Foreign Exchange Forecasting Models: LSTM and BiLSTM Comparison †

Abstract

:1. Introduction

2. Methods

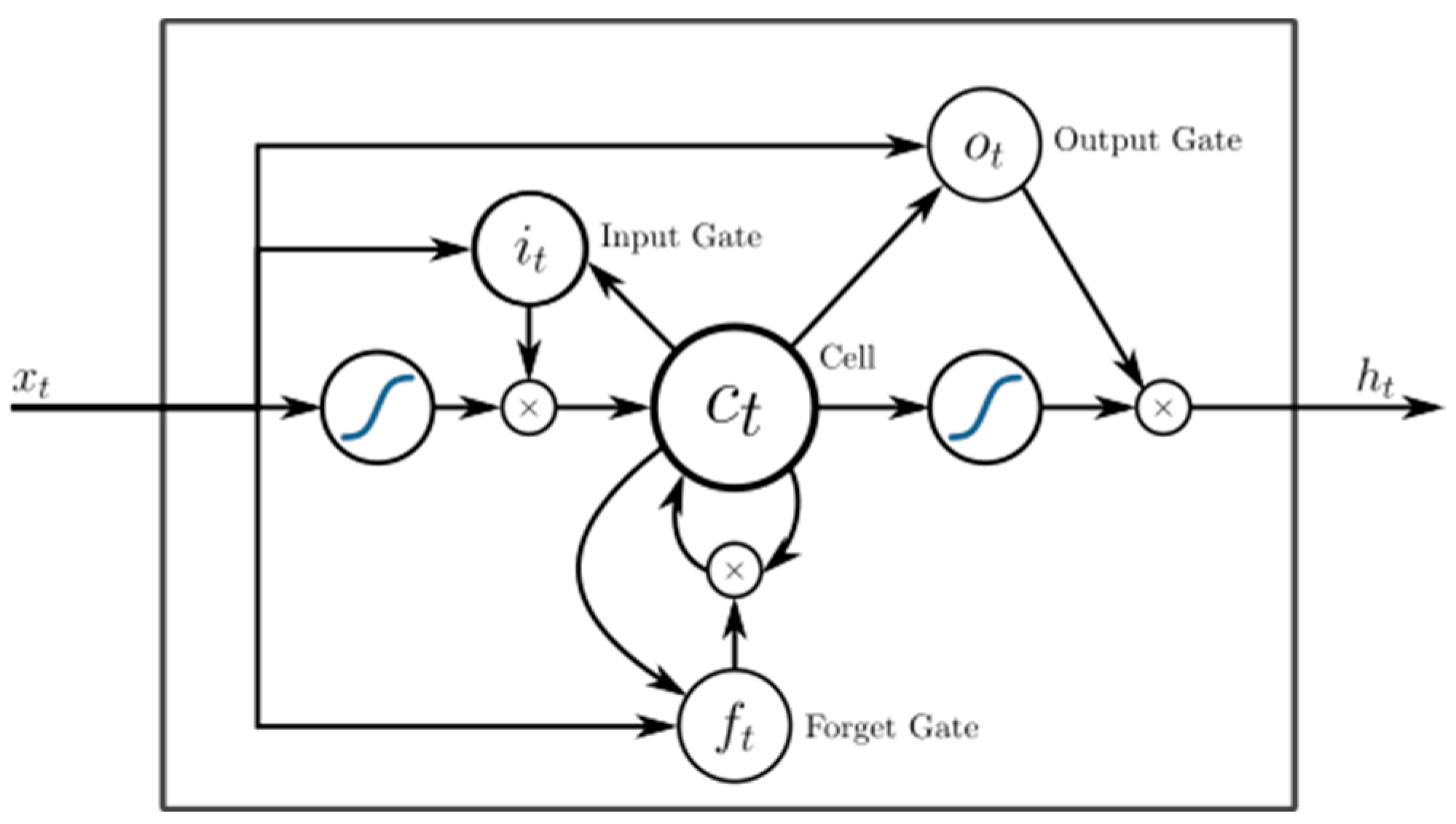

2.1. Long Short-Term Memory Neural Network

2.2. BiLSTM Model

3. Results

3.1. Database

3.2. Data Analysis and Processing

3.3. Model Estimation and Results

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ghalayini, L. Modeling and Forecasting the US Dollar/Euro Exchange Rate. Int. J. Econ. Financ. 2014, 6, 194–207. [Google Scholar] [CrossRef]

