1. Introduction

Financial technology, or FinTech, has become a prominent disruptor in the financial services industry, reshaping the way individuals and businesses manage, access, and invest their money (

Asif et al. 2023). The rapid growth of FinTech adoption and usage has introduced innovative solutions that offer convenience, efficiency, and accessibility. One of the primary drivers of FinTech adoption is the unparalleled convenience it offers to users (

Bajunaied et al. 2023). Through mobile apps, online platforms, and digital wallets, individuals can now access a wide range of financial services from the comfort of their smartphones or computers. FinTech solutions often come with lower fees and costs compared with traditional financial institutions. Users can save on transaction fees, account maintenance charges, and trading commissions, making it an attractive option for cost-conscious individuals (

Shaikh et al. 2023). This cost advantage has been a significant driver of FinTech adoption, particularly among younger and more tech-savvy consumers (

Shen et al. 2019). The streamlined processes of FinTech applications have significantly reduced paperwork and administrative delays (

Arner et al. 2020).

FinTech leverages data analytics and artificial intelligence to offer personalized financial recommendations and solutions (

Senyo and Osabutey 2020). Users benefit from tailored investment portfolios, budgeting advice, and loan offers based on their unique financial profiles. Robo-advisors and digital investment platforms have democratized wealth management (

Vyas and Jain 2021). These automated solutions provide retail investors with access to diversified portfolios and low-cost investment strategies that were once reserved for high-net-worth individuals. The rise of robo-advisors has reshaped the asset management industry (

Fan et al. 2023). The ability to receive customized financial guidance has become a compelling factor for adopting FinTech services (

Aduba et al. 2023). FinTech has the potential to bring financial services to underserved populations worldwide (

Fan et al. 2023). Digital banking, payment solutions, and mobile money services are able to reach individuals who previously lacked access to traditional banking services (

Chauhan 2015). This inclusivity aspect of FinTech aligns with global efforts to promote financial inclusion and reduce economic disparities (

Carè et al. 2023).

But in this era of innovation, trust becomes paramount. How do we navigate this delicate balance between convenience and potential risks? This is a question that takes us into the realms of regulatory challenges, cybersecurity concerns, and the broader implications of trust in the FinTech sector. The rapid growth of FinTech has outpaced regulatory frameworks in many countries, leading to concerns about consumer protection, cybersecurity, and compliance with financial regulations (

Alrawad et al. 2023). Achieving the right balance between innovation and regulation is a complex challenge. FinTech platforms handle vast amounts of sensitive financial data, making them attractive targets for cyberattacks (

Bongomin and Ntayi 2020). Ensuring robust cybersecurity measures is essential to safeguard user information and maintain trust in FinTech services (

Jangir et al. 2022). This trust factor influences user behavior, adoption rates, and the long-term sustainability of the FinTech sector (

Bongomin and Ntayi 2020). Distrust stemming from platform outages or technical glitches can deter users from the adoption and usage of FinTech solutions. Ensuring platform reliability is essential for building and maintaining trust. Striking a balance between leveraging data for innovation and respecting user privacy rights is an ongoing challenge (

Alrawad et al. 2023). Therefore, trust plays a pivotal role in the adoption and usage of FinTech services. Furthermore, users’ confidence in the reliability, security, and ethical conduct of FinTech helps them engage in financial transactions and sensitive data.

However, more research efforts need to examine FinTech usage through the lenses of both technology and trust theories. Thus, there is a pressing requirement to gain insights into the factors preceding the use of FinTech by employing a comprehensive multi-theory approach. Because trust plays a vital role in influencing behavioral intention and FinTech use, it is essential to identify the antecedents to behavioral intention from both the UTAUT2 perspective and TTM. The UTAUT2 explains the antecedents to behavioral intention, whereas TTM provides the basis for trust as a precursor to behavioral intention. FinTech use largely depends on how consumers perceive the price value, effort expectancy, performance expectancy, and habit. To the best of our knowledge, despite the vast literature on Fin Tech use, only a small number of scientists understand the importance of the variables of UTAUT2 and TTM. This research aims to bridge this gap in literature.

This research makes three significant contributions to the burgeoning literature on FinTech. First, this research fills the gap in the literature by drawing upon insights from the unified theory of acceptance and use of technology (UTAUT2) and the trust theoretic model (TTM) to explore the factors that affect the intention to adopt FinTech services. Second, this research is the first of its kind to combine two theories to provide a holistic understanding of FinTech use by individuals. The UTAUT2 examines factors related to technology adoption, whereas the TTM concentrates on the trust aspects of human interaction with technology. Consequently, we amalgamate the UTAUT2 and TTM in this study because each offers distinct antecedents that contribute to our understanding. By combining these theories, we can obtain a strong perspective on what leads to the adoption and usage of FinTech. Third, this research is a significant step in enabling service providers and policymakers to determine the elements that affect FinTech adoption and use.

The remainder of the paper is organized as follows:

Section 2 covers the review of existing literature and the formulation of hypotheses.

Section 3 outlines the research methodology, including the development of measurements, the sample, and the procedure for data collection. In

Section 4, we present the data analysis, evaluate the measurement and structural model, and share the results of hypothesis testing. Following that, the

Section 5 presents the discussion, along with theoretical and practical implications, limitations, and future directions for the study and conclusions.

2. Literature Review and Hypothesis Development

2.1. Unified Theory of Acceptance and Use of Technology 2 (UTAUT2)

The UTAUT model is a prominent theoretical framework developed by

Venkatesh et al. (

2003) to understand and predict individuals’ technology adoption behavior. The UTAUT model integrates various prior technology acceptance models and incorporates multiple factors that influence an individual’s intention to use and actual use of technology. The original UTAUT model, proposed by

Venkatesh et al. (

2003), includes four main factors: performance expectancy, effort expectancy, social influence, and facilitating conditions. These factors were seen as critical in explaining technology adoption. UTAUT2, introduced by

Venkatesh et al. (

2012), builds upon the UTAUT model by adding several new constructs such as hedonic motivation, price value, and habit. These additional factors aim to provide a more comprehensive understanding of technology adoption. It has been widely adopted and extended in the fields of information systems, human–computer interaction, and technology adoption research (

Gansser and Reich 2021;

Kilani et al. 2023;

Martinez and McAndrews 2023). The UTAUT2 model posits that these factors influence users’ behavioral intentions, which, in turn, impact their actual use behavior. Additionally, the model suggests that moderators, such as age, gender, and experience, can influence the strength of these relationships. Researchers and practitioners often use the UTAUT2 model to assess and predict technology adoption in various contexts, including the adoption of financial technology (FinTech) services, mobile apps, and information systems (

Alalwan et al. 2017;

De Blanes Sebastián et al. 2023;

Ong et al. 2023). This research utilizes the UTAUT2 framework as one of its theoretical perspectives because it offers greater comprehensiveness and appropriateness for uncovering the factors that lead to the actual usage of FinTech services.

2.1.1. Performance Expectancy

Performance expectancy refers to the user’s perception of how well a particular technology or system will help them perform their tasks or achieve their goals (

Venkatesh et al. 2012). In other words, it assesses the extent to which users believe that using the technology will enhance their performance and make their tasks easier or more efficient (

De Blanes Sebastián et al. 2023;

Martinez and McAndrews 2023). When users believe that a technology will improve their performance or productivity, they are more likely to adopt and use it (

Bajunaied et al. 2023). Optimizing user experiences to meet performance expectations is essential for the widespread acceptance and utilization of digital financial services (

Basri et al. 2022). When individuals perceive that digital financial services simplify transactions, offer convenience, and improve their financial management, they are more inclined to use them (

Arner et al. 2020;

Nawayseh 2020;

Senyo and Osabutey 2020). The prior studies collectively emphasize the strong relationship between performance expectancy and technology adoption. Accordingly, we propose the following hypothesis:

H1. Performance expectancy has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.2. Effort Expectancy

Effort expectancy refers to the perceived ease or difficulty of using a particular technology or system (

Bajunaied et al. 2023;

Venkatesh et al. 2012). In simpler terms, it assesses how easy users believe it is to learn and operate the technology effectively. Effort expectancy is influenced by several factors, including user interfaces, user-friendliness, the complexity of tasks required to use the technology, and the perceived ease of interaction (

Gansser and Reich 2021;

Tamilmani et al. 2021).

