Does Fintech-Driven Inclusive Finance Induce Bank Profitability? Empirical Evidence from Developing Countries

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

3. Data and Methodology

3.1. Data

3.2. Bank Profitability (Dependent Variables)

3.3. Construction of Fintech-Driven Inclusive Finance Indices (Independent Variables)

3.4. Control Variables

3.5. Model Specification

3.6. Data Analysis Techniques

3.6.1. Fixed Effect Regression

3.6.2. Two-Stage Least Squares (2SLS-IV) Regression

3.6.3. Two-Step System GMM Estimation

3.6.4. Generalized Least Squares (GLS) Estimation: Random Effects

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Granger Causality Tests

4.3. Regression Results: Fixed Effect

4.4. Robustness Tests: 2SLS-IV Regression

4.5. Robustness Tests: A Dynamic Panel Model

4.6. Robustness Tests: Random-Effects Generalized Least Squares (GLS)

4.7. Robustness Tests: Split Samples Based on FI Intensity (High FI vs. Low FI)

4.8. Sample Segmentation Based on Economic Development (High GDP vs. Low GDP)

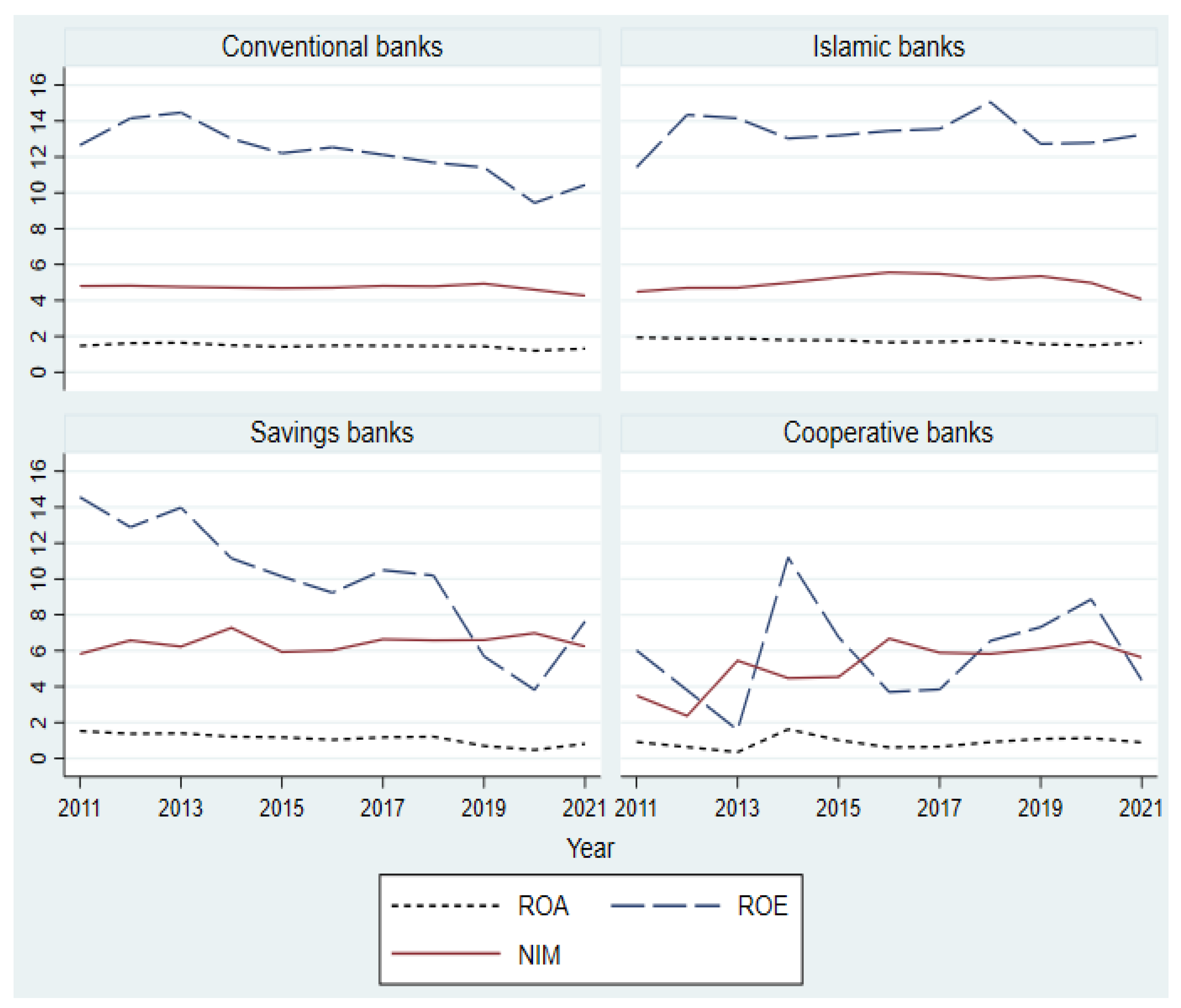

4.9. Further Insights: FI and Profitability Nexus Considering the Size and Type of Banks

4.10. Effect of Interaction between FI and COVID-19 (2020–2021) on Bank Profitability

5. Conclusions, Policy Implications, and Limitations

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Country | FI | FIA | FIP | FIU |

|---|---|---|---|---|

| (1) Afghanistan | 0.0491 | 0.0031 | 0.1278 | 0.0011 |

| (2) Albania | 0.1871 | 0.0658 | 0.4118 | 0.0161 |

| (3) Armenia | 0.2579 | 0.1312 | 0.4603 | 0.0790 |

| (4) Bangladesh | 0.4016 | 0.5918 | 0.2801 | 0.1088 |

| (5) Benin | 0.3242 | 0.2012 | 0.3644 | 0.2614 |

| (6) Botswana | 0.4137 | 0.0541 | 0.6876 | 0.3463 |

| (7) Burkina Faso | 0.2900 | 0.1205 | 0.3156 | 0.3090 |

| (8) Cambodia | 0.2209 | 0.0838 | 0.3669 | 0.1247 |

| (9) Cameroon | 0.2330 | 0.1043 | 0.3123 | 0.1845 |

| (10) Chad | 0.0419 | 0.0120 | 0.0969 | 0.0022 |

| (11) Eswatini | 0.3227 | 0.1731 | 0.4540 | 0.2039 |

| (12) Fiji | 0.2877 | 0.0717 | 0.6474 | 0.0438 |

| (13) Ghana | 0.4688 | 0.3187 | 0.5534 | 0.3225 |

| (14) Guinea | 0.1955 | 0.1065 | 0.2664 | 0.1298 |

| (15) Guyana | 0.1391 | 0.0226 | 0.3189 | 0.0287 |

| (16) Jordan | 0.1642 | 0.0406 | 0.3863 | 0.0094 |

| (17) Lesotho | 0.2919 | 0.1398 | 0.4227 | 0.1914 |

| (18) Madagascar | 0.0809 | 0.0360 | 0.1304 | 0.0436 |

| (19) Malawi | 0.1643 | 0.1129 | 0.1919 | 0.1136 |

| (20) Maldives | 0.4162 | 0.3797 | 0.5764 | 0.0997 |

| (21) Mali | 0.2420 | 0.1005 | 0.3360 | 0.1893 |

| (22) Mauritius | 0.3569 | 0.2885 | 0.5550 | 0.0691 |

| (23) Myanmar | 0.0892 | 0.0258 | 0.2039 | 0.0067 |

| (24) Namibia | 0.3661 | 0.0656 | 0.6036 | 0.2914 |

| (25) Nepal | 0.1730 | 0.1477 | 0.2722 | 0.0219 |

| (26) Niger | 0.0668 | 0.0288 | 0.1252 | 0.0206 |

| (27) Pakistan | 0.1476 | 0.1122 | 0.2031 | 0.0613 |

| (28) Panama | 0.2390 | 0.0795 | 0.4590 | 0.0886 |

| (29) Philippines | 0.2212 | 0.0953 | 0.4054 | 0.0765 |

| (30) Qatar | 0.3191 | 0.1351 | 0.6790 | 0.0243 |

| (31) Rwanda | 0.4855 | 0.5331 | 0.3901 | 0.2834 |

| (32) Senegal | 0.3443 | 0.2108 | 0.3921 | 0.2759 |

| (33) Seychelles | 0.3269 | 0.1843 | 0.6522 | 0.0153 |

| (34) South Africa | 0.2451 | 0.0746 | 0.5552 | 0.0189 |

| (35) Sudan | 0.1004 | 0.0129 | 0.2242 | 0.0302 |

| (36) Thailand | 0.4815 | 0.3407 | 0.6352 | 0.2535 |

| (37) Togo | 0.1875 | 0.0847 | 0.2719 | 0.1283 |

| (38) Uganda | 0.4906 | 0.3024 | 0.3779 | 0.5614 |

| (39) Zambia | 0.2577 | 0.1159 | 0.3651 | 0.1849 |

| (40) Zimbabwe | 0.4351 | 0.1273 | 0.4760 | 0.5198 |

| Null Hypothesis | p-Value | |

|---|---|---|

| H0 | FI does not Granger cause ROA | 0.000 *** |

| H0 | ROA does not Granger cause FI | 0.258 |

| H0 | FI does not Granger cause ROE | 0.002 *** |

| H0 | ROE does not Granger cause FI | 0.541 |

| H0 | FI does not Granger cause NIM | 0.000 *** |

| H0 | NIM does not Granger cause FI | 0.397 |

| Variables | VIF | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) FI | - | 1.000 | ||||||||||||

