Using Financial Instruments to Transfer the Information Security Risks

Norwegian Information Security Lab., Gjøvik University College, Teknologivn 22, 2815 Gjøvik, Norway

*

Author to whom correspondence should be addressed.

Future Internet 2016, 8(2), 20; https://doi.org/10.3390/fi8020020

Submission received: 5 November 2015

/

Revised: 22 April 2016

/

Accepted: 27 April 2016

/

Published: 17 May 2016

Abstract

:For many individuals and organizations, cyber-insurance is the most practical and only way of handling a major financial impact of an information security event. However, the cyber-insurance market suffers from the problem of information asymmetry, lack of product diversity, illiquidity, high transaction cost, and so on. On the other hand, in theory, capital market-based financial instruments can provide a risk transfer mechanism with the ability to absorb the adverse impact of an information security event. Thus, this article addresses the limitations in the cyber-(re)insurance markets with a set of capital market-based financial instruments. This article presents a set of information security derivatives, namely options, vanilla options, swap, and futures that can be traded at an information security prediction market. Furthermore, this article demonstrates the usefulness of information security derivatives in a given scenario and presents an evaluation of the same in comparison with cyber-insurance. In our analysis, we found that the information security derivatives can at least be a partial solution to the problems in the cyber-insurance markets. The information security derivatives can be used as an effective tool for information elicitation and aggregation, cyber risk pricing, risk hedging, and strategic decision making for information security risk management.

1. Introduction

In today’s hyper-connected world, currently cyber-insurance products are the only way of handling the residual information security risks. Recent incidents of cyber-attacks on various organizations [1] prove that even the most sophisticated technical defense systems are not sufficient to mitigate the residual (adverse financial) impact of cyber-security events. Thus, cyber-insurance products provide an opportunity to individuals and organizations to spread their risks. This ensures that no single entity receives a financial burden that is too large for it to bear. However, cyber-insurance markets are susceptible to information asymmetry between buyers and insurers, and between insurers and re-insurers; thus raising the cost of the transaction and inhibits transparency. Furthermore, due to interdependent and correlated nature of information security risks, the uncertainty about the quantum of risk exposure leads to the fear of systemic and huge losses for cyber-(re)insurance providers. This difficulty in quantifying the information security risks leads to underestimation of future losses, thus cyber-(re)insurance providers are incapable in underwriting the catastrophic impact of cyber risks [2]. Thus, in absence of adequate market mechanisms for risk acceptance, the interest of information security stakeholders who wish to transfer their risks and those who are willing to accept the risk are reduced. Furthermore, the World Economic Forum in its annual risk report stated that “A critical element in advancing this (on cyber risk management) discussion will be improving the collective ability to measure the economic impact of cyber risks, at all levels—within individual businesses, nationally and globally. Effective methods for measuring and pricing cyber risks may even lead to new market-based risk management structures, which would help in understanding the systemic inter-dependencies in the multiple domains that now depend on cyberspace” [3].

In theory, capital markets can be an effective mechanism to undertake a high impact and correlated information security risks. Capital market-based financial instruments can be developed as a risk transfer mechanism with the ability to absorb the risk of catastrophes and their potential to add liquidity and transparency to the risk transfer market [4,5,6,7,8,9]. Thus, the task of creating an information security risk market for risk transfer (hedging) faces two key challenges. The first is to design the market where various information security related financial instruments can be traded, and, second, the specification of financial instruments (derivatives/contracts) to address various information security risks. This article deals with the second problem, i.e., the specification of information security derivatives to allow hedging of risk exposure to the underlying information security event. The first challenge of designing an Information Security Prediction Market (ISPM) to allow the trading of such financial instruments has been addressed in [10,11,12].

The primary goal of a prediction market is to elicit and aggregate information about the trading contracts’ underlying events. Like other prediction markets, ISPM will allow traders to express their probability assessment for the possible outcome(s) of the underlying event. This is achieved by the trading of financial instruments (contracts), and the traders with more accurate predictions than others are compensated for the same. Thus, the participants have an economic incentive to improve the market accuracy by revealing any relevant information they may have. Therefore, in addition to the goal of achieving information elicitation and information aggregation, financial instruments trading at ISPM can be used as a mechanism for measuring and pricing of cyber risks and as a mechanism to transfer/hedge the underlying cyber (information) security risks. The market (ISPM) observers and participants can use the market information for strategic level cyber (information) security risk management decisions. Such decisions (to invest in security controls, deployment of necessary security tools, formulate organizational security policy, implementing regulatory compliance requirements, etc.) can benefit from the knowledge and perspectives of a large and diverse group of people participating in ISPM.

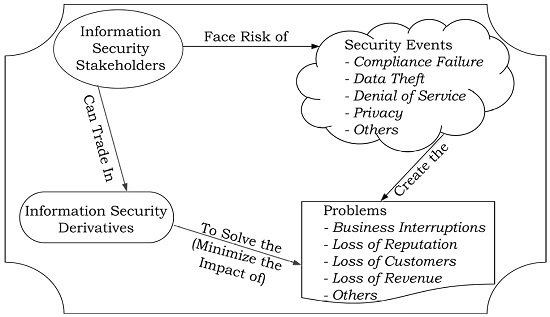

This article presents a set of specifications for Information Security Derivatives (ISD) that can be traded at an information security prediction market, to be used as a mechanism for risk hedging. The article presents a design for a set of ISD, namely Information Security Options (ISO), Information Security Vanilla Options (ISVO), Information Security Swaps (ISS), and Information Security Futures (ISF) that could be used to transfer the risk associated with the underlying information security event. An information security event is a potential source of peril that would cause a loss to the organization when it happens at anytime in the future. The loss (adverse impact) would be a result of damage, destruction, or unavailability of a resource that is critical for the normal operation of the organization. Furthermore, the article demonstrates the application of ISD in a given scenario and presents an evaluation of the same in comparison with cyber-insurance products.

The remainder of the article is structured as follows: Section 2 explains the research method followed for the article. Section 3 presents an overview of the related work. Section 4 explains the research problem addressed in the article. Section 5 identifies the functional requirements for ISD. Section 6 presents the design and development of the ISD. Section 7 demonstrates the application of ISD in hedging the financial impact of information security risks in the given scenario. Section 8 presents an evaluation of the ISD. Section 9 concludes the article with conclusion and directions for future work.

2. Research Method

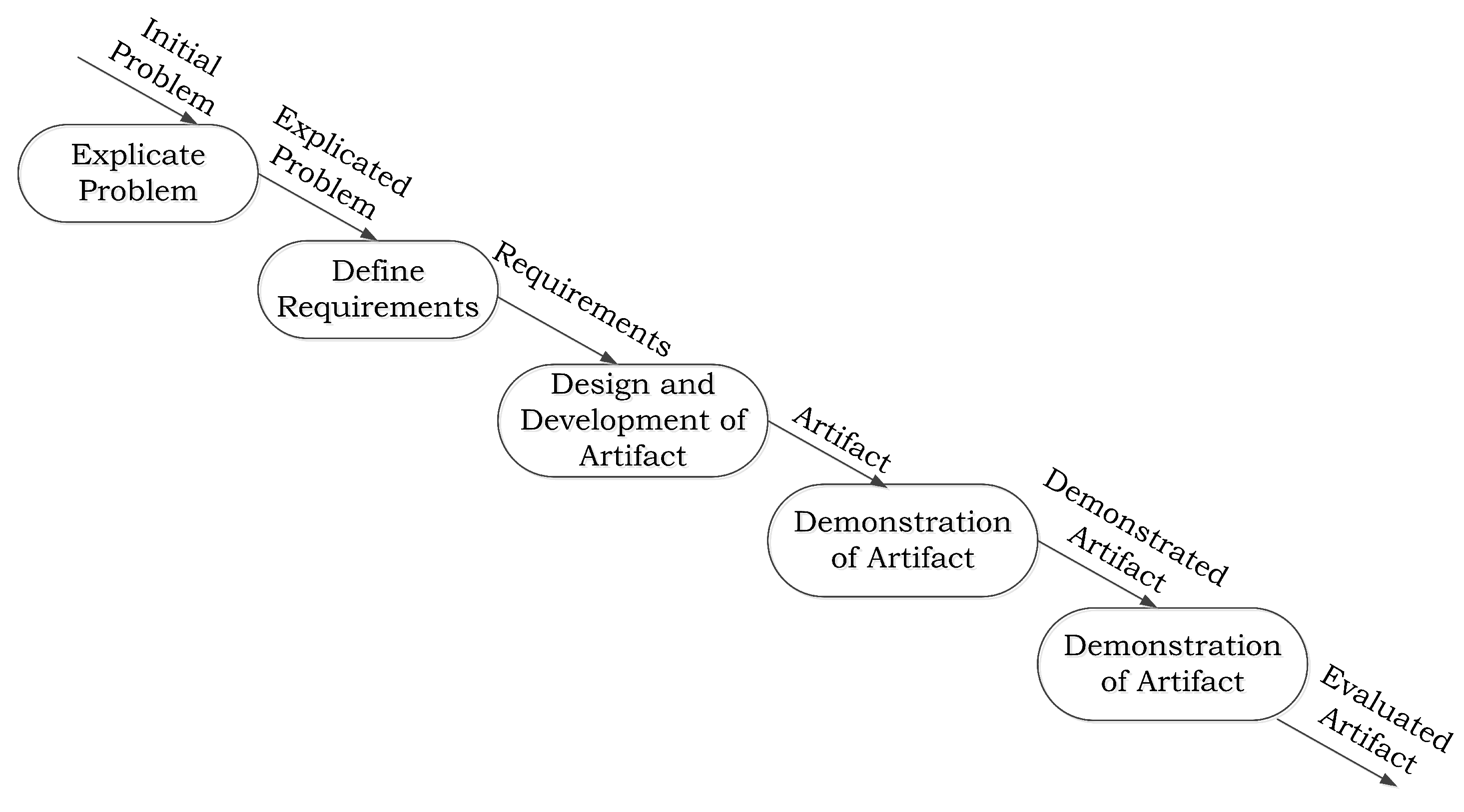

We followed the Design Science Research Approach (DSRA) for this article [13]. DSRA is used when innovations and ideas are created to develop technical capabilities and products for effective and efficient process development for artifacts [13]. Design science research leads to the creation of “knowledge and understanding of a design problem, and its solution are acquired in the building and application of an artifact” [14]. Design science research consists of “analysis of the use and performance of designed artifacts to understand, explain and very frequently to improve the behavior of aspects of information systems” [15]. A process flow model for DSRA is shown in Figure 1.

2.1. Explicate Problem

The DSRA process starts with the formulation of the initial problem, justifying the importance of the problem and investigating the underlying causes of the problem [13]. To explicate the problem, we started with reviewing the literature on information security economics, currently available market methods and financial instruments developed for the management of information security risks. We also reviewed the literature on various financial instruments that are used to manage risks in other domains. This enabled us in identifying the gaps in the literature on the management of financial impact of information security risks in the information security domain. The identified problem is explained in Section 4.

2.2. Define Requirements

The next step in DSRA is to identify and outline an artifact that solves the problem explicated in the previous step. The artifacts include but are not limited to algorithms, languages, human-computer interfaces, and system design methodologies. Rossi and Sein [16] and Purao [17] presented a list of outputs in DSRA. The list includes all the four output types proposed by March and Smith [18], namely “Constructs”, “Models”, “Methods” and “Instantiations”, and a new element in the list is “Better Theories”, as shown in Table 1.

Furthermore, this step elicits the requirements for the artifact [13]. An artifact requirement is defined as the characteristic of the artifact that is to be used for design and development of the artifact. The artifact requirement can be functional, structural, or environmental in nature. To solve the problem identified in the previous step, the functional requirements identified for the artifact are explained in Section 5.

2.3. Design and Development of the Artifact

Design and development of the artifact is the third step in DSRA. This step leads to the creation of an artifact to fulfill the requirements that were identified in the previous step. This step leads to the design of the functionality and structure of the artifact [13]. Section 6 explains the functionality and structure of the artifact.

2.4. Demonstration of the Artifact

The feasibility of the artifact is demonstrated in the fourth step in DSRA. Primarily, it consists of explaining the application of the artifact in one situation [13]. The demonstration is a weak form of evaluation to show that the artifact can, in fact, solve the problem (or some aspects of it) in the given scenario. This demonstration indicates that if the artifact can solve the problem in the given situation, then it might be able to address the problem in other similar situations as well [13]. Section 7 demonstrates the use of the artifact designed and developed in the previous steps.

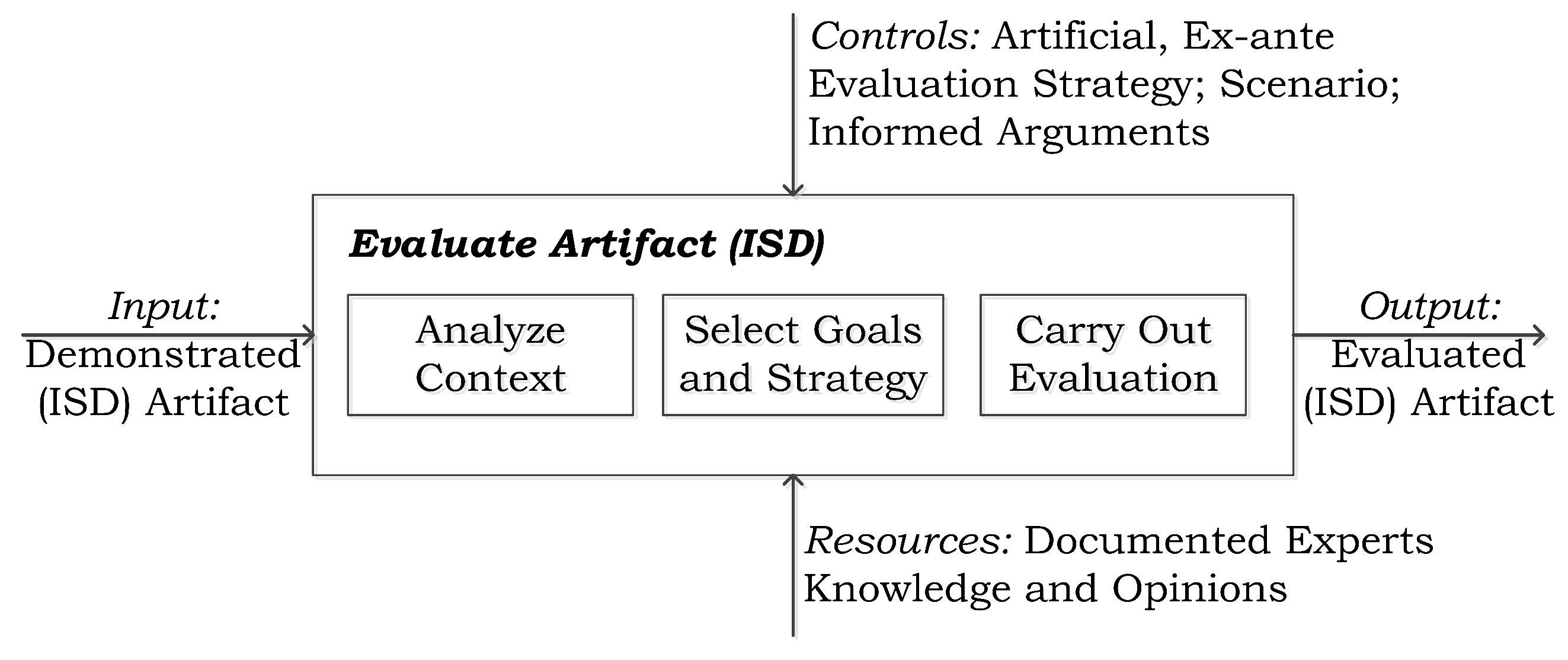

2.5. Evaluation of the Artifact

The fifth and the final step in DSRA is to evaluate the artifact. The evaluation is to determine the extent to which the artifact designed and demonstrated in the previous steps can solve the explicated problem and meets the artifact’s requirements [13]. Under the DSRA, the evaluation strategy can be an ex-ante or ex-post on the one hand and naturalistic or artificial on the other [13]. The strategy of evaluating the artifact when it is being fully developed or used is called an ex-ante evaluation. When the artifact is evaluated after its implementation, the evaluation strategy is called an ex-post evaluation. The naturalistic evaluation means that the artifact is evaluated in practice to assess to what extent it meets the desired objective. On the other hand, when the artifact is evaluated in an artificial and contrived setting, the evaluation strategy is termed as artificial evaluation.

