Challenges and Vulnerabilities on Public Finance Sustainability. A Romanian Case Study

1

Faculty of Law and Administrative Sciences, Stefan cel Mare University of Suceava, 13 Universităţii, 720229 Suceava, Romania

2

Faculty of Economics and Business Administration, Alexandru Ioan Cuza University of Iasi, 11 Carol I, 700506 Iaşi, Romania

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2018, 11(3), 55; https://doi.org/10.3390/jrfm11030055

Submission received: 2 August 2018

/

Revised: 11 September 2018

/

Accepted: 14 September 2018

/

Published: 17 September 2018

(This article belongs to the Section Sustainability and Finance)

Abstract

:Given the contradiction between the current demands for sustainability and the way that the financial system works, this paper explored in a retrospective and a prospective view, Romanian Public Finance Sustainability, highlighting the major challenges and vulnerabilities. Relating to the retrospective part, we concentrated mainly on empirical tests on Romanian government solvency between the period 1990–2020, by applying un it root and co-integration tests. To gain a better, general understanding of the behavior of policy-makers, in the second part we used a scenario analysis of budgetary adjustment in the short and medium run under alternative hypotheses. The results provided formal proof that policy makers decisions face critical and complex questions, and the way in which they manage fiscal stimuli has a direct implication on the sustainability of the country and on the lax implementation of fiscal policy.

1. Introduction

The study of public finance sustainability has been the focus of a large body of finance literature in recent decades. Clearly, policy makers’ poor fiscal performance and high fiscal risk-taking behavior resulted in fiscal decline, insolvency of the budget, and the likelihood of financial crisis. As such, the level of risk to which a country is exposed, and the level of its fiscal and financial performance, are not only prominent topics within the literature, but are also of importance to macroeconomic conjuncture. This increases the controversy and the desire to strengthen government accountability mechanisms.

Considering the current macroeconomic context, which is characterized by decisions based on tough political stakes, with oscillation in tackling anti-cyclical or procyclical policies; and the fact that it is hypothesized that the economic and political environments of Romania are characterized by instability, we can conduct an analysis of fundamental elements involving challenges and vulnerabilities in Romanian fiscal policy. This can reveal the need for accountability of decision-makers, and implicitly, better correlation of their decisions with the finality of the actions taken.

Starting from the recent line of debate on whether fiscal sustainability is assured, most papers focus on testing the assumption of cointegration between government revenues and expenditures, identifying a preference for application of unit roots in government debt and budget deficit series. Even if we do not find this type of empirical evidence and econometric tests on the Romania profile, the results on the profile of the Euro Area and USA conclude that both regions have adopted effective policies, which have led to a sustainable fiscal policy. This perhaps follows the fact that the issue of Romanian public finances is not usually studied from the point of critical factors behind public debt. On the other hand, given that modernity intervenes with major changes on this branch and the central element of analysis falls to the notion of accountability; at the global level, we also find a preference and a necessity to study the relationship between public finance sustainability and Fiscal Responsibility Laws (FRLs). On the world stage there have been approaches regarding several public policies for a framework to consolidate new fiscal rules, but these do not consider the changes that have taken place over time. In the conditions of a progressive deterioration of the primary balance under the exclusive impact of demographic factors, the sustainability of public finances may be more difficult to assure. As highlighted by Chan-Lau et al and Santos et al. (Chan-Lau and Santos 2010; Woo and Kumar 2015), the main idea of the notion of sustainability has deeply changed. If earlier, the phenomenon of public finance sustainability was analyzed by addressing rising budget deficits or the level of public debt as a percentage of GDP, contemporaneity brings into discussion demographic elements, the phenomenon of ageing population, consequently with the increasing spending on pensions and all social obligations which derives from this. In this case, we found that fiscal policy is sustainable when the government debt growth rate is lower than the long-term interest rate, considering that a sustainable fiscal policy is one that does not lead to: Excessive increase in indebtedness; drastic reduction of budget expenditures and/or significant increase of taxes; monetization of the budget deficit or repudiation of contracted public debt (Woo and Kumar 2015).

While on the world stage, the changes regarding public finance sustainability consider both political and social factors, on the Romanian profile, the subject is analyzed by addressing rising budget deficits or the level of public debt. This is also supported by Fiscal Responsibility Law No. 69/2010 from March 2010, which was designed to strengthen fiscal discipline and contribute to improving medium term fiscal planning. This law transposes five fiscal rules to achieve the budgetary objectives, set by Protocol 12 of the Treaty on the Functioning of the European Union TFEU and Stability Pact, but given the fact that the body responsible for monitoring compliance with rules, i.e., the Fiscal Council, has a consultative role, the consolidation of public finance sustainability is still lacking. However, it is revealed that the Romanian fiscal system is characterized by imbalances that require correction regarding inefficient fiscal management and excessive bureaucracy, things that invoke the need for a radical reform of the tax collection system, to ensure a significant increase in collected revenue and a reduction in the related administrative costs (Radulescu 2003; Săveanu 2015; Wilson 2010).

Literature has established two factors often cited in the itinerary of public finance sustainability: Political instability (and political uncertainty) on growth, and the relatively high debt level deepened by fiscal deterioration in the aftermath of the global financial crisis which started in 2008 (Badinger and Reuter 2015; Joireman et al. 2005; Neyapti and Bulut-Cevik 2014). Therefore, we can say that the implications of the normative and political framework, and the preferences for procyclical or anti-cyclical policy imply an unwanted confrontation of public finance with the test of facts, and as a result it implies the incidence of an intergenerational effect and a burden on society. In this case, the main questions relate to how public finance can improve sustainability, how changes in income and expense policy can manage the dynamics of fiscal balance and debt dynamics, and how strategies can be influenced by the legal framework in the area of fiscal performance.

The purpose of this paper is to analyze Romanian public finance sustainability using empirical analysis, combined with a retrospective and a prospective view. To provide this new evidence on the picture of fiscal sustainability in Romania, we used econometric tests on solvency and sustainability, and we set out a forward-looking scenario-analysis to investigate how Romanian public finances may evolve during the medium and long-run.

This paper also contributes to the way in which each of the analyzed Romanian fiscal policy contexts suffered budgetary adjustment or changes in macroeconomic circumstances, under the fiscal reforms process. Moreover, it explores the potential connection between the fiscal rules/fiscal responsibility law required and fiscal policy.

The remainder of this paper is structured as follows: Section 1 reviews some of the key literature on the main determinants of public finance sustainability; Section 2 refers to the Retrospective Testing of Budget sustainability in Romania and reveal the results of Unit Root and Cointegration Tests; Section 3 presents data and explains the methodology, the empirical results, and their interpretations based on simulating a number of scenarios. Our paper ends with concluding remarks, emphasizing policy recommendations, which in our opinion, should be considered for improving fiscal responsibility and consolidating public finance sustainability.

2. Theoretical Considerations and Empirical Experience

Literature on the issue of public finance sustainability reveals that there are few papers examining the link between the way to a sustainable fiscal policy and small, permanent, or even temporary changes in some important variables, such as interest rate, inflation, or demographic changes, with the costs of ageing. Some empirical studies have pointed out that both the ex post and ante post economic crisis periods, have been characterized by instability, inadequate decisions, and implicitly the wrong model adoption of collective discipline, leading to fiscal indiscipline in most European countries (Afonso 2005; Fatás and Mihov 2009; Neaime 2015).

We also find a direct link between the idea or desideratum of sustainable finances and the economic potential of each country, due to the fact that a high level of indebtedness prevents sustainable growth, which has led specialized literature to address an econometric model to estimate the causality between the sustainability of public debt and economic growth (Woo and Kumar 2015; Radulescu 2003; Săveanu 2015; Wilson 2010; Badinger and Reuter 2015; Joireman et al. 2005; Neyapti and Bulut-Cevik 2014; Afonso 2005; Fatás and Mihov 2009; Neaime 2015; Blanchard et al. 1990). As a rationale that justifies the implication of some variables like ageing costs on public finance sustainability, some authors note that public finance sustainability is synonymous with the concept of fiscal sustainability, which is focused on identifying the major challenges from this area, to better evaluatedebt through some important criteria: Liquidity, solvency, and realistic adjustment criteria, taking into account demographic aspects (Blanchard et al. 1990; Polito and Wickens 2005; Tanner and Samake 2008).

Several papers include empirical approaches concerning public finance sustainability of countries, the most common being focused on various and mixed methodology involving many instruments to measure sustainability. Referring to the example of some international organizations, regarding the International Monetary Fund (IMF), we identify the use of such tools as the ALM (Asset and Liability Management) model or the QUEST model developed by the European Commission, which is based on the analysis of many variables, where the simulation is relevant only if primary data entered in the model are correct (Chan-Lau and Santos 2010; Woo and Kumar 2015; Radulescu 2003; Săveanu 2015; Wilson 2010; Badinger and Reuter 2015; Joireman et al. 2005; Neyapti and Bulut-Cevik 2014; Afonso 2005; Fatás and Mihov 2009; Neaime 2015; Blanchard et al. 1990; Polito and Wickens 2005; Tanner and Samake 2008; Pinheiro and Geraldes 2007). Other authors (Blanchard et al. 1990; Alho et al. 2008), introduce an Index of Sustainability, calculated as the difference between the sustainable tax rate and the effective rate of taxation in the economy. Polito and Wicken assume a similar approach and propose an Index of Fiscal Stance (Polito and Wickens 2005; Ewijk et al. 2006). Other papers focused on analyzing the implication ofthe social sector in assessing sustainability (Pinheiro and Geraldes 2007; Bergman et al. 2016), or demographic perspectives and population ageing trends (Ewijk et al. 2006).

Analyzing the reports of the European Commission, we identify the incidence of a measure of the purpose of tax institutions. According to the data centralized in the Commission’s reports, the methodology used in the calculation of this index involves addressing indicators such as: Assessing the Fiscal Council’s compliance with the tax rules, implications in fiscal policy monitoring, involvement in improvement of correction mechanisms, quantification of policy measures, and long-term sustainability. All these indicators are quantified in terms of importance and implications of the bodies to obtain a final score, indicating an index that measures the purpose of the tax institutions. In the light of the Organization for Economic Cooperation and Development (OECD) settlement tribunals, revenue and expenditure balances are trimmed to ensure the sustainability of public finances. It is believed that if government revenue is high, it finances the supply of goods and services, and has a redistributive role; however, long-term revenue and expenditure should be balanced to ensure the sustainability of public finances.

