Ushering in a New Dawn: Demand-Side Local Flexibility Platform Governance and Design in the Finnish Energy Markets

1

School of Marketing and Communication, University of Vaasa, Wolffintie 34, 65200 Vaasa, Finland

2

School of Management, University of Vaasa, Wolffintie 34, 65200 Vaasa, Finland

*

Author to whom correspondence should be addressed.

Energies 2021, 14(15), 4405; https://doi.org/10.3390/en14154405

Submission received: 16 June 2021

/

Revised: 15 July 2021

/

Accepted: 19 July 2021

/

Published: 21 July 2021

(This article belongs to the Special Issue Smart Grids and Flexible Energy Systems)

Abstract

:Energy ecosystems are under a significant transition. Local flexibility marketplaces (LFM) and platforms are argued to have significant potential in contributing to such a transition. The purpose of this study was to answer the following research question: how do market conditions and stakeholders shape emerging LFM platform governance choices? We approached this objective with an exploratory single-case study by conducting ten semi-structured interviews with key stakeholders in the Finnish energy ecosystem. The results of the content and pattern analyses revealed the key challenges to LFM implementation such as the current regulatory treatment of flexibility, high costs of gadget installations, and ensuring sufficient liquidity in the market. In addition, we also demonstrated that despite such barriers, the Finnish ecosystem is largely pragmatic about LFMs’ in its midst. All in all, we contributed to the non-technological streams of LFM literature by developing an exhaustive framework with four distinctive dimensions (i.e., ecosystem readiness, value-creation logic, platform architecture and governance, platform competitiveness) for LFM development, which helps academics, practitioners, and policy-makers to understand how novel platforms emerge and develop.

1. Introduction

“Either you become a platform, or you will be killed by one” [1]

We live at the cusp of many significant changes that have been taking place in the realms of the energy business, where issues such as decarbonization or decentralization of the energy ecosystem have entered the mainstream consciousness [2]. Occurring concurrently, we have industrial internet gaining momentum in the energy cluster along with a mounting push for consumer empowerment [3]. Under such pressure, the status-quo sees corresponding innovations either as solutions in the market [4,5] or emerging technologies awaiting implementation [6]. One emerging example of such consumer empowerment can be found in the local flexibility marketplaces (LFM) for demand-side management. So, while flexibility markets for larger energy entities have been a regular part of the grid for some time [5], the race to take it to a micro level is a relatively new one. The target is that even small households can react to the optimal consumption design devised by this marketplace [7], increasing grid efficiency and reducing network investments [8,9].

Acknowledging the technological intensity of the energy sector, it is perhaps unsurprising that the literature on local flexibility marketplaces has been mostly technological in scope. However, from a non-technological perspective, we see two significant streams of research emerging. Firstly, a vibrant stream of literature discusses this development’s regulatory landscape [9,10,11]. Secondly, there is a stream looking at the market’s architecture and design, which includes subjects such as business models [12,13,14], stakeholder roles [15,16], and ecosystem design [7,9,17,18].

Prior studies looking into LFM design have mainly focused on its role in the increasingly localized energy ecosystem gaining momentum in the European Union [19,20]. Controversies and possibilities in making LFM a contagious part of the grid have also been investigated [8]. We can further see a proliferation of literature on prosumers’ role in the future energy management schemes, particularly the motivations, roadblocks, and instruments enabling their robust participation [19,21,22]. Previous studies have also examined the changing energy business models due to platform development [23], digitalization in smart grid networks [24], as well as the role of prosumers in the digital energy ecosystem [25].

However, the novelty of LFM increases as we account for the growing prominence of platforms in the energy markets. Platforms act as a foundation upon which an array of firms, together forming an ecosystem, can develop complementary products, technologies, and services [26]. It is the center of the digital economy and creates online infrastructures enabling a diverse range of human activities [27]. In the energy context, platforms are increasingly used to connect consumers to the grid. So, while industries, such as retail, real estate, or social media, have a solid foothold of the platform model, platforms as a phenomenon are relatively recent in the energy sector [23,27]. Moreover, while the prior studies provide valuable insight into LFM and most non-technological aspects are taking place on a platform, it is surprising that there is not much discussion highlighting this integral feature of the LFM. Put differently, there seems to be a dearth of literature combining the platform perspective and LFM developments.

Furthermore, we know that platform development is impacted by market conditions such as industry and firm-level characteristics, organizational networks, and access to customers or supply channels [28,29]. In other words, these external conditions shape the platform’s development process and mold its eventual properties. Furthermore, these conditions become even more pressing for emerging sectors, such as the LFM [29]. Stakeholder collaboration is paramount in this development process, and platform governance emerges as a useful concept here. It provides us with strategic frameworks that are grounded in technology and yet are stakeholder-driven, thus helping us to activate novel platforms in their broader context [1].

Therefore, this paper tapped into this opportunity by answering the following research question: how do market conditions and stakeholders shape emerging LFM platform governance choices? Through answering this question, we developed a framework with four focus areas in the LFM platform development process that requires careful consideration. For further contextualization of this framework, we conducted a case study within the Finnish energy ecosystem, as it has been labeled as one of the ‘smartest grids’ in Europe [30]. The same authors [30] also noted that a demand-side flexibility management platform is under development in this market, thus further validating the suitability of this study in the Finnish setting. Finally, the study identified market conditions and stakeholder issues relevant to the LFM development in this ecosystem.

Our motivation for undertaking this research rests on the idea that, in the fast-moving LFM design discussions, integrating platform perspectives can expedite this process. Platform literature provides us with access to varied development strategies [26,31], adoption frameworks [32,33], and consumer interaction pathways [34,35], among others. Since LFMs qualify as platforms, we can import frames to develop business models, control mechanisms, and governance structures for this marketplace. Ignoring this perspective, we fear there might be a risk of putting efforts behind reinventing the wheel.

The contribution of this study is threefold. First, this study contributes to the non-technological streams of LFM literature and opens a niche. Merging platform literature with the flexibility marketplaces, we developed an exhaustive framework for LFM development in the Finnish energy ecosystem. We believe this framework yields analytical value in understanding and developing other energy ecosystems, especially within the EU context. Another contribution of this study is the identification of Ecosystem Readiness as a distinct dimension to the novel platform development process. This dimension sets the tone for the platform development process as a whole. We believe that the addition of this foundational focus area transcends the LFM sector and helps to understand novel platform development processes better. Second, the findings hold essential insights relating to platform development for the practitioners in the energy cluster. It presented lessons for potential LFM operators as well as other stakeholders that could be impacted by this development. Issues such as how the LFM’s emergence impacts the energy sector, potential frictions among stakeholders, and their solutions were considered. We further identified significant challenges and opportunities associated with the LFM development in Finland. Third, this study offers comprehensive insights for policymakers concerning local flexibility marketplaces. This paper is the first such study in the Finnish context, and we identified several policy barriers and areas where further refinement is needed. In addition, we registered a willingness among regulators to accommodate such marketplaces in the ecosystem, particularly in geographical areas where the system operators can utilize the LFM to procure flexibility competitively.

The rest of the paper is structured as follows: Section 2 presents the literature review on LFMs and platform governance, followed by a preliminary theoretical framework. Section 3 describes the methodology for this paper. Section 4 outlines the findings from LFM and platform perspective, and in Section 5, the two perspectives are merged to develop the unifying LFM development framework. Finally, Section 5 concludes the paper with this paper’s limitations and further research possibilities.

