1. Introduction

The Danish Financial Supervisory Authority frequently publishes an evaluation of the current financial risks that dominate the Danish pension and insurance market. In their latest evaluation,

DFSA (

2022a), the focus is on the interest rate, inflation, and the risk of recession. These factors create a volatile and insecure financial market. Thus, Danish pension companies are encouraged to revisit the pension products they offer and reassess whether these meet the investor’s potential preferences for smoothing. The aim is to maintain the investor’s interests and keep the investor’s faith in the pension companies.

Most Danish pension companies offer market-rate pension products, where the size of the pension benefit depends on the return on investing pension savings in risky assets. Such products are comparable with variable life annuities. Thus, increased volatility and insecurity in the financial market might increase the need for the stability of pension benefits. In terms of optimal stochastic control theory with lifetime uncertainty, we think of the pension benefits as the consumption of an investor.

With stochastic optimal control theory, this paper aims to present optimal consumption and investment strategies that inspire the design of a smooth pension product.

Merton (

1969,

1971) formalized and solved the original problem of maximizing the total expected utility of intertemporal consumption and terminal wealth of an investor over a fixed time interval. Lifetime uncertainty was introduced to the stochastic optimal control problem by

Richard (

1975). The result of optimal consumption from the above literature resembles the design of a standard market rate life annuity offered by most Danish pension companies.

Introducing additive habit formation in preferences to the stochastic optimal control problem can explain the request for smooth consumption; see

Bruhn and Steffensen (

2013). The habit level of an investor depends on past consumption. By introducing habit formation to the problem, we assume that the investor only obtains utility from the current consumption level over the current habit level. Thus, we consider the current consumption level relative to past consumption.

Munk (

2008) studies optimal consumption and investment strategies with additive habit formation in preferences and stochastic variations in investment opportunities. He concludes that habit formation in preferences reduces the speculative investments of the investor to ensure the habit level as a minimum level of consumption.

Kashif et al. (

2020) investigate different optimal consumption and investment strategies for university endowment funds. Their objective is to find a strategy that smooths consumption over time. They present an ad hoc consumption strategy called the hybrid strategy. Consumption is specified as a weighted average of last year’s consumption level and a constant proportion of the current wealth of the investor. They show that the hybrid strategy is the least volatile strategy for consumption compared to the optimal consumption strategy in

Merton (

1969,

1971) and to consumption defined as a constant proportion of the current wealth. These strategies can be translated to pension product designs by introducing lifetime uncertainty.

This paper aims to understand which preferences lead to the request for consumption stability. We can only design a smooth pension product that meets these preferences with such an understanding. A main contribution is to connect the hybrid strategy suggested by

Kashif et al. (

2020) with the consumption profile arising from habit formation in the preferences. We realize through studying the consumption dynamics that the products they form overlap. This suggests continuing the design work within the class of hybrid strategies since we then know more about which preferences they satisfy.

We aim for a smooth pension product that is feasible, transparent, and fair from the perspective of both the investor and the pension company. An already existing smooth pension product is Tidspension, as discussed by

Bruhn and Steffensen (

2013). This pension product includes a buffer account to achieve a smoothing effect on consumption, increasing the design’s complexity. We seek for even more simplicity.

The rest of the paper is structured as follows.

Section 2 sets up the general framework of the investment market and the utility maximization problem and introduces lifetime uncertainty to the problem.

Section 3 presents three strategies for consumption and investment: the classical strategy, the habit strategy, and the hybrid strategy. Continuing to

Section 4, the dynamics of consumption under the three strategies are studied. Moreover, the similarities between the consumption dynamics under the habit and hybrid strategies are investigated. In

Section 5, the three strategies inspire two approaches for a smooth pension product.

Section 6 presents numerical examples of the classical strategy and the two approaches. The conclusion of the results is given in

Section 7.

Appendix A contains the proofs of the consumption dynamics from

Section 4.

4. The Development of Consumption over Time

The dynamics of a process reveal the development of the process over time. This section aims to study the effect of optimal consumption under the three strategies. We find the optimal consumption dynamics in the classical and habit strategies by Itô’s formula. In the hybrid strategy, we induce the already seen consumption dynamics by the optimal investment to find the optimal version of the dynamics.