The artifacts are evaluated using the methodologies available in the knowledge base. The evaluation of artifacts can be based on the accuracy, completeness, consistency, functionality, performance, reliability, usability, and other relevant quality attributes. A summary of evaluation methodologies is presented in Table 2.

Section 8 presents an evaluation of the artifact that was designed, developed and demonstrated to address the problems and requirements identified in the previous steps. The evaluation is based on the “descriptive” form of analysis [19]. This consists of constructing “scenarios” around the artifact and using “informed argument” from the knowledge base to demonstrate the usefulness of the artifact [19]. Vaishnavi and Kuechler[20] have called this form of evaluation as “Logical Reasoning”. According to them, the strength of the logical reasoning form of evaluation “depends on the strength and preciseness of its arguments and assumptions” [20].

Informed argument form of evaluation is an ex-ante, artificial evaluation method, and it consists of arguments to evaluate the performance of the artifact [13]. In the informed argument or descriptive analysis form of evaluation, researchers evaluate the artifact by reasoning and arguments for its usefulness in meeting the defined requirements and solving the explicated problem. This form of evaluation is often used to evaluate the artifacts that are highly innovative and are still immature [13]. Furthermore, wherever required, we have used the “comparison” form of evaluation [21], to compare our artifact with the only existing financial mechanism of cyber-insurance to mitigate the information security risks.

3. Related Work

This section is divided into three subsections, one on information security risk management, second on the financial engineering in risk management, and third on the financial instruments designed to hedge a variety of risks.

3.1. Information Security Risk Management

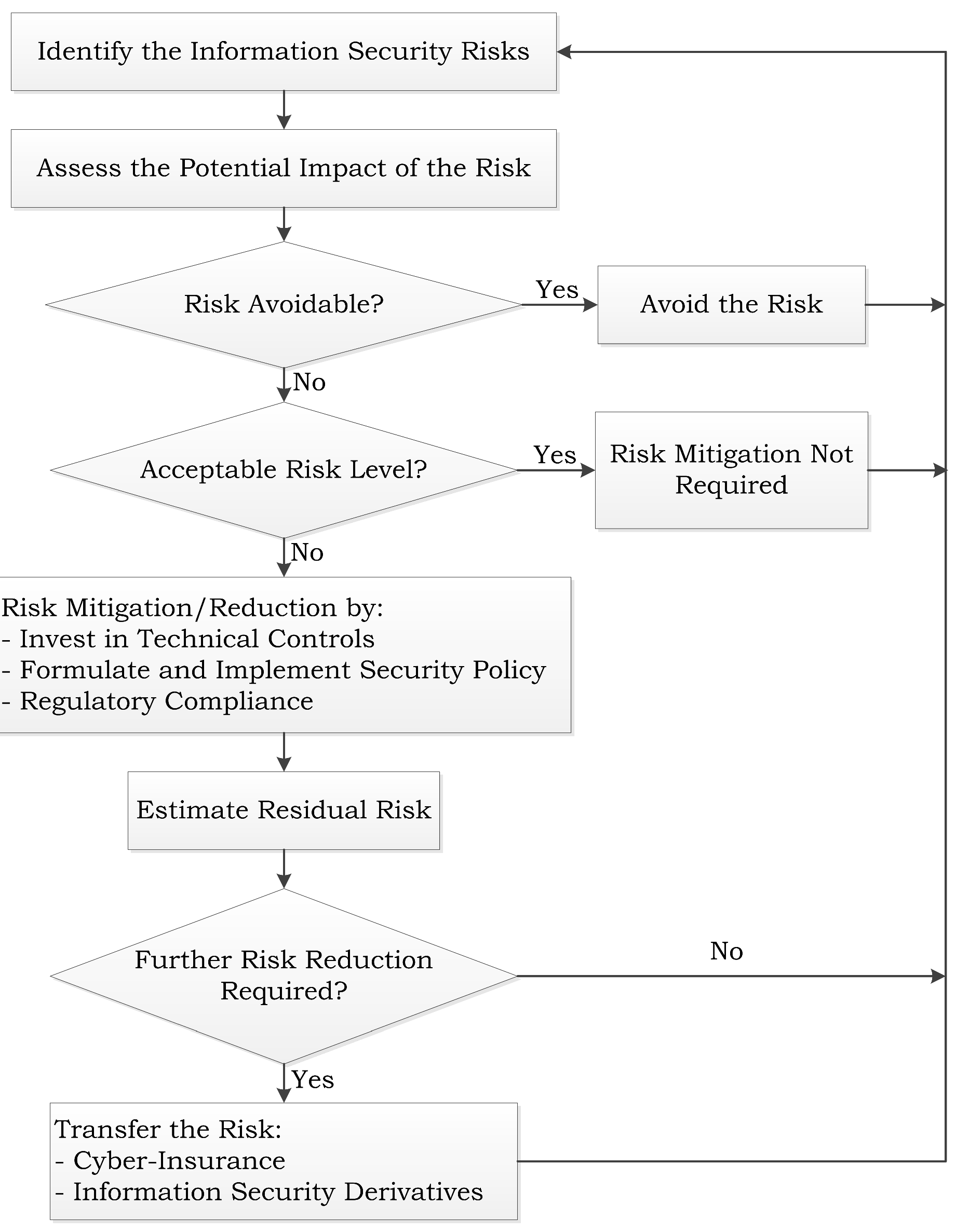

An information security risk management process is an iterative process. It should lead to continuous improvement in the security strength of the organization. An information security risk management process is shown in Figure 2.

The key steps in the risk management process are discussed as follows.

3.1.1. Risk Identification

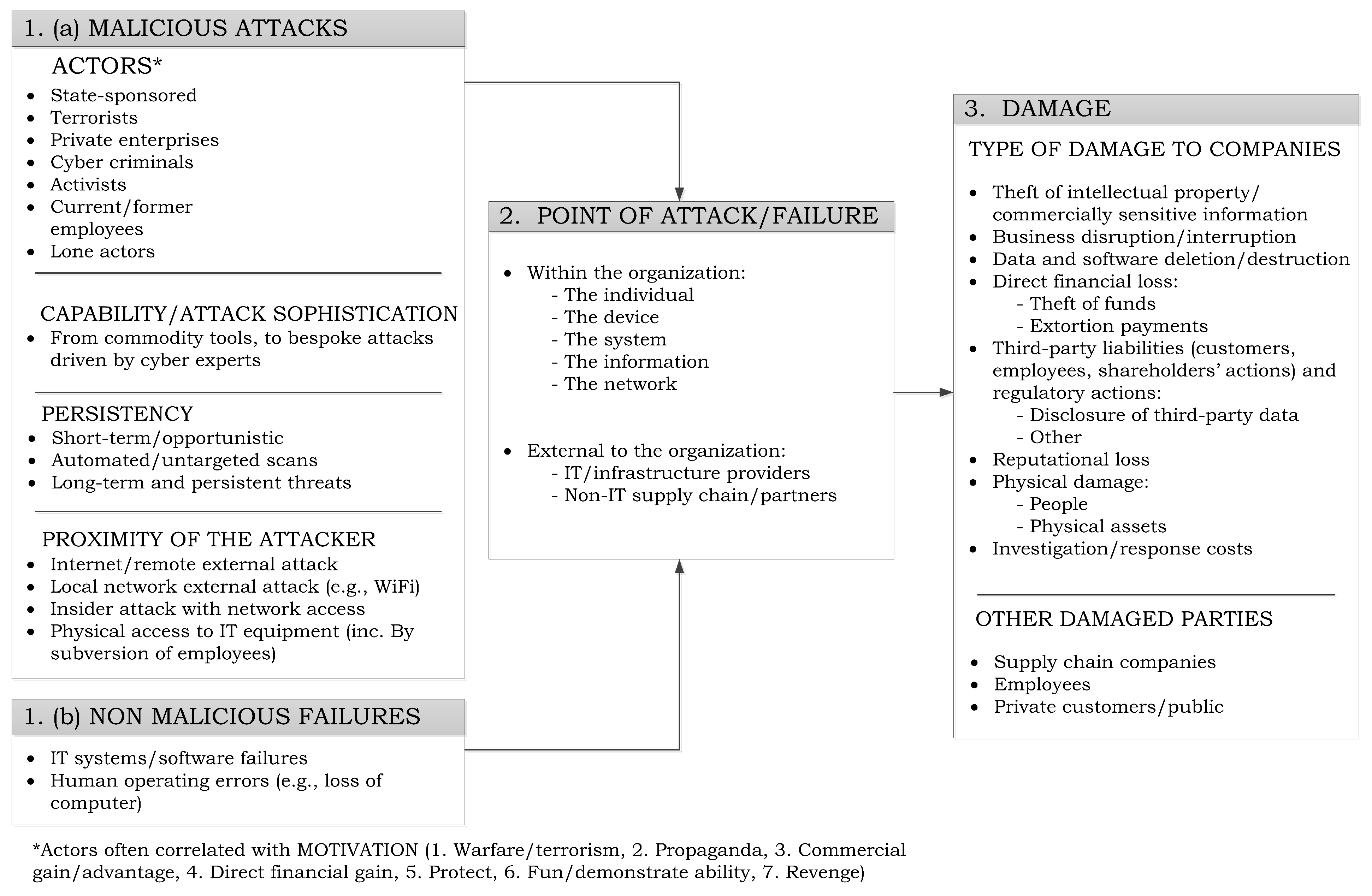

The risk identification process starts with the identification of assets (tangible and intangible) in the organization, that needs to be protected from a potential threat. Thus, the identification of possible cyber-threats to the organization plays a vital role in strengthening the security strategies. A cyber-threat taxonomy can be helpful in identifying the relevant cyber-threats to the organization. A cyber-threat taxonomy is shown in Figure 3.

After completing the risk identification process, the next step is to estimate (quantify) the risk exposure.

3.1.2. Risk Estimation

Risk estimation is the process of determining the potential impact of a risk. The estimation involves estimation of potential loss and probability of occurrence of an adverse event. The risk estimation is useful in formulating the organization’s risk management strategy, deciding on investments in security controls and minimizing the impact of residual risk. The risk estimation method can be categorized into quantitative and qualitative method. Quantitative method assigns numeric values to the likelihood and impact of the risk. Also, the numeric values are assigned to the costs and benefits related to the implementation of security controls. On the other hand, the qualitative method calculates the relative values. Unlike the assignment of exact values to assets, potential losses, and cost of control in the quantitative methods, the qualitative method is usually a combination of questionnaire and workshops. The problem with the quantitative method is a lack of a standard method to effectively calculate the various numerical values. The advantage of a qualitative method is that the accurate values for the asset and cost of controls are not required. However, this non-precise (vague) values may lead to inaccurate (far from real) risk estimates.

3.1.3. Risk Response

The risk response strategies can broadly be categorized into four, as follows:

- Avoidance: This strategy involves avoiding the possible threats and attacks. The source of risk or the asset’s exposure to the risk is eliminated. This strategy is usually used in the cases where the impact of the risk is more than the benefit of having that particular asset, such as full internet connectivity to all the computer systems in the company.

- Acceptance: This strategy involves accepting the security risk and its potential impact as a cost of doing the business. This strategy is applied in the cases where the cost of implementing the security control is likely to be higher than the potential impact of the risk materialization.

- Reduction (Mitigation): This strategy aims to reduce the risk exposure by implementing the appropriate security controls, security policies and compliance with regulatory requirements. It is a primary and commonly applied risk management strategy.

- Transference: Risk transferring strategy is applied to partially transfer the risk exposure to a third party by outsourcing the security services or purchasing a cyber-insurance or taking an appropriate position in the information security financial instruments. In the light of various cyber security incidents where technical defenses failed to prevent the attacks, risk-transference strategy can play a vital role in mitigating the residual risk.

Risk response objectives and strategies are shown in Table 3.

3.2. Financial Engineering and Risk Management

The discipline that deals with the design and development of innovative financial products (instruments) is called financial engineering [23]. The financial engineering attempts to satisfy the needs of the market participants to eliminate, transfer or manage financial and/or business risks [23]. Ross et al. introduced the process of financial engineering as the one which is followed to hedge the specific identified risks that may impact the organization [24]. Thus, “Financial engineering is the process of designing and manufacturing financial products using applicable structured system processes so as to satisfy a stated need relating principally, but not exclusively, to the management of financial risks” [23]. In the last two decades, a variety of financial instruments such as interest rate future and interest rate options, stock index future, stock-index options, weather derivatives, and catastrophe derivatives, have been introduced to allow risk management.

Various researchers such as Silber [25], Van Horne [26], Ross [27], Merton [28], Allen and Gale [29], have presented frameworks for the analysis of financial innovations. The theory of financial innovations should fulfill a set of criteria [30]. Firstly, the innovation must demonstrate that the innovation is able to satisfy the particular needs, and it provides an opportunity for profit earning. Secondly, the theory should explain the cause of innovation, i.e., why did the innovation occur?

3.3. Financial Derivatives to Hedge Risks

In the following subsections several capital market based financial instruments are presented. These innovative financial instruments were proposed or developed to hedge a variety of risks. As these exotic financial instruments were either proposed or developed with the core idea of risk hedging, they closely resemble our idea of capital market based financial instruments to hedge the information security risks.

3.3.1. Macro Market

A large international trading market called “macro market” was proposed by Shiller in 1993 [31]. The objective of macro-market was to allow trading of “futures” contract on long-term claims on major components of income shared by a large number of people or by an organization. The claims in the macro-market can be compared to the “equity” in an organization. Furthermore, the dividend in macro-market would be equal to the share of national income which is comparable to the share in the profit of the company. Traders could participate in the macro-market to invest in the claims on the countries or regions and to hedge the risk in their own national income.

3.3.2. Economic Derivatives

A new type of financial instrument called “Economic Derivatives” were developed to let the people bet on the release of macro-economic data [4]. Economic derivatives are different from the macro-market contracts, as they were designed to let the market participants hedge the risk exposure to the changes in macro-economic conditions. Goldman Sachs and Deutsche Bank introduced the economic derivatives to the market in October 2002 [4]. The Commodity Futures Trading Commission of USA, in 2004, issued an exchange license to a company called “HedgeStreet” to launch the public trading in economic derivatives [5]. Hedgestreet offered the trading in capped futures and options contracts. These options were binary options contract on a variety of variables such as inflation, hurricane, mortgage rate, etc.

3.3.3. Weather Derivatives

Weather derivatives emerged as a new class of risk hedging instrument in the mid 1990’s. For the first time, the weather derivatives were publicly (over-the-counter) traded in 1997 between the Koch Industries (Wichita, KS, USA) and Enron Corporation (Houston, TX, USA) [32]. Since then the weather derivatives market have grown remarkably to the size of multibillion dollars. The weather derivatives are used to hedge the risks associated with weather events, such as temperature, rainfall, etc. [6]. The Chicago Mercantile Exchange (CME) facilitates trading in a derivatives with variety of weather events (variables) such as temperature, frost, snowfall and hurricane [33]. The entities participating in the trading of weather derivatives include a number of energy companies, ski resorts, companies in the agriculture sector, insurers, re-insurers, banks and hedge funds.

3.3.4. Electricity Derivatives

Today, electricity is bought and sold at trading exchanges by numerous market participants such as electricity generators, suppliers and marketers. The prices in the market are set by the demand and supply equilibrium. As a consequence of competition, the market participants are exposed to a variety of risks such as price risk and volumetric risks. Thus, a wide variety of financial derivatives have emerged to facilitate hedging of risks in the electricity markets [34]. These electricity derivatives allow sharing and reduction of undesired consequences through hedging strategies. Ghosh & Ramesh [35] proposed a market for the trading of electricity options. Zhang & Zhou [36] proved that options can reduce the price risk. Oum et al. [37] Oum & Oren [38] argued on the possibility of using electricity options to hedge the risks faced by the retailers. Bhanot [39] explored the use of an electricity option by large consumers to mitigate the price increase risk. Chung et al. [40] proposed a design of forward contracts bundled with options contract to mitigate electricity risks. Oren [41] developed a model to use options for the demand side risk of electricity. Spinler et al. [42] proposed an analytical framework to value the electricity options contract.

3.3.5. Cloud Computing Derivatives

Market based approach for cloud computing systems has received significant attention in the research community [43,44,45,46,47,48]. The idea of cloud services management in a market arises from the concept of variable pricing of services, such as Amazon’s Spot Instances market [49] facilitates bidding on spare CPU-hour resources. The idea of market mechanisms for cloud services is not limited to academic research indeed companies like 6fusion [50], Virtustream [50], and Zimory [50] have taken the idea to the level of commercialization.

