Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries

Abstract

:1. Introduction

2. Literature Review

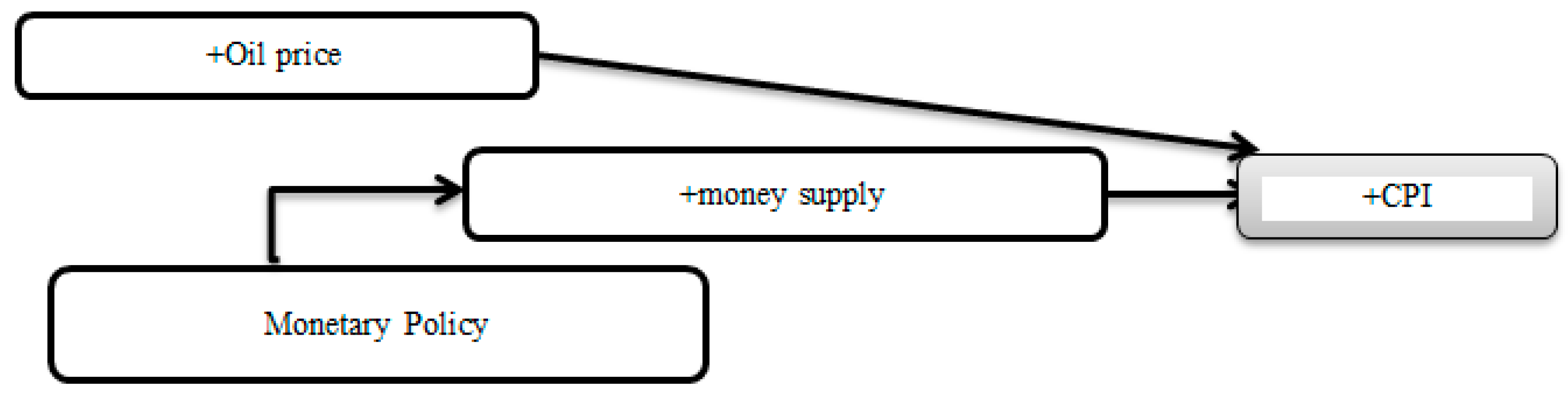

3. Theoretical Framework

4. Methodology, Data, and Sources

4.1. Specification of the Panel of ARDL Models

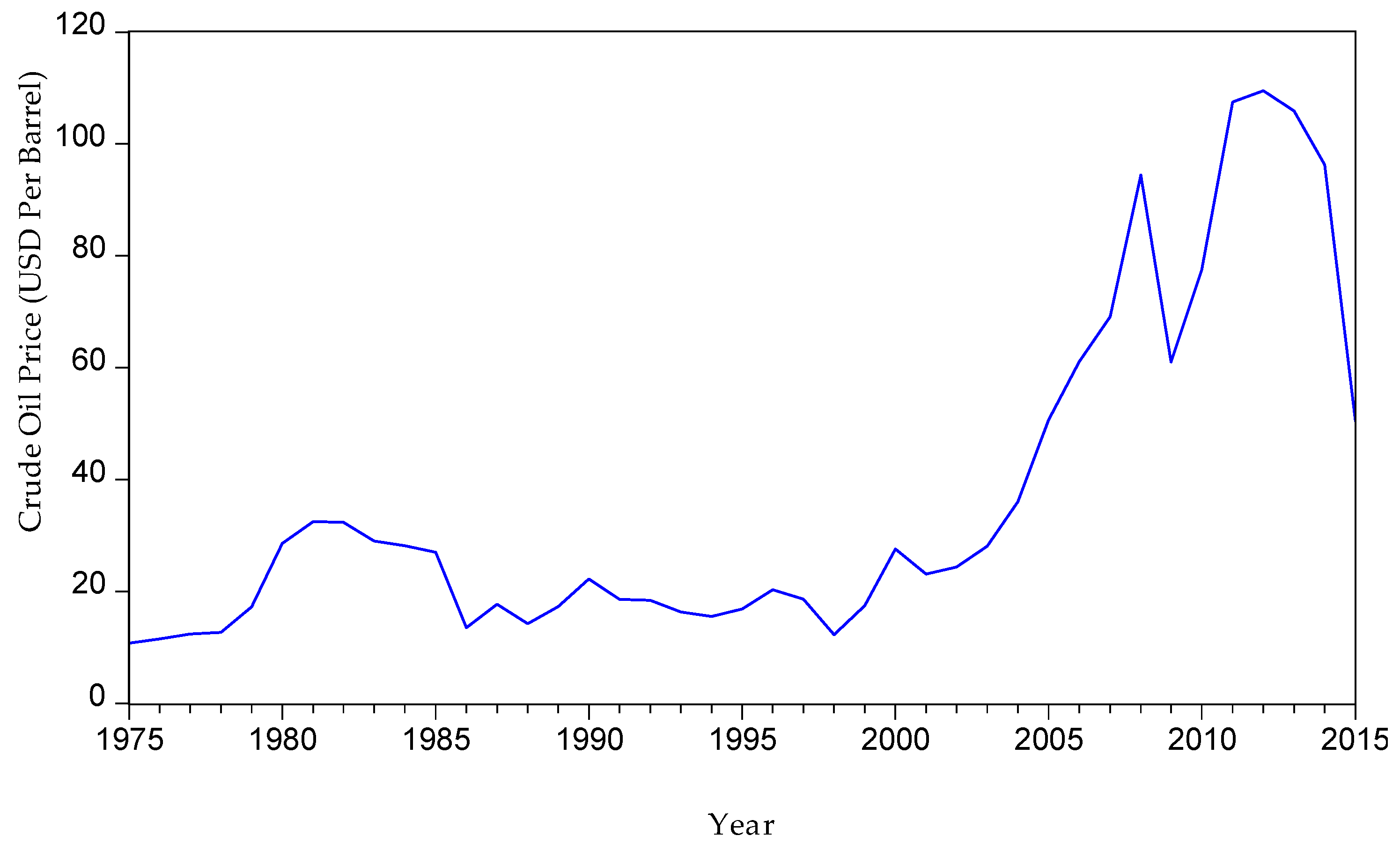

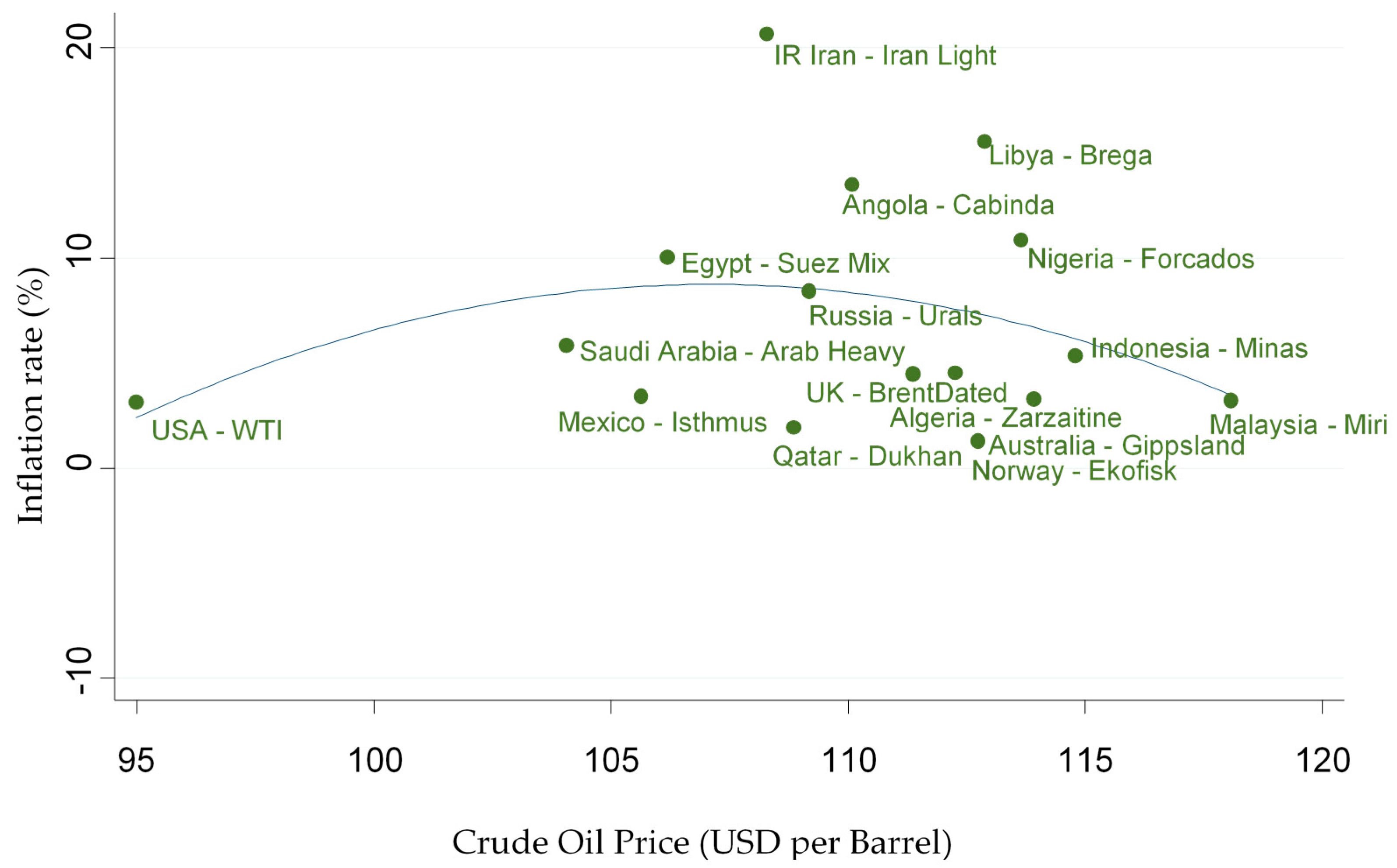

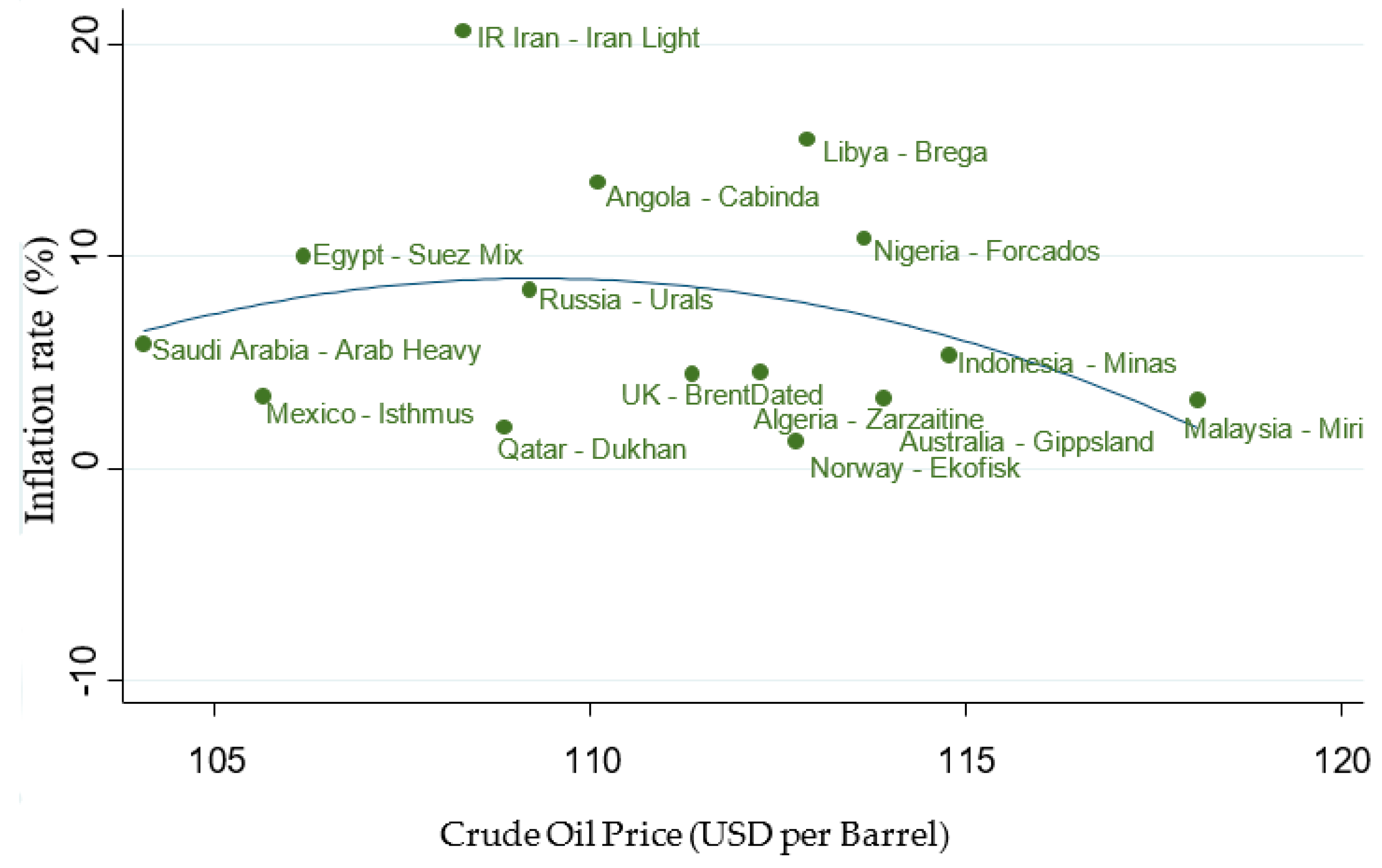

4.2. Data and Sources

5. Results and Discussion

5.1. Panel Unit-Root Test

5.2. Panel Cointegration Results

5.3. PMG and MG Results

6. Conclusions and Policy Recommendations

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|---|

| CPI | Overall | 74.9837 | 38.0718 | 0.0006 | 146.0394 |

