How Can European Regulation on ESG Impact Business Globally?

School of International and Public Affairs, Columbia University, New York, NY 10027, USA

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2022, 15(7), 291; https://doi.org/10.3390/jrfm15070291

Submission received: 24 April 2022

/

Revised: 16 June 2022

/

Accepted: 20 June 2022

/

Published: 30 June 2022

(This article belongs to the Special Issue Advances in Sustainable Accounting and Finance)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:The European Union (EU) has impacted regulation worldwide in areas ranging from data protection to trade or antitrust. In select fields, it has defined stringent standards and has had an impact on global business because of the size of its market and the price of participating in it. The purpose of this paper is to analyze the main provisions of the EU regulation on Environmental, Social, and Governance (ESG) and determine whether and how it will have an impact on business globally, including regulations around disclosure for companies, taxonomy for the asset management sector, supply chain due diligence requirements, new mechanisms such as carbon markets, or non-tariffs restrictions on international trade. For this, our analysis includes an in-depth review of the literature on EU regulation of the past 20 years, complemented with interviews with experts in the field, in order to understand the main tools used by European policymakers in ESG regulations to understand their effect. The analysis adds to the body of research pertaining to the impact of regulation on business and the growing body of research on sustainable finance. We find that the new ESG regulation impacts countries outside of the EU, influencing regulation worldwide, and raising the question of possible regulatory arbitrage.

1. Introduction

Over the past two decades, climate change has become a central concern for policymakers, companies, and public opinion, with climate action being the United Nations’ #13 sustainable development goal. The evidence is unequivocal: the rise in temperature of approximately 1.20 °C for the past two centuries; the top 100 m of the ocean have warmed more than 0.3 °C; and its surface has become more acidic due to carbon dioxide emissions. This, in turn, has caused a reduction in ice sheets and glaciers, rising the global sea level 20 cm and increasing the number of natural disasters due to climate change. Furthermore, this trend is accelerating (Earth Science Communications Team 2022).

It is therefore essential to develop a financial model that incorporates environmental and social sustainability. Climate change and environmental issues have been on the agenda of the world’s policymakers for decades, but it has not been until recently that they have stepped up their efforts to curb climate change and its impacts. In particular, requests for transparency and in-depth data regarding environmental risks, and mitigating actions, grouped with audits to enhance reliability, have been demanded from companies across the globe. What was initially treated as a reputational risk by corporates went on to be cemented by new regulatory standards. ESG—in particular its environmental portion—is considered a top risk for companies and investors today. In fact, even the threat of regulation can send a signal to investors and companies to adjust accordingly. Shareholders have also increased their involvement exponentially over the past years; their engagement with companies are increasingly related to ESG matters. Finally, customers are demanding companies improve their performance and help mitigate climate change and other pressing issues for society. According to data from Sprout Social, 70% of consumers consider that it is of utmost importance for companies to take a public stand on political and social issues (Sprout Social 2019). Moreover, the introduction of social media and the hike in its use has intensified this pressure.

Furthermore, lawmakers worldwide are also stepping up their efforts by issuing legislation aimed at tackling climate change. To this end, the European Union has put forward a set of standards to regulate ESG matters, including regulations around disclosure for companies, taxonomy for the asset management sector, due diligence requirements, new mechanisms such as carbon markets, or non-tariffs restrictions on international trade.

In the past decades, we have seen an increasing global interdependence in terms of regulation. Lawmakers are often affected by decisions made by decision-makers in other regions of the world due to this global interdependence and, as a result, both legal and natural persons are affected by legislation issued both in their country and overseas. In this regard, the European Union has led the path for countries worldwide in a wide variety of regulations, setting high standards in aspects like banking services and social protection.

The literature related to this phenomenon is well-articulated. The “Brussels Effect”, a term coined in 2012 by Anu Bradford, Columbia Law School Professor, refers to the European Union’s ability to set global standards for industrial and financial rules and regulations. “The EU is not generally thought of as an aggressive economic hegemon, but in sector after sector, it has set the rules for the world economy” (Beattie 2020), according to Bradford. This concept further explains another kind of power in contrast to that commonly understood in terms of military or economic: regulatory power.

Studies have shown how the European Union regulation is exported through market mechanisms and, to a certain extent, models regulation in third countries (Gady 2014; Lavenex 2014). Literature around the “Brussels Effect” contributes empirical evidence on how this effect takes place on matters such as international trade, waste and chemicals legislation, data regulation, and, finally, Environmental, Social, and Governance. Examples of this phenomenon include the European legislation on waste (Restrictions on Hazardous Substances—RoHs, Waste of Electronic Equipment—WEE) and on chemicals (Registration, Evaluation, Authorisation of Chemicals—REACH), or the General Data Protection Regulation (GDPR). These are considered pioneers in their fields and because of this, multinationals decided to adopt these standards for all their subsidiaries for efficiency and effectiveness (Golberg 2019).

This paper further analyzes the “Brussels Effect” on global businesses in the field of ESG, by reviewing the growing body of European ESG legislative measures, which are ultimately aimed at the decarbonization of the economy. This is analyzed from a perspective of whether the recent set of standards from the European Union might have an impact on countries’ legislations outside the EU, as well as on business globally. In addition to the regulator, European businesses, from both a shareholder and a corporate perspective, have been a significant driver of this ultimate set of thorough legislation.

We thus aim to contribute to the ongoing debate regarding the influence of the European Union in terms of setting global standards. For this, we explore three key topics: (i) the impact on disclosure, tax, and trade; (ii) the impact on investment activities, following the recent set of standards issued by the European Commission; and (iii) the potential regulatory arbitrage that might arise from diverging regulations between countries where business are based and operate. In this regard, we take into account current legislation being discussed abroad as well as key considerations from lawmakers and decision-makers in several countries.

The key findings of this paper conclude that the EU ESG regulation impacts business globally, derived mainly from three main considerations: (i) the scope of the standards themselves, which involves countries outside of the EU; (ii) past empirical evidence suggesting that the European Union has already impacted policy choices and business operations globally, due to the size of its market as well as the opportunity cost of not being able to operate in it; and finally, (iii) the European Union’s involvement in global institutions such as the Task Force on Climate-related Financial Disclosures (TFCD).

This paper has the following structure. Section 2 provides a literature review of the EU Law at the forefront of ESG considerations with empirical evidence. Section 3 offers an overview of the new ambitious toolkit that the European Union has set to regulate ESG considerations. Section 4 analyzes the implications of the “ESG Brussels Effect” worldwide and highlights the risk of regulatory arbitrage. Section 5 discusses the findings and concludes by establishing the need for policymakers to cooperate with each other to elaborate coherent regulation to prevent malpractices such as greenwashing and regulatory arbitrage, as well as advancing towards net-zero.

2. EU Law at the Forefront of ESG Considerations

2.1. The Decades-Long History of Environmental Law

From the First Earth Summit in 1972 to the United Nations Conference on Environment and Development in 1992, there was no major improvement in tackling climate change. Then, in 1992, circa 80% of the countries observed by the UN had signed its Framework Convention on Climate Change (UNFCCC), which entered into force in 1994 with the purpose of stabilizing atmospheric concentrations of CO2 (Jackson n.d.). The following year, the first Conference of the Parties to the UNFCC was held, and the Berlin Mandate was adopted, which aimed at more significant commitments regarding tackling climate change. Since then, several other agreements have taken place among the international community to prevent climate change’s potential disasters. These include the Kyoto Protocol, in 1997, which aimed at reducing emissions by 5% below 1990 levels before 2012 (Jackson n.d.).

At the 18th Conference of the Parties (COP) in 2012, delegates agreed to extend the Kyoto Protocol until 2020. They also reaffirmed their pledge from the previous COP to create a comprehensive and legally binding climate treaty including those major carbon emitters that decided to not abide by the Kyoto Protocol, such as China, India, and the United States (Jackson n.d.).

In 2015, the United Nations adopted the Sustainable Development Goals (SDGs), as part of the 2030 agenda. Two months later, the Paris Accord was adopted, effectively replacing the Kyoto Protocol, by the delegates at the 21st Conference of the Parties with the aim of limiting the increase in the world’s average temperature to no more than 2 °C above preindustrial levels (UNFCC n.d.).

Additionally, in 2015, the Financial Stability Board created the Task Force on Climate-related Financial Disclosures to develop recommendations for companies to be able to generate consistent climate-related financial risk disclosures to support investors, banks and insurance underwriters in the assessment and pricing of climate-related risks (FSB-TCFD 2022). TFCD has 3000-plus supporters from 95 jurisdictions, ranging from central banks, regulators, governments, and corporations, which aim to comply with the disclosure recommendations that TCFD issues (FSB-TCFD 2022).