Some researchers such as Song et al. [51], Mihailescu and Teo [52], Gomes et al. [53], and Vanmechelen et al. [54], have presented mechanisms for creation of markets and trading of resources. However, with the commodification of cloud services, comes the risk of heavy price fluctuation in the market. To address the risk of price fluctuation, Rahman [55] proposed an approach based on the financial option theory to address the risk of price variation. Bossenbroek et al. [56] proposed an option contracts based approach to deal with the price volatility in the grid resources market. Toosi et al. [57] proposed a financial option based approach to hedge the critical and risky situation in cloud resources allocation. Further, Du et al. [58] proposed an option pricing mechanism to facilitate hedging against the price risk and evaluated the effectiveness of the mechanism with respect to forward contracts. Du et al. [59] proposed a new model of dynamic forward contracts to allow efficient risk hedging in cloud computing markets. Furthermore, in an analysis of financification of cloud computing services, Kauffman et al. [60] analyzed the cloud computing services market based on the concepts and theories of financial market. Also, they identified the key elements for future development of cloud services markets on the lines of financial markets.

3.3.6. Natural Disaster Risk Management Instruments

A variety of financial instruments have been designed to mitigate the risk exposure to natural disasters. The financial instruments such as catastrophe futures, catastrophe swaps, catastrophe options, catastrophe bonds, insurance derivatives and others [7,61], are widely used to transfer (hedge) the natural disaster risk.

3.3.7. Terrorism Risk Management Instruments

4. Problem Elicitation

Currently, cyber-insurance products are the only financial instruments available in the market that facilitate transferring of information security risks to some extent. However, the cyber-insurance products come with various problems. An empirical analysis of insurability of cyber-risks is presented in [65], summarized in Table 4.

The problems in the existing cyber risk management market that are relevant to this article are discussed as follows:

- Limited Efficiency and Effectiveness of Cyber-Insurance: Cyber-insurance is the “statistical” approach to hedge the risks, and it relies on the law of large numbers. For the mechanism to work successfully, the risks covered must be reasonably independent to each other and the frequencies (estimation) must be known. All that is required for the success of insurance products is a reliable actuarial table, and a large pool of insureds to distribute the risk. However, unlike other insurance products, cyber-insurance products are designed in absence of proven actuarial tables. There is a lack of historical cyber-incidents data which limits the variety of cyber-insurance products and cyber-insurer’s are exposed to a risk of insolvency due to interconnected and high impact nature of cyber-risks. Thus, the correlated nature of cyber-risks negatively affects the efficiency and effectiveness of cyber-insurance products. The overall problem of inefficiency and ineffectiveness can be better understood in the light of following problems in the cyber-insurance products.

- Information Asymmetry: Cyber-insurance markets are inefficient and incur additional costs due to information asymmetry. The cyber-insurance products are often customized to address the specific requirements of the client, however, if the cyber-insurance buyer does not know all about the product coverage, then there is an information asymmetry between the client and the provider. This can be explained with the theory of “The Market for Lemons” proposed by George A. Akerlof [66]. Akerlof introduced “The Market for Lemons” with the question of why there is a “large price difference between new cars and those which have just left the showroom” [66]. It suggests that cyber-insurance products are a trust good, and all the coverage details are not visible to the buyer. As a buyer cannot differentiate between a “good” coverage and “less” coverage products, the product is traded at the price of “less” coverage products (and high risk) (lemons). The famous case of Sony and Zurich Insurance is a relevant example [67].In addition to the problem of lemons market, the cyber-insurance domain suffers from the problem of “adverse selection”. An adverse selection arises when the client has some relevant information and the information is not disclosed to the cyber-insurance provider, i.e., the client knows about the risk for which it wants to acquire a cyber-insurance policy. The adverse selection can be explained with the theory of “The Market for Insurance” [68].The third type of information asymmetry in the cyber-insurance field is “moral hazard”. A moral hazard arises when the buyer is purchasing a coverage based on the experience of losses. Thus, the buyer of the insurance product may have no or less incentive in mitigating the risk, instead the buyer prefers to transfer the risk to the insurer.

- Incomplete Markets: Cyber-insurance products available in the market are very limited in terms of variety of risks and their coverage [69,70]. In other words, the cyber-insurance markets do not provide an opportunity to hedge “all” (wide variety) of risks for which hedging mechanisms are required. In such a scenario, information security stakeholders have to bear the risk, or they use the less optimal mechanisms to transfer/hedge the risks [69]. This discrepancy in risk exposure and actual risk coverage is usually termed as “Basis Risk”.

- Lack of Liquidity: It is crucial to have liquid markets to achieve effective risk hedging. However, once a cyber-insurance policy is purchased, the client has no mechanism during the contract period to adjust (buy or sell) his position according to the latest risk scenario.

- High Transaction Cost: Currently, transaction costs are high in cyber-insurance and reinsurance markets. Typically, the risk is transferred through contracts, credit risk of counterparties is evaluated, and risk management systems are deployed and maintained. However, due to the interdependent and correlated nature of information security risks, the capitalization levels to support the insurance liabilities may be dramatically out of equilibrium [69,70,71].

- Regulatory Capital Requirements: Regulatory requirements, such as Solvency-II [72] require (re-)insurers to meet the capital requirements. These capital requirements and requirements to maintain a risk management system increases the cost of capital. Also, this creates barriers to entry for new entrants into the cyber-(re)insurance market.

- Counterparty Credit Risk: A counterparty to an insurance contract is exposed to the risk that its counterparty will go bankrupt during the life of the contract. In other words, an insurance cover can only be realized if the insurer is solvent when the risk is materialized. However, due to inefficient risk estimation [69,71], failure to comply with regulatory requirements [72], and simultaneous claims filed by multiple clients due to interdependent nature/materialization of risk [69,70,71], the insurer may not be able to settle all the claims.

- Lack of Data: The cyber-(re)insurance industry faces a unique challenge of lack of actuarial data. In absence of relevant historical data cyber-(re)insurer’s may not be close to actual risk probabilities and their risk assessment may either be an overestimate or an underestimate of the risk exposure, and its impact [69,71].

Thus, there is a need for novel financial instruments to address the problems mentioned above in the cyber-insurance products. Furthermore, the World Economic Forum has recognized the need of new financial products and markets, and one of its report states that “Opportunities will emerge for new businesses in insurance or risk markets to help businesses mitigate the potential downside from cyber risks” [76].

5. Requirements for Information Security Derivatives

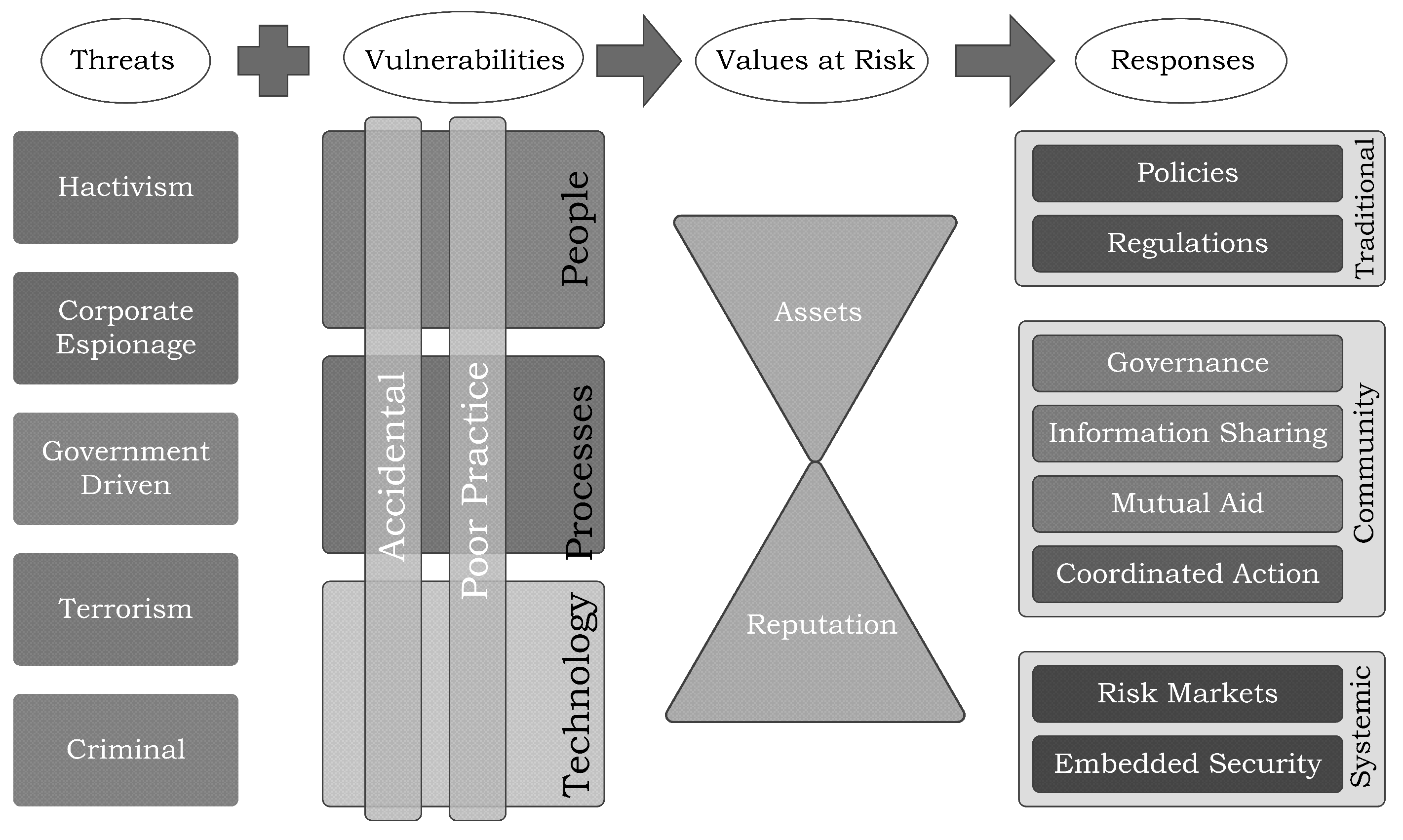

World Economic Forum identified that risk markets were one of the two ways to deal with systemic risk in information security domain [77], shown in Figure 4. Risk markets can provide a variety of financial instruments such as indemnification, insurance, and structured risk-transfer solutions for an organization to address the information security risks [76].

An alternative to “statistical” approach of cyber-insurance is to hedge the cyber risks through an “economic” approach. The economic approach is most suited for correlated risks. The principle behind the economic hedge mechanism is the concept of negative correlation. The hedger takes a position that is correlated with the risk but in the opposite direction (negatively correlated). The economic hedge mechanism is different from the statistical hedge mechanism in a way that it does not require a large number of people. Furthermore, there is no need of an actuarial table with the frequency of the underlying event (risk). Thus instead of pooling (insurance) the risks, the risks are traded in a market (exchange or over-the-counter).

Thus, based on the problems identified in Section 4, and the review of literature on risk-hedging financial instruments [4,5,6,7,31,32,61,62,63,64,78,79] we have identified the following fourteen requirements for the information security derivatives:

- The financial instrument should allow an effective and efficient hedging mechanism for the risk exposure to the underlying information security event.The information security derivatives should perform better than the cyber-insurance products on the following properties.

- Increased information elicitation and aggregation

- Strong manipulation resistance

- Increased market products and size

- Increased scalability

- Rapid implementation

- Increased liquidity

- Reduced transaction cost

- Increased price transparency

- Reduced cost of capital

- Reduced risk to the issuer or market operator

- Reduced settlement and clearing costs

- Diversification of counterparty credit risk

- Increased data generation

A mapping of problems in cyber-insurance products and corresponding functional requirements in ISD to address the aforementioned problems is shown in Table 5.

6. Design Specifications for Information Security Derivatives

Financial economists treat the real-world financial instruments as a combination of simpler, hypothetical financial instruments [80]. These hypothetical financial instruments are designed to pay a unit of currency to the trader or investor if a particular “state” (outcome) among a set of possible “states” (outcomes) occur. These set of states are exhaustive i.e., cover all possible outcomes and the chosen states are mutually exclusive. These financial instruments are designed to isolate and break-down complex risks into distinct states. The usefulness of these hypothetical instruments is that the returns from complicated financial products can be modeled as a linear combination of the returns of these hypothetical instruments.

The traders or investors participating in the market where trading of such financial instruments takes place, can bet on the state of the product for which they may have some relevant information. Thus, a variety of such financial instruments can be traded in an ISPM to provide the fundamental building blocks for information aggregation, analysis of risks and their impact and to hedge the underlying risk.

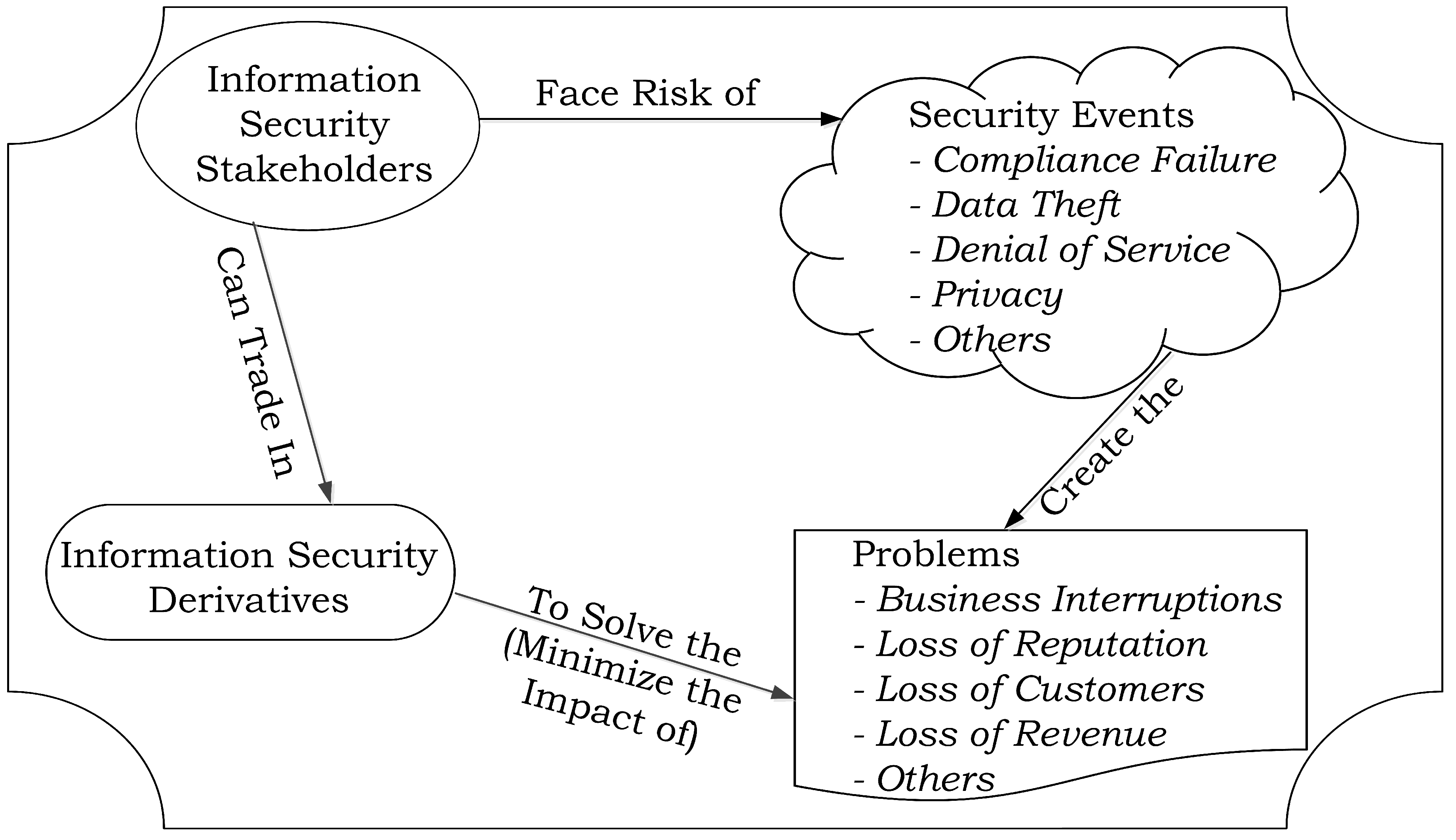

Information security derivatives would provide a financial protection to the hedgers against the negative impact of the underlying information security event. An application scenario of ISD is shown in Figure 5.

