Time-Series Modelling and Granger Causality Analysis of GDP and Energy Consumption: The Case of Ecuador 1965–2022 †

Abstract

1. Introduction

- Energy Consumption causes GDP growth.

- GDP growth causes Energy Consumption.

- Growth is produced in both directions.

- There is no effect from either variable.

2. Granger Causality

3. Methods

3.1. Data Collection

3.2. Econometrics Model

3.3. Causality Test

4. Results

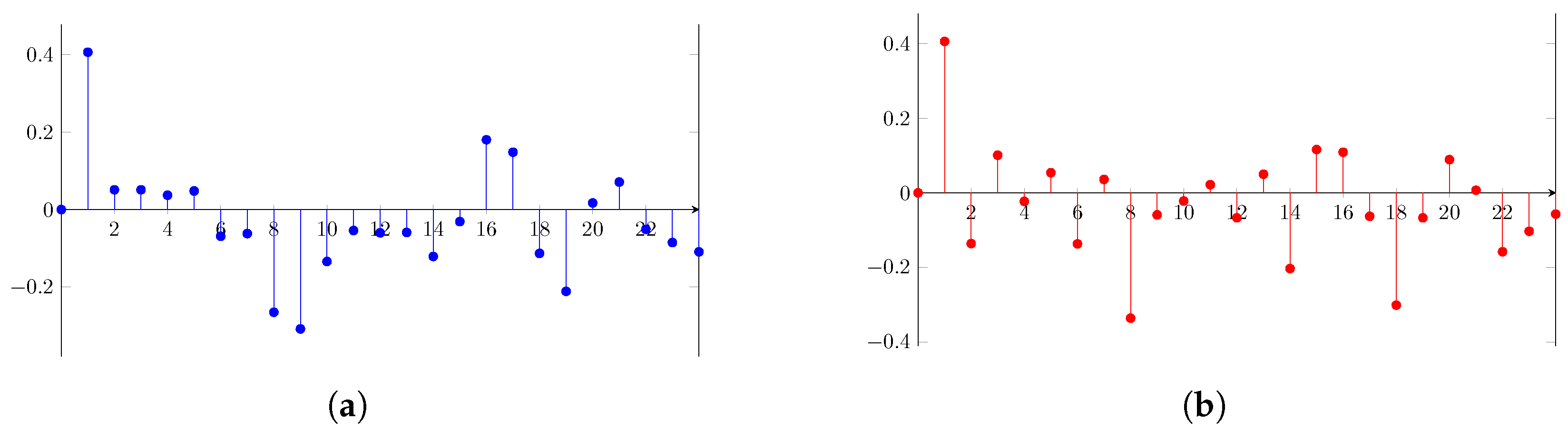

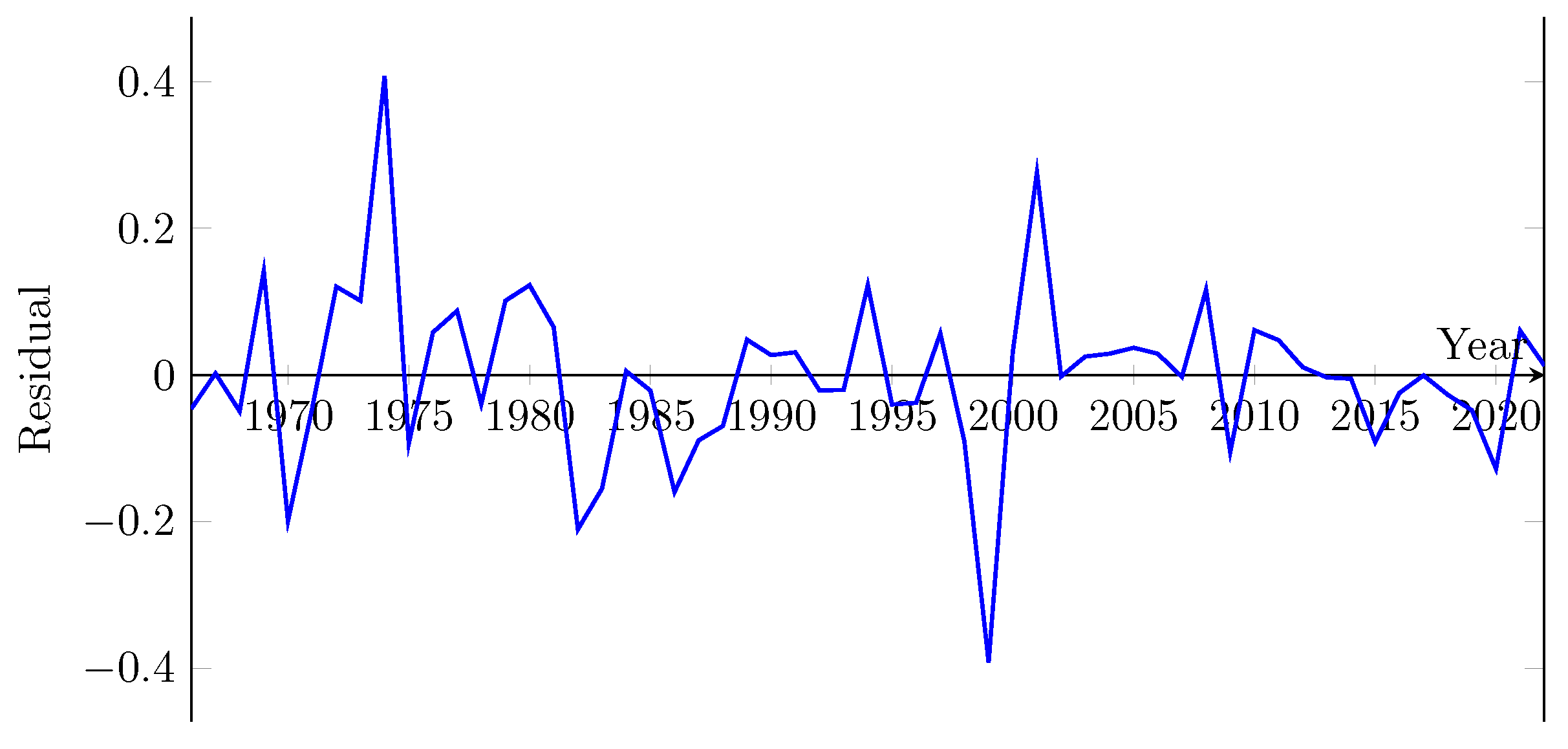