Finally, the Glasgow COP26 summit brought parties together with the purpose of accelerating action towards the Paris Accord goals. The International Sustainability Standards Board (ISSB) was then created to enhance the comparability and harmonization of standards. The ISSB has been tasked with standardizing sustainability-reporting guidelines using the four pillars of the TCFD (International Financial Reporting Standards 2021). Experts in the field believe that the creation of the ISSB will be essential for setting a global baseline for company reporting on sustainability.

Not complying with the Paris Accord would have disastrous consequences. Research expects that by 2030, circa 10 million people a year will be exposed to heat stress exceeding the survivability threshold. Moreover, with current emissions, the average proportion of global cropland affected by severe drought will rise. Accelerated shifting weather patterns can be expected to cause higher mortality rates in the form of food insecurity, changes to ecosystems, and the rise of diseases. Overall, this can lead to political instability and international conflict (Quiggin et al. 2021).

Figure 1 presents the global reported natural disasters caused by the worsening conditions due to climate change for the past five decades.

During the COVID-19 pandemic, greenhouse gas emissions dropped just by 5% (National Aeronautics and Space Administration 2021), suggesting that the race to net-zero will require ambitious actions together with global coordination. The rapid increase in the rate of climate change, added to the current economic, public health, and social justice crises, has triggered a rising interest in ESG factors.

2.2. ESG Framework Is Becoming More Robust, Led by EU Regulations

ESG is a framework under which companies can be evaluated for a broad range of socially desirable targets. It describes a set of factors used to measure the non-financial impacts of particular investments and companies. ESG also provides a range of business and investment opportunities (Bergman et al. 2020). While evidence is building up that ESG can be a profitable approach to project selection for companies and investors (Miralles-Quirós et al. 2019), as well as corporate social responsibility overall leading to superior financial performance (Flammer 2015), regulators can play a role to create the right incentives and prohibitions to accelerate the transition toward a lower-carbon economy.

Europe has issued significant regulations on ESG during the past decade, being at the forefront today of ESG implementation globally. This regulatory activity has aimed to not only foster ESG investment, targeting investors to consider environmental, social, and governance issues in their investment decision process (TEG 2020), but also to control the required compliance of corporations with the ESG commitment and, overall, at the same time, be able to meet with the Paris Accord milestones.

This has been boosted for years by civil society, which has been able to establish standards across jurisdictions with a certain ease. Among others, CDP, a UK-based NGO, established a standard for transparent reporting on greenhouse gases. Today, virtually every Fortune 500 company reports to CDP, following their standards. Shareholders and investors have also started demanding corporates involvement in tackling climate change, which can be seen in shareholders’ proxy statements to companies. This has fostered ESG disclosure from corporates, especially when initiated by institutional investors, and even more so when initiated by long-term institutional investors (Flammer et al. 2019). A 2017 study on the relevance of time horizons for these investors has proved that long-term institutional investors tend to strongly take into consideration corporate social responsibility (CSR) for their investments (Boubaker et al. 2017). Activism additionally plays a key role in the ESG arena and, with social media on the rise, is impossible for corporates to ignore.

ESG-aligned goals also translate into a wide range of targets and mechanisms on the side of Governments. The European Commission aims at growing green infrastructure. The European Central Bank is engaged in greening the financial system, and together with other Central Banks, including the US Federal Reserve System, comprise the Network for Greening the Financial System (NGFS) (Network for Greening the Financial System 2020). The NGFS includes 83 Central Banks and supervisors and 13 observers, with countries representing around 75% of global greenhouse gas emissions (Network for Greening the Financial System 2020). They supervise all global systemically important banks and two-thirds of international systemically important insurers (Network for Greening the Financial System 2020). Ultimately, they share best practices in the financial sector, contribute to its environmental and climate risk management, and mobilize the transition of the industry toward a sustainable economy (Network for Greening the Financial System 2020).

The ESG market has grown exponentially in recent years. ESG funds in Europe have attracted record inflows of USD 233 billion in 2020, almost double that of 2019. Asset managers launched 505 new ESG funds and repurposed more than 250 conventional funds last year to meet the demand (Bioy et al. 2020, p. 1). The US had circa USD 49.9 billion in net inflows on ESG funds during 2020 (Stankiewicz 2021). Additionally, more than 70% of funds focused on ESG investments outperformed their counterparts in the first quarter of 2020, and approximately 60% of ESG funds outperformed the overall market in the past decade.

Factors such as COVID-19, overall social unrest, as well as climate extreme events, reinforcing economic trends such as decarbonization and digitalization, among others, will continue to make investors shift focus to ESG investing (Papadopoulos et al. 2020). This will come hand in hand with the growing concern of consumers in the market, especially millennials and women (Zachs Equity Research 2021). Indeed, recent studies have shown that investors are actively responding to companies that have ESG integrated into their strategy and operations (Hartzmark and Sussman 2019). Therefore, the “Brussels Effect” has been materializing for the past decades throughout a regional manifestation in Europe triggered by civil society and corporates, which has inevitably ended in a governmental manifestation. Thus, both demand and supply are placing a growing value on ESG. In this regard, industry leaders have actively generated more transparent and comprehensive sustainability reports, provided information to ESG rating agencies, and publicly communicated their ESG commitments (Bergman et al. 2020).

Figure 2 below shows the increase in annual European sustainable fund flows in the past decade, which has particularly spiked in 2019 and 2020.

Assuming 15% growth, as per Bloomberg data analyses, ESG assets under management could spike to more than a third of the USD 140.5 trillion global expected by 2025 reaching USD 53 trillion globally (Diab and Adams 2021). While Europe accounts for half of the global ESG assets, the US had the most robust expansion throughout 2021 and may eventually become the industry leader, potentially followed by Japan (Diab and Adams 2021).

To meet this growing demand, there has been a large increase in green, social, sustainable, and, overall, sustainability-related bonds. Thus, the ESG debt market could reach USD 11 trillion by 2025 from $2.2 trillion in 2021, according to Bloomberg (Diab and Adams 2021).

Europe’s ESG fund growth may serve as a critical indicator of what to expect globally. As stated by Morningstar, assets in sustainable funds in Europe increased about 52% in 2020 to reach EUR 1.1 trillion by the end of 2020, as shown in Figure 3 below, due to repurposed assets and substantial inflows, in addition to financial markets being on the rise (Bioy et al. 2020).

The EU is the largest economy globally with a GDP per capita of EUR 25,000 for its circa 450 million consumers and ranks first in both inbound and outbound investments (European Commission n.d.). The expectation of the increasing foreign direct ESG investment in Europe, together with Europe’s green transition, in the words of Christine Lagarde, “offers a unique opportunity to build a truly European capital market that transcends national borders” (Lagarde 2021).

Additionally, not only has the market of green bonds skyrocketed in the European Union since 2015, but also the region has established itself as the pick for these bonds’ issuance, with the origination of almost two-thirds of the global issuance of green bonds in 2020 (Lagarde 2021).