Senyo and Osabutey (

2020) found that effort expectancy significantly influenced users’ behavioral intentions to adopt mobile money services. A study by

Liébana-Cabanillas et al. (

2020) on mobile banking adoption in Spain found that the perception of low effort requirements can motivate users to adopt FinTech services because they feel comfortable using these technologies to perform financial tasks. Users who found mobile payment apps easy to use were more inclined to adopt them for conducting financial transactions (

Basri et al. 2022;

Kilani et al. 2023;

Martinez and McAndrews 2023). These studies highlight the consistent relationship between effort expectancy and technology adoption. Hence, this study hypothesizes that:

H2. Effort expectancy has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.3. Social Influence

Social influence refers to the impact that social factors and the opinions of others have on an individual’s decision to adopt and use a technology (

Venkatesh et al. 2012). Social influence is particularly relevant when individuals perceive that influential people or groups in their social network have positive attitudes toward technology and encourage its use (

Kilani et al. 2023). A study by

De Blanes Sebastián et al. (

2023) on FinTech adoption in Spain found that peer recommendations and endorsements significantly influenced individuals’ decisions to adopt FinTech services. Recommendations, testimonials, and discussions on social platforms contributed to users’ perceptions of the usefulness and trustworthiness of mobile payment services (

Basri et al. 2022). Research by

Ong et al. (

2023) on behavioral intention to use digital payment systems among rural residents found that the involvement and support of family members played a vital role. In the context of FinTech, social influence not only shapes adoption but can also contribute to the development of trust and credibility for these services (

Kilani et al. 2023). Individuals are more likely to adopt FinTech if they believe their peers or close contacts have had positive experiences with it and support its use (

Alalwan et al. 2016;

Hsu and Lin 2016). Thus, the following hypothesis is developed:

H3. Social influence has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.4. Hedonic Motivation

Hedonic motivation represents the pleasure or enjoyment individuals derive from using technology (

Dzandu et al. 2022;

Venkatesh et al. 2012). It acknowledges that people are motivated to use technology not only for practical or utilitarian purposes but also for hedonistic reasons, such as entertainment, enjoyment, or social interaction (

George and Sunny 2020,

2022). It emphasizes that the perceived enjoyment and gratification associated with technology usage can play a significant role in shaping user behavior.

Yang et al. (

2023) discovered that the inclusion of gamified features, which enhance the hedonic aspect of using the app, positively influenced users’ adoption intentions. Users who found stock trading apps enjoyable and entertaining were more likely to adopt them, even when their primary goal was related to investment (

Lee et al. 2022;

Şenol and Onay 2023). These studies collectively highlight how the pleasure and enjoyment associated with technology usage, driven by hedonic motivation, can strongly influence individuals’ intentions to use technology services. Hence, the study proposes the following hypothesis:

H4. Hedonic motivation has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.5. Price Value

Price value can be described as the tradeoff between the perceived advantages of using FinTech applications and the financial expenses associated with their usage (

Aduba et al. 2023;

Asif et al. 2023;

Senyo and Osabutey 2020). A positive price value occurs when the perceived benefits of a technology outweigh the monetary costs, and such a positive price value significantly influences intention (

Venkatesh et al. 2012). In regard to customer FinTech readiness in Bangladesh,

Mahmud et al. (

2023), discovered that perceived cost savings, such as lower fees compared with traditional banking methods, positively influenced users’ intentions to adopt mobile banking. The cost-effectiveness of digital payment apps was a key driver of adoption among users, especially in regions with a focus on affordability (

Arner et al. 2020;

Carè et al. 2023). Lower fees and perceived cost savings played a role in the adoption of robo-advisory service decisions (

Back et al. 2023). Based on this discussion, we hypothesize that:

H5. Price value has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.6. Habit

Habit refers to ingrained, automatic behaviors that individuals repeatedly exhibit in response to specific cues or contexts (

Basri et al. 2022;

Venkatesh et al. 2012). When it comes to FinTech adoption, habits can either facilitate or hinder the process, depending on the individual’s prior financial behaviors and routines. Research by

Kilani et al. (

2023) on consumers after their adoption of e-wallets found that individuals who developed habits of using e-wallets tended to continue using them. Habitual use was linked to factors such as convenience, ease of access, and regular financial activities (

Senyo and Osabutey 2020). Habitual savings and investment practices can be cultivated through FinTech apps that promote automated savings or micro-investing (

George and Sunny 2020). These FinTech apps encourage users to make small contributions regularly, fostering saving and investment habits over time (

Lee et al. 2022). Once habits are formed, they contribute to the sustained usage of FinTech services, as individuals incorporate them into their daily routines (

George and Sunny 2022;

Venkatesh et al. 2012). On this basis, this study hypothesizes that:

H6. Habit has a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.7. Facilitating Conditions

Facilitating conditions represent the perceived resources, support, and infrastructure available to individuals for using a particular technology effectively (

Bajunaied et al. 2023;

Venkatesh et al. 2012). For individuals to engage with FinTech services, they must possess a mobile device, an active subscription with a carrier, and the proficiency to navigate their mobile devices effectively (

Alalwan et al. 2016;

Asif et al. 2023). Therefore, the presence of facilitating conditions has the potential to spark greater interest and subsequent adoption of FinTech services (

Aduba et al. 2023;

Arner et al. 2020).

Bajunaied et al. (

2023) found that access to technical support positively influenced users’ trust and usage of FinTech products. Training programs and digital literacy initiatives are essential facilitating conditions for FinTech adoption and usage (

Nawayseh 2020;

Ong et al. 2023). Based on the above literature, this study hypothesizes that:

H7. Facilitating conditions have a significant positive effect on users’ behavioral intention to use FinTech services.

2.1.8. Behavioral Intention

Behavioral intention refers to an individual’s willingness and intention to engage in a specific behavior, such as using FinTech services, while actual use reflects the tangible execution of that behavior (

Bajunaied et al. 2023;

Venkatesh et al. 2003,

2012). This relationship is grounded in the theory of planned behavior (

Ajzen 1991), which posits that behavioral intention strongly predicts actual behavior. Numerous studies have demonstrated the predictive power of behavioral intention in technology adoption. Research by

Venkatesh et al. (

2003) on the UTAUT found that behavioral intention significantly influenced the actual use of technology. Behavioral intention serves as a precursor to the actual use of FinTech services. Individuals who express a strong intention to use technology are more likely to follow through and use it in practice (

Ajzen 1991). Behavioral intention acts as a bridge between users’ attitudes, perceptions, and external influences and their actual engagement with FinTech services (

Chopdar et al. 2018). Based on the focus of the study and prior theoretical evidence we hypothesize that:

H14. Behavioral intention has a significant positive influence on users’ actual use of FinTech services.

2.2. Trust Theoretic Model (TTM)

The TTM for consumer adoption of M-payment systems was proposed and validated by

Chandra et al. (

2010). This model, built upon research in the fields of technology adoption and trust, not only postulates the significance of consumer trust in the adoption of M-payment solutions but also identifies key elements that foster trust in these systems. It delineates two main dimensions of trust catalysts: “mobile service provider characteristics” and “mobile technology environment characteristics” (

Chandra et al. 2010). They pinpointed two primary groups of mobile service provider traits that impact consumer trust: these are perceived reputation and perceived opportunism. Notably, the latter was found to have no significant impact. In terms of mobile technology features influencing consumer trust, the key factors identified revolve around perceived risk and perceived regulatory support (

Chandra et al. 2010). Moreover, numerous studies have found that service quality is a crucial factor in creating trust among consumers (

Chauhan 2015;

George and Kumar 2014;

George 2018;

George and Sunny 2022;

Liébana-Cabanillas et al. 2020;

Verma 2023;

Wang et al. 2019).

Service quality encompasses various aspects such as reliability, responsiveness, security, and customer support provided by FinTech platforms. When users perceive high service quality, it fosters trust in the technology, which, in turn, positively impacts adoption and continued usage (

Bongomin and Ntayi 2019). As a result, the TTM is extended to include the service quality element.

2.2.1. Perceived Risk

Perceived risk refers to individuals’ subjective assessments of the potential negative consequences, uncertainties, or vulnerabilities associated with adopting and using a particular technology, product, or service (

Alrawad et al. 2023;

Chandra et al. 2010). Security concerns, particularly related to data breaches, fraud, and privacy, are prominent factors in perceived risk (

Jangir et al. 2022). When individuals perceive that using FinTech services carries a high degree of risk, they may be hesitant to embrace these technologies (

Senyo and Osabutey 2020). The potential benefits outweigh the risks, and they may be more inclined to adopt FinTech services (

Ali et al. 2021). Conversely, high perceived risk can erode trust and deter adoption (

Laksamana et al. 2022). To encourage greater adoption and sustained usage, FinTech providers must prioritize building trust through robust security measures, transparent communication, and compliance with regulations (

Jangir et al. 2022). Thus, this study proposes the following hypothesis.