4.1. Consumption Dynamics in the Classical Strategy

Applying Itô’s formula to the optimal consumption in the classical strategy given by (

14), the dynamics of optimal consumption are derived by

Finding the derivatives of

, inserting these, the wealth dynamics with the optimal investment portfolio into (

32) and rearranging, we can state the following result:

Theorem 1. Consider optimal consumption in the classical strategy defined by (14). Then, the dynamics of optimal consumption are given bywhere the deterministic function is defined by (11). From Theorem 1, we note that optimal consumption in the classical strategy is a geometric Brownian motion. As

Bruhn and Steffensen (

2013), we deduce that the stock market fluctuations immediately affect the current consumption level due to the stochastic

-term.

The -term reveals the expected development of consumption over time since a Brownian motion has a mean zero. Disregarding the risk aversion parameter in the denominator of the -term, we see that consumption increases by the interest rate, the pricing intensity, and the quantity obtained from investing in the risky asset, i.e., capital gains. Moreover, consumption decreases with the impatience factor and the mortality rate. Consequently, ignoring capital gains, an increasing or decreasing tendency in the consumption level can be explained by the relation between the interest rate and the impatience factor or the pricing intensity and the mortality rate.

Regarding the impact of the risk aversion parameter on the development of consumption over time, observe that the -term and the -term explode as . On the other hand, both terms vanish as . Hence, the risk-tolerant investor experiences a highly volatile development in consumption, and the risk-averse investor prefers a less volatile or constant consumption level. Thus, the risk-averse investor is averse to variation over time.

4.2. Consumption Dynamics in the Habit Strategy

Again, by applying Itô’s formula to the optimal consumption in the habit strategy given by (

21), the dynamics of optimal consumption are in the following form:

Finding the partial derivatives of

, inserting these, the wealth dynamics, and the habit dynamics with the optimal investment portfolio into (

35) and rearranging, we obtain the following result:

Theorem 2. Consider optimal consumption in the habit strategy defined by (21). Then, the dynamics of optimal consumption are given bywhere The deterministic functions and are defined by (19) and (20), respectively. From Theorem 2, we infer that optimal consumption under the habit strategy is less volatile than optimal consumption under the classical strategy. Now, stock market fluctuations immediately affect only consumption over the current habit level. Optimal consumption over the current habit level is a geometric Brownian motion, which can be obtained by a minor rewriting of (

36) (see

Bruhn and Steffensen 2013). This supports the idea of using the habit strategy as a smoothing strategy for consumption.

Furthermore, the incorporation of additive habit formation impacts the expected development of consumption. Now, consumption evolves as a proportion of the current consumption level over a proportion of the existing habit level. The proportions are identical to the fraction in the -term of optimal consumption in the classical strategy, including a quantity, , added to the numerator as a result of introducing habit formation. Additionally, the habit preferences are added to the fraction.

Moreover, note that for and for all in Theorem 2, we arrive at the optimal consumption dynamics from Theorem 1. Hence, the structure of the dynamics allows us to switch between the classical and the habit strategy.

For another special case, observe that for

, the consumption dynamics in the habit strategy are equal to the habit dynamics given by (

17). Thus, the optimal consumption of a risk-averse investor with additive habit formation in the preferences evolves as the habit level.

Next, recall the expression of optimal consumption under the habit strategy given by (

21). Observe that

is affine in

h. Thus, isolating

h in the expression of

, we obtain an expression of the habit level in terms of optimal consumption and wealth:

Inserting (

38) into the dynamics of

given by Theorem 2 and rearranging, we rephrase the optimal consumption dynamics as follows.

Theorem 3. Consider the habit level given by (38). Then, the dynamics of optimal consumption in the habit strategy from Theorem 2 can be rewritten aswhere , , and are deterministic functions given by Proof of Theorem 3. The result of Theorem 3 follows directly from inserting the habit level given by (

38) into the optimal consumption dynamics given by (

36) and gathering the

-terms and

-terms multiplied by

and

X, respectively. □

Hence, we have rephrased the dynamics of optimal consumption in the habit strategy without the habit level. This is reasonable when considering the design of a pension product. The visible variables in a pension product should solely be consumption and wealth, but the habit formation of the investor could reasonably drive the underlying mechanisms. But it is difficult as a pension company to form the value of the initial habit level of the investor, and now we have avoided this difficulty.

In addition, recall that the optimal investment under the habit strategy is given by

Inserting the habit level expressed by (

38) into

, we obtain an expression of optimal investment without the habit level:

Hence, the optimal investment under the habit strategy has the same structure as the optimal investment in the hybrid strategy. Now, the actual investment, , is a proportion of the current wealth over a proportion of the current consumption level.