The individuals or organizations exposed to an information security event risk would purchase a corresponding derivative with the said event being the underlying of the derivative contract. The market participants who are participating in the market to reduce their exposure to the negative impact of the occurrence of the underlying information security event are called hedgers. Apart from the individuals and organizations who are exposed to an information security risk, cyber-insurers are likely to be a major participant in ISD trading to transfer their risk to the capital market and thus enhance their insurance capacity. Traditionally, insurers purchase derivatives as a vehicle to re-insure their risk exposure. Participation in capital markets allows the insurers to adjust their risk position than with traditional reinsurance companies rapidly. Furthermore, insurers and re-insurers can also be a seller in the market. The sellers of the ISD would rely on their premiums exceeding their payouts. To achieve this, sellers write a large number of different derivatives on many low-correlated and probabilistically diverse types of information security events. This allows the sellers to hedge their risk of making a big payout on multiple high impact information security events at the same time. Furthermore, the more likely an event is to occur; higher will be the premium for the corresponding contract. Other market participants (speculators) would be attracted to the opportunity of earning profit by anticipating the direction and timing of price changes in ISD. The speculators are essential for the functioning of ISPM, as they would provide liquidity- the ability to buy and sell the contracts quickly, easily and efficiently. The category of speculators may consist of a variety of participants such as hedge funds, proprietary trading firms, banks and individual traders.

6.1. Risk Mitigation with ISD

The ISD contracts are the financial instruments that derive their values from the probability of occurrence or non-occurrence of the underlying event. Therefore, their value depends on the future events. They are a form of contractual agreement between the buyer and the seller to exchange the privileges and liabilities linked to the underlying event. There are at least two parties involved in the trading of ISD. Therefore, the accounting gains made by one party are exactly equal to the accounting losses suffered by the counterparty. This is similar to the cash settled traditional derivatives.

Let us consider an ISD contract that has two “states”, State-1 and State-2 denoted as “s1” and “s2” respectively. The total investment in the state s1 is “Ts1” and in the state s2 is“Ts2”. If the state s1 occurs then the unit payout for the same is, “Us1” as expressed in Equation (1).

Similarly, if the state s2 occurs then the unit payout for the same is, “Us2”, as expressed in Equation (2).

The unit payout for the occurrence of an event with more than two states can be calculated as expressed in Equation (3).

In the Equation (3), the state si is the state for which the unit payout “Usi” is calculated. “n” is any positive number indicating the highest number of possible states (outcomes) for the given event. The total investment in any given state is represented as “Tsi”. “Tsj” is the total investment in all the states other than the state “i”.

In the above scenario of an event with two states, if a trader invests an amount of “Is1” in state s1 and if the said state occurs, then the total payout received by the trader is, “Ps1”, as expressed in Equation (4).

If the state 2 “s2” occurs then the payout is, “Ps2”, as expressed in Equation (5).

If the trader wants to hedge his risk exposure to the occurrence of state “s2”, then the investment required for “s2” can be calculated by equating the payouts in both the states with the planned hedge trade, as expressed in Equation (6).

Solving the above equation gives the investment which the trader is required to do in state “s2”, as expressed in Equation (7).

As shown in above equations, compared to traditional derivative instruments, the calculation and implementation of hedge trades using ISD is relatively straight forward. The hedge ratio Is2 computed for a simple two state instrument can be extended for the instruments with more than two states. Further, as the set of states in ISD consist of all the possible and mutually exclusive states, the states that can occur other than in which an investment has been made by a trader can be termed as “complementary states”. The process of hedging for a multi-state event consists of two steps, as follows:

- Determine the hedge amount to be invested in the complementary states

- Distribution of the said amount among the complementary states

The first step, determining the amount of investment required in complementary states is calculated as in Equation (8).

where, IC is the amount of investment in complementary state; IH is the amount of the existing investment in states to be hedged; EIC is the existing amount invested in complementary states; and EH is the amount invested in the states that need to be hedged, exclusive of IH.

The second step, allocation of hedge investment among the complementary states is achieved by allocating IC in proportion to the existing amount already invested in each of those states.

Let us consider a four state ISD contract with the following specifications:

- There are four possible states (outcomes) of the underlying event, namely s1, s2, s3, and s4.

- The states to be hedged are s1 and s2. Thus, the complementary states are s3 and s4.

- Existing investment in each state is $40, $50, $30, and $60 respectively.

- A trader has previously invested $10 (IH) in s1 and s2.

- Allocation of $10 in s1 and s2 is proportionate to existing investment in respective states. s1 is allocated $4.444 (=10 * (40/(40 + 50))) and s2 is allocated $5.555 (=10 * (50/(40 + 50))).

- Therefore, the amounts invested in each state minus the trader’s investment is $35.555, $44.444, $30, and $60 for the states s1, s2, s3, and s4, respectively.

The investment in states s1 and s2 minus the trader’s investment, i.e., ($35.555 + $44.444) is the quantity EH defined above. Thus, according to Equation (8), the amount of investment required for complementary states (s3 and s4) is computed as in Equation (9).

The second step is to proportionately distribute the above amount between the states s3 and s4. Thus, s3 is allocated $3.749 (=11.25 * (30/(30 + 60))) and s4 is allocated $7.499 (=11.25 * (60/(30 + 60))).

Thus, the trader’s investment in the four states s1, s2, s3, and s4 is $4.444, $5.555, $3.749, and $7.499, respectively. This implies that, the total investment in each state stands at $40, $50, $33.749, and $67.499, respectively.

The unit payout for each of the four states is calculated using the Equation (3), as shown in the following equations, Equations (10) to (13).

If the state s1 occurs, then according to Equation (4) the payout to the trader is computed as in Equation (14).

If the state s2 occurs, then according to Equation (4) the payout to the trader is computed as in Equation (15).

If the state s3 occurs, then according to Equation (4) the payout to the trader is computed as in Equation (16).

If the state s4 occurs, then according to Equation (4) the payout to the trader is computed as in Equation (17).

Thus, the trader in this case is fully hedged against all the possible outcomes (states). However, with the arrival of any new relevant information during the trading period, the consensus belief (probability of event and price of contract) of traders with respect to the possible outcomes may change and thus the payouts will change. Therefore, the trader would need to re-balance his hedge position.

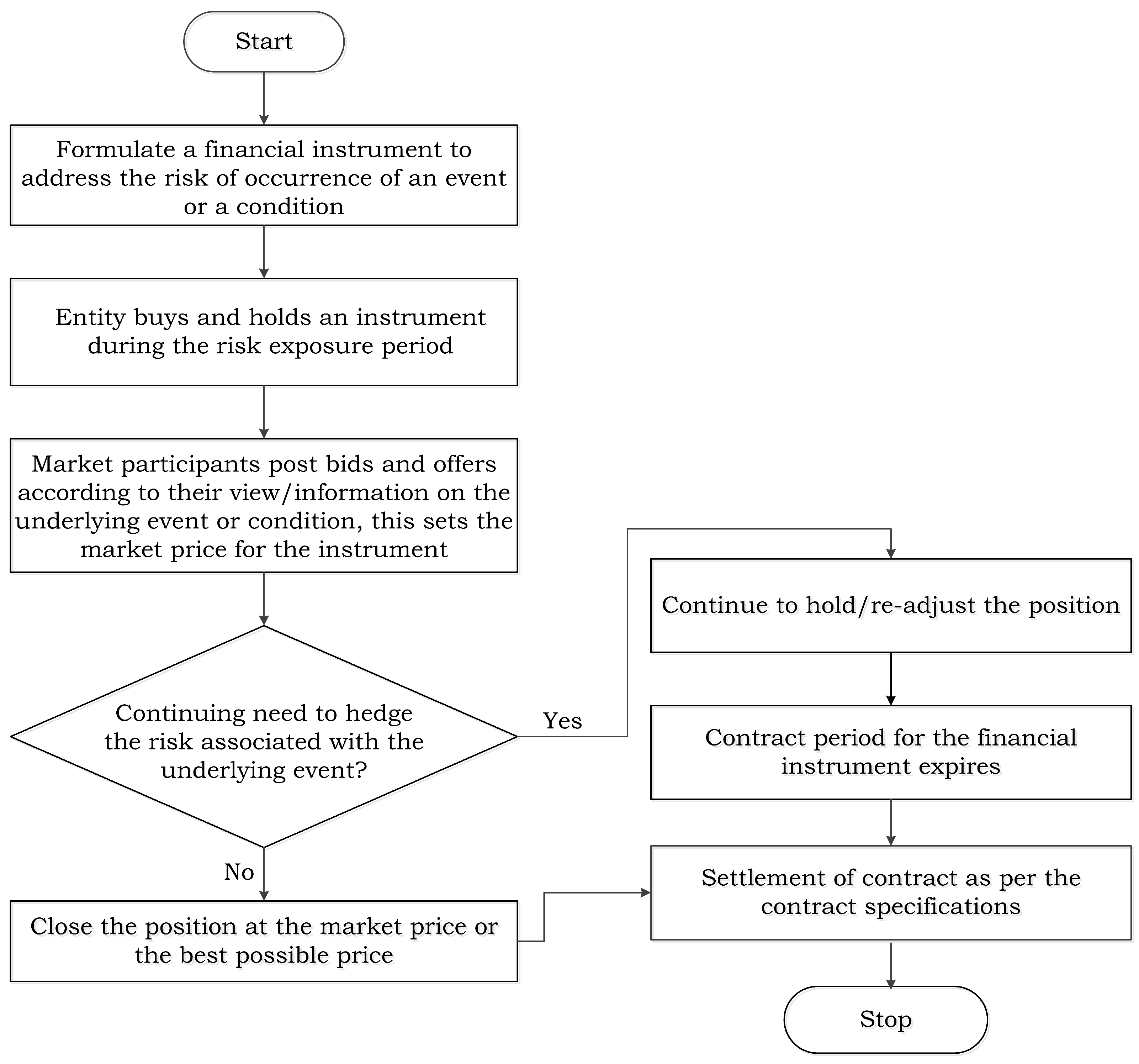

6.2. ISD Design Process

The process of designing and using ISDs is shown in Figure 6.

6.2.1. Identification of Security Events

The design of useful and effective ISD depends on the identification of the underlying events or conditions. The risk-hedging mechanism will depend on the occurrence of one or combination of predefined states of the underlying event. The underlying information security events that pose risk to an organization can be identified from the threat taxonomy presented in Section 3.1. Furthermore, the potential losses arising from cyber attacks and non-malicious IT failures could be categorized into 11 categories, as shown in Table 6. These loss categories can be used to identify the high impact risk events.

6.2.2. Defining States

In ISD a distribution of possible outcomes for the underlying event or conditions are partitioned into a defined range or states. In some forms of ISD, the states are mutually exclusive and collectively exhaustive, thus one state will always occur in these instruments. In ISD, the states are defined in such a way that the states form the basis of a probability distribution, such as the sum of the probabilities of all the possible outcomes is unity.

6.2.3. Types of ISD

The ISDs can be designed in at least four forms: (i) Information Security Options (ISO); (ii) Information Security Vanilla Options (ISVO); (iii) Information Security Futures (ISF); (iv) Information Security Swaps (ISS).

(i) Information Security Options: ISO are designed such that the buyer and seller agree to exchange a fixed payout linked to the occurrence of the underlying information security event or condition. In other words, the buyer of ISO is in money if the event occurs, and the seller is in money if the event does not occurs. Thus, there are only two possible outcomes (states). The payout received by the buyer and seller is same, however the price paid by the buyer and seller may be different. The difference in investment price depends on the event’s probability estimate by the market forces.

(ii) Information Security Vanilla Options: ISVO are designed as a variable payout instrument. The payment by the seller to the buyer depend on how far the underlying event results are from the payout trigger. ISVO are different from ISO in a way that the buyer pays a premium to the seller in exchange of a variable payment. However, the seller only gets the premium and is not entitled for a reciprocal right to receive a payment from the buyer in case of non-occurrence of the underlying event.

(iii) Information Security Future: ISF is a contract between two counterparties. In ISF, one counterparty pays a variable amount to the other if the underlying event occurs. For the future contract the payout will vary with the degree by which the actual result falls short or surpasses the trigger. The payout varies like in case of the ISVO, however in case of a future contract a payment from the buyer to seller is required if the underlying event does not occurs.

(iv) Information Security Swaps: A traditional swap agreement between the counterparties fixes the obligation to exchange the predefined payments over a predefined time frame in future. Similarly, the ISS would require a payment(s) to the buyer if the underlying event occurs in exchange of a payment(s) from the buyer. The amount of the payment can be variable or fixed.

(v) Bundled Information Security Derivatives: This would be a group of fixed or variable payout information security derivatives, each of which represents a mutually exclusive range of states of the underlying event, and only some of the “states” of the underlying event can occur. Furthermore, a bundle of derivatives can be designed, where the occurrence of one or more states in one or more of derivatives in the bundle is conditional upon the occurrence of one or more states in the bundle contract.

6.2.4. Pricing of ISD

The pricing of ISD would be more like the pricing of weather derivatives and economic derivatives than the standard pricing models such as Black-Scholes pricing model [82]. Like economic derivatives, the payout formula for an ISD would depend on the occurrence or non-occurrence of the underlying event, instead of variance in price of an underlying asset. Thus, the price modeling would not be based on a continuous variable with a standard distribution. In other words, the probability of (non-)occurrence of the underlying event is not a tradeable asset nor it can be linked to one. The payout from the ISD cannot be hedged through a dynamic trading strategy. Thus, the key issue in the pricing of ISD is the non-hedgeability of the payout trigger, such as a discovery of a vulnerability in a piece of software.

These issues are well-known to the option modelers. It is common to find options in exotic fixed income and credit derivatives that are modeled on directly unhedgeable variables. Some of these methods can be applied in pricing of ISD on variables that can be postulated to have known statistical or functional relationship to the underlying risk. In general, there can be three approaches to price the ISD, however they are yet to be explored by research, and briefly discussed as follows:

(i) Business Pricing: Business pricing requires the organization interested in using an ISD, to model the financial impact of an information security event across a variety of outcomes (states). Then the organization can determine the amount it is willing to pay (as premium) to protect the business against those adverse conditions (states) in case they occurred based on the output of CVaR model [83] and risk appetite of the organization. In this way, an organization can obtain a “guaranteed security” for the desired period, greatly reducing the variations in revenue and/or expenses due to an information security event. Alternatively, the counterparty seeking a certain level of return for assuming a certain level of risk can determine the price (premium) that it wants to charge to bear the expected outcome of the underlying information security event.

(ii) Actuarial (Historical) Pricing: The historical pricing method is based on the computation of future expectations. Like economic derivatives [5], the actuarial pricing method can be applied to the underlying information security variables that can be observed over time. Similar to economic variables, the information security variables cannot be bought or sold to hedge against the future payout of the derivative contract with the said variable as underlying.

Like an inflation index for economic derivatives, an information security index can be treated as a continuous variable, however as the hedge argument for the complete market does not apply, the martingale transformation cannot be used to calculate the present value of the hedge cost.

The properties of an information security variable is empirically researched to come up with parametric or numerical distribution of possible outcomes. In other words, the objective is to estimate subjective or historical means and variances, and solve for the in-the-money probability using the untransformed distribution. This would result in the following equation [5]:

where, PB is the price of the binary option (with two states), VO is the value of the option (expected payout), r is the interest rate, t is the time to expiry of the contract, Pr is the untransformed probability distribution (subjective cumulative probability of exceeding the strike), and K is the strike level.

The price is not equal to the present value of the hedge. It is the discounted value of a statistical expectation of the payoff. It is only good on average, and to the level that the distribution assumptions are right. Thus, the historical pricing mechanism may sometimes fail when there is a weak link between the probability of the underlying event and historical data or actuarial probability.

(iii) Odds-Maker Pricing: An organization might not have faced an information security event that it needs to hedge and thus the price of corresponding ISD based on an historical data is bound to be flawed. Furthermore, the counterparty may be wrong in its probabilistic estimate due to lack of relevant historical data. In such a scenario, like in economic derivatives [5], the price of the ISD would be far from the hedge considerations and it would be biased towards the odds-making balance of market forces (buyers and sellers). Thus, an informed or a near-monopolist market participant or the market-maker can use a subjective probability estimation to set the initial buy and sell prices.

This leads to price setting by the position inventory control mechanism. Sidney [84] explained the art of odds making. In his approach, the main principle is that the expected value of the “take” (net of cash received and paid for contracts sell and purchase, respectively) for the market-maker should exceed the expected liability at the expiry of the contract. This is expressed as:

where, nti is the number of contracts purchased or sold at time ti (positive if purchased and negative if sold), pti is the cash paid or received at ti. The left-hand side of the above equation is equal to the expiry value of the total payment obtained from the net options’ sales. On the other hand, the right-hand side of the equation equals to the expected total payout which the market-maker would earn at the options expiry, conditional to option being in-the-money. Since the market-maker cannot evaluate this payout expectation, inequality in the equation is purely a inventory control mechanism, without considering the market-maker’s subjective probability estimates.

