1. Introduction

Historical analysis of human mortality by demographers, actuaries, and statisticians has provided evidence of a significant decline in the mortality indices over time. Interestingly, country-wise mortality trends also indicate that life expectancy has increased significantly in most countries, especially in recent decades. This evidence is obvious in Ghana, where life expectancy in 1960 was estimated to be 45.84 years. Today, this number has increased to 64.07 years [

1,

2]. While such profound achievement is an indication of an illustrious milestone in human life, the associated actuarial financial ramifications are quite inconceivable [

3]. Owing to this, actuaries and financial engineers, especially in advanced countries (where improvements in human life are often fast-paced), recognize the significance of tackling such longevity in actuarial and financial-related instruments such as life insurance and pensions [

4]. De Waegenaere et al. said that longevity risk is present in pensions and life insurance products when there are uncertainties about mortality rates or, on the other hand, survival rates [

5]. This means that when the financial market is fully hedged against its risk, the uncertainty in the future lifetimes of pension participants or life product subscribers becomes the only source of risk to the solvency of pension schemes. Ref [

6] suggests constantly investigating the existence and uncertainty of this risk using the past mortality behavior of plan members.

Longevity risk arises as a result of unexpected changes in the mortality rates of populations [

7]. It is also said that a typical longevity risk is caused by uncertainty in the patterns of mortality and life expectancy. The fact that changes in the life expectancy of plan participants are unforeseeable makes it difficult to measure and securitize [

8]. These changes, however, are attributed to positive strides in technology and medical advancements, including sanitation. As there are two sides to every event, an increase in life expectancy as a positive human achievement comes with its own two-edged economic sword. For life insurers, higher life expectancies are golden for profit-making as this reduces liabilities for death benefit payments. However, for annuity-type policies or schemes, such as a pension, this may pose serious solvency issues for the firm [

9].

Historically, governments, policymakers, companies, and several other entities have heavily relied on data forecasts to make major decisions. In regard to pension schemes, pension fund managers rely on life expectancy data forecasts to determine periods of annuity payments. Consequently, they make economic investments to meet these expected future liabilities [

3,

10]. Therefore, to the pension scheme or invariably to the fund managers, “longevity risk” is the risk arising from life expectancy exceeding the expected age limit, thus creating extra annuity liabilities for the pension fund. This exposes the fund to benefit payments higher than originally anticipated or expected, thus amounting to serious solvency issues [

10,

11,

12]. Longevity improvement is a serious financial risk for pension funds and even for annuity products in general. In particular, suggestions based on pension buy-ins, buy-outs, and longevity swaps would be helpful to pension fund managers and other industry players. Current studies undertaken in African countries, such as South Africa, Kenya, Nigeria, Namibia, and Ghana, show increasing longevity in the population’s mortality, and these have direct effectsLee–Carter on longevity-bearing assets and liabilities [

12,

13,

14,

15,

16,

17]. In Ghana, both [

12] and [

15] found that population mortality was decreasing. Further, Nantwi et al.’s assessment of the longevity risk in defined benefit (DB) pension plans saw rising annuity liabilities associated with age in the Lee–Carter model [

15].

The utilization of stochastic mortality models is not new to the advanced world. These have been extensively used in research to price and adjust the valuation effects of numerous portfolios that have mortality risk measures. The Lee–Carter model [

18] has been extensively used owing to its simplification and how well it fitted the U.S. mortality rate at the time. Today, based on these models, numerous practices in advanced countries have postulated confidence intervals for mortality improvement as inclusion criteria in longevity-bearing assets and liabilities for almost all ages. These have even been used to determine the likely impact on several portfolios of annuity products, including pensions, and these serve as a guide for most plan sponsors [

18,

19,

20,

21,

22,

23,

24]. However, in most countries in Africa, little research has been carried out to study the effect of age, period, and cohort on mortality. This has been limited in particular due to data unavailability, as the usual static life tables are not strong enough to indicate the parameter effects being investigated in the stochastic models. Due to this, most research in the field only shows current advances.

This study extends the age-period effects in the population and includes extra models to determine cohort improvement as well. Furthermore, because the mortality of pension participants may differ from that of the general population, this study focused on using mortality estimates from the pension house via annual mortality reports. Empirically, this study contributes to the body of knowledge on the existence of longevity risks among pension schemes in Ghana and their possibly extended effects in the foreseeable future. Practically, this study will be highly significant to both industry players and academic researchers. Specifically, the objectives of this study are fourfold: (1) estimate mortality forecasts for pension members cumulatively using mortality models (Lee–Carter stochastic model, the Renshaw–Haberman stochastic model, the Cairns–Blake–Dowd stochastic model, and the quadratic Cairns–Blake–Dowd stochastic model); (2) to investigate the model that best fits the pensioners’ mortality data; (3) estimate the longevity risk (LR) associated with these forecasted mortality values in the pension fund, and (4) determine the economic impact of the risk (LR) on the likely annuity payments within the pensionable ages. This is highly imperative since contributions to pension funds in the country are also dwindling (see

https://www.ssnit.org.gh/news/only-11-of-workers-pay-ssnit-contribution/ accessed on 28 February 2022) (currently estimated at the beginning of 2021 to be receiving funds from only 11% of the active workforce). This coupling situation, at the moment, is more than likely exposing the Social Security and National Insurance Trust (SSNIT) to greater insolvency issues. This could make it impossible for the scheme sponsors (SSNIT) to meet their pensioner annuity obligations in the future.

3. Results and Discussion

3.1. Data

The data used for this study (pensioners’ enrollment and yearly survival numbers) were obtained from the Pension Regulatory Authority (NPRA). These were gathered and summarized into matrices of age-period deaths and exposures (numbers alive at the beginning of the periods 2010–2020). These data were from an excerpt since not all data were readily available for computing the overall pensioners mortality improvement and longevity statistics. While this is a fraction, the deaths and exposures of members were selected from the period 2010–2020 and for age brackets 40–83 years. The data also had a series of missing values for ages beyond 83 years, and these were dropped from the analysis.