4.3. Consumption Dynamics in the Hybrid Strategy

Recall the dynamics of consumption in the hybrid strategy:

with

. We found that optimal investment under the hybrid strategy is given by

where

solves the Riccati equation given by (

30). Inserting (

46) into the dynamics of

c given by (

45) and doing a minor rewriting, we obtain the following result:

Theorem 4. Consider consumption in the hybrid strategy defined by (24) following the dynamics given by (45). With the optimal investment strategy given by (46), the consumption dynamics in the hybrid strategy can be rewritten aswhere , , and are deterministic functions given by Proof of Theorem 4. The result of Theorem 4 follows directly from inserting the optimal investment strategy given by (

46) into the consumption dynamics given by (

45) and gathering the

-terms and

-terms multiplied by

c and

X, respectively. □

Note the astonishing similarities between the structure of the consumption dynamics from Theorems 3 and 4. We will elaborate and employ these similarities in the design of a smooth pension product in

Section 5. We formalize the comparison of the two strategies in the following subsection.

4.4. Comparing Consumption Dynamics in the Habit and the Hybrid Strategy

In the preceding section, we compare the habit and hybrid strategies by comparing their consumption dynamics.

Theorem 5. The consumption dynamics in the habit strategy given by Theorem 3 and the consumption dynamics in the hybrid strategy given by Theorem 4 coincide if Proof of Theorem 5. The result of Theorem 5 follows directly by comparing the consumption dynamics from Theorems 3 and 4. □

Hence, the habit strategy and the hybrid strategy for consumption are identical if Equations (

52)–(

55) in Theorem 5 are fulfilled. Even though the equations are not fulfilled, we still obtain that the structure of consumption and wealth is the same in the consumption dynamics under the two strategies. Thus, consumption under the two strategies evolves similarly but with (possibly) different deterministic functions. This remarkable result shows that the hybrid strategy complies with the preferences of additive habit formation. Hence, we conclude that the habit and hybrid strategies satisfy the same preferences.

5. Designing a Smooth Pension Product

This section aims to give two approaches for designing a smooth pension product, i.e., a smooth life annuity, which complies with the preferences of an investor who wants stability with respect to consumption and has no utility from their bequest. This is accomplished by inspiration of the habit and hybrid strategies and their similarities studied in

Section 4. In addition, we incorporate optimal consumption under the classical strategy. We aim for a feasible, transparent, and fair design from the perspective of both the investor and the pension company. In designing a pension product, we need to specify the strategy for consumption and investment in the risky asset. With inspiration from the habit strategy and the hybrid strategy, this boils down to defining the constant and the weight in the discrete-time formulation of consumption under the hybrid strategy given by (

24) and revisiting the optimal investment portfolio under the two strategies.

Consider the discrete-time formulation of consumption under the hybrid strategy given by (

24), but now let

w and

y be time-dependent. Thus, we redefine consumption by

In the design of a pension product, it is reasonable to let w and y be time-dependent. For feasibility and transparency, the liabilities of the pension company should be equal to the investor’s wealth. For fairness, the investor’s wealth should tend to zero as we reach termination, since we are considering a life annuity and assuming that the investor has no utility from the bequest. We can incorporate these criteria by allowing time-dependent w and y.

Let

y be defined as follows

where

is given by (

11) from the classical strategy. Recall that

is interpreted as an annuity with the utility-adjusted interest rate as the calculation rate and the utility-adjusted mortality rate as the calculation of mortality. Thus, with

y defined as (

57), we have that

is the optimal consumption under the classical strategy, which we interpreted as a standard market rate life annuity.

Now, let

w be defined as follows

where

is a non-negative constant, and we define

as an annuity given by

with the calculation rate given by an interest rate,

, and the utility-adjusted mortality rate as the calculation of mortality.

The reasoning behind the construction of

w given by (

58) is that the impact of last year’s consumption level should depend on where the investor is in the decumulation phase. At the beginning of the decumulation phase, we want a higher weight on last year’s consumption level to stabilize consumption. At the end of the decumulation phase, we want a higher weight on the future, i.e., a lower weight on past consumption, to let the standard market rate life annuity take over and the wealth go to zero. Observe that this reasoning is achieved by

w defined as (

58) since

for

. We use

instead of

since we want to change the interest rate to adjust the value of

w. The higher the value of

, the lower the value of

w. Inspired by the definition of the habit level given by (

16), we weigh the annuity by

to provide relative importance to past consumption.