6.2.5. Payout Trigger

In general, structuring an information security hedge would comprise of two components: the selection of the trigger (index) and the payoff structure for the given index. Particularly, the hedge effectiveness of information security derivatives would depend on the quality of the index in predicting losses and on the factors, such as trigger, tick size, and cap, defining the payout function. Thus, the challenge is to develop an index that meets the needs of the market participants. Ideally, the index should be easily understandable, easy to calculate, and based on verifiable data. In other words, the index should be transparent. Furthermore, the index must be calculated and settled within the shortest span of time if the underlying event occurs.

Designing a suitable information security risk index involves identification of source of the risk that the derivative contract is intended to hedge. The objective is to create information security risk indices that posses a high correlation with the risk event as this would affect the hedge effectiveness. The index must posses a high correlation with the financial impact of the information security event to be hedged. This is required to minimize the basis risk. An imperfect correlation of the index and financial impact of risk event may lead to inadequate hedging of risk impact.

An objective, consistent, transparent and rule-based computational index for information security risks can be designed in the same manner as the index for weather derivatives and stock market indices for macroeconomic models represent the market risk exposure correlation to other enterprise risks [85]. The information security risk index can be created from the data patterns of the organization’s Cyber-Value-at-Risk (Cyber-VaR) models [83] paired with the historical information, such as type of security event, frequency, loss and so on, to predict the probability and financial impact of the corresponding information security event. Furthermore, the historical information about the security event may include intra-organizational as well as industry wide information. The information security risk index can then be used as a threshold to trigger the derivatives payout.

The Gumbel’s method of exceedances [86] can be useful in predicting the number of future information security events or incidents (values) that would exceed the past values. The Gumbel method assumes that a hypergeometric stochastic process is followed for the frequency of events as expressed in Equation (20).

where, τ is the threshold (index strike), n is the total number of (information security) events, j is the total number of events above the threshold, and r is the number of future observations, Xn+1, ..., Xn+r, i.e., number of periods it would go ahead. Therefore, we can express the number of exceedances of Xτ,n among the next r observations, Xn+1, ..., Xn+r, as in Equation (21).

Let us say, the total (successful and unsuccessful) number of vulnerability exploitation in a particular smart grid system in the last one year stands at 31. Now, we need to know the probability of an event which is higher than the threshold and that would not happen in the next year. For this case, we consider the threshold as the event with highest impact. Therefore, for the software vulnerability exploitation in the given smart grid we have n = 31 (number of events recorded in the last one year), r = 1 (one year ahead), τ = 1 (number of highest impact event as threshold), and j = 0 (number of events above the threshold, i.e., the events with an impact higher than the impact of the event chosen as threshold). Using the Equation (21) and inputting the variable data we get the Equation (22).

Thus, the probability of an information security event in relation to the given smart grid system with an impact of higher than the previously recorded event in the next year is 1%. This information is critical for the pricing of ISD and setting a payout trigger for the underlying information security event.

The payout trigger in ISD must be clearly defined, correspond to a measurable or impact observable, transparent, and verifiable outcomes which occur at one of an upper and/or lower point of the defined range or state. Apart from the company specific information security risk index, other forms of payout triggers that can be used for ISDs are shown in Table 7.

6.2.6. Payout Structure

For the hedge to be most effective, all the available information about the company’s risk exposure should be considered when structuring an information security derivative to allow hedging of the underlying risk. In the structuring of derivative contract, the buyers (hedgers) and sellers both have high interest in the relationship between the premium and maximum payout. To hedge the information security risk effectively, the maximum payout is to be structured in such a way that it is adequate to cover the potential losses if the underlying information security event occurs. On the other hand, the sellers are compensated by premium payment for assuming the risk.

The payouts on ISD can be structured in a variety of ways. The payout structure depends on the underlying event or condition and on the type of ISD. A set of payout structures for ISDs are shown in Table 8.

6.2.7. Decision Criteria

The identification and specification of “standard” decision criteria and/or data sources is a critical element for the settlement and payout of contracts. The clearing house of ISPM will act as a definitive authority on the results and the decision by the authority would be based on the source(s) specified in the contracts specification. Depending upon the type of derivative contract and the underlying event or condition the source of decision could be a news article published in a previously specified media, an individual-such as security researchers or red teams, documents submitted in court of law or other legal documents, government sources/documents-such as reports or notifications from CERT, reports published by reputed consulting organizations-such as PWC, McKinsey, etc., reports published by research organizations-such as universities, etc., industry consortium, reputed organizations, regulatory bodies, and reporting made by the company to various regulatory bodies-such as securities and exchange commission, etc.

6.2.8. Specification of Derivatives

For the successful implementation and acceptance of ISD, it is must to avoid all sorts of confusion and disputes with respect to trading and settlement of contracts. Thus, the ISD contract’s specification should clearly define the underlying event or condition, trading period, payout trigger criteria, decision criteria, etc. Thus, we have identified a set of specification required for ISD, as shown in Table 9.

6.2.9. Trading of ISD

Once the ISDs are designed they can be either traded OTC or at ISPM. Trading at ISPM is the desired mode of trading to achieve market efficiency, information elicitation, transparency, lower transaction cost, higher liquidity, regulatory compliance, and manipulation resistance.

The hedger would need to estimate the dollar value of risk exposure if the underlying event of the corresponding derivative occurs. This information is crucial for the hedger to determine the number of contracts that are to be purchased to adequately hedge the risk.

7. Demonstration: An Example Application

This section is divided into four sub-sections. The first subsection demonstrates the application of an information security options contract. The second sub-section demonstrates the application of an information security vanilla options. The third sub-section demonstrates the application of an information security swap contract, and the fourth sub-section demonstrates the application of an information security futures contract.

In the following sub-sections several probabilistic estimates of information security events have been used, however the section does not attempts to compute the probability of the scenarios. Rather, it demonstrates how the financial impact of such a scenario can be hedged with information security derivatives.

7.1. Information Security Options

This subsection is divided into four parts to explain the application of ISO in hedging the impact of risk arising out of an information security event. The first part describes the scenario, second part presents the ISO specifications, third part identifies the potential market participants and their incentive to participate. Lastly in the fourth part the process of hedging with an ISO is explained.

7.1.1. Scenario

Let us consider an oil drilling and services company “O”. The company has four business units. The daily oil production at its unit-1 “U1” earns it a revenue of $20,000 per day. The company “O” has deployed sophisticated computer systems for the operation, maintenance, and security of the unit. However, if the technical defenses fail and the unit-1 suffers a major cyber-attack, such as [91,92,93,94,95,96], and the normal operations of the unit are adversely affected leading to loss of one full day’s revenue, then the company may lose upto $40,000. This potential loss of $40,000 includes one day’s revenue loss of $20,000 plus additional $20,000 in system recovery, forensics, and legal expenses. In such a scenario, the company “O” would like to reduce (mitigate) the adverse impact of a cyber-attack, through an ISO contract as explained below.

7.1.2. Contract Specification

The specifications of the ISO contract to address the risk in the given scenario is shown in Table 10.

7.1.3. Participants and Incentives

The prospective participants, their motivation and incentives for participation in trading of ISO at ISPM is shown in Table 11.

7.1.4. Risk Hedging

In the given scenario, there are two possible states of the underlying information security event for the given ISO. Thus, the event set of cyber-attack at the unit-1 consists of following two states:

- S1 = Unit-1 suffers a (pre-specified type of) cyber-attack and production at the unit is adversely affected.

- S2 = Unit-1 suffers no cyber-attack or the production at the unit is not affected.

(1) Risk Analysis and Impact Estimation

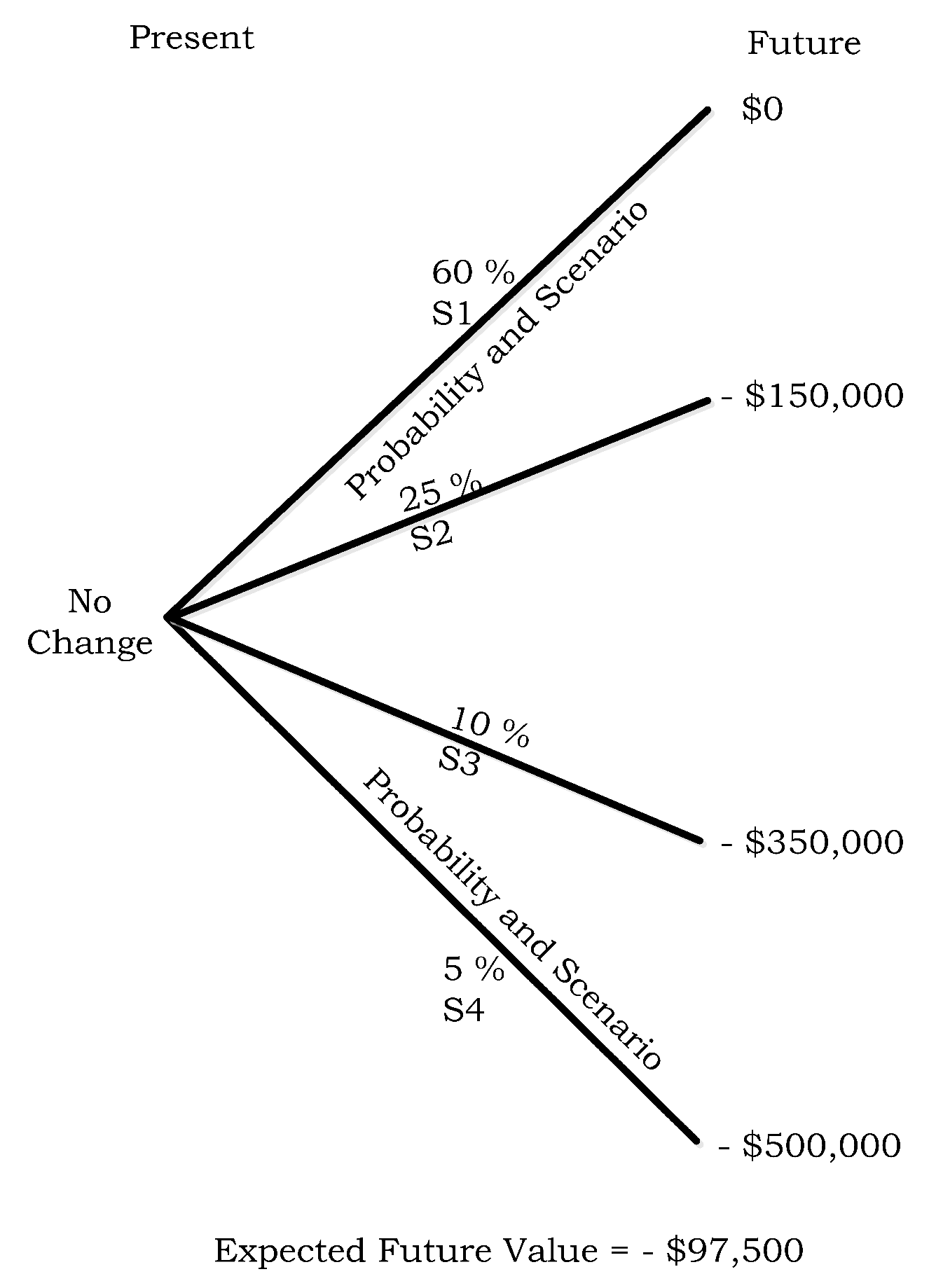

In order to devise a risk response strategy and to use the ISO contracts for impact hedging, we assume that the oil production company has done its risk analysis and impact estimation using a standard risk assessment model, such as CVaR Model [83]. The output of the CVaR model for the unit-1 of the company is as: “Given a successful cyber-attack, the unit-1 of the organization O would lose not more than $40,000 per day, for total of one day, with 50% probability during the three months period of 1 October 2015 to 31 December 2015”. Thus, if S1 occurs the company may lose upto $40,000. If S2 occurs the company continues its usual business and earns a revenue of $20,000 per day.

(2) Risk Response

Let us say, the ISO contract for the occurrence of cyber-attack at unit-1 of the company “O” is currently trading at $20 (buy) and $80 (sell). The buy and sell price of the contract indicates the market participant’s probabilistic estimate of the occurrence and non-occurrence of the underlying event [98]. Therefore, the buy price of $20 indicates that the market participants have estimated the probability of occurrence of the cyber-attack at unit-1 within the trading period as 20%. On the other hand, the market estimates 80% probability for the non-occurrence of the cyber-attack at the unit-1 during the contract trading period. This estimate is based on all the information known to the market participants (as per the efficient market hypothesis [99]). This market estimate is different from the output of CVaR model, i.e., 50% probability of cyber-attack and 50% probability of no cyber-attack at the unit-1 during the contract trading period.

In such a scenario, the first question that needs to be answered is if it is worth to hedge the risk exposure or not? This decision to hedge or not to hedge the risk can be based on the “Marking-to-Future” method [100]. The marking-to-future method gives the expected future value of the value at risk. The expected future value of the value at risk can be calculated as in Equation (23).

where, ρ is the probability of the risk event and µ is the impact value of the event.

(2.1) Unhedged Scenario

Based on the market participant’s estimate, if the oil company remains unhedged to the risk exposure to U1 then the expected future value is calculated as in Equation (24).

where, αm is the market’s expected future value (unhedged), ρs1 is the probability of s1, µu1 is the impact value (unhedged) for state 1, ρs2 is the probability of s2, µu2 is the impact value (unhedged) for state 2.

