Information Effect of Fintech and Digital Finance on Financial Inclusion during the COVID-19 Pandemic: Global Evidence

Abstract

:1. Introduction

2. Literature Review

3. Methodology

4. Empirical Results

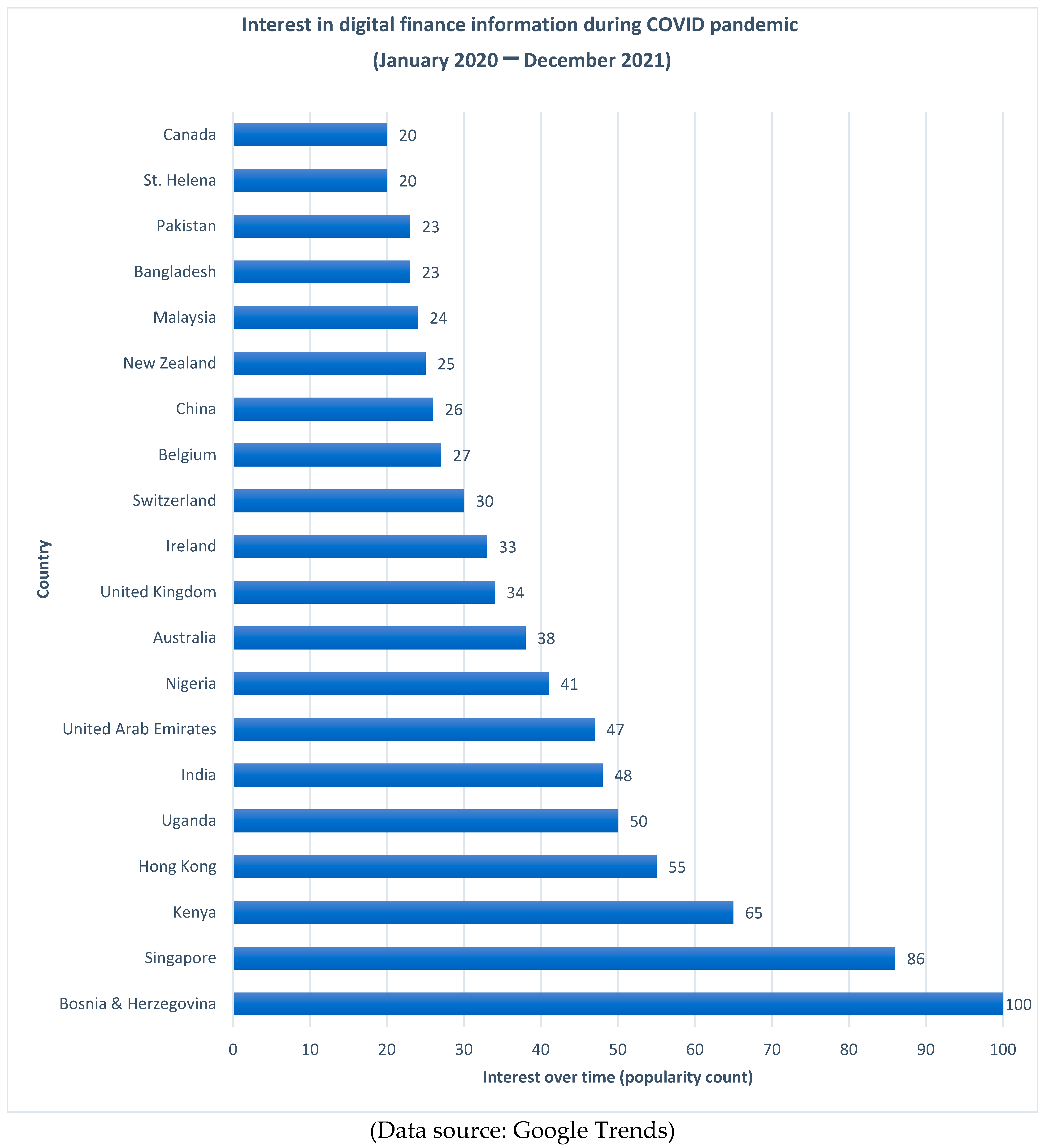

4.1. Graphical Analysis of Data Trends

4.2. Correlation Analysis

4.3. Granger Causality

4.3.1. Unit Root Test

4.3.2. Granger Causality

4.3.3. Univariate OLS Regression as an Alternative Test for Causation Based on R-Squared

4.3.4. Univariate GMM Regression as an Alternative Test for Causation Based on R-Squared

4.4. Effect of Interest in Digital Finance and Fintech Information on Interest in Financial Inclusion Information

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

| Google Trends Search Category | Countries and Regions |

| Web search | Zimbabwe, Eswatini, Rwanda, Uganda, Zambia, Fiji, Nigeria, Ghana, Ethiopia, Tanzania, Kenya, India, Cameroon, Nepal, Bangladesh, Mauritius, Cambodia, Singapore, South Africa, Philippines, Pakistan, Lebanon, Sri Lanka, Jordan, Malaysia, Bolivia, Egypt, Hong Kong, United Arab Emirates, United Kingdom, Indonesia, Switzerland, Australia, South Korea, United States, Thailand, Netherlands, Canada, Vietnam, Saudi Arabia, Mexico, Norway, Germany, France, Spain, Japan, Russia, Iran, Brazil, Marshall Islands, Micronesia, Tonga, Vanuatu, Eritrea, Solomon Islands, Samoa, American Samoa, Lesotho, Papua New Guinea, Palau, Sierra Leone, Malawi, Bhutan, Guinea-Bissau, Greenland, Burundi, Seychelles, The Gambia, Mayotte, Liberia, Botswana, St. Vincent and the Grenadines, Namibia, Timor-Leste, Grenada, Suriname, St. Kitts and Nevis, Belize, Afghanistan, Senegal, Somalia, South Sudan, Dominica, Mozambique, Myanmar (Burma), Haiti, Djibouti, Barbados, St. Helena, Côte D’Ivoire, Jamaica, Guyana, Maldives, Cayman