Requiring that for , we set the initial value of consumption equal to , where is the value of the wealth at the time of retirement. Thus, we assume that the initial consumption value in the smooth pension product is equal to that in the classical strategy. This is also reasonable when comparing the two strategies.

Summarizing the above assumptions of

w and

y, we rewrite consumption given by (

56) as

Hence, we have specified the strategy for consumption in the smooth pension product as a hybrid between a standard market rate life annuity and stability with respect to last year’s consumption level.

Regarding the investment portfolio in the smooth pension product, we need to reconsider how the optimal investment portfolio in the hybrid strategy was found before using the result given by (

31) from this strategy. The optimal investment portfolio was found by optimizing the expected utility of terminal wealth similar to

Kashif et al. (

2020). This is a somewhat artificial construction when designing a smooth pension product where we want to let the wealth go to zero as we reach termination. However, by Remark 1, we observe a simple structure of the optimal investment portfolio under the hybrid strategy. We wish to examine how this investment portfolio works with consumption specified as (

60). This constitutes the first approach to a smooth pension product.

To obtain even more feasibility and transparency of the investment portfolio in the smooth pension product, we become inspired by the optimal investment portfolio under both the habit and hybrid strategies. We employ the structure of the optimal investment portfolio under the habit strategy. Instead of subtracting a proportion of the current habit level from the wealth, we subtract a proportion of the current consumption level as in the optimal investment portfolio under the hybrid strategy given by (

22). Moreover, we avoid a term multiplied by the wealth in the denominator as in the optimal investment portfolio under the habit strategy. This constitutes the second approach to a smooth pension product.

Hence, we have two approaches for the investment portfolio in the smooth pension product. With

y and

w given by (

57) and (

58), respectively, such that consumption is given by (

60), we formalize two approaches for the smooth pension product.

5.1. First Approach

In the first approach, we employ the simple structure obtained by Remark 1. From the remark, we have that

where we insert

y and

w defined by (

57) and (

58), respectively, in the last equality. Inserting (

61) into the optimal investment portfolio under the hybrid strategy given by (

31), we specify the investment portfolio in the first approach for the smooth pension product by

Thus, the investment portfolio’s denominator equals a constant multiplied by the wealth. Moreover, the proportion subtracted from the wealth is the current consumption level multiplied by a function similar to an annuity.

5.2. Second Approach

In the second approach, we set the denominator of the optimal investment portfolio under the hybrid strategy given by (

31) equal to one multiplied by the wealth. Moreover, we specify the term subtracted from the wealth in the numerator by the current consumption level multiplied by an annuity. The construction is established by inspiration of the optimal investment portfolio under the habit strategy with the expression of the habit level in terms of optimal consumption and wealth inserted (see (

44)). Thus, we define the investment portfolio in the second approach by

for all

, where the annuity

is given by (

59). Compared to the first approach, the second approach attempts to achieve even more simplicity and transparency in the structure of the investment portfolio.

In the first and second approaches, the term multiplied by the current consumption level tends to zero as we reach termination. Furthermore, note that if we choose a high value of the interest rate, , in , then the term becomes small. Thus, it is interpreted as the lack of protection against a decline in the market in the attempt to achieve stability concerning consumption.

5.3. Valuation

With the structure of consumption and investment portfolio in the two approaches for a smooth pension product given above, we have that the liabilities of the pension company are precisely equal to the investor’s wealth. This holds by the fact that consumption, given by (

60), tends to the optimal consumption under the classical strategy such that the whole wealth is paid out when we reach termination. Thus, we omit the complexity of setting aside a buffer to achieve a smoothing effect on consumption, which is the case in the existing smooth pension product Tidspension by

Bruhn and Steffensen (

2013). The simplicity of the two approaches also relies on the fact that the consumption level is non-guaranteed. Instead, we aim at a less volatile development of consumption.

We have obtained two feasible, transparent, and fair designs considering everything. Compared to the existing smooth pension products, we have increased the simplicity.

