Energy-Extended CES Aggregate Production: Current Aspects of Their Specification and Econometric Estimation

Abstract

:1. Introduction

1.1. The Growing Use of CES Aggregate Production Functions

1.2. Adding Energy as a Factor of Production

1.3. Aim and Scope of Paper

2. Applications of C-D and CES Aggregate Production Functions

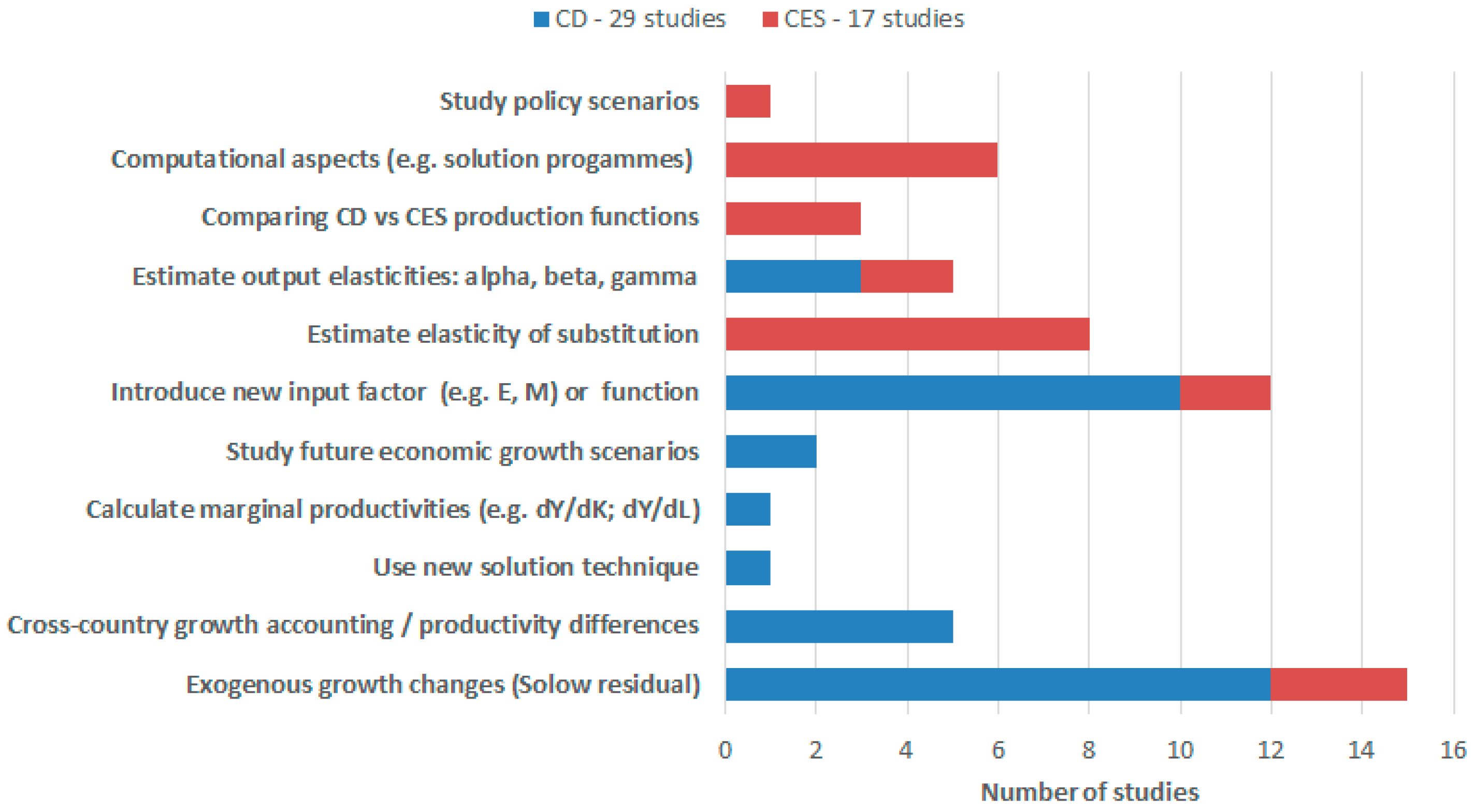

2.1. Sample Survey

2.2. Wider Literature Search

3. Empirical CES Model—Specification

3.1. Economic Output (Y)

3.2. Factors of Production (K, L, and E)

3.2.1. Unadjusted (Basic) Factors

3.2.2. Quality-Adjusted Factors

3.3. Nesting and Elasticity of Substitution

3.3.1. Nesting

3.3.2. Elasticity of Substitution, σ

Introspection tells us that the [inner-nest] elasticities of substitution should be substantially higher than the [outer-nest] elasticity. After all, we justify the aggregation by the fact that aggregated factors are similar in techno-economic characteristics. One of such similarities is obviously the ease of substitution.[164] (p. 203)