H8. Perceived risk has a significant negative effect on users’ trust in FinTech services.

2.2.2. Perceived Reputation

Perceived reputation refers to the perceptions and beliefs individuals hold about the reputation or standing of a particular technology, product, or service (

Chandra et al. 2010). It encompasses how users or potential adopters perceive the credibility, reliability, and trustworthiness of the technology and the organization or provider behind it (

Xi and Chen 2021). Research by

Nguyen et al. (

2022) on FinTech services found that users were more likely to adopt FinTech products when they perceived the service provider as reputable and trustworthy. Users often rely on the experiences and opinions of their peers to gauge the credibility and reputation of FinTech providers (

Wang 2023). A strong perceived reputation contributes to users’ confidence in the safety and security of their financial transactions (

Lin et al. 2022). A technology with a positive perceived reputation is more likely to gain user trust and attract adoption (

Chandra et al. 2010;

Schaarschmidt 2016). Hence, we form the following hypothesis.

H9. Perceived reputation has a significant positive effect on users’ trust in FinTech services.

2.2.3. Service Quality

Service quality in the context of technology adoption refers to the perceived excellence, reliability, and overall satisfaction with the services provided by a technology or a technology provider (

Wang et al. 2019). Research by

George (

2018) on internet banking adoption found that perceived service quality positively influenced users’ trust in internet banking services. The reliability of FinTech services, including factors such as uptime, transaction accuracy, and consistent performance, significantly impacts trust (

Liébana-Cabanillas et al. 2020). Users who experience reliable and error-free services are more likely to trust the provider (

Verma 2023). High service quality, characterized by reliability, security, positive user experience, and effective problem resolution, can build trust in FinTech providers (

George and Sunny 2022). Ensuring consistently high service quality is essential for FinTech providers to foster trust and encourage adoption in the highly competitive FinTech industry (

Chauhan 2015;

George and Kumar 2014). Based on the above discussion, the study proposes the following hypothesis.

H10. Service quality has a significant positive influence on users’ trust in FinTech services.

2.2.4. Perceived Regulatory Support

Perceived regulatory support refers to individuals’ perceptions and beliefs regarding the level of support, guidance, and regulation provided by government authorities, regulatory bodies, or relevant institutions for the technology or innovation (

Chandra et al. 2010;

Vyas and Jain 2021). Research by

Bongomin and Ntayi (

2020) on FinTech adoption found that users who perceive that there is a strong regulatory framework in place are more likely to trust FinTech services. A robust regulatory environment can provide users with a sense of security and confidence in the industry (

Nawayseh 2020;

Yue et al. 2022). Users’ trust in the safety and reliability of services can be elevated when they believe providers adhere to, and comply with, financial regulations (

König et al. 2023). When regulations are stable and consistent, users are more likely to trust the industry, as they anticipate a lower risk of regulatory changes impacting their use of FinTech services (

Yu et al. 2023). Individuals are more likely to accept and use FinTech services when they believe that regulations are in place to protect their interests, such as those associated with data privacy and financial security (

Xi and Chen 2021;

Shaikh et al. 2023). Therefore, the following hypothesis is proposed:

H11. Perceived regulatory support has a significant positive effect on users’ trust in FinTech services.

2.2.5. Trust

Trust refers to the confidence and belief that users have in the reliability, security, and integrity of FinTech platforms and providers (

Alalwan et al. 2016;

Chandra et al. 2010). Users who trust FinTech providers are more likely to express an intention to use their services. Research by

Bongomin and Ntayi (

2019) on mobile money adoption identified trust as a key predictor of the actual use of FinTech services. Users who trust that their financial data will be protected and their privacy respected are more inclined to express an intention to use FinTech platforms (

Chauhan 2015;

Bongomin and Ntayi 2020). Clear and transparent communication by FinTech providers about security practices, data handling, and privacy policies can foster trust and increase the use of FinTech services (

Bajunaied et al. 2023;

Kilani et al. 2023). Users often rely on peer experiences to evaluate trustworthiness. Positive user reviews, ratings, and recommendations can significantly influence trust and, consequently, users’ intentions to adopt and use FinTech services (

Laksamana et al. 2022;

Zarifis and Cheng 2022). Establishing and maintaining trust is crucial for FinTech providers looking to encourage adoption and long-term usage among their user base (

Basri et al. 2022). On this basis, this study proposes the following hypotheses:

H12. Trust has a significant positive effect on users’ behavioral intention to use FinTech services.

H13. Trust has significant positive influences on the actual use of FinTech services.

The conceptual model is presented in

Figure 1.

3. Research Methodology

3.1. Measures

This study used items that had been validated and verified in prior research to identify the factors influencing consumers’ intention to use FinTech services. Items assessing factors like performance and effort expectancy, social influence, price, habit, facilitating conditions, hedonic motivation, behavioral intention, and FinTech use were adapted from

Venkatesh et al. (

2012). Trust in Fintech was measured by items adapted from

Alalwan et al. (

2017), and

Gefen et al. (

2003). Additionally, items measuring perceived reputation, perceived risk, and perceived regulatory support were taken from

Chandra et al. (

2010), while those items related to service quality were adapted from

Zhou (

2013). Each measurement item was measured using a five-point Likert scale, ranging from “strongly disagree” (1) to “strongly agree” (5).

The research questionnaire comprised two sections: the first focused on gathering demographic information, and the second aimed to capture respondents’ perceptions of each variable in our model. The questionnaire was initially crafted and underwent a review and validation process by three academic experts, as well as one expert from the FinTech industry. The experts evaluated the clarity and understandability of each survey item. Specific attention was given to the language used, potential ambiguity, and the appropriateness of the terminology within the context of the target audience. Experts also examined the potential for response bias and sensitivity in the survey questions. Adjustments were made to minimize the likelihood of leading or biased questions, promoting more accurate and unbiased responses from participants. The FinTech industry expert provided feedback on the survey’s alignment with current industry practices. This ensured that the research instrument remained relevant and applicable to real-world scenarios, enhancing the external validity of the study. Before sharing the questionnaire with the intended participants, we conducted a pilot study involving 25 individuals to confirm the suitability of the measurement tool for this study. Following this pilot test, we made adjustments to multiple items and refined some of them based on the initial validity assessment within the pilot sample. One notable modification involved rephrasing certain survey questions that were deemed unclear or prone to misinterpretation by participants. This adjustment aimed to improve the overall comprehension of the survey items and minimize the likelihood of response errors. Additionally, adjustments were made to the survey’s structure, such as the ordering of questions, to optimize the flow and coherence of the instrument.

3.2. Sample and Data Collection

A structured questionnaire was created using Google Forms and shared with FinTech users. Due to the absence of a predefined sampling framework for FinTech users, we opted for the convenience sampling method, a practice recommended in prior studies (

Alrawad et al. 2023;

Bajunaied et al. 2023;

Senyo and Osabutey 2020). Convenience sampling has the potential to introduce bias into the sample composition as participants are not systematically selected from the entire population of interest. To address this concern, a concerted effort was made to collect comprehensive demographic information from participants, enabling a thorough characterization of the sample. This information was then utilized to assess the diversity of the sample and identify any potential biases in participant characteristics. Through this strategy, it was confirmed that there was no bias in the sample selection. Data collection spanned three months from June 2023 to August 2023. We disseminated the survey link via email, WhatsApp, and various social media channels, encouraging the initial respondents to share it widely to obtain a sizable sample. Each dissemination channel was selected based on its potential to reach a large and varied audience within this demographic. The survey link was distributed through email primarily to leverage its direct and personalized communication capabilities. WhatsApp and Facebook were chosen as distribution channels due to their ubiquity, especially among smartphone users in various demographic segments. Personal and professional WhatsApp groups related to FinTech, finance, and technology were identified and were utilized to share the survey link. We received a total of 404 responses. Among these responses, we identified 5 with suspicious response patterns (

Bauermeister et al. 2012). Responses containing inconsistent or contradictory answers to logically related questions were flagged. Straight-lining, wherein respondents consistently chose the same response option without variation or displayed a monotonous pattern in responses, was deemed indicative of inattentiveness or careless answering. Consequently, responses that could not be satisfactorily validated or clarified were excluded from the final dataset used for analysis. Therefore, the final statistical analysis was carried out using the 399 valid responses. To achieve the objectives of this study, the researcher determined the sample size using G*Power software (version 3.1). As mentioned earlier, the model in this study comprises thirteen predictors. The software recommended an effect size of 0.15 and a power level of 0.95. Consequently, it proposed a sample size of 189. Therefore, the chosen sample size for this study exceeded the minimum criteria. Descriptive statistics can be found in

Table 1.