3.2. Mortality Behavior and Rate Improvement in Ghana

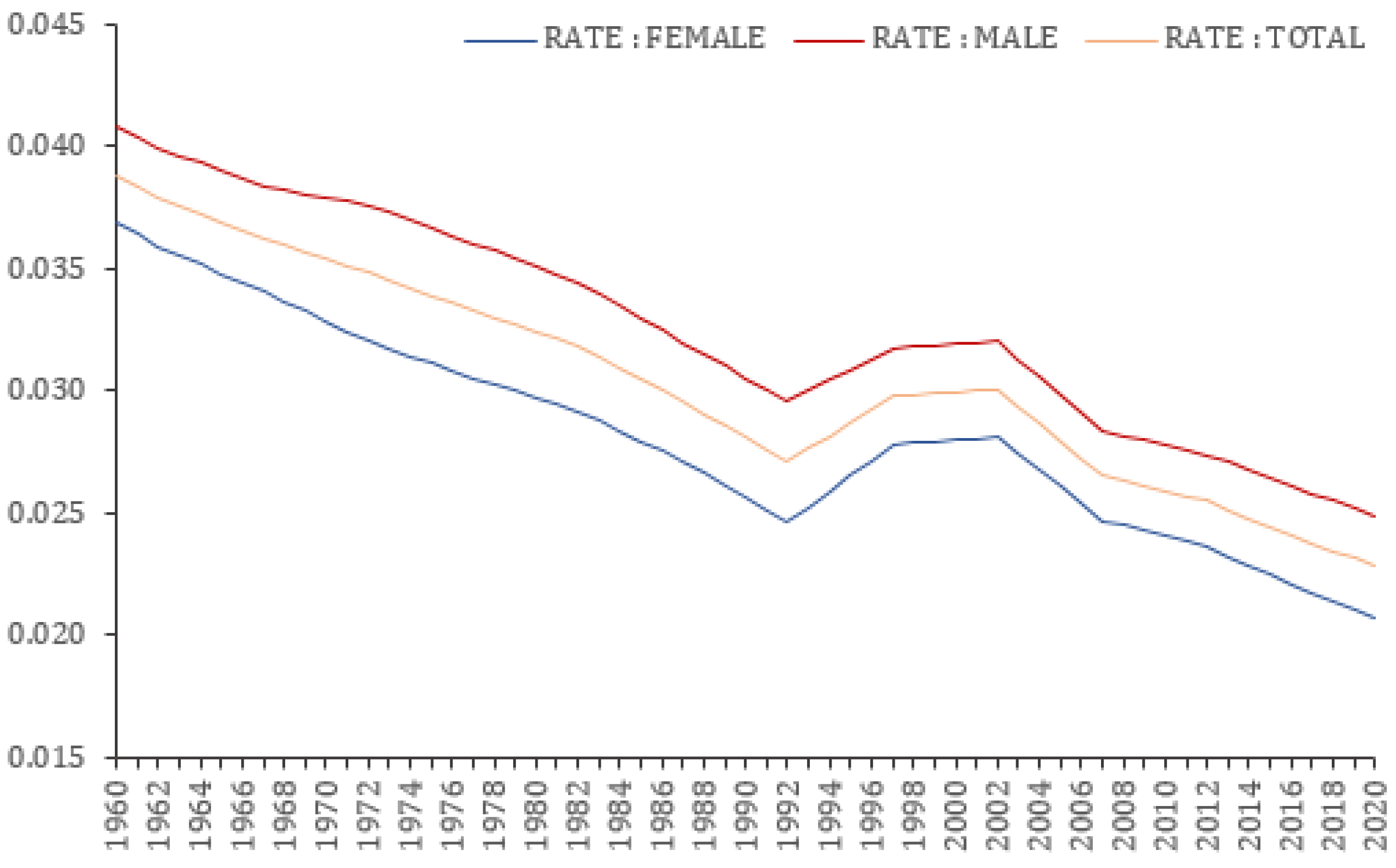

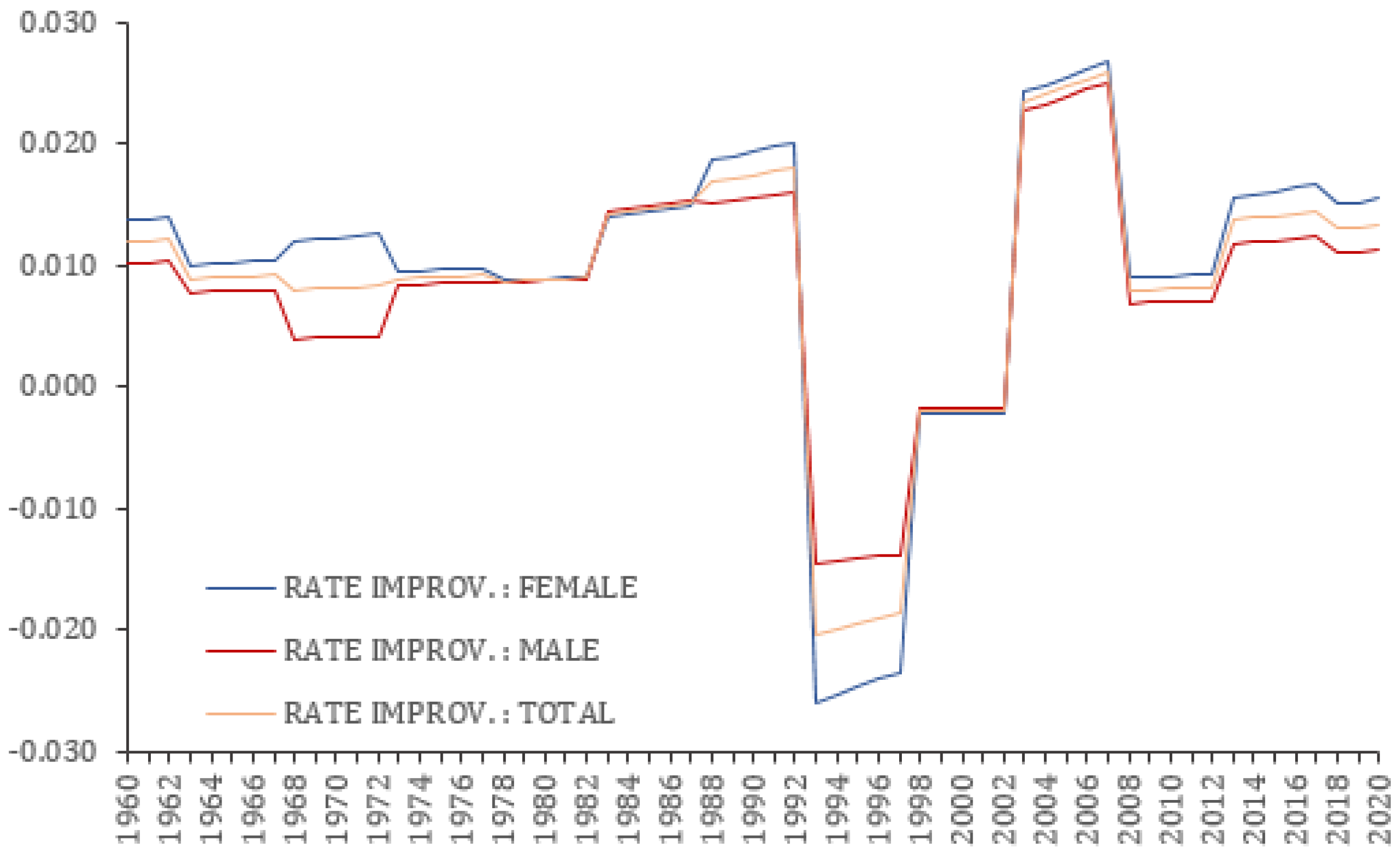

From

Figure 1, mortality from the last two decades shows more pronounced decline rates. Additionally,

Figure 2 shows the mortality improvement (i.e., female, male, and total) that has been witnessed in the Ghana adult population since 1960. It is observed that the rate of improvement has been positive over the years. Although the rate improvement has no discernible pattern other than increasing on average, the last ten years have shown positively increasing mortality rates. Furthermore, the desriptive statistics (see

Table 1) relating to female, male, and total population mortality improvement show that females have higher mortality improvement than males in Ghana (mean = 1.393% > 1.078%), with overall mortality improvement averaging 1.236% per year-on-year analysis. Half-decade mortality rates from the 2000s also showed that mortality rates have been improving for the population of both sexes but at decreasing rates.

3.3. Stochastic Mortality Models Estimation

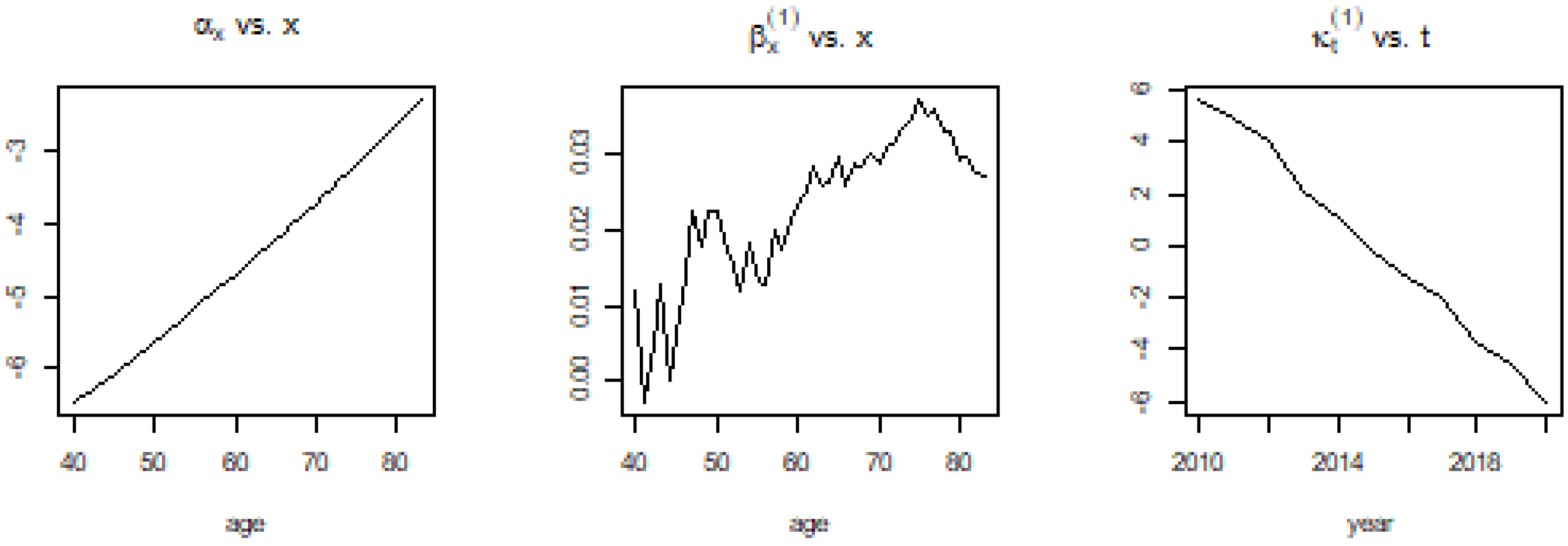

Parameters of interest in the models (, , ) show the rate improvement resulting from age-period and cohort group exposure over time. These are estimated using the R software and plotted to observe their shapes from the pensioners’ mortality data from 2010 to 2020 and within the ages of 40–83 years.