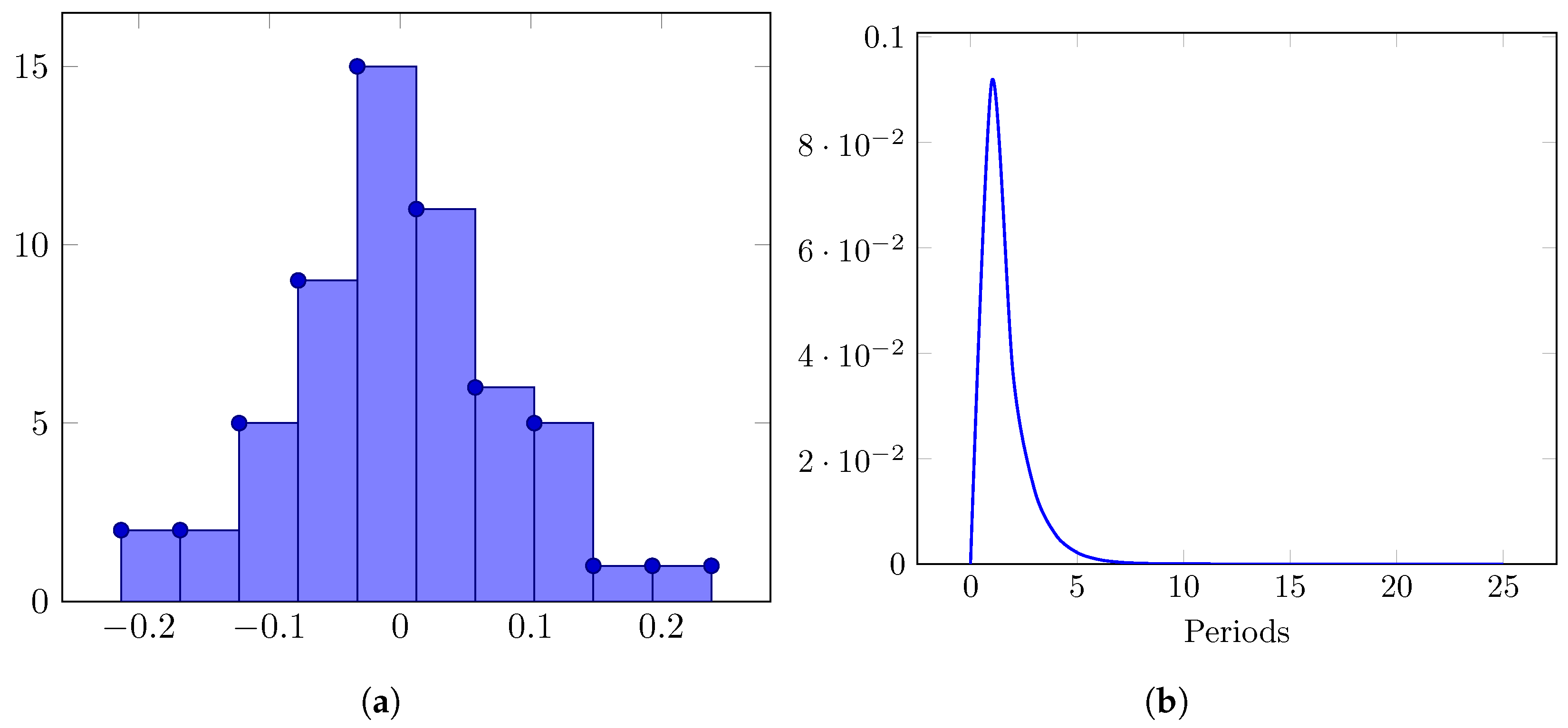

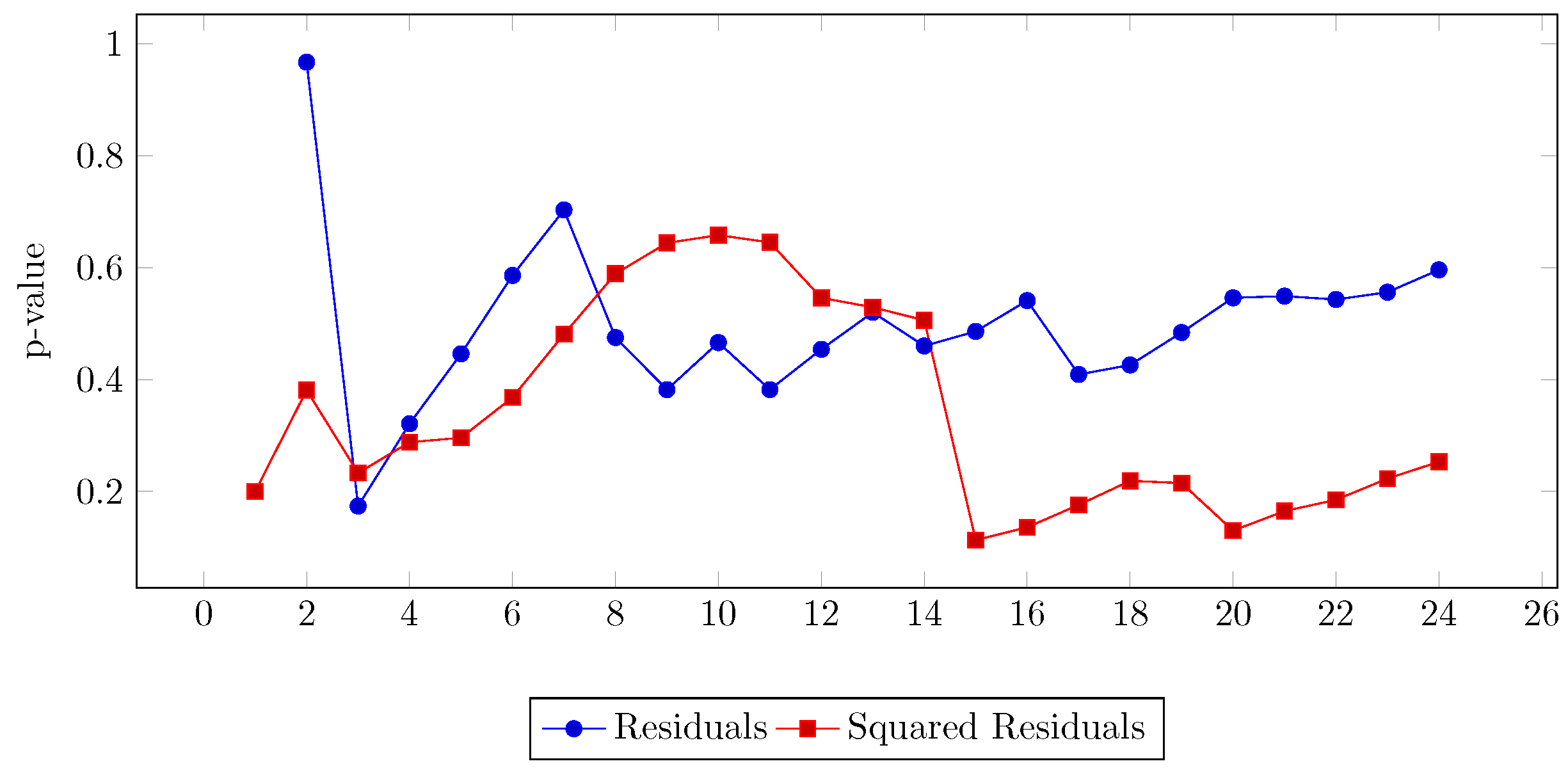

4.1. Modelling the GDP

4.2. Modelling Energy Consumption

4.3. VAR Model and Granger Causality Analysis

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Beaudreau, B.C. On the methodology of energy-GDP Granger causality tests. Energy 2010, 35, 3535–3539. [Google Scholar] [CrossRef]

- Tiwari, A.K. The asymmetric Granger-causality analysis between energy consumption and income in the United States. Renew. Sustain. Energy Rev. 2014, 36, 362–369. [Google Scholar] [CrossRef]

- Mutascu, M. A bootstrap panel Granger causality analysis of energy consumption and economic growth in the G7 countries. Renew. Sustain. Energy Rev. 2016, 63, 166–171. [Google Scholar] [CrossRef]

- Chiou-Wei, S.Z.; Chen, C.F.; Zhu, Z. Economic growth and energy consumption revisited—Evidence from linear and nonlinear Granger causality. Energy Econ. 2008, 30, 3063–3076. [Google Scholar] [CrossRef]

- Sunde, T. Energy consumption and economic growth modelling in SADC countries: An application of the VAR Granger causality analysis. Int. J. Energy Technol. Policy 2020, 16, 41–56. [Google Scholar] [CrossRef]

- Tran, B.L.; Chen, C.C.; Tseng, W.C. Causality between energy consumption and economic growth in the presence of GDP threshold effect: Evidence from OECD countries. Energy 2022, 251, 123902. [Google Scholar] [CrossRef]

- Odhiambo, N.M. Trade openness and energy consumption in sub-Saharan African countries: A multivariate panel Granger causality test. Energy Rep. 2021, 7, 7082–7089. [Google Scholar] [CrossRef]