Islands, Congo—Brazzaville, Curaçao, Benin, Luxembourg, Gabon, French Guiana, Mongolia, St. Lucia, Togo, Macao, Tajikistan, Brunei, Burkina Faso, Mali, Angola, Sudan, Bahrain, Niger, Madagascar, Laos, Jersey, Tunisia, Albania, Trinidad and Tobago, Armenia, The Bahamas, Palestine, Qatar, Oman, Turkmenistan, Congo—Kinshasa, Honduras, Uzbekistan, Kuwait, Belgium, Bosnia and Herzegovina, Ireland, Cyprus, Moldova, Georgia, Yemen, Iraq, Kyrgyzstan, Peru, Malta, Morocco, Nicaragua, El Salvador, Algeria, Paraguay, Azerbaijan, New Zealand, Libya, Uruguay, Guatemala, Ecuador, Taiwan, Estonia, China, Denmark, Panama, Colombia, North Macedonia, Costa Rica, Portugal, Greece, Croatia, Austria, Sweden, Bulgaria, Syria, Dominican Republic, Belarus, Israel, Hungary, Kazakhstan, Lithuania, Finland, Argentina, Romania, Turkey, Italy, Czechia, Chile, Ukraine, Poland, Venezuela, Slovakia, Serbia, Aruba, Anguilla, Andorra, Antarctica, French Southern Territories, Antigua and Barbuda, Caribbean Netherlands, St. Barts, Bermuda, Bouvet Island, Central African Republic, Cocos (Keeling) Islands, Cook Islands, Comoros, Cape Verde, Cuba, Christmas Island, Western Sahara, Falkland Islands (Islas Malvinas), Faroe Islands, Guernsey, Gibraltar, Guinea, Guadeloupe, Equatorial Guinea, Guam, Heard and McDonald Islands, Isle of Man, British Indian Ocean Territory, Iceland, Kiribati, Liechtenstein, Latvia, St. Martin, Monaco, Montenegro, Northern Mariana Islands, Mauritania, Montserrat, Martinique, New Caledonia, Norfolk Island, Niue, Nauru, Pitcairn Islands, Puerto Rico, French Polynesia, South Georgia and South Sandwich Islands, Svalbard and Jan Mayen, San Marino, St. Pierre and Miquelon, Sao Tome and Principe, Slovenia, Sint Maarten, Turks and Caicos Islands, Chad, Tokelau, Tuvalu, U.S. Outlying Islands, Vatican City, British Virgin Islands, U.S. Virgin Islands, Wallis and Futuna, Kosovo. |