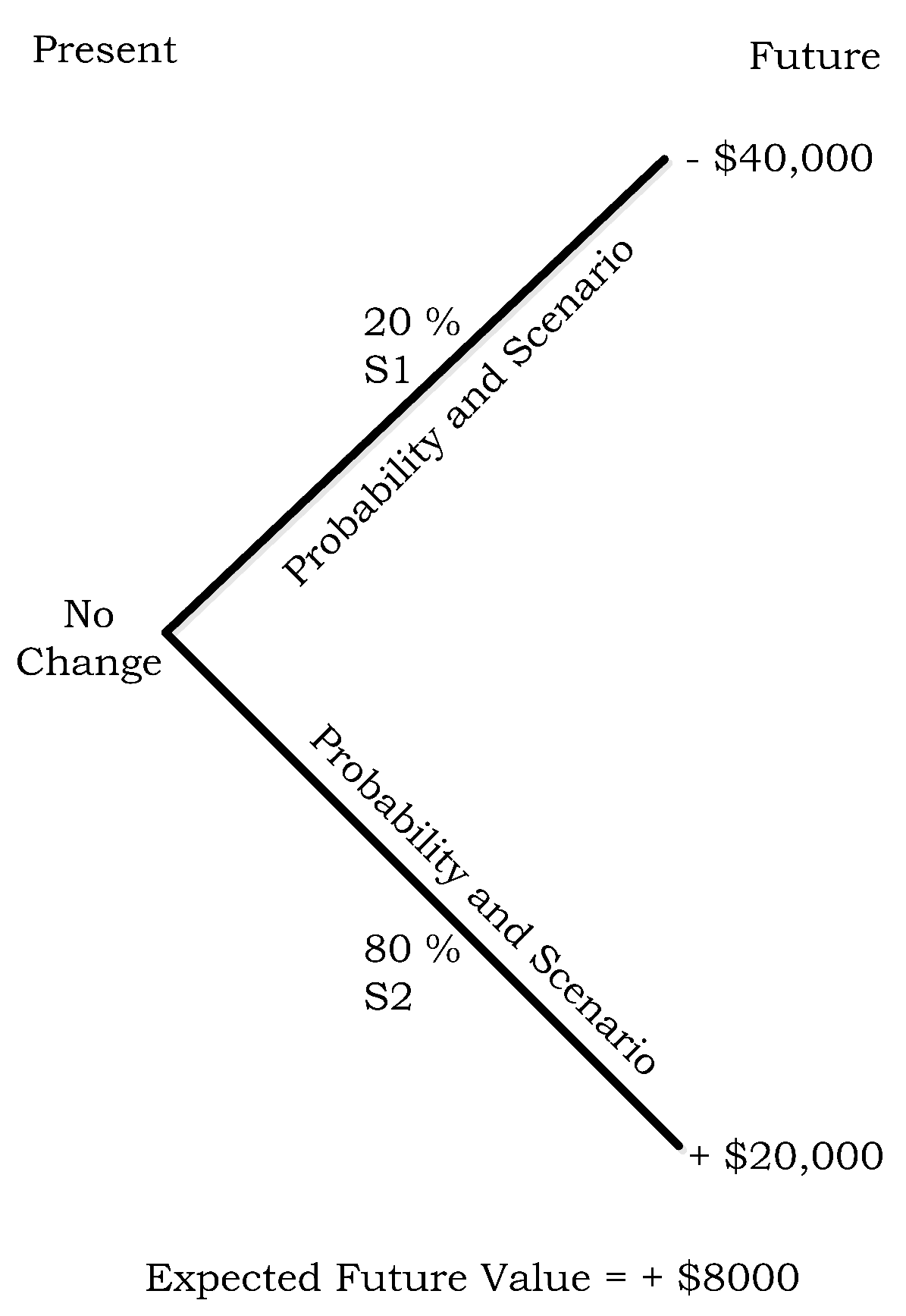

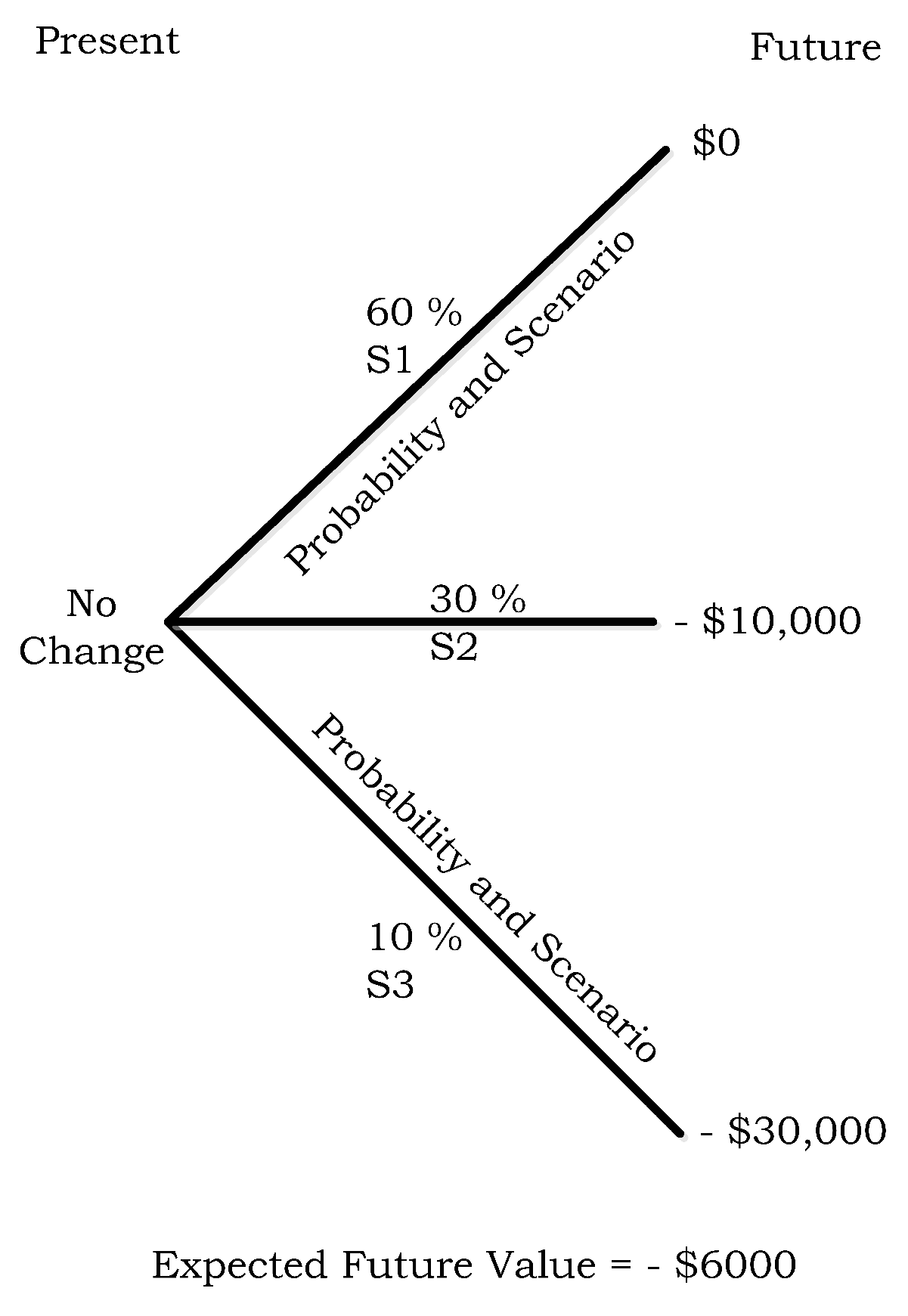

The expected future value from the market’s perspective in an unhedged scenario is shown in Figure 7, and calculated as shown in Equation (25).

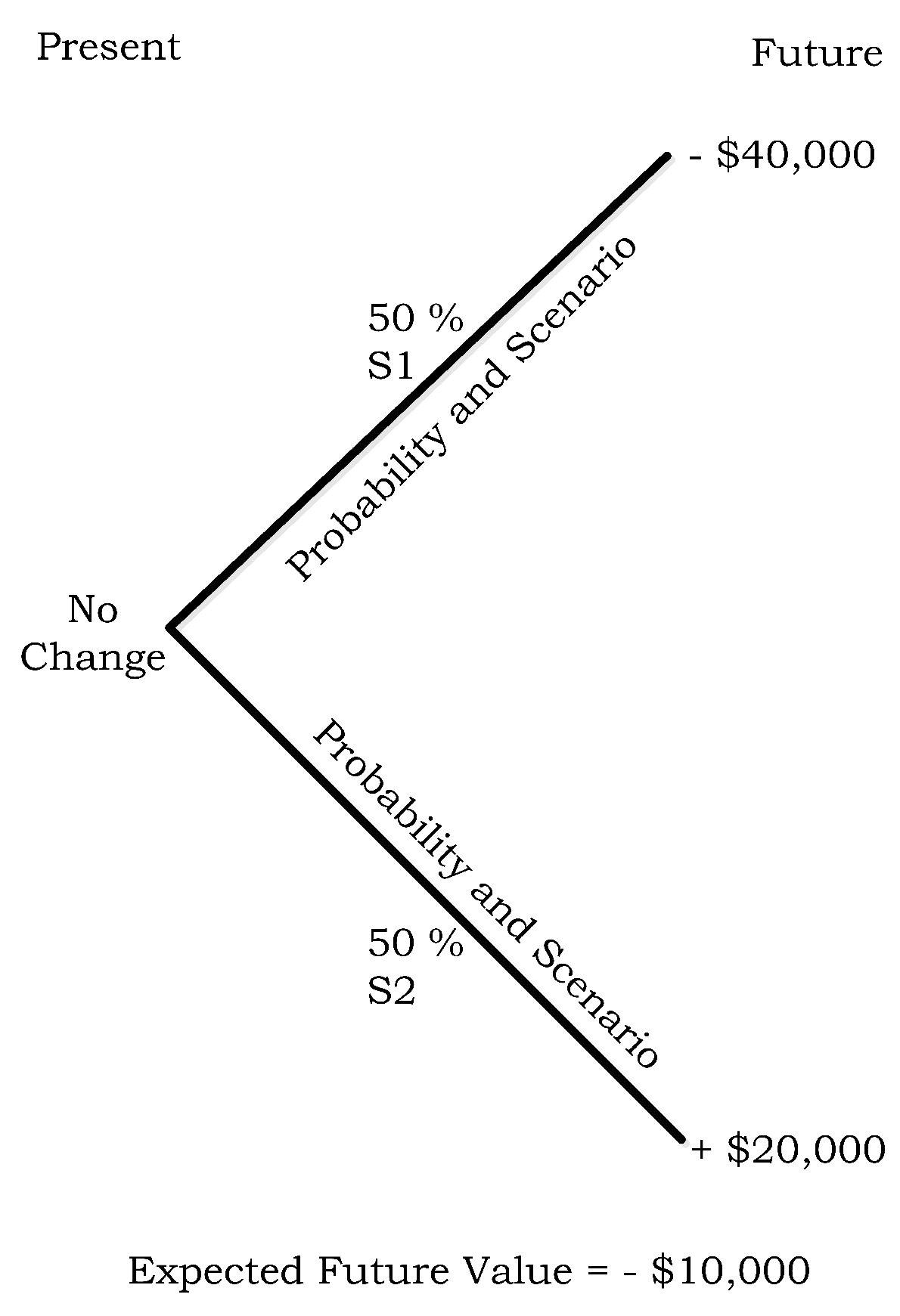

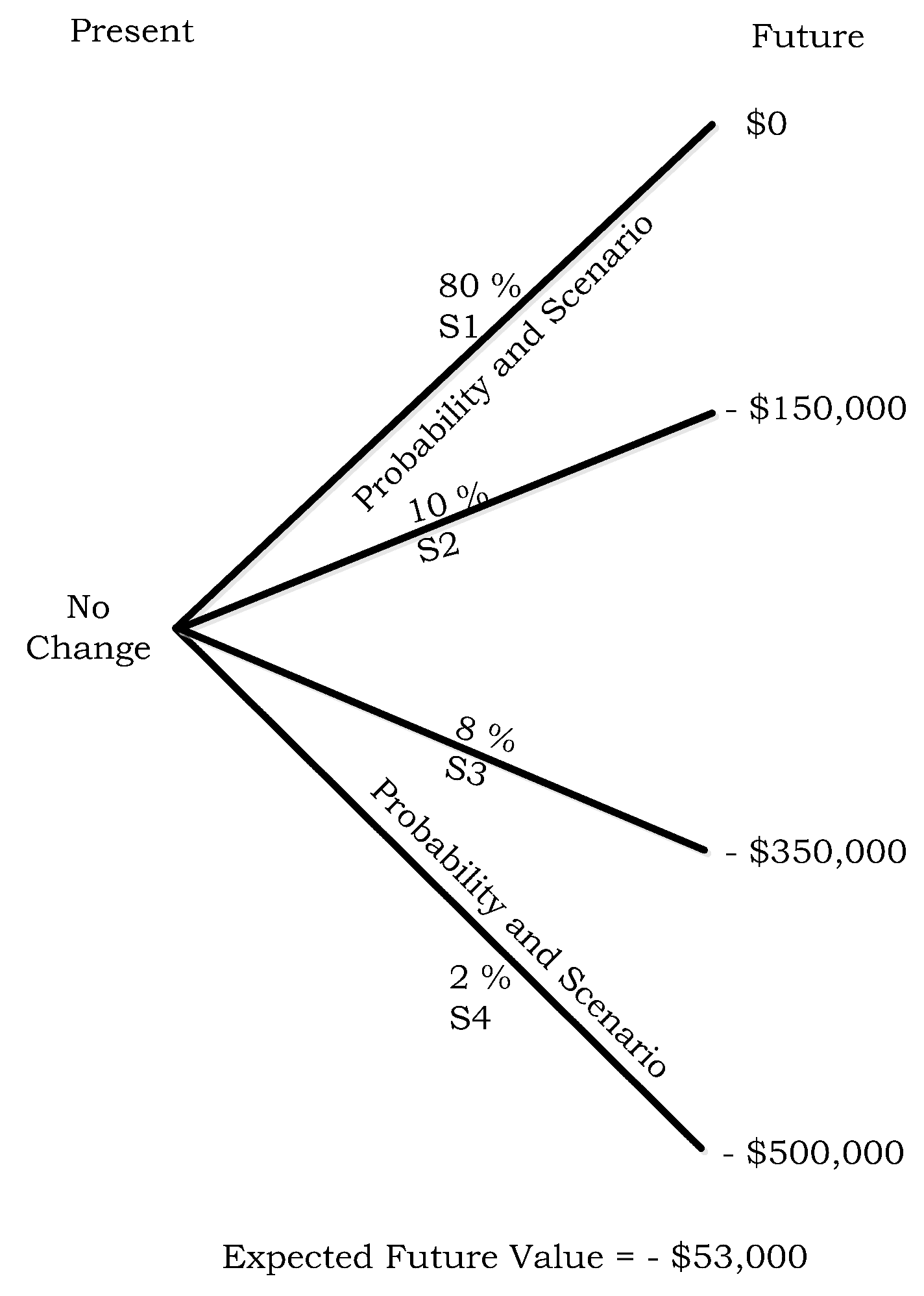

On the other hand, the expected future value based on the company’s CVaR model in an unhedged scenario can be calculated as shown in Equation (26).

where, αc is the expected future value (unhedged) based on the CVaR model, ρs1 is the probability of s1, µu1 is the impact value (unhedged) for state 1, ρs2 is the probability of s2, and µu2 is the impact value (unhedged) for state 2.

The expected future value from the company’s perspective in an unhedged scenario is shown in Figure 8, and calculated as shown in Equation (27).

Thus, in the unhedged scenario there is a large variance between the expected future value by market participants (+$8000) and the expected future value as per the CVaR model (−$10,000).

(2.2) Hedged Scenario

If the company decides to hedge its maximum risk exposure of $40,000, then the company needs to determine the number of ISO contracts they need to purchase. This can be determined by hedge ratio [83], expressed as in Equation (28).

where, θ denotes the hedge ratio. λ is the risk exposure due to an information security event, this risk exposure is estimated from the Cyber-VaR model. ω is the number of contracts of the financial instrument that are to be purchased to hedge the estimated risk. These financial instruments have the corresponding (that needs to be hedged) information security event as the underlying. ϕ is the payout per contract that will be received by the hedger when the underlying information security event occurs. γ is the transaction cost incurred (estimated) on the purchase of hedge position. This transaction cost also includes other indirect costs, such as cost of capital, interest rates, etc.

Thus, to perfectly hedge the risk exposure of $40,000, number of ISO contracts required are computed as shown in Equation (29).

For the sake of simple demonstration, we ignore the cost of transaction (interest rate, exchange fee, cost of capital, etc.).

As shown in Equation (30), with the payout of $100 per contract, the company needs to purchase 400 ISO contracts to perfectly hedge its risk of $40,000.

In the given scenario, to hedge the risk exposure with ISO contracts, an ex-ante assessment of effectiveness of the hedge is computed as shown in Equation (31) [83].

where, εd denotes the hedge effectiveness of information security derivatives, λ is the estimated or materialized risk impact, γ is the estimated or actual cost of hedging, and ηd is the expected or actual total payout from the information security derivative contracts.

As computed in Equation (32), the above hedge strategy with ISO is expected to be 83.34% effective in mitigating the underlying information security risk. In the above equation γ is $8000 paid to purchase 400 ISO contracts at the rate of $20 per contract. Other costs such as interest rate, cost of capital, etc. are ignored.