| (2) FIA | 1.50 | 0.804 * | 1.000 | |||||||||||

| (3) FIP | 3.04 | 0.729 * | 0.334 * | 1.000 | ||||||||||

| (4) FIU | 2.41 | 0.813 * | 0.462 * | 0.575 * | 1.000 | |||||||||

| (5) CIR | 1.30 | −0.016 | −0.082 * | −0.023 | 0.090 * | 1.000 | ||||||||

| (6) CAR | 1.32 | 0.167 * | 0.058 * | 0.144 * | 0.203 * | 0.077 * | 1.000 | |||||||

| (7) NPL | 1.18 | 0.026 | 0.054 * | −0.069 * | 0.059 * | 0.240 * | 0.024 | 1.000 | ||||||

| (8) SIZE | 1.56 | 0.161 * | 0.152 * | 0.231 * | 0.036 * | −0.320 * | −0.390 * | −0.143 * | 1.000 | |||||

| (9) LDR | 1.54 | 0.027 * | 0.033 * | 0.078 * | −0.063 * | −0.102 * | −0.068 * | −0.298 * | 0.007 | 1.000 | ||||

| (10) LR | 1.46 | −0.057 * | −0.157 * | −0.046 * | 0.064 * | 0.090 * | 0.228 * | 0.118 * | −0.155 * | −0.452 * | 1.000 | |||

| (11) GDP | 1.18 | −0.016 | 0.109 * | −0.220 * | −0.071 * | −0.002 | −0.052 * | −0.020 | −0.063 * | 0.090 * | −0.047 * | 1.00 | ||

| (12) INF | 1.26 | −0.118 * | 0.004 | −0.283 * | −0.019 | −0.076 * | 0.059 * | 0.109 * | −0.150 * | −0.260 * | −0.011 | −0.10 * | 1.00 | |

| (13) IQ | 2.33 | 0.225 * | 0.013 | 0.609 * | 0.050 * | −0.015 | −0.012 | −0.078 * | 0.166 * | 0.083 * | −0.045 * | −0.02 | −0.40 * | 1.00 |

| Mean VIF | 1.67 |

| 1 | Financial Access Survey (FAS) of International Monetary Fund (IMF), available online: https://data.imf.org/regular.aspx?key=61063968 (accessed on 15 January 2023). |

| 2 | The detailed results of fintech indices (FI, FIA, FIP, and FIU) constructed by PCA are available from the corresponding author on reasonable request. We also calculated fintech indices based on alternative methods of measurement (weighted average method) and found almost the same results (92.42% correlation). |

| 3 | We constructed the institutional quality (IQ) index as one of the control variables using PCA, including six components of world governance indicators: (i) Rule of Law, (ii) Regulatory Quality, (iii) Control of Corruption, (iv) Accountability, (v) Political Stability, and (vi) Government Effectiveness. |

References

- Ahamed, M. Mostak, and Sushanta K. Mallick. 2019. Is financial inclusion good for bank stability? International evidence. Journal of Economic Behavior & Organization 157: 403–27. [Google Scholar]

- Akhisar, Ilyas, K. Batu Tunay, and Necla Tunay. 2015. The effects of innovations on bank performance: The case of electronic banking services. Procedia-Social and Behavioral Sciences 195: 369–75. [Google Scholar] [CrossRef]

- Al-Eitan, Ghaith N., Bassam Al-Own, and Tareq Bani-Khalid. 2022. Financial inclusion indicators affect profitability of Jordanian commercial Banks: Panel data analysis. Economies 10: 38. [Google Scholar] [CrossRef]

- Alkhwaldi, Abeer F., Esraa Esam Alharasis, Maha Shehadeh, Ibrahim A. Abu-AlSondos, Mohammad Salem Oudat, and Anas Ahmad Bani Atta. 2022. Towards an understanding of FinTech users’ adoption: Intention and e-loyalty post-COVID-19 from a developing country perspective. Sustainability 14: 12616. [Google Scholar] [CrossRef]

- Alshatti, Ali Sulieman. 2015. The effect of the liquidity management on profitability in the Jordanian commercial banks. International Journal of Business and Management 10: 62. [Google Scholar]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of error-components models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Athanasoglou, Panayiotis P., Sophocles N. Brissimis, and Matthaios D. Delis. 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money 18: 121–36. [Google Scholar] [CrossRef]

- Baker, Hafez, Thair A. Kaddumi, Mahmoud Daoud Nassar, and Riham Suleiman Muqattash. 2023. Impact of Financial Technology on Improvement of Banks’ Financial Performance. Journal of Risk and Financial Management 16: 230. [Google Scholar] [CrossRef]

- Bali, Turan G., Stephen J. Brown, and Mustafa O. Caglayan. 2014. Macroeconomic risk and hedge fund returns. Journal of Financial Economics 114: 1–19. [Google Scholar] [CrossRef]

- Banna, Hasanul, and Md Rabiul Alam. 2021. Does digital financial inclusion matter for bank risk-taking? Evidence from the dual-banking system. Journal of Islamic Monetary Economics and Finance 7: 401–30. [Google Scholar] [CrossRef]

- Banna, Hasanul, Md Aslam Mia, Mohammad Nourani, and Larisa Yarovaya. 2021a. Fintech-based Financial Inclusion and Risk-taking of Microfinance Institutions (MFIs): Evidence from Sub-Saharan Africa. Finance Research Letters 45: 102149. [Google Scholar] [CrossRef]

- Banna, Hasanul, M. Kabir Hassan, and Mamunur Rashid. 2021b. Fintech-based financial inclusion and bank risk-taking: Evidence from OIC countries. Journal of International Financial Markets, Institutions and Money 75: 101447. [Google Scholar] [CrossRef]

- Bashiru, Shani, Alhassan Bunyaminu, Ibrahim Nandom Yakubu, Mamdouh Abdulaziz Saleh Al-Faryan, John Mac Carthy, and Kofi Afriyie Nyamekye. 2023. Quantifying the Link between Financial Development and Bank Profitability. Theoretical Economics Letters 13: 284–96. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Cameron, A. Colin, and Pravin K. Trivedi. 2013. Regression Analysis of Count Data. Cambridge: Cambridge University Press, vol. 53. [Google Scholar]

- Cámara, Noelia, and David Tuesta. 2014. Measuring Financial Inclusion: A Multidimensional Index. Bilbao: BBVA Research. [Google Scholar]

- Cho, Soohyung, Zoonky Lee, Sewoong Hwang, and Jonghyuk Kim. 2023. Determinants of Bank Closures: What Ensures Sustainable Profitability in Mobile Banking? Electronics 12: 1196. [Google Scholar] [CrossRef]

- Čihák, Martin, and Heiko Hesse. 2010. Islamic banks and financial stability: An empirical analysis. Journal of Financial Services Research 38: 95–113. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. 2020. The global Findex database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review 34: S2–S8. [Google Scholar] [CrossRef]

- Deng, Liurui, Yongbin Lv, Ye Liu, and Yiwen Zhao. 2021. Impact of Fintech on Bank Risk-Taking: Evidence from China. Risks 9: 99. [Google Scholar] [CrossRef]

- Dietrich, Andreas, and Gabrielle Wanzenried. 2014. The determinants of commercial banking profitability in low-, middle-, and high-income countries. The Quarterly Review of Economics and Finance 54: 337–54. [Google Scholar] [CrossRef]

- Ellul, Andrew, and Vijay Yerramilli. 2013. Stronger risk controls, lower risk: Evidence from US bank holding companies. The Journal of Finance 68: 1757–803. [Google Scholar] [CrossRef]

- Forcadell, Francisco Javier, Elisa Aracil, and Fernando Úbeda. 2020. The impact of corporate sustainability and digitalization on international banks’ performance. Global Policy 11: 18–27. [Google Scholar] [CrossRef]

- Gharbi, Inès, and Aïda Kammoun. 2023. Developing a Multidimensional Financial Inclusion Index: A Comparison Based on Income Groups. Journal of Risk and Financial Management 16: 296. [Google Scholar] [CrossRef]

- Hakimi, Abdelaziz, Rim Boussaada, and Majdi Karmani. 2021. Are financial inclusion and bank stability friends or enemies? Evidence from MENA banks. Applied Economics 54: 2473–89. [Google Scholar] [CrossRef]