2. Theoretical Background

2.1. Local Flexibility Marketplaces

A local market in the LFM context can be viewed as an institutional framework enabling the trading of flexibilities [5,17], and where flexibility is understood to be the possible generation and consumption adjustment upon a signal (i.e., price) [36]. The boundaries of an LFM are almost always understood through spatial constraints, limited to geographical entities such as neighborhoods, towns, or small cities [37]. A broad framework of LFM can be found in Ramos et al.’s [5] proposal suggesting that these markets are ‘long or short-term trading actions for electricity flexibility in a certain geographical location, voltage level, and system operator, given by grid conditions of balancing needs, where participants in a relevant market can be aggregated to provide flexibility services’ (p. 28). Many relevant stakeholders are typically part of the LFM, such as the distribution system operators (DSO) and transmission system operators (TSO), balance responsible parties (BRP), the consumers and prosumers, and the market operator itself [37,38]. The system operators and the BRPs buy flexibility from the consumers, prosumers, or aggregators [5]. However, although central in most frameworks, due to the lack of negotiation power and flexibility volume of the end consumers, the role of the aggregators is not deemed mandatory across proposals.

Designing such a market, one must consider the regulatory landscape that it operates in. For instance, in a classical regulated semi-competitive market, the competition is on the supply side, whereas only the TSO could be on the procuring end [5]. However, a recent EU amendment in the regulation made it possible for DSOs to procure flexibility for their grid management [39]. Another aspect fundamentally determining the market design is the technological reality of the given ecosystem. The penetration of distributed energy resources (DER) is a principal matter here, other prominent requirements being the capability of smart meters, ICT infrastructure, and grid topology [5,17]. A market design form can take various forms such as centralized optimization, game theory variants, models based on auction theory, and simulation models [37]. The most common formulations for LFMs are the centralized models, which can take two avenues based on their objectives: maximizing social welfare or minimizing operational costs. When it comes to LFM operationalization, Ramos et al. [5] proposed two possibilities: a sub-market of the wholesale market or a novel exchange platform run by the system operators or a third party. However, the latter option of system operators in charge of this market is a contested topic as it might compromise fair competition in the market [38]. As a result, both these operators have been barred by EU regulations from operating local markets [39].

The centrality of the system operators to this market also necessitates close coordination between the TSO and the DSO and multiple DSOs if they are active within the LFM [5,38]. Due to the in-depth knowledge that the DSOs have on their network customers, they must act as neutral arbitrators in the marketplace while ensuring system stability, power quality, technical efficiency, and cost-effectiveness [38]. Several authors [15,40] have proposed market designs focusing on DSO problem solving, congestion, and voltage violations. In the EU, market-based procurement of flexibility by promoting DER integration in the grid is essential [15]. TSOs, on the other hand, face a different question: whether they should participate in the LFM directly or settle in a broader role facilitating the market [38].

Lastly, local features, too, are central to the flexibility market’s design, and often these features are encapsulated in the form of an energy community where the LFM could play an important role. Local energy communities (LEC) can bring DER’s in a particular vicinity in the market; the upward trajectory of prosumer participation complements in this regard [18,37]. However, the role of LFMs in LECs is not mandatory, but considering that we are moving towards heightened use of technology among households and with DER penetration rising, a strong case can be made in favor of LFM’s [17]. The placement of aggregators plays a crucial role in these communities. New business models are incentivized through DER aggregators, making the flexibility trading more sustainable; the needed regulatory changes are currently underway [37]. The centrality of the aggregators in the local market can also be found in specific energy community designs where they play a crucial role in electricity production and consumption, settlements, and contract fulfillment [17,32]. We can summarize the principal components of LFM design as depicted in Figure 1.

2.2. Platform Governance

Moving on to platform governance, it is apparent that LFM shares many characteristics with platform development and design models. Though platforms are not a recent phenomenon [41], a contemporary understanding is intimately connected to the current digital economy. Many of the largest and most influential companies today are revolving around platforms, and adopting a platform model is seen as an existential move in many industries [1]. Prominent examples of industries operating on a platform can be found in social media (Facebook, Twitter), e-commerce (Amazon, eBay), or search-engine platforms such as Google. Perhaps because of its centrality in the digital economy, the current view on platforms was initially mainly technological, but the platforms were later studied as a prominent business model. According to Gawer and Henderson’s [33] view, platforms are a component of a dynamic technological system with a very strong interdependency among the sub-components. This system can exchange a broad consortium of services, content, software, or novelty exchange such as smart contracts [1]. Network effects, meaning the influence a network’s structure exerts on user behavior [34], play a central role in mobilizing this value exchange within a business ecosystem [1,42]. While most platforms operate with an external focus, there are also platforms with a more inward focus, used predominantly to facilitate a firm’s in-house product development, though sometimes along with its development partners [42].

Platform governance can be perceived as the framework guiding the platform’s decision-making process [31]. Furtenau et al. [43] stressed four focus areas relevant for this stage: strategy and governance, technical architecture design and standardization, community building, and engaging with the broader ecosystem. In a general setting, Tiwana et al. [31] proposed that platform governance is a function of the platform’s decision rights, control mechanism, and the proprietary versus shared element of the platform. We can further identify ensuring economic viability [42], ecosystem development [42], regulatory landscape [1], and transparency and communication channels design [1] to be the prominent issues in platform governance.

The economic viability of the platform calls into question many considerations; among them, pricing is an important one [42]. Business models become relevant here as they provide the framework to enable the platform’s economic engine. We can also identify the platform’s transaction partners, their value propositions, and how the platform operator connects to them [35]. However, economic viability cannot come as the sole strategic matter in the early stages of a platform, and issues such as risk-sharing [42], regulations [1], competitive landscape [35], and technological environment [44] should also be considered. Regulations are an apt topic, particularly as Fenwick et al. [1] pointed out; specifically, the current regulatory frameworks governing the market are not equipped to enact a thriving platform culture. Especially for a sensitive industry such as the energy sector [45], this issue is even more pressing, as Furstenau et al. [43] pointed out; besides coping with laws and regulations, it is also imperative to adhere to informal expectations (e.g., data security, quality control). Investigating platform governance, we summarize such issues as platform strategy in our proposed framework in Figure 2.

Platforms also require collaboration. More specifically, platform operators or developers must enact an innovating ecosystem for the platform partners [42]. Complementing that goal, Euchner [44] proposed that a value-adding network should be established, leading to collaborative innovation. A complementing business model becomes relevant here, along with an environment that nurtures it [42]. Furthermore, platform governance should make the threshold to join the platform as low as possible for its target user group to develop a thriving ecosystem and start the practice of sharing the benefit from the get-go [44]. However, there are endemic challenges to the platform’s ability to develop an ecosystem, such as the ones identified by Adner et al. [46]: execution risks, co-innovation risks, and adoption chain risks. Additionally, we can also add challenges such as developing coherent internal processes in the partner companies [42] and creating a winning strategic positioning for the platform [43]. We summarize these issues in the category of coalition building.

Moreover, the perceived usefulness and the perceived ease of use are the principal determinants of user adoption of a novel technological innovation, which aligns with the technology acceptance model proposed by Davis [47]. Moreover, for a platform’s long-term success, the reliability and security of its technological base must also be stressed [1]. For a novel platform, communication becomes paramount, as it reaches out to its ecosystem and builds an ongoing dialogue to develop trust and credibility [1]. If done correctly, the new technology generates a positive perception of its usefulness, which results in an increased intention to use it [41]. We classify this stage as working towards platform acceptance.