3.4. Other CES Function Parameters

3.4.1. Productivity/Technical Change Coefficients

3.4.2. Returns to Scale, (ν)

3.4.3. Output Share Parameters,

3.5. Normalisation

4. Empirical CES Model—Parameter Estimation

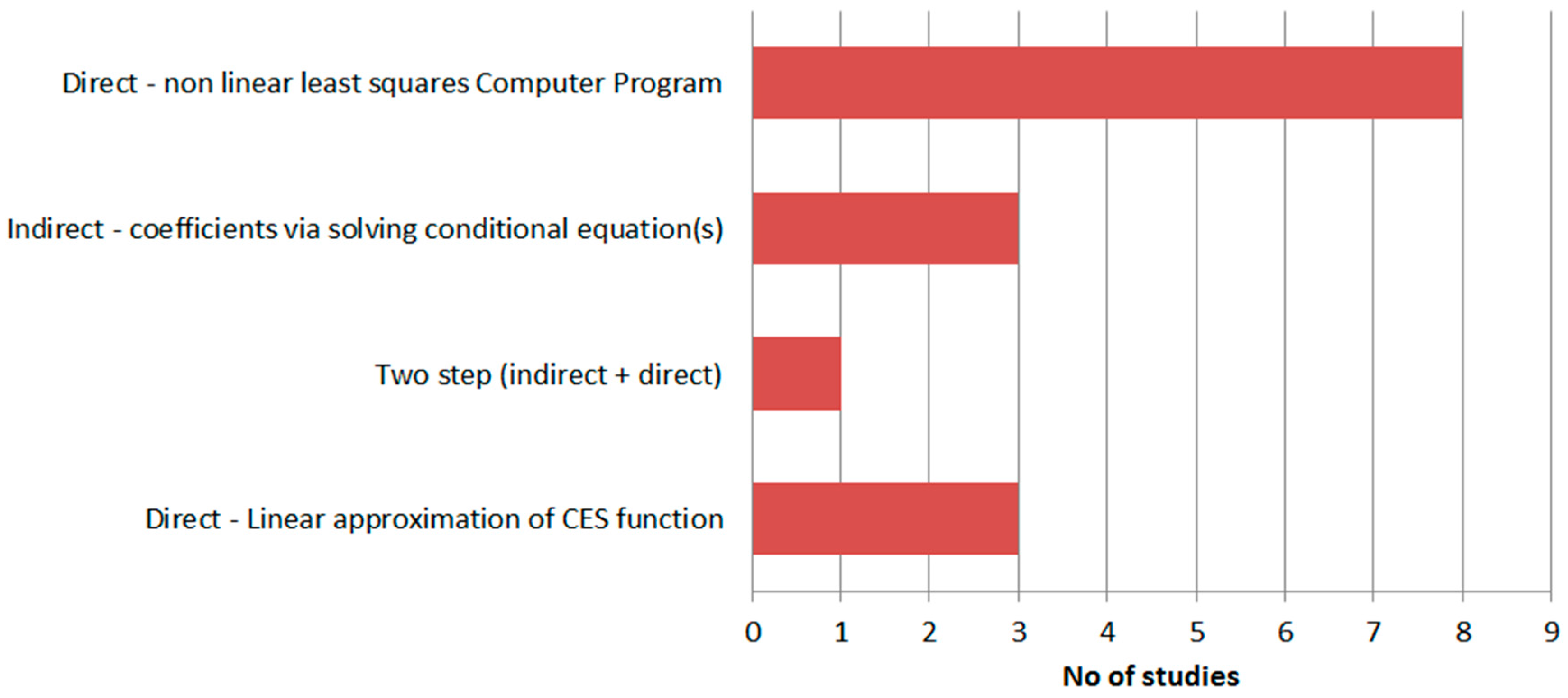

4.1. Estimation Methods

4.2. Statistical Reporting

5. Recommendations

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Dissou, Y.; Karnizova, L.; Sun, Q. Industry-level Econometric Estimates of Energy-capital-labour Substitution with a Nested CES Production Function. Altlantic Econ. J. 2012, 43, 107–121. [Google Scholar] [CrossRef]

- Smyth, R.; Kumar, P.; Shi, H. Substitution between energy and classical factor inputs in the Chinese steel sector. Appl. Energy 2011, 88, 361–367. [Google Scholar] [CrossRef]

- Solow, R.M. Technical Change and the Aggregate Production Function. Rev. Econ. Stat. 1957, 39, 312–320. [Google Scholar] [CrossRef]

- Nelson, R.R. Aggregate Production Functions and Medium-Range Growth Projections. Am. Econ. Rev. 1964, 54, 575–606. [Google Scholar]

- Kander, A.; Stern, D.I. Economic growth and the transition from traditional to modern energy in Sweden. Energy Econ. 2014, 46, 56–65. [Google Scholar] [CrossRef]

- Duffy, J.; Papageorgiou, C. A Cross-Country Empirical Investigation of the Aggregate Production Function Specification. J. Econ. Growth 2000, 5, 87–120. [Google Scholar] [CrossRef]

- Felipe, J.; Adams, F.G. A Theory of Production: The estimation of the Cobb-Douglas Function: A Retrospective View. East. Econ. J. 2005, 31, 427–445. [Google Scholar]

- Miller, E. An Assessment of CES and Cobb-Douglas Production Functions; US Congressional Budget Office Working Paper 2008–05; US Congressional Budget Office: Washington, DC, USA, 2008.

- Cobb, C.; Douglas, P. A theory of production. Am. Econ. Rev. 1928, 18, 139–165. [Google Scholar]

- Stern, D.I. Elasticities of substitution and complementarity. J. Prod. Anal. 2011, 36, 79–89. [Google Scholar] [CrossRef] [Green Version]

- Solow, R. A Contribution to the Theory of Economic Growth. Q. J. Econ. 1956, 70, 65–94. [Google Scholar] [CrossRef]

- Arrow, K.; Chenery, H.; Minhas, C.; Solow, R. Capital-Labor Substitution and Economic Efficiency. Rev. Econ. Stat. 1961, 43, 225–250. [Google Scholar] [CrossRef]

- Crafts, N. Solow and Growth Accounting: A Perspective from Quantitative Economics History. In Proceedings of the 20th Annual History of Political Economy Conference: Robert Solow and the Development of Growth, Urham, NC, USA, 25–27 April 2008.

- Denison, E.F. The Sources of Economic Growth in the United States and the Alternatives Before US; Supplementary Paper No 13; Committee for Economic Development: New York, NY, USA, 1962. [Google Scholar]

- Desai, P. Total factor productivity in postwar Soviet industry and its branches. J. Comp. Econ. 1985, 9, 1–23. [Google Scholar] [CrossRef]

- Chow, G.C.; Li, K.-W. China’s Economic Growth: 1952–2010. Econ. Dev. Cult. Chang. 2002, 51, 247–256. [Google Scholar] [CrossRef]

- Abramovitz, M. Resource and Output Trends in the United States since 1870; National Bureau of Economic Research: Cambridge, MA, USA, 1956; Volume 46, pp. 5–23. [Google Scholar]

- Hulten, C.R. Total Factor Productivity: A Short Biography. In New Developments in Productivity Analysis; Hulten, C.R., Dean, E.R., Harper, M.J., Eds.; University of Chicago Press: Chicago, IL, USA, 2001; pp. 1–55. [Google Scholar]

- Jorgenson, D.W.; Griliches, Z. The explanation of productivity change. Rev. Econ. Stud. 1967, 34, 249–283. [Google Scholar] [CrossRef]

- Denison, E.F. Accounting for Slower Economic Growth: The United States in the 1970’s; Brookings Institution Press: Washington, DC, USA, 1979. [Google Scholar]

- Hulten, C.R. Growth Accounting. National Bureau of Economic Research Working Paper 15341. 2009. Available online: http://www.nber.org/papers/w15341 (accessed on 8 February 2017).