- Hansen, Lars Peter. 1982. Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society 50: 1029–54. [Google Scholar] [CrossRef]

- Hausman, Jerry A. 1978. Specification tests in econometrics. Econometrica: Journal of the Econometric Society 46: 1251–1271. [Google Scholar] [CrossRef]

- Heffernan, Shelagh A., and Xiaoqing Fu. 2010. Determinants of financial performance in Chinese banking. Applied Financial Economics 20: 1585–600. [Google Scholar] [CrossRef]

- Ikram, Iqra, and Samreen Lohdi. 2015. Impact of financial inclusion on banks profitability: An empirical study of banking sector of Karachi, Pakistan. International Journal of Management Sciences and Business Research 4: 88–98. [Google Scholar]

- Islam, Md Shahidul, and Shin-Ichi Nishiyama. 2016. The determinants of bank net interest margins: A panel evidence from South Asian countries. Research in International Business and Finance 37: 501–14. [Google Scholar] [CrossRef]

- Issaka Jajah, Yussif, Ebenezer B. Anarfo, and Felix K. Aveh. 2022. Financial inclusion and bank profitability in Sub-Saharan Africa. International Journal of Finance & Economics 27: 32–44. [Google Scholar]

- Jonker, Nicole, and Anneke Kosse. 2022. The interplay of financial education, financial inclusion and financial stability and the role of Big Tech. Contemporary Economic Policy 40: 612–35. [Google Scholar] [CrossRef]

- Jouini, Jamel, and Rami Obeid. 2021. Do Financial Inclusion Indicators Affect Banks’ Profitability? Evidence from Selected Arab Countries. Arab Monetary Fund Working Paper. Available online: https://cutt.ly/2jFdZvT (accessed on 1 June 2023).

- Jungo, João, Mara Madaleno, and Anabela Botelho. 2022. The effect of financial inclusion and competitiveness on financial stability: Why financial regulation matters in developing countries? Journal of Risk and Financial Management 15: 122. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2011. The worldwide governance indicators: Methodology and analytical issues1. Hague Journal on the Rule of Law 3: 220–46. [Google Scholar] [CrossRef]

- Kelikume, Ikechukwu. 2021. Digital financial inclusion, informal economy and poverty reduction in Africa. Journal of Enterprising Communities: People and Places in the Global Economy 15: 626–40. [Google Scholar] [CrossRef]

- Kharabsheh, Buthiena, and Omar Gharaibeh. 2023. Does Financial Inclusion Affect Banks’ Efficiency? ELIT–Economic Laboratory for Transition Research 19: 125. [Google Scholar] [CrossRef]

- Khatib, Saleh F. A., Ernie Hendrawaty, Ayman Hassan Bazhair, Ibraheem A. Abu Rahma, and Hamzeh Al Amosh. 2022. Financial inclusion and the performance of banking sector in Palestine. Economies 10: 247. [Google Scholar] [CrossRef]

- Kleibergen, Frank, and Richard Paap. 2006. Generalized reduced rank tests using the singular value decomposition. Journal of Econometrics 133: 97–126. [Google Scholar] [CrossRef]

- Kumar, Vijay, Sujani Thrikawala, and Sanjeev Acharya. 2021. Financial inclusion and bank profitability: Evidence from a developed market. Global Finance Journal 2020: 100609. [Google Scholar] [CrossRef]

- Lee, Chien-Chiang, and Meng-Fen Hsieh. 2013. The impact of bank capital on profitability and risk in Asian banking. Journal of International Money and Finance 32: 251–81. [Google Scholar] [CrossRef]

- Lee, Chien-Chiang, Runchi Lou, and Fuhao Wang. 2023. Digital financial inclusion and poverty alleviation: Evidence from the sustainable development of China. Economic Analysis and Policy 77: 418–34. [Google Scholar] [CrossRef]

- Li, Dan Dan, and Zheng Xin Wang. 2023. Measurement Methods for Relative Index of Financial Inclusion. Applied Economics Letters 30: 827–33. [Google Scholar] [CrossRef]

- Lv, Shuli, Yangran Du, and Yong Liu. 2022. How do fintechs impact banks’ profitability?—An empirical study based on banks in China. FinTech 1: 155–63. [Google Scholar] [CrossRef]

- Lyons, Angela C., Josephine Kass-Hanna, and Ana Fava. 2021. Fintech development and savings, borrowing, and remittances: A comparative study of emerging economies. Emerging Markets Review 51: 100842. [Google Scholar]

- Markowitz, Harry. 1952. Portfolio Selection. The Journal of Finance 7: 77–91. [Google Scholar]

- Mehrotra, Aaron, and G. V. Nadhanael. 2016. Financial inclusion and monetary policy in emerging Asia. In Financial Inclusion in Asia: Issues and Policy Concerns. Berlin and Heidelberg: Springer, pp. 93–127. [Google Scholar]

- Montgomery, Douglas C., Elizabeth A. Peck, and G. Geoffrey Vining. 2021. Introduction to Linear Regression Analysis. Hoboken: John Wiley & Sons. [Google Scholar]

- Neaime, Simon, and Isabelle Gaysset. 2018. Financial inclusion and stability in MENA: Evidence from poverty and inequality. Finance Research Letters 24: 230–37. [Google Scholar] [CrossRef]

- Nguyen, Thi Truc Huong. 2021. Measuring financial inclusion: A composite FI index for the developing countries. Journal of Economics and Development 23: 77–99. [Google Scholar] [CrossRef]

- Nzyuko, Joseph Mutinda, Ambrose Jagongo, and Husborn Kenyanya. 2018. Financial inclusion innovations and financial performance of commercial banks in Kenya. International Journal of Management and Commerce Innovations 5: 849–56. [Google Scholar]

- Oranga, Odero Joshua, and Ibrahim Tirimba Ondabu. 2018. Effect of financial inclusion on financial performance of banks listed at the Nairobi securities exchange in Kenya. International Journal of Scientific and Research Publications 8: 624–49. [Google Scholar] [CrossRef]

- Park, Cyn Young, and Rogelio V Mercado. 2018. Financial inclusion: New measurement and cross-country impact assessment. Asian Development Bank 539: 1–29. [Google Scholar]

- Renzhi, Nuobu, and Yong Jun Baek. 2020. Can financial inclusion be an effective mitigation measure? evidence from panel data analysis of the environmental Kuznets curve. Finance Research Letters 37: 101725. [Google Scholar] [CrossRef]

- Roodman, David. 2009. How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal 9: 86–136. [Google Scholar] [CrossRef]

- Ross, Stephen A., Randolph W. Westerfield, Bradford D. Jordan, Joseph Lim, and Ruth Tan. 2016. Fundamentals of Corporate Finance. Asia Global Edition. New York: McGraw Hill Education. [Google Scholar]

- Saif-Alyousfi, Abdulazeez Y. H., and Asish Saha. 2021. Determinants of banks’ risk-taking behavior, stability and profitability: Evidence from GCC countries. International Journal of Islamic and Middle Eastern Finance and Management 14: 874–907. [Google Scholar] [CrossRef]

- Schultz, Emma L., David T. Tan, and Kathleen D. Walsh. 2010. Endogeneity and the corporate governance-performance relation. Australian Journal of Management 35: 145–63. [Google Scholar] [CrossRef]

- Sethy, Susanta Kumar, and Phanindra Goyari. 2022. Financial inclusion and financial stability nexus revisited in South Asian countries: Evidence from a new multidimensional financial inclusion index. Journal of Financial Economic Policy 14: 674–93. [Google Scholar] [CrossRef]

- Shehzad, Choudhry Tanveer, Jakob De Haan, and Bert Scholtens. 2013. The relationship between size, growth and profitability of commercial banks. Applied Economics 45: 1751–65. [Google Scholar] [CrossRef]

- Shen, Yan, Wenxiu Hu, and C. James Hueng. 2021. Digital Financial Inclusion and Economic Growth: A Cross-country Study. Procedia Computer Science 187: 218–23. [Google Scholar] [CrossRef]

- Shihadeh, Fadi. 2020. The influence of financial inclusion on banks’ performance and risk: New evidence from MENAP. Banks and Bank Systems 15: 59–71. [Google Scholar] [CrossRef]

- Shihadeh, Fadi. 2021. Financial inclusion and banks’ performance: Evidence from Palestine. Investment Management and Financial Innovation 18: 126–38. [Google Scholar] [CrossRef]

- Shihadeh, Fadi Hassan, Azzam M. T. Hannon, Jian Guan, Ihtisham Ul Haq, and Xiuhua Wang. 2018. Does financial inclusion improve the banks’ performance? Evidence from Jordan. In Global Tensions in Financial Markets. Bingley: Emerald Publishing Limited, pp. 117–38. [Google Scholar]