Table 1 illustrates the demographic characteristics of the respondents. Concerning age distribution, a substantial majority of participants (41.8%) belonged to the 25–35 age group, with the next significant portion falling within the 15–25 age range (27%). These findings underscore the predominant representation of young adults in the sample. In terms of gender, the results indicate a male majority (58.9%) compared with females (41.1%). Additionally, the data reveal that a significant proportion of respondents reside in urban areas (56.6%). Furthermore, most participants reported having over five years of FinTech usage experience (58.2%), followed by those with 2–5 years of experience (26.3%).

4. Data Analysis and Results

The data analysis process consisted of two stages: measurement model analysis, and structural model analysis. A partial least squares structural equation model (PLS-SEM) was used for the measurement and structural model analysis. Specifically, SmartPLS version 4.0 was employed for data analysis, chosen due to the exploratory nature of the research. PLS-SEM was selected for its ability to effectively address issues related to sample size and the distribution of data, especially when examining complex structural models (

Hair et al. 2019).

4.1. Assessment of Measurement Model

The measurement model serves as a critical foundation for structural equation modeling by ensuring that the instruments are valid and reliable and effectively measure the latent constructs of interest (

Hair et al. 2021). To assess the reliability and internal consistency of each construct, we examined Cronbach’s alpha and composite reliability scores. Generally, reliability, as evaluated through Cronbach’s alpha coefficient and composite reliability, is considered satisfactory when it exceeds the threshold of 0.70, consistent with the guidelines provided by

Henseler et al. (

2016). In this study, the Cronbach’s alpha coefficients and composite reliability values, as shown in

Table 2, range from 0.786 to 0.943. These values confirm the existence of reliability and internal consistency among the constructs of the research model.

According to

Hair et al. (

2021), to establish convergent validity, the AVE value for a construct should exceed the threshold of 0.50. As illustrated in

Table 2, all constructs in the model exhibit AVE values surpassing 0.50, signifying strong convergent validity. To establish discriminant validity, it is typically required for HTMT values to remain below the threshold of 0.85 (

Henseler et al. 2016). In the present study, the HTMT values, as displayed in

Table 3, fall within the range of 0.027 to 0.837, affirming the presence of discriminant validity among the constructs within the research model. Furthermore, we employed variance inflation factors (VIFs) to evaluate the extent of multicollinearity. The VIF values fall within the range of 1.552 to 2.991, which is lower than the recommended threshold of 3.3 (

Kock 2015). Hence, there are no significant issues related to multicollinearity in our dataset.

The sources of measures and the indicators of the measures were mentioned in

Appendix A.

4.2. Assessment of Structural Model

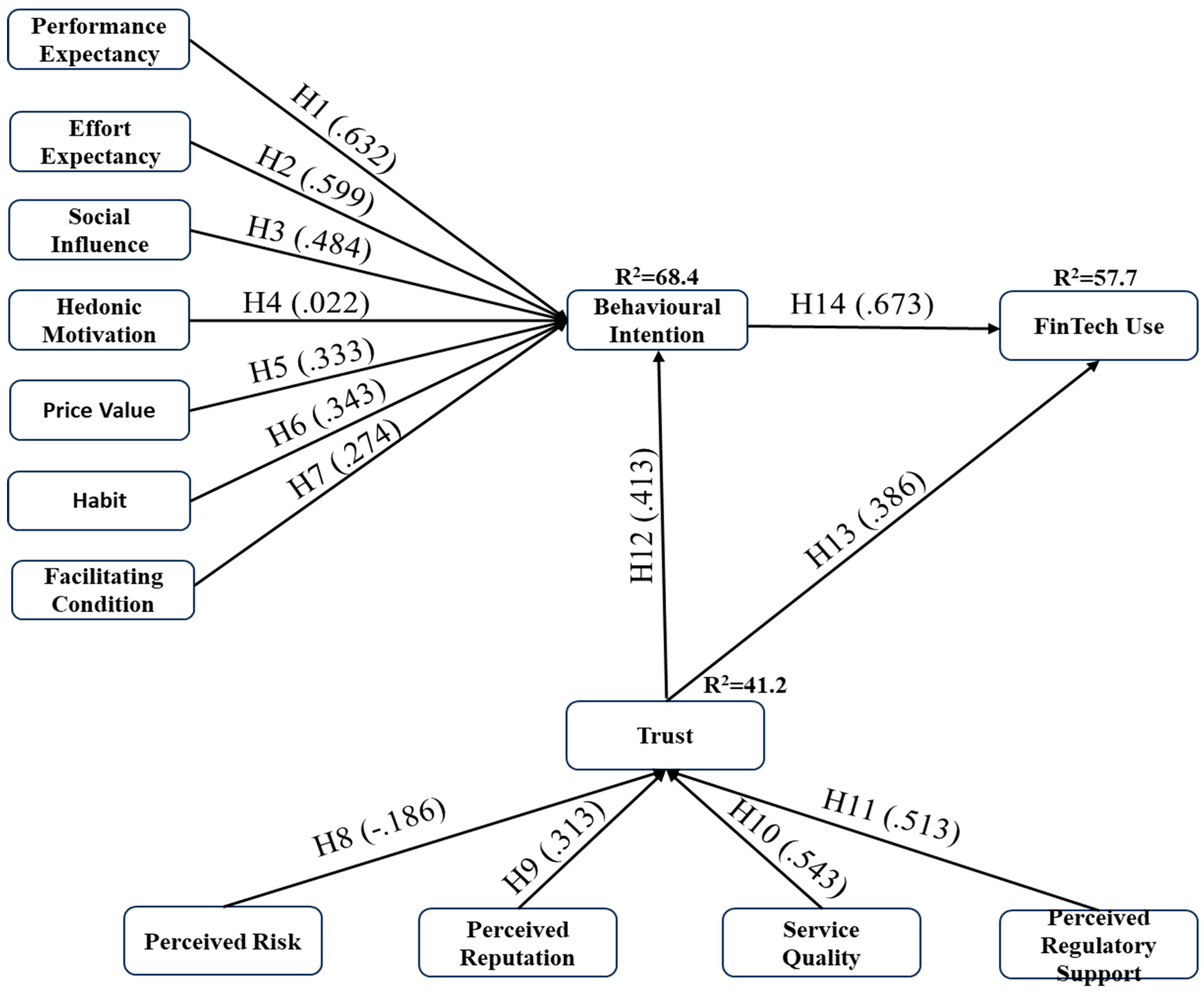

After confirming the validity of the measurement model, we proceeded to examine the hypotheses we proposed. We determined the significance of the path coefficients using a bootstrapping technique with 5000 samples. The results of the direct associations between the constructs are presented in

Table 4. The results indicate that there is a significant positive effect of performance expectancy (β = 0.632;

p < 0.001), effort expectancy (β = 0.599;

p < 0.001), social influence (β = 0.484;

p < 0.05), price value (β = 0.333;

p < 0.1), habits (β = 0.343;

p < 0.001), and facilitating conditions (β = 0.274;

p < 0.001), on behavioral intention to use FinTech services, thus supporting H1, H2, H3, H4, H6, and H7. Regarding the relation between perceived risk and trust in FinTech services, the analysis reveals a significant negative influence of perceived risk on trust (β = −0.186;

p < 0.001), thereby confirming H8. Similarly, the result shows that perceived reputation (β = 0.313;

p < 0.001), service quality (β = 0.543;

p < 0.001), and perceived regulatory support (β = 0.513;

p < 0.001) have a positive significant effect on trust in FinTech services. Therefore, H9, H10 and H11 were supported. However, the results also highlight the significant influence of trust on the behavioral intention to use FinTech services (β = 0.413;

p < 0.01) and actual use of FinTech services (β = 0.386;

p < 0.01), thereby accepting H12 and H13. Regarding the relation between behavioral intention and actual use of FinTech services, the results reveal that behavioral intention has a significant positive effect on the actual use of FinTech services (β = 0.673;

p < 0.001), thus supporting H14. On the contrary, hypotheses not confirmed by the model include the relationships between hedonic motivation (β = 0.022;

p > 0.1), and behavioral intention to use FinTech services, thereby rejecting H4.