6. Numerical Examples

In this section, numerical examples of consumption over time illustrate the smoothing effect on consumption under the two approaches for a smooth pension product. We compare the development of wealth, consumption, and investment portfolios under the two approaches and the classical strategy. See

Munk (

2008) for a numerical study of optimal consumption and investment with additive habit formation in preferences. See

Kashif et al. (

2020) for numerical examples of the hybrid strategy.

The first subsection below establishes the numerical setup by specifying the parameters to simulate the simplified financial market. Additionally, we decide upon a representative estimation of the mortality rate and the pricing intensity. In the second subsection, we illustrate and analyze the development of wealth, optimal consumption, and investment portfolio in the classical strategy. Continuing to the third and the fourth subsection, we give numerical examples of the two approaches for a smooth pension product from

Section 5. These examples are compared with the numerical results of the classical strategy from the second subsection.

6.1. Numerical Setup

The Euler scheme is used to simulate the development of the wealth process by a time-discretized approximation with independent normal random variables representing the Brownian motion for every year in the fixed time interval

. The simulation is repeated

n = 100,000 times under the classical strategy and the two approaches, respectively, with the chosen values of the parameters from

Table 1 and a specified model for the mortality rate and the pricing intensity as described below. We let the parameter

be equal to

aligned with

Munk (

2008). The rest of the parameters are chosen in line with comparable life insurance literature (see, e.g.,

Bruhn and Steffensen (

2011) or

Konicz et al. (

2015)). The time frame used for the simulation under the classical strategy is

s, while it is

s under the first approach, and

s under the second approach.

As we only consider the decumulation phase of the investor, the fixed investment time interval represents that the investor retires at time 0 with age 65, and we assume the specified time horizon at which the investor is age 110.

Regarding the lifetime uncertainty, we assume that

, i.e., zero market price of insurance risk, is modeled by a linear interpolation of the benchmark mortality rate for Danish women in 2021 over age 65 constituted by the Danish Financial Supervisory Authority (see

DFSA 2022b). We omit to consider expected future lifetime improvements. Thus, we assume that a 65-year-old woman today in 2023 has the same mortality rate as a 65-year-old woman in 2021. Next year, when she turns 66, we think she will have the same mortality rate as a 66-year-old woman in 2021. A more realistic model for the mortality rate could have been constructed, but it is not the focus of this paper.

All numerical results are based on the assumption of no utility from bequest such that full mortality credits are assigned to the investor’s wealth until death. The case of full utility from bequest, in the sense that no insurance is wanted, can, essentially, be obtained by setting

in all the formulas above. From a financial point of view, it corresponds to lowering the return rates

r and

simultaneously by

. This would lead to lower levels of consumption but along the same curvature as below. It is beyond the scope of this paper to examine in full the impact of utility from bequest, though. A different interesting case is where there is no utility from bequest but also no access to a life insurance market. The welfare loss from losing access to the insurance market is the main objective of

Steffensen and Søe (

2023) where there is no attention to smoothing, though.

6.2. The Classical Strategy

With the numerical setup from the preceding

Section 6.1, we demonstrate the development of wealth, optimal consumption, and investment portfolio under the classical strategy. The optimal consumption and investment portfolio are given by (

14) and (

15), respectively. The expected development over time, accompanied by the

and

quantile, illustrates the strategy’s volatility.

We leave out the graph of the optimal investment portfolio in the classical strategy as it is constant over time. With parameter values from

Table 1, the optimal quantity invested in the risky asset is

for all

. Thus, about one-third of the wealth is invested in the risky asset throughout the entire decumulation phase.

Figure 1 shows that the investor is more eager to consume at the beginning of the decumulation phase than at the end, as we observe a decreasing graph of expected optimal consumption. An explanation of this development can be found by inspecting the drift term in the dynamics of optimal consumption under the classical strategy given in Theorem 1. Disregarding the return of the risky asset, the drift term contains the interest rate subtracted from the impatience factor, and as the values of these parameters are chosen such that

, we experience a decline in consumption over time. Hence, the investor is impatient.

Moreover, the wealth tends to zero as we reach expiry; i.e., the entire wealth is consumed since the investor has no utility from the bequest. This observation aligns with the insurance company’s liabilities, which are repealed at expiry or the investor’s death. Hence, the figure shows that the liabilities are equal to the wealth.