- Smirlock, Michael. 1985. Evidence on the (non) relationship between concentration and profitability in banking. Journal of Money, Credit and Banking 17: 69–83. [Google Scholar] [CrossRef]

- Sodokin, Koffi, Moubarak Koriko, Dzidzogbé Hechely Lawson, and Mawuli K. Couchoro. 2022. Digital transformation, banking stability, and financial inclusion in Sub-Saharan Africa. Strategic Change 31: 623–37. [Google Scholar] [CrossRef]

- Sugianto, Sugianto, Fahmi Oemar, Luqman Hakim, and Endri Endri. 2020. Determinants of firm value in the banking sector: Random effects model. International Journal of Innovation, Creativity and Change 12: 208–18. [Google Scholar]

- Tan, Yong. 2016. The impacts of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions and Money 40: 85–110. [Google Scholar] [CrossRef]

- Tan, Yong, and Christos Floros. 2012. Bank profitability and GDP growth in China: A note. Journal of Chinese Economic and Business Studies 10: 267–73. [Google Scholar] [CrossRef]

- Tay, Lee Ying, Hen Toong Tai, and Gek Siang Tan. 2022. Digital financial inclusion: A gateway to sustainable development. Heliyon 8: e09766. [Google Scholar] [CrossRef] [PubMed]

- Tram, Thi Xuan Huong, Tien Dinh Lai, and Thi Truc Huong Nguyen. 2023. Constructing a composite financial inclusion index for developing economies. The Quarterly Review of Economics and Finance 87: 257–265. [Google Scholar] [CrossRef]

- Tran, Son Hung, and Liem Thanh Nguyen. 2020. Financial development, business cycle and bank risk in Southeast Asian countries. The Journal of Asian Finance, Economics and Business 7: 127–35. [Google Scholar] [CrossRef]

- Vo, Duc H., and Nhan T. Nguyen. 2021. Does financial inclusion improve bank performance in the Asian region? Asian-Pacific Economic Literature 35: 123–35. [Google Scholar] [CrossRef]

- Vo, Duc Hong, Nhan Thien Nguyen, and Loan Thi-Hong Van. 2021. Financial inclusion and stability in the Asian region using bank-level data. Borsa Istanbul Review 21: 36–43. [Google Scholar] [CrossRef]

- Wang, Rui, Jiangtao Liu, and Hang Luo. 2021. Fintech development and bank risk taking in China. The European Journal of Finance 27: 397–418. [Google Scholar] [CrossRef]

- Wang, Yanqi, Muhammad Ali, Asadullah Khaskheli, Komal Akram Khan, and Chin-Hong Puah. 2022. The interconnectedness of financial inclusion and bank profitability in rising economic powers: Evidence from heterogeneous panel analysis. International Journal of Social Economics. Available online: https://www.emerald.com/insight/content/doi/10.1108/IJSE-05-2022-0364/full/html (accessed on 25 February 2023).

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- Wooldridge, Jeffrey M. 2015. Introductory Econometrics: A Modern Approach. Boston: Cengage Learning. [Google Scholar]

- World Bank. 2022. World Development Indicators. Available online: https://databank.worldbank.org/source/world-development-indicators (accessed on 15 January 2023).

- Wu, Guo, Jiadong Luo, and Kejing Tao. 2023. Research on the influence of FinTech development on credit supply of commercial banks: The case of China. Applied Economics, 1–17. [Google Scholar] [CrossRef]

- Yadav, Vishal, Bhanu Pratap Singh, and Nirmala Velan. 2021. Multidimensional financial inclusion index for Indian states. Journal of Public Affairs 21: e2238. [Google Scholar] [CrossRef]

- Yakubu, Ibrahim Nandom, and Alhassan Musah. 2022. The nexus between financial inclusion and bank profitability: A dynamic panel approach. Journal of Sustainable Finance & Investment, 1–14. [Google Scholar] [CrossRef]

- Yin, Fang, Xiaomei Jiao, Jincheng Zhou, Xiong Yin, Ebuka Ibeke, Marvellous GodsPraise Iwendi, and Cresantus Biamba. 2022. Fintech application on banking stability using Big Data of an emerging economy. Journal of Cloud Computing 11: 43. [Google Scholar] [CrossRef]

| Particulars | Number |

|---|---|

| Population: All developing countries included in the database (FAS–IMF1) | 148 |

| Less: Countries lacking fintech data in the FAS and WDI databases | (104) |

| Less: Countries * lacking required bank-specific data in the OBF database | (4) |

| Final sample of developing countries | 40 |

| Variables | Symbol | Measurement | Sign | Data |

|---|---|---|---|---|

| Bank profitability (dependent variables) | ||||

| Return on assets | ROA | Net profits/Average total assets (%) | OBF | |

| Return on equity | ROE | Net profits/Average total equity (%) | OBF | |

| Net interest margin | NIM | Net interest income/Earning assets (%) | OBF | |

| Fintech indices (independent variables) | ||||

| Fintech index | FI | Using PCA combining FIA, FIP, and FIU | + | FAS, WDI |

| Availability dimension index | FIA | Using PCA including four components | + | FAS, WDI |

| Penetration dimension index | FIP | Using PCA including three components | + | FAS |

| Usage dimension index | FIU | Using PCA including three components | + | FAS |

| Bank-specific control variables | ||||

| Cost-to-income ratio | CIR | Operating expenses/Operating revenue (%) | - | OBF |

| Capital adequacy ratio | CAR | Tier 1 plus Tier 2 capital/ Risk-weighted assets (%) | +/- | OBF |

| Non-performing loan ratio | NPL | Non-performing loans/Gross loans (%) | - | OBF |

| Bank size | SIZE | ln(Total assets) | +/- | OBF |

| Loan-to-deposit ratio | LDR | Total loans/Total deposits (%) | +/- | OBF |

| Liquidity ratio | LR | Liquid assets/Total assets (%) | - | OBF |

| Macro-specific variables | ||||

| GDP growth | GDP | Annual increase rate of GDP (%) | + | WDI |

| Inflation | INF | Change in consumer price index (%) | +/- | WDI |

| Institutional quality index | IQ | Using PCA adding six elements of WGI | +/- | WGI |

| Instrumental variables | ||||

| Mobile phone share | MPS | In the nearby countries within the same region (%) | WDI | |

| Emergency fund sources | FnF | Borrowed from friends or family (%) | Findex |

| Variables | Obs. | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Dependent variables | |||||

| ROA | 5463 | 1.45 | 1.02 | 0.044 | 3.35 |

| ROE | 5459 | 11.99 | 8.07 | 0.32 | 25.81 |

| NIM | 5945 | 4.78 | 2.78 | 1.36 | 10.97 |

| Independent variables | |||||

| FI | 5991 | 0.285 | 0.190 | 0.00 | 1.00 |

| FIA | 5991 | 0.189 | 0.222 | 0.00 | 1.00 |

| FIP | 5991 | 0.397 | 0.186 | 0.00 | 1.00 |

| FIU | 5991 | 0.138 | 0.190 | 0.00 | 1.00 |

| Bank-specific | |||||

| CIR | 5981 | 57.412 | 17.007 | 33.786 | 87.958 |

| CAR | 4391 | 19.16 | 8.315 | 10.43 | 42.89 |

| NPL | 4336 | 6.464 | 6.541 | 0.293 | 24.964 |

| SIZE | 5991 | 13.380 | 1.875 | 6.606 | 19.520 |

| LDR | 5776 | 76.673 | 24.994 | 37.894 | 119.937 |

| LR | 5986 | 29.397 | 14.323 | 11.482 | 55.516 |

| Macro-specific | |||||

| GDP | 5991 | 4.139 | 3.125 | −3.63 | 8.642 |

| INF | 5991 | 4.683 | 4.202 | −0.846 | 16.564 |

| IQ | 5991 | 0.496 | 0.206 | 0.00 | 1.00 |

| Instrumental variables | |||||

| MPS | 5991 | 0.981 | 0.019 | 0.869 | 1.00 |

| FnF | 5832 | 31.009 | 16.924 | 3.410 | 77.150 |

| Variables | ROA | ROE | NIM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | |

| FI | 0.477 *** | 0.241 *** | 0.243 * | 0.421 *** | 0.993 *** | 0.314 * | 0.912 ** | 0.881 *** | 0.420 ** | 0.388 *** | 0.704 *** | 0.129 * |

| (0.104) | (0.08) | (0.145) | (0.092) | (0.309) | (0.070) | (0.265) | (0.203) | (0.185) | (0.142) | (0.256) | (0.165) | |

| CIR | −0.031 *** | −0.031 *** | −0.031 *** | −0.031 *** | −0.25 *** | −0.251 *** | −0.249 *** | −0.248 *** | −0.027 *** | −0.028 *** | −0.027 *** | −0.027 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.009) | (0.009) | (0.009) | (0.009) | (0.002) | (0.002) | (0.002) | (0.002) | |

