The Impact of Environmental Accounting Information Disclosure on Financial Risk: The Case of Listed Companies in the Vietnam Stock Market

Abstract

:1. Introduction

2. Literature Review and Theoretical Framework

2.1. Literature Review

2.2. Theoretical Background

2.3. Research Hypotheses

2.3.1. The Relationship between the Level of Environmental Accounting Information Disclosure and Financial Risk

2.3.2. Assessing the Differences in Financial Risk between Listed Companies Included in the List of the Top 100 Sustainable Companies in Vietnam and Those Not on This List

3. Research Methodology

3.1. Data Collection

3.2. Variable Measurements

3.2.1. Dependent Variable: Financial Risk (FR)

- SZLit = (profit before tax + depreciation + deferred tax)/current liabilities.

- SYit = pre-tax profit/operating capital.

- GLit = shareholders’ interests/current liabilities.

- YFit = net tangible assets/total liabilities.

- YZit = working capital/total assets.

3.2.2. Independent Variable: The Level of Environmental Accounting Disclosure (ENVI)

- Xnt is the score of item n disclosed by company i in year t.

3.2.3. Control Variables

4. Results and Discussion

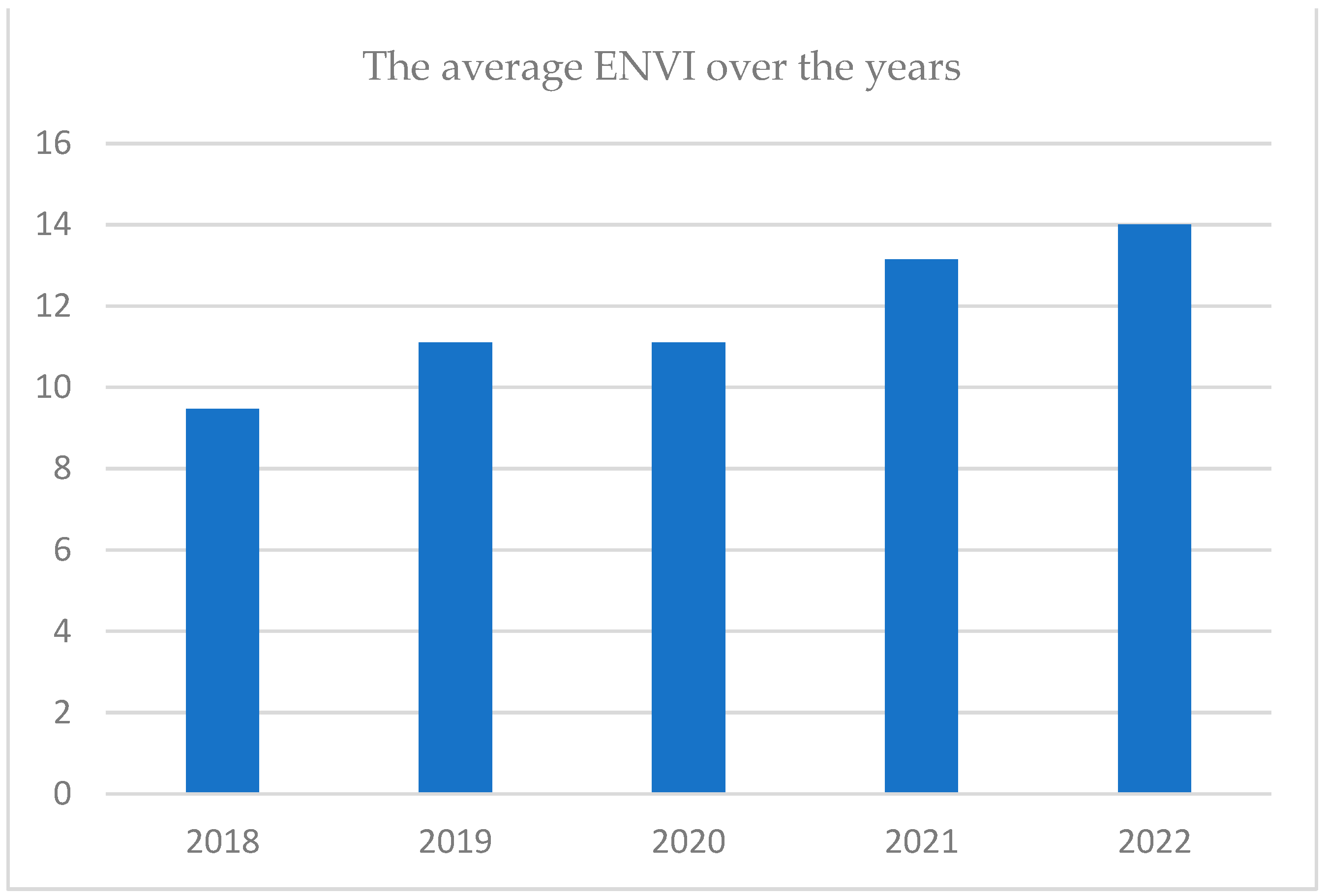

4.1. Descriptive Statistics

4.2. Assessing the Correlation between Variables

4.3. Research Finding and Discussions

4.3.1. The Relationship between the Level of Environmental Accounting Information Disclosure and the Financial Risk of the Current Year

4.3.2. The Relationship between the Level of Environmental Accounting Information Disclosure and the Financial Risk of the Following Year

4.3.3. Evaluate the Difference in Financial Risk between Companies Listed in the “Top 100 Sustainable Companies in Vietnam” and Those outside This List

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ahmed Sheikh, Nadeem, and Zongjun Wang. 2013. The impact of capital structure on performance: An empirical study of non-financial listed firms in Pakistan. International Journal of Commerce and Management 23: 354–68. [Google Scholar] [CrossRef]

- Albuquerque, Rui, Yrjö Koskinen, and Chendi Zhang. 2019. Corporate social responsibility and firm risk: Theory and empirical evidence. Management Science 65: 4451–69. [Google Scholar] [CrossRef]

- Al-Hadi, Ahmed, Bikram Chatterjee, Ali Yaftian, Grantley Taylor, and Mostafa Monzur Hasan. 2019. Corporate social responsibility performance, financial distress and firm life cycle: Evidence from Australia. Accounting & Finance 59: 961–89. [Google Scholar]