Bergman et al. and Landolfo, performed an empirical analysis on the profile of the Euro Area, for the period from 1966 to 2004, and the USA, for the period 1977–2003. By using cointegration and unit root tests to public debt, primary surplus, and interest rates, they evaluated fiscal sustainability and concluded basedon infinite horizon-tests, that both regions have adopted effective policies that led to a sustainable fiscal policy. The first author also emphasized the importance of tax rules in consolidating transparent fiscal policies and increasing tax solvency (Bergman et al. 2016; Landolfo 2008).

Afonso and Rault (Afonso and Rault 2008, 2010), found that among the EU-15, fiscal sustainability had been reached in certain sub-periods, more precisely 1970–1991 and 1992–2006. The authors use stationarity and cointegration analysis for the period from 1970–2006. Regarding the OECD, Afonso and Jalles (2012) performed an analysis of the same topic over the period 1970–2010 (Afonso and Jalles 2012). Based on unit root and cointegration analysis, they found that fiscal policy depended on the level of debt, management of revenues and expenditures, and in some countries, their analysis revealed the existence of a less sustainable fiscal policy. After two years, they improved the first paper by investigating the sustainability of fiscal policy in a set of nineteen countries, over the period 1880–2009 (Afonso and Jalles 2014). The authors highlighted also that vulnerability of public debt was influenced by its profile, and the characteristics of public debt structure (maturity, currency, lender) needed to be approached with great care in analyzing the critical situations which may arise in the management of public debt. A high weight of public debt with short-term initial maturity to total public debt, may indicate the country’s inability to issue long-term public debt, which increases refinancing risk and interest rates. A high share of public debt in foreign currency tototal public debt may increase exchange rate risk and may exert pressure on currency reserves.

In the case of Romania, we found fewer studies that focus on public finance sustainability. Some researchers such as Boiciuc (2015); Talpos and Enache (2008), attempted to analyze fiscal responsibility in terms of monthly values of public revenues and public expenditures, to obtain results using co-integration tests. They found that if public revenues remain unchanged, the public debt path will not change, ensuring long-term stability. Mura (2015); Patricia (2014), considering the period 2005–2013, analyze the main component of the budget referring to tax revenue, and concluded that the fiscal consolidation process of Romania has numerous vulnerabilities, which led to higher risk to fiscal sustainability. This idea was also supported by the reports of the European Commission, where Romania is included in the category of high-risk countries, regarding the sustainability of public finances.

There are some additional papers that focus on studying the specific elements of fiscal sustainability, like the importance of fiscal responsibility and rules, or the relationship between public debt, sovereign risk and sustainable development (Georgescu 2014; Zaman and Georgescu 2011). According to Canagarajah et al. (2012) Romania’s fiscal balance has deteriorated sharply following the global economic crisis, forcing Romania to implement an unsustainable fiscal consolidation, as a result of unsustainable growth rates; also highlighting the incidence of tax evasion and the inefficiency of fiscal policy. Furthermore, the authors stress the need for the tax consolidation process to be related to the specifics of Romania, considering its own fiscal capacity and the link with the macroeconomic context.

Radulescu (2003), also performed an analyses of Romania emphasizing the situation of the country’s budget sustainability during the 1990s, and concluding that during the transition period, an unsustainable fiscal policy was maintained. We also found that Boiciuc (2015) investigated the cyclical behavior of fiscal policy in Romania by calculating the structural deficit and the fiscal impulse for 2000–2013, concluding that fiscal policy was generally pro-cyclical, except in the year 2013.

In line with the above, in 2014, Tiţa, Oţetea, and Banu (Tiţa et al. 2014) revealed that the Romanian fiscal system should aim to increase the quality of public finances by improving the mechanisms of fiscal stimuli, consolidating fiscal governance, and strengthening fiscal discipline. The authors proposed legislative and institutional measures, involving the implication of a new law for fiscal responsibility, strict fiscal rules and an independent Fiscal Council.

3. Retrospective Testing of Budget Sustainability in Romania: Results of Unit Root and Cointegration Tests

The global financial crisis highlighted the importance of understanding the sources of vulnerabilities, which can lead to a systemic financial crisis. This reinforced the hypothesis that early identification of vulnerability sources was extremely important, as this would allow the introduction of policies to diminish their effect. In addition, contemporary period show us that the state is an important actor in both political, economic, and social life. In terms of sustainability of the actions undertaken, it is conditional on the procurement of resources through using several levers, including the tax system. From the point of view of its status as a public goods supplier and as a public service provider, the state enjoys legitimacy to obtain funding from the beneficiaries concerned. This legitimacy is exerted through public revenue policy, but there is always a need for interdependence between the need for public resources and the state’s role in the delivery of public goods and services. Given that financial stability is largely the result of the stability of public finances, it is an issue of efficient management of public resources and ensuring the sustainability of finances. Considering the above, the relationship between the financial crisis and public finance sustainability is complex. On the one hand, the crisis seriously impacted economies around the world. On the other hand, the failure of governments to respond to crises lead to a greater need for long-term accountability factors. An important consequence of the above is the current sovereign debt crisis, which affects many countries, including members of the European Union (EU) and the Euro area. Considering government decisions in promoting unsustainable growth, with unconsolidated budgets and a large volume of debt, it is important to identify the right way to manage difficulties in financing public debt and consolidating public finances.