- Rahman, M.H.; Ruma, A.; Hossain, M.N.; Nahrin, R.; Majumder, S.C. Examine the empirical relationship between energy consumption and industrialization in Bangladesh: Granger causality analysis. Int. J. Energy Econ. Policy 2021, 11, 121–129. [Google Scholar] [CrossRef]

- Krkošková, R. Causality between energy consumption and economic growth in the V4 countries. Technol. Econ. Dev. Econ. 2021, 27, 900–920. [Google Scholar] [CrossRef]

- Bayar, Y.; Sasmaz, M.U.; Ozkaya, M.H. Impact of trade and financial globalization on renewable energy in EU transition economies: A bootstrap panel granger causality test. Energies 2020, 14, 19. [Google Scholar] [CrossRef]

- AlKhars, M.; Miah, F.; Qudrat-Ullah, H.; Kayal, A. A systematic review of the relationship between energy consumption and economic growth in GCC countries. Sustainability 2020, 12, 3845. [Google Scholar] [CrossRef]

- Sanchez-Loor, D.A.; Zambrano-Monserrate, M.A. Causality analysis between electricity consumption, real GDP, foreign direct investment, human development and remittances in Colombia, Ecuador and Mexico. Int. J. Energy Econ. Policy 2015, 5, 746–753. [Google Scholar]

- Cetin, M.; Ecevit, E. The dynamic causal links between energy consumption, trade openness and economic growth: Time series evidence from upper middle income countries. Eur. J. Econ. Stud. 2018, 7, 58–68. [Google Scholar]

- Yoo, S.H.; Kwak, S.Y. Electricity consumption and economic growth in seven South American countries. Energy Policy 2010, 38, 181–188. [Google Scholar] [CrossRef]

- Rodríguez-Caballero, C.V.; Ventosa-Santaulària, D. Energy-growth long-term relationship under structural breaks. Evidence from Canada, 17 Latin American economies and the USA. Energy Econ. 2017, 61, 121–134. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Energy consumption and growth in South America: Evidence from a panel error correction model. Energy Econ. 2010, 32, 1421–1426. [Google Scholar] [CrossRef]

- Jin, S.J.; Lim, S.Y.; Yoo, S.H. Causal relationship between oil consumption and economic growth in Ecuador. Energy Sources Part B Econ. Plan. Policy 2016, 11, 782–787. [Google Scholar] [CrossRef]

- Pinzón, K. Dynamics between energy consumption and economic growth in Ecuador: A granger causality analysis. Econ. Anal. Policy 2018, 57, 88–101. [Google Scholar] [CrossRef]

- Granger, C.W. Investigating causal relations by econometric models and cross-spectral methods. Econom. J. Econom. Soc. 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Shojaie, A.; Fox, E.B. Granger causality: A review and recent advances. Annu. Rev. Stat. Its Appl. 2022, 9, 289–319. [Google Scholar] [CrossRef]

- Akaike, H. Akaike’s Information Criterion. In International Encyclopedia of Statistical Science; Lovric, M., Ed.; Springer: Berlin/Heidelberg, Germany, 2011; p. 25. [Google Scholar]

- Schwarz, G. Estimating the dimension of a model. Ann. Stat. 1978, 6, 461–464. [Google Scholar] [CrossRef]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill: New York, NY, USA, 2009. [Google Scholar]

- Franses, P.H.; Dijk, D.V.; Opschoor, A. Time Series Models for Business and Economic Forecasting, 2nd ed.; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar]

- Bank, W. World Bank National Accounts Data, and OECD National Accounts Data Files. 2024. Available online: https://data.worldbank.org (accessed on 2 May 2024).

- BP. Energy Outlook. 2024. Available online: https://www.bp.com (accessed on 5 May 2024).