- Altman, Edward I. 1968. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance 23: 589–609. [Google Scholar] [CrossRef]

- Anh-Tuan, Le, Nguyen Thi Huyen-Tram, Nguyen Xuan-Hung, and Nguyen Vuong Thanh-Long. 2022. Disclosure of environmental accounting information at business enterprises in the hotel sector: Case study in Vietnam. Geo Journal of Tourism and Geosites 42: 700–7. [Google Scholar] [CrossRef]

- Attig, Najah, Sadok El Ghoul, Omrane Guedhami, and Jungwon Suh. 2013. Corporate social responsibility and credit ratings. Journal of Business Ethics 117: 679–94. [Google Scholar] [CrossRef]

- Ayadi, Mohamed, Martin I. Kusy, Minyoung Pyo, and Samir Trabelsi. 2015. Corporate social responsibility, corporate governance, and managerial risk-taking. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Bathory, Alexander. 1984. Predicting Corporate Collapse: Credit Analysis in the Determination and Forecasting of Insolvent Companies. London: Financial Times Business Information Ltd. [Google Scholar]

- Beaver, William H. 1966. Financial ratios as predictors of failure. Journal of Accounting Research 4: 71–111. [Google Scholar] [CrossRef]

- Benlemlih, Mohammed, Amama Shaukat, Yan Qiu, and Grzegorz Trojanowski. 2018. Environmental and social disclosures and firm risk. Journal of Business Ethics 152: 613–26. [Google Scholar] [CrossRef]

- Bhattacharyya, Asit. 2016. Factors associated with the social and environmental reporting of Australian companies. Australasian Accounting, Business and Finance Journal 8: 25–50. [Google Scholar] [CrossRef]

- Bhunia, Amalendu, and Somnath Mukhuti. 2012. Financial risk measurement of small and medium-sized companies listed in Bombay Stock Exchange. International Journal of Advances in Management and Economics 1: 27–34. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Alexis Cellier, Riadh Manita, and Asif Saeed. 2020. Does corporate social responsibility reduce financial distress risk? Economic Modelling 91: 835–51. [Google Scholar] [CrossRef]

- Cai, Li, Jinhua Cui, and Hoje Jo. 2016. Corporate environmental responsibility and firm risk. Journal of Business Ethics 139: 563–94. [Google Scholar] [CrossRef]

- Cheung, Adrian. 2016. Corporate social responsibility and corporate cash holdings. Journal of Corporate Finance 37: 412–30. [Google Scholar] [CrossRef]

- Cooper, Elizabeth, and Hatice Uzun. 2019. Corporate social responsibility and bankruptcy. Studies in Economics and Financ 36: 130–53. [Google Scholar] [CrossRef]