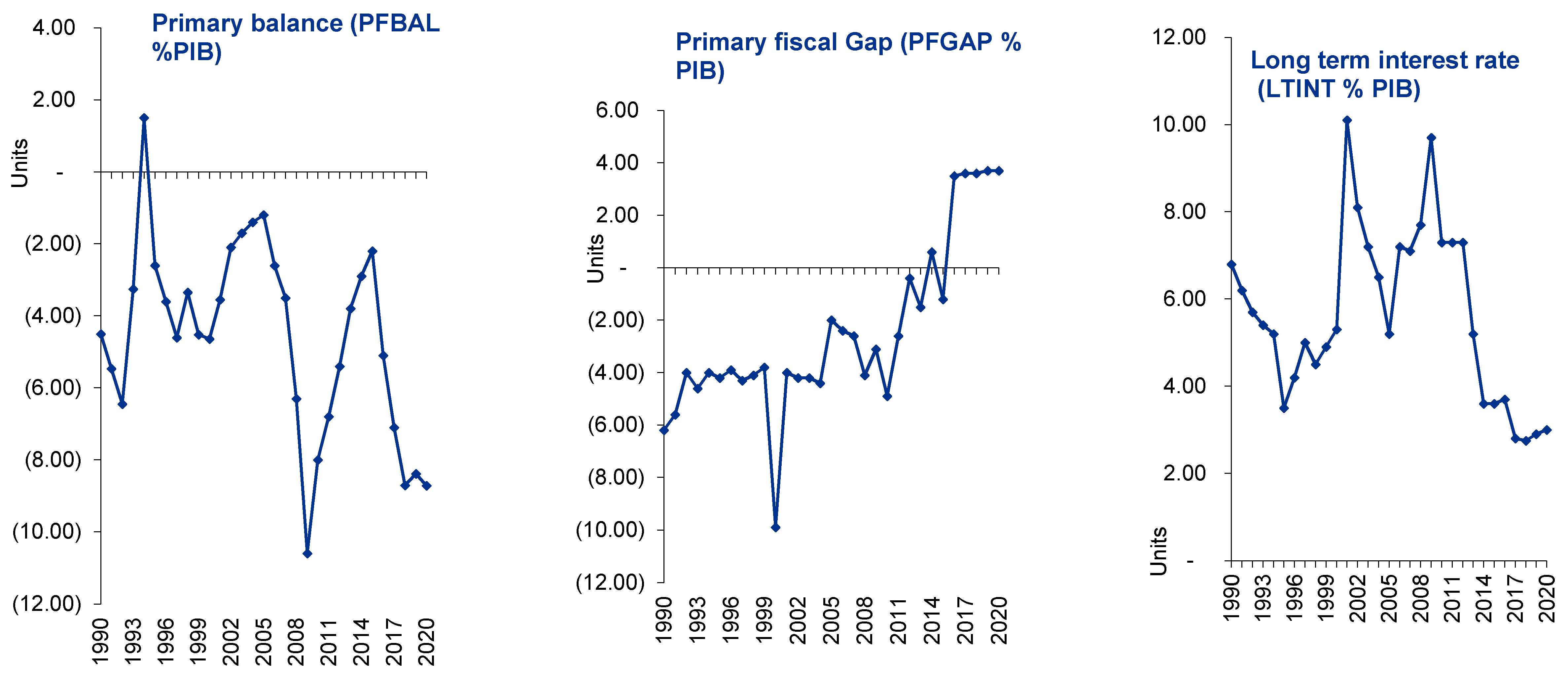

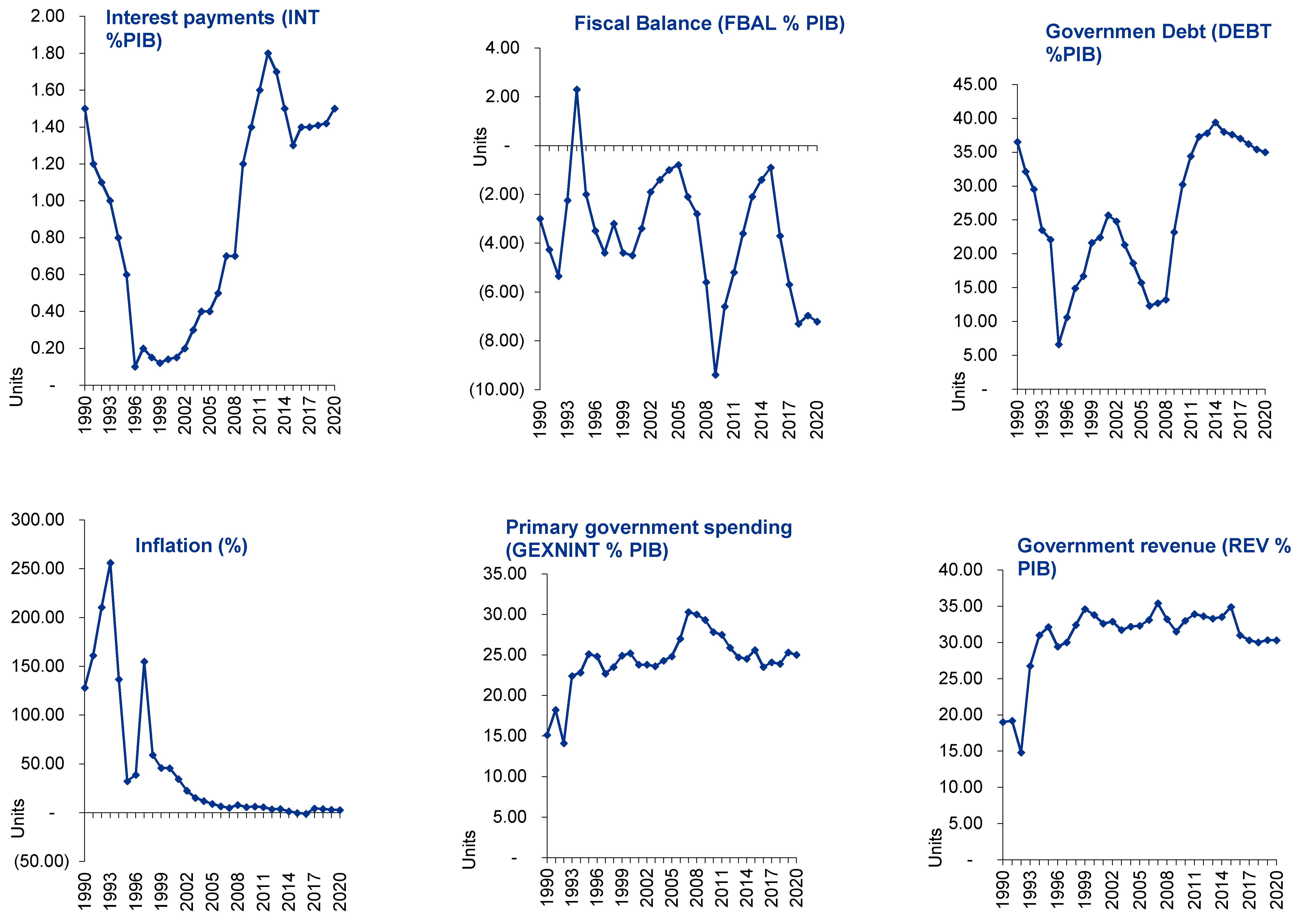

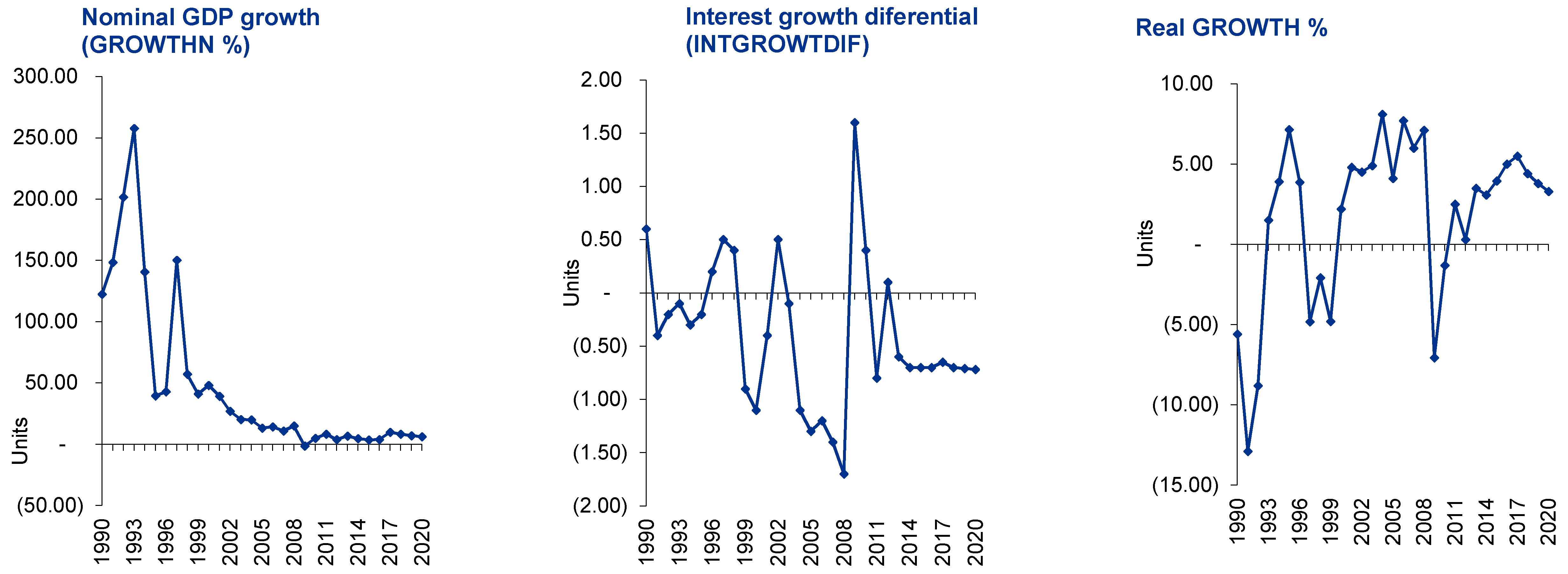

This study aims to analyze Romanian fiscal sustainability, considering both past events and situations, as well as prospecting the future, where we consider it appropriate to first understand the current public finances and challenges. Thus, we first analyze the fiscal situation from the past, specifically the last thirty years, by summarizing in Figure 1, the trends that follow macroeconomics and budgetary frameworks between 1990 and 2020. After this, because the retrospective is not enough, through the prospective approach, we document if future evolution of fiscal sustainability is negative or positive.

To test the retrospective part of this study, we applied empirical tests on Romanian government solvency during the last three decades, using standard unit root and co-integration tests. Moreover, we use a scenario analysis of budgetary adjustment in the short and medium run, under alternative hypotheses, to highlight the changes which may result from incorrect government decisions or lack of impact on sustainable growth.

Romanian public finances are facing many challenges but given contemporary conjuncture and the persistence of some variables with a direct implication on future sustainability, we will focus on those considered as key challenges. These are usually approached at the global level as the most common indicators for changes in public finance sustainability. The novelty of our approach cites limited research of this type on Romania, over the period considered and using the mixed models proposed. Furthermore, the approach highlights and analyzes the budgetary costs of ageing, using expenditure related with age, which has a direct implication not only on the public sector, but also on macroeconomic stability. We use data from the annual macro-economic databases of the European Commission’s (AMECO) database and Knoema World Data Atlas, and for the years 2018–2020, we used forecasts made at https://www.statista.com.