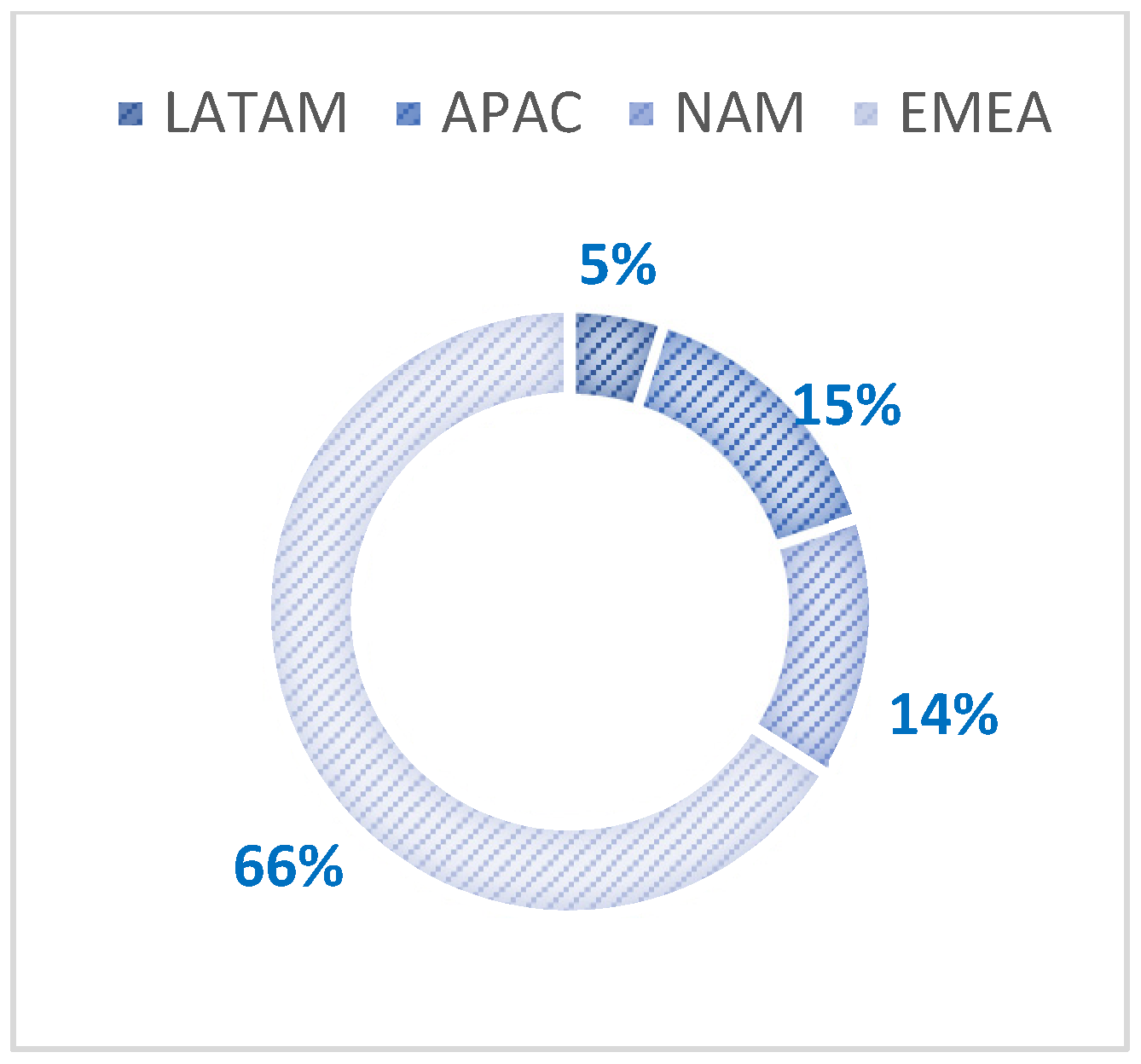

Figure 4 below shows the distribution of global bond issuance among the range of sustainable bond types, as well as the figure projected for 2022, which amounts to 1.5 trillion. Additionally, Figure 5 and Figure 6 break down the volume of global bond issuance per geography and currency respectively.

Finally, the Euro has become the global currency for sustainable finance, with a high 50% of global sustainable capital markets denominated in Euro vs. the 27% in USD (Janse and Bradford 2021). As a result of the high concentration of ESG funds and sustainable bonds emitted by the EU, it will inevitably attract significant non-EU investment, as has been witnessed in recent years.

2.3. Why ESG Matters for Corporates

ESG has become increasingly important not only for the demand side of investments but also for the supply side. The demand for sustainable assets has largely driven the supply of such assets and attracted the attention of companies. Since ESG’s remarkable rise in the 2000s, the literature has drawn attention to the fact that focusing on corporate social responsibility, far from generating worse results for companies—compared to those that do not attend to environmental matters in their decision-making—tends to achieve the opposite, increasing returns and reducing financial risk (Giese et al. 2019). Since Friedman, there has been a long debate about the relationship between CSR, firm value and performance. Despite more than 50 years of research, this topic presents many discussions and different points of view, and there is not a consensus about it (Carvalhal and Nakahodo 2022).

Studies range from different points of view on how ESG integration impacts financial performance, from valuation to higher returns. CSR practices can, at times, represent the goodwill of the firm’s managers in complying with their fiduciary duty of creating value for their shareholders (Godfrey et al. 2009).

El Ghoul et al. (2011) provide an answer to long-time calls on whether corporate social responsibility is priced by capital markets. Indeed, this study suggests that boosting CSR performance decreases the cost of equity for companies. The study involves both an insight into the cost of capital for companies that develop responsible product strategies, employee relations, and environmental policies, as well as companies in “sin” industries such as nuclear power and tobacco. The findings exhibit that positive CSR scores, such as those that the former companies have, result in cheaper access to equity financing, whereas negative CSR scores of the latter companies result in higher costs in terms of the cost of capital. The study argues this is achieved by lowering the perceived riskiness of the firm and a reduction in agency and asymmetry of information, both of which reduce the cost of equity, which at the same time directly impacts the required rate of return on corporate investments, enhancing the firm’s value (El Ghoul et al. 2011). This is how capital markets would trigger firms to become environmentally sustainable.

Gregory et al. (2014) investigated the effect of CSR on firm value, namely short-term growth, long-term growth, and the cost of capital, to identify the source of such value. Their results show that financial markets mostly value CSR in a positive way due to the fact that, in the long-run, firms that have incorporated ESG matters into their decision-making tend to outperform those that have not in terms of abnormal earnings growth.

ESG integration has therefore become a useful tool for companies to increase their valuation and financial performance via a multichannel process, respectively both through their profile in terms of systematic risk, lowering their costs of capital, and in terms of idiosyncratic risk, lowering exposure to tail risk (Giese et al. 2019). Thus, companies are slowly realizing that investing sustainably does not preclude them from generating top results. To realize these results, the structure of corporate governance, both internal and external, is the key to driving corporate environmental performance (Boubaker and Nguyen 2019).

Finally, recent studies have exhibited that during the COVID-19 pandemic and the subsequent financial crisis, those firms that had ESG integrated into their global strategy generally had better results than those companies that did not. Broadstock et al. (2020) furthered that, in fact, ESG performance acted as a financial risk mitigator during the crisis and considered that ESG integration was of more relevance during the pandemic, exposing an increasing overperformance during the financial crisis. Furthermore, Boubaker et al. (2022) showed that CSR practices improve the firm’s reputation, and thus those firms with high accounts receivable supporting these practices were able to better overcome the health crisis because customers were more willing to cooperate in paying back faster. This is supported by previous studies regarding the performance of ESG-integrated companies during the 2008–09 financial crisis: Cornett et al. (2016) (Lins et al. 2017) found that US financial institutions’ performance was positively associated to their ESG scores, an idea that Lins et al. (2017) (Cornett et al. 2016) supported for non-financial companies (Broadstock et al. 2020).

3. The EU Has Developed a Broad Toolkit around ESG

Since 2017, the European Commission has laid the critical foundations for a set of regulations for sustainable investing, with a focus on the mandate to companies to base their ESG claims on sound and detailed data. This set can be divided into the following main pillars: (i) Non-Financial Reporting Directive (NDFR); (ii) Second Shareholders Rights Directive (SRE II); (iii) Sustainable Finance Disclosure Regulation (SFDR); (iv) Prudential Legislative Texts integrating ESG risks into the broader risk framework; (v) Taxonomy Regulation for a strict assessment of investments before providing the environmentally sustainable label; (vi) EU Green Bond Standard; and (vii) proposal of extension of EU Ecolabel to the financial services’ industry.

The central norms of this set will be analyzed. The group of measures that make up the EU’s Action Plan on Sustainable Finance is a direct and ambitious response to the Paris Agreement’s targets and the need to mobilize more capital. The original Action Plan of 2018 was complemented in July 2021 by the publication of the EU’s Sustainable Finance Strategy, with a second wave of regulatory initiatives, including sustainability-linked and transition bonds, considerations on green mortgages, an expansion of the Taxonomy, and a clarification that investors’ fiduciary duty includes ESG considerations. In addition to regulatory action, the EU is also aligning its funding objectives with the Taxonomy and green bond standards.

The EU measures are of two types: conduct-based and prudential. The latter measures cover credit institutions and investment firms and involve integrating ESG risk into the broader prudential risk management framework. These measures also include integrating ESG risk into “Pillar III” disclosures, related to reporting requirements.

NFRD, SFDR, and the EU Taxonomy are essential for sustainability disclosure but overlap in certain items. In essence, the Taxonomy is a disclosure regulation that applies to companies and asset managers in the scope of SFDR and NFRD. SFDR and NFRD are focused on capturing and mitigating sustainability risks (Godemer 2021). NFRD is also essential as a conduct measure, the first ESG-related legislative text enacted.

3.1. Non-Financial Reporting Directive

The NFRD, which entered into force in 2017, requires in particular large EU corporates to disclose data on their firm’s impact on ESG and vice versa. The scope of the NFRD is European-listed and large public-interest companies with more than 500 employees and that have either a balance sheet total of more than EUR 20 million or a net turnover of more than EUR 40 million (European Commission 2014).