| CAR | 0.015 *** | 0.016 *** | 0.016 *** | 0.016 *** | −0.009 | −0.004 | −0.005 | −0.007 | −0.009 ** | −0.009 ** | −0.009 ** | −0.007 * |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.021) | (0.021) | (0.021) | (0.021) | (0.004) | (0.004) | (0.004) | (0.004) | |

| NPL | −0.024 *** | −0.023 *** | −0.023 *** | −0.023 *** | −0.221 *** | −0.218 *** | −0.218 *** | −0.219 *** | −0.014 *** | −0.014 *** | −0.014 *** | −0.014 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.019) | (0.019) | (0.019) | (0.019) | (0.004) | (0.004) | (0.004) | (0.004) | |

| SIZE | −0.099 *** | −0.093 ** | −0.083 ** | −0.085 ** | −0.681 ** | −0.724 ** | −0.774 ** | −0.763 ** | −0.732 *** | −0.736 *** | −0.72 *** | −0.716 *** |

| (0.038) | (0.038) | (0.038) | (0.038) | (0.333) | (0.333) | (0.332) | (0.331) | (0.069) | (0.069) | (0.069) | (0.069) | |

| LDR | −0.001 | −0.002* | −0.002* | −0.001 | −0.035 *** | −0.039 *** | −0.037 *** | −0.033 *** | 0.007 *** | 0.007 *** | 0.007 *** | 0.007 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.008) | (0.008) | (0.008) | (0.008) | (0.002) | (0.002) | (0.002) | (0.002) | |

| LR | −0.004 *** | −0.004 *** | −0.004 *** | −0.004 *** | −0.022 * | −0.024 ** | −0.023 * | −0.021 * | −0.003 | −0.003 | −0.003 | −0.003 |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.012) | (0.012) | (0.012) | (0.012) | (0.003) | (0.003) | (0.003) | (0.003) | |

| GDP | 0.022 *** | 0.023 *** | 0.023 *** | 0.021 *** | 0.157 *** | 0.165 *** | 0.164 *** | 0.152 *** | 0.005 | 0.004 | 0.004 | 0.005 |

| (0.004) | (0.005) | (0.005) | (0.005) | (0.039) | (0.039) | (0.039) | (0.039) | (0.008) | (0.008) | (0.008) | (0.008) | |

| INF | 0.004 | 0.005 | 0.004 | 0.003 | 0.15 *** | 0.155 *** | 0.15 *** | 0.142 *** | 0.036 *** | 0.038 *** | 0.036 *** | 0.036 *** |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.034) | (0.034) | (0.034) | (0.034) | (0.007) | (0.007) | (0.007) | (0.007) | |

| IQ | 0.119 | 0.04 | 0.20 | 0.296 | 0.561 * | 0.883 * | 0.343 * | 0.423 | 0.592 | 0.793 | 0.589 | 0.508 |

| (0.341) | (0.348) | (0.342) | (0.34) | (0.979) | (0.034) | (0.983) | (0.969) | (0.600) | (0.606) | (0.599) | (0.600) | |

| Constant | 4.51 *** | 4.55 *** | 4.29 *** | 4.25 *** | 24.36 *** | 24.47 *** | 22.75 *** | 22.71 *** | 16.01 *** | 16.22 *** | 15.73 *** | 15.80 *** |

| (0.55) | (0.555) | (0.551) | (0.549) | (4.807) | (4.845) | (4.804) | (4.796) | (1.002) | (1.009) | (0.999) | (1.00) | |

| Obs. | 3615 | 3615 | 3615 | 3615 | 3612 | 3612 | 3612 | 3612 | 3871 | 3871 | 3871 | 3871 |

| R-squared | 0.33 | 0.327 | 0.326 | 0.33 | 0.299 | 0.297 | 0.298 | 0.299 | 0.14 | 0.13 | 0.14 | 0.14 |

| F-statistic | 76.76 *** | 75.88 *** | 75.41 *** | 76.76 *** | 66.48 *** | 65.96 *** | 66.08 *** | 66.62 *** | 22.97 *** | 23.10 *** | 23.10 *** | 22.71 *** |

| Time fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Bank fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Variables | ROA | ROE | NIM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | |

| FI | 0.325 * | 0.263 * | 0.469 ** | 0.256 * | 0.525 * | 0.438 * | 0.753 ** | 0.293 * | 0.525 * | 0.395 * | 1.122 *** | 0.214 * |

| (0.184) | (0.163) | (0.211) | (0.186) | (0.604) | (0.425) | (0.837) | (0.425) | (0.317) | (0.292) | (0.364) | (0.322) | |

| CIR | −0.031 *** | −0.031 *** | −0.031 *** | −0.031 *** | −0.248 *** | −0.249 *** | −0.248 *** | −0.248 *** | −0.028 *** | −0.028 *** | −0.027 *** | −0.027 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.009) | (0.009) | (0.009) | (0.009) | (0.002) | (0.002) | (0.002) | (0.002) | |

| CAR | 0.015 *** | 0.016 *** | 0.016 *** | 0.016 *** | −0.005 | −0.003 | −0.007 | −0.001 | −0.009 ** | −0.009 ** | −0.01 ** | −0.008 * |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.02) | (0.02) | (0.02) | (0.02) | (0.004) | (0.004) | (0.004) | (0.004) | |

| NPL | −0.024 *** | −0.023 *** | −0.023 *** | −0.023 *** | −0.219 *** | −0.218 *** | −0.219 *** | −0.217 *** | −0.013 *** | −0.014 *** | −0.013 *** | −0.014 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.018) | (0.018) | (0.018) | (0.018) | (0.004) | (0.004) | (0.004) | (0.004) | |

| SIZE | −0.093 ** | −0.093 ** | −0.083 ** | −0.083 ** | 0.716 ** | 0.723 ** | 0.777 ** | 0.778 ** | −0.72 *** | −0.721 *** | −0.707 *** | −0.701 *** |

| (0.036) | (0.036) | (0.036) | (0.036) | (0.315) | (0.317) | (0.311) | (0.311) | (0.066) | (0.066) | (0.064) | (0.064) | |

| LDR | −0.001 | −0.002 ** | −0.001 * | −0.001 | −0.038 *** | −0.04 *** | −0.037 *** | −0.039 *** | 0.007 *** | 0.007 *** | 0.007 *** | 0.007 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.008) | (0.007) | (0.007) | (0.008) | (0.002) | (0.002) | (0.002) | (0.002) | |

| LR | −0.004 *** | −0.004 *** | −0.004 *** | −0.004 *** | −0.025 ** | −0.026 ** | −0.025 ** | −0.026 ** | −0.003 | −0.003 | −0.003 | −0.003 |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.012) | (0.011) | (0.011) | (0.012) | (0.002) | (0.002) | (0.002) | (0.002) | |

| GDP | 0.024 *** | 0.025 *** | 0.025 *** | 0.024 *** | 0.176 *** | 0.183 *** | 0.183 *** | 0.177 *** | −0.003 | −0.002 | −0.001 | −0.003 |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.038) | (0.038) | (0.038) | (0.039) | (0.008) | (0.008) | (0.008) | (0.008) | |

| INF | 0.004 | 0.006 | 0.005 | 0.004 | 0.159 *** | 0.166 *** | 0.161 *** | 0.156 *** | 0.036 *** | 0.038 *** | 0.036 *** | 0.036 *** |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.032) | (0.033) | (0.032) | (0.032) | (0.007) | (0.007) | (0.007) | (0.007) | |

| IQ | 0.169 | 0.029 | 0.159 | 0.29 | 0.884 * | 0.568 * | 0.242 * | 0.182 | 0.855 | 0.042* | 0.879 | 0.732 |

| (0.325) | (0.353) | (0.325) | (0.321) | (0.839) | (0.079) | (0.832) | (0.805) | (0.568) | (0.601) | (0.566) | (0.568) | |

| Constant | 5.073 *** | 5.225 *** | 4.902 *** | 4.902 *** | 29.09 *** | 29.89 *** | 27.62 *** | 28.33 *** | 19.79 *** | 20.01 *** | 19.44 *** | 19.58 *** |

| (0.47) | (0.484) | (0.475) | (0.481) | (4.116) | (4.235) | (4.152) | (4.209) | (0.859) | (0.89) | (0.86) | (0.87) | |

| Obs. | 3565 | 3565 | 3565 | 3565 | 3562 | 3562 | 3562 | 3562 | 3815 | 3815 | 3815 | 3815 |

| R-squared | 0.798 | 0.798 | 0.797 | 0.798 | 0.761 | 0.761 | 0.761 | 0.761 | 0.908 | 0.908 | 0.908 | 0.908 |

| Chi2 | 140.6 *** | 140.6 *** | 140.2 *** | 140.0 *** | 113.7 *** | 113.5 *** | 113.1 *** | 113.7 *** | 375.1 *** | 375.2 *** | 375.3 *** | 375.2 *** |