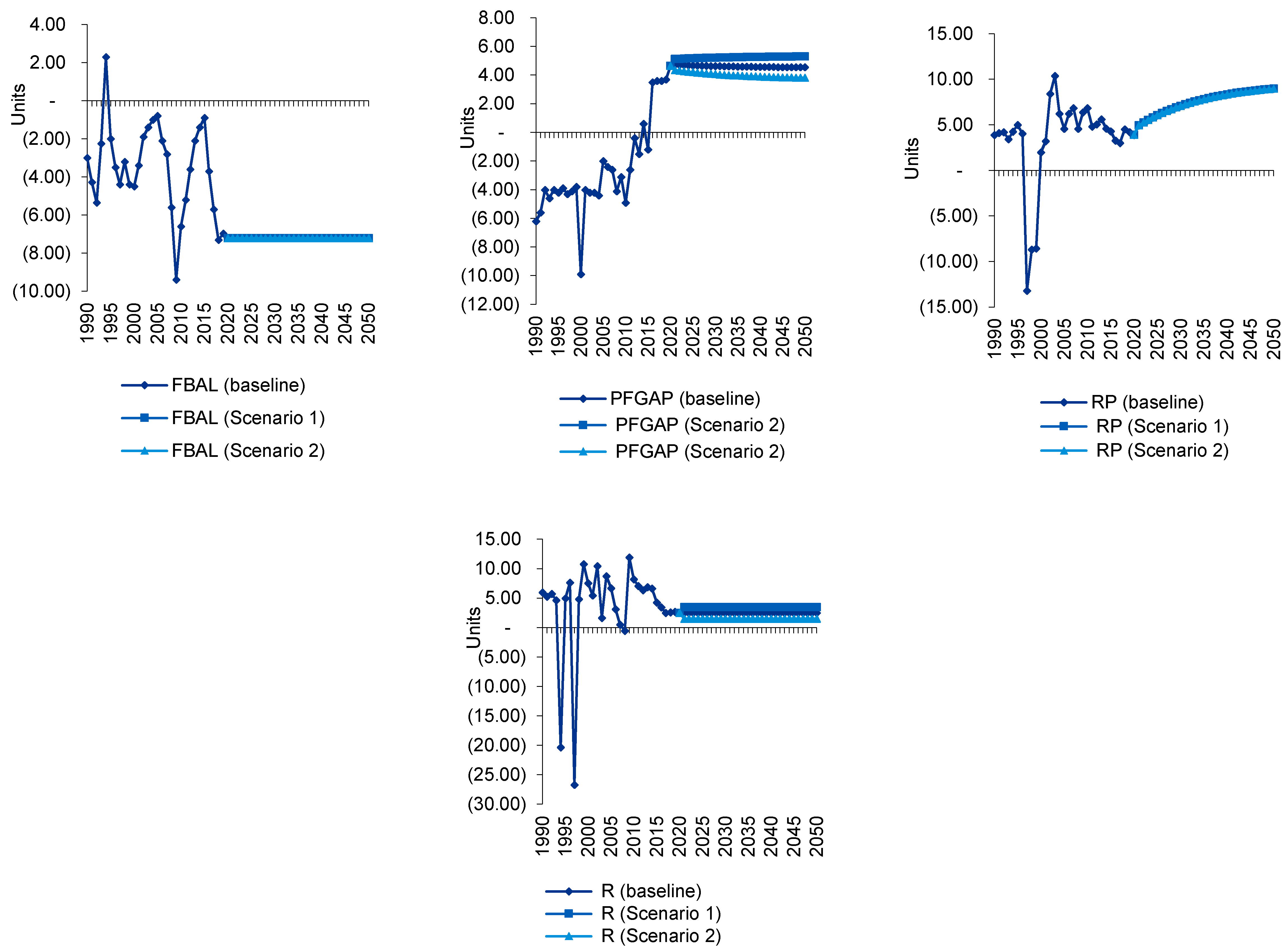

Achieving performance with a volatile European and global macroeconomic environment is extremely difficult, especially since there have been a series of events that have marked the world economy: Brexit, intensification of the refugee crisis, deterioration in international trade growth, modest economic growth of the main emerging countries (such as Brazil and Russia), and the rebalancing of China’s economy, all of which have contributed to increasing uncertainties about future developments of the global economy. Figure 1 shows the Romanian fiscal and macroeconomic variables during 1990–2020. All the variables are described in Prospective Approach of our study. This picture of Romanian public finance sustainability, indicates a series of major challenges to the sustainability of Romanian public finances, highlighted by both public debt levels and unsustainable growth rates, accompanied by high inflation in some years. We started with 1990, because in this year Romania adopted ‘The Strategy for Implementing the Market Economy in Romania (1990), where the main reform in the country’s public policy was the gradual reduction in public funds allocated from the state budget for economic goals. Therefore, it is appropriate to follow trends in problems of fiscal sustainability during this period and capture paradoxical situation of the rationality of formulating policies. The choice of variables was motivated by existing interest in analyzing the effects of fiscal policy on the main macroeconomic variables, such as GDP, inflation, interest rate, employment; and also because empirical literature on sustainability of public finances mainly addresses these variables by testing the effects of fiscal policy (or their magnitude) on macroeconomic variables (Bohn 1991; Ewijk et al. 2006; Afonso and Jalles 2012; Afonso and Jalles 2014). Moreover, according to purpose of this paper, we assume there is a logical relationship between fiscal and macroeconomic variables. For instance, since fiscal variables significantly deteriorated from 2007 onwards, the macroeconomic balance between growth and interest rate deteriorated around the same time, which led to a rapidly increasing government debt to GDP ratio. Given that unsustainable public finances imply a violation of the rules on budget constraints, literature shows that most empirical studies analyze this topic by estimating stationarity of fiscal balances, and testing the cointegration between debt and the primary fiscal balance. Bohn and Afonso (Bohn 1991; Afonso 2005), chose to analyze the subject from the same perspective and test the cointegration between government revenues and government expenditures. Given our aim is to examine if general political agreements and policy-makers decisions from the area of fiscal policy have really affected public finance sustainability over the last three decades, for our sample, to test whether the Romanian budget was sustainable, we applied the econometric tests used in the aforementioned literature. Table 1 illustrates the results of the unit-root tests on gross public debt, the fiscal balance (primary), government expenditures, government revenue, and the fiscal gap.

Table 1 reports that over the past three decades, some variables, such as government debt, government spending, and government revenue, were non-stationary. As far as the primary balance is concerned, we found it to be stationary during this period at a 10% confidence interval. However, when applying the first difference, it becomes non-stationary. The fiscal gap was at the borderline between stationarity and non-stationarity, giving the first indication that inter-temporal budgetary balance was not ensured in Romania, even before the fiscal decline in 2009. The non-stationarity of public debt and of the primary fiscal balance, also raises questions about the solvency of the budget. Given the result of non-stationarity regarding the (primary) fiscal balance, we could say that intertemporal solvency was not thoroughly ensured in Romania during the last three decades, and in the context of economic and political uncertainty, public finance sustainability will be affected by social circumstances and all unsupported efforts to achieve sustainability. This perhaps follows the fact that the issue of Romanian public finances faces some critical aspects: First, examining how the state finances its deficit, we could say that budget deficits are an important source of inflation. Second, the principles enshrined in the treaties, the Stability and Growth Pact (SGP), as well as the multilateral supervision process through the European Semester, have contributed far too little to fiscal consolidation in Romania.

Knowing the right itinerary, meaning that if the real interest rate (expected return) is constant, to maintain the balance of the intertemporal budget, the stock of debt and the primary deficit must be cointegrated. To test such a cointegration relationship between debt and the primary deficit in the case of Romania, we applied both the Johansen procedure (results presented in Table 2) and the Engle-Granger methodology to test the existence of cointegration between the two series of data. In the latter case, we also gave recourse to estimating a regression between the two variables and testing the residual stationarity of the resulting residuals. The cointegration test between primary deficit and debt is provided in Table 2, and in Table 3 we found the results of the Engle-Granger test on co-integration between the primary deficit and government debt

Empirical results point to a lack of connection between the stock of debt and the primary budget balance (Table 3). The fact that there is no cointegration between these two variables emphasizes that the crisis led to an additional negative impact on public finance sustainability. Moreover, the fact that the government’s solvency is a difficult task to achieve does not necessarily imply a generalization trend given the real interest rate situations, as well as other indicators with a direct impact on the change in the economic cycle, this view being fully supported in the literature (Trehan and Walsh 1991). Additionally, results show that the time variation of interest rate expectations was plausible given that the Romanian economy underwent changes by preparing for the fiscal consolidation and changes before and after the economic crisis, and due to several implementation convergence and stabilization programs aimed at convergence to fiscal sustainability. On the other hand, the same researcher showed that there was a close link between the deficit and the budget, and that the inter-temporal budgetary balance was assured if the expected real interest rate had positive values (Trehan and Walsh 1991). However, we believe that for the government to reduce slippage of the budget, it must focus on strengthening a mechanism that will ensure a political balance preventing fiscal measures restoring the balance of the budget to a counter-cyclical position.

Table 4 and Table 5 provide the Johansen test results on co-integration between revenues and expenditures. Cointegration is rejected through the Engel-Granger procedure, with a small exception when a quadratic deterministic trend is included in the cointegration equation. These results suggested that given the fiscal data from this paper, Romania can consolidate a sustainable public budget process in the long run, economic coordinates allow this, but the preference for pro-cyclicality of adopted policies will negatively impact future generations. So, even if we can count on the growth of the economy by increasing public spending, the analysis of real data from the Romanian economy does not support such a theory, the trend shows that an increase in public spending leads to a decrease in consumption in the private sector. Moreover, there is still an effect that has so far been little analyzed in domestic literature: It increases the number of employees in the public sector and not in the private sector, which would prevent growth through entrepreneurship, innovation, and investment.

Considering these results, we can say that government revenues and expenditures in Romania did not reflect consumption stimulation and increases in this period were driven by a particular component of aggregate demand, with a real problem with the level of investment (on which future growth depends).

From a brief retrospective of both unit-root tests and co-integration results, we can say that the picture on solvency of Romanian public finances, since 1990, marked all the important periods, with the post-communist situation, the economic crisis, and the economic recovery and fiscal consolidation efforts. Of course, in terms of the implications of data series on research results, in prospective consolidation from the second part of the study, we will not report to the entire sample, but we will relate to the variation and the mean of some variables of interest.

4. A Prospective Approach of Fiscal Sustainability in Romania

Keep in gin mind the main objective of this paper and citing the previous section, for a good understanding of current Romanian public finance challenges and vulnerabilities, we have analyzed the fiscal developments of the last three decades, whilst at the same time highlighting a general picture of the macroeconomic and budgetary trends. This outline allowed a good understanding of the Romania’s fiscal policy and the trend of decisions in this area, with a clear delineation of the preference for pro-cyclical or anti-cyclical measures.