- Rasch, R.H.; Tatom, J.A. Energy Resources and Potential GNP; Federal Reserve Bank of St Louis Review June 1977; Federal Reserve Bank: St. Louis, MO, USA, 1977; pp. 10–24. [Google Scholar]

- Renshaw, E.F. Energy efficiency and the slump in labour productivity in the USA. Energy Econ. 1981, 3, 36–42. [Google Scholar] [CrossRef]

- Berndt, E.R.; Wood, D.O. Technology, Prices and Derived Demand for Energy. Rev. Econ. Stud. Stat. 1975, 57, 259–268. [Google Scholar] [CrossRef]

- Van der Werf, E. Production functions for climate policy modeling: An empirical analysis. Energy Econ. 2008, 30, 2964–2979. [Google Scholar] [CrossRef]

- Zha, D.; Zhou, D. The elasticity of substitution and the way of nesting CES production function with emphasis on energy input. Appl. Energy 2014, 130, 793–798. [Google Scholar] [CrossRef]

- Stern, D.I. Energy and economic growth in the USA: A multivariate approach. Energy Econ. 1993, 15, 137–150. [Google Scholar] [CrossRef]

- Bruns, S.B.; Gross, C.; Stern, D.I. Is There Really Granger Causality Between Energy Use and Output? Energy J. 2014, 35, 101–134. [Google Scholar] [CrossRef] [Green Version]

- Kalimeris, P.; Richardson, C.; Bithas, K. A meta-analysis investigation of the direction of the energy-GDP causal relationship: Implications for the growth-degrowth dialogue. J. Clean. Prod. 2014, 67, 1–13. [Google Scholar] [CrossRef]

- Henningsen, A.; Henningsen, G. Econometric Estimation of the “Constant Elasticity of Substitution” Function in R: Package micEconCES; Institute of Food and Resource Economics, University of Copenhagen—FOI Working Paper 2011/9; University of Copenhagen: Copenhagen, Denmark, 2011. [Google Scholar]

- Saunders, H.D. Fuel conserving (and using) production functions. Energy Econ. 2008, 30, 2184–2235. [Google Scholar] [CrossRef]

- Klump, R.; Preissler, H. CES Production Functions and Economic Growth. Scand. J. Econ. 2000, 102, 41–56. [Google Scholar] [CrossRef]

- Shen, K.; Whalley, J. Capital-Labor-Energy Substitution in Nested CES Production Functions for China; NBER Working Paper 19104; National Bureau of Economic Research: Cambridge, MA, USA, 2013. [Google Scholar]

- Temple, J. The calibration of CES production functions. J. Macroecon. 2012, 34, 294–303. [Google Scholar] [CrossRef]

- Heun, M.K.; Santos, J.; Brockway, P.E.; Pruim, R.; Domingos, T. From theory to econometrics to energy policy: Cautionary tales for policymaking using aggregate production functions. Energies 2017, in press. [Google Scholar]

- Pavelescu, F. Some aspects of the translog production function estimation. Romanian J. Econ. 2011, 32, 131–150. [Google Scholar]

- Fare, R.; Yoon, B.J. Variable Elasticity of Substitution in Urban Housing Production. J. Urban Econ. 1981, 10, 369–374. [Google Scholar] [CrossRef]

- Warr, B.; Ayres, R.U. Useful work and information as drivers of economic growth. Ecol. Econ. 2012, 73, 93–102. [Google Scholar] [CrossRef]

- Thurston, N.K.; Libby, A.M. A Production Function for Physician Services Revisited. Rev. Econ. Stat. 2002, 84, 184–191. [Google Scholar] [CrossRef]

- Li, T.; Rosenman, R. Estimating Hospital Costs With a Generalised Leontief Function. Health Econ. 2001, 10, 523–538. [Google Scholar] [CrossRef] [PubMed]

- Bentzen, J. Estimating the rebound effect in US manufacturing energy consumption. Energy Econ. 2004, 26, 123–134. [Google Scholar] [CrossRef]

- Saunders, H.D. Historical evidence for energy efficiency rebound in 30 US sectors and a toolkit for rebound analysts. Technol. Forecast. Soc. Chang. 2013, 80, 1317–1330. [Google Scholar] [CrossRef]

- Adetutu, M.O. Energy efficiency and capital-energy substitutability: Evidence from four OPEC countries. Appl. Energy 2014, 119, 363–370. [Google Scholar] [CrossRef]

- Lecca, P.; Swales, K.; Turner, K. An investigation of issues relating to where energy should enter the production function. Econ. Model. 2011, 28, 2832–2841. [Google Scholar] [CrossRef]

- Hanley, N.; McGregor, P.G.; Swales, J.K.; Turner, K. Do increases in energy efficiency improve environmental quality and sustainability? Ecol. Econ. 2009, 68, 692–709. [Google Scholar] [CrossRef]

- Koesler, S.; Schymura, M. Substitution Elasticities in a CES Production Framework. An Empirical Analysis on the Basis of Non-Linear Least Squares Estimations; ZEW Discussion Paper No 12-007; ZEW: Mannheim, Germany, 2012. [Google Scholar]

- Punt, C.; Pauw, K.; van Schoor, M.; Gilimani, B.; Rantho, L.; McDonald, S.; Chant, L.; Valente, C. Functional Forms Used in CGE Models: Modelling Production and Commodity Flows; PROVIDE Project Background Paper; TMIP FMIP: Atlanta, GA, USA, 2003. [Google Scholar]

- Sajadifar, S.; Arakelyan, A.; Khiabani, N. The Linear Approximation of the CES Function to parameter estimation in CGE Modeling. In Proceedings of the International Conference on Business and Economics Research (ICBER), Kuala Lumpur, Malaysia, 26–28 Novemner 2010; pp. 1–10.