2.3. Theoretical Framework

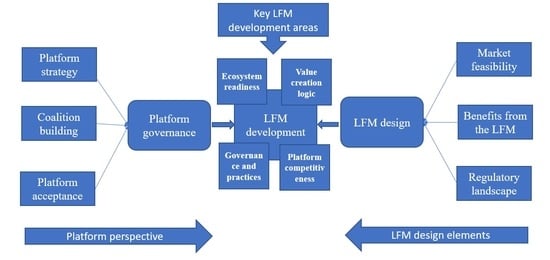

Based on the above discussions, we conceptualize the domain of our inquiry in the following framework in Figure 3. The intersecting area between platform governance and LFM design perspectives, at the center, becomes our focus area going forward. In analyzing the intersection, we consider the platform design framework provided by Tura et al. [48]. The framework enables us to holistically investigate the stakeholder influence and market forces on the LFM by going through the following problematic areas common in platform design: platform architecture, value creation logic, governance and practices, and the platform’s competitive atmosphere [48].

3. Methods

We opted for an exploratory single-case study to investigate the LFM governance phenomenon since it provides the opportunity to examine selected issues in greater depth and detail [49]. Exploratory case studies are suitable when answering ‘how’ or ‘why’ questions and explaining presumed casual links that may be too complex for surveys or experimentation [50]. Moreover, since the phenomenon in question, LFM markets, is still in the emerging phase, the standardized quantitative methods would not have been a good fit in this instance. Known for its attention to context [51], a single-case study design provided us with the framework to examine the factors forming the Finnish energy sector holistically—people, policies, organizations, and technology—and their interrelationships as we blend the platform perspective with the perspective of LFM.

Since the operation of LFMs depends on its possible integration in the energy grid, studying the actors on this plane is necessary. Therefore, we first mapped out the stakeholders that an LFM would need to engage within the Finnish energy ecosystem: regulators, system operators (TSO, DSOs), aggregators, balance responsible parties, and industrial actors. We then went a step ahead and studied a few emerging LFMs in Europe from a platform perspective. Our aim here was to develop a benchmark for the potential Finnish LFM.

The sample size in a qualitative inquiry depends on the scope, resources at disposal, and the purpose of the study [52]. We employed a purposeful sampling method to decide on these organizations. Yin [50] defines purposeful sampling as when cases are selected because they are rich in information and offer practical manifestations of the phenomenon of interest; furthermore, sampling aims to gain insight about the phenomenon and not a statistical generalization.

In the sampling process, naturally, the TSO came as the primary party to be consulted with. In Finland, a single TSO entity is in charge of the nationwide electricity transmission. Therefore, we opted for multiple perspectives from this organization and settled with a Senior Corporate Director, who has a birds-eye view of the ecosystem and a Specialist with expertise on the flexibility marketplaces in Finland. In the next step, we chose a DSO operating in the countryside that also has retail operations. To get a diverse sense of the retailer perspective, we approached and interviewed a retailer from the capital region of Helsinki. This particular retailer is also active in a BRP role, allowing us to probe both angles. We opted for senior executives with flexibility market expertise from both these organizations. Aggregators are key in bringing smaller consumers to the LFM, and we opted for an operational aggregator from the south-western Finnish city of Turku. It can be mentioned that aggregators are a new addition to the Finnish grid, and this particular entity is the sole commercial aggregator in the country.

Moreover, to get a sense of the industrial actors vis-à-vis the LFM, we chose two organizations in proximity to the energy sector, where one is from the manufacturing sector while the other from the service side. The manufacturing company operates in the forestry industry and is active in the balancing markets. The energy services firm is one of Finland’s most prominent energy consulting houses and has significant in-house know-how of the Finnish energy sector. In both cases, we interviewed veteran experts, respectively being a Vice-President and a Director. Finally, we opted for the regulator and industry interest groups’ points of view, since both these operators are connected closely with policy making. We interviewed two senior experts from the industry interest group and the Deputy Director General from the energy regulator in charge of the system operators. This set of stakeholders from the Finnish energy ecosystem has shown to be appropriated from the saturation perspective and provides a good balance between the study’s depth and breadth.

Ten semi-structured interviews were conducted with the selected stakeholders. Semi-structured interviews enable thematic questioners while allowing the possibility to modify elements of the questioner case by case [53]. From the interviews, three were conducted online, while the rest were held face to face; all the interviews were recorded and carefully transcribed. We conducted two separate interviews from the TSO (interviews B and C), while for interview E, we held two separate sessions with the same contact. Following a semi-structured philosophy, the interview guide was divided into three sections. The first section probed the general state of the Finnish energy ecosystem and the suitability of the LFM in this context. Issues such as barriers and opportunities were investigated here. This sector was common throughout the interviews. The second section was more interviewee-specific, meaning depending on their organization’s role and their individual experiences, we had a set of more specific questions. Finally, the third section was kept open for a free-flow discussion to follow any interesting lead that may have arisen during the interview. Detailed information on the interviews can be found in Table 1.

The second set of interviews were conducted with four LFM projects in various stages of their development (Table 2). These were chosen from Europe as they operate in relatively similar conditions vis-à-vis the regulatory landscape, market conditions, and technological benchmarks, among other factors. We investigated their best practices guided by our theoretical framework and subsequently developed an interview guide focusing on three themes: business models, platform design and governance, and the regulatory landscape. Two of the LFMs in question are research-oriented, while the remaining two have commercial ambitions. However, the UK case is the only example of being in an entirely commercial operation. The executives interviewed here have all been part of the development process. Much like the interviews in the previous stage, these interviews were semi-structured as well. Finally, the benchmark developed from this round was juxtaposed with the findings from the Finnish ecosystem. In doing so, it was possible to adopt more realistic scenarios during our analysis of the Finnish ecosystem.

The data analysis started with a content analysis of the interviews by identifying, coding, and categorizing the primary patterns in the data [52]. Once the transcribing was complete, the coding began following a two-step process. Firstly, the raw case data were assembled, consisting of the transcripts, notes from the interviews, and secondary sources. Secondly, several case records were constructed, organizing the raw data based on the themes identified in the theoretical framework. Subsequently, a pattern analysis was conducted by condensing these case records as we searched for recurring regularities in the data [52]. For a more visual representation of the data, we constructed a data structure following [54] (Figure 4), where the most critical patterns identified in the previous step were placed as first-order themes. It was followed by grouping them into the six theoretical pillars found in the outer circles in Figure 3. Lastly, they were further aggregated into the two central pillars of this study: platform governance and LFM design. Finally, a case study narrative was written in the form of findings (Section 4), where all the identified patterns were discussed in detail [52].

4. Findings

4.1. LFM Design

Section 4.1 presents the findings on the LFM design elements, where three principal sections are highlighted: the marketplace’s feasibility, benefits, and the regulatory landscape. A summary of the findings can be found in Table 3.

4.1.1. Market Feasibility

When gauging the feasibility of the LFM, the need for enough liquidity in the marketplace repeatedly came up from all sectors of the ecosystem. It was pointed out that the intraday markets are fragmented enough, resulting in limited liquidity in each case. This notion of markets turning into low-liquidity islands have been put forward as a potential roadblock to the LFM implementation, as stressed here in Interview A: ‘we have to make sure that all resources and all (EU) member states get to all of those marketplaces and we have actual liquidity that makes use of the technology. Otherwise, we will be stuck on an island’. Furthermore, if this market wanted to have industrial players in its midst, then offering enough liquidity emerged as a decisive factor: ‘you just want to hope that the markets are very liquid, that you have all the flexibility offered in the markets (to manage large imbalances)’ comments a senior industry manager from Interview F.