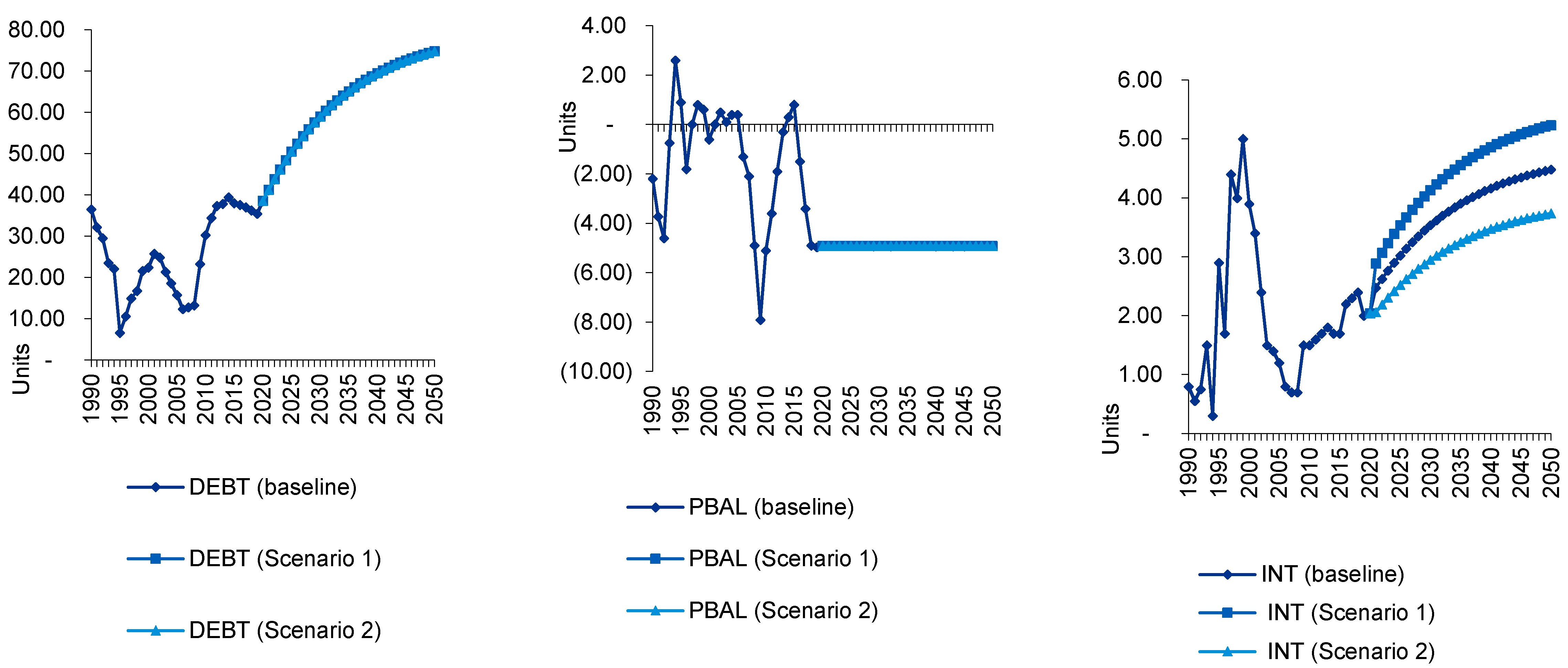

In this section, to explain and to capture the behavior of Romanian government decisions in fiscal policy and the path to fiscal sustainability, we used an estimation model of Romanian public finances. The period under review was from 1990 to 2020, and considering the objective to consolidate a prospective picture of fiscal variables, we used it as a baseline scenario. So, to bring an innovation to our study, we simulated starting from the baseline situation, a future trend of fiscal-budgetary variables, which allows an analysis of the consequences of budgetary sustainability in the case of modification in the mandatory factors. Given the implication of the post-communist period, we assumed in the baseline scenario, variations in the most recent 10 years, and depending on the status of each variable, we chose to address either the variation of the variables or the average of the last 10 years under analysis. Given that almost all fiscal variables were interdependent, and in the specialized literature we identified vague delimitation of the specific interferences, we illustrate in Table 6 a short sustainability model of Romanian public finances. All the variables used in the study are described in Table 7, which adds to Table 6 and explains the macroeconomic and fiscal variables reported at the beginning of our study in Figure 1. An interesting analysis of three cases scenarios, highlighting the future trend in public finances is shown in Reference (Konings and van Aarle 2011).

The model proposed by us in Table 6, used in the first equation a way to ascertain the dynamics of the debt-to GDP ratio (B/Y), as an outcome of the deficit to GDP ratio D/Y, the GDP growth rate, and a stock-flow adjustment, named (sfadj) in this paper. The stock-flow adjustment is the difference between the government debt change and the public deficit/surplus over a given period. Stock flow adjustments occur, for example, through the acquisition of financial assets

The Equation (2) defined the deficit, and Equations (3)–(5) and (7)–(9) were explained in the previous table. Equation (6) relates to the nominal interest rate, which is most often calculated according to the inflation rate and is calculated as the sum of the latter and the real interest rate, (real interest rate (r) + expected inflation (). After we had run the regression of the Romanian long-term interest rate differential on the level of debt, results suggested a value of α is 0.012. Considering implications from the debt level means that the debt-dynamics become quadratic in the debt level, since (1)–(7) imply:

To outline a prospective image, in the second part of this study, we performed a simulation based on the previously exemplified model, considering the most viable aspects of the baseline scenario (retrospective approach). Firstly, we set a baseline scenario for the exogenous variables in the model for the period 2020–2050, and then we analyzed the consequences on budgetary sustainability of several alternative scenarios. Even though this baseline scenario should not necessarily be considered the most likely, the dynamics of political choices, often dictating the future of sustainable development, given the fact that we offer several features, it could be a useful benchmark. Second, we divide the six latter scenarios into three main categories: Changes in the real interest rate (S1 > 1%, S2 < 1%) are assumed to be 1%, as a result of the trend over the last 4 years, averaging 1%; Growth rate changes (S3 > 1% S4 < 1%) in the present case, because the growth rate depends on a number of factors with the first change being possible and as a result of momentary decisions, we have reported the average of the last 10 years (2010–2020 ); In the third case (S5 > 1%, S6 < 1%), we have made changes to the primary fiscal balance, also referring to the average of the last ten years.

The current crisis has brought into discussion the determinant role that public finances have in macroeconomic stability. Even if the public debt path provides a long-term perspective regarding the sustainability of public finances, Romania needs a sustained annual growth to keep public debt on a sustainable footing. Moreover, there are many variables that dictate the path of a viable fiscal consolidation process and many more considerations that need to be looked at distinctly. For example, a higher interest rate on loans will lead to an increase in the public debt/GDP ratio. An increase of 100 basis points in the real interest rate may add the equivalent of 1.1% of GDP to the public debt. A 5% depreciation of the RON against the EUR, may add the equivalent of 1% of GDP to the public debt (expressed in RON). In the short term, the risk of depreciation of the leu can be boosted by both a higher interest rate on loans and an under-expected growth of the economy, and/or achieving a level of budget revenues under the proposed target.

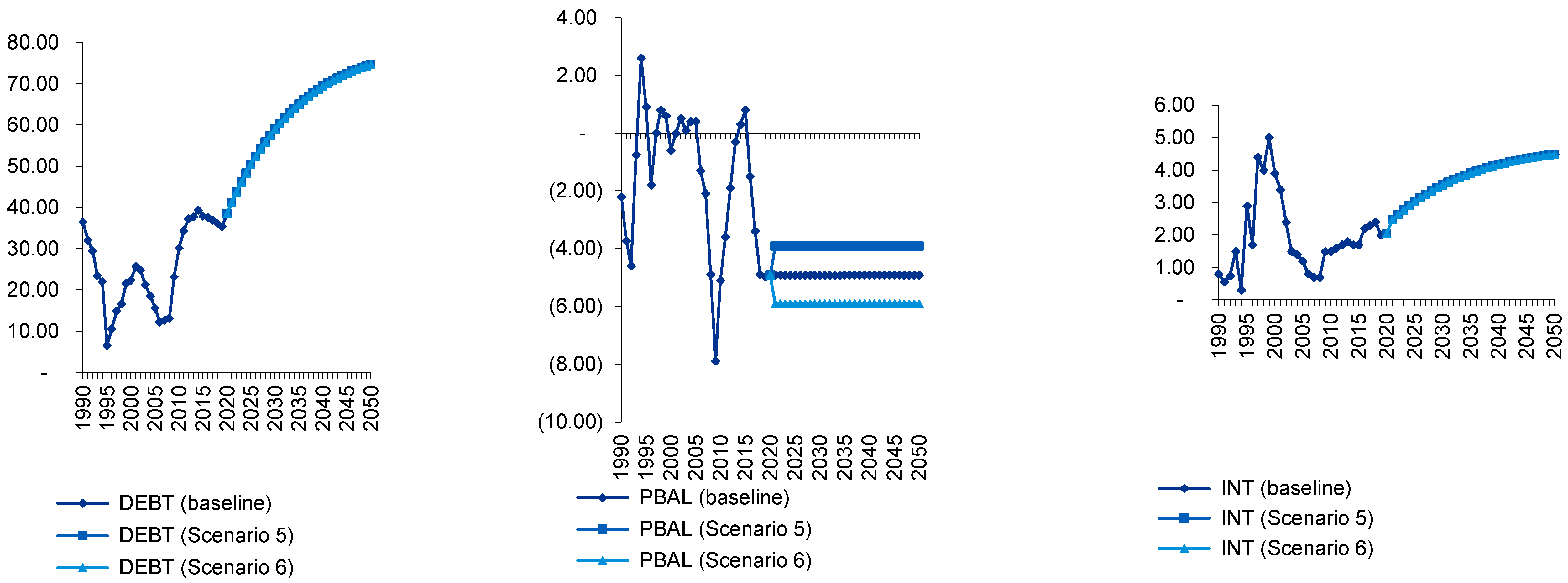

4.1.The Implication of Interest Rate Changes

As we can see in the scenario below (Figure 2), changes in interest rates affect some of the fiscal variables addressed in the analysis. This scenario illustrates the importance of the relationship between interest rates, exchange rates, and inflation, resulting from their impact and volatility on economic equilibrium. With higher levels of public debt, public finances become more sensitive to changes in interest rates, precisely because of the impact on the fiscal balance. For emerging economies such as Romania, public debts have an important role in economic development and in producing real returns, output growth, and supporting fiscal restraint in ensuring sustainability; therefore, it is important to take into account that changes in interest rates may have direct implications on the right itinerary.

In this case, the effects of a 1% change in the interest rate are analyzed, a similar result would be achieved if we applied a 1% shock on the risk premium. Whilst economic growth is a stabilizing factor, changes in interest rates are a destabilizing factor for debt versus GDP dynamics. A higher interest rate implies not only a greater burden on overdue debts, but also greater instability with rising government debt figures. By comparison with the baseline scenario, an increase in the interest rate implies a long-term fiscal deterioration. However, although the decrease may be the path to fiscal consolidation, we must also remember that this effect is supported to a small extent by the risk nonlinearity (risk premium).