- Feldstein, M.S. Specification of the Labour Input in the Aggregate Production Function. Rev. Econ. Stud. 1967, 34, 375–386. [Google Scholar] [CrossRef]

- Fisk, P.R. The Estimation of Marginal Product from a Cobb-Douglas Production Function. Econometrica 1966, 34, 162–172. [Google Scholar] [CrossRef]

- Hayami, Y.; Ruttan, V.W. Agricultural Productivity Differences Among Countries. Am. Econ. Rev. 1970, 60, 895–911. [Google Scholar]

- Prais, Z. A new look at real money balances as a variable in the production function. J. Money Credit Bank. 1975, 7, 535–543. [Google Scholar] [CrossRef]

- Ulveling, E.; Fletcher, L. A Cobb-Douglas Production Function with Variable Returns to Scale. Am. J. Agric. Econ. 1970, 52, 322–326. [Google Scholar] [CrossRef]

- Uri, N.D. The impact of technical change on the aggregate production function. Appl. Econ. 1984, 16, 555–567. [Google Scholar] [CrossRef]

- Khan, A.H.A.; Ahmad, M. Real Money Balances in the Production Function of a Developing Country. Rev. Econ. Stat. 1985, 67, 336–340. [Google Scholar] [CrossRef]

- Mankiw, N.G.; Romer, D.; Weil, D.N. A Contribution to the Empirics of Economics Growth; NBER Working Paper No 3541; National Bureau of Economic Research: Cambridge, MA, USA, 1990. [Google Scholar]

- Finn, M.G. Variance properties of Solow’s productivity residual and their cyclical implications. J. Econ. Dyn. Control 1995, 19, 1249–1281. [Google Scholar] [CrossRef]

- Dougherty, C.; Jorgenson, D.W. International Comparisons of the Sources of Economic Growth. Am. Econ. Rev. 1996, 86, 25–29. [Google Scholar]

- Kalirajan, K.P.; Obwona, M.B.; Zhao, S. A Decomposition of Total Factor Productivity Growth: The Case of Chinese Agricultural Growth before and after Reforms. Am. J. Agric. Econ. 1996, 78, 331–338. [Google Scholar] [CrossRef]

- Hall, R.E.; Jones, C.I. Why do some countries produce so much more output per worker than others? Q. J. Econ. 1999, 114, 83–116. [Google Scholar] [CrossRef]

- Garcia-Milà, T.; McGuire, T.J. The contribution of publicly provided inputs to states’ economies. Reg. Sci. Urban Econ. 1992, 22, 229–241. [Google Scholar] [CrossRef]

- Kalaitzidakis, P.; Korniotiis, G. The Solow growth model: Vector autoregression (VAR) and cross-section times-series. Appl. Econ. 2000, 32, 737–747. [Google Scholar] [CrossRef]

- Caselli, F. Accounting for Cross-Country Income Differences; Centre for Economic Performance CEP Discussion Paper No 667; Working Paper of Centre for Economic Performance: London, UK, 2005; pp. 1–69. [Google Scholar]

- Vouvaki, D.; Xepapadeas, A. Total Factor Productivity Growth when Factors of Production Generate Environmental Externalities; Munich Personal RePEc Archive—MPRA Paper No 10237; Munich Personal RePEc Archive: Munich, Germany, 2008; pp. 1–31. [Google Scholar]

- Autor, D.H.; Katz, L.F.; Kearney, M.S. The Polarization of the U.S. Labor Market; National Bureau of Economic Research Working Paper 11986; National Bureau of Economic Research: Cambridge, MA, USA, 2006; Available online: http://www.nber.org/papers/w11986 (accessed on 8 February 2017).

- Martin, W.; Mitra, D. Productivity Growth and Convergence in Agriculture versus Manufacturing. Econ. Dev. Cult. Chang. 2001, 49, 403–422. [Google Scholar] [CrossRef]

- Fernald, J.; Neiman, B. Growth Accounting with Misallocation: Or, Doing Less with More in Singapore; Federal Reserve Bank of San Francisco Working Paper 2010–18; Federal Reserve Bank of San Francisco: San Francisco, CA, USA, 2010; pp. 1–49. [Google Scholar]

- Long, K.; Franklin, M. Multi–factor productivity: Estimates for 1994–2008. Econ. Labour Mark. Rev. 2010, 4, 67–72. [Google Scholar] [CrossRef]

- Hájková, D.; Hurník, J. Cobb-Douglas production function: The case of a converging economy. Czech J. Econ. Financ. 2007, 57, 465–476. [Google Scholar]

- Yuan, C.; Liu, S.; Wu, J. Research on energy-saving effect of technological progress based on Cobb-Douglas production function. Energy Policy 2009, 37, 2842–2846. [Google Scholar] [CrossRef]

- The Conference Board. Projecting Global Growth; Economics Working Papers, EPWP #12-02; The Conference Board: New York, NY, USA, 2012. [Google Scholar]

- Daude, C. Understanding Solow Residuals in Latin America. Economia 2014, 13, 109–138. [Google Scholar]

- Kotowitz, Y. Capital-Labour Substitution in Canadian Manufacturing 1926–1939 and 1946–1961. Can. J. Econ. 1968, 1, 619–632. [Google Scholar] [CrossRef]

- Zarembka, P. On the empirical relevance of CES Production Function. Rev. Econ. Stat. 1970, 52, 47–53. [Google Scholar] [CrossRef]

- O’Donnell, A.T.; Swales, J.K. Factor Substitution, the C.E.S. Production Function and U.K. Regional Economics. Oxf. Econ. Pap. 1979, 31, 460–476. [Google Scholar]

- Desai, P.; Martin, R. Efficiency Loss From Resource Misallocation in Soviet Industry. Q. J. Econ. 1983, 98, 441–456. [Google Scholar] [CrossRef]

- Rusek, A. Industrial Growth in Czechoslovakia 1971–1985: Total Factor Productivity and Capital-Labor Substitution. J. Comp. Econ. 1989, 13, 301–313. [Google Scholar] [CrossRef]

- Easterly, W.; Fischer, S. The soviet economic decline. World Bank Econ. Rev. 1995, 9, 341–371. [Google Scholar] [CrossRef]

- Kemfert, C. Estimated substitution elasticities of a nested CES production function approach for Germany. Energy Econ. 1998, 20, 249–264. [Google Scholar] [CrossRef]

- Gohin, A.; Hertel, T. A note on the CES Functional form and Its Use in the GTAP model. GTAP Research Memorandum No. 2. 2001. Available online: https://www.gtap.agecon.purdue.edu/resources/download/1610.pdf (accessed on 8 February 2017).