One way of generating such liquidity is through accommodating enough prosumers. Lowering the participation threshold from 100 KW to allow household-level loads is still considered inefficient for the grid and unlikely to occur soon. However, the Finnish TSO acknowledges the need to activate smaller players to utilize full flexibility potential, and lowering this threshold emerged as a gradual process, as elaborated by a specialist in the Finnish TSO in Interview C:

‘already in our current processes… we are (going to) smaller sizes, the minimum size, which is often something that the smaller market players would like to have. That should you have five megawatts, why cannot it be one megawatt, to be able to offer something.’

The solution for the time being lies in aggregation, and significant background work on aggregation rules is taking place, primarily focusing on business models and regulatory frameworks. Another aspect that requires greater attention in activating aggregators here is the coordination framework between DSOs and aggregators. It has emerged that this cooperation needs to be active and real-time, and the greater the aggregation is, the bigger the need for a framework maintaining this contact.

Flexibility requirements are different for transmission and distribution system operators. Though both require flexibility to balance their systems, their needs come at different levels of the grid. For example, the TSO needs flexibility at a central level, whereas the DSO needs are somewhat regional or local. This attribute calls for the LFM to offer services accordingly, especially when a resource can be valuable for both parties. An example can be found here in Interview H:

‘(The) platform needs to somehow to control who is buying and from whom, because if you have a resource that (part of an aggregation) can be valuable for the TSO…but the same resource can be a single resource valuable for the DSO…(then) the platform has to manage how and who eventually buys it.’

The launch of the Datahub, the Finnish TSO’s centralized information exchange, will occur on February 2022. Interested parties can access data related to accounting points and contract information from here. The Datahub will also integrate the electricity consumption data from the smart meters to this exchange, and therefore it could play a significant role in streamlining the LFM with the ecosystem. Reflecting how this development is relevant for the LFM feasibility, a specialist in the Finnish TSO reflects in Interview C:

‘If somebody else (an aggregator) is trading my energy…then I might give my data (from the Datahub) to the aggregator, so they have more information to work on. So, they could see my address and, what kind of heating I have and, if I have a battery and solar panels, and how my consumption was going last year, that kind of information can be given to some other party with a click of a button, so then the Datahub gives access to some other party (LFM).’

We must pay special attention to attracting simultaneous supply and demand to the platform to foster a network effect. Our findings suggested that creating demand is the less-tricky matter in this instance, as the energy need (alternative flexibility) is on an upward trajectory. The issue, which must be addressed on the demand side, relates to regulations, which can help streamline this demand. Moreover, it was suggested that in an early stage of platform operations, system operators might assist with generating demand: ‘when this kind of local flexibility markets start, in the beginning, there might not be the demand and then…we need to be the market makers and doing some buying’, suggested in Interview C. However, we do not notice such institutional support on the supply side, especially when it comes to the smaller consumers, where the emphasis was placed on aggregation.

4.1.2. LFM Benefit

Our findings indicated that an LFM can bring new value to flexibility, especially since it opens a fresh avenue for flexibility trading and invites previously untapped flexibility to the market. We can further highlight the scenario that the energy production in Finland is going towards an inflexible place, especially as it continues to rely on nuclear and brings wind energy into the mix. An LFM in this context is in an excellent position to steer flexibility to that equation: ‘a lot of money involved in flexibility, and there will be (even) more money because the production structure of Finland is going to a direction where there (it) is less and less flexible’ commented the Business Director in Interview E.

In the evolving energy landscape, it might be soon enough that we see a situation in which EVs, PVs, or household storage capacities are commonplace in residential neighborhoods, and an LFM has the potential to emerge as a facilitator of such localized energy trading. A possible arrangement can be that these household participants only trade among them within the neighborhood, bypassing the grid operators. Furthermore, an LFM can be handy in incentivizing consumers to lower their overall consumption through increased demand-side management. It can also incentivize the end consumers to avoid high spot price hours. For the retailers, this possibility promises increased stability in their estimation process. As a result, the retailers will increase their savings, and with LFM, it could further be possible to share the monitory benefits with a more extensive consumer base. The Business Director from a large retailer explains in Interview E: ‘Demand-side management creates (for) us, a possibility of saving money, pure money from our side. And then, of course, we should have some kind of a system where we can compensate part of the money to the customers as well’.

An LFM makes it easier for DSOs to procure flexibility competitively. As discussed earlier, the DSO flexibility needs are projected to be local, often in remote areas. Procuring flexibility in those locations could be tricky, especially if there is no competition involved in the process. A senior energy regulator sees LFM as a potential solution in Interview G:

‘We do not like that the DSO will purchase (flexibility through) contracts with one participant only. That will be inefficient. And that is why if there is a platform to provide services to different DSOs, for example, it will be a more open and market-based solution.’

An LFM also has the potential to generate savings for DSOs, especially if flexibility can substitute investing in networks. Once again, this comes quite handy for isolated locations where distribution lines often need high investments, resulting in higher energy costs. If flexibility can alleviate some of the energy need from there and substitute grid investments, LFM might emerge as a cost-saver for the DSOs.

4.1.3. Regulatory Landscape

The rebuilding of the electricity network has been underway for quite some time in Finland, driven by regulations emphasizing network investments. It emerged that such investments typically favor grid reinforcements over flexibility deployment. Our findings also indicated that the grid developments leave the smartness of the grid at the endpoint combined with centralized production resources. The Development Director for an energy services firm comments in Interview A:

‘All of the networks are now facing huge problems with the existing regulation, so they are quite reluctant to make collaborative efforts because all of their focus is on rebuilding the network because of the Network Electricity Act.’

We also noticed that specific TSO regulations could be construed as restrictive in participating in an LFM, especially for industrial actors. For instance, the reactivation period after being downregulated is often too little for large players. After a certain downregulation period, the reactivation period could be anywhere between two to twelve hours in large productions, but the TSO regulations call for a much faster reaction. A company in the forestry sector finds this a particular barrier in being active in an LFM, as observed in Interview F: ‘and our experience has been that the rules (from the TSO) are often quite restrictive’.

How costs incurred from flexibility are treated, as either operational expenditure (OPEX) or capital expenditure (CAPEX), has significant consequences. It is not beneficial to increase OPEX, and regulation currently treats flexibility as OPEX, providing a bottleneck that reduces deployment. When operators avoid network investments, they end up with higher OPEX, favoring network reinforcement. A solution can be to treat flexibility as CAPEX; until we see that change in regulations, optimizing flexibility remains difficult. For instance, we can highlight a TSO point of view on this matter from Interview C: ‘if using flexibility increases OPEX…it is not a viable tool in comparison of network reinforcements’.

However, in the upcoming regulatory model, which will be implemented in 2024, flexibility will be considered CAPEX. The aim is to increase options for the DSOs: ‘(in this regulatory model) the DSOs can use flexibility or other services to have a choice, not only built more cables, which is the case today’, noticed a TSO Specialist in Interview C.

The regulations on aggregation and aggregators are slowly taking form as the Finnish energy sector witnesses their arrivals in specific markets. It is noteworthy that independent aggregators can already be active in markets with capacity components. The question of balance responsibility becomes relevant here, and as it stands now, capacity trading by independent aggregators is allowed as long as it is not affecting the balancing responsibility of others. For the DSOs, there are no obvious regulatory barriers in sourcing aggregated flexibilities, yet, up until 2024, when flexibilities are treated as OPEX, the market incentives are relatively limited to do so.