References

- Demirgüç-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. Measuring Financial Inclusion, and the Fintech Revolution. In The Global Findex Database 2017; World Bank Group: Washington, DC, USA, 2017. [Google Scholar]

- Fintel, D.; Orthofer, A. Wealth inequality and financial inclusion: Evidence from South African tax and survey records. Econ. Model. 2020, 91, 568–578. [Google Scholar] [CrossRef]

- Ozili, P.K.; Mhlanga, D. Why is financial inclusion so popular? An analysis of development buzzwords. J. Int. Dev. 2024, 36, 231–253. [Google Scholar] [CrossRef]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Thomas, H.; Hedrick-Wong, Y. How digital finance and fintech can improve financial inclusion. In Inclusive Growth: The Global Challenges of Social Inequality and Financial Inclusion; Emerald Publishing Limited: Bingley, UK, 2019; pp. 27–41. [Google Scholar]

- Singh, S.; Sahni, M.M.; Kovid, R.K. What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model. Manag. Decis. 2020, 58, 1675–1697. [Google Scholar] [CrossRef]

- Chong, T.-P.; Choo, K.-S.W.; Yip, Y.-S.; Chan, P.-Y.; The, H.-L.J.; Ng, S.-S. An adoption of fintech service in Malaysia. South East Asia J. Contemp. Bus. 2019, 18, 134–147. [Google Scholar]

- Ozili, P.K. Contesting digital finance for the poor. Digit. Policy Regul. Gov. 2020, 22, 135–151. [Google Scholar]

- Yan, C.; Siddik, A.B.; Akter, N.; Dong, Q. Factors influencing the adoption intention of using mobile financial service during the COVID-19 pandemic: The role of FinTech. Environ. Sci. Pollut. Res. 2021, 30, 61271–61289. [Google Scholar] [CrossRef]

- Ozili, P.K.; Arun, T. Spillover of COVID-19: Impact on the Global Economy. In Managing Inflation and Supply Chain Disruptions in the Global Economy; IGI Global: Hershey, PA, USA, 2023; pp. 41–61. [Google Scholar]

- Vargo, D.; Zhu, L.; Benwell, B.; Yan, Z. Digital technology use during COVID-19 pandemic: A rapid review. Hum. Behav. Emerg. Technol. 2021, 3, 13–24. [Google Scholar] [CrossRef]

- Papouli, E.; Chatzifotiou, S.; Tsairidis, C. The use of digital technology at home during the COVID-19 outbreak: Views of social work students in Greece. Soc. Work. Educ. 2020, 39, 1107–1115. [Google Scholar] [CrossRef]

- Kanungo, R.P.; Gupta, S. Financial inclusion through digitalisation of services for well-being. Technol. Forecast. Soc. Chang. 2021, 167, 120721. [Google Scholar] [CrossRef]

- Fu, J.; Mishra, M. Fintech in the time of COVID-19: Technological adoption during crises. J. Financ. Intermediat. 2022, 50, 100945. [Google Scholar] [CrossRef]

- Shafeeq, M.; Beg, S. A study to assess the impact of COVID-19 pandemic on digital financial services and digital financial inclusion in India. Afr. J. Account. Audit. Financ. 2021, 7, 326–345. [Google Scholar] [CrossRef]

- Sahay, M.R.; von Allmen, M.U.E.; Lahreche, M.A.; Khera, P.; Ogawa, M.S.; Bazarbash, M.; Beaton, M.K. The Promise of Fintech: Financial Inclusion in the Post COVID-19 Era; International Monetary Fund: Washington, DC, USA, 2020. [Google Scholar]

- Arner, D.W.; Barberis, J.N.; Walker, J.; Buckley, R.P.; Dahdal, A.M.; Zetzsche, D.A. Digital Finance & the COVID-19 Crisis; University of Hong Kong Faculty of Law Research Paper; Hong Kong University: Hong Kong, 2020; p. 17. [Google Scholar]

- Al Nawayseh, M.K. Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of Fintech applications. J. Open Innov. Technol. Mark. Complex. 2020, 6, 153. [Google Scholar] [CrossRef]

- Senyo, P.K.; Osabutey, E.L.; Kan, K.A.S. Pathways to improving financial inclusion through mobile money: A fuzzy set qualitative comparative analysis. Inf. Technol. People 2021, 34, 1997–2017. [Google Scholar] [CrossRef]