- Bonga-Bonga, L. The South African Aggregate Production Function: Estimation of the Constant Elasticity of Substitution Function. S. Afr. J. Econ. 2009, 77, 332–349. [Google Scholar] [CrossRef]

- Szeto, K.L. An Econometric Analysis of a Production Function for New Zealand; New Zealand Treasury Working Paper 01/31; New Zealand Treasury: Wellington, New Zealand, 2001. [Google Scholar]

- Kemfert, C.; Welsch, H. Energy-Capital-Labor Substitution and the Economic Effects of CO2 Abatement. J. Policy Model. 2000, 22, 641–660. [Google Scholar] [CrossRef]

- Cantore, C.; Levine, P.; Yang, B. CES Technology and Business Cycle Fluctuations; University of Surrey Discussion papers 2014/DP04–14; University of Surrey: Guildford, UK, 2014. [Google Scholar]

- Wang, Y. Estimating CES Aggregate Production Functions of China and India. In Proceedings of the 4th World Conference Applied Economics and Business Development (AEBD), Porto, Portugal, 1–3 July 2012.

- Capalbo, S.M.; Denny, M.G.S. Testing Long-Run Productivity Models for the Canadian and U.S. Agricultural Sectors. Am. J. Agric. Econ. 1986, 68, 615–625. [Google Scholar] [CrossRef]

- Binswanger, H.C.; Ledergerber, E. Bremsung des Energiezuwachses als Mittel der Wachstumskontrolle; Wirtschaftspolitik in der Umweltkrise; DVA: Stuttgart, Germany, 1974; pp. 103–125. [Google Scholar]

- Dale, M.; Krumdieck, S.; Bodger, P. Global energy modelling—A biophysical approach (GEMBA) Part 1: An overview of biophysical economics. Ecol. Econ. 2012, 73, 152–157. [Google Scholar] [CrossRef]

- Dale, M.; Krumdieck, S.; Bodger, P. Global energy modelling—A biophysical approach (GEMBA) Part 2: Methodology. Ecol. Econ. 2012, 73, 158–167. [Google Scholar] [CrossRef]

- Stern, D.I. The role of energy in economic growth. Ann. N. Y. Acad. Sci. 2011, 1219, 26–51. [Google Scholar] [CrossRef] [PubMed]

- Kümmel, R. The impact of energy on industrial growth. Energy 1982, 7, 189–203. [Google Scholar] [CrossRef]

- US Energy Information Administration (US EIA). Energy Consumption, Expenditures, and Emissions Indicators Estimates, Selected Years, 1949–2011 [Internet]. US Energy Information Administration: Annual Energy Review 2011; 2011. Available online: http://www.eia.gov/totalenergy/data/annual/pdf/sec1_13.pdf (accessed on 8 February 2017). [Google Scholar]

- Platchkov, L.M.; Pollitt, M.G. The Economics of Energy (and Electricity) Demand; Electricity Policy Research Group University of Cambridge (EPRG) Working Paper 1116; University of Cambridge: Cambridge, UK, 2011. [Google Scholar]

- Stresing, R.; Lindenberger, D.; Kümmel, R. Cointegration of output, capital, labor, and energy. Eur. Phys. J. B 2008, 14, 279–287. [Google Scholar] [CrossRef]

- Aucott, M.; Hall, C. Does a Change in Price of Fuel Affect GDP Growth? An Examination of the U.S. Data from 1950–2013. Energies 2014, 7, 6558–6570. [Google Scholar] [CrossRef]

- Mishra, S.K. A Brief History of Production Functions. IUP J. Manag. Econ. 2010, VIII, 6–34. [Google Scholar] [CrossRef]

- Shaikh, A. Laws of Production and Laws of Algebra: The Humbug Production Function. Rev. Econ. Stat. 1974, 56, 115–120. [Google Scholar] [CrossRef]

- Felipe, J.; Holz, C.A. Why do Aggregate Production Functions Work? Fisher’s simulations, Shaikh’s identity and some new results. Int. Rev. Appl. Econ. 2001, 15, 261–285. [Google Scholar] [CrossRef]

- Felipe, J.; McCombie, J.S.L. The CES Production Function, the accounting identity, and Occam’s razor. Appl. Econ. 2001, 33, 1221–1232. [Google Scholar] [CrossRef]

- Robinson, J. The Production Function and the Theory of Capital. Rev. Econ. Stud. 1953, 21, 81–106. [Google Scholar] [CrossRef]

- Fisher, F.M. The Existence of Aggregate Production Functions. Econometrica 1969, 37, 553–577. [Google Scholar] [CrossRef]

- Felipe, J.; McCombie, J.S.L. What is wrong with aggregate production functions. On Temple’s “aggregate production functions and growth economics”. Int. Rev. Appl. Econ. 2010, 24, 665–684. [Google Scholar] [CrossRef]

- Felipe, J.; McCombie, J.S.L. The Aggregate Production Function: “Not Even Wrong.”. Rev. Political Econ. 2014, 26, 60–84. [Google Scholar] [CrossRef]

- Felipe, J.; Fisher, F.M. Aggregation in Production Functions: What Applied Economists should know. Metroeconomica 2003, 54, 208–262. [Google Scholar] [CrossRef]

- Ravel, D. Estimation of a CES Production Function with Factor Augmenting Technology; US Center for Economic Studies (CES) Working Paper 11-05; U.S. Census Bureau: Washing DC, USA, 2011; pp. 1–58.

- Groth, B.C.; Gutierrez-domenech, M.; Srinivasan, S. Measuring Total Factor Productivity for the United Kingdom; Bank of England Quarterly Bulletin: London, UK, 2004; pp. 63–73. [Google Scholar]

- Baier, S.L.; Dwyer, G.P., Jr.; Tamura, R. How Important Are Capital and Total Factor Productivity for Economic Growth? Working Paper 2002-2a; Federal Bank Reserve of Atlanta: Atlanta, GA, USA, 2002. [Google Scholar]

- Klump, R.; Mcadam, P.; Willman, A. The Normalised CES Production Function: Theory and Empirics; European Central Bank Working Paper 1294; European Central Bank: Frankfurt, Germany, 2011. [Google Scholar]

- Growiec, J. On the Measurement of Technological Progress Across Countries; National Bank of Poland Working Paper No73; National Bank of Poland: Warszawa, Poland, 2010. [Google Scholar]

