Evaluating the World’s First Sovereign Blue Bond: Lessons for Operationalising Blue Finance

{kind=link}

{kind=link}

Abstract

1. Introduction

Seychelles Blue Finance Context

2. Materials and Methods

2.1. Sampling Strategy

2.2. Ethical Considerations

2.3. Data Collection and Analysis

2.4. Limitations

3. Blue Financing in Seychelles

3.1. Debt Restructuring, the Swap and SeyCCAT

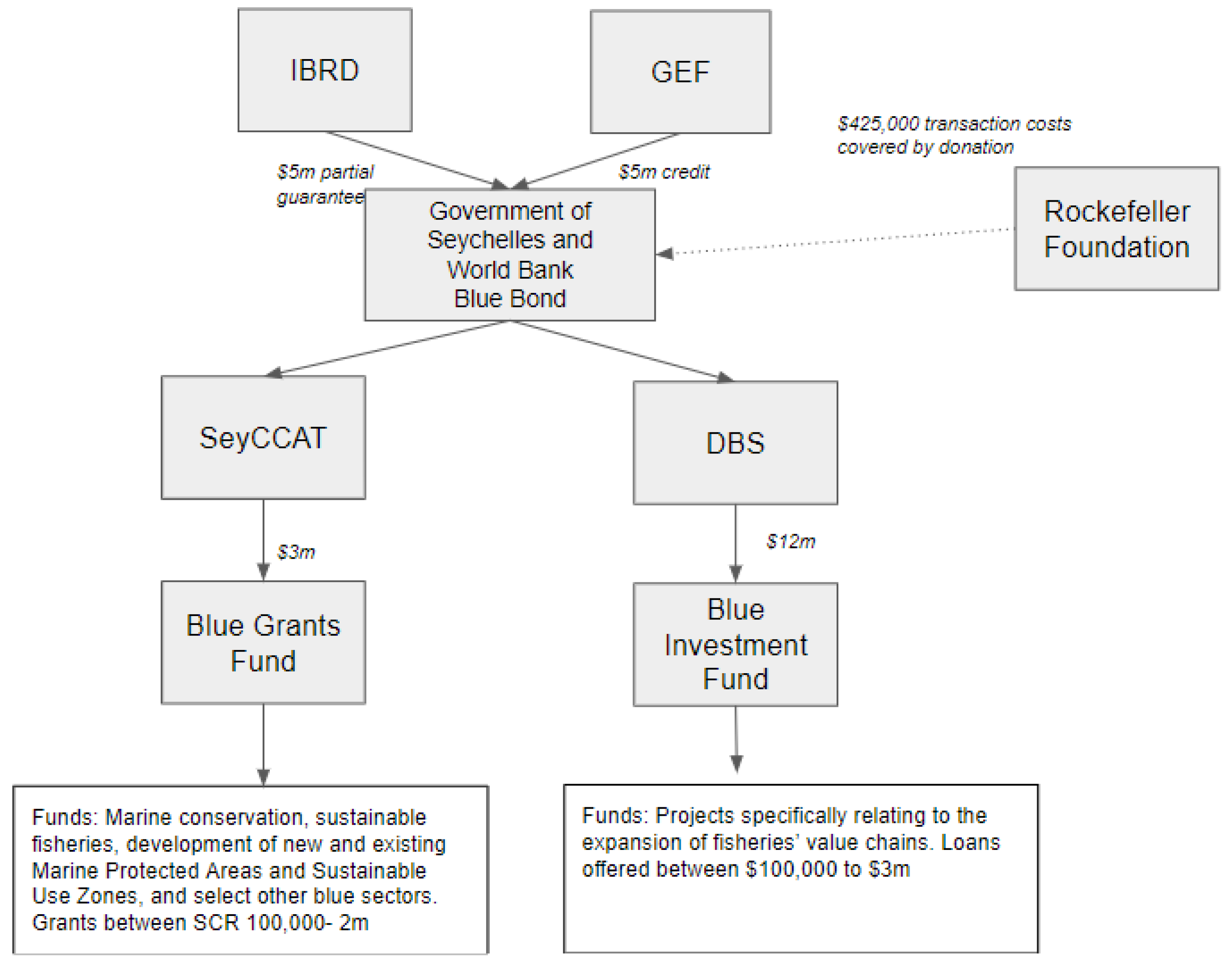

3.2. Blue Bond Structure and Setup