R-square values provide insights into the model’s goodness of fit and the proportion of variance explained by the endogenous variables in the model. Based on the values of the R

2, the model explained 68.4% of the variance in behavioral intention to use FinTech services and 57.7% of the variance in actual use of FinTech services. Similarly, perceived reputation, perceived risk, perceived regulatory support, and service quality together explained 41.2% of the variance in trust in FinTech services. Moreover, to validate the predictive relevance of the model we put forward, we computed Stone–Geisser test criterion (Q

2) values for the dependent variables. The results indicate that the values of behavioral intention (Q

2 = 0.17), trust in FinTech services (Q

2 = 0.22), and FinTech use (Q

2 = 0.14) were more than zero (Q

2 > 0), thus confirming the model’s predictive accuracy (

Hair et al. 2021).

The results of structural model were presented in

Figure 2.

5. Discussion

In this study, we investigated the factors influencing the customers’ intention to use FinTech services, especially the role of trust in the use of FinTech services. The motivation behind this study arises from a lack of comprehensive knowledge and inconclusive findings in existing research regarding the determinants of FinTech service use. Recognizing FinTech as a pivotal innovation for enhancing financial inclusion, particularly in developing nations, it becomes imperative to comprehend the factors influencing its adoption and usage. To bridge these knowledge gaps, this study integrated elements from two theories, specifically UTAUT2 and the TTM.

The findings indicate that performance expectations have a substantial impact on the intention to use FinTech services (H1), which aligns with prior research (

Bajunaied et al. 2023;

Basri et al. 2022;

Martinez and McAndrews 2023;

Venkatesh et al. 2012). This confirmation indicates that performance expectancy positively influences behavioral intention to adopt FinTech because users anticipate and experience real advantages in terms of convenience, efficiency, and cost-effectiveness when managing their finances through these technological solutions. The results indicate that effort expectancy positively affects the intention to use FinTech services (H2), aligning with previous research (

Kilani et al. 2023;

Tamilmani et al. 2021). This suggests that users are more inclined to adopt and regularly use FinTech platforms when they perceive that these services require minimal effort and are user-friendly. This study confirms previous research (

Alalwan et al. 2016;

Hsu and Lin 2016;

Ong et al. 2023) that reports that social influence has a significant and positive impact on the intention to use FinTech services (H3). This research did not support the positive effect of hedonic motivation on behavioral intention (H4), which is contradictory to the findings from the previous studies. Though hedonic motivation has a significant influence on behavioral intention with regard to the consumption of products, it does not have any impact on the intention to use FinTech services. However, the relationship between hedonic motivation and behavioral intention to use FinTech is positive, though not significant (H4). These findings underscore the idea that peer influence and social networks are key factors driving user adoption of FinTech platforms, highlighting the importance of positive feedback, recommendations, and endorsements from their peers. Furthermore, price value has a significant positive effect on behavioral intention to use FinTech (H5). These findings suggest that users are more likely to intend to use FinTech when they see value for money, affordability, and clear benefits in the services offered. This study confirms previous research (

Basri et al. 2022;

Lee et al. 2022;

Venkatesh et al. 2012) that reports that habit significantly influences behavioral intention to use FinTech services (H6). This indicates that people tend to develop routines around the convenience and accessibility of FinTech platforms, making them a natural choice for financial tasks. It was also found in the results that facilitating conditions had a positive relationship with behavioral intention to use FinTech (H7). This implies that when users have access to the required infrastructure, support, and resources that facilitate the use of FinTech, they are more likely to adopt financial technology services.

The results of this study confirm the observations of previous studies (

Chandra et al. 2010;

Lin et al. 2022;

Xi and Chen 2021) that perceived that reputation significantly influences trust in FinTech services (H9). This finding supports the assumption that users trust and use FinTech platforms with strong reputations because they are perceived to be reliable, secure, and credible. Furthermore, these outcomes show that perceived regulatory support has a significant positive effect on trust in FinTech services (H11). These results demonstrate that users are more likely to trust and use FinTech services when they believe the platform complies with financial regulations, prioritizes consumer protection, ensures data security, promotes transparency, and provides dispute resolution mechanisms. Similarly, the results imply that service quality has a positive impact on trust in FinTech services (H10). This suggests that high service quality contributes to a positive user experience and fosters trust in FinTech services. Interestingly, the findings indicate that perceived risk exerts a negative influence on trust in FinTech services. These outcomes imply that perceived risk can encompass concerns related to data security, privacy, financial stability, or the reliability of the FinTech provider. Users might express reservations about the safety and confidentiality of their financial transactions and sensitive information when using FinTech services. Concerns regarding potential data breaches, unauthorized access to personal information, or the misuse of financial data could contribute to a diminished level of trust. When users have reservations about these aspects, they are less likely to trust the platform with their financial transactions and sensitive information.

Another insight derived from the findings is that trust significantly influences behavioral intention to use FinTech services (H12) and actual use of FinTech services (H13). This outcome suggests that users who trust the platform believe that their financial transactions and data will be handled safely, and that the provider will act in their best interests. This trust positively influences their intention to use the service because they perceive it as dependable and worthy of their confidence. This finding aligns with the idea proposed by

Bongomin and Ntayi (

2019), that the higher the level of trust, the more inclined users are to express an intention to use these services. In this way, they are more likely to turn their intentions into action, and actively use financial technology services. Consistent with various research findings (

Bajunaied et al. 2023;

Chandra et al. 2010;

Venkatesh et al. 2012), this study reaffirms the favorable impact of behavioral intention on the actual use of FinTech services. This outcome underscores the commonly accepted notion that when individuals have a strong intention to use FinTech services, they are more likely to translate that intention into action by using these services. In the list of factors influencing the utilization of FinTech services, behavioral intention holds the highest significance, followed by performance expectancy, effort expectancy, social influence, habit, price value, and facilitating conditions in that order.

In contrast, the findings indicate that hedonic motivation (H4) does not impact the intention to use FinTech services. This outcome contradicts certain earlier research (

Lee et al. 2022;

Şenol and Onay 2023) but aligns with

Oliveira et al. (

2016), who also explored technology adoption. Unlike some other technological innovations that might be inherently enjoyable or entertaining, FinTech services primarily serve practical and utilitarian purposes in managing financial tasks. Individuals may perceive these services more as tools for efficiency and convenience rather than as sources of hedonic pleasure. Therefore, it can be deduced that individuals do not perceive the use of financial technology innovations as an enjoyable activity; instead, they view it as a serious and practical endeavor.

6. Theoretical Implications

This study’s integration of both the UTAUT2 and the TTM contributes to the theoretical understanding of FinTech adoption. By combining elements from these two theories, the study offers a more comprehensive framework for exploring the factors influencing the intention to use FinTech services. This approach showcases the value of drawing from multiple theories to gain a holistic perspective on technology adoption. The study’s findings provide clarity on the specific factors that significantly influence the intention to use FinTech services. It identifies the relative importance of these factors, such as performance expectancy, effort expectancy, social influence, habit, and trust. This clarity can guide future research in refining existing theories and models related to technology adoption and trust. The study’s result that hedonic motivation does not influence the intention to use FinTech services contradicts some prior research findings. This inconsistency highlights the need for a deeper exploration of users’ motivations and perceptions regarding FinTech. Future research could delve into the reasons why users do not find FinTech services inherently enjoyable and whether this perception varies across different user segments. The study underscores the central role of trust in the adoption and usage of FinTech services. Trust is identified as a significant factor that influences both intention and actual use. This finding emphasizes the importance of trust-building mechanisms for FinTech providers and suggests that trust-related constructs should be integrated into technology adoption models. Moreover, the theoretical contribution of this research lies in the fact that, while trust has garnered considerable interest from both researchers and practitioners, the majority of the existing literature has neglected to study the multidimensional nature of trust when examining the implicit decision-making involved in the adoption and continuous usage of new technologies and innovations. Hence, this study explores customers’ intentions by assessing four dimensions of trust: perceived reputation, perceived risk, service quality, and perceived regulatory support. Moreover, this study serves as a motivation for other researchers to conduct comprehensive analyses of how consumers develop their trust beliefs.