| Between | - | 19.4111 | 53.4242 | 96.8450 | |

| Within | - | 34.1070 | 21.5602 | 167.5989 | |

| OPC | Overall | 54.8368 | 35.6944 | 12.2800 | 114.1500 |

| Between | - | 0.8666 | 53.9565 | 55.8295 | |

| Within | - | 35.6864 | 11.7773 | 113.1574 | |

| OPEC | Overall | 52.8825 | 34.32606 | 12.28 | 109.45 |

| Between | - | 0 | 52.8825 | 52.8825 | |

| Within | - | 34.32606 | 12.28 | 109.45 | |

| OP | Overall | 53.3972 | 33.58019 | 13.07667 | 105.0125 |

| Between | - | 0 | 53.39722 | 53.39722 | |

| Within | - | 33.58019 | 13.07667 | 105.0125 | |

| FPI | Overall | 100.5181 | 32.0088 | 46.0700 | 213.3900 |

| Between | - | 7.4388 | 91.6992 | 109.5935 | |

| Within | - | 31.3454 | 36.9945 | 204.3146 | |

| E | Overall | 59.2915 | 50.3602 | 0.0027 | 158.5526 |

| Between | - | 45.2360 | 0.9945 | 110.3545 | |

| Within | - | 31.3369 | −29.1785 | 107.4897 | |

| M2 | Overall | 40.7900 | 23.9209 | 13.2307 | 131.7197 |

| Between | - | 19.2011 | 22.1446 | 57.8042 | |

| Within | - | 17.0938 | 8.9813 | 114.7056 | |

| GDP | Overall | 95,851.01 | 110,624 | 4670 | 561600 |

| Between | - | 62,940.88 | 46,625.75 | 178,607 | |

| Within | - | 96,067.12 | −50,229.99 | 478,844 | |

| Model | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Equation | ||||||

| Assumption | w/o trend | with trend | w/o trend | with trend | w/o trend | with trend |