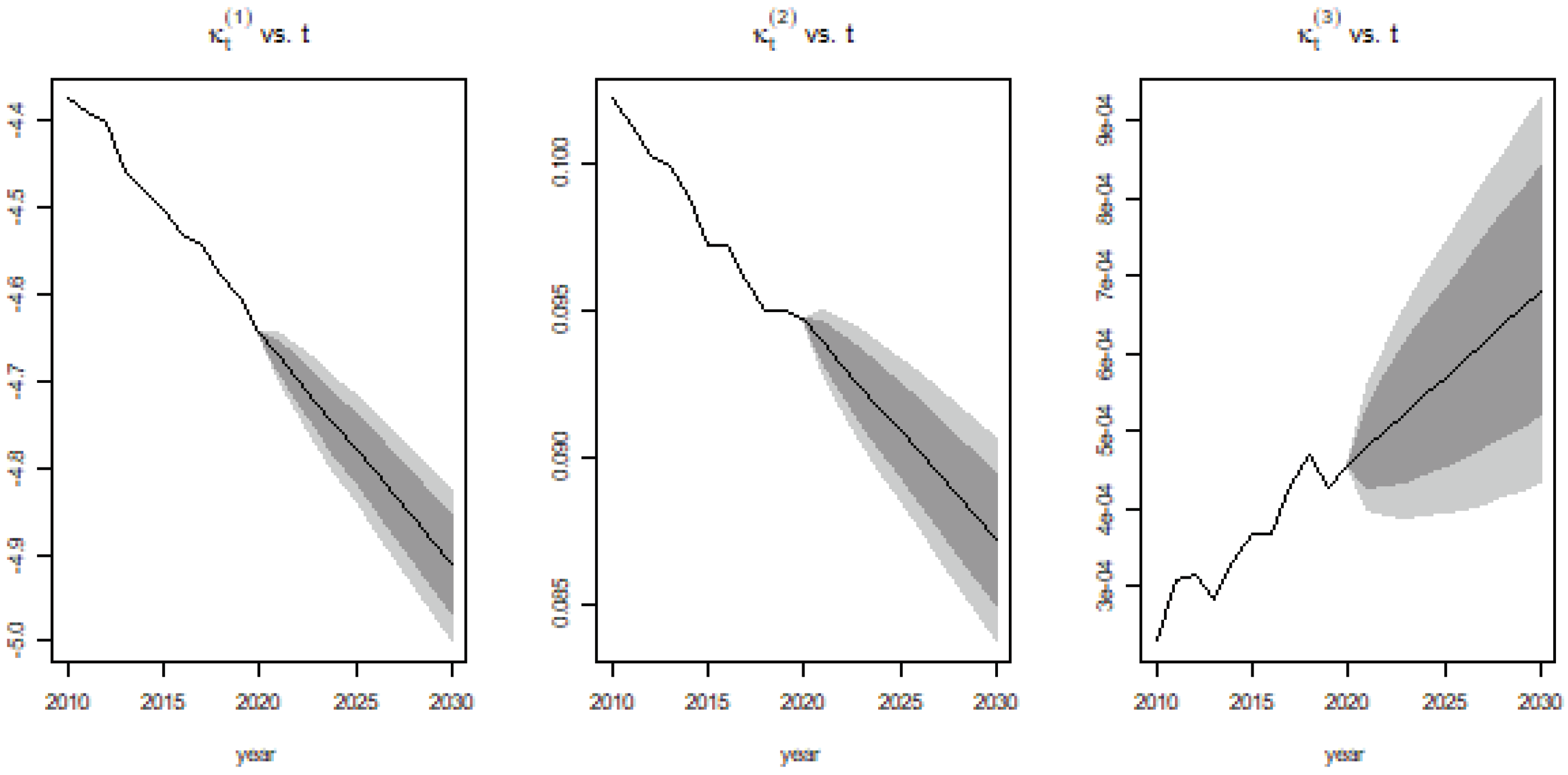

3.3.1. Lee-Carter Model

As shown in

Figure 3, the overall rate of mortality improvement (

) is slowing, indicating that mortality has been declining for a long time. This is supported by the speed coefficient (

), which rises with increasing age. This, therefore, shows that the Lee–Carter model predicts decreasing mortality rates in the future.