7. Practical Implications

The findings from this study have several implications for the policymakers, practitioners, and researchers in the FinTech industry. Further, this study on the antecedents determining the intention to use FinTech services has real-world implications for financial institutions, FinTech firms, and various industry stakeholders. The study indicates that performance expectancy and effort expectancy are the most significant factors affecting the use of FinTech among consumers. Thus, FinTech companies should continue to focus on making their services convenient and easily accessible to users. User-friendly interfaces, clear communication of benefits, and positive feedback mechanisms can encourage more individuals to adopt these services. Given the significant role of trust in FinTech adoption, service providers should prioritize building and maintaining trust. The study revealed that the perceived risks associated with technology usage have a significant negative influence on the trust in FinTech services. A comprehensive analysis of the different threats that users perceive when using technology, along with effective mitigation strategies implemented by service providers, can enhance the seamless adoption and sustained usage of the technology. This includes robust data security measures, compliance with regulations, transparent practices, and effective customer support. Establishing a strong reputation and demonstrating commitment to user protection can attract and retain users. Adhering to financial regulations and consumer protection measures is not only a legal requirement but also a trust-building factor. Ensuring that the necessary infrastructure and conditions are in place to support FinTech adoption is crucial. This could involve improving internet connectivity, digital literacy programs, and access to smartphones or computers, especially in underserved areas. Continuously monitoring and improving service quality can lead to a positive user experience and, subsequently, trust in the platform.

8. Limitations and Scope for Further Study

The study provides valuable insights but also has limitations. One notable limitation lies in the sampling method employed, which relies on convenience sampling. Because participants are selected based on their availability and willingness to participate, the sample may not be representative of the broader population. The study’s findings may be influenced by the geographic region in which it was conducted. FinTech adoption and usage can vary significantly between countries and regions, so the results may not be universally applicable. The study’s data were collected at a single point in time, providing a snapshot of user perceptions and behaviors. Longitudinal data could offer insights into how these factors evolve over time. The study relies on self-reported data from survey respondents, which may introduce response bias and social desirability bias. Observational or behavioral data could provide a more objective perspective.

To expand the knowledge in this domain, future research can explore similar studies in different cultural contexts that could shed light on how cultural factors influence FinTech adoption. Cultural nuances may play a significant role in shaping trust and usage patterns. Additionally, qualitative research methods, such as in-depth interviews and focus groups, could provide a deeper understanding of the nuances of trust and usage motivations among FinTech users. This study focuses on certain trust factors such as reputation, regulatory support, service quality, and perceived risk. Future research could explore additional dimensions of trust that may impact FinTech use.

9. Conclusions

This research aimed to explore the factors that influence the real-world usage of FinTech services. To achieve this, it integrated two distinct theories, UTAUT2 and TTM, to create and scrutinize a unique research model. The findings demonstrate that the research model possesses substantial explanatory capability, confirming its effectiveness in predicting both behavioral intention and the actual utilization of FinTech services. This study sheds light on the intricate landscape of FinTech adoption and usage by employing a comprehensive multi-theory approach. The findings reveal a multitude of factors that influence the adoption of FinTech services, contributing to a deeper understanding of this evolving phenomenon. Performance expectancy emerged as a significant driver of FinTech adoption, highlighting the importance of the perception of users that they receive tangible benefits and ease of use in these services. Effort expectancy also played a pivotal role, emphasizing the significance of user-friendly and low-effort interactions with FinTech platforms. Social influence was found to be a substantial motivator, indicating that positive feedback and recommendations from peers encourage individuals to explore and embrace FinTech solutions. Habit, developed around the convenience and accessibility of FinTech, was another influential factor promoting the use of FinTech. Price value and facilitating conditions were shown to positively affect the behavioral intention to use FinTech services, underlining the importance of perceived affordability and an enabling environment.

On the trust side, several factors were identified as key determinants of users’ trust in FinTech services. These included perceived reputation, regulatory support, service quality, and the absence of perceived risk. These aspects collectively contribute to building and maintaining trust, a pivotal factor influencing both behavioral intention and actual usage. Overall, this research underscores the complex interplay of technological and trust-related factors in shaping FinTech adoption and usage. It provides valuable insights for service providers and policymakers, highlighting the need for user-centric design, robust cybersecurity measures, and adherence to regulatory standards. By addressing these factors, stakeholders can foster trust, enhance user experience, and promote the continued growth of the FinTech sector. As FinTech continues to reshape the financial landscape, this study contributes to a holistic understanding of the dynamics driving its adoption and usage.

Author Contributions

Conceptualization, M.B.A., M.S. and M.R.; methodology, M.R., M.S. and S.S.; software, M.S. and S.S.; validation, M.B.A., M.S. and S.P.; data curation, M.S., M.R. and S.S.; writing—original draft preparation, M.B.A., M.S. and S.S.; writing—review and editing, M.S., S.S. and S.P.; visualization, M.S., M.R. and S.S.; supervision, M.S. and M.R.; project administration, M.S., M.R. and S.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The data are available from the corresponding author upon request.

Acknowledgments

The authors would like to especially thank the anonymous reviewers for their helpful comments in the earlier version of the manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

| Constructs | Items | Questions | Sources |

| Effort expectancy | EE1 | I expect that I can quickly learn how to use FinTech apps and platforms. | Venkatesh et al. (2012) |

| EE2 | I believe that FinTech platforms are user-friendly and intuitive. |

| EE3 | I believe that using FinTech services will not require a significant amount of time to get things done. |

| EE4 | I expect that I will not need extensive training or assistance to use FinTech apps effectively. |

| Performance expectancy | PE1 | Using FinTech services will make my financial tasks easier and more efficient. | Venkatesh et al. (2012) |

| PE2 | I anticipate that FinTech services will help me save time and effort when managing my finances |

| PE3 | I expect that FinTech solutions will offer a higher level of convenience compared to traditional financial methods |

| PE4 | I anticipate that FinTech apps will help me achieve my financial goals more effectively |

| Social influence | SI1 | People who matter to me believe that I should use FinTech services. | Venkatesh et al. (2012) |

| SI2 | People who have an impact on my behaviour believe that I should use FinTech services. |

| SI3 | People whose opinions I value prefer that I use FinTech services |

| SI4 | The positive feedback and reviews from other users motivate me to use the FinTech platform. |

| Facilitating conditions | FC1 | I have access to the required technology (e.g., internet, smartphone) for using FinTech services. | Venkatesh et al. (2012) |

| FC2 | I have the knowledge necessary to use FinTech services |

| FC3 | There is sufficient customer support and assistance available when I encounter issues with FinTech services |

| FC4 | The availability of reliable internet connectivity facilitates my use of FinTech services |

| Hedonic motivation | HM1 | I use FinTech services because I find them enjoyable and fun | Venkatesh et al. (2012) |

| HM2 | I enjoy exploring the innovative features and functionalities of FinTech services |

| HM3 | I am motivated to use FinTech services because they provide a sense of adventure in managing my finances |

| HM4 | I find satisfaction in customizing my financial experience when using FinTech platforms |

| Price value | PV1 | I expect that the benefits I receive from FinTech services will outweigh the fees or charges associated with them. | Venkatesh et al. (2012) |

| PV2 | I believe that using FinTech platforms is a cost-effective way to manage my finances |

| PV3 | I perceive that the pricing of FinTech services is competitive compared with traditional financial options. |

| PV4 | I believe that the pricing of FinTech services is reasonable considering the value they offer. |

| Habit | HA1 | I have developed a routine of using FinTech services for various financial tasks | Venkatesh et al. (2012) |

| HA2 | The thought of using FinTech solutions occurs to me automatically when I have financial tasks to complete. |

| HA3 | I use FinTech tools without actively considering alternative methods |

| HA4 | I find it hard to break away from the habit of using FinTech services. |

| Behavioural intention | BI1 | I intend to use FinTech services | Venkatesh et al. (2012) |

| BI2 | I intend to continue using FinTech services for my financial needs in the future. |

| BI3 | I plan to increase my usage of FinTech services for a wider range of financial tasks. |

| BI4 | I am motivated to explore and adopt new FinTech solutions as they become available. |

| FinTech use | FU1 | I regularly use FinTech payment options (e.g., mobile wallets, online transfers) for making purchases. | Venkatesh et al. (2012) |

| FU2 | I utilize FinTech investment platforms (e.g., robo-advisors, online trading) to manage my investments |

| FU3 | I use digital FinTech services (e.g., peer-to-peer lending, online loans) when in need of financial assistance |

| FU4 | I am an active user of FinTech insurance services for purchasing and managing insurance policies |

| Trust | TR1 | I trust that the FinTech platform will securely handle my financial information. | Alalwan et al. (2017) and Gefen et al. (2003) |