4. Results and Discussion

4.1. Relationship of the Bond to Other Actors and Donors

4.2. The Role of the Blue Bond in Advancing Seychelles’ Blue Economy

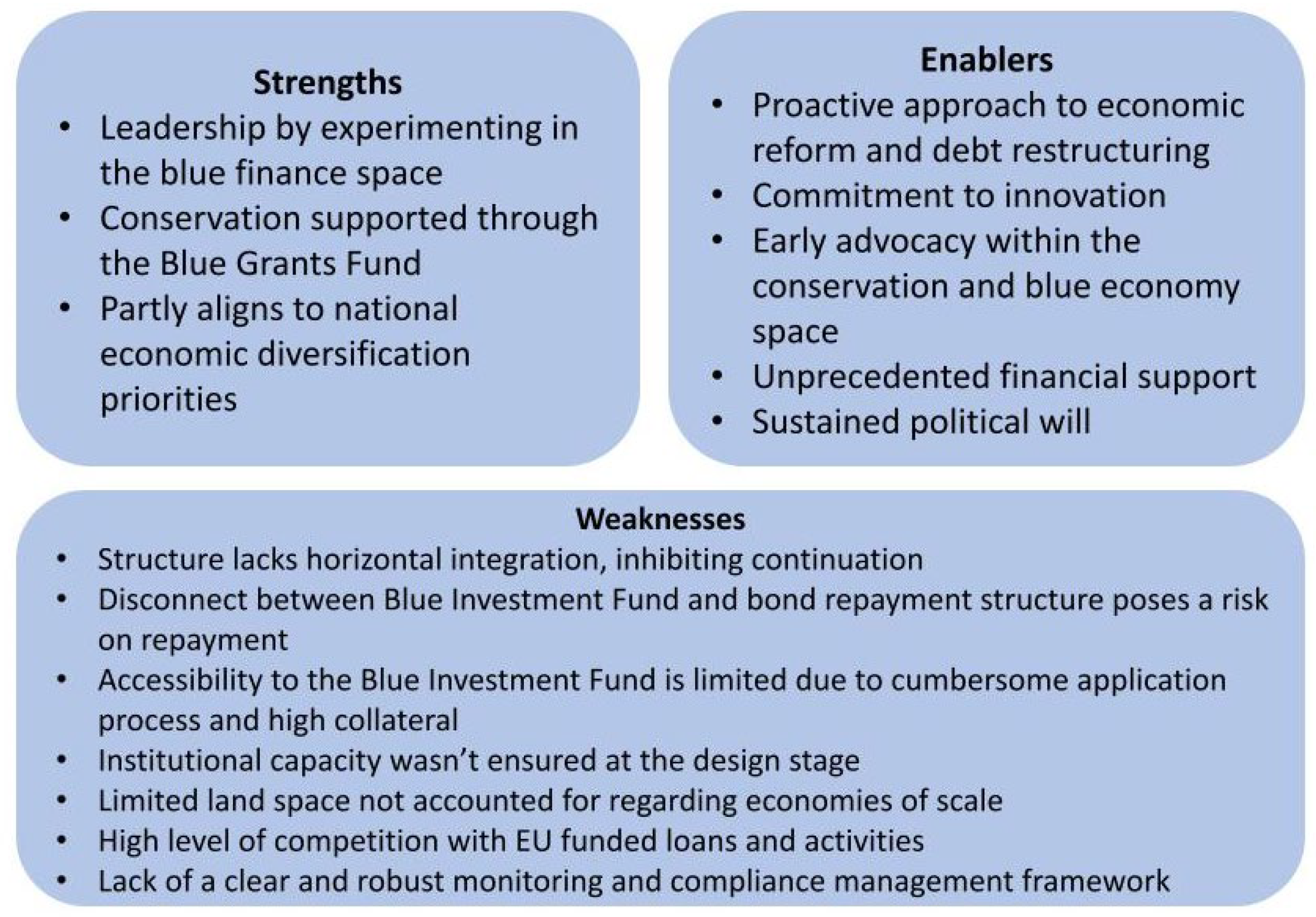

4.3. Strengths and Weaknesses of Seychelles Blue Bond

5. Future Considerations for Blue Bonds

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- OECD. The Ocean Economy in 2030; OECD: Paris, France, 2016. [Google Scholar] [CrossRef]