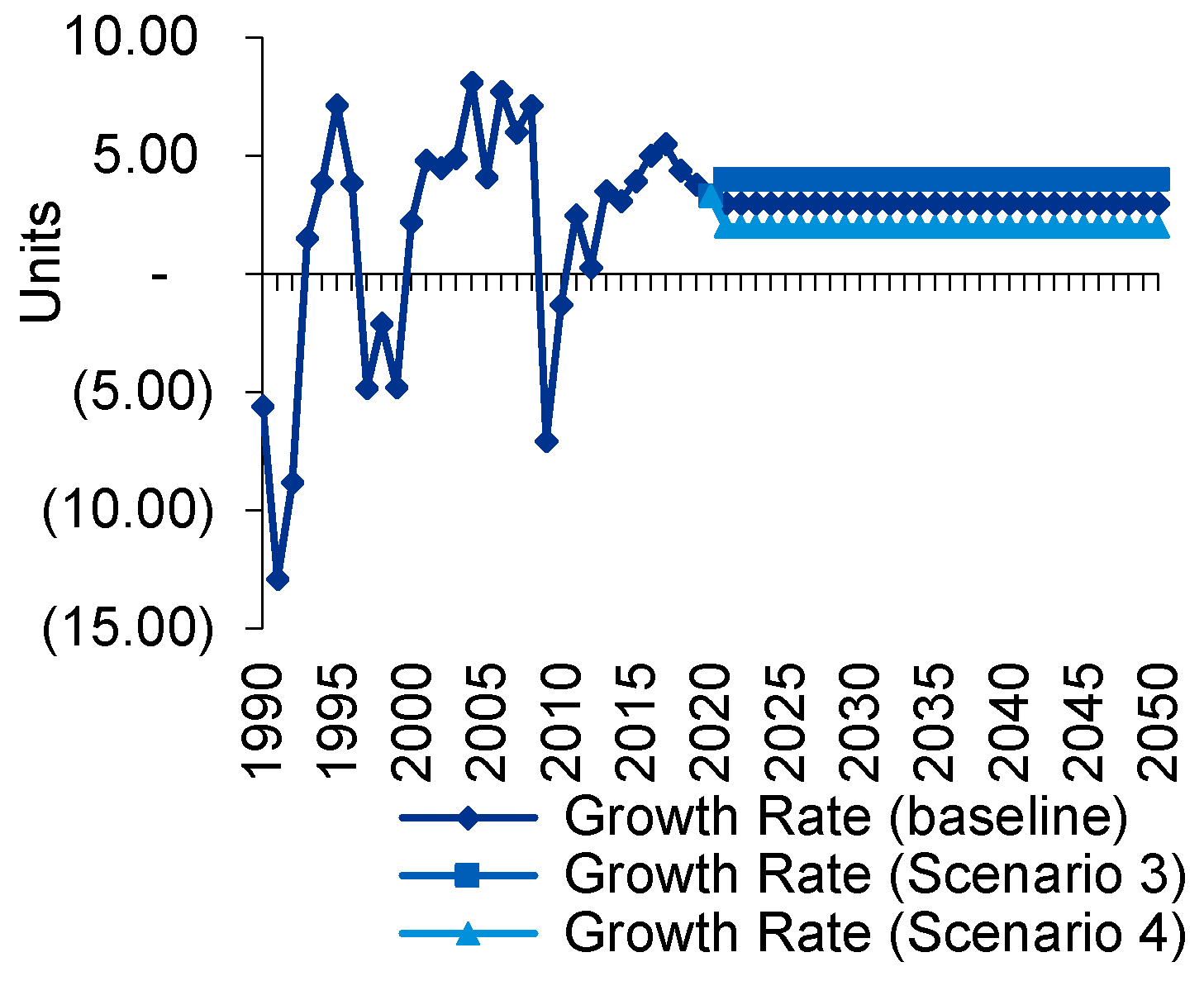

4.2. Implications of Growth Rate Changes

Figure 3 simulates the results that may occur in the case of a 1% improvement in the growth rate (decrease), compared to the baseline scenario. We can see that any minimal but sustained changes to growth have direct implications on public finances. The impact of growth changes on debt dynamics, declining pathways, and all tax variables is improving. This leads to the conclusion that the correct use of fiscal stimuli and the preference for a fiscal policy that strengthens sustainable growth is not an impossible task but is dependent on the political decision-making power guided by the most frequent political stakes and related costs.

The results illustrated by the second scenario reiterate the idea that sustainable economic growth fully determines the fiscal bases from which government expenditures, deficits, and public debt can be financed. The uncertainty about sustainable long-term growth is generally high. Thus, these scenarios highlight the importance of assessing the impact of alternative growth assumptions on public finances. Given that economic growth determines the tax bases on which government spending, deficits, and debt can be funded, the allocation of attention on this matter is important. Uncertainty about the economy is highlighted by this scenario, in which case we can see that though the Romanian government announced and is trying to implement different measures to revive economic growth through restructuring and modernization of the private and public sectors, the trend in data contradicts the viability of these measures and raises a question as to the economic, political, and social limits. Indeed, even if from a theoretical point of view, the Romanian government can significantly change the data of the problem by addressing populist policies based on inflation financing of budget deficits, where such a scenario could be an important milestone in long-term positioning.

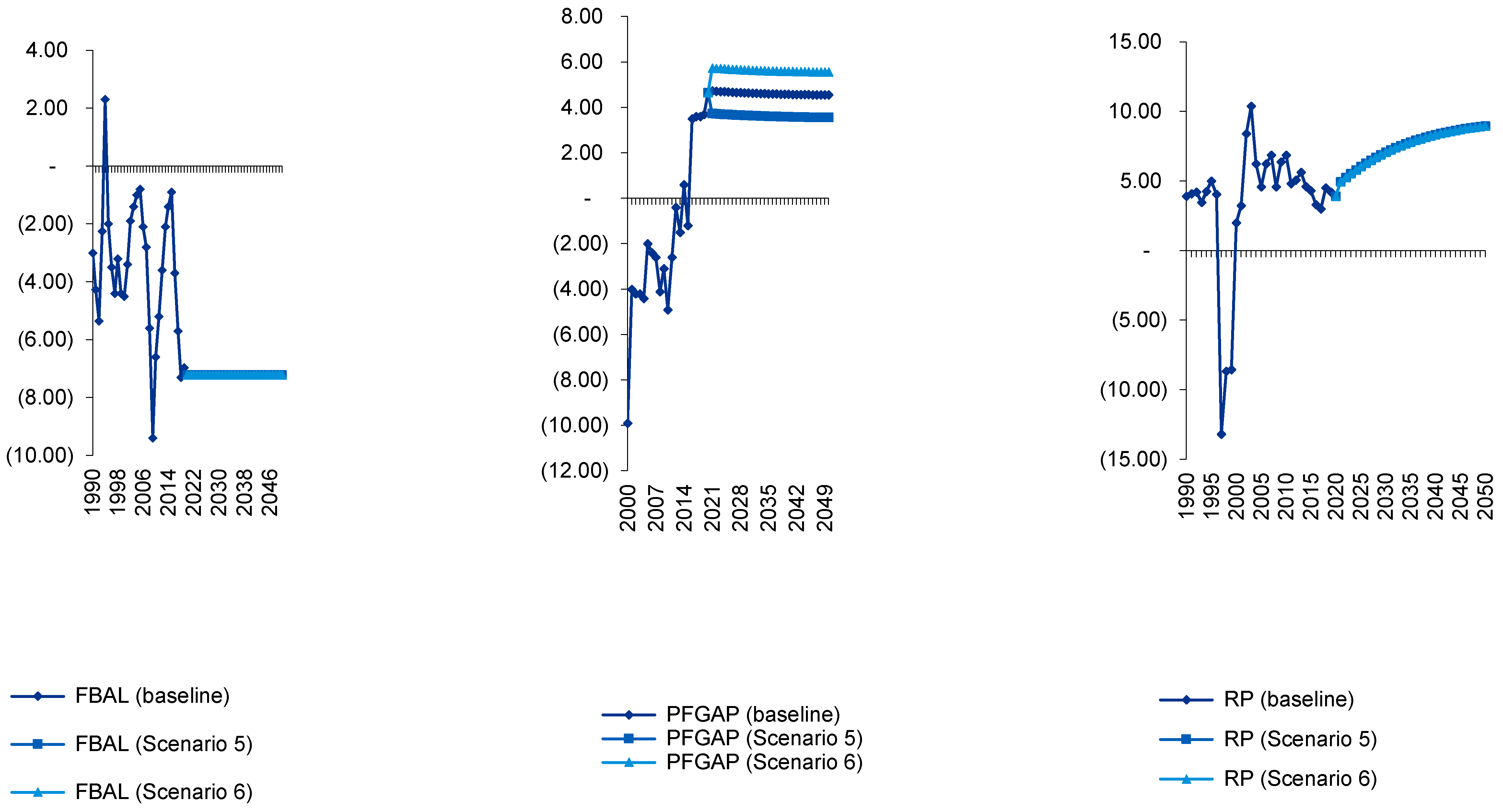

4.3. Primary Fiscal Balance Adjustments

Recent macroeconomic data, especially those on GDP growth, are weak, thus supporting the idea that strong action is needed by policy-makers. Adjustments in the primary fiscal balance are a crucial factor in controlling the sustainability of long-term public finances. Figure 4, through Scenarios 5 and 6 consider fiscal consolidation (expansion) in efforts to reduce (increase) primary government spending over 2020–2050. Over this period, a primary surplus of 1% is considered.

The analysis of the last scenario shows that the national context is characterized by lax implementation of fiscal sustainability programs. Even with an improvement (fiscal consolidation) at these coordinates, this would not be enough to judge long-term results. The way to reducing public debt in GDP, consolidate sustainable growth, and achieve a budgetary balance is not impossible, but it requires sustained efforts by policy-makers, in line with strategies that eliminate preference for pro-cyclical policies. In a weakly-functioning democracy, where governance in the ascending stages of the business cycle is being conducted through the poorer policies, there are some major dangers. Firstly, the recession is deepening and the level of production is reduced below potential. Secondly, the loss of conventional monetary policy can be achieved. This effect occurs if interest rates and inflation are low at the time of the recession. In other words, the monetary policy rate cut to zero may not be enough to stimulate exit from the recession and the rapid return of output to the potential, with central banks having to resort to unconventional monetary policies, such as quantitative relaxations. According to this last scenario analysis, it emphasizes the implications of a large sensitivity, predominantly from a long-term perspective of the Romania budgetary situation to small, permanent changes in the primary balance. Making a comparison with the baseline, we can deduce that any deterioration in primary fiscal balances inevitably implies a negative effect on fiscal sustainability. In fact, the results confirm some of the above-mentioned opinions in the specialized literature, emphasizing the importance of correlating fiscal changes in the long and medium term tothe macroeconomic context and the decisions and strategies for fiscal consolidation.

5. Discussion and Conclusions

The literature concerning the issue of Romanian public finance sustainability is limited and inconclusive. The link between the way to a sustainable fiscal policy and some variables with regards demographic elements, the costs of an ageing population, and consequently with the increasing spending on pensions and all social obligations derives from this, and yet is little studied. Even if some empirical studies highlight that the financial crisis showed inadvertent adoption of some wrong models for collective discipline, deepening the occurrence of fiscal indiscipline over most European countries, it is not clear what are the key changes and vulnerabilities of public finances and this is due perhaps to the fact that countries are not homogenous.