- De Jonghe, Olivier, Maaike Diepstraten, and Glenn Schepens. 2015. Banks’ size, scope and systemic risk: What role for conflicts of interest? Journal of Banking & Finance 61: S3–S13. [Google Scholar]

- Deegan, Craig. 2002. Introduction: The legitimising effect of social and environmental disclosures—A theoretical foundation. Accounting, Auditing & Accountability Journal 15: 282–311. [Google Scholar]

- Ding, Xiangan, Andrea Appolloni, and Mohsin Shahzad. 2022. Environmental administrative penalty, corporate environmental disclosures and the cost of debt. Journal of Cleaner Production 332: 129919. [Google Scholar] [CrossRef]

- Do, Trung K. 2022. Corporate social responsibility and default risk: International evidence. Finance Research Letters 44: 102063. [Google Scholar] [CrossRef]

- Dutta, Sunil, and Alexander Nezlobin. 2017. Information disclosure, firm growth, and the cost of capital. Journal of Financial Economics 123: 415–31. [Google Scholar] [CrossRef]

- Edmister, Robert O. 1972. An empirical test of financial ratio analysis for small business failure prediction. Journal of Financial and Quantitative Analysis 7: 1477–93. [Google Scholar] [CrossRef]

- El Ghoul, Sadok, Omrane Guedhami, Chuck C. Y. Kwok, and Dev R. Mishra. 2011. Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance 35: 2388–406. [Google Scholar]

- Elias, Rafik Z. 2004. The impact of corporate ethical values on perceptions of earnings management. Managerial Auditing Journal 19: 84–98. [Google Scholar] [CrossRef]

- Eriandani, Rizky, and Liliana Inggrit Wijaya. 2021. Corporate Social Responsibility and Firm Risk: Controversial Versus Noncontroversial Industries. The Journal of Asian Finance, Economics and Business 8: 953–65. [Google Scholar]

- Freeman, Edward, and Jeanne Liedtka. 1997. Stakeholder capitalism and the value chain. European Management Journal 15: 286–96. [Google Scholar] [CrossRef]

- Freeman, R. Edward. 1984. Strategic Management: A Stakeholder Approach. Cambridge: Cambridge University Press. [Google Scholar]

- Global Reporting Initiative (GRI). 2016. Sustainability Reporting Guidelines. Boston: GRI. [Google Scholar]

- Godfrey, Paul C., Craig B. Merrill, and Jared M. Hansen. 2009. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal 30: 425–45. [Google Scholar] [CrossRef]

- Hair, Joe F., Christian M. Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Jo, Hoje, and Haejung Na. 2012. Does CSR reduce firm risk? Evidence from controversial industry sectors. Journal of Business Ethics 110: 441–56. [Google Scholar] [CrossRef]

- Kytle, Beth, and John Gerard Ruggie. 2005. Corporate Social Responsibility as Risk Management. Working Paper No. 10. Cambridge, MA: John F. Kennedy School of Government, Harvard University. [Google Scholar]

- Lin, K. C., and Xiaobo Dong. 2018. Corporate social responsibility engagement of financially distressed firms and their bankruptcy likelihood. Advances in Accounting 43: 32–45. [Google Scholar] [CrossRef]

- Linh, Hoang Thuy. 2013. Environmental Financial Accounting and Application Orientation in Vietnam. Master’s thesis, University of Economics Ho Chi Minh City, Ho Chi Minh City, Vietnam. [Google Scholar]

- Liu, Min, and Weijie Lu. 2021. Corporate social responsibility, firm performance, and firm risk: The role of firm reputation. Asia-Pacific Journal of Accounting & Economics 28: 525–45. [Google Scholar]

- Luo, Xueming, and Chitra Bhanu Bhattacharya. 2009. The debate over doing good: Corporate social performance, strategic marketing levers, and firm-idiosyncratic risk. Journal of Marketing 73: 198–213. [Google Scholar] [CrossRef]

- Manini, Muganda Munir, Umulkher Ali Abdillahi, Kadian W. Wanyama, and John Simiyu. 2016. Effect of Business Financing on the Performance of Small and Medium Enterprises in Lurambi Sub-County, Kenya. Available online: http://erepository.kibu.ac.ke/handle/123456789/1017 (accessed on 1 October 2023).