- García, F.; Guijarro, F.; Oliver, J. A Multicriteria Goal Programming Model for Ranking Universities. Mathematics 2021, 9, 459. [Google Scholar] [CrossRef]

- Burmann, C.; García, F.; Guijarro, F.; Oliver, J. Ranking the Performance of Universities: The Role of Sustainability. Sustainability 2021, 13, 13286. [Google Scholar] [CrossRef]

- Repetto, M.; La Torre, D.; Tariq, M. Goal Programming in Federated Learning: An Application to Time Series Forecasting. In Proceedings of the 2022 International Conference on Decision Aid Sciences and Applications (DASA), Chiangrai, Thailand, 23–25 March 2022; pp. 1672–1677. [Google Scholar] [CrossRef]

- Nwankwo, S.C. Autorregressive Inegrated Moving Average (ARIMA) Model for Exchange Rate (Naira to Dollar). Acad. J. Interdiscip. Stud. 2014, 3, 429–433. [Google Scholar] [CrossRef]

- Asadullah, M. Forecast Foreing Exchange Rate: The Case Study of PKR/USD. Mediterr. J. Soc. Sci. 2020, 11, 129–137. [Google Scholar] [CrossRef]

- Dunis, C.L.; Huang, X. Forecasting and trading currency volatility: An application of recurrent neural regression and model combination. J. Forecast. 2002, 21, 317–354. [Google Scholar] [CrossRef]

- Mbaga, Y.V.; Olubusoye, O.E. Foreign Exchange Prediction: A Comparative Analysis of Foreign Exchange Neural Network (FOREXNN) and ARIMA Models. 2014. Available online: https://www.researchgate.net/publication/280040546 (accessed on 3 July 2024).

- Kamruzzaman, J.; Sarker, R.A. Comparing ANN Based Models with ARIMA for Prediction of Forex Rates. ASOR Bull. 2003, 22, 2–11. [Google Scholar]

- Huang, W.; Lai, K.K.; Wang, S. Forecasting Foreign Exchange Rates With Artificial Neural Networks: A Review. Int. J. Inf. Technol. Decis. Mak. 2004, 3, 145–165. [Google Scholar] [CrossRef]

- Escudero, P.; Alcocer, W.; Paredes, J. Recuerrent Neural Networks and ARIMA Models for Euro/Dollar Exchange Rate Forecasting. Appl. Sci. 2021, 11, 5658. [Google Scholar] [CrossRef]

- Kaushik, M.; Giri, A.K. Forecasting Foreign Exchange Rate: A Multivariate Comparative Analysis between Traditional Econometric Contemporary Machine Learning & Deep Learning Techniques. arXiv 2002, arXiv:2002.10247. [Google Scholar] [CrossRef]

- Islam, M.S.; Hossain, E.; Rahman, A.; Shahadat, M.; Andersson, K. A Review on Recent Advancements in Forex Currency Prediction. Algorithms 2020, 13, 186. [Google Scholar] [CrossRef]

- Hajirahimi, Z.; Khashei, M. Hybrid structures in time series modeling and forecasting: A review. Eng. Appl. Artif. Intell. 2019, 86, 83–106. [Google Scholar] [CrossRef]

- Khashei, M.; Bijari, M. A new class of hybrid models for time series forecasting. Expert Syst. Appl. 2012, 39, 4344–4357. [Google Scholar] [CrossRef]

- Zougagh, N.; Charkaoui, A.; Echchatbi, A. Artificial intelligence hybrid models for improving forecasting accuracy. Procedia Comput. Sci. 2021, 184, 817–822. [Google Scholar] [CrossRef]

- Mucaj, R.; Sinaj, V. Exchange Rate Forecasting using ARIMA, NAR and ARIMA-ANN Hybrid Model. J. Multidiscip. Eng. Sci. Technol. 2017, 4, 8581–8586. [Google Scholar]

- Wang, L.; Zou, H.; Li, L.; Chaudhry, S. An ARIMA-ANN Hybrid Model for Time Series Forecasting. Syst. Res. Behav. Sci. 2013, 30, 244–259. [Google Scholar] [CrossRef]