In this sample, we carried out an analysis regarding Romanian public finance sustainability, by using retrospective, as well as the prospective views. For the first approach, we concentrated mainly on empirical tests on Romanian government solvency during the last three decades, by applying standard unit root and co-integration tests, and to have a better understanding of the behavior of policy-makers, in the second part we used a scenario analysis of budgetary adjustment in the short and medium run, under alternative hypotheses. The results of this paper bring novelty to the existent empirical literature by studying the relationship between Romanian fiscal policy determinants and economic conjuncture from the last three decades, relating the context of the recent financial crisis, and investigating the future situation in a prospective view.

This approach in a double manner, allowed us to provide a general picture of de facto elements regarding the picture of public finances, and their correlation to the future of Romanian public finances. These results suggest that there is no evidence that Romania has run prudent fiscal policies capable to develop the country, and we can judge that the preference for pro-cyclical policies, along with social and economic limits reinforced the intergenerational effect of wasting political stakes, with the possible intergenerational effect. We have shown that the existing fiscal sustainability trends involve policy-makers’ efforts to manage the current political orientation to be sustainable in the long run. Consistent with the theory, we find that for practical purposes, long-term objectives and indicators are not useful enough and a short-term indicator is needed.

We have signaled the non-existence and the necessity of an independent body to monitor the applicability of fiscal rules (an independent Fiscal Council), designed to strengthen fiscal discipline and to contribute to improving the medium term fiscal planning.

The study shows, in both retrospective and prospective parts, a series of major challenges to the sustainability of public finances, highlighted by both public debt levels and an unsustainable growth rate, accompanied by high inflation in some years.

Interestingly, and in line with past literature findings, there appears to be some evidence that the primary balance is stationary during this period at a 10% confidence interval, but when applying the first difference, it becomes non-stationary. The fiscal gap is at the borderline between stationarity and non-stationary, given the first indication that the inter-temporal budgetary balance was not ensured in Romania, even before the fiscal decline in 2009. The non-stationarity of the public debt and the primary fiscal balance raises questions about the solvency of the budget. However, given the result of non-stationarity regarding the (primary) fiscal balance, we can say that intertemporal solvency was not thoroughly ensured in Romania during the last three decades.

The prospective image, relates to how changes in interest rates affects some of the fiscal variables addressed in the analysis. With higher levels of public debt, public finances become more sensitive to changes in interest rates, precisely because of the impact on the fiscal balance. The implication of growth rate changes highlight the importance of assessing the impact of alternative growth assumptions on public finances, and the analysis of the last scenario showed that the national context is characterized by poor implementation of fiscal sustainability programs. Even with an improvement (fiscal consolidation) at these coordinates, it would not be enough to judge long-term results.

Therefore, we conclude that the inappropriate diagram of economic policies in past years, and the lax implementation of fiscal policy will affect the position of the future generations, which have to bear the costs of political stakes and live in a poorly developed environment in economic, political, and social terms. The results also highlight the need to include both instruments for penalizing the policymakers with a preference for pro-cyclical policies, as well as an extended period of fiscal consolidation with the implications on political and social costs.

Author Contributions

Authors have equally contributed to the paper. Research methods were developed by I.B., A.F.G. performed the analyses and C.T. prepared the manuscript.

Acknowledgments

We are grateful for helpful comments from the Editor.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Afonso, António. 2005. Fiscal Sustainability: The Unpleasant European Case. Finanz Archiv 61: 19–44. [Google Scholar] [CrossRef]

- Afonso, António, and João Tovar Jalles. 2012. Revisiting Fiscal Sustainability: Panel Cointegration and Structural Breaks in Oecd Countries. ECB Working paper Series No. 1465; Frankfurt: European Central Bank. [Google Scholar]

- Afonso, António, and João Tovar Jalles. 2014. A Longer-Run Perspective on Fiscal Sustainability. Empirica 41: 821–47. [Google Scholar] [CrossRef]

- Afonso, António, and Christophe Rault. 2008. 3-Step Analysis of Public Finances Sustainability: The Case of the European Union. ECB Working Paper No. 908. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1138608 (accessed on 14 February 2017).

- Afonso, António, and Christophe Rault. 2010. What Do We Really Know about Fiscal Sustainability in the EU? A Panel Data Diagnostic. Review of World Economics 145: 731–55. [Google Scholar] [CrossRef]

- Alho, Juha M., Svend E. Hougaard Jensen, and Jukka Lassila. 2008. Uncertain Demographics and Fiscal Sustainability. Cambridge: Cambridge University Press. [Google Scholar]

- Badinger, Harald, and Wolf Heinrich Reuter. 2015. Measurement of Fiscal Rules: Introducing the Application of Partially Ordered Set (POSET) Theory. Journal of Macroeconomics 43: 108–23. [Google Scholar] [CrossRef] [Green Version]

- Bergman, U. M., M. M. Hutchison, and S. E. H. Jensen. 2016. Promoting Sustainable Public Finances in the European Union: The Role of Fiscal Rules and Government Efficiency. European Journal ofPolitical Economy 44: 1–9. [Google Scholar] [CrossRef]

- Blanchard, Olivier, Jean-Claude Chouraqui, Robert P. Hagemann, and Nicola Sartor. 1990. The Sustainability Fiscal Policy: New Answers to an Old Questions. OECD Economic Studies 15: 1–36. [Google Scholar]

- Bohn, Henning. 1991. The Sustainability of Budget Deficits with Lump-Sum and with Income-Based Taxation. Journal of Money, Credit and Banking 23: 580. Available online: http://www.jstor.org/stable/1992692 (accessed on 12 May 2018).

- Boiciuc, Ioana. 2015. The Cyclical Behavior of Fiscal Policy in Romania. Procedia Economics and Finance 32: 286–91. Available online: http://linkinghub.elsevier.com/retrieve/pii/S2212567115013933 (accessed on 5 June 2018).

- Canagarajah, Sudharshan, Martin Brownbridge, Anca Paliu, and Ionut Dumitru. 2012. The Challenges to Long Run Fiscal Sustainability in Romania. Policy Research Working paper No. 5927. Washington, DC, USA: The World Bank, pp. 1–32. [Google Scholar]

- Chan-Lau, Jorge A., and Andre Oliveira Santos. 2010. Public Debt Sustainability and Management in a Compound Option Framework. Washington, DC: International Monetary Fund, Available online: http://www.ssrn.com/abstract=1536508 (accessed on 9 March 2018).

- Ewijk, Casper Van, Nick Draper, Harry Rele, and Ed Westerhout. 2006. Ageing and the Sustainability of Dutch Public Finances. The Hague: CPB Netherlands Bureau for Economic Policy Analysis. [Google Scholar]

- Fatás, Antonio, and Ilian Mihov. 2009. Why Fiscal Stimulus Is Likely to Work. International Finance 12: 57–73. [Google Scholar] [CrossRef]

- Georgescu, George. 2014. Public Debt, Sovereign Risk and Sustainable Development of Romania. Procedia Economics and Finance 8: 353–61. [Google Scholar] [CrossRef]

- Joireman, Jeff, David E. Sprott, and Eric R. Spangenberg. 2005. Fiscal Responsibility and the Consideration of Future Consequences. Personality and Individual Differences 39: 1159–68. [Google Scholar] [CrossRef]

- Konings, Joep, and Bas van Aarle. 2011. Sustainability of Belgian Public Finance: Challenges and Vulnerabilities. VIVES—Discussion paper No. 24. Leuven, Belgium: KU Leuven, pp. 1–16. Available online: https://lirias.kuleuven.be/bitstream/123456789/344922/1/VIVES DP24.pdf (accessed on 9 May 2018).

- Landolfo, Luigi. 2008. Assessing the Sustainability of Fiscal Policies: Empirical Evidence from the Euro Area and the United States. Journal of Applied Economics XI: 305–26. [Google Scholar]

- Mura, Petru-Ovidiu. 2015. Public finance sustainability in Romania. Recent developments. Annals of the University of Oradea, Economic Science Series 25: 757–69. [Google Scholar]

- Neaime, Simon. 2015. Sustainability of Budget Deficits and Public Debts in Selected European Union Countries. Journal of Economic Asymmetries 12: 1–21. [Google Scholar] [CrossRef]

- Neyapti, Bilin, and Zeynep Burcu Bulut-Cevik. 2014. Fiscal Efficiency, Redistribution and Welfare. Economic Modelling 41: 375–82. [Google Scholar] [CrossRef] [Green Version]

- Patricia, Ana. 2014. Sustainability of tax system in Romania. SEA: Practical Application of Science II: 327–32. [Google Scholar]

- Pinheiro, Maximiano, and Vanda Geraldes. 2007. MISS: A Model for Assessing the Sustainability of Public Social Security in Portugal. Banco de Portugal Occasional Paper No. 71. Available online: http://www.bportugal.pt/en-US/BdP Publications Research/OP200703.pdf (accessed on 10 March 2018).

- Polito, Vito, and Mike Wickens. 2005. Measuring Fiscal Sustainability. Centre for Dynamic Macroeconomic Analysis Conference Papers 44: 1–56. [Google Scholar]

- Radulescu, Doina Maria. 2003. An Assessment of Fiscal Sustainability in Romania. Post-Communist Economies 15: 259–76. [Google Scholar] [CrossRef]

- Săveanu, Tomina Gabriela. 2015. Determinants of Social Responsibility Expenditures of Small and Medium Enterprises from Bihor County. Annals of the University of Oradea, Economic Science Series 25: 567–75. [Google Scholar]

- Talpos, Ioan, and C. Enache. 2008. Fiscal Policy Sustainability in Romania. Annales Universitatis Oeconomica Apulensis Series II: 233–43. [Google Scholar]

- Tanner, Evan, and Issouf Samake. 2008. Probabilistic Sustainability of Public Debt: A Vector Autoregression Approach for Brazil, Mexico, and Turkey. IMF Staff Papers 55: 149–82. [Google Scholar] [CrossRef]

- Tiţa, Cristina (Bătuşaru), Alexandra (Vasile) Oţetea, and Ilie Banu. 2014. The Importance of a Medium-Term Budgetary Framework in Enhancing the Sustainability of Public Finances in Romania. Procedia Economics and Finance 16: 270–74. [Google Scholar] [CrossRef]

- Trehan, Bharat, and Carl E. Walsh. 1991. Testing Intertemporal Budget Constraints: Theory and Applications to U.S. Federal Budget and Current Account Deficits. Journal of Money, Credit, and Banking 23: 206–23. [Google Scholar] [CrossRef]

- Wilson, Clevo. 2010. Why Should Sustainable Finance Be given Priority? Accounting ResearchJournal 23: 267–80. Available online: http://www.emeraldinsight.com/doi/10.1108/10309611011092592 (accessed on 6 July 2018).