- Quevedo, C. Ecuador: Petróleo y crisis económlca. In El Sector Energético Ecuatoriano y la Caída de los Precios Internacionales del Petróleo; FLACSO: Ciudad de Guatemala, Guatemala, 1986; pp. 91–150. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.0744 | 0.0208 | 3.5710 | 0.0008 |

| Dummy | −0.3175 | 0.0380 | −8.3393 | 0 |

| dummy(-1) | −0.0834 | 0.0806 | −1.0348 | 0.3055 |

| AR(1) | 0.3926 | 0.1343 | 2.9234 | 0.0051 |

| SIGMASQ | 0.0076 | 0.0016 | 4.5908 | 0 |

| R-squared | 0.5114 | Mean dependent var | 0.0679 | |

| Adj. R-squared | 0.4739 | S.D. dependent var | 0.1263 | |

| S.E. of regression | 0.0916 | Akaike info criterion | −1.855 | |

| Sum squared resid | 0.4366 | Schwarz criter. | −1.6762 | |

| Log likelihood | 57.8808 | Hannan–Quinn criter. | −1.7858 | |

| F-statistic | 13.6110 | Durbin–Watson stat. | 1.9054 | |

| Prob (F-statistic) | 0 | Inverted AR Roots | 0.39 | |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.0591 | 0.0095 | 6.2418 | 0.0000 |

| dummy | −0.1495 | 0.0455 | −3.2872 | 0.0018 |

| dummy(-1) | 0.0082 | 0.0253 | 0.3229 | 0.7481 |

| AR(1) | 0.0205 | 0.1768 | 0.1161 | 0.9080 |

| SIGMASQ | 0.0035 | 0.0007 | 5.2052 | 0.0000 |

| R-squared | 0.2554 | Mean dependent var | 0.056656 | |

| Adj. R-squared | 0.1981 | S.D. dependent var | 0.068727 | |

| S.E. of regression | 0.0615 | Akaike info criterion | −2.654476 | |

| Sum squared resid | 0.1970 | Schwarz criter. | −2.475261 | |

| Log likelihood | 80.6526 | Hannan–Quinn criter. | −2.584827 | |

| F-statistic | 4.4582 | Durbin–Watson stat. | 1.994629 | |

| Prob (F-statistic) | 0.0036 | Inverted AR Roots | 0.02 | |

| GDP | GDP (EC) | EC | EC (GDP) | |

|---|---|---|---|---|

| Akaike info criterion | −1.855 | −1.8313 | −2.6544 | −2.5837 |

| Schwarz criterion | −1.6762 | −1.6123 | −2.4752 | −2.3647 |

| Dependent Variable: D (log(GDP)) | Dependent Variable: D (log(energy)) | ||||||

|---|---|---|---|---|---|---|---|

| Excluded | Chi-sq | df | Prob. | Excluded | Chi-sq | df | Prob. |

| D (log(energy)) | 8.0869 | 2 | 0.0175 | D (log(GDP)) | 0.0516 | 2 | 0.9745 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Valencia, F. Time-Series Modelling and Granger Causality Analysis of GDP and Energy Consumption: The Case of Ecuador 1965–2022. Eng. Proc. 2024, 77, 6. https://doi.org/10.3390/engproc2024077006

Valencia F. Time-Series Modelling and Granger Causality Analysis of GDP and Energy Consumption: The Case of Ecuador 1965–2022. Engineering Proceedings. 2024; 77(1):6. https://doi.org/10.3390/engproc2024077006

Chicago/Turabian StyleValencia, Fausto. 2024. "Time-Series Modelling and Granger Causality Analysis of GDP and Energy Consumption: The Case of Ecuador 1965–2022" Engineering Proceedings 77, no. 1: 6. https://doi.org/10.3390/engproc2024077006

APA StyleValencia, F. (2024). Time-Series Modelling and Granger Causality Analysis of GDP and Energy Consumption: The Case of Ecuador 1965–2022. Engineering Proceedings, 77(1), 6. https://doi.org/10.3390/engproc2024077006