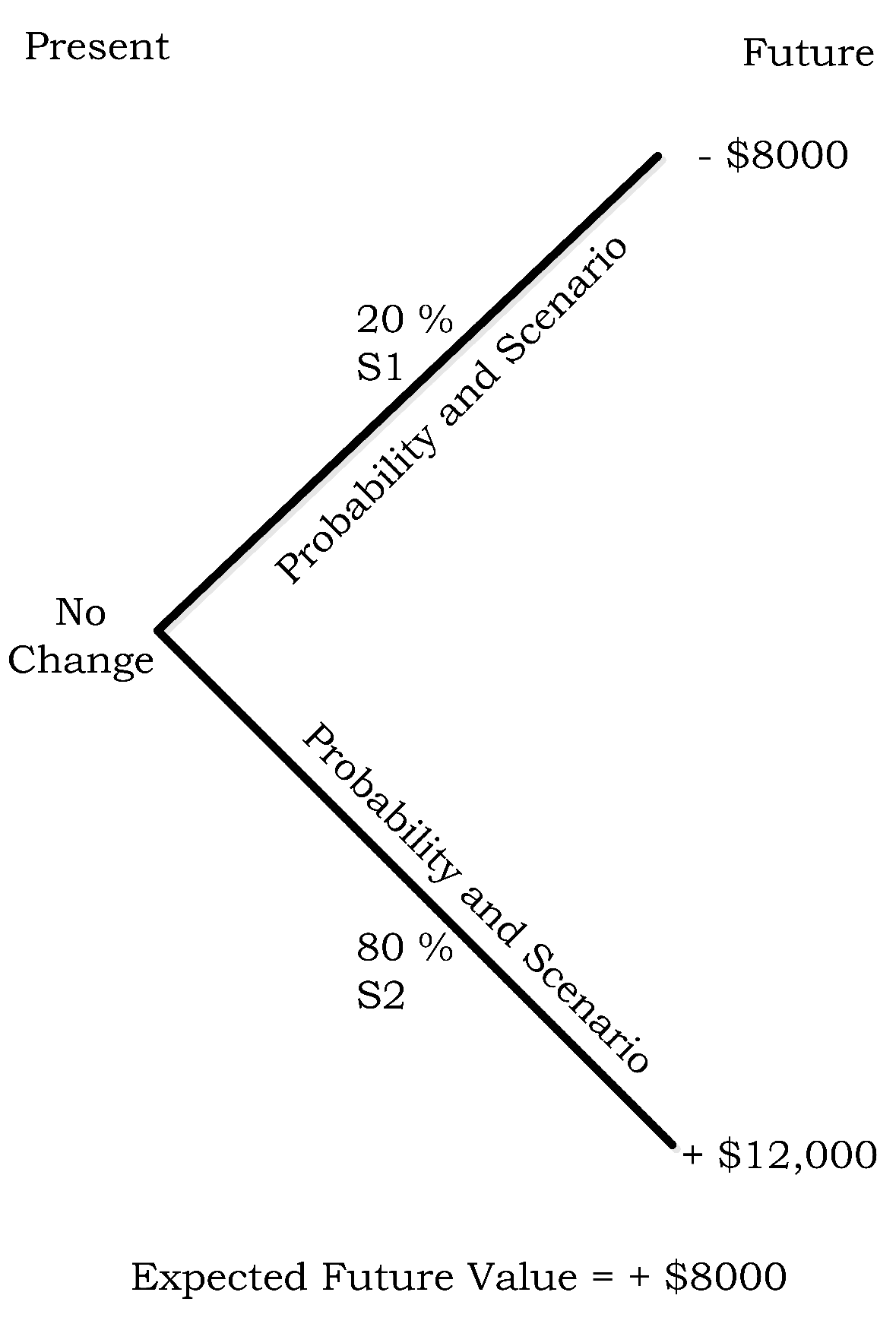

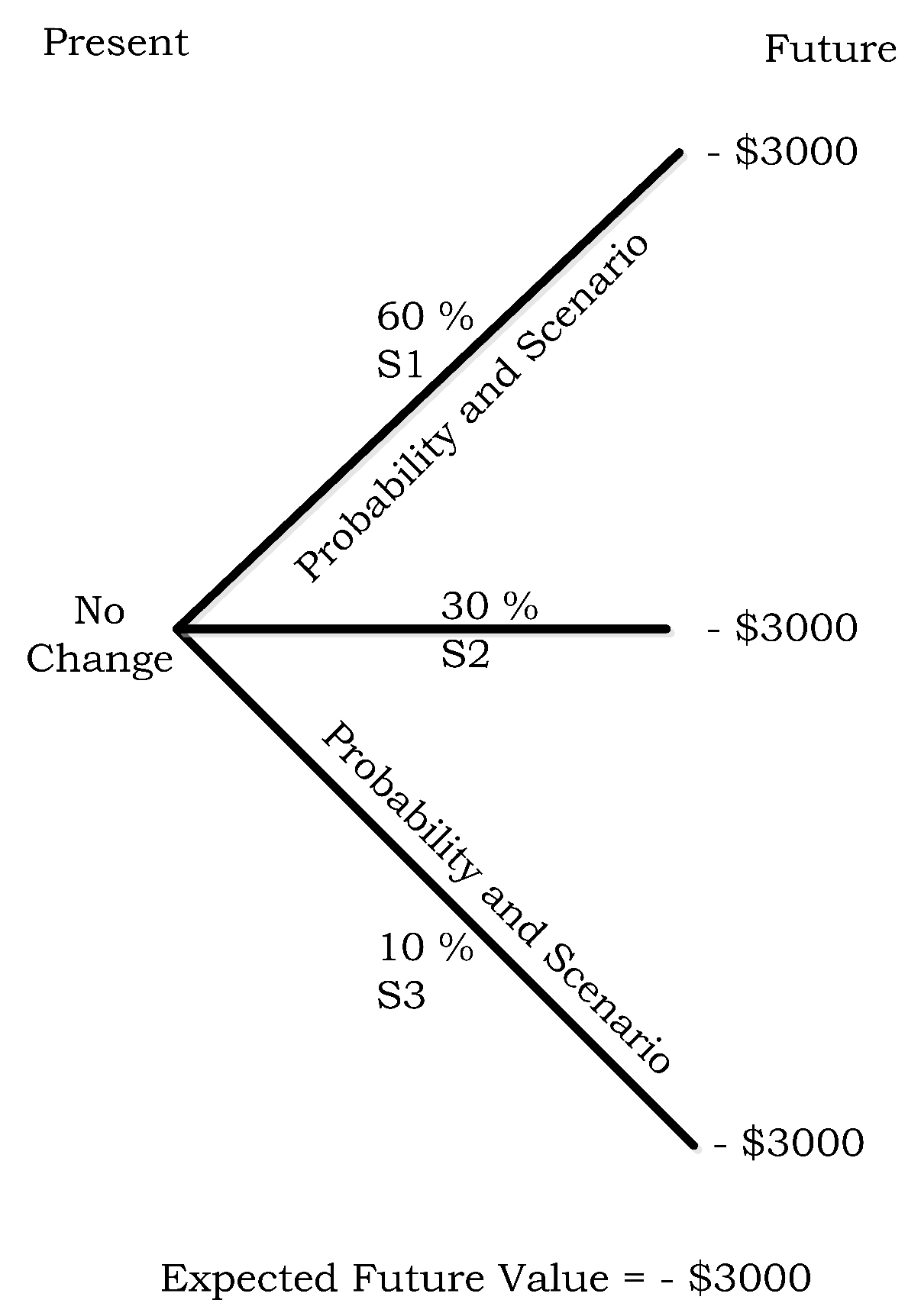

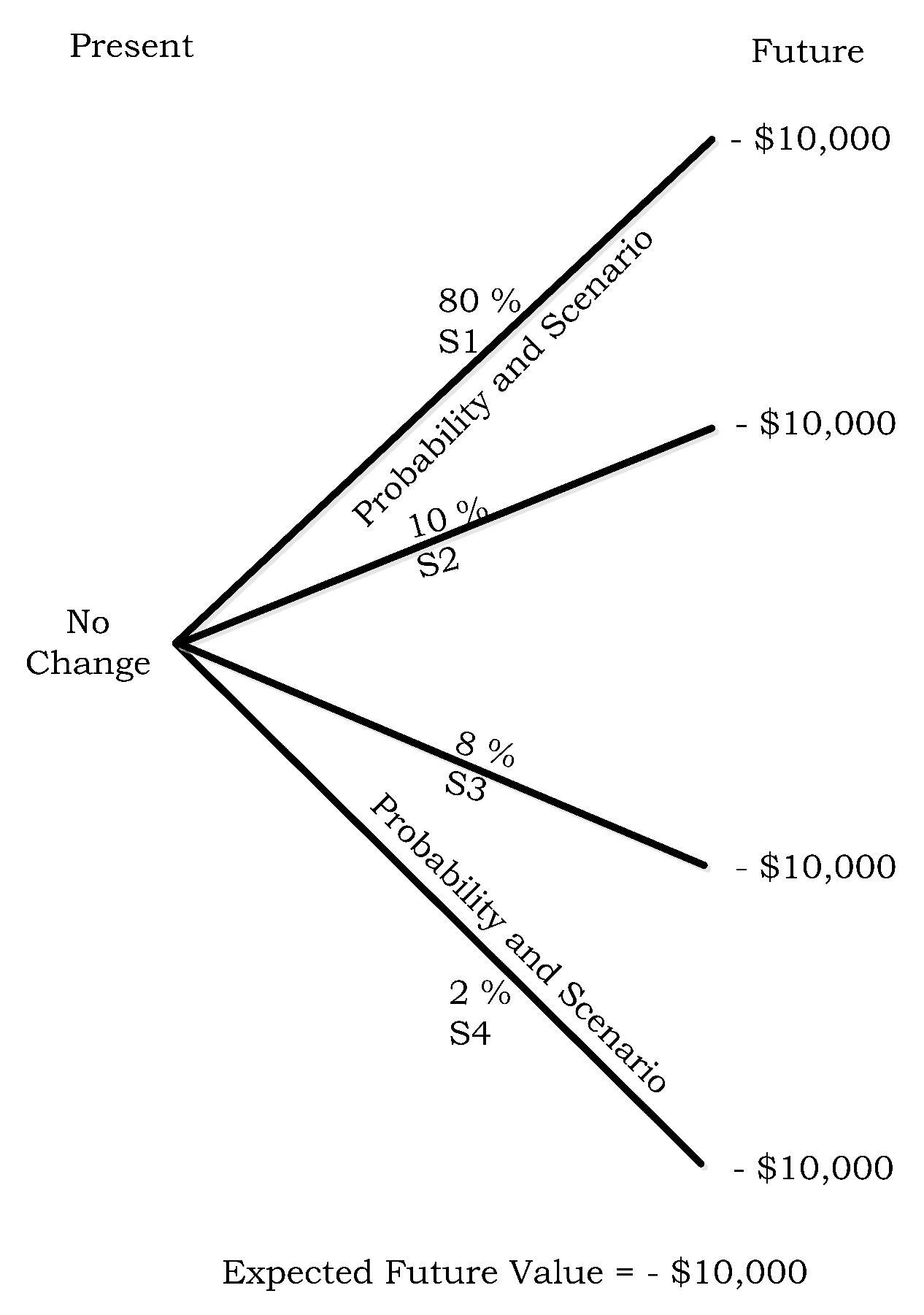

In the perfectly hedged scenario, the expected future value from the market participant’s perspective can be calculated as shown in Equation (33).

where, βm is the market’s expected future value (hedged), ρs1 is the probability of s1, µh1 is the impact value (hedged) for state 1, ρs2 is the probability of s2, and µh2 is the impact value (hedged) for state 2.

In the perfectly hedged scenario, the expected future value from the market participant’s perspective is shown in Figure 9, and calculated as in Equation (34).

- µh1 = −$8000 (=−$40,000 loss + $40,000 payout from 400 ISO contracts − $8000 paid to purchase 400 ISO contracts).

- µh2 = $12,000 (=$20,000 revenue earned − $8000 (=$20 * 400) cost of 400 ISO contracts)