The

and

quantile emphasized by the dashed lines in

Figure 1 visualize that

of the simulated paths of wealth and optimal consumption lie within this interval indicated by the shaded area. The path volatility expresses how the risky asset investment affects wealth development and optimal consumption over time. As observed by the dynamics of optimal consumption under the classical strategy from 1, consumption is immediately influenced by the volatility in the financial market. This uncertainty might be undesirable to an investor who favors stability in consumption over time. Hence, the optimal investment portfolio in the classical strategy is too risky to comply with the preferences of this type of investor.

6.3. The First Approach of a Smooth Pension Product

Now, we illustrate the first approach of a smooth pension product, where consumption and investment portfolio are specified as (

60) and (

62), respectively. The developments of wealth and consumption are shown in

Figure 2. We examine the sensitivity of wealth and consumption to different values of the interest rate

in the annuity

.

By

Figure 2, we observe that the development of consumption under the first approach is less volatile than consumption under the classical strategy. The lower the value of

, the less volatility of consumption. This holds since the lower the value of

, the higher the value of

w. Thus, for lower values of

, we maintain a higher proportion of last year’s consumption level in calculating the current consumption level. At the same time, we observe that consumption under the first approach tends to consumption under the classical strategy as the value of

increases. This holds since the weight,

w, becomes small for higher values of

. By constructing consumption in the smooth pension product, consumption under the classical strategy takes over. Additionally, we observe a lower expected level of consumption for lower values of

. It is a compensation for maintaining a higher proportion of last year’s consumption level.

As we approach termination, the volatility of consumption increases. An explanation of this can be found in developing the investment portfolio under the first approach.

Unlike the classical strategy, the investment portfolio under the first approach of a smooth pension product is time-dependent.

Figure 3 visualizes the impact of different values of

on the investment portfolio. The investment portfolio has different initial values for different values of

: a lower value of

leads to a lower initial investment portfolio value. Thus, we invest less in risky assets to maintain a higher proportion of last year’s consumption.

Moreover, the investment portfolio is increasing and tending to the same value for the different values of

. The increasing development of the investment portfolio holds because the first approach is a special case of the hybrid strategy, where the optimal investment portfolio results from maximizing the expected utility of terminal wealth. However, by constructing consumption under the smooth pension product, we let the wealth go to zero as we reach expiry, which we observe by

Figure 2. The increasing investment portfolio is also why we keep increasing volatility in consumption over time.

At last, we substantiate the above analysis by illustrating the function

given by (

61) and the weights,

y and

w, defined by (

57) and (

58), respectively, for different values of

.

By

Figure 4, we only observe one graph of

y, since

y is independent of

. Thus, the graphs of

y for different values of

are indistinguishable. Note that the graph of

y is increasing over time and is rapidly closer to expiry such that the rest of the wealth is paid out by the construction of consumption under the smooth pension product.

The graphs of

w in

Figure 4 show that the weight decreases over time such that the standard market rate life annuity takes over as we reach expiry. For lower values of

, the higher the initial value of

w and vice versa. Thus, we maintain a higher proportion of last year’s consumption level for lower values of

. Conversely, the standard market rate life annuity is more dominant for higher values of

.

Moreover, the function

decreases rapidly through the entire decumulation phase. This contributes to the fact that we observe an increasing investment portfolio since the numerator decreases slower than the denominator by the structure of Equation (

62). Additionally, the lower the value of

, the higher the value of

. Thus, for higher values of

, we subtract a higher proportion of the current consumption level to determine the quantity invested in the risky asset. This dampens the risk taking at the beginning of the decumulation phase, as

Figure 3 shows.