- Saunders, H.D. Recent Evidence for Large Rebound: Elucidating the Drivers and their Implications for Climate Change Models. Energy J. 2015, 36, 23–48. [Google Scholar] [CrossRef]

- Wei, T. Impact of energy efficiency gains on output and energy use with Cobb–Douglas production function. Energy Policy 2007, 35, 2023–2030. [Google Scholar] [CrossRef]

- Fröling, M. Energy use, population and growth, 1800–1970. J. Popul. Econ. 2011, 24, 1133–1163. [Google Scholar] [CrossRef]

- Lu, Y.; Stern, D.I. Substitutability and the Cost of Climate Mitigation Policy. Energy Procedia 2014, 61, 1622–1625. [Google Scholar] [CrossRef]

- Chirinko, R.S. Sigma: The long and short of it. J. Macroecon. 2008, 30, 671–686. [Google Scholar] [CrossRef]

- Palivos, T. Comment on “Sigma: The long and short of it”. J. Macroecon. 2008, 30, 687–690. [Google Scholar] [CrossRef]

- Turner, K. Negative rebound and disinvestment effects in response to an improvement in energy efficiency in the UK economy. Energy Econ. 2009, 31, 648–666. [Google Scholar] [CrossRef]

- Bor, Y.J.; Huang, Y. Energy taxation and the double dividend effect in Taiwan’s energy conservation policy-an empirical study using a computable general equilibrium model. Energy Policy 2010, 38, 2086–2100. [Google Scholar] [CrossRef]

- Sancho, F. Calibration of CES Functions for Real-World Multisectoral Modeling. Econ. Syst. Res. 2009, 21, 45–58. [Google Scholar] [CrossRef]

- Annabi, N.; Cockburn, J.; Decaluwe, B. Functional Forms and Parametrization. MPIA Working Paper 2006-04. 2006. Available online: https://ssrn.com/abstract=897758 (accessed on 8 February 2017).

- Sanchez, C. Calibration, Solution and Validation of the CGE Model. In Rising Inequality and Falling Poverty in Costa Rica’s Agriculture during Trade Reform A Macro-Micro General Equilibrium Analysis; Shaker: Maastrict, The Netherlands, 2004; Chapter 7; pp. 189–226. [Google Scholar]

- Klump, R.; Saam, M. Calibration of Normalised CES Production Functions in Dynamic Models; ZEW Discussion Paper No 06-078; ZEW: Mannheim, Germany, 2006. [Google Scholar]

- Hulten, C.R. Accounting for the Wealth of Nations: The Net versus Gross Output Controversy and Its Ramifications. Scand. J. Econ. 1992, 94, S9–S24. [Google Scholar] [CrossRef]

- Cobbold, T. A Comparison of Gross Output and Value-Added Methods of Productivity Estimation; Australian Government Productivity Commission: Canberra, Australia, 2003.

- Inklaar, R.; Timmer, M.P. Capital, Labor and TFP in PWT8.0; Groningen Growth and Development Centre—Technical Report; University of Groningen: Groningen, The Netherlands, 2013; pp. 1–38. [Google Scholar]

- O’Mahony, M.; Timmer, M.P. Output, input and productivity measures at the industry level: The EU KLEMS database. Econ. J. 2009, 119, 374–403. [Google Scholar] [CrossRef]

- Kander, A.; Stern, D.I. Economic Growth and the Transition from Traditional to Modern Energy in Sweden; Centre for Applied Macroeconomic Analysis (CAMA) Working Paper 65/2013; Centre for Applied Macroeconomic Analysis: Canberra, Australia, 2013. [Google Scholar]

- Turner, K.; Lange, I.; Lecca, P.; Soo, J.H. Econometric Estimation of Nested Production Functions and Testing in a Computable General Equilibrium Analysis of Economy-Wide Rebound Effects. USAEE Working Paper No. 2054122. 2012, pp. 1–26. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2054122 (accessed on 8 February 2017).

- Sun, Q. Technology Change for a Two-Level CES Production Function: An Empirical Study for Canada; University of Ottawa: Ottawa, ON, Canada, 2012. [Google Scholar]

- Liddle, B. OECD energy intensity. Energy Effic. 2012, 27, 583–597. [Google Scholar] [CrossRef]

- Steinberger, J.K.; Krausmann, F.; Eisenmenger, N. Global patterns of materials use: A socioeconomic and geophysical analysis. Ecol. Econ. 2010, 69, 1148–1158. [Google Scholar] [CrossRef]

- (ONS) UK Office of National Statistics. Statistical Bulletin: Capital Stocks, Consumption of Fixed Capital, 2014 [Internet]. 2014. Available online: http://www.ons.gov.uk/ons/rel/cap-stock/capital-stock--capital-consumption/capital-stocks-and-consumption-of-fixed-capital--2013/stb---capital-stocks.html?format=print (accessed on 8 February 2017). [Google Scholar]

- Schreyer, P.; Dupont, J.; Koh, S.-H.; Webb, C. Capital Stock Data at the OECD—Status and Outlook; OECD: Paris, France, 2011. Available online: http://www.oecd.org/std/productivity-stats/48490768.doc (accessed on 8 February 2017).

- Schreyer, P. Capital Stocks, Capital Services and Multi-factor Productivity Measures; OECD Economic Studies; OECD: Paris, France, 2004; pp. 163–184. [Google Scholar]

- International Energy Agency (IEA). “Extended world energy balances”, IEA World Energy Statistics and Balances (database) [Internet]. 2013. Available online: http://www.oecd-ilibrary.org/energy/data/iea-world-energy-statistics-and-balances/extended-world-energy-balances_data-00513-en (accessed on 8 February 2017).

- Feenstra, R.C.; Inklaar, R.; Timmer, M.P. Penn World Tables 8.1 [Internet]. 2015. Available online: http://www.rug.nl/research/ggdc/data/pwt/pwt-8.1 (accessed on 8 February 2017).

- British Petroleum (BP) Ltd. Statistical Review of World Energy 2014 BP World Energy Review (2014). Available online: http://www.bp.com/content/dam/bp-country/de_de/PDFs/brochures/BP-statistical-review-of-world-energy-2014-full-report.pdf (accessed on 8 February 2017).

