White Noise and Its Misapplications: Impacts on Time Series Model Adequacy and Forecasting

,

,  , , and

, , and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Theoretical Background

2.1. Definitions

2.1.1. Mean

2.1.2. Autocovariance Function

2.1.3. Autocorrelation Function (ACF)

2.1.4. Sample Mean

2.1.5. Sample Autocovariance

2.1.6. Sample Autocorrelation

2.1.7. Spectral Density Function

2.2. Bartlett’s Formula

2.3. Variance of and MA(q) Model Identification

- (a) IID Noise: If the process consists of independent and identically distributed (iid) noise such that for all h:then the variance of the sample autocorrelation function (ACF) simplifies to

- (b) Moving Average Process MA(q): Consider the MA(q) process defined byFor this process, the autocorrelation coefficients vanish beyond lag q:Consequently, the variance of the sample ACF for is given by

- (c) Asymptotic Distribution: Asymptotically, the distribution of is approximately normal, with the mean and variance as derived above. For reliable estimation, Box and Jenkins recommend

- Examination of the Sample ACF for Model Identification:

- –

- (i) If for all , the process can be modeled as MA(0) (a white noise sequence).

- –

- (ii) If , compare subsequent values of with the critical value:However, since is unknown, two alternatives arise:

- Replace with its estimate , and check ifIf true, assume an MA(1) model.

- Alternatively, for large n, approximate the termCheck ifIf true, assume an MA(1) model.

- –

- (iii) More generally, if and for all , then assume an MA(q) model with .

- –

- Since positive terms are discarded in the variance calculation, if is approximately , it should be considered within the confidence interval.