Under the current version of the Directive—the European Commission has recently proposed the Corporate Sustainability Reporting Directive, amending specific reporting requirements to it focusing on non-financial elements—large companies and all listed companies (notwithstanding micro-enterprises) will have to publish reports, which will then have to be audited, on their policies regarding environmental protection, social responsibility, human rights, anti-corruption and bribery, and board diversity. It includes reporting on gender equality, health, safety, or CO2 emissions. This report must cover both the risks and the associated mitigating activities. ESG disclosure is on a comply or explain basis (European Commission 2021).

3.2. Sustainable Financial Disclosure Regulations

The SFDR, which entered into force in December 2019 and started to apply in March 2021, is a set of rules that require firms to disclose information on their portfolios’ ESG risks and classify their products into categories that convey, at the same time, further disclosure requirements. The scope of SFDR is asset managers, financial advisors, and insurance providers in the European Union. This includes subsidiaries based in the EU, with their parent companies based in non-EU countries, in addition to non-EU companies that operate or market funds in the EU and, indirectly, to managers providing portfolio management and/or investment advice services to EU firms that are subject to the rules (European Commission 2019a). Furthermore, it includes specific disclosure requirements aimed at asset managers and financial advisors who do not work with any ESG or sustainability products or services (European Commission 2019a). A recent analysis by S&P Global (Mankikar 2021) found that companies outside the EU with a combined market capitalization greater than USD 3 trillion could be subject to SFDR (European Commission 2019b).

A key goal of SFDR is to tackle greenwashing, a phenomenon that has emerged with the disparity of voluntary measures that preceded this new regulation, by which companies disguise their activities into ESG plans to market themselves before consumers and also aim at complying with regulation. With SFDR, investors will have further insight into how a fund is complying with ESG objectives. Additionally, SFDR incorporates the concept of double materiality, both financial and non-financial (LSE Grantham Research Institute on Climate Change 2021). Therefore, SFDR aims at companies to be transparent about the sustainability risks that might have a negative impact on their investments and the negative impact that their investments might have on ESG items.

The main requirements that SFDR establishes are: (i) disclosure on their investments’ double materiality; (ii) statement of due diligence of sustainability risks and integration of sustainability factors in the remuneration policies; and (iii) transparency of the adverse sustainability impacts at the entity level as well as product level. For this purpose, the report should be performed on key data items called “Principal Adverse Impacts” (European Commission 2019c).

Under SFDR, managers will classify their funds into one of three categories, requiring different levels of disclosure. In particular, Article 6 requires all funds to provide a certain level of disclosure for all managed products, while Article 8 and Article 9 require further detail in the disclosures, the former of which is aimed at funds that aim at environmental or social goals, while the latter is aimed at funds with a sustainable objective (European Commission 2019c).

3.3. EU Taxonomy for Sustainable Activities

The EU Taxonomy regulation goes together with both the SFDR and the NFRD, aiming to create consistent environmentally sustainable standards. Article 3 sets a classification system, establishing the criteria for environmentally sustainable economic activities, against which the investment analyzed within NFDR parameters will be assessed (European Commission 2022). Article 9 of the Taxonomy covers six objectives and the mandate is for firms to contribute to at least one actively—either through economic activities that contribute to or financially support sustainable activities—with little to no harm to the rest. These objectives are: (i) climate change mitigation; (ii) climate change adaptation; (iii) the sustainable use and protection of water and marine resources; (iv) the transition to a circular economy; (v) pollution prevention and control; and (vi) the protection and restoration of biodiversity and ecosystems (European Commission 2020).

The Taxonomy also modifies specific items of the SFDR, introducing new financial disclosure requirements for products affected by the Taxonomy regulation. The modifications include additional rules covering pre-contractual disclosures and/or periodic reports for sustainable investments or investments with social or environmental characteristics (European Commission 2020). The scope of the EU Taxonomy is that of NFRD or SFDR, depending on whether it conveys specificities of the former or the latter. Regarding NFRD, it includes all companies to which NFRD is applicable. In terms of SFDR, it applies to financial participants in the scope of SFDR.

The specific request for companies and asset managers is to report information on the proportion of the turnover, capital expenditure, or operating expenditure of such large non-financial companies associated with environmentally sustainable economic activities and KPIs tailored for large financial companies (European Commission 2020).

3.4. Regulatory Technical Standards

A suite of Regulatory Technical Standards (RTS) has been compiled by the European Supervisory Authorities to enrich both the SFDR and the EU Taxonomy. It aims to strengthen disclosure requirements at the product level and confirm alignment with environmental objectives under the EU taxonomy. The standards include the details of the information regarding the Do No Significant Harm (DNSH) principle that applies to all sustainable investments (Joint Committee of the European Supervisory Authority 2021).

Additionally, the critical changes to product disclosure include: (i) identification of the environmental or social objectives towards which the product contributes; (ii) to what extent the investment is aligned to EU Taxonomy, including a third-party audit on compliance with the Taxonomy; and (iii) further insight into mandatory pre-contractual and periodic disclosure templates for financial products with environmental or social objectives (Joint Committee of the European Supervisory Authority 2021).

4. The “Brussels Effect”

4.1. The Impact on Disclosure, Tax, and Trade

The “Brussels Effect” arises when the world’s largest trading block issues a regulation in a sector, which has the power to lead other regions to follow to be able to operate in the market. Similar to this phenomenon, in the past, some have commented on the “California Effect” at the national level, which began in the 1980s in the United States. It derived from corporates in need to participate in the Californian economy because of its relevance, with the inevitable consequence of California’s regulation impacting the whole country. The effect will most probably be stronger in Brussels, because of the larger size of its economy.

The literature review suggests in essence that the “Brussels Effect” takes place when the EU creates incentives to adjust to its stringent standards, and thus market participants respond through imitation in their global business. Regulations, therefore, spread through market forces, i.e., companies adopt the rules that the EU established as a cost of operating in the European Union and then apply these standards to the rest of their business globally to homogenize their running of the business, minimizing costs of compliance with the regulation. For instance, this has happened with the General Data Protection Regulation, which the EU issued to protect consumers regarding privacy and data governance. Gady argued that the Snowden revelations triggered unilateral regulatory globalization, making the “Brussels Effect” more likely. Fear of being excluded from the EU market made some US companies more willing to comply globally with the strict set of standards (Gady 2014). In this regard, Apple, for instance, followed GDPR to operate in the European Union and decided to adopt it in its global businesses. Google, in turn, failed to comply with the stringent requirements that the GDPR lays out, being fined USD 57 million by the French regulators and resulting in an inflection point for the industry showing the consequences should multinationals not comply with requirements but still transfer data to and from the European market.

Stringency is not necessarily the key driver for EU leadership in these matters, as countries may have different approaches to the same goal. Being a pioneer, however, does. Other Governments, including the US, are embracing this regulation derived from a lack of their own and a means of operating with Europe. Others may be just following the path to high-quality regulation on specific matters that require it. Rwanda, for instance, recently passed the Data Protection and Privacy Law, which emulates many of the aspects of the GDPR in terms of consumer protection, such as the right to object, the right to correct or delete personal data, or the right to data portability (Rizzi and Kumari 2021).

In other areas, from consumer health and safety to antitrust, the European Union has managed to bring its views to the world. Thanks to the EU antitrust and mergers regulation, many companies have claimed their right to fair competition within the borders of the 27 member countries. The EU can claim antitrust authority whenever the activities of a company, regardless of its nationality, have a significant and on-purpose effect within the EU. Compared to the US, the EU has been more receptive to concerns about anticompetitive conduct.

The EU´s carbon border adjustment mechanism is another such example. The mechanism currently under consideration would impose a tax on imported carbon-intensive products, to trigger behavioral change and prevent companies from carbon leaking: where companies transfer production (and emissions) to other countries outside the EU to prevent the high costs of polluting in Europe. The proposal is still under consideration by the 27 member countries, and if implemented it will be in a transition phase from January 2023 to December 2025 and will be fully in force in January 2026. The effect will not just be noted by EU importers and non-EU producers, but also ultimately by the EU industries that use the taxed products and, in turn, global businesses (Figures et al. 2021).

This same effect that the carbon tax is thought to have can be applicable to the new EU Proposal on deforestation and forest degradation. In November 2021, the EU adopted a proposal to guarantee that EU products do not contribute to forest degradation and deforestation. As per the European Commission data, EU citizens supported the object of this proposal with 1.2 million responses to the public consultation launched ahead. The measure could have a positive impact on biodiversity loss and emissions. This is a landmark piece of regulation, following the line of reasoning that the EU has introduced lately to accelerate climate action. Even though it still needs to be passed by the European Parliament and the Council, it has already attracted the attention of other countries. The UK developed and enacted similar legislation—still missing key definitions and due diligence obligations—at the end of 2021 and the US developed the Forest Act´s passage, with circa the same relevant commodities and covered products as that of the EU (Weiss et al. 2022).