- Philippon, T. On fintech and financial inclusion. Natl. Bur. Econ. Res. 2019, w26330. [Google Scholar] [CrossRef]

- Beck, T. Fintech, and Financial Inclusion: Opportunities and Pitfalls; ADBI Working Paper Series; Asian Development Bank Institute (ADBI): Tokyo, Japan, 2020; p. 1165. [Google Scholar]

- Djoufouet, W.F.; Pondie, T.M. Impacts of Fintech on Financial Inclusion: The Case of Sub-Saharan Africa. Copernic. J. Financ. Account. 2022, 11, 69–88. [Google Scholar] [CrossRef]

- Alber, N.; Dabour, M. The dynamic relationship between FinTech and social distancing under COVID-19 pandemic: Digital payments evidence. Int. J. Econ. Financ. 2020, 12, 11. [Google Scholar] [CrossRef]

- Fu, J.; Mishra, M. The Global Impact of COVID-19 on FinTech Adoption; Swiss Finance Institute Research Paper; Swiss Finance Institute: Zürich, Switzerland , 2020; pp. 20–38. [Google Scholar]

- Ahmad, N.W.; Bahari, N.; Ripain, N. COVID-19 Outbreak: The Influence on Digital Finance and Financial Inclusion. In Proceedings of the International Conference on Syariah & Law, Online, 6 April 2021; pp. 160–166. [Google Scholar]

- Dluhopolskyi, O.; Pakhnenko, O.; Lyeonov, S.; Semenog, A.; Artyukhova, N.; Cholewa-Wiktor, M.; Jastrzębski, W. Digital financial inclusion: COVID-19 impacts and opportunities. Sustainability 2023, 15, 2383. [Google Scholar] [CrossRef]

- Banna, H.; Hassan, M.K.; Ahmad, R.; Alam, M.R. Islamic banking stability amidst the COVID-19 pandemic: The role of digital financial inclusion. Int. J. Islam. Middle East. Financ. Manag. 2022, 15, 310–330. [Google Scholar] [CrossRef]

- Vasenska, I.; Dimitrov, P.; Koyundzhiyska-Davidkova, B.; Krastev, V.; Durana, P.; Poulaki, I. Financial transactions using Fintech during the COVID-19 crisis in Bulgaria. Risks 2021, 9, 48. [Google Scholar] [CrossRef]

- Abu Daqar, M.; Constantinovits, M.; Arqawi, S.; Daragmeh, A. The role of Fintech in predicting the spread of COVID-19. Banks Bank Syst. 2021, 16, 1–16. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Period | Interest in Financial Inclusion Information | Interest in Fintech Information | Interest in Digital Finance Information |

|---|---|---|---|

| (Interest over Time, Scale: 0–100) | (Interest over Time, Scale: 0–100) | (Interest over Time, Scale: 0–100) | |

| 2020-January | 42 | 85 | 72 |

| 2020-February | 42 | 86 | 71 |

| 2020-March | 35 | 64 | 77 |

| 2020-April | 24 | 61 | 65 |

| 2020-May | 32 | 67 | 93 |

| 2020-June | 34 | 71 | 91 |

| 2020-July | 31 | 74 | 83 |

| 2020-August | 34 | 70 | 79 |

| 2020-September | 38 | 81 | 94 |

| 2020-October | 31 | 67 | 80 |

| 2020-November | 32 | 67 | 70 |

| 2020-December | 36 | 65 | 71 |

| 2021-January | 44 | 82 | 71 |

| 2021-February | 46 | 86 | 96 |

| 2021-March | 39 | 88 | 92 |

| 2021-April | 35 | 77 | 91 |

| 2021-May | 35 | 75 | 91 |

| 2021-June | 34 | 79 | 89 |

| 2021-July | 43 | 75 | 78 |

| 2021-August | 39 | 87 | 100 |

| 2021-September | 42 | 86 | 92 |

| 2021-October | 36 | 79 | 81 |

| 2021-November | 34 | 100 | 62 |

| 2021-December | 35 | 76 | 66 |

| Statistic: | |||

| Mean | 36 | 77 | 81 |

| Median | 35 | 76.5 | 80.5 |

| Maximum | 46 | 100 | 100 |

| Minimum | 24 | 61 | 62 |

| Std. Dev. | 5.05 | 9.5 | 11.2 |

| Observations | 24 | 24 | 24 |

| Variable | Interest in Financial Inclusion Information | Interest in Digital Finance Information | Interest in Fintech Information |