2.4. Reevaluating White Noise Theoretical Assumptions

3. Validating Theory in Practice: A Critical Examination

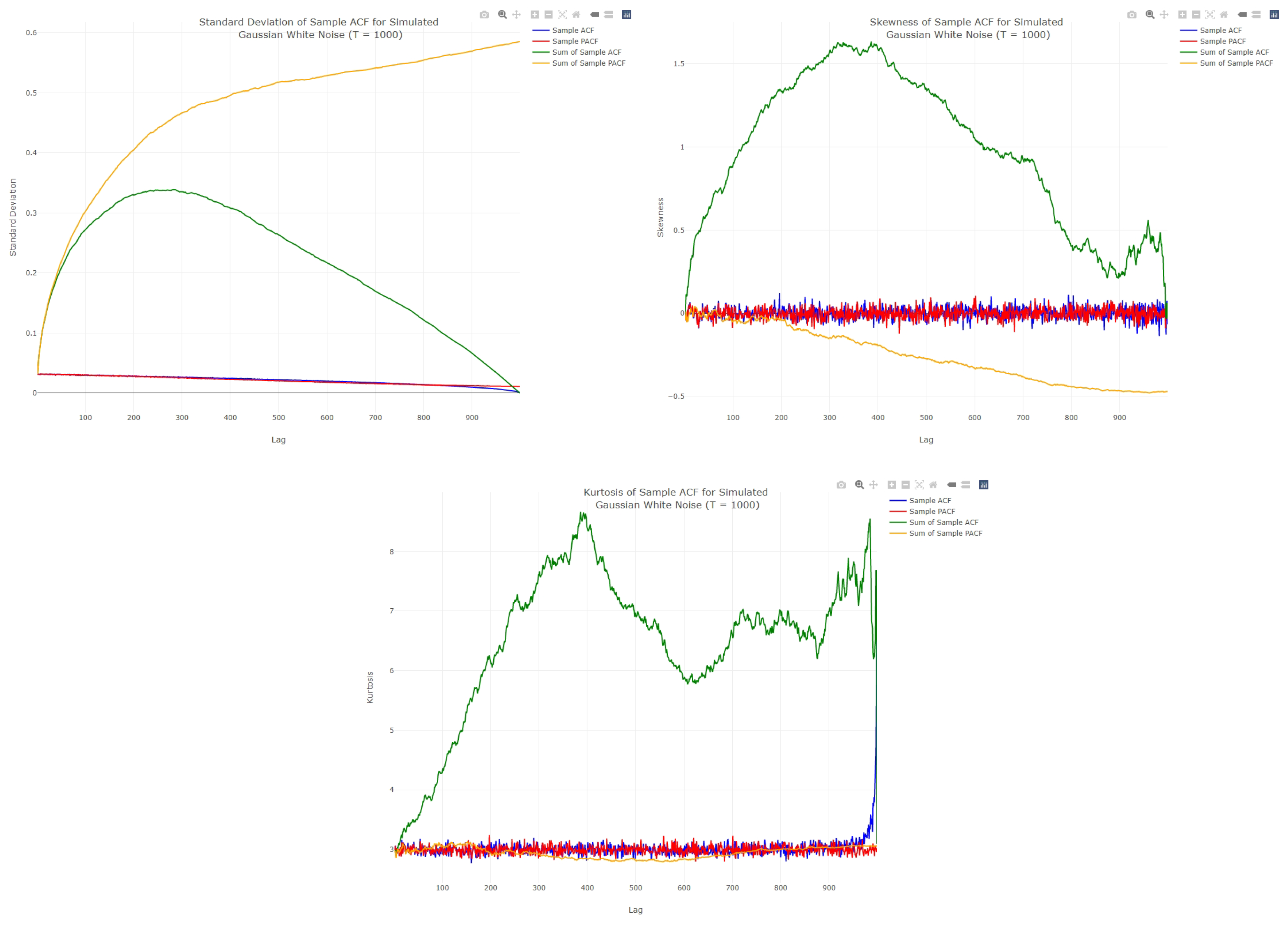

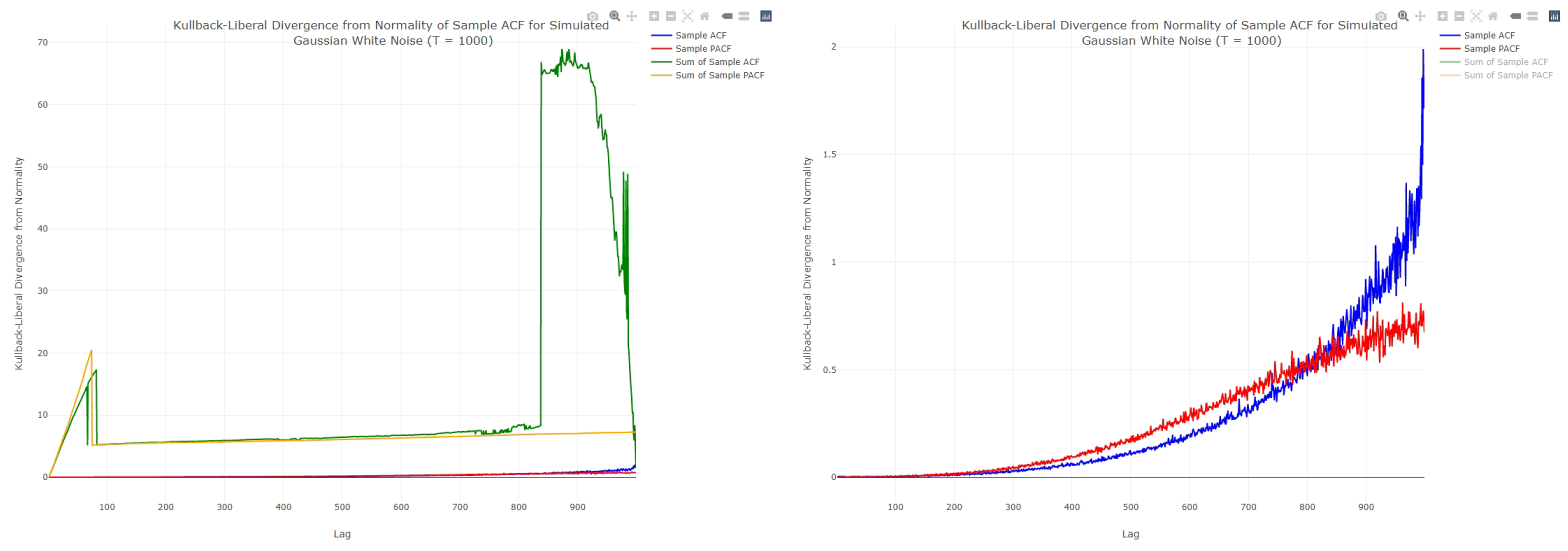

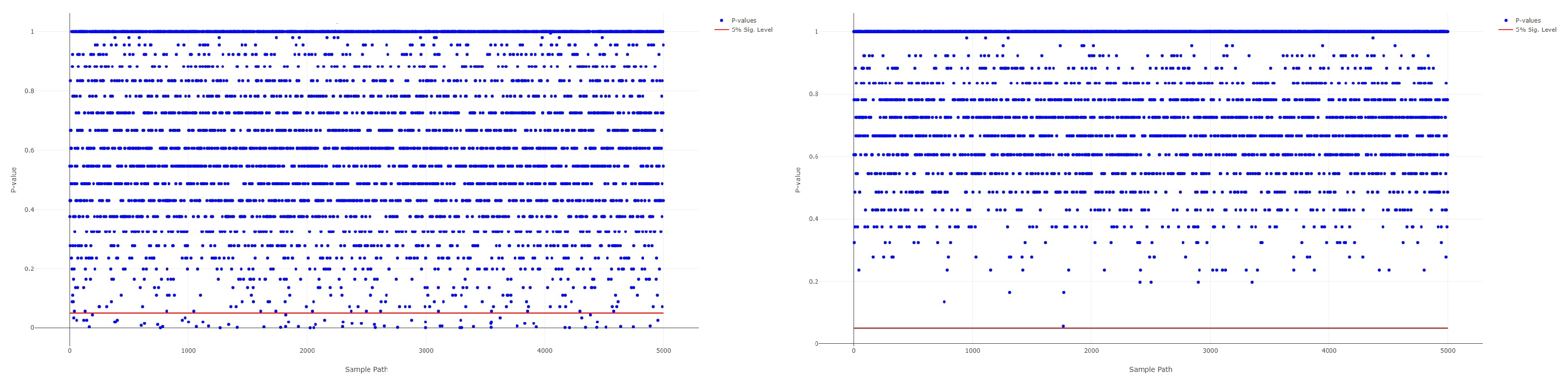

3.1. White Noise Empirical Characteristics

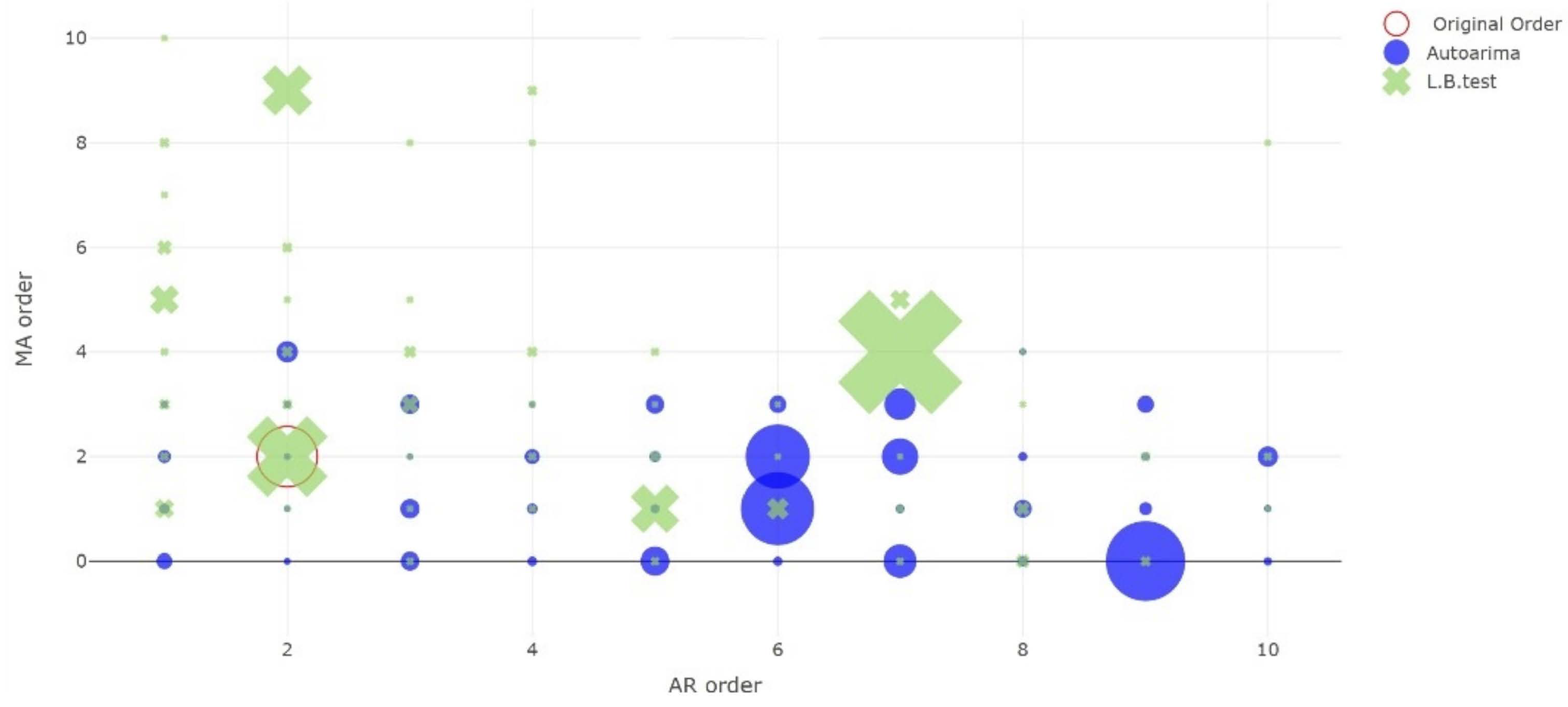

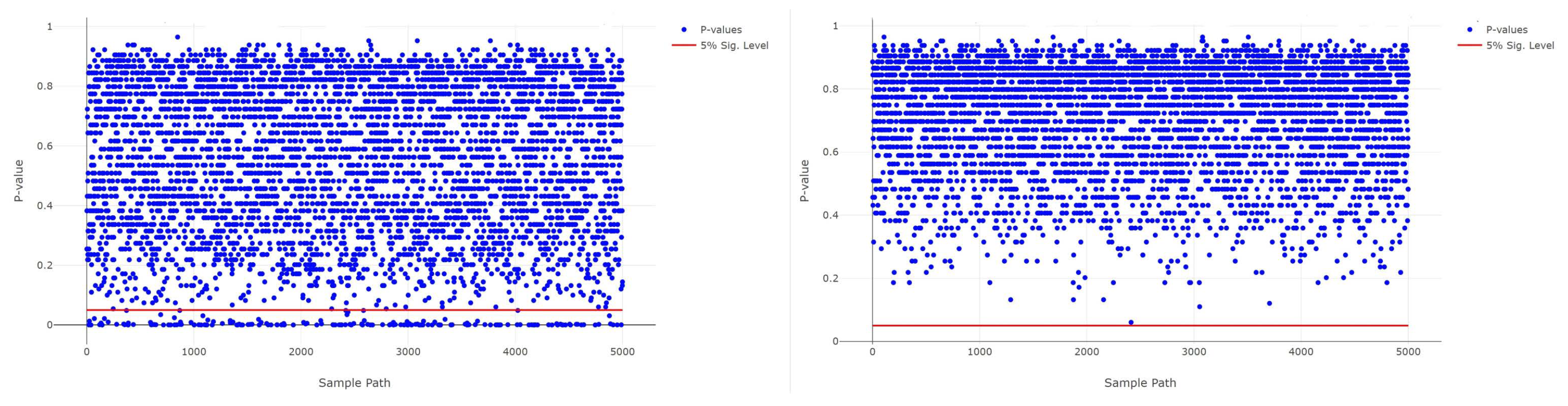

3.2. Impact of White Noise Empirical Characteristics on Models Selection

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Hassani, H.; Silva, E.S. A Kolmogorov-Smirnov Based Test for Comparing the Predictive Accuracy of Two Sets of Forecasts. Econometrics 2015, 3, 590–609. [Google Scholar] [CrossRef]

- Hassani, H.; Yarmohammadi, M.; Mashhad, L.M. Uncovering Hidden Insights with Long-Memory Process Detection: An In-Depth Overview. Risks 2023, 11, 113. [Google Scholar] [CrossRef]