| TR2 | I believe that the FinTech platform will protect my personal data from unauthorized access. |

| TR3 | I have confidence in the security measures implemented by the FinTech platform to prevent fraud or identity theft. |

| TR4 | I trust that the FinTech platform will handle financial transactions accurately and reliably. |

| Perceived reputation | PR1 | I consider the reputation of a FinTech company when deciding whether to use their services. | Chandra et al. (2010) |

| PR2 | The reputation of a FinTech platform influences my confidence in its ability to protect my financial information |

| PR3 | I perceive the reputation of the FinTech companies as a reliable indicator of their quality and trustworthiness |

| PR4 | I trust that the FinTech companies I use will resolve any issues or disputes in a manner consistent with their reputation. |

| Perceived risk | PK1 | I worry that I might make a financial mistake or error when using FinTech platforms. | Chandra et al. (2010) |

| PK2 | I perceive a risk of unauthorized access to my financial accounts or transactions when using FinTech apps. |

| PK3 | I am concerned about the potential for technical glitches or system failures with FinTech services. |

| PK4 | I perceive a risk of fraud or scams when conducting financial transactions through FinTech apps. |

| Service quality | SQ1 | The FinTech platform consistently provide high-quality services. | Zhou (2013) |

| SQ2 | The FinTech platform responds promptly to inquiries and requests for assistance |

| SQ3 | The customer support provided by the FinTech platform is helpful and knowledgeable |

| SQ4 | The FinTech platform delivers services accurately and without errors |

| Perceived regulatory support | PRS1 | Government initiatives and policies positively influence my decision to use FinTech services. | Chandra et al. (2010) |

| PRS2 | I am more inclined to use FinTech services due to government campaigns promoting their benefits |

| PRS3 | Government support makes me feel more secure and confident in using FinTech services |

| PRS4 | Government support contributes to the accessibility and affordability of FinTech services |

References

- Aduba, Joseph, Jr., Behrooz Asgari, and Hiroshi Izawa. 2023. Does FinTech penetration drive financial development? Evidence from panel analysis of emerging and developing economies. Borsa Istanbul Review 23: 1078–97. [Google Scholar] [CrossRef]

- Ajzen, Icek. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Alalwan, Ali Abdallah, Yogesh K. Dwivedi, and Nripendra P. Rana. 2017. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management 37: 99–110. [Google Scholar] [CrossRef]

- Alalwan, Ali Abdallah, Yogesh K. Dwivedi, Nripendra P. Rana, and Michael D. Williams. 2016. Consumer adoption of mobile banking in Jordan. Journal of Enterprise Information Management 29: 118–39. [Google Scholar] [CrossRef]

- Ali, Muhammad, Syed Ali Raza, Bilal Khamis, Chin Hong Puah, and Hanudin Amin. 2021. How perceived risk, benefit and trust determine user Fintech adoption: A new dimension for Islamic finance. Foresight 23: 403–20. [Google Scholar] [CrossRef]

- Alrawad, Mahmaod, Abdalwali Lutfi, Mohammed Amin Almaiah, and Ibrahim A. Elshaer. 2023. Examining the influence of trust and perceived risk on customers intention to use NFC mobile payment system. Journal of Open Innovation 9: 100070. [Google Scholar] [CrossRef]

- Arner, Douglas W., Ross P. Buckley, Dirk Andreas Zetzsche, and Robin Veidt. 2020. Sustainability, FinTech and Financial Inclusion. European Business Organization Law Review 21: 7–35. [Google Scholar] [CrossRef]

- Asif, Mohammad, Mohd Naved Khan, Sadhana Tiwari, Showkat K. Wani, and Firoz Alam. 2023. The impact of fintech and digital financial services on financial inclusion in India. Journal of Risk and Financial Management 16: 122. [Google Scholar] [CrossRef]

- Back, Camila, Stefan Morana, and Martin Spann. 2023. When do robo-advisors make us better investors? The impact of social design elements on investor behavior. Journal of Behavioral and Experimental Economics 103: 101984. [Google Scholar] [CrossRef]

- Bajunaied, Kholoud, Nazimah Hussin, and Suzilawat Kamarudin. 2023. Behavioral intention to adopt FinTech services: An extension of unified theory of acceptance and use of technology. Journal of Open Innovation 9: 100010. [Google Scholar] [CrossRef]

- Basri, Savitha, Iqbal Thonse Hawaldar, and Naveen Kumar K. 2022. Continuance intentions to use FinTech peer-to-peer payments apps in India. Heliyon 8: e11654. [Google Scholar] [CrossRef]

- Bauermeister, José A., Emily S. Pingel, Marc A. Zimmerman, Mick P. Couper, Alex Carballo-Diéguez, and Victor J. Strecher. 2012. Data quality in HIV/AIDS Web-Based surveys. Field Methods 24: 272–91. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, and Joseph Mpeera Ntayi. 2019. Trust: Mediator between mobile money adoption and usage and financial inclusion. Social Responsibility Journal 16: 1215–37. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, and Joseph Mpeera Ntayi. 2020. Mobile money adoption and usage and financial inclusion: Mediating effect of digital consumer protection. Digital Policy, Regulation and Governance 22: 157–76. [Google Scholar] [CrossRef]

- Carè, Rosella, Iustina Alina Boitan, and Razia Fatima. 2023. How do FinTech companies contribute to the achievement of SDGs? Insights from case studies. Research in International Business and Finance 66: 102072. [Google Scholar] [CrossRef]

- Chandra, Shalini, Shirish C. Srivastava, and Yin-Leng Theng. 2010. Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical analysis. Communications of the Association for Information Systems 27: 29. [Google Scholar] [CrossRef]

- Chauhan, Sumedha. 2015. Acceptance of mobile money by poor citizens of India: Integrating trust into the technology acceptance model. Info 17: 58–68. [Google Scholar] [CrossRef]

- Chopdar, Prasanta Kr, Nikolaos Korfiatis, V. Sivakumar, and Miltiadis D. Lytras. 2018. Mobile shopping apps adoption and perceived risks: A cross-country perspective utilizing the Unified Theory of Acceptance and Use of Technology. Computers in Human Behavior 86: 109–28. [Google Scholar] [CrossRef]

- De Blanes Sebastián, María García, Arta Antonovica, and José Ramón Sarmiento Guede. 2023. What are the leading factors for using Spanish peer-to-peer mobile payment platform Bizum? The applied analysis of the UTAUT2 model. Technological Forecasting and Social Change 187: 122235. [Google Scholar] [CrossRef]

- Dzandu, Michael Dzigbordi, Charles Hanu, and Hayford Amegbe. 2022. Gamification of mobile money payment for generating customer value in emerging economies: The social impact theory perspective. Technological Forecasting and Social Change 185: 122049. [Google Scholar] [CrossRef]

- Fan, Shuangshuang, Yehua Dennis Wei, Ning Xiao, Tomas Baležentis, and Leonardo Agnusdei. 2023. Can FinTech development pave the way for a transition towards inclusive growth: Evidence from an emerging economy. Structural Change and Economic Dynamics 67: 439–58. [Google Scholar] [CrossRef]

- Gansser, Oliver, and Christina Reich. 2021. A new acceptance model for artificial intelligence with extensions to UTAUT2: An empirical study in three segments of application. Technology in Society 65: 101535. [Google Scholar] [CrossRef]

- Gefen, David, Elena Karahanna, and Detmar W. Straub. 2003. Trust and TAM in online shopping: An integrated model. Management Information Systems Quarterly 27: 51. [Google Scholar] [CrossRef]

- George, Ajimon. 2018. Perceptions of Internet banking users—A structural equation modelling (SEM) approach. Iimb Management Review 30: 357–68. [Google Scholar] [CrossRef]

- George, Ajimon, and Geeta Trilok Kumar. 2014. Impact of service quality dimensions in internet banking on customer satisfaction. Decision 41: 73–85. [Google Scholar] [CrossRef]

- George, Ajimon, and Prajod Sunny. 2020. Developing a research model for mobile wallet adoption and usage. IIM Kozhikode Society & Management Review 10: 82–98. [Google Scholar]

- George, Ajimon, and Prajod Sunny. 2022. Why do people continue using mobile wallets? An empirical analysis amid COVID-19 pandemic. Journal of Financial Services Marketing. [Google Scholar] [CrossRef]

- Hair, Joseph F., Claudia Binz Astrachan, Ovidiu Ioan Moisescu, Lăcrămioara Radomir, Marko Sarstedt, Santha Vaithilingam, and Christian M. Ringle. 2021. Executing and interpreting applications of PLS-SEM: Updates for family business researchers. Journal of Family Business Strategy 12: 100392. [Google Scholar] [CrossRef]