The European Clean Energy Package (CEP) is a positive development for increasing flexibility use. The CEP mandates that the member states create favorable conditions for increased demand response usage in their grids, emphasizing that flexibility should be treated as an alternative to network investments given the conditions are right: ‘(CEP mandates) they should use flexibility for grid purposes. And regulators should create conditions that incentivize this’, says a senior expert in the Finnish TSO in Interview B. This package has been implemented in Finland by 2020 and is currently going through a trial phase. When implemented fully, it will influence the role of the DSO as a buyer of flexibility, as it ensures non-discrimination among various grid stability tools. Furthermore, the CEP will also address the barrier for smaller consumers and prosumers being a part of flexibility marketplaces.

Finally, we have noticed an ambiguity regarding regulatory sandbox legislation. It can be an issue impeding the LFM development in case a trial run is required. This problem becomes particularly apparent if an actor in a trial run wants to scale up their activities. A senior regulator commented, ‘our current legislation is not very straightforward on that’ in Interview G. Scaling up of operations might be needed in some instances where a larger sample size or geographical area is needed to simulate a realistic setting. Under current legislation, it might not be easy to accomplish as the extent of the sandboxes is not clearly defined.

4.2. Platform Governance

Section 4.2 presents the key findings concerning platform governance, including strategy, platform acceptance, and coalition building (see Table 4).

4.2.1. Platform Strategy

For platforms wanting to break into the energy sector, the network and the stakeholders in the ecosystem should be carefully considered when designing the strategy concerning entry and positioning logic. According to our informants, the overarching Finnish grid strategy is spearheaded by network investments; for instance, a development director from an energy services company comments in Interview A: ‘(in Finland) we are digging up the entire distribution system and installing cables. Doing so means that the distribution component here will be far longer used and far more used than in many other countries. From a platform perspective, this implies that the network’s ability to connect with DERs is limited, as not enough smart technology is integrated. Moreover, since a principal reason for this focus is rooted in ensuring the security of supply, this situation is unlikely to change shortly.

Not all smart meters in Finland currently have the required interface for demand response management, adding another layer of complexity for DER-platform integration. This situation casts a profound effect on designing profitable business models that want to bring households into its fold. The state agencies are in the process of updating these, and by the year 2025, there should be enough smart meters capable of responding to demand response signals. However, until then, we require flexibility enabling gadgets to be installed on the premises. These gadgets, along with their installation, make for a high cost: ‘the cost (per household) can be as high as 700–1000 euros, and if that cost is not repaid at a reasonable period of time then it is a difficult business case’, commented an aggregator Operations Manager in Interview I. It appeared that any real business case would entail sharing this cost with the prosumers, having implications for the platform’s operatory and financial schemes.

Furthermore, a 100 KW threshold is currently in effect to join the energy marketplaces in Finland, which constitutes an obstacle for household-level consumers from directly taking part. As abovementioned, from an LFM platform perspective, which wants to activate end consumers, this comes as a roadblock and stresses the platform’s adaptability to aggregation services. Our findings indicated a strong momentum in favor of this barrier since lifting this limit raises the risk of increased operational costs for the whole system; as stated by a market regulator, ‘of course, we would like consumers and prosumers to be more active in markets. But it has been problematic if it actually increases the whole system operating costs’ in Interview G.

Coming to the possible economic models in the platform marketplace, we observe a clear preference on market-based approaches; a TSO specialist in Interview C says: ‘our main principle is that price is formed on the markets, and when there is enough liquidity, the flexibility is used where there is the most value for it’. The energy market is strongly liberalized in Finland, and instruments to influence the prices (subsidies, regulatory incentives) are not preferred. The market regulators, in this respect, are unwilling to follow the French or German models vis-à-vis regulated consumer prices or subsidizing energy storage systems. Instead, they want to leave it to the market and work towards a change in DSO tariffs on household batteries. Therefore, any economic strategy of the platform must brace itself for market-driven pricing for its product offerings and allow true competition among its participants. Moreover, system operators cannot own or operate batteries in Finland as they must purchase them from third parties, bringing opportunities for an LFM platform since it is a market-driven avenue to such DER services.

Put together, these issues are will influence the way an LFM platform operates in this particular ecosystem. However, when addressed carefully, the challenges listed here can also act as catalysts that might give the platform a realistic chance of surviving in the ecosystem.

4.2.2. Platform Acceptance

Concerning the platform’s acceptance by the energy ecosystem, there exist similarities between the industrial consumers and their household counterparts, with their need for monetary benefits in participating in flexibility arrangements. This could be seen in this statement by a potential industry participant in Interview F: ‘I would need to be fairly confident and sure that this is going to be a profitable decision’. Similar sentiments are also echoed from the household side of the market. Furthermore, for industrial participants, the profitability of participation should also be weighed against the potential layer of organizational complexity it might add. In other words, the system integration with the platform should be seamless, requiring little effort from the participants’ side. Superior customer service and ease of navigating the platform were also mentioned, as could be seen with this aggregator in Interview I: ‘it should be easy to use and the reporting process as easy as possible’. Therefore, operators should carefully consider user profitability, friendly experience, and integration with existing frameworks when conceptualizing the platform schemes.

Platform transparency is essential to attract and maintain adoptions. An important issue here is delivering what is sold. In the event of a delivery failure, the penalties should be laid down. In this instance, our findings indicate that the penalties set by the Finnish TSO are an acceptable remedy: ‘they (penalties for non-delivery) can be like the ones that Fingrid already has on their market’, stated an aggregator operations manager from Interview I. It was also mentioned that the penalties for delivery failures should be similar for participants regardless of their size or position in the market (e.g., aggregators or DSOs). Another point of emphasis is that the platform must also clarify the aggregator rules concerning their suppliers, ensure fair play, and ward off any potential loopholes: ‘if there is an independent aggregator (it); the same connection point has two suppliers. And the rules between these two suppliers must be clear enough. And fair enough. Otherwise, there might be a place for loopholes’, reflects a TSO specialist in Interview C.

Coming to the BRP point of view, the platform must ensure that the flexibility suppliers can indeed keep their end of the bargain: ‘when it is the decision not to invest on the (electricity production) but the flexibility, then it kind of requires quite trustworthy security from the platform side’, stresses the Head of a BRP Risk Management unit from Interview D. As a remedy, we can highlight the experts’ suggestion from the energy industry interest group, who stressed the need for prosumer verification as a tool ensuring supplier accountability, based on agreements with the aggregators, in Interview H: ‘different verification methods are needed by different marketplaces… (and in case of a flexibility market) verification requirements should be based on what would be acceptable for aggregation to verify’.

Market liquidity was stressed as an antidote against high volatility, which can be ensured by high prosumer participation in the platform. Automated bidding in the platform has been recommended to encourage such participation as prosumers might not have the needed knowledge to participate in the bidding themselves. As observed by a TSO expert from Interview B, ‘(it may be so) customers will never participate directly in this existing market because it is too complicated for them…the bidding process is especially difficult for them’. Domain automation has been suggested to alleviate this issue, making it easier for other smaller players to be part of the platform.

Another factor that might influence prosumer participation in the marketplace is double taxation, which applies when exporting energy to the grid and repurchasing it for consumption when needed. However, it was not seen as a significant barrier, as there are no taxes incurred for self-consumption: as ‘taxation is not so big problem for these small customers’, because ‘many are charging their batteries from their own production and free from the electricity tax’, as observed by industry experts in Interview H. However, considering the uptake of EVs, we can see a potential problem stemming here when households can participate with the grid to a greater extent: ‘in the future, if, for example, charging and discharging EVs would come into a question, maybe there could be a problem with double taxation’ reflected the experts. Therefore, the recommendation for the flexibility platform is to stick to the power or frequency-based markets and not in energy markets, to ward off double taxations further.

