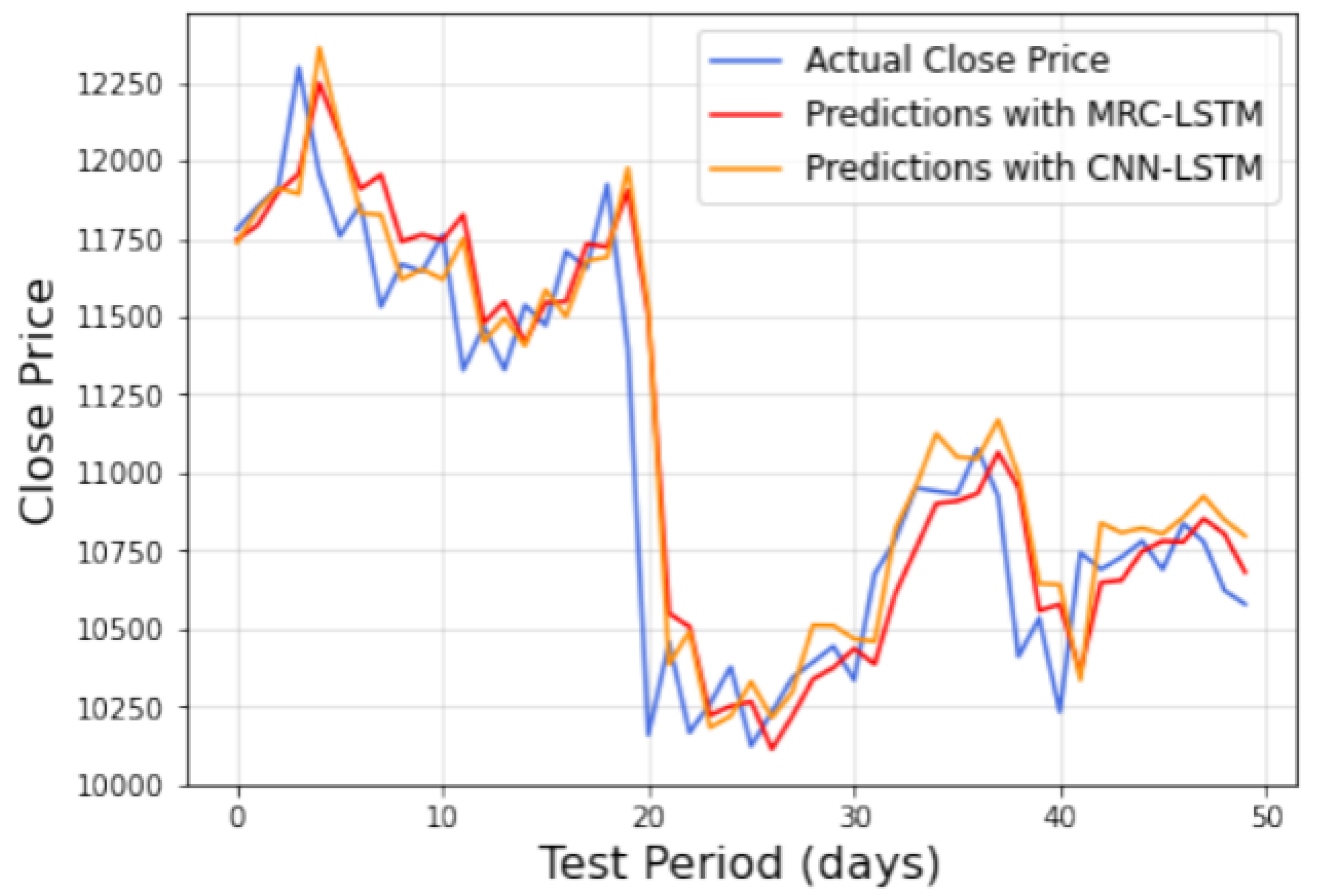

To further explain why predictability and in turn profitability have been under-addressed, it is noted that the price prediction models presented have an element of lag in their results, which causes ambiguity in their actual performance compared to the presented accuracy values when applied to real time transactions. While the results presented have been shown to be quite accurate with respectable values for their performance indicators (such as MAE, MSE, RMSE, MAPE and coefficient of determination () values), the ability for these models to be profitable for an investor can be questioned. For example, visual inspection of the results for predicting the daily closing price of Bitcoin against the actual values, shown in Figure 9 [38], demonstrate impressive statistical accuracy of this approach. However, the prediction period used is five days, which means the closing price of Bitcoin on the sixth day is predicted using the characteristic parameter data from the previous five days. This means at day ‘t’, the prediction value for only day is calculated (based on information from ). Further analysing Figure 9, it can be seen that at any day ‘t’ on the ‘actual close price’ (blue) curve, only one data point (day) ahead on the prediction model curves (red and orange) curves can be seen, which determines whether to place an order. Placing a buy or sell order for Bitcoin on day ‘t’, based on what is predicted for day , whether it is higher or lower than the price on day t, will not yield a positive result as often as implied by the high accuracy rates and impressive error statistics reported. Just simply looking at the actual close price at any time ‘t’ on the graph and then comparing whether the predicted value and actual value for are both higher or lower than the price on day t, can easily show how this prediction model can be considered reasonably accurate, but not profitable.

Figure 9.

Prediction results compared with actual closing prices [38].

Current state-of-the-art methodologies often showcase impressive accuracy rates and error statistics, yet there is a critical gap in evaluating the reliability and profitability of these models in real-world trading scenarios. The prevalent lag in model results introduces ambiguity in assessing the actual performance of models when applied to live transactions, questioning their profitability for investors [4,37,38]. The inherent lag in the results indicate a delay in the model’s response to market changes and can therefore diminishes the models profitability in real-time trading scenarios.

A critical analysis of the models’ ability to yield positive results for investors is essential for advancing the field beyond accuracy metrics and error statistics. This nuanced understanding is crucial for researchers and practitioners aiming to bridge the gap between accurate predictions and profitable trading strategies in the dynamic cryptocurrency market and emphasises why determining the predictability of cryptocurrencies and profitability of the prediction models require more attention in the literature.

5.4. Performance Indicators

In order to assess the performance or accuracy of proposed prediction models various performance indicators have been considered. Most works employ error analysis by referring to commonly used error statistics, such as MAPE, MAD, MSE, RMSE, among others, to assess performance. These are well-addressed in the literature as they give a quantitative determination of the accuracy presented by the models considered in the literature. Another performance indicator widely addressed is the comparison of various models, or comparison of proposed models with the state-of-the-art methods. These give a strong indication of an accuracy hierarchy of various models, and which of these should and should not be considered for price prediction analysis.

An under-researched performance indication was found to be the inclusion of a simple profitability analysis. Given the main goal of a cryptocurrency price prediction model is to accurately predict future prices to inform investor decisions, it is surprising to see that profitability analysis is not widely considered in literature; however, given that determining the predictability of cryptocurrencies and profitability of the prediction models utilised were research focuses found to require more attention, this can be expected. The lack of scarcity of profitability analyses is most likely since the focus of most studies has been academic in nature and not from an investor’s or trader’s standpoint in attempting to turn a profit—hence they typically consider the accuracy of the prediction model and not the predictability or profitability per se.

6. Future Directions in Cryptocurrency Price Prediction