- Department for Business, Energy & Industrial Strategy (BEIS). Energy Consumption in the UK: 2013 update [Internet]. 2013. Available online: https://www.gov.uk/government/collections/energy-consumption-in-the-uk (accessed on 8 February 2017). [Google Scholar]

- Schreyer, P.; Bignon, P.; Dupont, J. OECD Capital Services Estimates: Methodology and a First Set of Results; OECD Statistics Working papers, 2003/06; OECD Publishing: Paris, France, 2003. [Google Scholar]

- Wallis, G.; Oulton, N. Integrated Estimates of Capital Stocks and Services for the United Kingdom: 1950–2013. In Proceedings of the IARIW 33rd General Conference, Rotterdam, The Netherlands, 24–30 August 2014.

- Paquet, A.; Robidoux, B. Issues on the measurement of the Solow residual and the testing of its exogeneity: Evidence for Canada. J. Monet. Econ. 2001, 47, 595–612. [Google Scholar] [CrossRef]

- Barro, R.; Lee, J. International data on educational attainment: Updates and implications. Oxf. Econ. Pap. 2001, 53, 541–563. [Google Scholar] [CrossRef]

- Nilsen, Ø.A.; Raknerud, A.; Rybalka, M.; Skjerpen, T. The importance of skill measurement for growth accounting. Rev. Income Wealth 2011, 57, 293–305. [Google Scholar] [CrossRef]

- Cleveland, C.J.; Kaufmann, R.K.; Stern, D.I. Aggregation and the role of energy in the economy. Ecol. Econ. 2000, 32, 301–317. [Google Scholar] [CrossRef]

- Ayres, R.U.; Warr, B. Accounting for growth: The role of physical work. Struct. Chang. Econ. Dyn. 2005, 16, 181–209. [Google Scholar] [CrossRef]

- Stern, D.I. Energy quality. Ecol. Econ. 2010, 69, 1471–1478. [Google Scholar] [CrossRef]

- Warr, B.; Ayres, R.; Eisenmenger, N.; Krausmann, F.; Schandl, H. Energy use and economic development: A comparative analysis of useful work supply in Austria, Japan, the United Kingdom and the US during 100 years of economic growth. Ecol. Econ. 2010, 69, 1904–1917. [Google Scholar] [CrossRef]

- Inklaar, R. The sensitivity of capital services measurement: Measure all assets and the cost of capital. Rev. Income Wealth 2010, 56, 389–412. [Google Scholar] [CrossRef]

- Berndt, E.R. Energy use, technical progress and productivity growth: A survey of economic issues. J. Prod. Anal. 1990, 2, 67–83. [Google Scholar] [CrossRef]

- Warr, B.S.; Ayres, R.U. Evidence of causality between the quantity and quality of energy consumption and economic growth. Energy 2010, 35, 1688–1693. [Google Scholar] [CrossRef]

- Burda, M.C.; Severgnini, B. Solow residuals without capital stocks. J. Dev. Econ. 2014, 109, 154–171. [Google Scholar] [CrossRef]

- Prywes, M. A nested CES approach to capital-energy substitution. Energy Econ. 1986, 8, 22–28. [Google Scholar] [CrossRef]

- Mcfadden, D. Constant Elasticity of Substitution Production Functions. Rev. Econ. Stud. 1963, 30, 73–83. [Google Scholar] [CrossRef]

- Edenhofer, O.; Bauer, N.; Kriegler, E. The impact of technological change on climate protection and welfare: Insights from the model MIND. Ecol. Econ. 2005, 54, 277–292. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Hunt, L.; Sorrell, S. Review of Evidence for the Rebound Effect Technical Report 3: Elasticity of Substitution Studies; UKERC Working Paper UKERC/WP/TPA/2007/011; UKERC: London, UK, 2007. [Google Scholar]

- Chirinko, R.S.; Mallick, D. The Substitution Elasticity, Factor Shares, Long-Run Growth, and the Low-Frequency Panel Model. CESifo Working Paper No. 4895. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2479816 (accessed on 8 February 2017).

- Mallick, D. The role of the elasticity of substitution in economic growth: A cross-country investigation. Labour Econ. 2012, 19, 682–694. [Google Scholar] [CrossRef]

- Piketty, T. Capital in the Twenty-First Century; Harvard: Cambridge, MA, USA; London, UK, 2014. [Google Scholar]

- Rognlie, M. A Note on Piketty and Diminishing Returns to Capital. 2014. Available online: http://www.conta-conta.ro/economisti/Thomas_Piketty_file%2030_.pdf (accessed on 8 February 2017).

- Rowthorn, R. A Note on Thomas Piketty’s Capital in the Twenty-First Century. 2014. Available online: http://tcf.org/assets/downloads/A_Note_on_Thomas_Piketty3.pdf (accessed on 8 February 2017).

- Semieniuk, G. Piketty’s Elasticity of Substitution: A Critique; Schwartz Center for Economic Policy Analysis and Department of Economics, The New School for Social Research, Working Paper 2014-8; The New School: New York, NY, USA, 2014. [Google Scholar]

- Klump, R.; de la Grandville, O. Economic growth and the elasticity of substitution: Two theorems and some suggestions. Am. Econ. Rev. 2000, 90, 282–291. [Google Scholar] [CrossRef]

- Blackorby, C.; Russell, R.R.R. Will the Real Elasticity of Substitution Please Stand Up? (A Comparison of the Allen/Uzawa and Morishima Elasticities). Am. Econ. Rev. 1989, 79, 882–888. [Google Scholar]

- Sorrell, S. Energy Substitution, Technical Change and Rebound Effects. Energies 2014, 29, 2850–2873. [Google Scholar] [CrossRef]

- Sato, K. A Two-Level Constant-Elasticity-of-Substitution Production Function. Rev. Econ. Stud. 1967, 34, 201–218. [Google Scholar] [CrossRef]

- Hogan, W.W.; Manne, A.S. Energy-Economy Interactions: The Fable of the Elephant and the Rabbit? Working EMF Report 1 of the Energy Modeling Forum (Stanford University); Stanford University: Stanford, CA, USA, 1977. [Google Scholar]

- Bosetti, V.; Carraro, C.; Galeotti, M.; Massetti, E.; Tavoni, M. WITCH: A World Induced Technical Change Hybrid Model; Working Paper Department of Economics University of Venice No 46/WP/2006; Department of Economics University of Venice: Venezia, Italy, 2007. [Google Scholar]