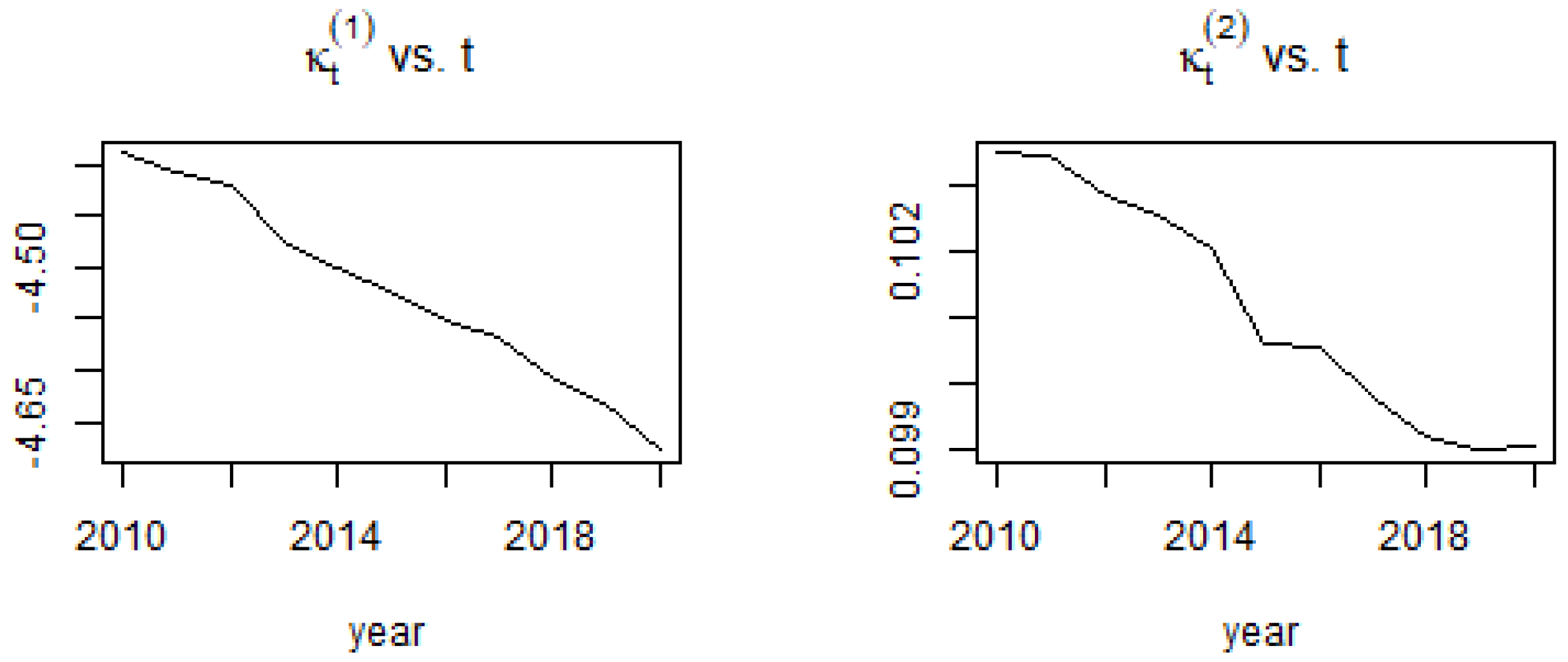

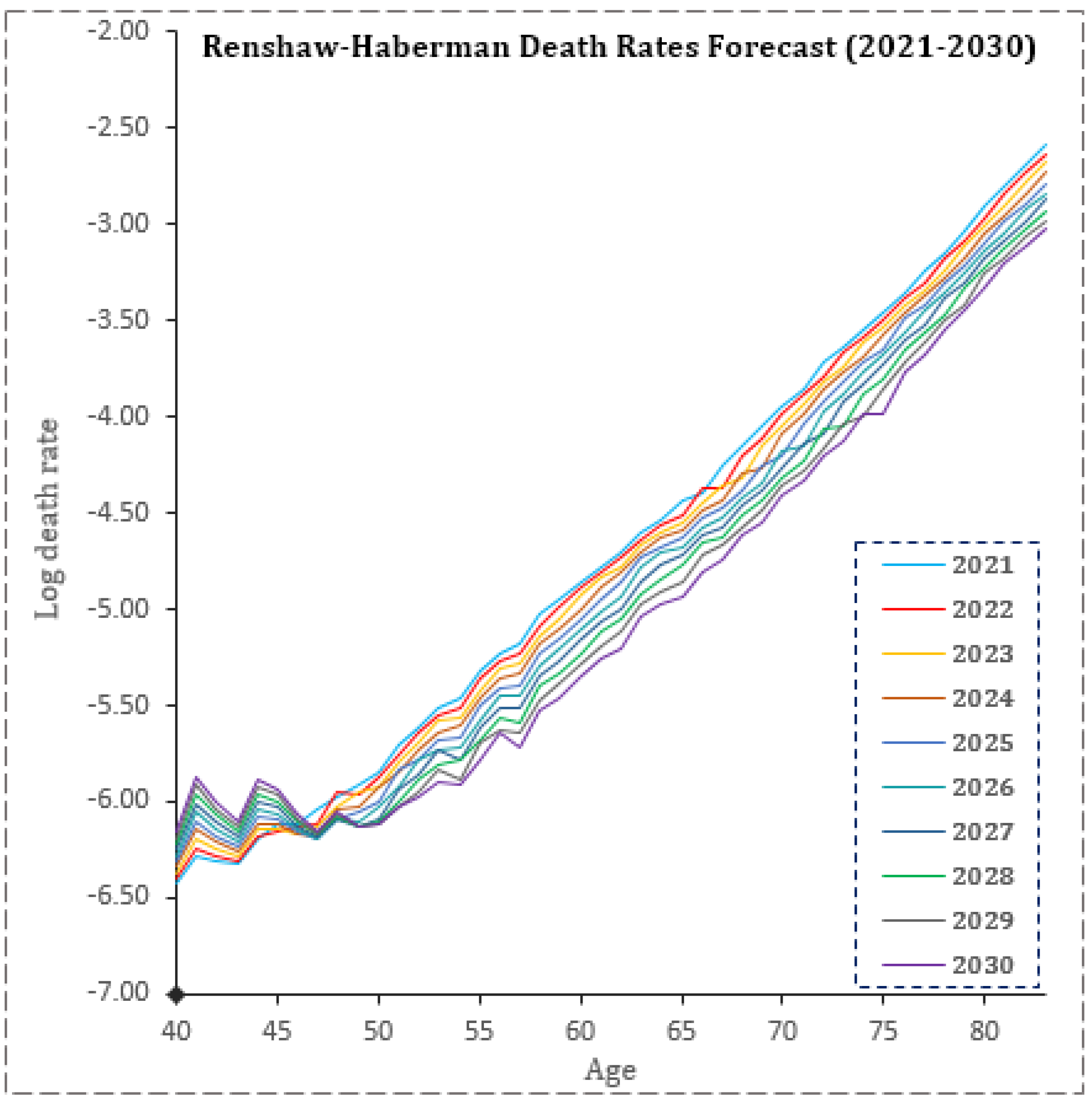

3.3.2. Renshaw–Haberman Model

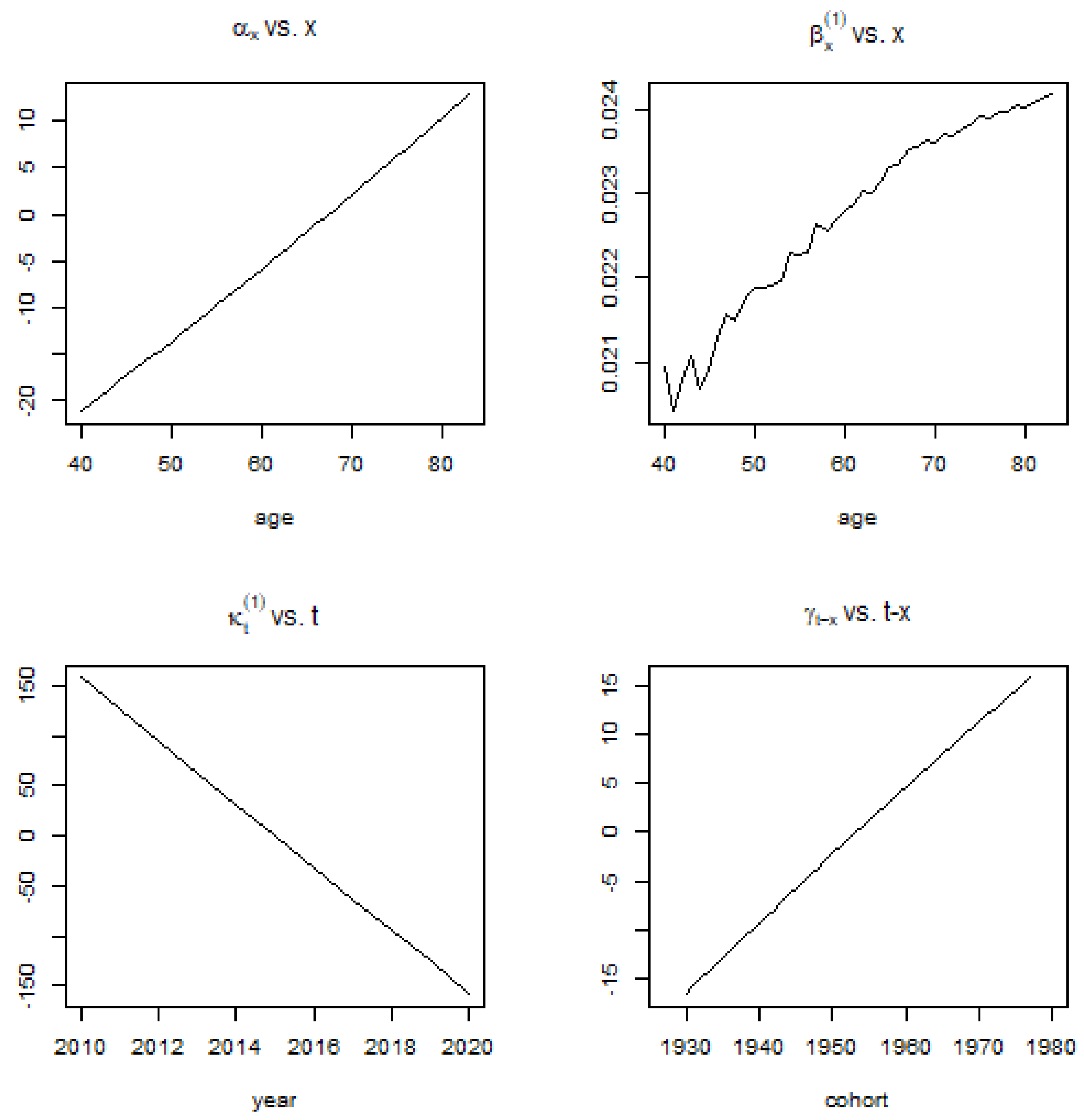

Renshaw–Haberman’s model shows similar observations for the parameters (

and

) similar to the Lee–Carter model. This demonstrates that the cohort effect is increasing over time, and as such, cohorts in later years have higher mortality improvements. In

Figure 4, the parameters of the Renshaw–Haberman Model is fitted to the Ghana Pension Population for Ages 40–83 and the Period 2010–2020.

3.3.3. Cairns-Blake-Dowd Model

Cairns et al. model shows declining mortalities for both period effects (

and

) of the pensioners’ mortality data [

26]. This is observed in

Figure 5 below.