- Huang, M.C.; Voyer, M.; Benzaken, D.; Watanabe, A. Blue Economy and Blue Finance: Toward Sustainable Development and Ocean Governance; Morgan, P.J., Huang, M., Voyer, M., Benzaken, D., Watanabe, A., Eds.; Asian Development Bank: Tokyo, Japan, 2023; ISBN 9784899742524. [Google Scholar]

- March, A.; Failler, P.; Bennett, M. Challenges when designing blue bond financing for Small Island Developing States. ICES J. Mar. Sci. 2023, 80, 2244–2251. [Google Scholar] [CrossRef]

- Tirumala, R.D.; Tiwari, P. Innovative financing mechanism for blue economy projects. Mar. Policy 2022, 139, 104194. [Google Scholar] [CrossRef]

- Johansen, D.F.; Vestvik, R.A. The cost of saving our ocean–estimating the funding gap of sustainable development goal 14. Mar. Policy 2020, 112, 103783. [Google Scholar] [CrossRef]

- World Economic Forum. Friends of Ocean Action. SDG14 Financing Landscape Scan: Tracking Funds to Realize Sustainable Outcomes for the Ocean [White Paper]. 2022. Available online: https://www3.weforum.org/docs/WEF_Tracking_Investment_in_and_Progress_Toward_SDG14.pdf (accessed on 28 March 2023).

- Shiiba, N.; Wu, H.H.; Huang, M.C.; Tanaka, H. How blue financing can sustain ocean conservation and development: A proposed conceptual framework for blue financing mechanism. Mar. Policy 2022, 139, 104575. [Google Scholar] [CrossRef]

- UNEPFi. Rising Tide: Mapping Ocean Finance for a New Decade; Nations Environment Programme Finance Initiative: Geneva, Switzerland, 2021; p. 79. [Google Scholar]

- Deschryver, P.; de Mariz, F. What Future for the Green Bond Market? How Can Policymakers, Companies, and Investors Unlock the Potential of the Green Bond Market? J. Risk Financial Manag. 2020, 13, 61. [Google Scholar] [CrossRef]

- ICMA. Bonds to Finance the Sustainable Blue Economy: A Practitioner’s Guide; International Capital Market Association: Zürich, Switzerland, 2023. [Google Scholar]

- Bosmans, P.; de Mariz, F. The Blue Bond Market: A Catalyst for Ocean and Water Financing. J. Risk Financial Manag. 2023, 16, 184. Available online: https://www.mdpi.com/1911-8074/16/3/184 (accessed on 25 March 2024). [CrossRef]

- de Mariz, F.; Savoia, J. Financial Innovation with a Social Purpose: The Growth of Social Impact Bonds. September 2018. Available online: https://papers.ssrn.com/abstract=3306818 (accessed on 28 March 2024).

- Sumaila, U.R.; Walsh, M.; Hoareau, K.; Cox, A.; Teh, L.; Abdallah, P.; Akpalu, W.; Anna, Z.; Benzaken, D.; Crona, B.; et al. Financing a sustainable ocean economy. Nat. Commun. 2021, 12, 3259. [Google Scholar] [CrossRef] [PubMed]

- UNDESA. Promotion and Strengthening of Sustainable Ocean-Based Economies. 2021. Available online: https://sdgs.un.org/sites/default/files/2022-01/2014248-DESA-Oceans_Sustainable_final-WEB.pdf (accessed on 25 March 2023).

- SeyCCAT. High-Resolution 2D/3D Coastal Mapping on the Island of Mahé. The Seychelles Conservation and Climate Adaptation Trust. Available online: https://seyccat.org/high-resolution-2d-3d-coastal-mapping-and-monitoring-using-unmanned-aerial-vehicle-and-structure-from-motion-photogrammetry-techniques-on-the-island-of-mahe/ (accessed on 12 October 2023).