| Time fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Bank fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| LM test | 147.91 | 153.18 | 133.67 | 168.24 | 101.38 | 123.32 | 79.21 | 163.87 | 149.65 | 174.81 | 97.32 | 189.57 |

| Hansen J | 0.31 | 0.25 | 0.43 | 0.23 | 0.56 | 0.39 | 0.67 | 0.27 | 0.49 | 0.41 | 0.89 | 0.32 |

| p-value (J) | 0.18 | 0.48 | 0.34 | 0.24 | 0.31 | 0.21 | 0.56 | 0.32 | 0.71 | 0.43 | 0.87 | 0.23 |

| Variables | ROA | ROE | NIM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | |

| Lag depen. | 0.717 *** | 0.72 *** | 0.72 *** | 0.72 *** | 0.725 *** | 0.714 *** | 0.717 *** | 0.715 *** | 0.925 *** | 0.931 *** | 0.929 *** | 0.927 *** |

| (0.007) | (0.008) | (0.008) | (0.008) | (0.006) | (0.007) | (0.008) | (0.007) | (0.002) | (0.003) | (0.003) | (0.002) | |

| FI | 0.276 *** | 0.323 *** | 0.172** | 0.192 *** | 0.551 * | 1.793 *** | 2.629 *** | 0.458 * | 0.277 *** | 0.859 *** | 0.526 *** | 0.494 *** |

| (0.061) | (0.056) | (0.078) | (0.064) | (0.329) | (0.425) | (1.016) | (0.214) | (0.105) | (0.106) | (0.09) | (0.106) | |

| CIR | −0.009 *** | −0.008 *** | −0.009 *** | −0.008 *** | −0.042 *** | −0.052 *** | −0.049 *** | −0.048 *** | −0.002 *** | −0.003 *** | −0.002 *** | −0.002 ** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.003) | (0.003) | (0.003) | (0.003) | (0.0003) | (0.0003) | (0.0003) | (0.0002) | |

| CAR | 0.006 *** | 0.006 *** | 0.006 *** | 0.006 *** | −0.036 *** | −0.028 *** | −0.025 *** | −0.023 *** | 0.005 *** | 0.006 *** | 0.005 *** | 0.005 *** |

| (0.002) | (0.002) | (0.002) | (0.001) | (0.003) | (0.004) | (0.004) | (0.004) | (0.001) | (0.0005) | (0.001) | (0.001) | |

| NPL | −0.002 *** | −0.003 *** | −0.002 *** | −0.002 *** | −0.057 *** | −0.087 *** | −0.086 *** | −0.086 *** | −0.005 *** | −0.006 *** | −0.004 *** | −0.004 ** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.006) | (0.007) | (0.007) | (0.007) | (0.001) | (0.001) | (0.001) | (0.001) | |

| SIZE | −0.001 | −0.001 | −0.001 | −0.003 | 0.166 *** | 0.163 *** | 0.172 *** | 0.195 *** | 0.011 *** | 0.013 *** | 0.011 *** | 0.013 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.02) | (0.017) | (0.02) | (0.02) | (0.002) | (0.003) | (0.003) | (0.003) | |

| LDR | −0.001 *** | −0.001 ** | −0.001 *** | −0.001 *** | −0.014 *** | −0.013 *** | −0.014 *** | −0.011 *** | 0.001 | 0.001 | 0.001 | 0.001 * |

| (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.002) | (0.002) | (0.002) | (0.0002) | (0.0002) | (0.0002) | (0.0002) | |

| LR | 0.002 | 0.003 | 0.001 | 0.004 | 0.007 *** | 0.004 | 0.003 | 0.007** | −0.005 *** | −0.005 *** | −0.005 *** | −0.005 ** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.003) | (0.003) | (0.003) | (0.003) | (0.0004) | (0.0004) | (0.0004) | (0.0004) | |

| GDP | 0.015 ** | 0.016 *** | 0.03 *** | 0.014 ** | 0.605 *** | 0.473 *** | 0.279 *** | 0.194 *** | 0.036 *** | 0.007 | 0.034 *** | 0.04 *** |

| (0.006) | (0.006) | (0.006) | (0.006) | (0.048) | (0.049) | (0.062) | (0.061) | (0.006) | (0.009) | (0.008) | (0.006) | |

| INF | 0.02 *** | 0.022 *** | 0.027 *** | 0.019 *** | 0.132 *** | 0.145 *** | 0.051 | 0.094 ** | −0.072 *** | −0.069 *** | −0.075 *** | −0.086 ** |

| (0.005) | (0.004) | (0.005) | (0.004) | (0.031) | (0.044) | (0.044) | (0.047) | (0.007) | (0.007) | (0.008) | (0.009) | |

| IQ | 0.972 *** | 0.452 *** | 0.575 *** | 0.141 *** | 0.38 *** | 0.13 *** | 0.47 *** | 0.092 *** | 0.449 ** | 0.722 *** | 0.552 ** | 0.032 ** |

| (0.032) | (0.028) | (0.0261) | (0.012) | (0.024) | (0.0517) | (0.021) | (0.032) | (0.221) | (0.233) | (0.225) | (0.036) | |

| Constant | 0.719 *** | 0.979 *** | 0.874 *** | 0.96 *** | 4.691 *** | 6.602 *** | 5.707 *** | 5.612 *** | 0.684 *** | 0.619 *** | 0.651 *** | 0.666 *** |

| (0.161) | (0.157) | (0.16) | (0.155) | (1.37) | (1.033) | (1.17) | (1.077) | (0.218) | (0.238) | (0.221) | (0.231) | |

| Obs. | 3087 | 3087 | 3087 | 3087 | 3084 | 3084 | 3084 | 3084 | 3338 | 3338 | 3338 | 3338 |

| Time fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Bank fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| AR(1) | 0.001 | 0.000 | 0.002 | 0.001 | 0.000 | 0.000 | 0.000 | 0.003 | 0.000 | 0.005 | 0.000 | 0.001 |

| AR(2) | 0.185 | 0.188 | 0.193 | 0.178 | 0.497 | 0.446 | 0.423 | 0.410 | 0.429 | 0.373 | 0.427 | 0.393 |

| Hansen test | 0.753 | 0.835 | 0.789 | 0.763 | 0.688 | 0.685 | 0.738 | 0.825 | 0.631 | 0.707 | 0.731 | 0.695 |

| Variables | ROA | ROE | NIM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | FI | FIA | FIP | FIU | |

| FI | 0.155 *** | 0.027 * | 0.615 *** | 0.941 *** | 1.303 *** | 0.053 ** | 4.348 *** | 6.603 *** | 1.338 *** | 0.015 * | 2.457 *** | 3.14 *** |

| (0.056) | (0.003) | (0.078) | (0.036) | (0.401) | (0.003) | (0.542) | (0.35) | (0.145) | (0.003) | (0.199) | (0.155) | |

| CIR | −0.031 *** | −0.031 *** | −0.031 *** | −0.032 *** | −0.234 *** | −0.233 *** | −0.238 *** | −0.241 *** | −0.013 *** | −0.01 *** | −0.012 *** | −0.013 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.004) | (0.004) | (0.004) | (0.004) | (0.001) | (0.001) | (0.001) | (0.001) | |

| CAR | 0.021 *** | 0.023 *** | 0.019 *** | 0.017 *** | −0.061 *** | −0.069 *** | −0.077 *** | −0.103 *** | 0.037 *** | 0.04 *** | 0.035 *** | 0.035 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.009) | (0.009) | (0.009) | (0.008) | (0.003) | (0.003) | (0.003) | (0.002) | |

| NPL | −0.016 *** | −0.017 *** | −0.016 *** | −0.016 *** | −0.183 *** | −0.184 *** | −0.176 *** | −0.182 *** | 0.02 *** | 0.018 *** | 0.021 *** | 0.021 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.011) | (0.011) | (0.01) | (0.01) | (0.003) | (0.003) | (0.003) | (0.002) | |

| SIZE | −0.071 *** | −0.076 *** | −0.08 *** | −0.071 *** | −0.152 *** | −0.108** | −0.229 *** | −0.056 | −0.494 *** | −0.462 *** | −0.521 *** | −0.463 *** |

| (0.005) | (0.004) | (0.005) | (0.005) | (0.044) | (0.049) | (0.044) | (0.041) | (0.016) | (0.014) | (0.017) | (0.016) | |

| LDR | −0.002 *** | −0.002 *** | −0.002 *** | −0.002 *** | −0.055 *** | −0.052 *** | −0.056 *** | −0.049 *** | −0.003 *** | −0.005 *** | −0.003 *** | −0.002 ** |

| (0.0001) | (0.0001) | (0.0001) | (0.0001) | (0.003) | (0.003) | (0.003) | (0.002) | (0.001) | (0.001) | (0.001) | (0.001) | |