4.2.3. Coalition Building

Regarding coalitions in and around the flexibility marketplace, we observed the need for cooperation frameworks among the different grid players, namely, between the TSO and the DSOs and among the DSOs themselves. This issue represents a much-discussed area that determines many future possibilities concerning flexibility utilization. A specialist from the TSO comments in Interview C, ‘(regarding inter DSO cooperation) it is a timely question…that we are actually thinking a lot about (and) many of our people focusing quite heavily on exactly that topic’. When designing the coordination framework, Finland is looking at the Dutch model as a promising option. In the Netherlands, the DSOs have developed a joint platform to communicate the grid bottlenecks and deploy flexibility as a potential solution.

Moreover, regarding TSO-DSO cooperation, the Dutch model employs a platform as well. Therefore, Finland could opt for a similar setting as it addresses this issue. However, a significant difference between the context of these two countries can be found in the number of DSOs. Whereas the Netherlands only has five DSOs, in Finland, the number is well into the 70s [55].

Coordinating with the end resources appeared as another roadblock in achieving the full flexibility potential. The Development Director from an energy advisory firm views the offerings to solve this issue as unstructured; he further comments in Interview A: ‘to solve this we have very heterogeneous offering out there if we can provide structure to that, if we can provide the capability to that then it (flexibility marketplace) is easily implementable’. Although we register a cautious optimism for a flexibility marketplace, we should also highlight a certain reticence towards adopting this platform, which might appear primarily among the well-rooted industrial players. For instance, a senior executive from a large industrial organization states in Interview F, ‘I have been working in this sector for so many years, and I am so accustomed and used to working with the existing markets’. While this mental disposition is not a decisive driver, it does present an obstacle in adopting a new marketplace, especially if it falls short of providing a clear business case.

The challenge to bring end consumers to a flexibility platform is a prominent one. For instance, the topic of flexibility or its benefit are well known to larger stakeholders. However, a regular consumer might not be familiar with the phenomenon or its benefits. Therefore, convincing them to participate remains difficult. For example, the Business Director from a large retailer explains in Interview D, ‘it is very difficult to explain to normal people, domestic customers, how the market works and what flexibility actually is and what benefits the customer might get from the flexibility’.

Moreover, there seems to be a lack of specialized infrastructure in this case. A Development Director from the energy services provider highlighted the need for B2B-centric communications to evolve to reach out to the end customers. As elaborated in Interview A, ‘a principal challenge right now is the lack of endpoint spokesperson. The networks, suppliers, TSOs are all very established and can talk to the stakeholders. But the endpoints of the transition and the forming groups do not have to say in the matter’. This situation calls for specialized B2C communication regimes for the platform.

Lastly, aggregators are emerging in this ecosystem, and their roles and responsibilities have been slowly taking shape. Particular attention should be paid to the incumbent actors in the marketplace that could be impacted by aggregators (e.g., retailers or the BRP). We noticed a degree of anxiety among the retailers with some facets of the possible business models. As a senior executive from a retailer elaborates in Interview D, ‘(among the) four different types of aggregation models proposed…the most brutal was so that the aggregator would just aggregate and all the energy that is not consumed would be then counted as an aggregators profit’. This model, proposed by the Smart Grid Task Force, places retailers in an awkward position because it allows the aggregator to profit through the energy the retailer had bought in the first place. The possible repercussion for such rules could be the reluctance to admit aggregators in the ecosystem, which in turn hurts the prospects for a flexibility marketplace, as evidenced in this statement from a large retailer in Interview F.

‘If somebody gets hurt, this somebody will do everything to prevent flexibility from happening. And if this somebody is an electricity sales company, that has a relatively strong, grip of the customer and has very good channels of communicating with the customer and so forth’.

Therefore, the platform must ensure an acceptable profit-sharing mechanism concerning the unconsumed energy, as conveyed in this retailer statement in Interview D: ‘in the more acceptable models, there is some settlement price for the energy that is not then consumed that how you share somehow the profit’.

Finally, the issue of balancing responsibility for the aggregators emerged as a matter of importance. If aggregators are required to take full balance responsibility, that will entail a 24/7 operational activity on their part, which might serve as an entry barrier for smaller operators, with particular implications for the aggregator dynamics within the platform. On the other hand, from the retailer’s point of view, it appeared that they prefer aggregators taking on the balance responsibility by themselves. As observed by the Head of Risk Management from Interview D:

‘if the aggregators are playing, so that that the seller of the initial energy is going to pay the bill, then they are not welcome. But if the aggregators, for example, if they would take the balance responsible for themselves, then why not.’

5. Discussion

The blending of perspectives from platform governance and LFM design, as expressed using Tura et al.’s [48] platform design framework, served as the starting point of our discussion. As expressed in Figure 3, we considered the following areas: platform architecture, value creation logic, governance and practices, and platform competitiveness. However, after analyzing the Finnish energy ecosystem, a new and distinctive area emerged that was not fitting in the pre-determined fields. This area concerns the readiness for the ecosystem to accept and adopt such a platform and is a precursor to further platform developments. Therefore, we amend the original framework by introducing a new dimension: Ecosystem Readiness (see Figure 5). We also merge Platform Architecture with Platform Governance and practices since both areas have a more internal platform-centric focus and complement each other well in the context of a novel platform.

5.1. Ecosystem Readiness

For an LFM to operate in the Finnish energy landscape, the overall electricity network situation must be considered designing the operational and business models. The network’s conditions and its development considerably affect DER integration with the LFM since the network’s ability to connect to distributed resources remains limited, affecting the value propositions of the platform’s potential partners [35]. Besides the network, risk-sharing among the platform participants has been stressed for platform design [42]. Here we stress the need for the specific mechanisms that allow sharing the upfront costs of flexibility gadgets and their installations at a household level. Our findings indicated that this sum can reach anywhere between 1000 to 1500 euros due to the high labor costs in Finland. This cost increases the threshold for investments for any platform operator, and its solution should include a cost-sharing regime with the consumers. Relating to this topic, Euchner [44] identified the technological environment as a significant denominator in the platform’s ecosystem, and here we stress the smart meters situation in Finland. Currently, not all smart meters can be used for demand response integration; however, by the year 2025, all these meters will be updated to accommodate demand response, which might significantly influence the technological investments needed for the stakeholders.

Furthermore, the integrational capability of smart meter technology also depends on the advent of Datahub, the Finnish TSO’s centralized data exchange. Datahub comes into active operation on February 2022, which impacts DER integration with the grid, corresponding to Olivella-Rosell et al. [17] and Ramos et al. [5]. The next challenge for the Finnish ecosystem is to ensure technological reliability, which ushers in further momentum to the platform development [1]. Another major challenge in this ecosystem is ensuring direct prosumer participation in the energy markets. Euchner [44] pointed out that the threshold to participate in the platform should be low enough to accommodate the needed userbase; however, with the LFM, households face barriers most prominently in the form of a 100 KW energy output requirement but also in terms of knowledge gaps and insufficient monetary incentives.

The solution for the time being lies in the aggregation of prosumer-generated electricity, but the LFM should move towards direct prosumer involvement in the long term. Aggregation in this ecosystem is an emerging concept, and the rules concerning independent aggregation are still taking shape. The regulatory authorities should move towards codifying the rules between aggregator’s suppliers to ensure fair competition. Otherwise, we may run into what Adner et al. [46] termed ‘adoption chain’ risk in the platform’s ecosystem.

Lastly, regulatory sandboxes for LFMs are not well defined in Finland, and this might prohibit platform growth. In particular, for an LFM platform wanting to test the market by conducting large-scale tests might run into a problem as the size and scale of sandboxes are not defined.