| Panel v-statistic | −0.307 | 0.290 | −0.315 | 0.540 | −0.415 | 0.290 |

| (0.62) | (0.38) | (0.62) | (0.29) | (0.66) | (0.38) | |

| Panel rho-statistic | 1.075 | 1.966 | 1.068 | 2.113 | 0.998 | 1.966 |

| (0.85) | (0.97) | (0.85) | (0.98) | (0.84) | (0.97) | |

| Panel PP-statistic | −3.41 *** | −4.251 *** | −3.36 *** | −2.971 *** | −4.180 *** | −4.251 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Panel ADF-statistic | −1.763 ** | −4.390 *** | −3.37 *** | −3.793 *** | −2.119 ** | −4.390 *** |

| (0.03) | (0.00) | (0.00) | (0.00) | (0.01) | (0.00) | |

| Group rho-statistic | 1.927 | 2.082 | 2.0714 | 2.187 *** | 1.851 | 2.082 |

| (0.97) | (0.98) | (0.98) | (0.98) | (0.96) | (0.98) | |

| Group PP-statistic | −3.19 *** | −4.340 *** | −2.76 *** | −3.101 *** | −3.726 *** | −4.340 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Group ADF-statistic | −1.508 * | −3.107 *** | −2.093 ** | −2.507 *** | −1.854 ** | −3.107 *** |

| (0.06) | (0.00) | (0.01) | (0.00) | (0.03) | (0.00) | |

| Model | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Long Term | PMG | MG | PMG | MG | PMG | MG |

| OPC | 0.34 ** | 0.41 | - | - | - | - |

| (2.39) | (0.89) | |||||

| OPEC | - | - | 0.39 ** | 0.50 | - | - |

| (2.44) | (1.03) | |||||

| OP | - | - | - | - | 0.37 *** | 0.37 |

| (2.70) | (0.75) | |||||

| LM2 | 0.21 *** | 0.43 * | 0.20 *** | 0.48 * | 0.20 *** | 0.37 * |

| (2.74) | (1.92) | (2.61) | (1.85) | (2.91) | (1.69) | |

| LE | 0.22 *** | −0.10 | 0.21 *** | −0.17 | 0.21 *** | −0.01 |

| (5.08) | (−0.25) | (5.03) | (−0.38) | (5.63) | (−0.03) | |

| LFPI | −1.55 *** | −4.19 | −1.57 *** | −4.75 | −1.57 *** | −4.27 |

| (−3.18) | (−1.00) | (−3.17) | (−0.99) | (−3.47) | (−1.04) | |

| LGDP | 0.38 *** | 0.58 ** | 0.35 *** | 0.56 | 0.39 *** | 0.70 *** |

| (6.40) | (1.78) | (5.08) | (1.24) | (7.32) | (2.84) | |

| ECT | −0.18 ** | 0.05 | −0.18 ** | 0.05 | −0.18 ** | 0.02 |

| (−2.17) | (0.18) | (−2.14) | (0.20) | (−2.05) | (0.09) | |

| Short Term | PMG | MG | PMG | MG | PMG | MG |

| OPC | 0.22 | 0.07 | - | - | - | - |

| (1.15) | (0.89) | |||||

| OPEC | - | - | 0.22 | 0.07 | - | - |

| (1.15) | (0.93) | |||||

| OP | - | - | - | - | 0.21 | 0.09 |

| (1.15) | (1.08) | |||||

| LM2 | −0.05 * | −0.07 ** | −0.05 * | −0.07 ** | −0.06 * | −0.07 ** |

| (−1.83) | (−2.33) | (−1.85) | (−2.64) | (−1.81) | (−2.24) | |

| LE | −0.06 | 0.06 | −0.06 | 0.06 | −0.06 | 0.04 |

| (−0.84) | (0.68) | (−0.81) | (0.73) | (−0.79) | (0.50) | |

| LFPI | −0.04 ** | 0.02 | −0.04 ** | 0.04 | −0.05 ** | 0.04 |

| (−2.45) | (0.47) | (−2.43) | (0.55) | (−2.45) | (0.55) | |

| LGDP | −0.14 | 0.01 | −0.15 | 0.02 | −0.12 | −0.005 |

| (−0.81) | (0.37) | (−0.80) | (0.51) | (−0.77) | (−0.12) | |

| Cons | 0.82 *** | 3.55 ** | 0.86 ** | 3.63 ** | 0.85 ** | 3.51 ** |

| (2.65) | (2.19) | (2.58) | (2.38) | (2.50) | (2.02) | |

| Hausman | - | (0.62) | - | (N) | - | (N) |

| Size (N × T) | 320 | 320 | 320 | 320 | 320 | 320 |

References

- Leblanc, M.; Chinn, M.D. Do High Oil Prices Presage Inflation? The Evidence from G-5 Countries; Department of Economics, UCSC UC: Santa Cruz, CA, USA, 2004. [Google Scholar]

- De-Gregorio, J.; Landerretche, O.; Neilson, C. Another pass-through bites the dust? Oil prices and inflation. Economía 2007, 7, 155–196. [Google Scholar] [CrossRef]

- Lu, W.; Liu, T.; Tseng, C. Volatility transmissions between shocks to the oil price and inflation: Evidence from a bivariate GARCH approach. J. Inf. Optim. Sci. 2010, 31, 927–939. [Google Scholar] [CrossRef]

- Akpan, E.O. Oil resource management and food insecurity in Nigeria. In Proceedings of the European Report on Development (ERD) Conference, Accra, Ghana, 21–23 May 2009; pp. 21–23. [Google Scholar]

- Hamilton, J.D. Historical Oil Shocks; NBER Working Papers 16790; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 2011. [Google Scholar]

- Rafiq, S.; Salim, R.; Bloch, H. Impact of crude oil price volatility on economic activities: An empirical investigation in the Thai economy. Resour. Policy 2009, 34, 121–132. [Google Scholar] [CrossRef]

- Baffes, J.; Kose, M.A.; Ohnsorge, F.; Stocker, M. The Great Plunge in Oil Prices: Causes, Consequences, and Policy Responses; World Bank Group: Washington, DC, USA, 2015; pp. 1–51. [Google Scholar]

- OPEC Annual Statistical Bulletin, Vienna, Austria, 2015. Available online: www.opec.org (accessed on 26 October 2017).