| LR | 0.002 *** | 0.001 ** | 0.001 *** | 0.001 | 0.019 *** | 0.016 *** | 0.02 *** | 0.021 *** | −0.004 *** | −0.009 *** | −0.001 | −0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.005) | (0.005) | (0.004) | (0.004) | (0.001) | (0.001) | (0.001) | (0.001) | |

| GDP | 0.016 *** | 0.019 *** | 0.02 *** | 0.011 *** | 0.069 *** | 0.11 *** | 0.085 *** | 0.038** | −0.012 *** | −0.008** | 0.001 | −0.01 ** |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.017) | (0.017) | (0.016) | (0.017) | (0.004) | (0.004) | (0.004) | (0.004) | |

| INF | 0.024 *** | 0.026 *** | 0.024 *** | 0.025 *** | 0.253 *** | 0.266 *** | 0.246 *** | 0.216 *** | 0.061 *** | 0.057 *** | 0.07 *** | 0.062 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.017) | (0.018) | (0.017) | (0.017) | (0.005) | (0.005) | (0.005) | (0.005) | |

| IQ | 0.249 *** | 0.249 *** | −0.079 | 0.164 *** | −0.292 | −0.779 ** | −2.56 *** | −0.083 | 0.587 *** | 1.165 *** | −0.304 * | 0.897 *** |

| (0.042) | (0.036) | (0.06) | (0.045) | (0.368) | (0.379) | (0.439) | (0.292) | (0.14) | (0.126) | (0.168) | (0.108) | |

| Constant | 3.63 *** | 3.765 *** | 3.855 *** | 3.849 *** | 32.31 *** | 31.94 *** | 34.13 *** | 32.09 *** | 10.91 *** | 10.49 *** | 11.12 *** | 10.3 *** |

| (0.111) | (0.105) | (0.103) | (0.112) | (0.963) | (1.049) | (0.945) | (0.921) | (0.29) | (0.277) | (0.317) | (0.305) | |

| Obs. | 3603 | 3603 | 3603 | 3603 | 3600 | 3600 | 3600 | 3600 | 3862 | 3862 | 3862 | 3862 |

| Wald chi2 | 128.2 *** | 79.6 *** | 150.8 *** | 138.5 *** | 120.1 *** | 70.8 *** | 117.5 *** | 210.7 *** | 67.3 *** | 24.7 *** | 93.8 *** | 97.1 *** |

| Time fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Variables | Low FI | High FI | ||||

|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | |

| ROA | ROE | NIM | ROA | ROE | NIM | |

| FI | 0.471 | 0.717 | 0.091 | 0.517 *** | 0.559 *** | 1.153 *** |

| (0.248) | (0.543) | (0.053) | (0.169) | (0.477) | (0.272) | |

| CIR | −0.03 *** | −0.248 *** | −0.022 *** | −0.033 *** | −0.257 *** | −0.034 *** |

| (0.001) | (0.012) | (0.002) | (0.002) | (0.015) | (0.004) | |

| CAR | 0.013 *** | −0.05 * | −0.006 | 0.018 *** | 0.035 | −0.009 |

| (0.003) | (0.028) | (0.008) | (0.004) | (0.032) | (0.008) | |

| NPL | −0.022 *** | −0.257 *** | −0.009* | −0.026 *** | −0.19 *** | −0.021 ** |

| (0.003) | (0.024) | (0.005) | (0.004) | (0.031) | (0.008) | |

| SIZE | −0.078 | −0.197 | −0.53 *** | −0.083 | 2.127 *** | −1.074 *** |

| (0.049) | (0.419) | (0.105) | (0.063) | (0.554) | (0.155) | |

| LDR | −0.001 | −0.059 *** | −0.003 | −0.001 | −0.008 | 0.019 *** |

| (0.001) | (0.01) | (0.002) | (0.001) | (0.012) | (0.003) | |

| LR | −0.003 | −0.018 | −0.006 * | −0.004 | −0.03 | −0.001 |

| (0.002) | (0.015) | (0.003) | (0.002) | (0.02) | (0.005) | |

| GDP | 0.002 | −0.063 | −0.024 ** | 0.046 *** | 0.405 *** | 0.016 |

| (0.006) | (0.05) | (0.011) | (0.007) | (0.063) | (0.014) | |

| INF | −0.003 | 0.111 ** | 0.015 | 0.004 | 0.141 *** | 0.062 *** |

| (0.006) | (0.049) | (0.011) | (0.006) | (0.049) | (0.016) | |

| IQ | −0.639 | −6.82 ** | −0.517 | 2.11 *** | 11.259 * | 2.139 * |

| (0.397) | (3.429) | (0.733) | (0.733) | (6.425) | (0.281) | |

| Constant | 4.606 *** | 39.72 *** | 11.676 *** | 3.14 *** | −7.089 | 17.462 *** |

| (0.694) | (5.995) | (1.539) | (0.969) | (8.501) | (2.306) | |

| Observations | 2014 | 2013 | 2148 | 1601 | 1599 | 1723 |

| R-squared | 0.337 | 0.339 | 0.098 | 0.351 | 0.299 | 0.289 |

| F-statistic | 44.15 *** | 44.38 *** | 10.14 *** | 37.02 *** | 29.11 *** | 17.31 *** |

| Time fixed effect | yes | yes | yes | yes | yes | yes |

| Bank fixed effect | yes | yes | yes | yes | yes | yes |

| Variables | Low GDP | High GDP | ||||

|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | |

| ROA | ROE | NIM | ROA | ROE | NIM | |

| FI | 0.233 | 0.107 | 0.254 | 0.913 *** | 1.802 *** | 0.778 *** |

| (0.176) | (0.117) | (0.334) | (0.16) | (0.452) | (0.269) | |

| CIR | −0.035 *** | −0.27 *** | −0.023 *** | −0.032 *** | −0.255 *** | −0.033 *** |

| (0.002) | (0.016) | (0.004) | (0.001) | (0.013) | (0.003) | |

| CAR | 0.01 ** | −0.022 | −0.013 * | 0.018 *** | 0.002 | −0.009 |

| (0.004) | (0.033) | (0.007) | (0.004) | (0.032) | (0.006) | |

| NPL | −0.032 *** | −0.305 *** | 0.027 *** | −0.014 *** | −0.149 *** | −0.005 |

| (0.003) | (0.029) | (0.006) | (0.003) | (0.03) | (0.006) | |

| SIZE | −0.101 | 1.116 ** | −0.571 *** | −0.122 ** | 0.752 | −1.026 *** |

| (0.064) | (0.535) | (0.117) | (0.055) | (0.496) | (0.099) | |

| LDR | −0.001 | −0.04 *** | 0.007 *** | −0.001 | −0.025 ** | 0.006 *** |

| (0.001) | (0.012) | (0.003) | (0.001) | (0.011) | (0.002) | |

| LR | −0.002 | −0.03 | 0.000 | −0.004 * | −0.008 | −0.009 ** |

| (0.002) | (0.019) | (0.004) | (0.002) | (0.018) | (0.004) | |

| GDP | 0.018 * | 0.208 ** | −0.008 | 0.011 | 0.136 | 0.003 |

| (0.01) | (0.086) | (0.019) | (0.01) | (0.095) | (0.019) | |

| INF | −0.027 *** | −0.083 | 0.052 *** | 0.004 | 0.216 *** | 0.04 *** |

| (0.006) | (0.053) | (0.012) | (0.007) | (0.062) | (0.012) | |

| IQ | 0.022 | −6.01 | −0.617 | 0.426 | 2.746 | 0.413 |

| (0.58) | (4.87) | (0.988) | (0.486) | (4.405) | (0.876) | |

| Constant | 5.11 *** | 23.40 *** | 13.37 *** | 4.60 *** | 17.38** | 19.85 *** |

| (0.925) | (7.783) | (1.707) | (.799) | (7.243) | (1.441) | |

| Observations | 1625 | 1622 | 1749 | 1990 | 1990 | 2122 |

| R-squared | 0.349 | 0.352 | 0.085 | 0.322 | 0.276 | 0.182 |

| F-statistic | 31.44 *** | 31.81 *** | 6.01 *** | 36.73 *** | 29.45 *** | 18.70 *** |

| Time fixed effect | yes | yes | yes | yes | yes | yes |

| Bank fixed effect | yes | yes | yes | yes | yes | yes |

| Variables | ROA | ROE | NIM | |||

|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | |

| Small Banks | Large Banks | Small Banks | Large Banks | Small Banks | Large Banks | |