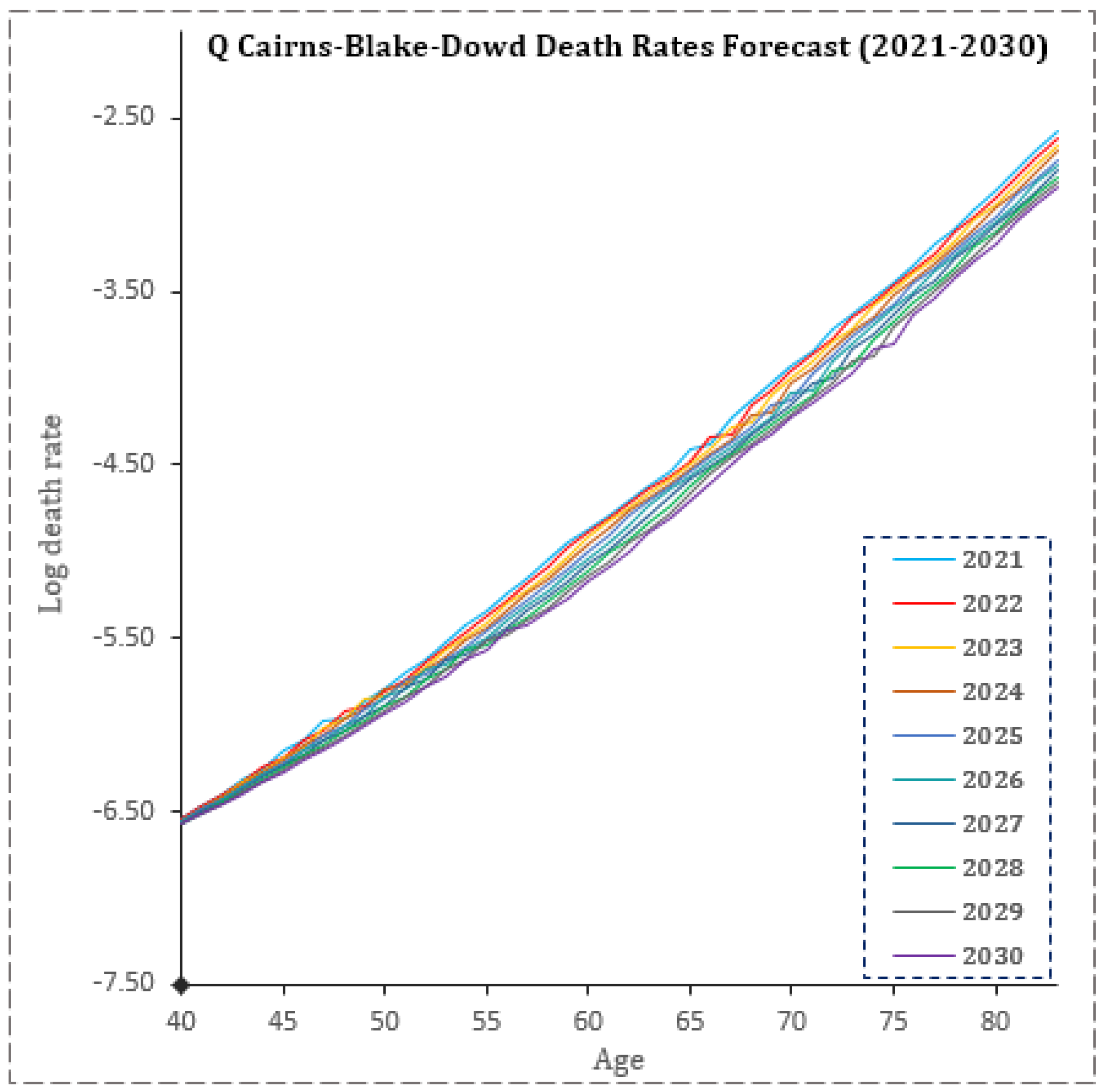

3.3.4. Quadratic Cairns–Blake–Dowd Model

Similarly, Cairns et al.’s quantitative extension of their original 2006 model shows declining period effects

and

, but the quadratic term rises over time [

28]. This indicates that the average variation in mortality relating to period t is increasing (see

Figure 6).

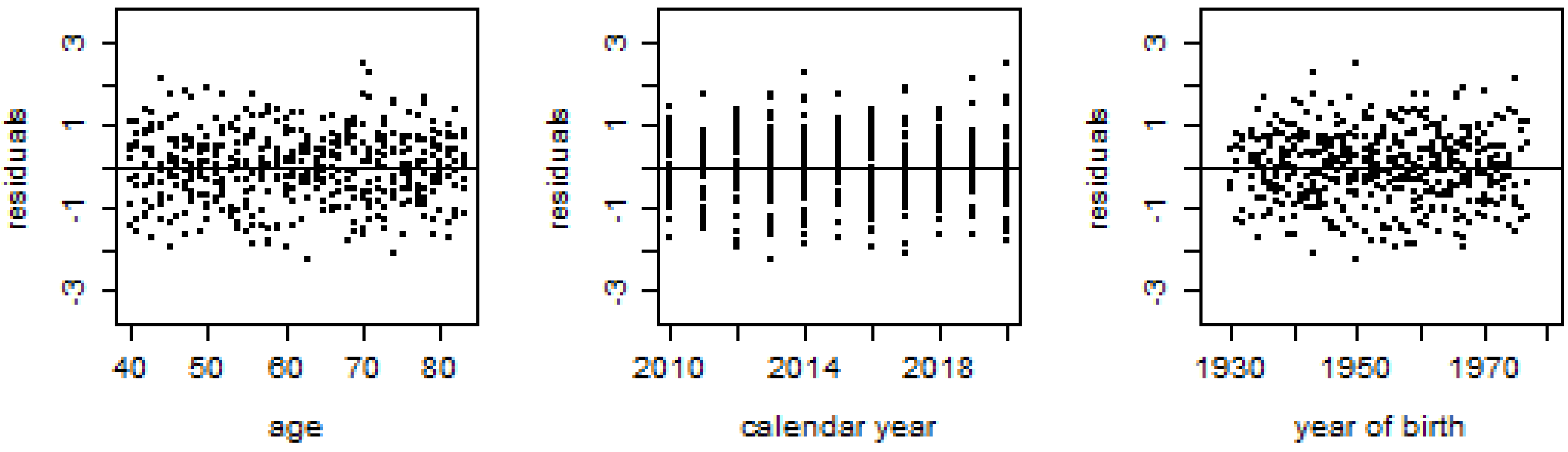

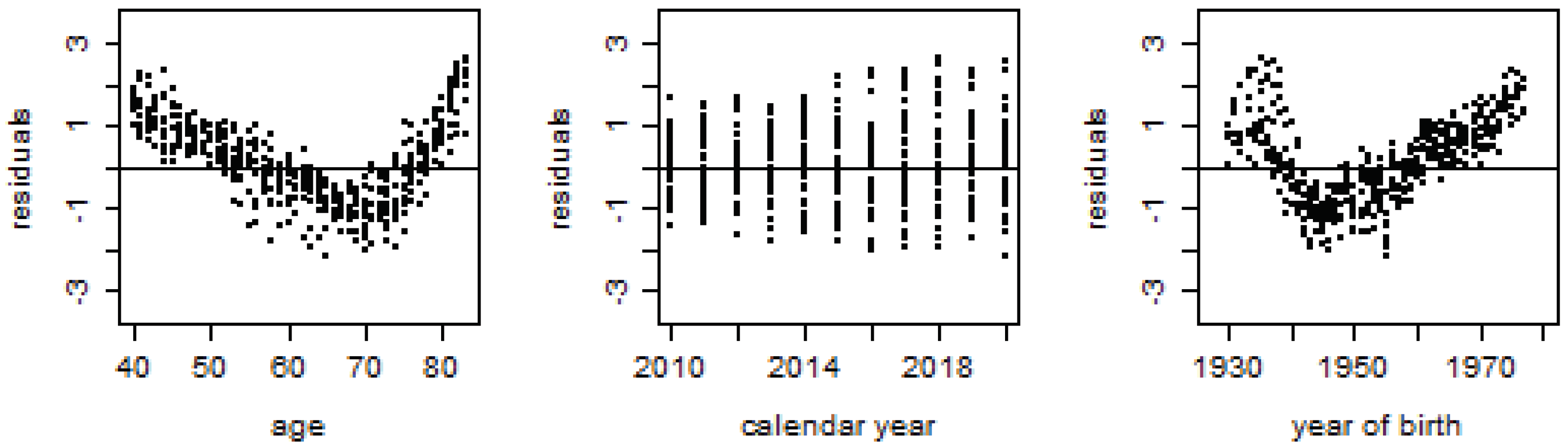

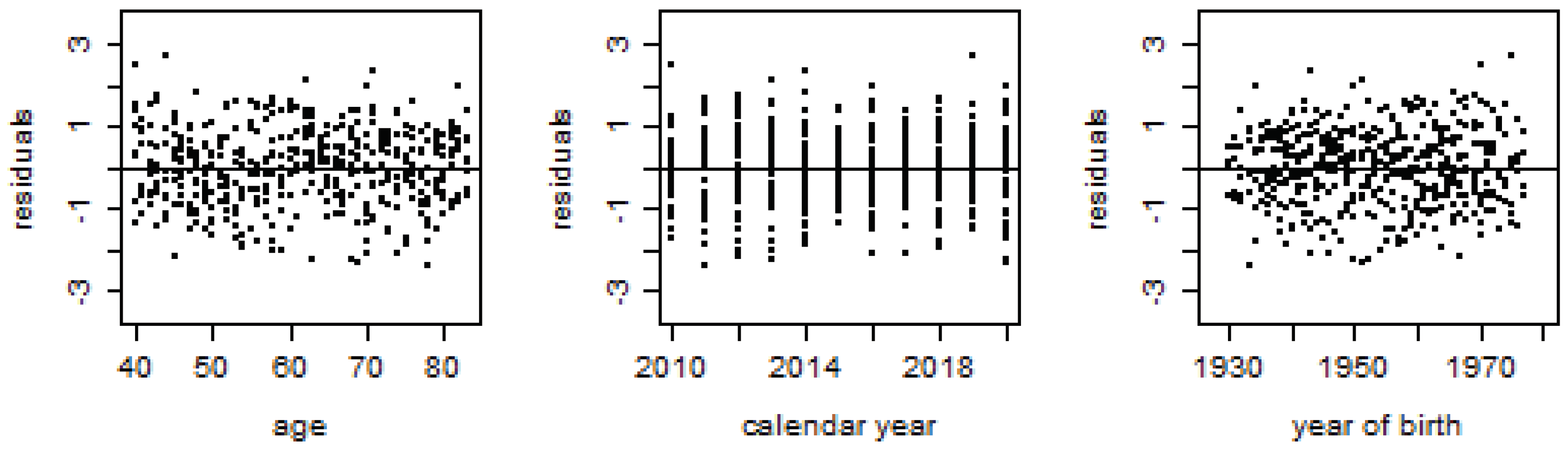

3.4. Models Goodness of Fit

The mortality models are subject to diagnostic and selection criteria to determine the most optimal fit to the pensioners’ mortality data in order to compute rate improvements. The MAFE, RMSSFE, and MAPFE are used in evaluating the mortality models.