- Razmi, F.; Azali, M.; Chin, L.; Shah, H.M. The role of monetary transmission channels in transmitting oil price shocks to prices in ASEAN-4 countries during pre- and post-global financial crisis. Energy 2016, 101, 581–591. [Google Scholar] [CrossRef]

- Valcarcel, V.J.; Wohar, M.E. Changes in the oil price-inflation pass-through. J. Econ. Bus. 2013, 68, 24–42. [Google Scholar] [CrossRef]

- Gao, L.; Kim, H.; Saba, R. How do oil price shocks affect consumer prices? Energy Econ. 2014, 45, 313–323. [Google Scholar] [CrossRef] [Green Version]

- Xuan, P.P.; Chin, L. Pass-through effect of oil price into consumer price: An Empirical study. Int. J. Econ. Manag. 2015, 9, 143–161. [Google Scholar]

- Kilian, L. Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. Am. Econ. Rev. 2009, 99, 1053–1069. [Google Scholar] [CrossRef]

- Hooker, M. Are oil shocks inflationary? Asymmetric and nonlinear specifications versus changes in regime. J. Money Credit Bank. 2002, 34, 540–561. [Google Scholar] [CrossRef]

- Basnet, H.C.; Upadhyaya, K.P. Impact of oil price shocks on output, inflation and the real exchange rate: Evidence from selected ASEAN countries. Appl. Econ. 2015, 47, 3078–3091. [Google Scholar] [CrossRef]

- Chou, K.-W.; Lin, P.-C. Oil price shocks and producer prices in Taiwan: An application of non-linear error-correction models. J. Chin. Econ. Bus. Stud. 2013, 11, 59–72. [Google Scholar] [CrossRef]

- Lamotte, O.; Porcher, T.; Schalck, C.; Silvestre, S. Asymmetric gasoline price responses in France. Appl. Econ. Lett. 2013, 20, 457–461. [Google Scholar] [CrossRef]

- Farzanegan, M.R.; Markwardt, G. The effects of oil price shocks on the Iranian economy. Energy Econ. 2009, 31, 134–151. [Google Scholar] [CrossRef] [Green Version]

- Ghosh, S.; Kanjilal, K. Oil price shocks on Indian economy: Evidence from Toda Yamamoto and Markov regime-switching VAR. Macroecon. Financ. Emerg. Mark. Econ. 2013, 7, 122–139. [Google Scholar] [CrossRef]

- Çat, A.N.; Önder, A.Ö. An asymmetric analysis of the relationship between oil prices and output: The case of Turkey. Econ. Model. 2013, 33, 884–892. [Google Scholar] [CrossRef]

- Ibrahim, M.H. Oil and food prices in Malaysia: A nonlinear ARDL analysis. Agric. Food Econ. 2015, 3, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Belke, A.; Dreger, C. The Transmission of oil and food prices to consumer prices: Evidence for the MENA countries. Int. Econ. Econ. Policy 2015, 12, 143–161. [Google Scholar] [CrossRef]

- Ianchovichina, E.; Loening, J.; Wood, C. How Vulnerable Are Arab Countries to Global Food Price Shocks? World Bank Policy Research Working Paper 6018; World Bank: Washington, DC, USA, 2015. [Google Scholar]

- Belke, A.; Awad, J. On the pass-through of food prices to local inflation in MENA countries. WSEAS Trans. Bus. Econ. 2014, 38, 307–316. [Google Scholar]

- Ferrucci, G.; Jiménez-Rodríguez, R.; Onorante, L. Food Price Pass-Through in the Euro Area: The Role of Asymmetries and Non-Linearities; ECB Working Paper No. 1168; European Central Bank: Frankfurt/Main, Germany, 2010. [Google Scholar]

- IMF. Is inflation back? Commodity prices and inflation. In World Economic Outlook: Financial Stress, Downturns and Recoveries; International Monetary Fund: Washington DC, USA, 2008; pp. 83–128. [Google Scholar]

- Kofi, P.A.; Zumah, F.; Mubarik, A.W.; Ntodi, B.N.; Darko, C.N. Analysing inflation dynamics in Ghana. Afr. Dev. Rev. 2015, 27, 1–13. [Google Scholar]

- Bala, U.; Chin, L.; Ranjanee, S.; Ismail, N.W. The Impacts of oil export and food production on inflation in African OPEC members. Int. J. Econ. Manag. 2017, 11, 573–590. [Google Scholar]

- Ratti, R.A.; Vespignani, J.L. Oil prices and global factor macroeconomic variables. Energy Econ. 2016, 59, 198–212. [Google Scholar] [CrossRef]