In the case of supply chains, in 2021, the EU passed a resolution calling for corporate due diligence for EU companies or companies with operations within the EU. Experts consider that the EU regulation will mirror existing regulations in the 27 member countries in many aspects and, in particular, that in France and Germany a bottom threshold will be set (Thompson 2022). Other examples include Belgium, whose due diligence draft bill scope includes suppliers across all its value chain and, therefore, companies must apply their risk management to them as well (Thompson 2022). The new rules on due diligence will follow the UN guidelines on business and human rights and would require large EU companies to verify that their supply chains respect environmental and human rights. It is probable that more countries would follow.

The mechanisms of contagion of the “Brussels Effect” incorporate the effects of international trade, as the private sector is required to adopt standards to operate in the region, thus supporting the spread of EU-crafted regulations. Multinational corporations would thus be compelled to comply with the European regulation as a price for accessing its market. As has happened in other industries, it is probable that these corporations adopt these standards in their global businesses to avoid the cost of having to comply with several regulations. For too long, environment and trade have followed different paths, and now the opportunity has arisen for a global engagement in trade and environmental cohesion to tackle climate change.

The development of ESG goes hand in hand with more regulations, including outside of the EU. In recent years, Mexico has had a regulatory trend for the incorporation of ESG in business daily activities. This includes an amendment to the General Law of Mercantile Companies and the Securities Market Law, which requires increased participation of women on the boards of directors, in favor of a more just and inclusive society; the strengthening of the Corporate Social Responsibility and Corporate Due Diligence Law; or the initiative for the General Circular Economy Law, which establishes the obligation to redesign and reuse products, to maintain valuable life and minimize waste.

4.2. The Impact on Investments Activities

Aside from trade considerations, EU regulation also impacts asset management companies that target EU-based investors. The European Stability Mechanism explains that to qualify as an EU-approved ESG investment, every listed company in either the firms’ equity or fixed income portfolios would have a percentage of their investment aligned with the EU Taxonomy. The final portfolio alignment would result from the weighted average of each position (Janse and Bradford 2021).

The “Brussels Effect” has gone beyond regulation. It is also due to a combination of factors, such as civil society, including activists and shareholders, European NGOs, and European corporates.

Support for ESG regulation is increasing, not just among individual investors but also among institutional ones. For instance, JPMorgan Asset Management backed an additional 28% environmental resolutions globally in 2020 compared to 2019, and Wellington more than quintupled the percentage for that period. Pension funds followed this lead, with Scottish Widows’ divestment of approximately GBP 0.5 billion pounds from companies that failed to meet ESG standards per their exclusions policy (Gerber et al. 2021). A survey carried out in November 2020 of 40 large European companies from different industries shows that 77.5% of corporate leaders wanted their senior managers to speak up in matters of public concern (Cewe 2020). In addition to this, in 2021, 60 organizations worldwide, representing EUR 8.5 trillion in assets, released an open letter to the European Commission to promote a global baseline set of ESG disclosure standards (World Economic Forum 2021).

Overall, there is consensus on the need to improve environmental protection and make sure there is relevant action being taken toward climate change. There is also a strong interest—at least on the corporate side—for that protection to be implemented in the most efficient way, and this is why more actionable items need to be undertaken. It is not always a matter of stringency or protectiveness; it may just be more work that is needed to homogenize regulation. Multinationals operate in the most efficient way, looking to achieve better environmental performance while reducing transaction costs. Considering the increasing operational costs and risks associated with not adhering to climate action, regardless of whether there is regulation, but in particular, if there is, multinationals will be in favor of reducing the variability, with a focus on efficiency.

Furthermore, rating agencies have introduced new ESG ratings. Failure to comply with such standards may make capital-raising more expensive for corporates, as those companies considered to be non-compliant will end up on an exclusion list (Janse and Bradford 2021). In fact, Moody’s just released its Temperature Alignment Data, a dataset to help investors and companies assess their alignment with net-zero targets. It will present alignment with the global temperature benchmark and their progress in meeting targets (Business Wire 2021).

Until recently, American regulators have been reluctant to legislate on ESG matters. However, in March 2021, the discourse changed. The SEC’s then-Acting Chair, Allison Herren Lee, announced that the SEC would be “working toward a comprehensive ESG disclosure framework” and offering guidance to encourage the reporting and rulemaking of specific metrics such as workforce and Board diversity (Katz and McIntosh 2021). The SEC’s traditional focus has been on requiring companies to report on their financially material information; however, with ESG, it is said to have been aiming at tackling non-financially material information, under the concept of double materiality. Prof. Amanda M. Rose, from Vanderbilt Law and Business, considers that requesting the SEC to adopt a disclosure framework on topics that might appear non-financially material is a shift in the SEC’s rulemaking (Rose 2021). In April 2021, US climate envoy John Kerry said that the United States would likely join Europe in the mandate that financial institutions and companies disclose climate change risks, and even suggested that they would work with European leaders to harmonize disclosure standards (Whieldon 2021). Rose points out that the EU ESG regulation was legitimized by the European Parliament’s legitimacy to create disclosure requirements to target investors’ needs and provide consumers with a sufficient level of transparency on companies’ impact on society (Rose 2021). However, Rose believes that the SEC’s legitimacy would be challenged if they acted on their own, reinforcing the idea of the public debate around legitimate ESG metrics to be disclosed.

In February 2021, the ESG Disclosure Simplification Act of 2021 was introduced by US Congress. If passed, it would require annual reports to disclose ESG metrics and include the issuers’ views on the connection between these and the long-term business strategy, as well as the methodology used to determine the metrics’ impact on such strategy (Vargas 2021). According to the Act, the SEC would be in charge of defining ESG metrics and to “incorporate any internationally recognized, independent, multi-stakeholder environmental, social, and governance disclosure standards” (Vargas 2021) in that definition under its discretion. This “internationally recognized” incorporation of disclosure standards is what gives way to the “Brussels Effect”.

Finally, making a strong statement regarding the American stand on ESG matters, the Securities Exchange Commission proposed rules to enhance and standardize climate-related disclosures on 21 March 2022. The SEC would serve as regulator on ESG disclosures as of today, instead of Congress (Foelber 2022).

The proposal would require registrants to include climate risk-related disclosures in their registration statements and periodic reports, including information about climate-related risks that will likely have a material impact on their business, results of operations, or financial condition, as well as additional climate-related financial statement metrics to their audited financial statements. It would additionally require disclosure of the registrant’s greenhouse gas emissions, those that occur from sources owned or controlled by the company (Scope 1), indirect gas emissions from purchased and consumed electricity and other forms of energy (Scope 2), and greenhouse gas emissions consequence from the company’s activities, from its value chain upstream and downstream activities but that are neither owned nor controlled by them (Scope 3) (U.S. Securities and Exchange Commission 2022a). “I am pleased to support today’s proposal because, if adopted, it would provide investors with consistent, comparable, and decision-useful information for making their investment decisions, and it would provide consistent and clear reporting obligations for issuers,” said SEC Chair Gary Gensler (U.S. Securities and Exchange Commission 2022b). This sets a cornerstone in the US view towards ESG, shifting toward the alignment with accepted disclosure standards, such as the Task Force on Climate-related Financial Disclosures, and sets a clear path going forward.

In the UK, the Chancellor made clear the UK’s intention to implement its own green taxonomy; however, he added that this regulation would likely use the scientific metrics adopted in the EU taxonomy as a base for creating their own (Norman et al. 2021). The reason for this is the aim to reduce both the complexity and inherent risk of competing compliance requirements of both regulations. Specialists in the industry in the UK believe that eventually the UK will adapt its ESG rulebook to the EU directives, making its mandate more direct and transparent to financial advisors while increasing disclosure requirements. Additionally, experts stress the need for a coherent taxonomy in the interest of products’ comparison and investors’ understanding.

Other member countries are aligned with this new set of standards aiming at a carbon-zero economy. The German Federal Financial Supervisory Authority (BaFin)’s Guidance Notice of 2019, modified in 2020, offers orientation for entities supervised by BaFin, including credit institutions, insurance undertakings and pension funds, asset management companies, and financial services institutions on documentation and reporting of environmental, social, and governance risks and their management (BaFin, Federal Financial Supervisory Authority 2020). This Guidance Notice gives way to the expectation of alignment with the European law and, in particular, conveys that audit requirements will be further expected to comply with EU regulation (Herkströter et al. 2020).