Table 2 demonstrates that the quadratic Cairns–Blake–Dowd model exhibits the best fit to the mortality data and has the lowest MAFE, RMSFE, and MAPFE. Moreover, the residual statistics in

Figure 7,

Figure 8,

Figure 9 and

Figure 10 give further evidence to support the model selection. While the Q-CBD shows greater fitness to the mortality data, all four models were used for forecasting to observe variations around forecasted mortality rates.

Using the Diebold–Mariano test [

29], the predictive accuracy of the models are compared using the following hypotheses,

: Model 1 is not more accurate than Model 2.

: Model 1 is more accurate than Model 2.

Clearly, from

Table 3, Q-CBD = LC > CBD > RH. This is consistent with the results obtained from

Table 2.

The residual plots in

Figure 7,

Figure 8,

Figure 9 and

Figure 10 show that almost all the models fit the mortality data well except the CBD model (

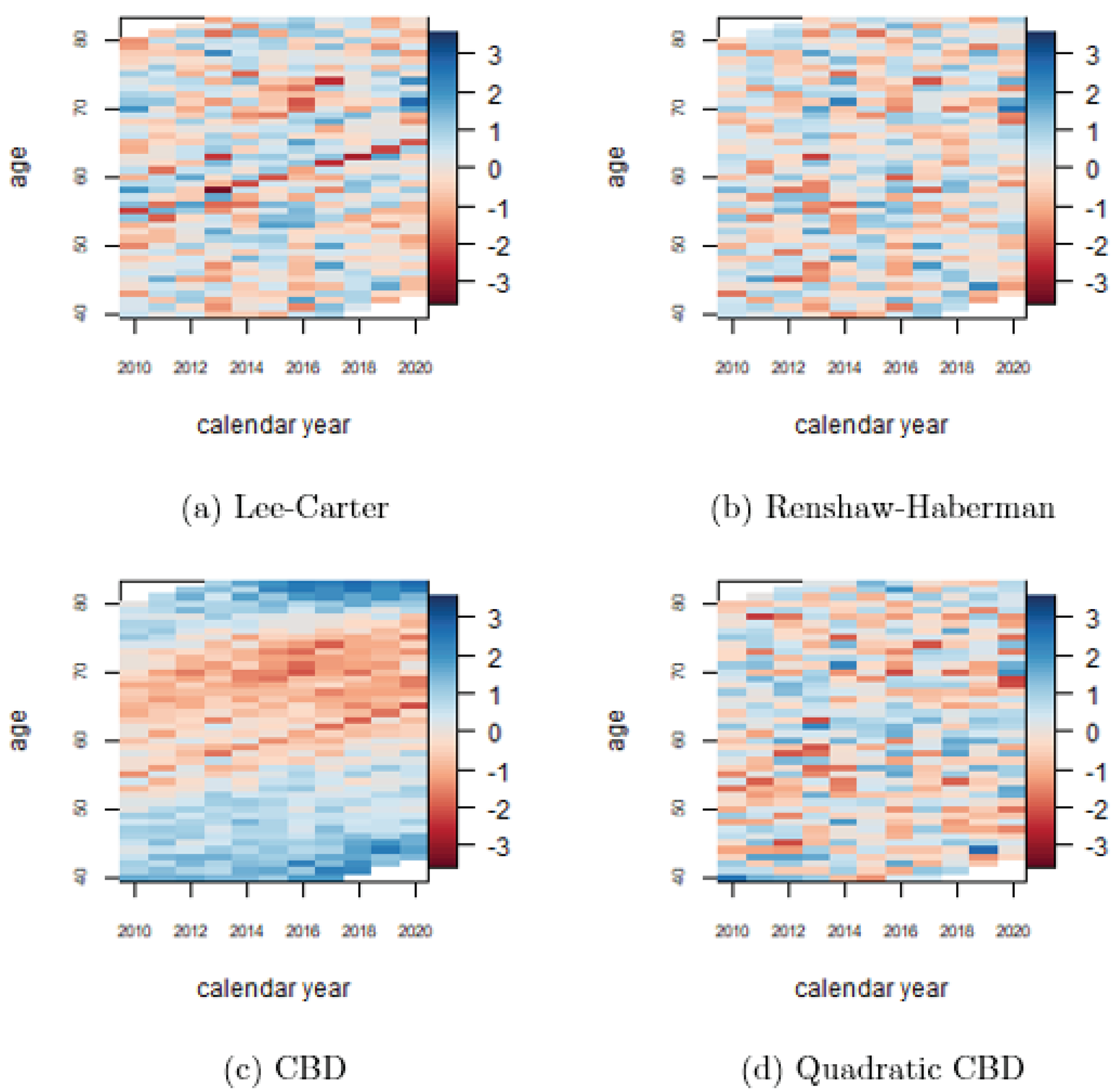

Figure 9), which shows the age and cohort effects will be appropriately modeled by some quadratic function (Q-CBD). This is further reflected in the heat-map snippet (c) in

Figure 11. This map shows a reduced amount of roughness, thus indicating a low level of randomness in residuals as compared to the LC, RH, and Q-CBD heat maps.