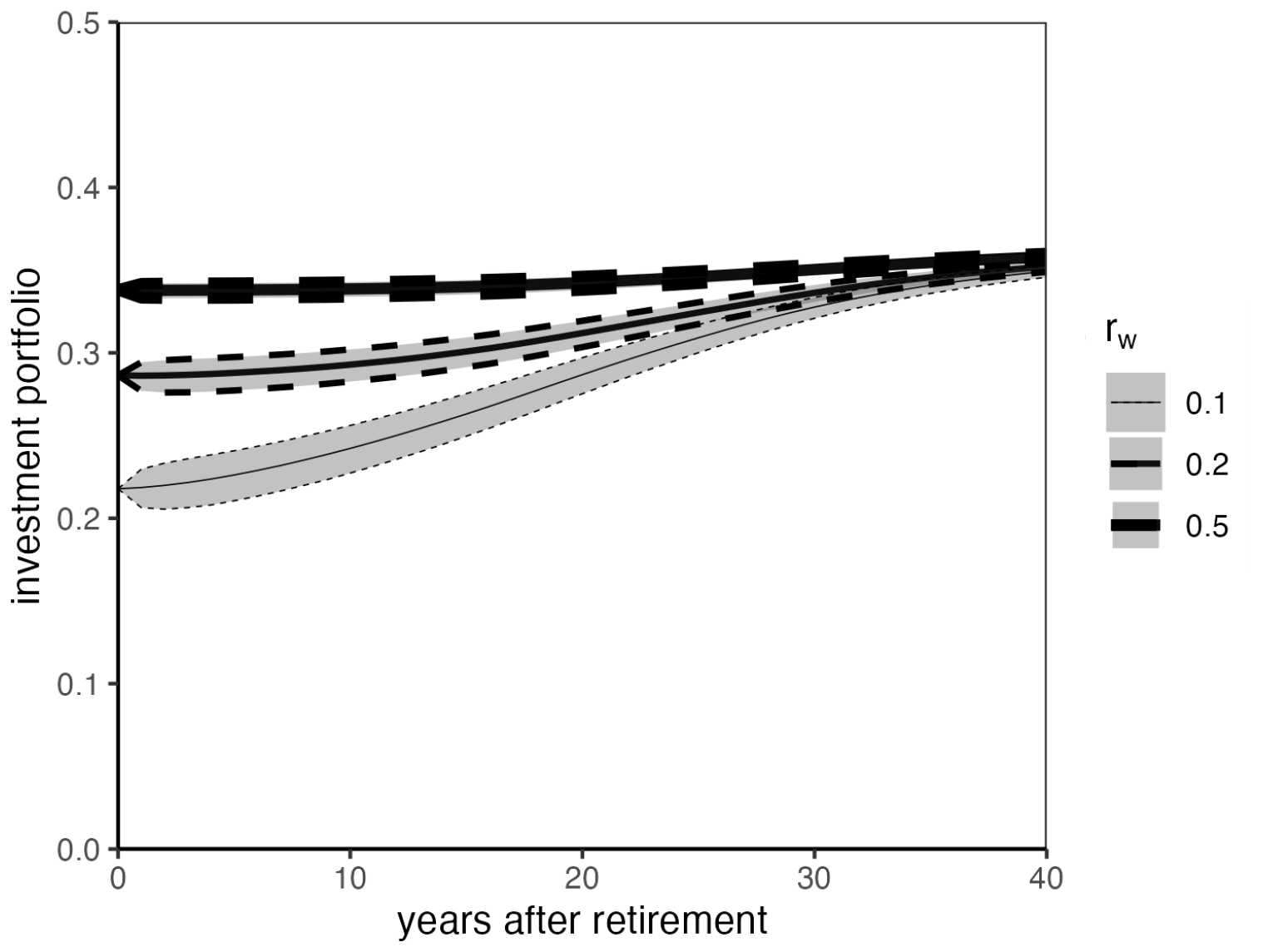

6.4. The Second Approach of a Smooth Pension Product

Next, we illustrate the second approach of a smooth pension product, where consumption and investment portfolio are defined by (

60) and (

63), respectively. The development of wealth and consumption is shown in

Figure 5. Again, we study the sensitivity of wealth and consumption to different values of the interest rate

in the annuity

.

By

Figure 5, we observe that the development of consumption under the second approach is less volatile than consumption under the classical strategy and consumption under the first approach. The same smoothing effect is reflected in wealth development under the second approach. Both wealth and consumption become less volatile for lower values of

. Note that consumption volatility increases at the beginning of the decumulation phase but stabilizes later in the decumulation phase. The stabilization of volatility happens sooner for lower values of

. This observation is supported by developing the investment portfolio under the second approach, as shown in

Figure 6.

As in the first approach, the investment portfolio of a smooth pension product under the second approach is time-dependent.

Figure 6 presents the impact of different values of

on the investment portfolio. Again, we observe different initial investment portfolio values for different values of

. In contrast to the first approach, we observe that the investment portfolio is decreasing over time, which explains the stabilization of volatility in

Figure 5. As opposed to both the first approach and the classical strategy, the quantity invested in the risky asset is smaller compared to the three graphs of the expected investment portfolio with the respective corresponding value of

. Hence, to obtain less consumption volatility, the risk appetite is reduced.