- Balke, N.S.; Brown, S.P.A.; Yucel, M.K. Oil price shocks and the U.S. economy: Where does the asymmetry originate? Energy J. 2002, 23, 27–52. [Google Scholar] [CrossRef]

- Tang, W.; Wu, L.; Zhang, Z. Oil price shocks and their short- and long-term effects on the Chinese economy. Energy Econ. 2010, 32, 3–14. [Google Scholar] [CrossRef]

- Dillon, B.M.; Barrett, C.B. Global oil prices and local food prices: Evidence from East Africa. Am. J. Agric. Econ. 2016, 98, 154–171. [Google Scholar] [CrossRef]

- Brown, S.P.A.; Yucel, M.K. Energy prices and aggregate economic activity: An interpretative survey. Q. Rev. Econ. Financ. 2002, 42, 193–208. [Google Scholar] [CrossRef]

- Shin, Y.; Yu, B.; Greenwood-Nimmo, M. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt; Springer: New York, NY, USA, 2014; Volume 44, pp. 1–35. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y. An autoregressive distributed lag modelling approach to cointegration analysis. In Econometrics and Economic Theory in the 20th Century; Cambridge University Press: Cambridge, UK, 1999; pp. 1–31. [Google Scholar]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef] [Green Version]

- Levin, A.; Lin, C.F.; Chu, C.S.J. Unit root tests in panel data: Asymptotic and finite-sample properties. J. Econom. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econom. 2003, 115, 53–74. [Google Scholar] [CrossRef]

- Maddala, G.S.; Wu, S. A comparative study of unit root tests with panel data and a new simple test. Oxf. Bull. Econ. Stat. 1999, 61, 631–652. [Google Scholar] [CrossRef]

- Kang, W.; Ratti, R.A.; Vespignani, J.L. Oil price shocks and policy uncertainty: New evidence on the effects of the US and non-US oil production. Energy Econ. 2017, 66, 536–546. [Google Scholar] [CrossRef]

- Global Energy Statistical Yearbook 2018. Available online: https://yearbook.enerdata.net/crude-oil/crude-oil-balance-trade-data.html (accessed on 5 September 2018).

- World Integrated Trade Solution (WITS), World Bank. Available online: https://wits.worldbank.org/about_wits.html (accessed on 5 September 2018).

- Belke, A.; Gros, D. A simple model of an oil based global savings glut—The “China factor” and the OPEC Cartel. Int. Econ. Econ. Policy 2014, 11, 413–430. [Google Scholar] [CrossRef]

- Pedroni, P. Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxf. Bull. Econ. Stat. 1999, 61, 653–670. [Google Scholar] [CrossRef]

- Bala, U.; Songsiengchai, P.; Chin, L. Asymmetric behavior of exchange rate pass-through in Thailand. Econ. Bull. 2017, 37, 1289–1297. [Google Scholar]

| Years | 1995 | 2000 | 2005 | 2010 | 2014 | |

|---|---|---|---|---|---|---|

| Exchange Rate | Algeria | 47.66 | 75.26 | 73.28 | 74.39 | 80.58 |

| Angola | 0.0027 | 10.04 | 87.16 | 91.91 | 98.30 | |

| Libya | 0.42 | 0.51 | 1.31 | 1.27 | 1.29 | |

| Nigeria | 21.90 | 101.70 | 131.27 | 150.30 | 158.55 | |

| Money Supply (M2) | Algeria | 37.17 | 37.83 | 53.83 | 69.05 | 79.42 |

| Angola | 40.10 | 17.28 | 15.90 | 35.33 | 41.00 | |

| Libya | 79.62 | 48.51 | 26.56 | 47.64 | 127.47 | |

| Nigeria | 15.87 | 21.96 | 17.73 | 21.03 | 20.16 | |

| Variable | Assumption | LLC | IPS | Fisher-ADF | Fisher PP | LLC | IPS | Fisher-ADF | Fisher PP |

|---|---|---|---|---|---|---|---|---|---|

| Level | First Difference | ||||||||

| CPI | No trend | 7.11 | 7.17 | 0.50 | 0.16 | −2.41 *** | −1.82 ** | 16.70 *** | 14.61 |

| (1.00) | (1.00) | (0.99) | (1.00) | (0.00) | (0.03) | (0.03) | (0.06) | ||

| Trend | −0.29 | 1.84 | 4.99 | 3.17 | −2.03 ** | −1.87 ** | 15.74 ** | 32.48 *** | |

| (0.38) | (0.96) | (0.75) | (0.92) | (0.02) | (0.03) | (0.04) | (0.00) | ||

| OPC | No trend | −0.86 | 1.73 | 1.58 | 1.08 | −5.48 *** | −5.28 *** | 40.41 *** | 73.05 *** |

| (0.19) | (0.95) | (0.99) | (0.99) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −4.00 *** | −1.66 ** | 13.58 | 11.53 | −4.04 *** | −3.79 *** | 27.91 *** | 70.78 *** | |

| (0.00) | (0.04) | (0.09) | (0.17) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| OPEC | No trend | −0.78 | 1.80 | 1.49 | 1.02 | −5.35 *** | −5.25 *** | 40.17 *** | 63.32 *** |

| (0.21) | (0.96) | (0.99) | (0.99) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −3.98 *** | −1.63 | 13.43 | 11.49 | −4.10 *** | −3.79 *** | 27.92 *** | 73.68 *** | |