- Hassani, H.; Royer-Carenzi, M.; Mashhad, L.M.; Yarmohammadi, M.; Yeganegi, M.R. Exploring the Depths of the Autocorrelation Function: Its Departure from Normality. Information 2024, 15, 449. [Google Scholar] [CrossRef]

- Wang, M.; Guo, X.; She, Y.; Zhou, Y.; Liang, M.; Chen, Z.S. Advancements in Deep Learning Techniques for Time Series Forecasting in Maritime Applications: A Comprehensive Review. Information 2024, 15, 507. [Google Scholar] [CrossRef]

- Renteria-Mena, J.B.; Plaza, D.; Giraldo, E. Multivariate Hydrological Modeling Based on Long Short-Term Memory Networks for Water Level Forecasting. Information 2024, 15, 358. [Google Scholar] [CrossRef]

- Westergaard, G.; Erden, U.; Mateo, O.A.; Lampo, S.M.; Akinci, T.C.; Topsakal, O. Time Series Forecasting Utilizing Automated Machine Learning (AutoML): A Comparative Analysis Study on Diverse Datasets. Information 2024, 15, 39. [Google Scholar] [CrossRef]

- Wang, X.; Dong, S.; Zhang, R. An Integrated Time Series Prediction Model Based on Empirical Mode Decomposition and Two Attention Mechanisms. Information 2023, 14, 610. [Google Scholar] [CrossRef]

- Hassani, H.; Yeganegi, M.R. Sum of squared ACF and the Ljung-Box statistics. Phys. Stat. Mech. Its Appl. 2019, 520, 81–86. [Google Scholar] [CrossRef]

- Tsay, R. Analysis of Financial Time Series, 3rd ed.; John Wiley & Sons: New York, NY, USA, 2010. [Google Scholar]

- Teyssière, G.; Kirman, A. Microeconomic models for long memory in the volatility of financial time series. Phys. A 2002, 370, 26–31. [Google Scholar]

- Arunachalam, V.; Jaafar, A. Forecasting Dengue Incidence in Penang, Malaysia: A Comparison of ARIMA and GARCH Models. Am. J. Trop. Med. Hyg. 2011, 85, 827–833. [Google Scholar]

- Glass, G.V.; Willson, V.L.; Gottman, J.M. Design and Analysis of Time-Series Experiments. Annu. Rev. Psychol. 1975, 26, 609–653. [Google Scholar]

- Luis, C.O.; Francisco, G.S.; Jose, M.S. Forecasting of Emergency Department Admissions. Healthc. Manag. Sci. 2012, 15, 215–224. [Google Scholar]

- Campbell, J.Y.; Perron, P. An Empirical Investigation of the Relations between Climate Change and Agricultural Yield: A Time Series Analysis of Maize Yield in Nigeria. J. Agric. Environ. Sci. 2004, 5, 217–230. [Google Scholar]