|---|---|---|---|

| Interest in financial inclusion information | 1.000 | ||

| – | |||

| – | |||

| Interest in digital finance information | 0.232 | 1.000 | |

| (1.12) | – | ||

| ((0.27)) | – | ||

| Interest in Fintech information | 0.609 *** | 0.139 | 1.000 |

| (3.60) | (0.66) | – | |

| ((0.00)) | ((0.52)) | – |

| Null Hypothesis: “Interest in financial inclusion information” time series data have a unit root | ||||

| Exogenous: Constant | ||||

| Lag Length: 0 (Automatic—based on SIC, maxlag = 5) | ||||

| t-Statistic | Prob. | |||

| Augmented Dickey–Fuller test statistic | −2.939 | 0.056 | ||

| Test critical values: | 1% level | −3.753 | ||

| 5% level | −2.998 | |||

| 10% level | −2.639 | |||

| Null Hypothesis: “Interest in digital finance information” time series data have a unit root | ||||

| Exogenous: Constant | ||||

| Lag Length: 0 (Automatic—based on SIC, maxlag = 5) | ||||

| t-Statistic | Prob. | |||

| Augmented Dickey–Fuller test statistic | −2.947 | 0.055 | ||

| Test critical values: | 1% level | −3.752 | ||

| 5% level | −2.998 | |||

| 10% level | −2.638 | |||

| Null Hypothesis: “Interest in Fintech information” time series data have a unit root | ||||

| Exogenous: Constant | ||||

| Lag Length: 0 (Automatic—based on SIC, maxlag = 5) | ||||

| t-Statistic | Prob. | |||

| Augmented Dickey–Fuller test statistic | −3.178 | 0.035 | ||

| Test critical values: | 1% level | −3.752 | ||

| 5% level | −2.998 | |||

| 10% level | −2.638 | |||

| Time Series Data | t-Statistic | p-Value | Decision Rule (If p > 0.5, Data Have a Unit Root and Are Non-Stationary) | Remark |

|---|---|---|---|---|

| Interest in financial inclusion information | −2.947 | 0.056 | p > 0.05; the data have a unit root | Data are non-stationary |

| Interest in digital finance information | −2.947 | 0.055 | p > 0.05; the data have a unit root | Data are non-stationary |

| Interest in Fintech information | −3.178 | 0.035 | p < 0.05; the data do not have a unit root | Data are stationary |

| Pairwise Granger Causality Tests | |||

| Sample: 2020-Jan–2021-Dec | |||

| Lags: 2 | |||

| Null Hypothesis: | Obs. | F-Statistic | Prob. |

| Interest in Fintech information does not Granger cause d (interest in financial inclusion information) | 21 | 5.365 | 0.016 |

| d (Interest in financial inclusion information) does not Granger cause interest in Fintech information | 2.026 | 0.164 | |

| Pairwise Granger Causality Tests | |||

| Sample: 2020-Jan–2021-Dec | |||

| Lags: 2 | |||

| Null Hypothesis: | Obs. | F-Statistic | Prob. |

| Interest in Fintech information does not Granger cause d (interest in digital finance information) | 21 | 2.066 | 0.159 |

| d (Interest in digital finance information) does not Granger cause interest in Fintech information | 0.335 | 0.721 | |

| Pairwise Granger Causality Tests | |||

| Sample: 2020-Jan–2021-Dec | |||

| Lags: 2 | |||

| Null Hypothesis: | Obs. | F-Statistic | Prob. |

| d (Interest in financial inclusion information) does not Granger cause d (interest in digital finance information) | 21 | 0.957 | 0.405 |

| d (Interest in digital finance information) does not Granger cause d (interest in financial inclusion information) | 0.938 | 0.412 | |

| Granger Causality Tests (Number of Lags: 2) | F-Statistic | p-Value | Is There Granger Causality? |

|---|---|---|---|

| Null hypothesis | |||

| “Interest in Fintech information” does not Granger cause “d (Interest in financial inclusion information)” | 5.365 | (p = 0.016) | Yes, there is Granger causality |

| “d (Interest in financial inclusion information)” does not Granger cause “Interest in Fintech information” | 2.026 | (p = 0.164) | No Granger causality |