- Minor, Dylan, and John Morgan. 2011. CSR as reputation insurance: Primum non nocere. California Management Review 53: 40–59. [Google Scholar] [CrossRef]

- Mishra, Saurabh, and Sachin B. Modi. 2013. Positive and negative corporate social responsibility, financial leverage, and idiosyncratic risk. Journal of Business Ethics 117: 431–48. [Google Scholar] [CrossRef]

- Nguyen, Canh Thi, Liem Thanh Nguyen, and Nhu Quynh Nguyen. 2022. Corporate social responsibility and financial performance: The case in Vietnam. Cogent Economics & Finance 10: 2075600. [Google Scholar]

- Nguyen, Thu Hien. 2022. Factors affecting the implementation of environmental management accounting: A case study of pulp and paper manufacturing enterprises in Vietnam. Cogent Business & Management 9: 2141089. [Google Scholar]

- Nguyen, Thuy An, Phuoc Huong Le, Huu Dang Nguyen, Thi Cam Tu Luong, and My Tran Ngo. 2023. The effect of environmental accounting information disclosure on financial performance of Vietnamese listed industrial firms: The moderating role of Leverage and Big4. CTU Journal of Innovation and Sustainable Development 15: 126–38. [Google Scholar] [CrossRef]

- Nguyen, Tung Dao. 2020. Factors influencing environmental accounting information disclosure of listed enterprises on Vietnamese stock markets. The Journal of Asian Finance, Economics and Business (JAFEB) 7: 877–83. [Google Scholar] [CrossRef]

- Ohlson, James A. 1980. Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research 18: 109–31. [Google Scholar] [CrossRef]

- Oikonomou, Ioannis, Chris Brooks, and Stephen Pavelin. 2012. The impact of corporate social performance on financial risk and utility: A longitudinal analysis. Financial Management 41: 438–515. [Google Scholar] [CrossRef]

- Orlitzky, Marc, and John D. Benjamin. 2001. Corporate social performance and firm risk: A meta-analytic review. Business & Society 40: 369–96. [Google Scholar]

- Pfeffer, Jeffrey, and Gerald Salancik. 1978. The External Control of Organizations: A Resource Dependence Perspective. Urbana, IL: University of Illinois at Urbana-Champaign’s Academy for Entrepreneurial Leadership Historical Research Reference in Entrepreneurship. [Google Scholar]

- Pham, Minh Vuong, and Phuong Trang Duong. 2022. Impact of the Environmental Information Disclosure on the Financial Performance of Listed Companies in Vietnam. Vietnam Trade and Industry Review, Research and Application of Scientific Results and Technology, Issue 5. Available online: https://tapchicongthuong.vn/bai-viet/anh-huong-cua-cong-bo-thong-tin-ve-tac-dong-moi-truong-len-hieu-qua-tai-chinh-cua-cac-cong-ty-niem-yet-tai-viet-nam-90106.htm (accessed on 1 October 2023).

- Tauchen, George. 1986. Finite state markov-chain approximations to univariate and vector autoregressions. Economics Letters 20: 177–81. [Google Scholar] [CrossRef]

- Ullmann, Arieh A. 1985. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and Economic Performance of U.S. Firms. Academy of Management 10: 540–57. [Google Scholar] [CrossRef]

- Weber, Max. 1922. Economy and Society. Berkeley: University of California Press. [Google Scholar]

{kind=link}

| Industry | Number of Companies | Observations |

|---|---|---|

| Manufacturing | 42 | 210 |

| Utilities | 8 | 40 |

| Construction and Real Estate | 6 | 30 |

| Transportation and Warehousing | 2 | 10 |

| Wholesale | 2 | 10 |

| Total | 60 | 300 |

| No. | Field | Number of Items | Referencing to GRI |

|---|---|---|---|

| 1 | Materials | 4 | 301 |

| 2 | Energy | 6 | 302 |

| 3 | Water | 4 | 303 |

| 4 | Biodiversity | 5 | 304 |

| 5 | Emissions | 8 | 305 |

| 6 | Effluents and Waste | 6 | 306 |

| 7 | Environmental Compliance | 2 | 307 |

| 8 | Supplier Environmental Assessment | 3 | 308 |

| The Level of Information Disclosure | Score |

|---|---|

| Full disclosure of required information through quantitative data or qualitative information | 2 |

| Partial disclosure of required information but not complete | 1 |

| Non-disclosure of required content or disclosure of irrelevant information | 0 |

| Item | Content | Score | Item | Content | Score |

|---|---|---|---|---|---|

| 301-0 | Management approach | 1 | 305-0 | Management approach | 1 |

| 301-1 | Materials used by weight or volume | 0 | 305-1 | Direct (Scope 1) GHG emissions | 1 |