5.2. Platform Architecture and Governance

Tura et al. [48] proposed investigating platform leadership, ownership, and platform governance and operations rules. The design problems studied here are managing the platform, ownership nature, the internal rules and processes governing the platform itself or its services.

Designing the governance structure of the LFM platform requires careful consideration of the regulations and legislations present in the energy ecosystem. The burden of regulatory constraints starts already at the ownership stage, as not all entities are allowed to own and operate this platform. As Bouloumpasis et al. [38] pointed out, the system operator participation in the LFM is a contested topic as it might stand in the way of fair competition. We have seen this fear reflected in EU regulations barring both TSOs and DSOs from operating such markets [39]. We have also seen the impact of this legislative decision already in a Norwegian LFM platform that started as a TSO venture but had to disassociate themselves from any ownership and operational influences on the platform. Therefore, in the Finnish context, too, this platform must be owned or operated by a party not related to system operators.

Following that, Ramos et al. [5] proposed two possibilities regarding the operationalization of the LFM, either as a sub-market of the wholesale market or a novel exchange platform run by the system operators or a third party. Unfortunately, regulation already crosses out system operators from this equation, and we do not have enough data from the wholesale markets in Finland to judge the other possibility. However, our findings validated the possibility of LFM operating as a third-party operator, particularly in localized settings, where ownership entities may include energy communities, housing companies, or municipalities.

Developing the governance mechanisms also includes penalty rules [48]. We have noted that the non-delivery of services to be a big concern among the potential stakeholders. It appeared that market parties agree on the Finnish TSO’s penalty regime for transactional issues and would welcome similar instruments in the LFM. It is also imperative to ensure that penalties are non-discriminatory towards the participants, regardless of their size or grid status.

Furthermore, developing comprehensive platform governance rules are particularly apt, as Fenwick et al. [1] observed that the current frameworks governing the market are not equipped to enact a thriving platform culture. Moreover, there is a high degree of informal expectations for the regulated energy sector that must be sustained, such as data security [37]. In this regard, the subscription to the GDPR and promoting this fact to the public will help the platform gain consumer confidence. The platform must also focus on developing coherent internal processes in the partner companies [37], as it generates synergy and reduces the risks of misalignment, leading to lesser needs for punitive measures.

Moving on to platform architecture, deciding on the market structure (i.e., two-sided vs. multi-sided) and identifying and including the relevant stakeholders are crucial decisions [48]. Thus, platform strategy is vital in this phase as it sets the course for architecture development. Gawer and Henderson’s [33] view of platforms (as a component of a dynamic technological system with a strong interdependency among the sub-components) is especially suitable here because, in order to facilitate energy flexibility, LFM platforms’ must also facilitate exchanges of communication, knowledge, and financial transaction among other services. This suggestion is also in line with Fenwick et al.’s [1] proposal of platforms as a system facilitating a broad consortium of services.

In designing the platform’s market structure, the economic viability of the platform calls into specific considerations. For example, Gawer and Cusumano [42] identified pricing as a central question in the platform business model. In Finland, we have registered a stakeholder preference towards market-driven pricing. Unsurprisingly, price manipulation instruments such as subsidies or regulatory incentives are deemed unnecessary in Finnish energy markets.

In developing the platform architecture identifying key actors are necessary [48]. According to Jin et al. [37], LFM boundaries are usually understood through spatial constraints. As such, this already tilts the LFM stakeholder landscape to a more geographic setting. Our findings were consistent with this suggestion, as we noticed LFMs’ to have particular suitability for remote locations. However, regardless of its location, it is still operating in conjunction with the grid and must consider the system operators: DSOs’ are immediately relevant, and the TSO, too, if the platform aims to be active on a national level. Following Bouloumpasis et al. [38], other important actors needed to activate an LFM are the balance responsible parties, the consumers and prosumers, and the market operator. Here we propose to add the regulatory authorities to this list; LFM platforms are still a novel concept, and as such, intimate consideration of the regulatory bodies facilitates its development process.

5.3. Value Creation Logic

Value creation logic concerns defining the platform benefits and how the platform actors instigate this value. It further constitutes delineating stakeholder roles, evolutions, value propositions for the different participants, and the revenue model for the platform and its participants [48].

First off, we see evidence of the need for profitable stakeholder participation, as stressed by Gawer and Cusumano [42]. This sentiment is echoed in commercial entities such as industrial actors and smaller entities such as prosumers. Therefore, designing the value propositions, the financial incentives should be considered carefully. However, as we hinted in the previous section, reaching out to end consumers is made difficult by an output requirement of 100 KW in Finland. These circumstances call for the involvement of aggregators in the platform. Aggregators are a new concept to the current grid, and its regulatory and business frameworks are taking shape. A critical issue to consider here is being mindful not to affect any of the incumbent players with this development adversely. Retailers, for example, could be negatively impacted as aggregators take place in the ecosystem. To avoid an impasse, aggregator business models must ensure that profits will be shared with the retailers when both parties are involved in a transaction. Lastly, concerning aggregators, we find more symmetry with the LFM design frameworks considering aggregators, and if a flexibility marketplace wants to involve end consumers in its midst, their role is nearly unavoidable in the Finnish context.

Communication plays an essential role in facilitating stakeholder roles and the value chain, cf. Fenwick [1], as the platform reaches out to its potential userbase and develops credibility. However, our findings indicated that the traditional B2B communication in this ecosystem needs to evolve to reach the end consumers. In addition, we noticed a dearth of awareness regarding flexibility or its benefits among the end consumers. Furthermore, it becomes easier to establish a positive perception of the demand response utility with effective communication, which is paramount to attracting and retaining a user base [41]. Therefore, both the platform operator and its stakeholders on the buying side must develop B2C communication frameworks to start an ongoing dialogue with the consumers.

With adequately exercised communication, it also becomes easier to establish the potential benefits for the actors on the platform, an essential factor stated by Davis [47]. In this regard, among the potential institutional stakeholders, typically on the buying side, we have noticed a pragmatic attitude towards an LFM platform. This platform can complement efforts to reduce overall energy consumption for the retail sector, especially during the high spot-priced hours. Furthermore, this platform also can offer some relief to the increasingly rigid energy production, as Finland is increasing its share of nuclear and wind energy. Once they have been initiated into the marketplace, the end consumers or prosumers will have monetary incentives to utilize their DERs to extract the highest flexibility potential.

As proposed by Esmat [40] or Minniti [15], the DSO’s role in this platform is particularly noteworthy through their LFM frameworks revolving around DSO issues. Our findings validated the literature with DSO utility from the LFM concerning congestion management, voltage violations, and alternative grid re-enforcement. We could point out that these issues have manifested in a UK-based flexibility platform currently in commercial operation. This UK-based platform is designed with DSOs exclusively on the buying side. In the Finnish context, we have registered a resonance with this design where system operators exclusively occupy the buying side. In general, the regulatory authorities in Finland are receptive to the idea of competitive sourcing of flexibility for the DSOs, especially in remote locations, where an LFM can enact market competition.

Finally, the TSO role is also essential to this platform. Although the EU regulations bar TSOs from operating an LFM platform, they can purchase flexibility at a central level. In the EU, there is an ongoing discussion, as Bouloumpasis et al. [38] pointed out, as to should the TSO participate directly in the market or play a facilitating role. In Finland, we have seen a willingness for the TSO to be a direct party in the LFM, initially adopting a buying role if sufficient demand is not being generated.