| (0.00) | (0.05) | (0.09) | (0.17) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| OP | No trend | −0.86 | 1.76 | 1.55 | 1.02 | −5.72 *** | −5.07 *** | 38.77 *** | 73.68 *** |

| (0.19) | (0.96) | (0.99) | (0.99) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −0.42 *** | −1.89 ** | 14.84 | 13.19 | −7.93 *** | −6.32 *** | 43.26 *** | 66.82 *** | |

| (0.00) | (0.02) | (0.06) | (0.10) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| M2 | No trend | −0.38 | −0.52 | 9.21 | 6.40 | −5.90 *** | −4.20 *** | 32.76 *** | 56.21 *** |

| (0.35) | (0.29) | (0.32) | (0.60) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −1.90 ** | −0.08 | 8.62 | 8.79 | −6.11 *** | −5.29 *** | 36.79 *** | 48.22 *** | |

| (0.02) | (0.46) | (0.37) | (0.36) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| FPI | No trend | 2.84 | 3.23 | 2.30 | 2.49 | 0.20 | −4.25 *** | 33.71 *** | 75.84 *** |

| (0.99) | (0.99) | (0.97) | (0.96) | (0.58) | (0.00) | (0.00) | (0.00) | ||

| Trend | 0.25 | −0.61 | 10.76 | 13.64 | 1.05 | −5.88 *** | 41.43 *** | 63.05 *** | |

| (0.60) | (0.27) | (0.21) | (0.09) | (0.85) | (0.00) | (0.00) | (0.00) | ||

| E | No trend | −1.74 ** | −0.29 | 6.80 | 7.81 | −5.28 *** | −4.17 *** | 31.11 *** | 28.61 *** |

| (0.04) | (0.38) | (0.55) | (0.45) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −0.89 | −0.31 | 9.15 | 2.98 | −4.81 *** | −3.21 *** | 23.05 *** | 21.74 ** | |

| (0.19) | (0.37) | (0.32) | (0.93) | (0.00) | (0.00) | (0.00) | (0.02 | ||

| GDP | No trend | 3.16 | 4.32 | 3.45 | 3.33 | −6.94 *** | −6.07 *** | 45.56 *** | 49.80 *** |

| (0.99) | (1.00) | (0.90) | (0.91) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Trend | −1.41 | 0.51 | 5.78 | 5.93 | −7.67 *** | −6.46 *** | 45.52 *** | 63.41 *** | |

| (0.07) | (0.69) | (0.67) | (0.65) | (0.00) | (0.00) | (0.00) | (0.00) | ||

| Model | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Equation | ||||||

| Assumption | Model w/o trend | Model with trend | Model w/o trend | Model with trend | Model w/o trend | Model with trend |

| Panel v-statistic | −0.1030 | −0.3197 | −0.1388 | −0.4456 | −0.1593 | −0.4650 |

| (0.54) | (0.62) | (0.55) | (0.67) | (0.56) | (0.67) | |

| Panel rho-statistic | 1.0994 | 1.7611 | 1.1786 | 1.8051 | 1.1760 | 1.8150 |

| (0.86) | (0.96) | (0.88) | (0.96) | (0.88) | (0.96) | |

| Panel PP-statistic | −5.4535 *** | −5.1350 *** | −5.6242 *** | −5.2748 *** | −5.4877 *** | −5.1856 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Panel ADF-statistic | −7.5297 *** | −6.7085 *** | −8.3785 *** | −7.2733 *** | −8.2525 *** | −7.2418 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Group rho-statistic | 2.2824 | 2.5763 | 2.3969 | 2.7397 | 2.3887 | 2.7185 |

| (0.98) | (0.99) | (0.99) | (0.99) | (0.99) | (0.99) | |

| Group PP-statistic | −2.0298 ** | −1.8908 ** | −1.9966 ** | −1.8098 ** | −1.9178 ** | −1.8415 ** |

| (0.02) | (0.02) | (0.02) | (0.03) | (0.02) | (0.03) | |

| Group ADF-statistic | −3.8141 *** | −2.9324 *** | −4.4643 *** | −3.1794 *** | −4.4129 *** | −3.2274 *** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| Model | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| Long Term | PMG | MG | PMG | MG | PMG | MG |