| 301-2 | Recycled input materials used | 2 | 305-2 | Energy indirect (Scope 2) GHG emissions | 1 |

| 301-3 | Reclaimed products and their packaging materials | 0 | 305-3 | Other indirect (Scope 3) GHG emissions | 0 |

| 302-0 | Management approach | 1 | 305-4 | GHG emissions intensity | 1 |

| 302-1 | Energy consumption within the organization | 1 | 305-5 | Reduction in GHG emissions | 1 |

| 302-2 | Energy consumption outside of the organization | 0 | 305-6 | Emissions of ozone-depleting substances (ODS) | 0 |

| 302-3 | Energy intensity | 1 | 305-7 | Nitrogen oxides (NOx), sulfur oxides (SOx), and other significant air emissions | 0 |

| 302-4 | Reduction in energy consumption | 2 | 306-0 | Management approach | 1 |

| 302-5 | Reduction in energy requirements of products and services | 2 | 306-1 | Water discharge by quality and destination | 1 |

| 303-0 | Management approach | 1 | 306-2 | Waste by type and disposal method | 2 |

| 303-1 | Water withdrawal by source | 2 | 306-3 | Significant spills | 1 |

| 303-2 | Water sources significantly affected by withdrawal of water | 1 | 306-4 | Transport of hazardous waste | 1 |

| 303-3 | Water recycled and reused | 1 | 306-5 | Water bodies affected by water discharges and/or runoff | 1 |

| 304-0 | Management approach | 1 | 307-0 | Management approach | 0 |

| 304-1 | Operational sites owned, leased, managed in, or adjacent to, protected areas and areas of high biodiversity value outside protected areas | 0 | 307-1 | Non-compliance with environmental laws and regulations | 0 |

| 304-2 | Significant impacts of activities, products, and services on biodiversity | 1 | 308-0 | Management approach | 1 |

| 304-3 | Habitats protected or restored | 1 | 308-1 | New suppliers that were screened using environmental criteria | 2 |

| 304-4 | IUCN Red List species and national conservation list species with habitats in areas affected by operations | 0 | 308-2 | Negative environmental impacts in the supply chain and actions taken | 1 |

| Total score (X) = 34 | |||||

| Code | Control Variable | Measurement | References |

|---|---|---|---|

| SIZE | Business size | Log(Total Assets) | Ohlson (1980); De Jonghe et al. (2015); Al-Hadi et al. (2019) |

| LEV | Financial leverage | Liabilities/Total Assets | Ayadi et al. (2015); Benlemlih et al. (2018); Al-Hadi et al. (2019) |

| ROA | Return on assets | (Net Income/Average Total Assets)*100 | Altman (1968); Bhunia and Mukhuti (2012); Ahmed Sheikh and Wang (2013); Al-Hadi et al. (2019) |

| CR | Current ratio | Current Assets/Current Liabilities | Beaver (1966); Edmister (1972); Ohlson (1980); Bhunia and Mukhuti (2012) |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| FR | 300 | 5.293275 | 7.30096 | −1.028936 | 108.3492 |

| ENVIt | 300 | 11.76333 | 8.842773 | 0 | 39 |

| ENVIt−1 | 240 | 11.20417 | 8.701223 | 0 | 38 |

| SIZE | 300 | 3.485007 | 0.5990884 | 2.296665 | 5.411173 |

| LEV | 300 | 0.4409413 | 0.198406 | 0.079096 | 0.9310873 |

| ROA | 300 | 8.815633 | 7.520865 | −1.1 | 47.51 |

| CR | 300 | 2.30426 | 1.520973 | 0.252497 | 10.84211 |

| FR | ENVIt | ENVIt−1 | SIZE | LEV | ROA | CR | VIFt | VIFt−1 | |

|---|---|---|---|---|---|---|---|---|---|

| FR | 1.0000 | - | - | ||||||

| ENVIt | 0.0565 | 1.0000 | 1.25 | - | |||||

| ENVIt−1 | 0.0020 | 0.8970 | 1.0000 | - | 1.24 | ||||

| SIZE | −0.1669 | 0.3190 | 0.3188 | 1.0000 | 1.28 | 1.29 | |||

| LEV | −0.3235 | −0.1502 | −0.1354 | 0.2612 | 1.0000 | 2.07 | 2.04 | ||

| ROA | 0.2450 | 0.2190 | 0.2094 | −0.1863 | −0.4675 | 1.0000 | 1.35 | 1.35 | |

| CR | 0.3298 | 0.0875 | 0.0680 | −0.1577 | −0.6402 | 0.2960 | 1.0000 | 1.70 | 1.65 |

| FR | ||||

|---|---|---|---|---|

| OLS | FEM | REM | FGLS | |

| ENVIt | 0.0230811 (0.642) | −0.01655 (0.884) | 0.014334 (0.801) | 0.0037033 (0.041) |