- Woo, Jaejoon, and Manmohan S. Kumar. 2015. Public Debt and Growth. Economica 82: 705–39. [Google Scholar] [CrossRef]

- Zaman, Gheorghe, and George Georgescu. 2011. Sovereign Risk and Debt Sustainability: Warning Levels for Romania. MPRA paper 32924. Munich, Germany: University Library of Munich, pp. 234–70. [Google Scholar]

Figure 1.

Fiscal and macro-economic variables, Romanian, 1990–2020. Source: AMECO and Knoema World Data Atlas. Source: AMECO, Atlas World Data Knoema, and https://www.statista.com for forecasts 2018–2020.

Figure 1.

Fiscal and macro-economic variables, Romanian, 1990–2020. Source: AMECO and Knoema World Data Atlas. Source: AMECO, Atlas World Data Knoema, and https://www.statista.com for forecasts 2018–2020.

Figure 2.

Baseline scenario Romanian public finances 2020–2050, 1% decrease in the interest rate of 1% (case of scenario 1) vs. 1% increase in the interest rate case of scenario 2).

Figure 2.

Baseline scenario Romanian public finances 2020–2050, 1% decrease in the interest rate of 1% (case of scenario 1) vs. 1% increase in the interest rate case of scenario 2).

Figure 3.

Baseline scenario Romanian public finances 2020–2050 (dark blue lines), 1% increase in the real GDP growth rate of 1% (Scenario 3) vs. 1% decrease in the real GDP growth rate (Scenario 4).

Figure 3.

Baseline scenario Romanian public finances 2020–2050 (dark blue lines), 1% increase in the real GDP growth rate of 1% (Scenario 3) vs. 1% decrease in the real GDP growth rate (Scenario 4).

Figure 4.

Baseline scenario Romanian public finances 2020–2050, a fiscal consolidation effort of 1% of GDP during 2020–2050, (Scenario 5,) vs. a fiscal spending deterioration of 1% of GDP during 2020–2050 (Scenario 6).

Figure 4.

Baseline scenario Romanian public finances 2020–2050, a fiscal consolidation effort of 1% of GDP during 2020–2050, (Scenario 5,) vs. a fiscal spending deterioration of 1% of GDP during 2020–2050 (Scenario 6).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Unit root test results.

| Variables | Deterministics | ADF | PP | ||

|---|---|---|---|---|---|

| t-Stat | Prob | t-Stat | Prob | ||

| Government gross debt | None | −0.08 | (0.9333) | −0.08 | (0.9333) |

| Intercept | −2.25 | (0.0337) | −1.2 | (0.2371) | |

| Intercept and trend | −1.24 | (0.2261) | −1.24 | (0.2261) | |

| Fiscal balance | None | −1.31 | (0.2014) | −1.31 | (0.2014) |

| Intercept | −3.70 | (0.001) | −2.81 | (0.0089) | |

| Intercept and trend | −4.32 | (0.0005) | −2.76 | (0.0102) | |

| Prim. government | |||||

| spending | None | 0.35 | (0.7293) | 0.35 | (0.7293) |

| Intercept | −2.20 | (0.0362) | −2.2 | (0.0362) | |

| Intercept and trend | −1.84 | (0.0768) | −1.84 | (0.0768) | |

| Primary balance | None | −1.01 | (0.3227) | −1.01 | (0.3227) |

| Intercept | −3.12 | (0.0044) | −1.97 | (0.0587) | |

| Intercept and trend | −3.19 | (0.0038) | −2.12 | (0.043) | |

| Primary fiscal gap | None | −1.08 | (0.2886) | −1.4 | (0.1715) |

| Intercept | −3.22 | (0.0033) | −3.22 | (0.0033) | |

| Intercept and trend | −4.53 | (0.0001) | −4.53 | (0.0001) | |

| Government revenue | None | 0.49 | (0.6279) | 0.42 | (0.6758) |

| Intercept | −2.54 | (0.0186) | −1.94 | (0.062) | |

| Intercept and trend | −1.70 | (0.101) | −1.7 | (0.101) |

Note: Augmented Dickey-Fuller and Phillips-Perron unit root tests. Sample: 1986–2016, test statistic and p-value (in parenthesis).

Table 2.

Johansen test on co-integration between the primary deficit and government debt.

| Johansen | Primary Deficit and Debt | ||||

|---|---|---|---|---|---|

| Data Trend: | None | None | Linear | Linear | Quadratic |

| Test Type | No Intercept | Intercept | Intercept | Intercept | Intercept |

| No | |||||

| No Trend | No Trend | Trend | Trend | Trend | |

| Trace | 0 | 0 | 0 | 0 | 0 |

| Max-Eig | 0 | 0 | 0 | 0 | 0 |

Critical values based on MacKinnon-Haug-Michelis (1999).

Table 3.

Engle-Granger test on co-integration between the primary deficit and government debt. Engle-Granger Null hypothesis: Series are not cointegrated, Cointegrating equation deterministic: C.

Table 3.

Engle-Granger test on co-integration between the primary deficit and government debt. Engle-Granger Null hypothesis: Series are not cointegrated, Cointegrating equation deterministic: C.

| Dependent | t-Stat | Prob.* | z-Stat | Prob.* |

|---|---|---|---|---|

| PBAL | −3.18 | 0.1 | −22.89 | 0.01 |

| DEBT | −2.26 | 0.41 | −16.17 | 0.06 |

* MacKinnon (1996) p-values, automatic lags specification based on Schwarz criterion.

Table 4.

Johansen test on co-integration between revenues and expenditures.

| Revenues and Expenditures | |||||

|---|---|---|---|---|---|

| Data Trend: | None | None | Linear | Linear | Quadratic |

| Test Type | No Intercept | Intercept | Intercept | Intercept | Intercept |

| No | |||||

| No Trend | No Trend | Trend | Trend | Trend | |

| Trace | 0 | 0 | 0 | 0 | 0 |

| Max-Eig | 0 | 0 | 0 | 0 | 0 |

Table 5.

The results of Engle-Granger test on co-integration between revenues and spending.

| Dependent | t-Stat | Prob.* | z-Stat | Prob.* |

|---|---|---|---|---|

| REV | 2.83 | 0.19 | −16.69 | 0.05 |

| GEXNINT | 2.32 | 0.38 | −9.08 | 0.36 |

* MacKinnon (1996) p-values.

Table 6.

A designed model of the Romanian public finances.

| Equation (1) | |

| Equation (2) | |

| Equation (3) | |

| Equation (4) | |

| Equation (5) | |

| Equation (6) | |

| Equation (7) | |

| Equation (8) | |

| Equation (9) |

Table 7.

Variables employed in data analysis.

| Code | Variable | Definition | Data Source |

|---|---|---|---|

| DEBT | Government debt (DEBT, % GDP) | Debt owed by a government | |

| FBAL | Fiscal balance (FBAL, % GDP) | The mirror of all budget revenues and expenditures. | AMECO |

| INT | Interest payments (INT, % GDP) | Payments made from the state budget to the public debt account | AMECO |

| PFBAL | Primary fiscal gap (PFGAP, % GDP) | By reference to Equation (4), is the difference between the Fiscal Balance and the interest payments, as defined in Equation (5). | AMECO database and Knoema World Data Atlas. |

| GROWTHN | Nominal GDP growth (GROWTHN, %) | Equation (8) explains this variable as the sum of real growth and the rate of inflation. An essential concept for public debt projection. | AMECO |

| LTINT | Long term interest rate (LTINT %) | It refers to long-term government bonds, more precisely, with a maturity of ten years | AMECO |

| RP | Risk premium (RP %) | Indicates rate risk in government bonds, and according to Equation (7) our model assumes this depends on the level of debt | AMECO |

| INTGROWDIF | Interest growth differential (INTGROWDIF %) | Represents the difference between the interest rate paid on government debt and the growth rate of GDP and drives the inertial or “snowball” dynamics of the debt ratio. It is a key concept in assessing fiscal sustainability. | AMECO database and Knoema World Data Atlas. |

| REV | Government revenue (REV% GDP) | An important instrument of government and fiscal policy, all sources of public spending financing | AMECO |

| GEXNINT | Primary government spending (GEXNINT % GDP) | According to Equation (3), this variable includes an essential element, more exactly, the expenditures that are related to ageing, being the sum between these, primary expenditures, G^P/Y and interest expenditures (in % of GDP). | AMECO |

| REALGROWTH | Real GDP growth (%) | Real GDP = GDP/(1 + Inflation since base year). Based on Equation (8), we found that in regard to the concept of nominal growth, we use the sum of real growth and inflation. | AMECO |

| INFL | Inflation (%) | An increase in the overall price level for both goods and services as purchasing power decreases, or as an increase in the price level from one year to the next year. | AMECO |

| INT | Real interest rate | Based on Fisher equation, the real interest rate = nominal interest rate − the inflation rates | AMECO |

| SFADJ | Stock-flow adjustment (SFADJ, % GDP | Explains the difference between the change in government debt and the government deficit/surplus for a given period | AMECO database and Knoema World Data Atlas. |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Bostan, I.; Toderașcu, C.; Gavriluţă, A.F. Challenges and Vulnerabilities on Public Finance Sustainability. A Romanian Case Study. J. Risk Financial Manag. 2018, 11, 55. https://doi.org/10.3390/jrfm11030055

AMA Style

Bostan I, Toderașcu C, Gavriluţă AF. Challenges and Vulnerabilities on Public Finance Sustainability. A Romanian Case Study. Journal of Risk and Financial Management. 2018; 11(3):55. https://doi.org/10.3390/jrfm11030055

Chicago/Turabian StyleBostan, Ionel, Carmen Toderașcu, and Anca Florentina Gavriluţă (Vatamanu). 2018. "Challenges and Vulnerabilities on Public Finance Sustainability. A Romanian Case Study" Journal of Risk and Financial Management 11, no. 3: 55. https://doi.org/10.3390/jrfm11030055