The definition of a taxonomy is not exempt from debate, as evidenced by controversy raised by the inclusion of nuclear power and gas in the green taxonomy set by the European Union in December 2021 (Bradford 2022).

Finally, the role of the Task Force on Climate-related Financial Disclosures (TCFD) is critical for the determination of the reasonability of application of the ESG EU Taxonomy on other countries. Almost 60% of the top 100 public companies globally, along with 59% of all publicly listed companies in Europe and North America and 46% in the Asia Pacific, support or are in line with the TCFD’s recommendations (Task Force on Climate-Related Disclosures 2020). “TCFD represents best practice in climate disclosure, providing financial market participants with important and decision-useful information,” […] validated by more than 2000 companies worldwide representing USD 23 trillion in market cap, according to Kate Vyvyan, from Clifford Chance (Global Capital 2021). This is further proof of civil society’s engagement towards the tackling of climate change.

Europe’s Taxonomy has been aligned to the TCFD recommendations. New Zealand, Japan, Switzerland, the UK, South Africa, Brazil, and Mexico (S&P Global 2022), among other countries, have committed to making financial disclosures regarding climate change mandatory. In June 2021, US Treasury Secretary Janet Yellen signed on to the G7 Finance Ministers and Central Bank Governors Communiqué, which calls for compulsory climate disclosures per the TCFD recommendations (US Department of the Treasury 2021). Canada also supported this Communiqué, and in October 2021, the Canadian Securities Administrators published proposed climate-related disclosure requirements, which contemplate disclosure broadly consistent with the TCFD recommendations (Norton Rose Fulbright 2021).

Overall, it is most probable that countries will follow EU standards to a certain extent, whether on a trial-and-error basis, considering what has worked and what has not, or directly bringing some of its requirements into their own legislation. This, as discussed, will depend on their view on the structure of the EU regulation and whether they consider it an efficient regime. One way to describe the “Brussels Effect” on ESG matters is that the EU approach introduces new ideas into the regulatory concept and it suggests possibilities; once these are suggested they would often manifest themselves into legislation abroad that reflects these ideas.

4.3. Regulatory Arbitrage and Criticism of ESG Regulations

Diverging or conflicting regulations between markets might notably lead to tensions between countries, as evidenced by the EU new carbon tariff. Differences in regulations could also be construed as non-tariff trade barriers. The stricter environment in the EU may create regulatory arbitrage for select companies, which may not be fully integrated into the global economy or have less exposure to the EU single market. We have been able to witness this regulatory arbitrage take place with other regulations in the supply chain or labor, so if regulatory arbitrage is a concern when it comes to these spaces, it could certainly be when it comes to ESG matters.

”One growing concern is the potential for regulatory arbitrage—‘taxonomy shopping’—as some have termed it,” according to Kate Vyvyan, from Clifford Chance (Global Capital 2021). The inclusion of natural gas and nuclear power in the EU Taxonomy underscores the potential divergence between jurisdictions. She adds that this “could incentivize issuers to adopt whichever taxonomy is least burdensome for them”.

Select US scholars and industry leaders have raised concerns on ESG regulation and applicability. David Katz and Laura McIntosh, from Wachtell, Lipton, Rosen & Katz, explain that it is critical that the SEC ultimately protects registrants regarding ESG estimates or assumptions made in good faith as they are made in the interest of maximizing the decision-useful information provided to investors. They consider that safe harbors will potentially encourage issuers to be more transparent in their disclosures and boost dialogue between them and investors conveying better reporting. Moreover, responding to the concern of US scholars regarding the introduction of non-financially material information in disclosure, they go beyond proposing no liability for issuers that go past SEC enforcement nor federal prosecution for intentional fraud as, in their opinion, ESG disclosures should not be considered “material” even if required. Thus, there should be no private right to act on them (Katz and McIntosh 2021).

5. Conclusions

ESG regulation comes from a much-needed change in corporations’ operations and investment practices worldwide, as climate impacts are on the rise. A regulatory emphasis on ESG has boosted the existing momentum for corporates and investors alike, meeting the rising aspirations of several types of stakeholders. The EU has led ambitious ESG regulations, which impact in particular disclosure, accountability, carbon markets, due diligence and international trade, and investment activities. Those regulations will likely have a long-lasting impact on businesses globally. Companies that promote social value creation will be better equipped for a business environment where ESG-aligned regulations become more common.

It has been argued that the field of environmental law has been following a race to the bottom due to regulatory competition, but there is not much empirical evidence in this regard. There is in fact evidence showing the opposite, a race to the top, for instance, in terms of the “California Effect”. California became a pioneer in this field by adopting stringent car emissions standards, and the other states of the United States followed its path (Holzinger and Knill 2004). While the EU has taken the lead in ESG regulations, other countries are incorporating this focus into policymaking, supporting the idea of an “ESG Brussels Effect”.

This paper aims to further the perspective of the role of the EU as a regulatory power in the field of ESG. While the EU as a global regulator has been true de facto for a wide variety of matters on which the EU has been a pioneer legislating, or its lawmaking has been proved to be accurate and efficient, it is recognizable that this happens certainly in an informal manner. Regulatory competition and regulatory cooperation must be borne hand in hand in order to prevent the challenges derived from non-harmonized legislation in the globalized world. In those areas where the EU has not been able to capitalize directly on market access to forward its regulatory power, regulatory cooperation exponentiates to the extent that the relationship between decision-makers does not just derive from the socio-economic reality, but also because of the trans-governmental networking (Lavenex 2014).

EU regulation on ESG maters is impacting business globally due primarily to the stringent scope of its regulation and its membership in key global institutions. The latter has proven to be one of the most strategic ways in which the European Union has driven its influence to third countries (Golberg 2019). This is possible, although not inevitable, when the EU acts in terms of regulatory cooperation, without the possibility of exclusion; however, it is inevitable once the exclusion comes into place (Young 2015).

Regulatory cooperation still has ample space for improvement. Formal agreements between institutions’ country members can be effective toward reaching the ultimate goal of tackling climate change. Thus, areas of focus include further analysis of the urgent need for collaboration of key players towards standardized regulations and how this can be managed in order to prevent greenwashing, protectionism, and regulatory arbitrage, and foster sustainable growth and prosperity. Regulatory oversight and high-quality third-party auditing will boost corporates’ aim to reach the Paris Accord net-zero objectives.

Author Contributions

Conceptualization, R.R.A. and F.d.M.; methodology, R.R.A.; validation, R.R.A. and F.d.M.; formal analysis and investigation, R.R.A.; data curation, R.R.A. and F.d.M.; writing—original draft preparation, R.R.A.; writing—review and editing, R.R.A. and F.d.M.; supervision, F.d.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank D. Evan van Hook and Flammer, Columbia University, for their comments on an earlier version of this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- BaFin, Federal Financial Supervisory Authority. 2020. Sustainability Risks: BaFin Publishes Guidance Notice. Available online: https://www.bafin.de/SharedDocs/Veroeffentlichungen/EN/Meldung/2019/meldung_191220_MB_Nachhaltigkeitsrisiken_en.html (accessed on 23 April 2022).

- Beattie, Alan. 2020. The Brussels Effect, by Anu Bradford. Available online: https://www.ft.com/content/82219772-3eaa-11ea-b232-000f4477fbca (accessed on 23 April 2022).

- Bergman, Mark S., Ariel J. Deckelbaum, and Brad S. Karp. 2020. Introduction to ESG. Available online: https://corpgov.law.harvard.edu/2020/08/01/introduction-to-esg/ (accessed on 23 April 2022).

- Bioy, Hortense, Elizabeth Stuart, Dimitar Boyadzhiev, Andy Pettit, and Amrutha Alladi. 2020. European Sustainable Funds Landscape: 2020 in Review. A Year of Broken Records Heralding a New Era for Sustainable Investing in Europe. p. 1. Available online: https://vdocuments.net/european-sustainable-funds-landscape-2020-in-review-a-climate-change-themed.html (accessed on 23 April 2022).

- Boubaker, Sabri, and Duc Khuong Nguyen, eds. 2019. Corporate Social Responsibility, Ethics and Sustainable Prosperity. Singapore: World Scientific, chp. 2. [Google Scholar]

- Boubaker, Sabri, Lamia Chourou, Darlene Himick, and Samir Saadi. 2017. It’s about time! The influence of institutional investment horizon on corporate social responsibility. Thunderbird International Business Review 59: 571–94. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Zhenya Liu, and Yaosong Zhan. 2022. Customer relationships, corporate social responsibility, and stock price reaction: Lessons from China during health crisis times. Finance Research Letters 47: 102699. [Google Scholar] [CrossRef]

- Bradford, Hazel. 2022. Pensions and Investments 2022. EU Green Taxonomy Changes Are Meeting Resistance. Available online: https://www.pionline.com/esg/eu-green-taxonomy-changes-are-meeting-resistance (accessed on 23 April 2022).