| “d (Interest in digital finance information)” does not Granger cause “d (Interest in financial inclusion information)” | 1.387 | (p = 0.278) | No Granger causality |

| “d (Interest in financial inclusion information)” does not Granger cause “Interest in digital finance information” | 1.252 | (p = 0.312) | No Granger causality |

| “d (Interest in digital finance information)” does not Granger cause “Interest in Fintech information” | 0.335 | (p = 0.721) | No Granger causality |

| “Interest in Fintech information” does not Granger cause “d (Interest in digital finance information)” | 2.066 | (p = 0.159) | No Granger causality |

| Dependent Variable | ||||

|---|---|---|---|---|

| Variable | Interest in Financial Inclusion Information | Interest in Digital Finance Information | Interest in Fintech Information | |

| Independent Variable | Coefficient | Coefficient | Coefficient | |

| (t-statistic) | (t-statistic) | (t-statistic) | ||

| ((p-value)) | ((p-value)) | ((p-value)) | ||

| R-squared | R-squared | R-squared | ||

| Interest in financial inclusion information | 2.208 | 2.099 | ||

| (28.59) | (42.13) | |||

| Nil | ((0.000)) | ((0.000)) | ||

| −54.13% | 11.11% | |||

| Interest in digital finance information | 0.440 | 0.931 | ||

| (28.59) | (28.52) | |||

| ((0.000)) | Nil | ((0.000)) | ||

| −51.09% | −91.05% | |||

| Interest in Fintech information | 0.470 | 1.045 | ||

| (42.12) | (28.52) | |||

| ((0.000)) | ((0.000)) | Nil | ||

| 29.34% | −54.91% | |||

| Dependent Variable | ||||

|---|---|---|---|---|

| Variable | Interest in Financial Inclusion Information | Interest in Digital Finance Information | Interest in Fintech Information | |

| Independent Variable | Coefficient | Coefficient | Coefficient | |

| (t-statistic) | (t-statistic) | (t-statistic) | ||

| ((p-value)) | ((p-value)) | ((p-value)) | ||

| R-squared | R-squared | R-squared | ||

| Interest in financial inclusion information | 2.331 | 2.123 | ||

| (27.64) | (39.97) | |||

| Nil | ((0.000)) | ((0.000)) | ||

| −53.16% | 8.12% | |||

| Interest in digital finance information | 0.448 | 0.932 | ||

| (27.06) | (23.66) | |||

| ((0.000)) | Nil | ((0.000)) | ||

| −44.92% | −81.46% | |||

| Interest in Fintech information | 0.471 | 1.097 | ||

| (39.84) | (29.74) | |||

| ((0.000)) | ((0.000)) | Nil | ||

| 25.76% | −57.88% | |||

| Variable | OLS | GMM |

|---|---|---|

| Coefficient (t-statistic) | Coefficient (t-statistic) | |

| Interest in digital finance information | 0.104 (1.70) | −0.005 (−0.03) |

| Interest in Fintech information | 0.362 *** (5.59) | 0.477 ** (2.58) |

| R-squared | 37.56 | 24.84 |

| Adjusted R-squared | 34.73 | 21.26 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ozili, P.K.; Mhlanga, D.; Ammar, R.; Fersi, M. Information Effect of Fintech and Digital Finance on Financial Inclusion during the COVID-19 Pandemic: Global Evidence. FinTech 2024, 3, 66-82. https://doi.org/10.3390/fintech3010005

Ozili PK, Mhlanga D, Ammar R, Fersi M. Information Effect of Fintech and Digital Finance on Financial Inclusion during the COVID-19 Pandemic: Global Evidence. FinTech. 2024; 3(1):66-82. https://doi.org/10.3390/fintech3010005

Chicago/Turabian StyleOzili, Peterson K., David Mhlanga, Rym Ammar, and Marwa Fersi. 2024. "Information Effect of Fintech and Digital Finance on Financial Inclusion during the COVID-19 Pandemic: Global Evidence" FinTech 3, no. 1: 66-82. https://doi.org/10.3390/fintech3010005

APA StyleOzili, P. K., Mhlanga, D., Ammar, R., & Fersi, M. (2024). Information Effect of Fintech and Digital Finance on Financial Inclusion during the COVID-19 Pandemic: Global Evidence. FinTech, 3(1), 66-82. https://doi.org/10.3390/fintech3010005