- Hair, Joseph F., Jeffrey J. Risher, Marko Sarstedt, and Christian M. Ringle. 2019. When to use and how to report the results of PLS-SEM. European Business Review 31: 2–24. [Google Scholar] [CrossRef]

- Henseler, Jörg, Geoffrey S. Hubona, and Pauline Ash Ray. 2016. Using PLS path modeling in new technology research: Updated guidelines. Industrial Management and Data Systems 116: 2–20. [Google Scholar] [CrossRef]

- Hsu, Chin-Lung, and Judy Chuan-Chuan Lin. 2016. Effect of perceived value and social influences on mobile app stickiness and in-app purchase intention. Technological Forecasting and Social Change 108: 42–53. [Google Scholar] [CrossRef]

- Jangir, Kshitiz, Vikas Sharma, Sanjay Taneja, and Ramona Rupeika-Apoga. 2022. The moderating effect of perceived risk on users’ continuance intention for FinTech services. Journal of Risk and Financial Management 16: 21. [Google Scholar] [CrossRef]

- Kilani, Abd Al-Haleem ’Zaid, Dana Kakeesh, Ghazi A. Al-Weshah, and Mutaz M. Al-Debei. 2023. Consumer Post-Adoption of E-Wallet: An Extended UTAUT2 Perspective with Trust. Journal of Open Innovation 9: 100113. [Google Scholar] [CrossRef]

- Kock, Ned. 2015. Common method bias in PLS-SEM. International Journal of e-Collaboration 11: 1–10. [Google Scholar] [CrossRef]

- König, Pascal D., Stefan Wurster, and Markus B. Siewert. 2023. Sustainability challenges of artificial intelligence and Citizens’ regulatory preferences. Government Information Quarterly 40: 101863. [Google Scholar] [CrossRef]

- Laksamana, Patria, Suharyanto Suharyanto, and Yohanes Ferry Cahaya. 2022. Determining factors of continuance intention in mobile payment: Fintech industry perspective. Asia Pacific Journal of Marketing and Logistics 35: 1699–718. [Google Scholar] [CrossRef]

- Lee, Edmund Wei Jian, Vera S.H. Lim, and Clement J. K. Ng. 2022. Understanding public perceptions and intentions to adopt traditional versus emerging investment platforms: The effect of message framing and regulatory focus theory on the technology acceptance model. Telematics and Informatics Reports 8: 100024. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, Francisco, Sebastian Molinillo, and Arnold Japutra. 2020. Exploring the determinants of intention to use P2P mobile payment in Spain. Information Systems Management 38: 165–80. [Google Scholar] [CrossRef]

- Lin, Sheng-Wei, Eugenia Y. Huang, and Kai-Teng Cheng. 2022. Understanding organizational reputation formation in mobile commerce. Electronic Commerce Research and Applications 55: 101200. [Google Scholar] [CrossRef]

- Mahmud, Khaled, Md. Mahbubul Alam Joarder, and Kazi Sakib. 2023. Customer Fintech Readiness (CFR): Assessing customer readiness for fintech in Bangladesh. Journal of Open Innovation 9: 100032. [Google Scholar] [CrossRef]

- Martinez, Briana, and Laura McAndrews. 2023. Investigating U.S. consumers’ mobile pay through UTAUT2 and generational cohort theory: An analysis of mobile pay in pandemic times. Telematics and Informatics Reports 11: 100076. [Google Scholar] [CrossRef]

- Nawayseh, Mohammad K. Al. 2020. FinTech in COVID-19 and beyond: What factors are affecting customers’ choice of FinTech applications? Journal of Open Innovation 6: 153. [Google Scholar] [CrossRef]

- Nguyen, Yen Thi Hoang, Tommi Tapanainen, and Hai Thi Thanh Nguyen. 2022. Reputation and its consequences in Fintech services: The case of mobile banking. International Journal of Bank Marketing 40: 1364–97. [Google Scholar] [CrossRef]

- Oliveira, Tiago, Manoj A. Thomas, Gonçalo Baptista, and Filipe Campos. 2016. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior 2: 404–14. [Google Scholar] [CrossRef]

- Ong, Mohd Hanafi Azman, Muhammad Yassar Yusri, and Nur Ibrahim. 2023. Use and behavioural intention using digital payment systems among rural residents: Extending the UTAUT-2 model. Technology in Society 74: 102305. [Google Scholar]

- Schaarschmidt, Mario. 2016. Frontline employees’ participation in service innovation implementation: The role of perceived external reputation. European Management Journal 34: 540–49. [Google Scholar] [CrossRef]

- Şenol, Doğaç, and Ceylan Onay. 2023. Impact of gamification on mitigating behavioral biases of investors. Journal of Behavioral and Experimental Finance 37: 100772. [Google Scholar] [CrossRef]

- Senyo, Prince Kwame, and Ellis L. C. Osabutey. 2020. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 98: 102155. [Google Scholar] [CrossRef]

- Shaikh, Aijaz A., Richard Glavee-Geo, Heikki Karjaluoto, and Robert Ebo Hinson. 2023. Mobile money as a driver of digital financial inclusion. Technological Forecasting and Social Change 186: 122158. [Google Scholar] [CrossRef]

- Shen, Yupeng, C. James Hueng, and Wang Hu. 2019. Using digital technology to improve financial inclusion in China. Applied Economics Letters 27: 30–34. [Google Scholar] [CrossRef]

- Tamilmani, Kuttimani, Nripendra P. Rana, Samuel Fosso Wamba, and Rohita Dwivedi. 2021. The extended Unified Theory of Acceptance and Use of Technology (UTAUT2): A systematic literature review and theory evaluation. International Journal of Information Management 57: 102269. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2012. Consumer Acceptance and use of Information technology: Extending the unified theory of acceptance and use of technology. Management Information Systems Quarterly 36: 157. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, M. G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User Acceptance of Information Technology: Toward a Unified View. Management Information Systems Quarterly 27: 425. [Google Scholar] [CrossRef]

- Verma, Jyoti. 2023. Embracing Fintech Applications in the Banking Sector Vis-á-Vis Service Quality. Leeds: Emerald Publishing Limited, pp. 207–19. [Google Scholar]

- Vyas, Vishal, and Priyanka Jain. 2021. Role of digital economy and technology adoption for financial inclusion in India. Indian Growth and Development Review 14: 302–24. [Google Scholar] [CrossRef]

- Wang, Jen-Sheng. 2023. Reconfigure and evaluate consumer satisfaction for open API in advancing FinTech. Journal of King Saud University—Computer and Information Sciences 35: 101738. [Google Scholar] [CrossRef]

- Wang, Zhenning, Zhengzhi Guan, Fangfang Hou, Boying Li, and Wangyue Zhou. 2019. What determines customers’ continuance intention of FinTech? Evidence from YuEbao. Industrial Management and Data Systems 119: 1625–37. [Google Scholar] [CrossRef]

- Xi, Zhou, and Shou Chen. 2021. FinTech innovation regulation based on reputation theory with the participation of new media. Pacific-basin Finance Journal 67: 101565. [Google Scholar]

- Yang, Xiaoping, Jingshan Yang, Yilin Hou, Shuyang Li, and Shiwei Sun. 2023. Gamification of mobile wallet as an unconventional innovation for promoting Fintech: An fsQCA approach. Journal of Business Research 155: 113406. [Google Scholar] [CrossRef]

- Yu, Hongyang, Jinchao Wang, Jian Hou, Bolin Yu, and Yuling Pan. 2023. The effect of economic growth pressure on green technology innovation: Do environmental regulation, government support, and financial development matter? Journal of Environmental Management 330: 117172. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihan Gizem Korkmaz, Zhichao Yin, and Haigang Zhou. 2022. The rise of digital finance: Financial inclusion or debt trap? Finance Research Letters 47: 102604. [Google Scholar] [CrossRef]

- Zarifis, Alex, and Xusen Cheng. 2022. A model of trust in Fintech and trust in Insurtech: How Artificial Intelligence and the context influence it. Journal of Behavioral and Experimental Finance 36: 100739. [Google Scholar] [CrossRef]

- Zhou, Tao. 2013. An empirical examination of continuance intention of mobile payment services. Decision Support Systems 54: 1085–91. [Google Scholar] [CrossRef]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

,

,

{kind=link}

{kind=link}