- Zheng, X.; Basher, R.E. Structural Time Series Models and Trend Detection in Global and Regional Temperature Series. J. Clim. 1999, 12, 2347–2358. [Google Scholar] [CrossRef]

- Box, G.; Pierce, D. Distribution of Residual Autocorrelations in Autoregressive-Integrated Moving Average Time Series Models. J. Am. Statist. Assoc. 1970, 65, 1509–1526. [Google Scholar] [CrossRef]

- Ljung, G.; Box, G. On a Measure of a Lack of Fit in Time Series Models. Biometrika 1978, 65, 297–303. [Google Scholar] [CrossRef]

- Priestley, M.B. Spectral Analysis and Time Series. J. Time Ser. Anal. 1981, 2, 85–106. [Google Scholar] [CrossRef]

- Brockwell, P.; Davis, R. Time Series: Theory and Methods, 2nd ed.; Springer: New York, NY, USA, 1991. [Google Scholar]

- Chatfield, C. The Analysis of Time Series: An Introduction; CRC Press: Boca Raton, FL, USA, 2003. [Google Scholar]

- Hamilton, J.D. Time Series Analysis. Econ. Rev. 1994, 13, 147–192. [Google Scholar]

- Montgomery, D.C.; Jennings, C.L.; Kulahci, M. Introduction to Time Series Analysis and Forecasting; John Wiley & Sons: Hoboken, NJ, USA, 2008. [Google Scholar]

- Shumway, R.H.; Stoffer, D.S. Time Series Analysis and Its Applications: With R Examples; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Hassani, H. Sum of the sample of autocorrelation function. Random Oper. Stoch. Eqs. 2009, 17, 125–130. [Google Scholar] [CrossRef]

- Wei, W.W.S. Time Series Analysis Univariate and Multivariate Methods, 2nd ed.; Addison Wesley: New York, NY, USA, 2006. [Google Scholar]

- Brockwell, P.J.; Davis, R.A. Introduction to Time Series and Forecasting; STS; Springer: Cham, Switzerland, 2016. [Google Scholar]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice, 2nd ed.; OTexts: Melbourne, Australia, 2018; Available online: https://otexts.com/fpp2/ (accessed on 20 January 2025).

- Bisaglia, L.; Gerolimetto, M. Testing for Time Series Linearity Using the Autocorrelation Function. Stat. Methods Appl. 2009, 18, 23–50. [Google Scholar]

- Boutahar, M.; Royer-Carenzi, M. Identifying trends nature in time series using autocorrelation functions and stationarity tests. Int. J. Econ. Econom. 2024, 14, 1–22. [Google Scholar] [CrossRef]

- Kendall, M.G. Time-Series; Oxford University Press: Oxford, UK, 1976. [Google Scholar]

- Granger, C.W.J.; Joyeux, R. An Introduction to Long-Memory Time Series Models and Fractional Differencing. J. Time Ser. Anal. 1980, 1, 15–29. [Google Scholar] [CrossRef]

- Hassani, H.; Yeganegi, M.R.; Mehreyan, S.Z.; Sayyareh, A. On the Sample Autocorrelation Function’s Absolute Summability. Fluct. Noise Lett. 2022, 21, 2250004. [Google Scholar] [CrossRef]

- Hosking, J. Asymptotic distribution of the sample mean, autocovariances, autocorrelations of long-memory time series. J. Econ. 1996, 73, 261–284. [Google Scholar] [CrossRef]

- Dimitriadis, P.; Koutsoyiannis, D. Climacogram versus Autocovariance and Power Spectrum in Stochastic Modelling for Markovian and Hurst-Kolmogorov Processes. Stoch. Environ. Res. Risk Assess. 2015, 15, 1649–1669. [Google Scholar] [CrossRef]

- Liu, S.; Xie, Y.; Fang, H.; Du, H.; Xu, P. Trend Test for Hydrological and Climatic Time Series Considering the Interaction of Trend and Autocorrelations. Water 2022, 14, 3006. [Google Scholar] [CrossRef]