Finally, we assist the above analysis by considering the annuity

given by (

59), which is multiplied by the current consumption level and subtracted from the wealth in the investment portfolio under the second approach given by (

63). In

Figure 7, we present

and the weights,

y and

w, defined by (

57) and (

58), respectively, for different values of

.

Note that the graphs of the weights in

Figure 7 are identical to those in

Figure 4. This holds since the definition of consumption and the weights are similar under the two approaches. Thus, regarding the weights, the same analysis and interpretation remain as above.

Figure 7 shows that the graphs of the annuity

decrease over time. The higher the value of

, the higher the initial value of

. Thus, for lower values of

, we subtract a higher proportion, i.e.,

, of the current consumption level directly from the actual amount invested in the risky asset by the construction of the investment portfolio in the second approach given by (

63). As we subtract a proportion directly from the amount invested in the risky asset, the risk taking is dampened in the entire decumulation phase for all values of

as observed by

Figure 6. The value of

dictates how much the risk taking is dampened.

7. Conclusions

With inspiration from three strategies for consumption and investment, we have managed to design two approaches to a smooth pension product. The three strategies are the classical strategy, the habit strategy, and the hybrid strategy. Combining and modifying these strategies engenders the two approaches.

It turns out that optimal consumption under the classical strategy has the same structure as a standard market rate life annuity. Deriving the consumption dynamics under the classical and hybrid strategies, we observe that additive habit formation in preferences leads to the request for consumption stability. Comparing the consumption dynamics under the habit strategy and the hybrid strategy, we observe that the structures of the dynamics coincide. Hence, we deduce that the hybrid strategy meets the same preferences as the habit strategy. We wanted to understand these preferences to design a smooth pension product.

The objective of the smooth pension product is not to guarantee the same consumption level each year, but it is an attempt to smoothen the volatility of consumption. Moreover, we aim for a smooth pension product that is feasible, transparent, and fair from the perspective of both the investor and the pension company. Highly inspired by the consumption structure under the hybrid strategy, we let consumption be a weighted average of last year’s consumption level and consumption under the classical strategy, i.e., a hybrid between stability with respect to last year’s consumption level and a standard market rate life annuity. We let the weight be time-dependent such that the traditional market rate life annuity takes over as we reach termination. Hence, the pension company’s liabilities equal the investor’s wealth. Thus, we have obtained the smooth pension product’s feasibility, transparency, and fairness. Reconsidering and inspired by both the hybrid strategy and the habit strategy, we give two approaches for the investment portfolio of the smooth pension product.

The development of the wealth process is simulated under the classical strategy and the two approaches, respectively. Each simulation is repeated n = 100,000, and the time frame under the classical strategy is s, while it is s under the first approach and s under the second approach. The numerical examples show that consumption under the first and second approaches for the smooth pension product is less volatile than consumption under the classical strategy, i.e., a standard market rate life annuity. We see that consumption under the second approach is even less volatile than the first. An explanation for this result can be found in developing the investment portfolio under the respective approaches.

In the first approach, the quantity invested in the risky asset increases over time because the first approach is a special case of the hybrid strategy. The optimal investment portfolio under the hybrid strategy is found by maximizing the expected utility of terminal wealth. Thereby, we observe an increasing investment portfolio under the first approach.

The second approach is established to obtain an even simpler investment portfolio structure. It is inspired by the structure of the result obtained under the habit strategy with the expression of the habit level in terms of optimal consumption and wealth inserted.

For further research, we would study whether maximizing the expected utility of intertemporal consumption is possible given specified consumption dynamics when finding the optimal investment portfolio under the hybrid strategy. We claim that this changes the final result under the hybrid strategy.

We observed that the development of the investment portfolio impacts consumption volatility. Thus, we might have found the dynamics of the investment portfolio under the three strategies to increase the understanding of the development over time. Then, the influence of the different terms in the dynamics of the investment portfolio could be studied.

Finally, the investment portfolio under the second approach is low compared to the classical strategy. This is a result of smoothing the volatility of consumption. One might wonder whether the price of the smooth pension product is too high as the investor is dictated to take too low a risk. We need to avoid the smooth pension product becoming a guaranteed pension product. Thus, for further research, we could consider lower values of the risk aversion parameter such that the investment portfolio under the second approach is increased at the beginning of the decumulation phase but still decreasing over time such that the volatility of consumption is still smoothed over time. Hence, we aim to take enough risk over the entire decumulation phase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}