- Broadstock, David C., Kalok Chan, Louis T. W. Cheng, and Xiaowei Wang. 2020. The Role of ESG Performance during Times of Financial Crisis: Evidence from COVID-19 in China. National Library of Medicine. Elsevier Public Health Emergency Collection. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3627439 (accessed on 23 April 2022).

- Business Wire. 2021. Moody’s ESG Solutions Launches Dataset to Help Investors and Companies Assess Alignment with Net Zero Targets. Available online: https://www.businesswire.com/news/home/20211208005683/en/Moody%E2%80%99s-ESG-Solutions-Launches-Dataset-to-Help-Investors-and-Companies-Assess-Alignment-With-Net-Zero-Targets (accessed on 23 April 2022).

- Carvalhal, Andre, and Sidney Nakahodo. 2022. Do Environmental, Social and Governance (ESG) Practices Affect Abnormal Returns During the COVID-19 Pandemic? Evidence from Brazil. Working Paper. Unpublished. [Google Scholar]

- Cewe, Christoph. 2020. The Political CEO: Rationales behind CEO Sociopolitical Activism. Available online: https://www.united-europe.eu/wp-content/uploads/2020/10/ChristophCewe_ThePoliticalCEO.pdf (accessed on 23 April 2022).

- Cornett, Marcia Millon, Otgontsetseg Erhemjamts, and Hassan Tehranian. 2016. Greed or good deeds: An examination of the relation between corporate social responsibility and the financial performance of U.S. commercial banks around the financial crisis. Journal of Banking & Finance 70: 137–59. [Google Scholar]

- Diab, Adeline, and Gina M. Adams. 2021. ESG Assets May Hit $53 Trillion by 2025, a Third of Global AUM. Bloomberg Intelligence. Available online: https://www.bloomberg.com/professional/blog/esg-assets-may-hit-53-trillion-by-2025-a-third-of-global-aum/ (accessed on 23 April 2022).

- Earth Science Communications Team. 2022. Global Climate Change Vital Signs of the Planet. Climate Change: How Do We Know? Earth Science Communications Team. Available online: https://www.nasa.gov/ (accessed on 23 April 2022).

- El Ghoul, Sadok, Omrane Guedhami, Chuck C. Y. Kwok, and Dev R. Mishra. 2011. Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance 35: 2388–406. [Google Scholar]

- European Commission. 2014. Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups. Brussels: European Commission. [Google Scholar]

- European Commission. 2019a. Regulation (EU) 2019/2088 of the European Parliament and of the COUNCIL of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector, Article 1, Article 2. Brussels: European Commission. [Google Scholar]

- European Commission. 2019b. Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector, Article 4. Brussels: European Commission. [Google Scholar]

- European Commission. 2019c. Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector, Article 6, Article 8, Article 9. Brussels: European Commission. [Google Scholar]

- European Commission. 2020. Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation (EU) 2019/2088. Brussels: European Commission. [Google Scholar]

- European Commission. 2021. Directive of the European Parliament and of the Council Amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as Regards Corporate Sustainability Reporting. Brussels: European Commission. [Google Scholar]

- European Commission. 2022. EU Taxonomy. For Sustainable Activities, What the EU Is Doing to Create an EU-Wide Classification System for Sustainable Activities. Brussels: European Commission. [Google Scholar]

- European Commission. n.d. EU Position in World Trade. Brussels: European Commission.

- Figures, Tim, Marc Gilbert, Michael McAdoo, and Nicole Voigt. 2021. The EU’s Carbon Border Tax Will Redefine Global Value Chains. Available online: https://www.bcg.com/publications/2021/eu-carbon-border-tax (accessed on 23 April 2022).

- Flammer, Caroline. 2015. Does Corporate Social Responsibility Lead to Superior Financial Performance? A Regression Discontinuity Approach. Management Science 61: 2549–68. [Google Scholar] [CrossRef] [Green Version]

- Flammer, Caroline, Michael W. Toffel, and Kala Viswanathan. 2019. Shareholder activism and firms’ voluntary disclosure of climate change risks. Wiley. Strategic Management Journal 42: 1850–79. [Google Scholar] [CrossRef]

- Foelber, Daniel. 2022. ESG Review, SEC Proposal Could Be Game Changing For ESG Growth. Available online: https://esgreview.net/2022/03/30/sec-proposal-could-be-game-changing-for-esg-growth/ (accessed on 23 April 2022).

- FSB-TCFD. 2022. Financial Stability Board, Task Force on Climate-Related Financial Disclosures. Available online: www.fsb-tcfd.org (accessed on 23 April 2022).

- Gady, Franz-Stefan. 2014. EU/U.S. Approaches to Data Privacy and the “Brussels Effect”: A Comparative Analysis. Georgetown Journal of International Affairs 4: 12–23. [Google Scholar]

- Gerber, Marc S., Scott C. Hopkins, Greg Norman, Simon Toms, Helena J. Derbyshire, Louise Batty, Adam M. Howard, Caroline S. Kim, Damian R. Babic, Zoe Q. Cooper Sutton, and et al. 2021. Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates, ESG: Key Trends in 2020 and Expectations for 2021. Available online: https://www.skadden.com/insights/publications/2021/02/esg-key-trends-in-2020-and-expectations-2021 (accessed on 23 April 2022).

- Giese, Guido, Linda-Eling Lee, Dimitris Melas, Zoltán Nagy, and Laura Nishikawa. 2019. Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk, and Performance. The Journal of Portfolio Management 45: 69–83. [Google Scholar] [CrossRef]

- Global Capital. 2021. Sustainable Finance 2021: Engaging Capital to Drive the Transition. Global Capital. July. Available online: https://www.globalcapital.com/pdf/b1smjmk4jsw6rl/sustainable-finance-2021 (accessed on 23 April 2022).

- Godemer, Maia. 2021. The relationships between SFDR, NFRD and EU Taxonomy. Bloomberg Professional Services. Available online: https://www.bloomberg.com/professional/blog/the-relationships-between-sfdr-nfrd-and-eu-taxonomy/ (accessed on 23 April 2022).

- Godfrey, Paul C., Craig B. Merrill, and Jared M. Hansen. 2009. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal 30: 425–45. [Google Scholar] [CrossRef]

- Golberg, Elizabeth. 2019. Regulatory Cooperation—A Reality Check. M-RCBG Associate Working Paper Series; No. 115. Cambridge: Harvard Kennedy School. [Google Scholar]

- Gregory, Alan, Rajesh Tharyan, and Julie Whittaker. 2014. Corporate Social Responsibility and Firm Value: Disaggregating the Effects on Cash Flow, Risk and Growth. Journal of Business Ethics 124: 633–57. [Google Scholar] [CrossRef] [Green Version]

- Hartzmark, Samuel M., and Abigail B. Sussman. 2019. Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows. The Journal of Finance 74: 2789–837. [Google Scholar] [CrossRef]

- Herkströter, Caroline, Michael Born, and Nadine Gerstenkorn. 2020. Norton Rose Fulbright, ESG: German Regulator Publishes Guidance Notice on Sustainability. Available online: https://www.regulationtomorrow.com/de/esg-german-regulator-publishes-guidance-notice-on-sustainability/ (accessed on 23 April 2022).

- Holzinger, Katharina, and Christoph Knill. 2004. Competition and Cooperation in Environmental Policy: Individual and Interaction Effects. Journal of Public Policy 24: 25–47. [Google Scholar] [CrossRef] [Green Version]

- International Financial Reporting Standards. 2021. Consolidation with CDSB and VRF, and Publication of Prototype Disclosure Requirements. IFRS Foundation Announces International Sustainability Standards Board. Available online: https://www.ifrs.org/news-and-events/news/2021/11/ifrs-foundation-announces-issb-consolidation-with-cdsb-vrf-publication-of-prototypes/ (accessed on 23 April 2022).

- Jackson, Peter. n.d. From Stockholm to Kyoto: A Brief History of Climate Change; New York: UN Chronicle. Available online: https://www.un.org/en/chronicle/article/stockholm-kyoto-brief-history-climate-change (accessed on 23 April 2022).

- Janse, Kalin Anev, and Anu Bradford. 2021. European Sustainability Mechanism, Europe Greening the World: The “Brussels Effect” on Sustainable Finance. Available online: https://www.esm.europa.eu/blog/europe-greening-world-brussels-effect-sustainable-finance (accessed on 23 April 2022).