| FI | 0.074 | 0.639 *** | 1.003 | 3.011 *** | 0.183 | 0.403 *** |

| (0.211) | (0.106) | (1.699) | (1.044) | (0.193) | (0.35) | |

| CIR | −0.035 *** | −0.026 *** | −0.256 *** | −0.242 *** | −0.027 *** | −0.029 *** |

| (0.002) | (0.001) | (0.014) | (0.012) | (0.003) | (0.002) | |

| CAR | 0.018 *** | 0.012 *** | 0.016 | −0.034 | −0.003 | −0.011 |

| (0.004) | (0.004) | (0.029) | (0.037) | (0.006) | (0.007) | |

| NPL | −0.025 *** | −0.022 *** | −0.23 *** | −0.224 *** | 0.023 *** | −0.002 |

| (0.003) | (0.003) | (0.028) | (0.029) | (0.006) | (0.005) | |

| SIZE | −0.059 | −0.199 *** | 0.771 | 0.697 | −1.089 *** | −0.539 *** |

| (0.063) | (0.055) | (0.51) | (0.54) | (0.109) | (0.101) | |

| LDR | 0.002 | −0.002 ** | −0.022 ** | −0.032 *** | 0.01 *** | 0.007 *** |

| (0.001) | (0.001) | (0.011) | (0.012) | (0.002) | (0.002) | |

| LR | −0.004 * | −0.002 | −0.013 | −0.011 | −0.006 | −0.009 |

| (0.002) | (0.002) | (0.018) | (0.018) | (0.004) | (0.003) | |

| GDP | 0.014 * | 0.026 *** | 0.087 | 0.186 *** | −0.011 | −0.002 |

| (0.007) | (0.005) | (0.06) | (0.052) | (0.013) | (0.01) | |

| INF | −0.007 | 0.029 *** | 0.078 | 0.258 *** | 0.042 *** | 0.036 *** |

| (0.006) | (0.005) | (0.049) | (0.051) | (0.011) | (0.01) | |

| IQ | 0.756 | 0.655 * | −1.444 | 3.355 | 0.682 | −1.407 * |

| (0.614) | (0.396) | (4.947) | (3.891) | (0.983) | (0.739) | |

| Constant | 3.574 *** | 5.948 *** | 20.326 *** | 20.449 ** | 19.44 *** | 13.718 *** |

| (0.865) | (0.844) | (6.996) | (8.296) | (1.496) | (1.564) | |

| Observations | 1669 | 1946 | 1666 | 1946 | 1862 | 2009 |

| R-squared | 0.331 | 0.397 | 0.295 | 0.339 | 0.134 | 0.171 |

| F-statistic | 33.20 *** | 55.05 *** | 28.09 *** | 42.75 *** | 11.82 *** | 17.84 *** |

| Time fixed effect | yes | yes | yes | yes | yes | yes |

| Bank fixed effect | yes | yes | yes | yes | yes | yes |

| Variables | ROA | ROE | NIM | ||||||

|---|---|---|---|---|---|---|---|---|---|

| I | II | III | IV | V | VI | VII | VIII | IX | |

| Conventional Bank | Islamic Bank | Savings Bank | Conventional Bank | Islamic Bank | Savings Bank | Conventional Bank | Islamic Bank | Savings Bank | |

| FI | 0.521 *** | 0.121 | −0.055 | 3.622 *** | 1.323 | 2.973 | 0.694 *** | 0.291 | 0.828 |

| (0.107) | (0.513) | (1.311) | (0.944) | (4.013) | (10.906) | (0.185) | (0.393) | (0.353) | |

| CIR | −0.031 *** | −0.03 *** | −0.038 *** | −0.249 *** | −0.278 *** | −0.274 *** | −0.028 *** | 0.006 | −0.082 *** |

| (0.001) | (0.004) | (0.011) | (0.01) | (0.031) | (0.093) | (0.002) | (0.011) | (0.016) | |

| CAR | 0.018 *** | −0.01 | 0.072 *** | 0.013 | −0.193 *** | 0.459 ** | 0.001 | −0.053 *** | −0.032 |

| (0.003) | (0.006) | (0.022) | (0.023) | (0.05) | (0.187) | (0.005) | (0.019) | (0.032) | |

| NPL | −0.022 *** | −0.051 *** | −0.036 * | −0.216 *** | −0.416 *** | −0.255 | −0.017 *** | −0.057 ** | 0.014 |

| (0.002) | (0.008) | (0.02) | (0.02) | (0.066) | (0.166) | (0.014) | (0.024) | (0.03) | |

| SIZE | −0.101 ** | −0.257 ** | 0.376 | 0.685 * | −1.643 * | 2.407 | −0.746 *** | 0.153 | −1.215 ** |

| (0.04) | (0.111) | (0.362) | (0.353) | (0.868) | (3.01) | (0.07) | (0.309) | (0.518) | |

| LDR | −0.001 | −0.006 * | −0.015 | −0.035 *** | −0.035 | −0.158 * | 0.011 *** | −0.007 | −0.056 *** |

| (0.001) | (0.003) | (0.011) | (0.008) | (0.023) | (0.09) | (0.002) | (0.009) | (0.015) | |

| LR | −0.004 *** | 0.006 | −0.062 *** | −0.019 | 0.049 | −0.518 *** | −0.005 * | 0.046 *** | −0.068 ** |

| (0.001) | (0.005) | (0.019) | (0.013) | (0.037) | (0.158) | (0.003) | (0.013) | (0.027) | |

| GDP | 0.021 *** | 0.025 | 0.084 * | 0.162 *** | 0.031 | 0.613 | −0.001 | −0.03 | 0.046 |

| (0.005) | (0.017) | (0.049) | (0.041) | (0.132) | (0.411) | (0.008) | (0.046) | (0.061) | |

| INF | 0.009 ** | −0.032 ** | −0.142 *** | 0.191 *** | −0.218 * | −0.967 *** | 0.044 *** | −0.024 | 0.03 |

| (0.004) | (0.016) | (0.038) | (0.035) | (0.125) | (0.313) | (0.007) | (0.046) | (0.055) | |

| IQ | 0.002 | 1.296 | −0.654 | 5.556 * | −0.652 | −5.054 | 0.827 ** | 13.402* | −9.667 |

| (0.358) | (1.074) | (4.368) | (3.149) | (8.396) | (36.339) | (0.305) | (3.081) | (5.806) | |

| Constant | 4.454 *** | 6.793 *** | 2.109 | 23.602 *** | 55.91 *** | 26.429 | 15.841 *** | −4.302 | 39.93 *** |

| (0.577) | (1.776) | (5.774) | (5.072) | (13.889) | (48.033) | (1.013) | (5.033) | (8.307) | |

| Obs. | 3314 | 219 | 77 | 3311 | 219 | 77 | 3550 | 231 | 84 |

| R-squared | 0.336 | 0.482 | 0.718 | 0.306 | 0.502 | 0.679 | 0.152 | 0.378 | 0.594 |

| F-statistic | 72.48 *** | 8.04 *** | 5.72 *** | 63.04 *** | 8.71 *** | 4.77 *** | 27.74 *** | 5.62 *** | 3.81 *** |

| Time fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Bank fixed | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Variables | ROA | |||

|---|---|---|---|---|

| I | II | III | IV | |

| FI | FIA | FIP | FIU | |

| FI | 0.47 *** | 0.216 ** | 0.31 ** | 0.373 *** |

| (0.126) | (0.091) | (0.158) | (0.111) | |

| COVID-19 | −0.501 *** | −0.41 *** | −0.368 *** | −0.466 *** |

| (0.079) | (0.069) | (0.096) | (0.071) | |

| FI × COVID-19 | 0.101 *** | |||

| (0.309) | ||||

| FIA × COVID-19 | 0.143 *** | |||

| (0.105) | ||||

| FIP × COVID-19 | 0.131 *** | |||

| (0.319) | ||||

| FIU × COVID-19 | 0.174 *** | |||

| (0.106) | ||||

| All control variables | yes | yes | yes | yes |

| Observations | 3615 | 3615 | 3615 | 3615 |

| R-squared | 0.33 | 0.327 | 0.326 | 0.33 |

| F-statistic | 73.08 *** | 72.26 *** | 71.88 *** | 73.12 *** |

| Time fixed effect | yes | yes | yes | yes |

| Bank fixed effect | yes | yes | yes | yes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zheng, C.; Rahman, M.A.; Hossain, S.; Moudud-Ul-Huq, S. Does Fintech-Driven Inclusive Finance Induce Bank Profitability? Empirical Evidence from Developing Countries. J. Risk Financial Manag. 2023, 16, 457. https://doi.org/10.3390/jrfm16100457

Zheng C, Rahman MA, Hossain S, Moudud-Ul-Huq S. Does Fintech-Driven Inclusive Finance Induce Bank Profitability? Empirical Evidence from Developing Countries. Journal of Risk and Financial Management. 2023; 16(10):457. https://doi.org/10.3390/jrfm16100457

Chicago/Turabian StyleZheng, Changjun, Md Ataur Rahman, Shahadat Hossain, and Syed Moudud-Ul-Huq. 2023. "Does Fintech-Driven Inclusive Finance Induce Bank Profitability? Empirical Evidence from Developing Countries" Journal of Risk and Financial Management 16, no. 10: 457. https://doi.org/10.3390/jrfm16100457