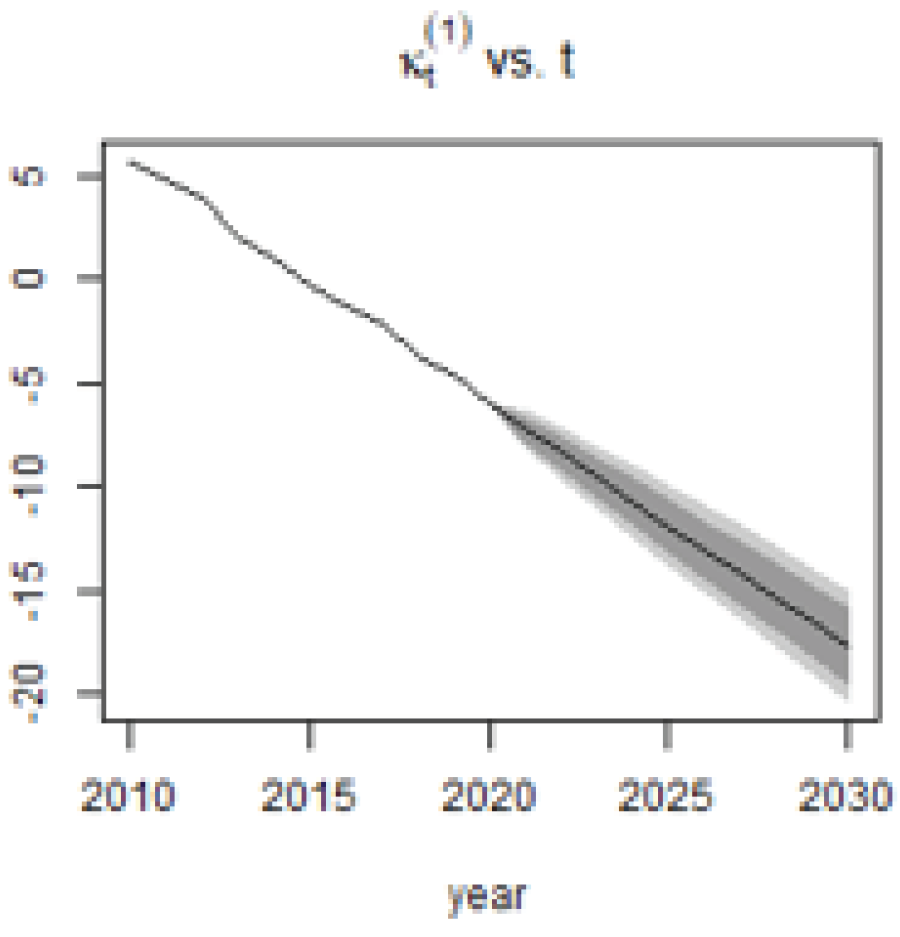

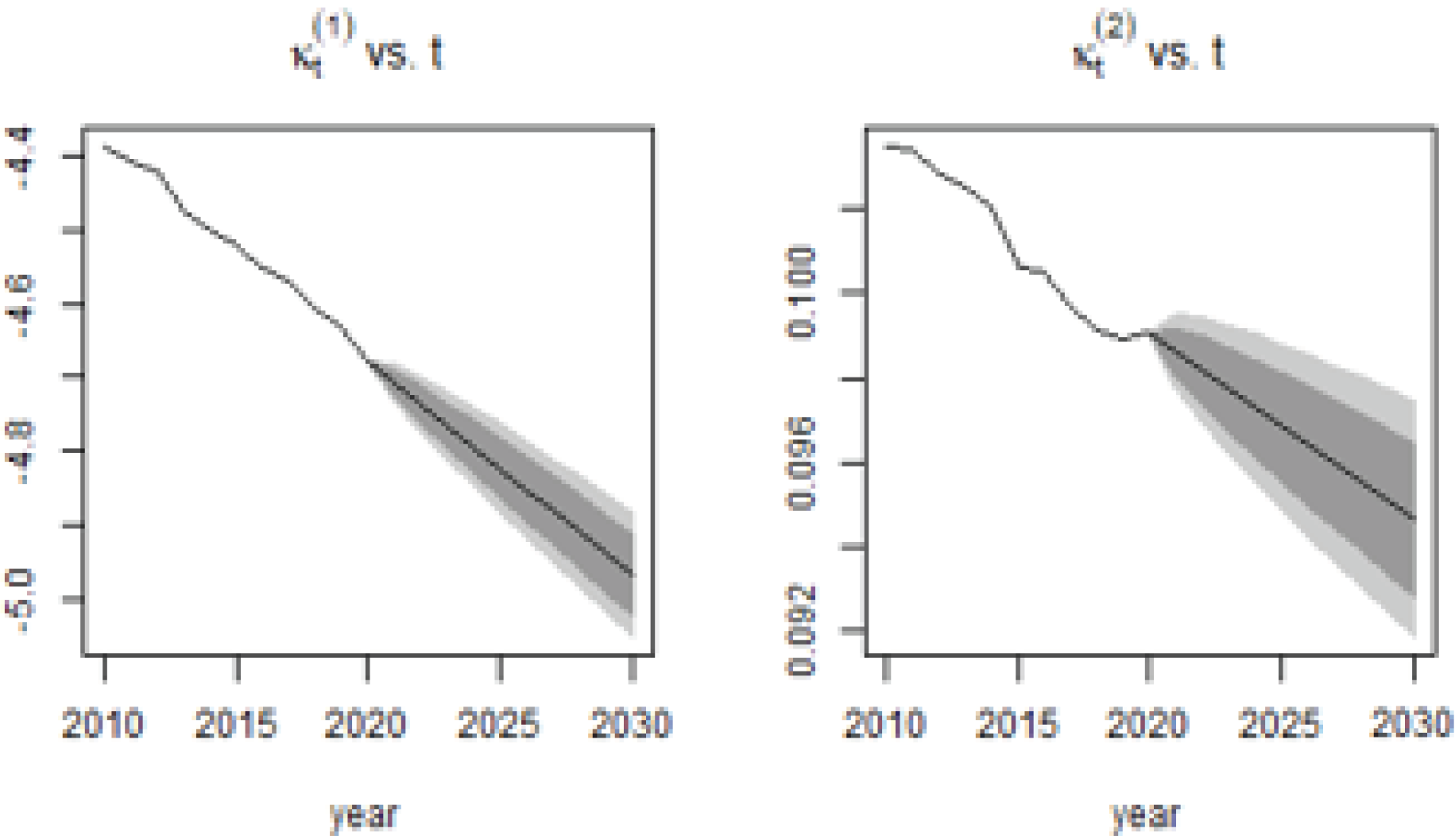

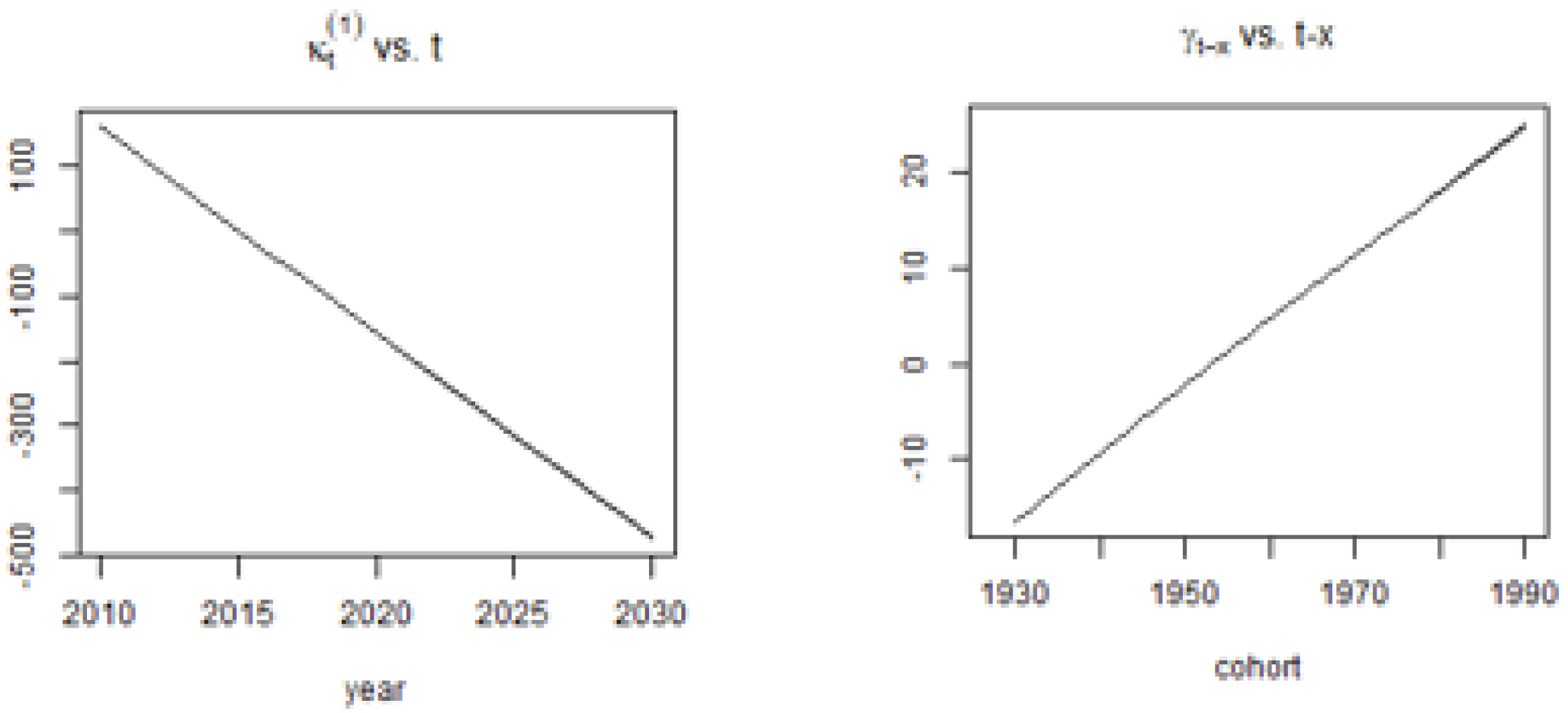

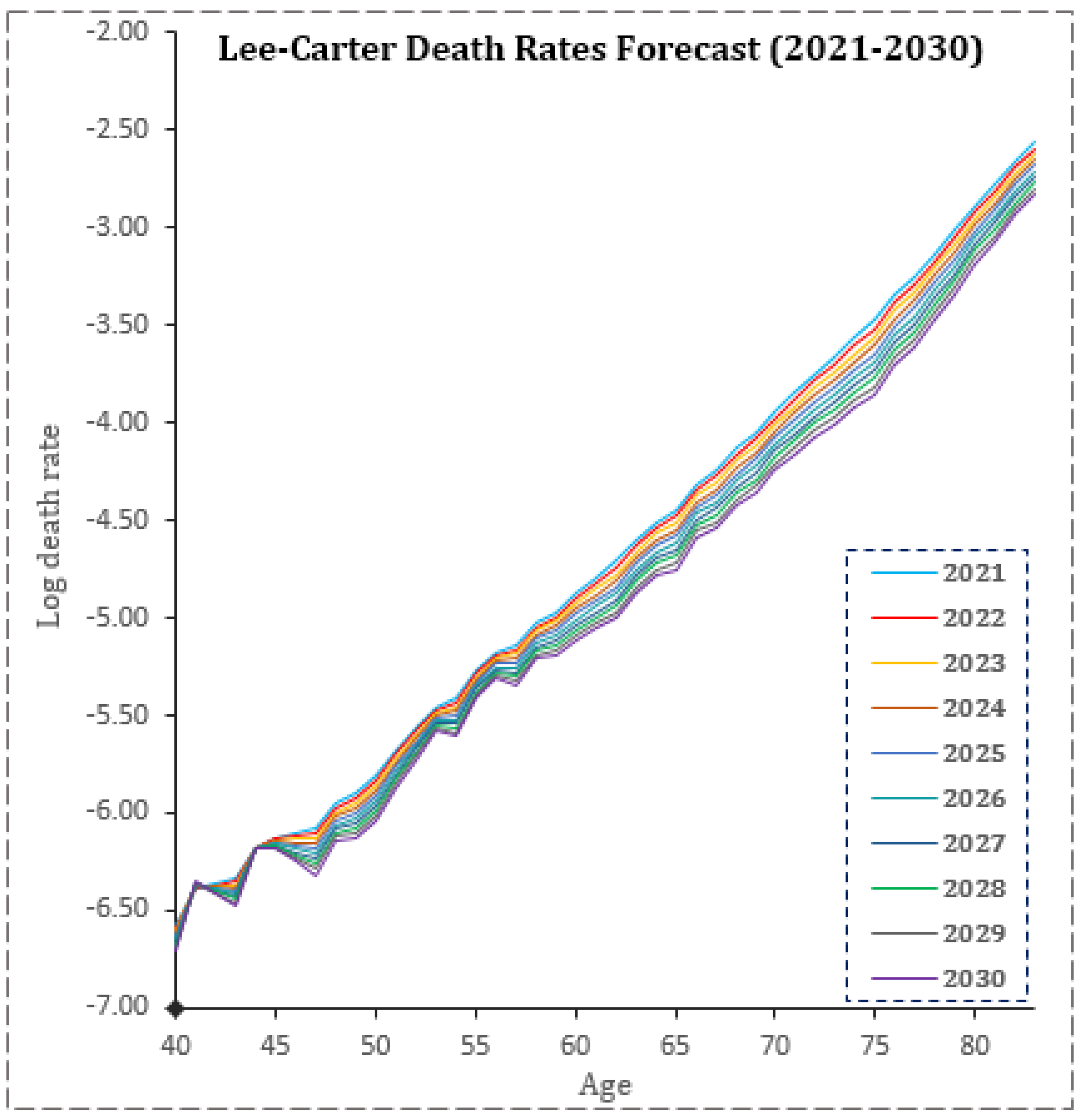

3.5. Mortality Models Rate Forecasts

From 2021 to 2030, model parameters were predicted to follow discernible paths. As seen in

Figure 12,

Figure 13,

Figure 14 and

Figure 15, all models show period and cohort effects to be, respectively, decreasing and increasing within the forecasting horizon. These models are then used to produce the rates forecast for the calendar years 2021–2030 (see

Appendix A).

3.6. Mortality Improvement

Mortality improvements associated with the four models are shown in

Table 4. The greatest risk to pension funds is from those of pensionable age who live beyond their expected lifespan. Observations from the forecasted improvement rates for pension ages 60, 65, 70, 75, and 80 show no major discernible differences between the values produced by the models. The Renshaw–Haberman model also produced the largest estimates of mortality improvement within two, five, and ten years. Additionally, the models produced increasing mortality improvements for increasing ages in the retirement frame. This should let the people who run pension plans know that their pensioners may have a higher chance of living longer than the general population. Furthermore, relying on the Q-CBD, the overall mortality improvement for ages 40–83 expected within 2021–2030 is around 2.534% (see

Table 4), which is double the national average of 1.236% (see

Table 1). This should inform pension plan sponsors that their pension participants may have a higher mortality improvement than the general population.

3.7. Present Annuity Value Factor for Pension Ages

The projected annuity value factor within 2021–2030 for ages 55, 57, 60, 62, and 65 is summarized in

Table 5,

Table 6,

Table 7 and

Table 8 for the four models. The GHS 1 annual pension cost paid GHS 1/12 monthly for pensionable ages shows no strong differences in the single annuity value for the ages 55, 57, 60, 62, and 65. This demonstrates that as members age, their mortality rate decreases, having no effect on pension costs as a result of the improved mortality rate. This is observed in

Table 5,

Table 6,

Table 7 and

Table 8, where the annuities for all models show no differences in value with increasing ages. In other words, the amount expected to be paid to a 55-year-old is the same as the amount expected to be paid to a 65-year-old within the pension period.

3.8. Discussion

As seen, the time-varying effects of age, period, and cohort are fittingly modeled by the quadrature CBD due to the curvature of age and cohort (birth year). Often, this model is an improvement over the Lee–Carter and the CBD base models, especially when curvature in age, period, or dimensional cohort effects are observed in mortality data, as seen in this study. The actuarial profession has acknowledged the fitting importance of such curve inclusion in U.S., UK, and Canadian mortality models, as well as other countries, and this has proved significantly important for pension managers in pension ratemaking [

30,

31,

32,

33]. The study’s identification of the Cairns–Blake–Dowd model with quadratic age and cohort effects for the Ghanaian pensioners’ mortality is significant in estimating mortality improvement for pensionable ages. Furthermore, all models revealed a decreasing mortality trend (increasing longevity improvement) among aging pensioners. This is in tandem with numerous studies, including [

31,

32,

34], who found that pensioners in current times live longer than anticipated and that the effects of age and cohort are hugely evident. Resulting from the decreasing nature of mortality for the pensioners, the longevity risk, as measured by the mortality improvement, was severe. This indicated that older ages are associated with greater improvements than expected, while similar observations are made in several countries, even in gender disparity models [