| OPC+ | 0.005 *** | 0.002 | - | - | - | - |

| (4.08) | (1.32) | |||||

| OPC- | 0.007 ** | 0.002 | - | - | - | - |

| (2.18) | (0.90) | |||||

| OPEC+ | - | - | 0.02 *** | 0.007 | - | - |

| (3.79) | (1.12) | |||||

| OPEC- | - | - | 0.04 ** | 0.017 | - | - |

| (2.18) | (0.84) | |||||

| OP+ | - | - | - | - | 0.02 *** | 0.007 |

| (3.79) | (1.12) | |||||

| OP- | - | - | - | - | 0.04 ** | 0.017 |

| (2.18) | (0.84) | |||||

| LM2 | 0.50 *** | 0.36 ** | 0.54*** | 0.34 *** | 0.54 *** | 0.34 |

| (6.39) | (2.55) | (6.30) | (2.71) | (6.30) | (2.71) *** | |

| LE | 0.34 *** | 0.46 *** | 0.39 *** | 0.47 ** | 0.39 *** | 0.47 ** |

| (7.59) | (2.69) | (7.60) | (2.46) | (7.60) | (2.46) | |

| LFPI | −0.78 ** | −0.81 | −1.17 *** | −0.80 | −1.17 *** | −0.80 |

| (−2.10) | (−1.18) | (−2.76) | (−1.12) | (−2.76) | (−1.12) | |

| LGDP | 0.48 *** | 0.42 *** | 0.51 *** | 0.38 *** | 0.51 *** | 0.38 *** |

| (9.14) | (4.56) | (8.84) | (4.26) | (8.84) | (4.26) | |

| ECT | −0.23*** | −0.007 | −0.21 *** | 0.02 | −0.21 *** | 0.02 |

| (−3.22) | (0.001) | (−2.65) | (0.05) | (−2.65) | (0.05) | |

| Short Term | PMG | MG | PMG | MG | PMG | MG |

| OP+ | 0.001 *** | 0.004 | 0.01 ** | −0.001 | 0.01 ** | −0.001 |

| (2.63) | (0.65) | (2.48) | (−0.30) | (2.48) | (−0.30) | |

| OP- | −0.004 | 0.009 | −0.02 | 0.001 | −0.02 | 0.001 |

| (−0.85) | (1.07) | (−0.89) | (0.16) | (−0.89) | (0.16) | |

| LM2 | 0.01 | 0.01 | 0.02 | 0.02 | 0.02 | 0.02 |

| (0.25) | (0.29) | (0.33) | (0.42) | (0.33) | (0.42) | |

| LE | −0.03 | 0.17 | 0.003 | 0.18 | 0.003 | 0.18 |

| (−0.33) | (1.61) | (0.04) | (1.64) | (0.04) | (1.64) | |

| LFPI | −0.03 | −0.01 | −0.01 | −0.01 | −0.01 | −0.01 |

| (−1.33) | (−0.59) | (−0.64) | (−0.48) | (−0.64) | (−0.48) | |

| LGDP | 0.13 | 0.02 | 0.13 | 0.02 | 0.13 | 0.02 |

| (1.47) | (0.30) | (1.56) | (0.40) | (1.56) | (0.40) | |

| Cons | 0.02 | 2.26 | 0.28* | 2.26 | 0.28 * | 2.26 |

| (0.19) | (1.27) | (1.78) | (1.35) | (1.78) | (1.35) | |

| Hausman Test | - | (0.50) | - | (0.96) | - | (0.96) |

| Size (N × T) | 320 | 320 | 320 | 320 | 320 | 320 |

| Model | Robustness Check 1 (External Shock: USA GDP) | Robustness Check 2 (External Shock: China’s GDP) | Robustness Check 3 (External Shock: Global GDP) |

|---|---|---|---|

| Long Run | PMG | PMG | PMG |

| OPC+ | 0.0035 *** | 0.0051 *** | 0.0018 |

| (2.74) | (3.81) | (1.25) | |

| OPC- | 0.0121 *** | 0.0031 | 0.01370 *** |

| (5.01) | (0.83) | (4.44) | |

| LM2 | 0.3064 *** | 0.5241 *** | 0.3553 *** |

| (5.62) | (7.11) | (6.01) | |

| LE | 0.3931 *** | 0.3210 *** | 0.4007 *** |

| (8.47) | (4.99) | (7.00) | |

| LFPI | −0.2868 ** | −0.7387 ** | −0.1332 |

| (−2.01) | (−1.97) | (−0.67) | |

| LGDP | 0.3829 *** | 0.5131 *** | 0.3420 *** |

| (9.71) | (9.59) | (6.48) | |

| LGDPUS | −0.0818 *** | - | - |

| (−2.76) | |||

| LGDPChina | - | −0.0412 | - |

| (−0.74) | |||

| LGDPWorld | - | - | −0.0576 |

| (−1.38) | |||

| Error Correction | −0.2621 *** | −0.2429 *** | −0.2577 *** |

| (−5.69) | (−3.03) | (−4.73) | |

| Short Run | PMG | PMG | PMG |

| OPC+ | 0.0016 ** | 0.0022 ** | 0.0015 *** |

| (2.58) | (2.00) | (3.57) | |

| OPC- | −0.0040 | −0.0170 | −0.0035 |

| (−0.68) | (−0.62) | (–0.61) | |

| LM2 | −0.0245 | −0.0320 | −0.0475 |

| (−0.36) | (−0.51) | (−0.35) | |

| LE | −0.0888 | −0.0828 | −0.0534 |

| (−0.98) | (−0.99) | (−0.45) | |

| LFPI | −0.0159 | 0.0006 | −0.0197 |

| (−0.74) | (0.02) | (−0.50) | |

| LGDP | 0.1137 | 0.0983 | 0.1250 |

| (1.20) | (1.07) | (0.88) | |

| LGDP | −0.1946 | −0.0036 | −0.0203 |

| (−1.59) | (−1.54) | (−1.01) | |

| Cons | −0.1946 | −0.1997 | −0.2812 ** |

| (−1.59) | (−1.57) | (−2.38) | |

| Size (N × T) | 320 | 320 | 320 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bala, U.; Chin, L. Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries. Energies 2018, 11, 3017. https://doi.org/10.3390/en11113017

Bala U, Chin L. Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries. Energies. 2018; 11(11):3017. https://doi.org/10.3390/en11113017

Chicago/Turabian StyleBala, Umar, and Lee Chin. 2018. "Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries" Energies 11, no. 11: 3017. https://doi.org/10.3390/en11113017

APA StyleBala, U., & Chin, L. (2018). Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries. Energies, 11(11), 3017. https://doi.org/10.3390/en11113017