- Benzaken, D.; Voyer, M.; Pouponneau, A.; Hanich, Q. Good governance for sustainable blue economy in small islands: Lessons learned from the Seychelles experience. Front. Political Sci. 2022, 4, 1040318. Available online: https://www.frontiersin.org/articles/10.3389/fpos.2022.1040318 (accessed on 2 December 2022). [CrossRef]

- Hume, A.; Leape, J.; Oleson, K.L.; Polk, E.; Chand, K.; Dunbar, R. Towards an ocean-based large ocean states country classification. Mar. Policy 2021, 134, 104766. [Google Scholar] [CrossRef]

- Laing, S. Socio-Economic Assessment of the Blue Economy in Seychelles; United Nations Economic Commission for Africa: Addis Ababa, Ethiopia, 2021. [Google Scholar]

- Ministry of Finance, National Planning and Trade. Seychelles National Development Strategy 2019–2023. Government of Seychelles. 2018. Available online: http://www.finance.gov.sc/uploads/files/Seychelles_National_Development_Strategy_2019_2023_new.pdf (accessed on 23rd March 2023).

- Ministry of Finance, National Planning and Trade, ‘Vision 2033′. Government of Seychelles. Available online: http://www.finance.gov.sc/uploads/files/vision2033_vers_14_LR.pdf (accessed on 23 March 2023).

- Failler, P.; Ayoubi, H.E. Seychelles Blue Economy Action Plan; Government of Seychelles: Victoria, Seychelles, 2020. [Google Scholar]

- Commonwealth Secretariat. Sustainable Blue Economy Innovative Financing–Debt for Conservation Swap, Seychelles’ Conservation and Climate; Commonwealth Secretariat: London, UK, 2020; Available online: https://production-new-commonwealth-files.s3.eu-west-2.amazonaws.com/s3fs-public/2022-02/Case%20Study%20-%20Innovative%20Financing%20%E2%80%93%20Debt%20for%20Conservation%20Swap,%20Seychelles%E2%80%99%20Conservation%20and%20Climate%20Adaptation%20Trust%20and%20the%20Blue%20Bonds%20Plan,%20Seychelles%20(on-going).pdf (accessed on 23 March 2023).

- Convergence. Seychelles Debt Conversion for Marine Conservation and Climate Adaptation: Case Study, Convergence; NatureVest. The Nature Conservancy: Arlington County, VA, USA, 2017. Available online: http://tinyurl.com/2dc6rkj5 (accessed on 23 March 2023).

- Silver, J.J.; Campbell, L.M. Conservation, development and the blue frontier: The Republic of Seychelles’ Debt Restructuring for Marine Conservation and Climate Adaptation Program. Int. Soc. Sci. J. 2018, 68, 241–256. [Google Scholar] [CrossRef]

- SeyCCAT. Blue Finance. The Seychelles Conservation and Climate Adaptation Trust. Available online: https://seyccat.org/blue-finance/ (accessed on 10 October 2023).

- Mathew, J.; Robertson, C. Shades of blue in financing: Transforming the ocean economy with blue bonds. J. Invest. Compliance 2021, 22, 243–247. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research and Application: Design and Methods; SAGE Publications: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- Allmark, P.; Boote, J.; Chambers, E.; Clarke, A.; McDonnell, A.; Thompson, A.; Tod, A.M. Ethical Issues in the Use of In-Depth Interviews: Literature Review and Discussion. Res. Ethics 2009, 5, 48–54. [Google Scholar] [CrossRef]

- World Bank. Sovereign Blue Bond Issuance: Frequently Asked Questions. Available online: https://www.worldbank.org/en/news/feature/2018/10/29/sovereign-blue-bond-issuance-frequently-asked-questions (accessed on 12 September 2023).

- Directorate-General for Maritime Affairs and Fisheries. EU and Seychelles Take Stock of Fisheries Partnership. 2021. Available online: https://oceans-and-fisheries.ec.europa.eu/news/eu-and-seychelles-take-stock-fisheries-partnership-2021-11-29_en (accessed on 21 October 2023).