- Joint Committee of the European Supervisory Authority. 2021. Final Report on draft Regulatory Technical Standards. Paris: Joint Committee of the European Supervisory Authority. [Google Scholar]

- Katz, David A., and Laura A. McIntosh. 2021. SEC Regulation of ESG Disclosures. Harvard Law School Forum on Corporate Governance. Available online: https://corpgov.law.harvard.edu/2021/05/28/sec-regulation-of-esg-disclosures/ (accessed on 23 April 2022).

- Lagarde, Christine. 2021. Towards a Green Capital Markets Union for Europe. Frankfurt am Main: European Central Bank. [Google Scholar]

- Lavenex, Sandra. 2014. The power of functionalist extension: How EU rules travel. Journal of European Public Policy 21: 885–903. [Google Scholar] [CrossRef] [Green Version]

- Lins, Karl V., Henri Servaes, and Ane Tamayo. 2017. Social capital, trust, and firm performance: The Value of Corporate Social Responsibility during the Financial Crisis. The Journal of Finance 72: 1785–824. [Google Scholar] [CrossRef] [Green Version]

- LSE Grantham Research Institute on Climate Change. 2021. ‘Double Materiality’: What Is It and Why Does It Matter? Green Central Banking. Available online: https://www.lse.ac.uk/granthaminstitute/news/double-materiality-what-is-it-and-why-does-it-matter/ (accessed on 23 April 2022).

- Mankikar, Divya. 2021. S&P Global, More than $3T of Companies Outside the EU Could Be on the Hook for SFDR. Available online: https://www.spglobal.com/esg/insights/more-than-3t-of-companies-outside-the-eu-could-be-on-the-hook-for-europe-s-sustainable-finance-disclosure-regulation (accessed on 23 April 2022).

- Miralles-Quirós, María Mar, José Luis Miralles-Quirós, and Jesús Redondo Hernández Hernandez. 2019. ESG performance and value creation in the banking industry: International differences. Sustainability 11: 1404. [Google Scholar] [CrossRef] [Green Version]

- National Aeronautics and Space Administration. 2021. Emission Reductions from Pandemic Had Unexpected Effects on Atmosphere. Global Climate Change, Vital Signs of the Planet News, November 9. [Google Scholar]

- Network for Greening the Financial System. 2020. US Federal Reserve joins NGFS and Two New Publications Released. Available online: https://www.ngfs.net/en/communique-de-presse/us-federal-reserve-joins-ngfs-and-two-new-publications-released (accessed on 23 April 2022).

- Norman, Greg, Adam M. Howard, William K. Hardaway, and Abigail B. Reeves. 2021. ESG Rules: Will the UK Align with the EU? Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates. Available online: https://www.skadden.com/insights/publications/2021/02/insights-special-edition-brexit/esg-rules-will-the-uk-align-with-the-eu (accessed on 23 April 2022).

- Norton Rose Fulbright. 2021. Climate-Related Reporting Standards including the TCFD Framework and Their Impact on the Aviation Industry. Available online: https://www.nortonrosefulbright.com/en/knowledge/publications/741e5326/Climate-related%20reporting%20standards%20including%20the%20TCFD%20framework%20and%20their%20impact%20on%20the%20aviation%20industry (accessed on 23 April 2022).

- Our World in Data. 2019 Global Reported Natural Disasters by Type, 1970 to 2019. Available online: https://ourworldindata.org/grapher/natural-disasters-by-type (accessed on 23 April 2022).

- Papadopoulos, Kosmas, Rodolfo Araujo, and Simon Toms. 2020. ESG Drivers and the COVID-19 Catalyst. Harvard Law School Forum on Corporate Governance. Available online: https://corpgov.law.harvard.edu/2020/12/27/esg-drivers-and-the-covid-19-catalyst/ (accessed on 23 April 2022).

- Quiggin, Daniel, Kris De Meyer, Lucy Hubble-Rose, and Antony Froggatt. 2021. Climate Change Risk Assessment. London: Chatham House. [Google Scholar]

- Rizzi, Alexandra (Alex), and Tanwi Kumari. 2021. Trust of Data Usage, Sources, and Decisioning: Perspectives from Rwandan Mobile Money Users. Washington, DC: Accion, Center for Financial Inclusion. [Google Scholar]

- Rose, Amanda M. 2021. A Response to Calls for SEC-mandated ESG Disclosure. Washington University Law Review 98: 1821. [Google Scholar]

- S&P Global. 2022. Tracking ESG Regulation. Available online: https://www.spglobal.com/esg/insights/global-esg-regulation (accessed on 23 April 2022).

- Shapiro, Lori, and Matthew S. Mitchell. 2022. Global Sustainable Bond Issuance To Surpass $1.5 Trillion in 2022. Available online: https://www.spglobal.com/ratings/en/research/articles/220207-global-sustainable-bond-issuance-to-surpass-1-5-trillion-in-2022-12262243 (accessed on 23 April 2022).

- Sprout Social. 2019. #BrandsGetReal: Brands Creating Change in the Conscious Consumer Era. Chicago: Sprout Social. [Google Scholar]

- Stankiewicz, Alyssa. 2021. Sustainable Fund Flows Reach New Heights in 2021’s First Quarter. Available online: https://www.morningstar.com/articles/1035554/sustainable-fund-flows-reach-new-heights-in-2021s-first-quarter (accessed on 23 April 2022).

- Task Force on Climate-Related Disclosures. 2020. 2020 Status Report. Available online: https://www.fsb.org/2020/10/2020-status-report-task-force-on-climate-related-financial-disclosures/ (accessed on 23 April 2022).

- Technical Expert Group on Sustainable Finance (TEG). 2020. Financial Stability, Financial Services and Capital Markets Union. Available online: https://ec.europa.eu/info/departments/financial-stability-financial-services-and-capital-markets-union_en (accessed on 23 April 2022).

- Thompson, Linda A. 2022. In the Age of ESG, European Countries Offer Clues to the EU’s Upcoming Regulations on Environmental and Human Rights Due Diligence. Available online: https://www.law.com/international-edition/2022/01/21/in-the-age-of-esg-european-countries-offer-clues-to-the-eus-upcoming-regulations-on-environmental-and-human-rights-due-diligence/ (accessed on 23 April 2022).

- U.S. Securities and Exchange Commission. 2022a. 17 CFR 210, 229, 232, 239, and 249, [Release Nos. 33-11042; 34-94478; File No. S7-10-22] RIN 3235-AM87. The Enhancement and Standardization of Climate-Related Disclosures for Investors. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwi-0JS7lLz4AhXMxosBHa9QDUYQFnoECAkQAQ&url=https%3A%2F%2Fwww.sec.gov%2Frules%2Fproposed%2F2022%2F33-11042.pdf&usg=AOvVaw1_VArwiQllo7bND9YR6Dcj (accessed on 23 April 2022).

- U.S. Securities and Exchange Commission. 2022b. Press Release, SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors. Available online: https://www.sec.gov/news/press-release/2022-46 (accessed on 23 April 2022).

- UNFCC—United Nations Climate Change. n.d. The Paris Agreement. Geneva: UNFCC.

- US Department of the Treasury. 2021. Press Release, G7 Finance Ministers & Central Bank Governors Communiqué. Available online: https://home.treasury.gov/news/press-releases/jy0215 (accessed on 23 April 2022).

- Vargas, Juan. 2021. H. R. 1187 117th Congress, 1st Session (2021–2022). Corporate Governance Improvement and Investor Protection Act. Available online: https://www.congress.gov/bill/117th-congress/house-bill/1187 (accessed on 23 April 2022).

- Weiss, Jeffrey, Katy Shin, Eva Monard, Simon Tilling, and Byron Maniatis. 2022. Comparing recent deforestation measures of the United States, European Union, and United Kingdom. Global Trade Policy Blog, January 21. [Google Scholar]

- Whieldon, Esther. 2021. S&P Global How Biden’s 1st 100 Days Changed the Course of US ESG and Sustainability Policy. Available online: https://www.spglobal.com/esg/insights/how-biden-s-1st-100-days-changed-the-course-of-us-esg-and-sustainability-policy (accessed on 23 April 2022).

- World Economic Forum. 2021. 60 Organizations Release Open Letter for EU to Act on ESG. Available online: https://www.weforum.org/agenda/2021/10/57-organizations-release-open-letter-for-eu-to-act-on-esg/ (accessed on 23 April 2022).

- Young, A. 2015. The European Union as a Global Regulator? Context and Comparison. Journal of European Public Policy 22: 1233–52. [Google Scholar] [CrossRef] [Green Version]