5.4. Platform Competitiveness

The last area identified by Tura et al.’s [48] platform design framework relates to the competitive atmosphere of the platform. This issue encompasses ensuring easy access, addressing the chicken-and-egg problem, and the growth prospects of the platform. Firstly, the chicken and egg problem is a common issue for platform design, referring to the difficulty of attaining a critical mass to garner a positive feedback loop [56]. In other words, demand and supply are interdependent and it is difficult to generate one without the other. It is even more relevant for a novel platform, and as such, our findings indicated that a higher degree of effort should be placed on the supply side. Since the energy demand is constantly increasing and energy production is becoming inflexible, demand response is on a good trajectory.

Moreover, we have seen the willingness among the institutional players, such as system operators, to be the market maker if there is not enough demand initially. The supply side is more unorganized and requires more effort for mobilization. On the other hand, households being the smallest target suppliers, an effective organization requires much effort, especially in a novel platform.

Jin et al. [37] observed that most formulations of LFM models are centralized, which can take two propagations based on their objectives, social welfare, or minimizing operational costs. Therefore, deciding on the intent of the LFM is very important in the current climate. Firstly, we have to consider the technological landscape, where not all smart meters can enact demand response, erecting a barrier to end-consumers profitability. Adding to that is the current situation of flexibility being treated as OPEX, which prefers grid reinforcement. However, this situation will change in 2024 when the new regulatory model goes into effect.

Therefore, it remains a challenging ordeal for an LFM platform seeking profitability in the short term. However, the ecosystem does believe in the long-term commercial prospects for this marketplace as DER penetration intensifies and battery technologies are improving. The EV figures are believed to be a good indicator in this regard. At least for the time being, it might be better to opt for LFM models that maximize social benefits given the existing conditions. Neighborhood-based energy communities and LFMs operated by housing companies where the goal is to promote sustainability rather than profit could be the use cases of this frame. Furthermore, we also see credence for social welfare maximizing LFM models from existing platforms which, among other issues, finds it difficult to compete with the Spot market price. One such platform from Germany admitted that price alone cannot be the competing point for such platforms and that a social angle is needed to sustain it.

Based on the above discussion, we revise the theoretical framework proposed in Figure 3. In addition, the intersecting region containing the LFM development focus areas is elaborated with the key findings of our study.

6. Conclusions

With the increasing technological possibilities in the grid and the overall regulatory and political reality in Finland, the momentum propelling LFMs can only increase. Taking platform perspective into account, we can facilitate this novel idea further to design optimal governance and business models for the demand response markets. The primary contribution of this paper was to serve as a starting point to that discussion.

For policymakers and practitioners, this study identified various LFM implementation challenges. The critical barriers are relevant now but that can potentially be solved in the near term are the OPEX treatment of flexibility, prioritizing network reinforcement over demand response, and the high costs for smart device installation at the household level. On the other hand, more long-term challenges arise from the Finnish grid’s focus on traditional network development, often unable to connect DERs at the endpoints. Moreover, a significant challenge remains in garnering an attractive financial return for LFM participants, which is more applicable for smaller consumers.

However, this paper also identified many possibilities for an LFM in the Finnish context. As the energy production mix becomes inflexible, it calls for flexibility on the demand side. The ongoing implementation of the CEP opens up new avenues for demand response. Furthermore, we observed a positive view from the regulators who see this platform as promoting the free market principles for flexibility procurements. In the liberalized energy markets in Finland, this is an important benchmark.

Theoretically, this paper introduced platform perspective to LFMs and contextualized a platform development framework in the novel LFM development. However, a significant contribution of this paper was the addition of a new dimension to novel platform development: Ecosystem Readiness. While adopting a platform development framework, we noticed that for novel platforms, especially in emerging sectors, the more significant ecosystem readiness appeared as a distinct and foundational dimension for platform development. We believe that the utility of this addition to the platform development framework could potentially help understand the novel platform development processes better.

The main limitation of this research was the lack of primary data from operating LFMs. As we do not have such marketplaces in Finland, we had to rely on similar European projects. Except for one, all these platforms are in a development phase. Consequently, the data garnered from there were often hypothetical. We also had to consider the differences in the market context and the platform focus. Even after contextualizing the findings to a Finnish setting, there could be a gap in its appropriation. Our principal source of data was the Finnish energy sector, and by casting a wide net, we collected broad and holistic perspectives. However, doing so meant that we had to forfeit the opportunity to go deeper into actor perspectives.

Thus, we recommend highlighting the actor-specific flexibility requirements in future research on this topic (for instance, actor-centric LFM design particularities). In addition, a study devoted to the regulatory challenges and opportunities to LFM services in Finland would also be timely. Lastly, another prominent contribution to this topic could be to look into the aggregator-retailer interaction in a flexibility context.

Author Contributions

Conceptualization, N.R. and R.R.; methodology, N.R.; investigation, N.R. and R.R.; writing—original draft and preparation, N.R.; writing review and editing, R.R., J.P., A.R. and N.R.; supervision, R.R. and A.R. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Business Finland as part of the FLEXIMAR (Novel Marketplace for Energy Flexibility) project.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fenwick, M.; McCahery, J.; Vermeulen, E. The end of ‘corporate’ governance: Hello platform governance. Eur. Bus. Organ. Law Rev. 2019, 20, 171–199. [Google Scholar] [CrossRef] [Green Version]

- Treffers, D.; Faaij, A.; Spakman, J.; Seebregts, A. Exploring the possibilities for setting up sustainable energy systems for the long term: Two visions for the Dutch energy system in 2050. Energy Policy 2005, 33, 1723–1743. [Google Scholar] [CrossRef]

- Bevilacqua, M.; Ciarapica, F.; Diamantini, C.; Potena, D. Big data analytics methodologies applied at energy management in the industrial sector: A case study. Int. J. RF Technol. Res. Appl. 2017, 8, 105–122. [Google Scholar] [CrossRef]

- Emmerick, P.; Hülemeier, A.; Jendryczko, D.; Baumann, M.J.; Weil, M.; Baur, D. Public acceptance of emerging energy technologies in the context of the German energy transition. Energy Policy 2020, 142, 111516. [Google Scholar] [CrossRef]

- Ramos, A.; Jonghe, C.D.; Gomez, V.; Belmans, R. Realizing the smart grid’s potential: Defining local markets for flexibility. Util. Policy 2016, 40, 26–35. [Google Scholar] [CrossRef]

- Solomon, B.D.; Krishna, K. The coming sustainable energy transition: History, strategies, and outlook. Energy Policy 2011, 39, 7422–7431. [Google Scholar] [CrossRef]

- USEF Foundation. USEF: The Framework Explained; USEF: Lexington, KY, USA, 2015. [Google Scholar]

- Schittekatte, T.; Meeus, L. Flexibility markets: Q&A with project pioneers. Util. Policy 2020, 63, 101017. [Google Scholar]

- Hadush, S.Y.; Meeus, L. DSO-TSO Cooperation Issues and Solutions for Distribution Grid Congestion Management. Energy Policy 2018, 120, 610–621. [Google Scholar] [CrossRef] [Green Version]

- INTERRFACE Report. TSO-DSO-Consumer INTERFACE aRchitecture to Provide Innovative Grid Services for an Efficient Power System; CORDIS: Luxembourg, 2019. [Google Scholar]

- Lind, L.; Avila, J.P.C. Deliverable D1.1. Market and Regulatory Analysis: Analysis of Current Market and Regulatory Framework in the Involved Areas. CoordiNet. 2019. Available online: https://www.iit.comillas.edu/docs/IIT-19-051I.pdf (accessed on 7 March 2021).