- DBS. Development Bank of Seychelles. Annual Report for the Year 2021. 2021. Available online: https://www.dbs.sc/sites/default/files/downloads/Merged%20Annual%20Report%20%26%20Financial%20Statement%20%202021.pdf (accessed on 23 March 2023).

- Seychelles Blue Carbon–Blue Carbon Lab. Available online: https://www.bluecarbonlab.org/seychelles-blue-carbon/ (accessed on 23 March 2024).

- TNC. Mapping Ocean Wealth. Seychelles. Available online: https://oceanwealth.org/project-areas/seychelles/ (accessed on 31 September 2023).

- Arınç, O.K. Blue Bonds: Shifting the Responsibility Innovatively. Debt and Green Transition Blog Series. Available online: https://www.developmentresearch.eu/?p=1544 (accessed on 30 September 2023).

- Samways, M.J.; Hitchins, P.M.; Bourquin, O.; Henwood, J. Restoration of a tropical island: Cousine Island, Seychelles. Biodivers. Conserv. 2008, 19, 425–434. [Google Scholar] [CrossRef][Green Version]

- Stobart, B.; Teleki, K.; Buckley, R.; Downing, N.; Callow, M. Coral recovery at Aldabra Atoll, Seychelles: Five years after the 1998 bleaching event. Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 2005, 363, 251–255. [Google Scholar] [CrossRef] [PubMed]

- Thompson, B.S. Blue bonds for marine conservation and a sustainable ocean economy: Status, trends, and insights from green bonds. Mar. Policy 2022, 144, 105219. [Google Scholar] [CrossRef]

- World Bank. World Bank and Credit Suisse Partner to Focus Attention on Sustainable Use of Oceans and Coastal Areas–the “Blue Economy”. Available online: https://www.worldbank.org/en/news/press-release/2019/11/21/world-bank-and-credit-suisse-partner-to-focus-attention-on-sustainable-use-of-oceans-and-coastal-areas-the-blue-economy (accessed on 23 March 2023).

- Bollinger, P.A. Seychelles: Beyond Dramatic Imaginary. Samudra Report No. 82. 2020. Available online: https://aquadocs.org/bitstream/handle/1834/41223/Sam_82_art01_Seychelles_Svein_Jentoft.pdf?sequence=1&isAllowed=y (accessed on 23 March 2023).

- Drakeford, B.M.; Failler, P.; Toorabally, B.; Kooli, E. Implementing the fisheries transparency initiative: Experience from the seychelles. Mar. Policy 2020, 119, 104060. [Google Scholar] [CrossRef]

- WEF. Accelerating Innovation for Ocean Health. World Economic Forum 1000 Ocean Startups. Available online: https://www.1000oceanstartups.org/home (accessed on 10 October 2023).

- Commonwealth Secretariat. The Commonwealth Blue Charter Project Incubator. Available online: https://thecommonwealth.org/bluecharter/commonwealth-blue-charter-project-incubator (accessed on 10 October 2023).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

March, A.; Evans, T.; Laing, S.; Raguain, J. Evaluating the World’s First Sovereign Blue Bond: Lessons for Operationalising Blue Finance. Commodities 2024, 3, 151-167. https://doi.org/10.3390/commodities3020010

March A, Evans T, Laing S, Raguain J. Evaluating the World’s First Sovereign Blue Bond: Lessons for Operationalising Blue Finance. Commodities. 2024; 3(2):151-167. https://doi.org/10.3390/commodities3020010

Chicago/Turabian StyleMarch, Antaya, Tegan Evans, Stuart Laing, and Jeremy Raguain. 2024. "Evaluating the World’s First Sovereign Blue Bond: Lessons for Operationalising Blue Finance" Commodities 3, no. 2: 151-167. https://doi.org/10.3390/commodities3020010

APA StyleMarch, A., Evans, T., Laing, S., & Raguain, J. (2024). Evaluating the World’s First Sovereign Blue Bond: Lessons for Operationalising Blue Finance. Commodities, 3(2), 151-167. https://doi.org/10.3390/commodities3020010