- García, F.; Guijarro, F.; Oliver, J.; Tamošiūnienė, R. Foreign Exchange Forecasting Models: ARIMA and LSTM Comparison. Eng. Proc. 2023, 39, 81. [Google Scholar] [CrossRef]

- Siami-Namini, S.; Tavakoli, N.; Namin, A.S. The Performance of LSTM and BiLSTM in Forecasting Time Series. In Proceedings of the 2019 IEEE International Conference on Big Data (Big Data), Los Angeles, CA, USA, 24 February 2020; pp. 3285–3292. [Google Scholar] [CrossRef]

- Box, G.E.P.; Jenkins, G.M. Time Series Analysis: Forecasting and Control; Holden-Day: San Francisco, CA, USA, 1976. [Google Scholar]

- Hochreiter, S.; Schmidhuber, J. Long Short-Term Memory. Neural Comput. 1997, 9, 1735–1780. [Google Scholar] [CrossRef] [PubMed]

- Huang, C.-G.; Yin, X.; Huang, H.-Z.; Li, Y.-F. An Enhanced Deep Learning-Based Fusion Prognostic Method for RUL Prediction. IEEE Trans. Reliab. 2020, 69, 1097–1109. [Google Scholar] [CrossRef]

- Schuster, M.; Paliwal, K.K. Bidirectional recurrent neural networks. IEEE Trans. Signal Process. 1997, 45, 2673–2681. [Google Scholar] [CrossRef]

- Altché, F.; de La Fortelle, A. An LSTM Network for Highway Trajectory Prediction. In Proceedings of the IEEE 20th International Conference on Intelligent Transportation Systems (ITSC), Yokohama, Japan, 15 March 2018; 2017; pp. 353–359. [Google Scholar] [CrossRef]

- Wang, C.; Qiao, J. Construction Project Prediction Method Based on Improved BiLSTM. Appl. Sci. 2024, 14, 978. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Mean | Median | Sd | Skew. | Kurt. | |

|---|---|---|---|---|---|

| BTC/USD | 29,677 | 27,915 | 9330.58 | 0.528 | −0.761 |

| EUR/GBP | 0.861 | 0.861 | 0.016 | −0.116 | −0.750 |

| EUR/JPY | 144.621 | 143.404 | 9.894 | 0.123 | −1.027 |

| EUR/NZD | 1.709 | 1.702 | 0.066 | 0.035 | −0.961 |

| EUR/USD | 1.070 | 1.075 | 0.041 | −0.556 | −0.135 |

| GBP/USD | 1.244 | 1.242 | 0.058 | −0.048 | 0.041 |

| Model | GBP/USD | EUR/USD | EUR/NZD | EUR/JPY | EUR/GBP | BTC |

|---|---|---|---|---|---|---|

| MAPE | ||||||

| LSTM | 0.0153 | 0.0376 | 0.0161 | 0.0405 | 0.0110 | 0.1232 |

| BiLSTM | 0.0160 | 0.0219 | 0.0137 | 0.0375 | 0.0094 | 0.0707 |

| MAE | ||||||

| LSTM | 0.0132 | 0.0331 | 0.0145 | 0.0351 | 0.0102 | 0.0638 |

| BiLSTM | 0.0139 | 0.0189 | 0.0122 | 0.0326 | 0.0087 | 0.0339 |

| RMSE | ||||||

| LSTM | 0.0172 | 0.0366 | 0.0178 | 0.0395 | 0.0123 | 0.0798 |

| BiLSTM | 0.0185 | 0.0224 | 0.0151 | 0.0372 | 0.0105 | 0.0465 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

García, F.; Guijarro, F.; Oliver, J.; Tamošiūnienė, R. Foreign Exchange Forecasting Models: LSTM and BiLSTM Comparison. Eng. Proc. 2024, 68, 19. https://doi.org/10.3390/engproc2024068019

García F, Guijarro F, Oliver J, Tamošiūnienė R. Foreign Exchange Forecasting Models: LSTM and BiLSTM Comparison. Engineering Proceedings. 2024; 68(1):19. https://doi.org/10.3390/engproc2024068019

Chicago/Turabian StyleGarcía, Fernando, Francisco Guijarro, Javier Oliver, and Rima Tamošiūnienė. 2024. "Foreign Exchange Forecasting Models: LSTM and BiLSTM Comparison" Engineering Proceedings 68, no. 1: 19. https://doi.org/10.3390/engproc2024068019