- Manne, A.; Mendelsohn, R.; Richels, R. MERGE: A model for evaluating regional and global effects of GHG reduction policies. Energy Policy 1995, 23, 17–34. [Google Scholar] [CrossRef]

- Jacoby, H.D.; Reilly, J.M.; McFarland, J.R.; Paltsev, S. Technology and technical change in the MIT EPPA model. Energy Econ. 2006, 28, 610–631. [Google Scholar] [CrossRef]

- Saunders, H.D. The Khazzoom-Brookes Postulate and Neoclassical Growth. Energy J. 1992, 13, 131–148. [Google Scholar] [CrossRef]

- Hannon, B.; Joyce, J. Energy and technical progress. Energy 1981, 6, 187–195. [Google Scholar] [CrossRef]

- Papageorgiou, C.; Saam, M.; Schulte, P. Substitution between Clean and Dirty Energy Inputs—A Macroeconomic Perspective; International Monetary Fund Working Paper; International Monetary Fund: Washington, DC, USA, 2015. [Google Scholar]

- Layson, S.K. The Increasing Returns to Scale CES Production Function and the Law of Diminishing Marginal Returns. South. Econ. J. 2015, 82, 408–415. [Google Scholar] [CrossRef]

- De La Grandville, O.; Solow, R.M. Capital-labour substitution and economic growth. In Economic Growth: A Unified Approach; Cambridge University Press: Cambridge, UK, 2009; Chapter 5. [Google Scholar]

- Jorgenson, D.W. Econometrics (Volume 1): Econometric Modeling of Producer Behavior; The MIT Press: Cambridge, MA, USA, 2000. [Google Scholar]

- Greene, W. Nonlinear, semiparametric and nonparametric regression models. In Econometric Analysis, 7th ed.; Pearson Prentice Hall: Madrid, Spain, 2010; Chapter 7. [Google Scholar]

- Henningsen, A.; Henningsen, G. On estimation of the CES production function-Revisited. Econ. Lett. 2012, 115, 67–69. [Google Scholar] [CrossRef] [Green Version]

- Nerlove, M. Recent empirical studies of the CES and related production function. In The Theory and Empirical Analysis of Production; Brown, M., Ed.; NBER and Columbia University Press: New York, NY, USA, 1967. [Google Scholar]

- Kmenta, J. On Estimation of the CES Production Function. Int. Econ. Rev. 1967, 8, 180–189. [Google Scholar] [CrossRef]

- Mundlak, Y. Elasticity of substitution and the theory of derived demand. Rev. Econ. Stud. 1968, 35, 225–236. [Google Scholar] [CrossRef]

- Caballero, R.J. Small sample bias and adjustment costs. Rev. Econ. Stat. 1994, 76, 52–58. [Google Scholar] [CrossRef]

- Chirinko, R.S.; Fazzari, S.; Meyer, A. That Elusive Elasticity: A Long-Panel Approach to Estimating the Capital-Labor Substitution Elasticity; CESIFO Working Paper No. 1240; CESIFO Group: Munich, Germany, 2004; Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=573246 (accessed on 8 February 2017).

- Giraud, G. How Dependent is Growth from Primary Energy? The Dependency ratio of Energy in 33 Countries. Centre d’Economie de la Sorbonne CES Working Paper 201497. 2014, pp. 1–26. Available online: http://econpapers.repec.org/paper/msecesdoc/14097.htm (accessed on 8 February 2017).

- Barro, R.; Lee, J.-W. Barro-Lee Educational Attainment Dataset v2.0 [Internet]. 2014. Available online: http://www.barrolee.com/ (accessed on 8 February 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author/Study | Year | Energy Measure | Output Measure |

|---|---|---|---|

| Kemfert [79] | 1998 | Final energy | GVA |

| Kemfert and Welsch [83] | 2000 | Final energy | GVA |

| Van der Werf [25] | 2008 | Final energy | GVA + energy cost |

| Koesler and Schymura [46] | 2012 | Final energy | Gross Output |

| Turner et al. [127] | 2012 | Final energy | Gross Output |

| Dissou et al. [1] | 2012 | Final energy | Industry GVA |

| Sun [128] | 2012 | Final energy | GVA + energy cost |

| Kander and Stern [5] | 2014 | Primary energy | GVA + energy cost |

| Shen and Whalley [33] | 2014 | Primary energy | GDP |

| Zha and Zhou [26] | 2014 | Final energy | Not stated |

| Section | Aspect | Options | Recommendation |

|---|---|---|---|

| Section 3.1 | Output measure, Y |

| “Modified” gross output metric, measured as GVA + value of intermediate inputs (i.e., GVA + cost of energy). |

| Section 3.2.2 | Quality-adjusted inputs |

| Yes, quality-adjust where possible.

|

| Section 3.3 | Nesting |

| Estimate and report parameters for all three nesting options. |

| Section 3.3 | Substitution parameters, ρ |

| Estimate unconstrained parameters first. Then re-estimate (for comparison) with constrained substitution parameters. |

| Section 3.4.1 | Technical change parameters τL τK τE |

| Introduce if values are known/available, but be wary of conflict with quality-adjusted input data. |

| Section 3.4.2 | Returns-to-scale ν |

| Estimate unconstrained parameters first. Then re-estimate (for comparison) with constant returns-to-scale (ν = 1) parameter. |

| Section 3.4.3 | Share parameters, δ |

| Estimate function parameters with constrained (between 0 and 1) share parameters. Exact values to be determined by the estimation process. |

| Section 3.5 | Normalisation of Y, K, L, E | Normalise or not | Always normalize for three factor CES functions. |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Brockway, P.E.; Heun, M.K.; Santos, J.; Barrett, J.R. Energy-Extended CES Aggregate Production: Current Aspects of Their Specification and Econometric Estimation. Energies 2017, 10, 202. https://doi.org/10.3390/en10020202

Brockway PE, Heun MK, Santos J, Barrett JR. Energy-Extended CES Aggregate Production: Current Aspects of Their Specification and Econometric Estimation. Energies. 2017; 10(2):202. https://doi.org/10.3390/en10020202

Chicago/Turabian StyleBrockway, Paul E., Matthew K. Heun, João Santos, and John R. Barrett. 2017. "Energy-Extended CES Aggregate Production: Current Aspects of Their Specification and Econometric Estimation" Energies 10, no. 2: 202. https://doi.org/10.3390/en10020202