- Phojanamongkolkij, N.; Kato, S.; Wielicki, B.A.; Taylor, P.C.; Mlynczak, M.G. A Comparison of Climate Signal Trend Detection Uncertainty Analysis Methods. J. Clim. 2014, 27, 3363–3376. [Google Scholar] [CrossRef]

- Xie, Y.; Liu, S.; Fang, H.; Wang, J. Global Autocorrelation Test Based on the Monte Carlo Method and Impacts of Eliminating Nonstationary Components on the Global Autocorrelation Test. Stoch. Environ. Res. Risk Assess. 2020, 34, 1645–1658. [Google Scholar] [CrossRef]

- Belmahdi, B.; Louzazni, M.; El Bouardi, A. One month-ahead forecasting of mean daily global solar radiation using time series models. Optik 2020, 219, 165207. [Google Scholar] [CrossRef]

- Gostischa, J.; Massolo, A.; Constantine, R. Multi-species feeding association dynamics driven by a large generalist predator. Front. Mar. Sci. 2021, 8, 739894. [Google Scholar] [CrossRef]

- Yang, Y.; Qin, S.; Liao, S. Ultra-chaos of a mobile robot: A higher disorder than normal-chaos. Chaos Solitons Fractals 2023, 167, 113037. [Google Scholar] [CrossRef]

- Bai, M.; Zhou, Z.; Chen, Y.; Liu, J.; Yu, D. Accurate four-hour-ahead probabilistic forecast of photovoltaic power generation based on multiple meteorological variables-aided intelligent optimization of numeric weather prediction data. Earth Sci. Inform. 2023, 16, 2741–2766. [Google Scholar] [CrossRef]

- Orlando, G.; Bufalo, M. Empirical evidences on the interconnectedness between sampling and asset returns’s distributions. Risks 2021, 9, 88. [Google Scholar] [CrossRef]

- Wang, X.; Yang, J.; Yang, F.; Wang, Y.; Liu, F. Multilevel residual prophet network time series model for prediction of irregularities on high-speed railway track. J. Transp. Eng. Part Syst. 2023, 149, 04023012. [Google Scholar] [CrossRef]

- Hassani, H. A note on the sum of the sample autocorrelation function. Phys. A Stat. Mech. Appl. 2010, 389, 1601–1606. [Google Scholar] [CrossRef]

- Hassani, H.; Yeganegi, M. Selecting optimal lag order in Ljung-Box test. Phys. A 2020, 541, 123700. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Khandakar, Y. Automatic time series forecasting: The forecast package for R. J. Stat. Softw. 2008, 27, 1–22. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hassani, H.; Mashhad, L.M.; Royer-Carenzi, M.; Yeganegi, M.R.; Komendantova, N. White Noise and Its Misapplications: Impacts on Time Series Model Adequacy and Forecasting. Forecasting 2025, 7, 8. https://doi.org/10.3390/forecast7010008

Hassani H, Mashhad LM, Royer-Carenzi M, Yeganegi MR, Komendantova N. White Noise and Its Misapplications: Impacts on Time Series Model Adequacy and Forecasting. Forecasting. 2025; 7(1):8. https://doi.org/10.3390/forecast7010008

Chicago/Turabian StyleHassani, Hossein, Leila Marvian Mashhad, Manuela Royer-Carenzi, Mohammad Reza Yeganegi, and Nadejda Komendantova. 2025. "White Noise and Its Misapplications: Impacts on Time Series Model Adequacy and Forecasting" Forecasting 7, no. 1: 8. https://doi.org/10.3390/forecast7010008

APA StyleHassani, H., Mashhad, L. M., Royer-Carenzi, M., Yeganegi, M. R., & Komendantova, N. (2025). White Noise and Its Misapplications: Impacts on Time Series Model Adequacy and Forecasting. Forecasting, 7(1), 8. https://doi.org/10.3390/forecast7010008