35]. However, a decreasing life expectancy was seen in Malaysia among pensioners and among the aging population [

36,

37].

Moreover, anticipated increases in expectancy increase the projected annuities for pensions. This study showed increasing annuities for pensioners within the pensionable age range. Furthermore, the improvement compensates for the effect of aging within the pensionable age or the retirement period. This is also in line with what has been seen in the literature, where the amount paid to annuitants increases with age due to the direct relationship between annuities and mortality improvements [

38,

39].

Furthermore, longevity risk as measured by the mortality improvement in this study showed that older ages were associated with greater mortality improvement, which was, on average, about 2.534% in the study’s forecasted horizon (2021–2030). This was more than the national mortality average of 1.236%. Furthermore, the projected annuity value within the study’s horizon showed no significant differences in value for pension ages 55, 57, 60, 62 and 65 years, thus indicating that the improvement seems to diminish the effect of increasing age within the retirement period.

4. Conclusions and Policy Recommendation

In this paper, we estimate the longevity risk associated with Ghana’s pension scheme and determine its possible impact on the sponsor’s liability over time. Using different stochastic mortality models (Lee–Carter, Renshaw–Haberman, Cairns–Blake–Dowd, and Quadratic Cairns–Blake–Dowd), we forecast the mortality improvements between 2021 and 2030. In the analysis, the Lee–Carter, Renshaw–Haberman, and Cairns–Blake–Dowd models predicted a decreasing trend in mortality rate for pensioners. This meant that pensioners’ ages did not seem to predict an increasing mortality rate as expected, and all mortality improvement parameters were trending downward within the study’s forecasted horizon (2021–2030). Owing to this, the forecasted mortality rates for pension participants are expected to decrease further, resulting in serious longevity risk for the pension scheme in the next ten years. The longevity risk, as measured by the mortality improvement, showed that older ages are associated with greater mortality improvement, which averages about 2.534% in the study’s forecasted horizon (2021–2030). This is more than the national mortality average of 1.236%. Hence, in the next ten years, the notion of older people dying faster among the pension participants may be diminished since, even at such ages, participants have greater chances of surviving the next period than even those who are young. Furthermore, the projected annuity value within the study’s horizon showed no significant differences in value for pension ages of 55, 57, 60, 62, and 65 years, indicating that the improvement seems to diminish the effect of increasing ages within the retirement period. Owing to these observations, the impact on the scheme was direct. The present annuity value showed that the monies that are expected to be paid to pensioners who have already received about five years of pension are no different from those who just went on the pension. This shows the canceling effect of longevity on ages within the retirement period.

Based on the conclusion, it is recommended that pension plan sponsors in Ghana look to explore longevity-bearing assets to tackle the effect of the longevity improvement observed among pension participants. This should seek to immunize the canceling effect of mortality improvement associated with increasing ages within the retirement period. Furthermore, other than general longevity risks that affect pension schemes, there exist different risk features such as socioeconomic associations [

40] and asymmetry in mortality [

41] that also affect the scheme. In future studies, we will extend this paper to include these other risk features. Future studies will also compare the stochastic mortality models used in this paper to Bayesian formalization, such as that contained in the paper of Giudici et al. [

42].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}