| SIZE | −1.144191 (0.124) | −7.334444 (0.108) | −1.189315 (0.181) | −0.5217391 (0.000) |

| LEV | −4.034508 (0.158) | 0.9085111 (0.901) | −3.549392 (0.280) | −4.410638 (0.000) |

| ROA | 0.1046479 (0.086) | 0.1090136 (0.450) | 0.1083972 (0.121) | 0.0785901 (0.000) |

| CR | 1.010112 (0.003) | 1.716255 (0.008) | 1.094589 (0.004) | 0.9329858 (0.000) |

| Constant | 7.538163 (0.013) | 25.73223 (0.094) | 7.356697 (0.038) | 5.527951 (0.000) |

| Observations | 300 | 300 | 300 | 300 |

| R2 | 0.1340 | 0.0927 | 0.1482 | - |

| FR | ||||

|---|---|---|---|---|

| OLS | FEM | REM | FGLS | |

| ENVIt−1 | −0.0414766 (0.088) | 0.0322612 (0.399) | −0.0013598 (0.962) | 0.0215336 (0.000) |

| SIZE | −0.511191 (0.152) | −1.212972 (0.436) | −0.7889314 (0.161) | −1.140958 (0.000) |

| LEV | −6.725794 (0.000) | −2.706355 (0.300) | −4.719109 (0.007) | −2.385443 (0.000) |

| ROA | 0.1181029 (0.000) | 0.0799709 (0.089) | 0.0934042 (0.008) | 0.0808845 (0.000) |

| CR | 1.005345 (0.000) | 1.511309 (0.000) | 1.32014 (0.000) | 1.435245 (0.000) |

| Constant | 6.814886 (0.000) | 5.846111 (0.274) | 5.943473 (0.004) | 5.394794 (0.000) |

| Observations | 240 | 240 | 240 | 240 |

| R2 | 0.5315 | 0.5020 | 0.5283 | - |

| FR | The Relationship with the Variable FR | The Relationship with Financial Risk | ||

|---|---|---|---|---|

| Non-Lag | Lag | |||

| ENVIt | 0.0037033 | - | + | – |

| ENVIt−1 | - | 0.0215336 | + | – |

| SIZE | −0.5217391 | −1.140958 | – | + |

| LEV | −4.410638 | −2.385443 | – | + |

| ROA | 0.0785901 | 0.0808845 | + | – |

| CR | 0.9329858 | 1.435245 | + | – |

| Group | Obs | Mean | Std. Err. | Std. Dev. | Pr(|T| > |t|) | |

|---|---|---|---|---|---|---|

| FR | Non-TOP | 178 | 4.501455 | 0.3002183 | 4.005411 | 0.0230 |

| TOP | 122 | 6.448553 | 0.9320428 | 10.29475 | ||

| ENVIt | Non-TOP | 178 | 9.11236 | 0.483452 | 6.450048 | 0.0000 |

| TOP | 122 | 15.63115 | 0.93627 | 10.34144 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

La Soa, N.; Duy, D.D.; Thanh Hang, T.T.; Ha, N.D. The Impact of Environmental Accounting Information Disclosure on Financial Risk: The Case of Listed Companies in the Vietnam Stock Market. J. Risk Financial Manag. 2024, 17, 62. https://doi.org/10.3390/jrfm17020062

La Soa N, Duy DD, Thanh Hang TT, Ha ND. The Impact of Environmental Accounting Information Disclosure on Financial Risk: The Case of Listed Companies in the Vietnam Stock Market. Journal of Risk and Financial Management. 2024; 17(2):62. https://doi.org/10.3390/jrfm17020062

Chicago/Turabian StyleLa Soa, Nguyen, Do Duc Duy, Tran Thi Thanh Hang, and Nguyen Dieu Ha. 2024. "The Impact of Environmental Accounting Information Disclosure on Financial Risk: The Case of Listed Companies in the Vietnam Stock Market" Journal of Risk and Financial Management 17, no. 2: 62. https://doi.org/10.3390/jrfm17020062