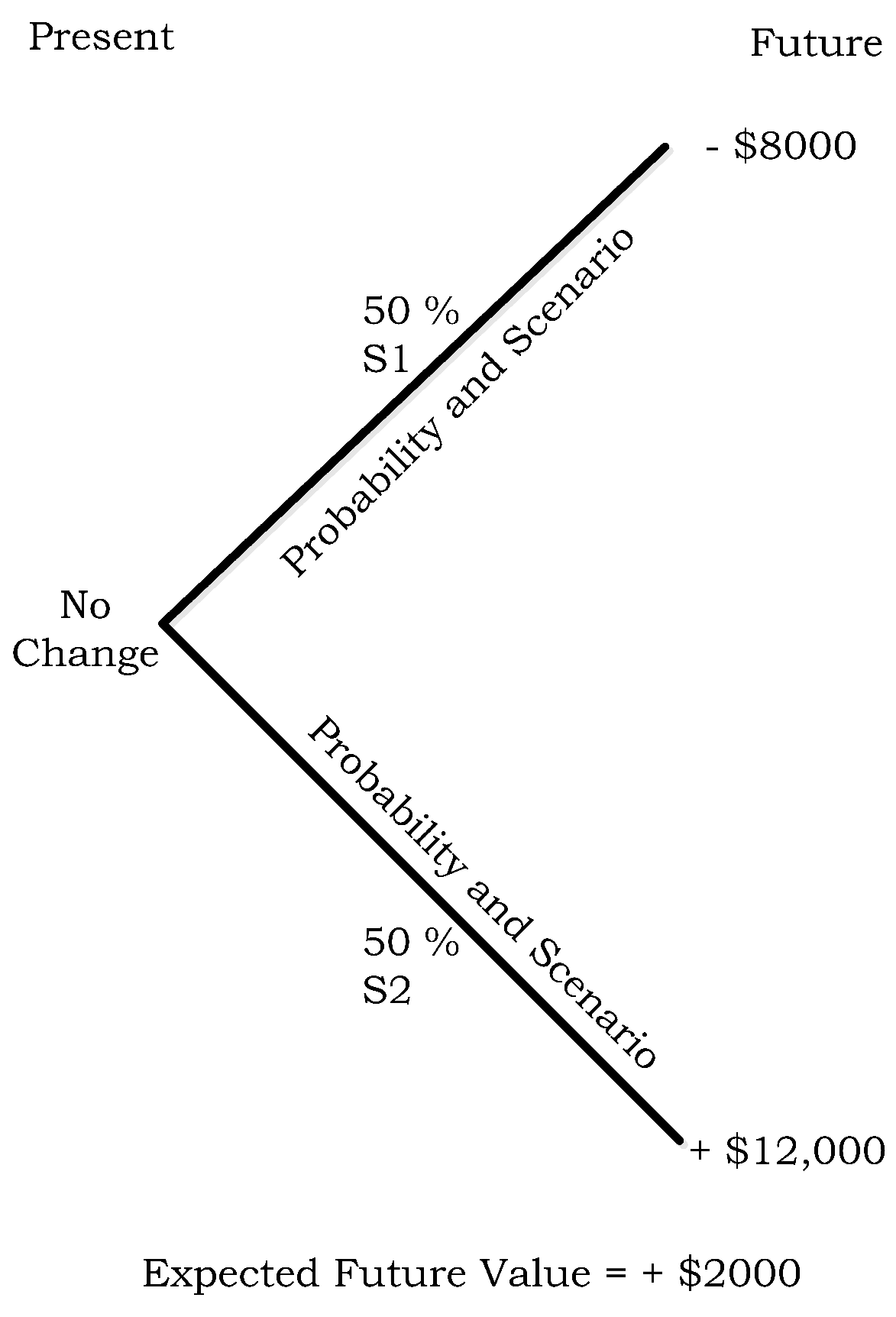

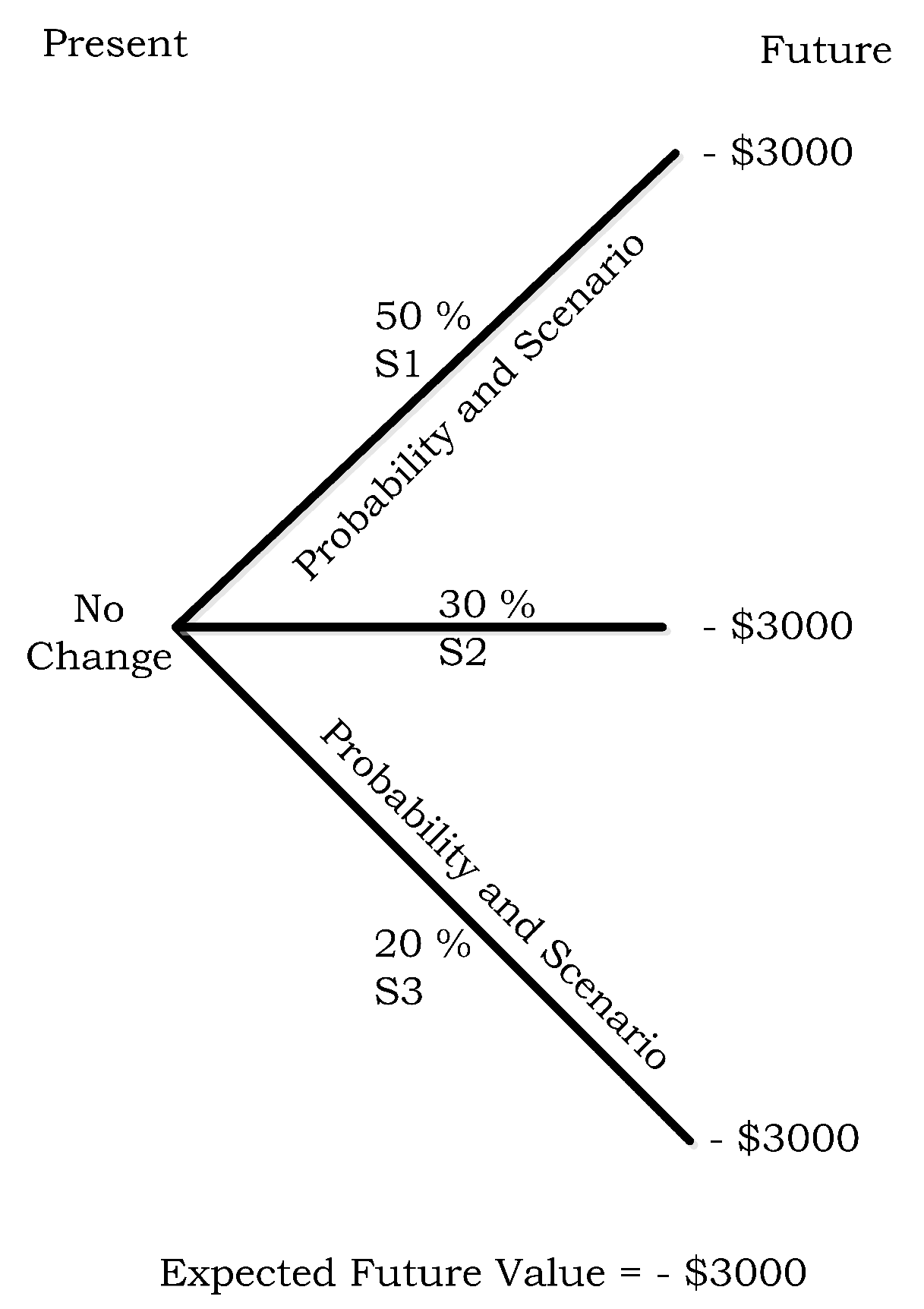

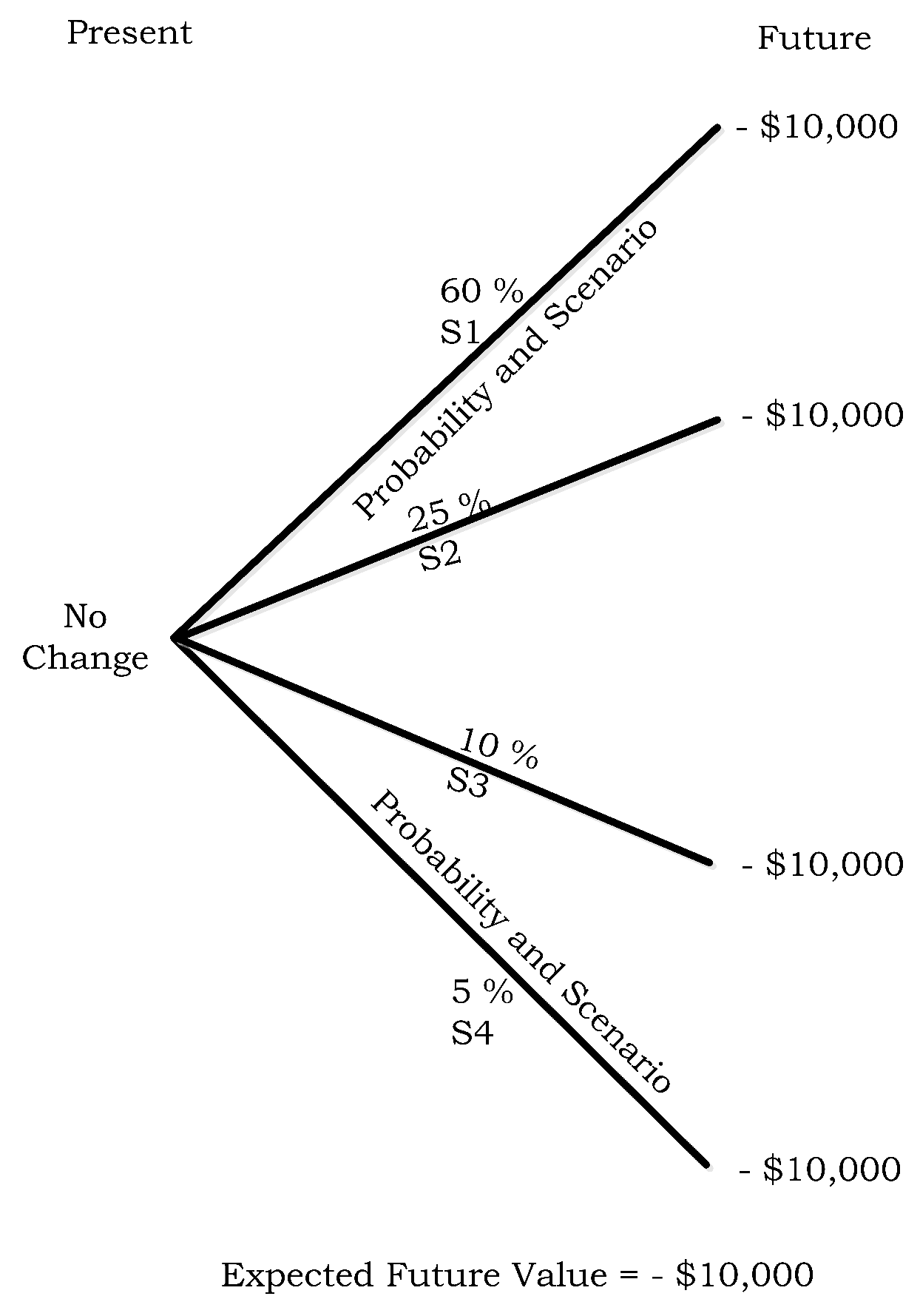

The hedged expected future value based on the company’s CVaR model can be calculated as shown in Equation (35).

where, βc is the company’s expected future value (hedged), ρs1 is the probability of s1, µh1 is the impact value (hedged) for state 1, ρs2 is the probability of s2, and µh2 is the impact value (hedged) for state 2.

In the perfectly hedged scenario, the expected future value from the company’s perspective is shown in Figure 10, and calculated as in Equation (36).

- µh1 = −$8000 (−$40,000 loss + $40,000 payout from 400 ISO contracts − $8000 paid to purchase 400 ISO contracts).

- µh2 = $12,000 ($20,000 revenue − $8000 (=$20*400) cost of 400 ISO contracts.

So, even if the hedger’s probability estimates are wrong and market’s probability estimates are correct, the hedger may still like to hedge the risk to minimize the variance in the potential impact (expected future value) of the underlying information security event.

In the given scenario, when the risk exposure has been hedged with an ISO contract, the ex-post performance of the hedge strategy (hedge efficiency) can be calculated as shown in Equation (37) [83].

where, Υe is the hedge efficiency, ξ is the expected or materialized impact of the risk event, γ is the expected or actual cost of hedging, and ηd is the expected or actual payout from the information security derivative contracts.

A value above or below the zero for Υe indicates over or under hedging. Since, the Υe obtained from the above equation is −20%, the hedge strategy is 20% less efficient than the perfect hedge strategy.

7.2. Information Security Vanilla Options

This subsection is divided into four parts to explain the application of ISVO in hedging the impact of an information security risk. The first part describes the scenario, second part presents the ISVO specifications, third part identifies the potential market participants and their incentive to do so. Lastly, in the fourth part the process of hedging with an ISVO is explained.

7.2.1. Scenario

Let us say a company “C” is in the business of providing cloud based services to its multinational clients. If the company suffers a cyber-attack (such as DDoS), such as [101,102,103], and its services are unavailable for some time then the company would suffer a major financial and reputational loss. The company estimates that an unavailability of services would cost $10,000 per hour.

7.2.2. Contract Specifications

The specifications of an ISVO contract to address the risk in the given scenario is shown in Table 12.

7.2.3. Participants and Incentives

The prospective participants, their motivation and incentives for participation in trading of ISVO at ISPM is shown in Table 13.

7.2.4. Risk Hedging

To demonstrate the application of ISVO, we consider only three states of the risk event in the given scenario. The three states are as follows:

- S1 = C does not suffers a cyber-attack in the trading period or its services are not adversely affected if attacked.

- S2 = C suffers a cyber-attack and its services are unavailable for 1 h.

- S3 = C suffers a cyber-attack and its services are unavailable for 3 h.

(1) Risk Analysis and Impact Estimation

We assume that the company “C” has completed its risk analysis and impact assessment. The company’s estimate based on the CVaR model is as, probability of no cyber-attack or no adverse impact is 50%, probability of service unavailability for one hour due to a cyber-attack as 30%, and probability of service unavailability for three hours due to a cyber-attack as 20%. Furthermore, if S1 occurs there is no loss to the company “C”. If S2 occurs the company may lose $10,000, as estimated by it. If S3 occurs the company may lose $30,000.

(2) Risk Response

In the given scenario, the cloud service provider may choose to hedge the risk by purchasing ISVO contracts. The buyer can buy an ISVO contract at $30 per option and the contract pays $100 per contract for each one hour of service unavailability and pays nothing if the company’s services are not adversely affected by a cyber-attack.

The current market price for the three states of the ISVO indicate that the market estimates the probability of no cyber-attack or no adverse impact of the attack as 60%, unavailability of the services for one hour as 30%, and unavailability of services for three hours as 10%.

(2.1) Unhedged Scenario

Based on the market’s probability estimate for the three states, the expected future value for the company in an unhedged scenario can be calculated as shown in Equation (39).

where, αm is the market’s expected future value (unhedged), ρs1 is the probability of s1, µu1 is the impact value (unhedged) for state 1, ρs2 is the probability of s2, µu2 is the impact value (unhedged) for state 2, ρs3 is the probability of s3, and µu3 is the impact value (unhedged) for state 3.

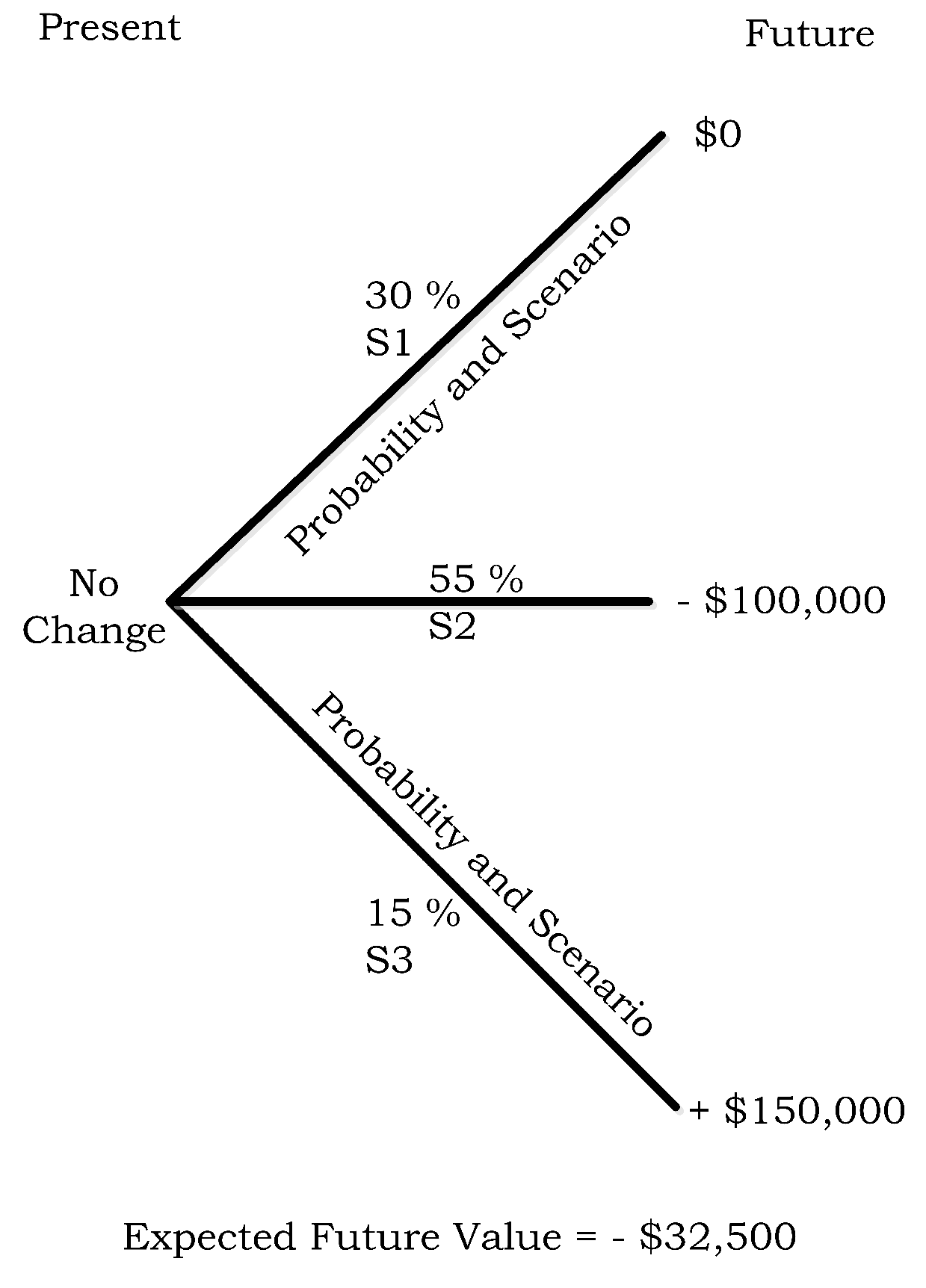

The expected future value from the market’s perspective in an unhedged scenario is shown in Figure 11, and calculated as shown in Equation (40).

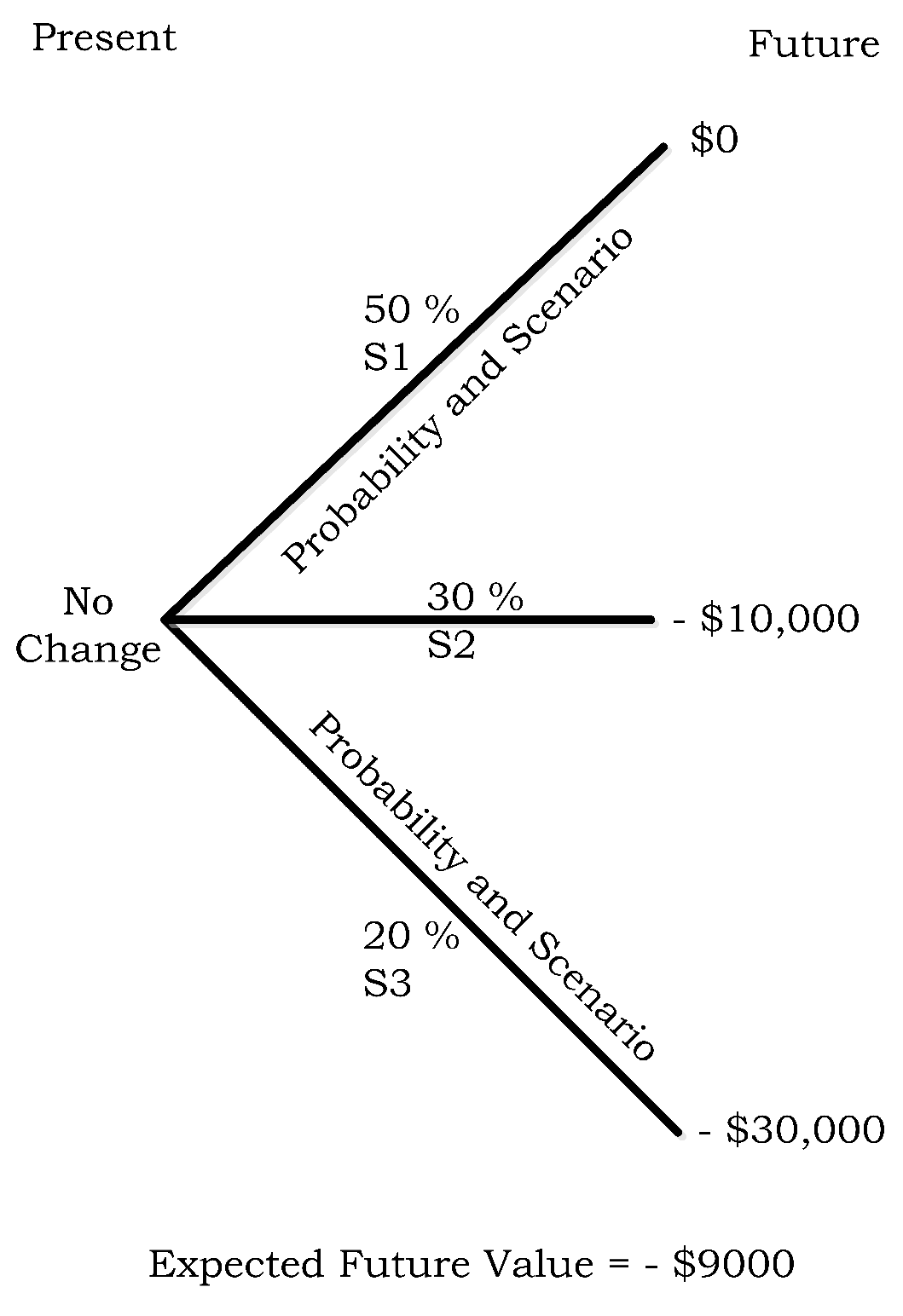

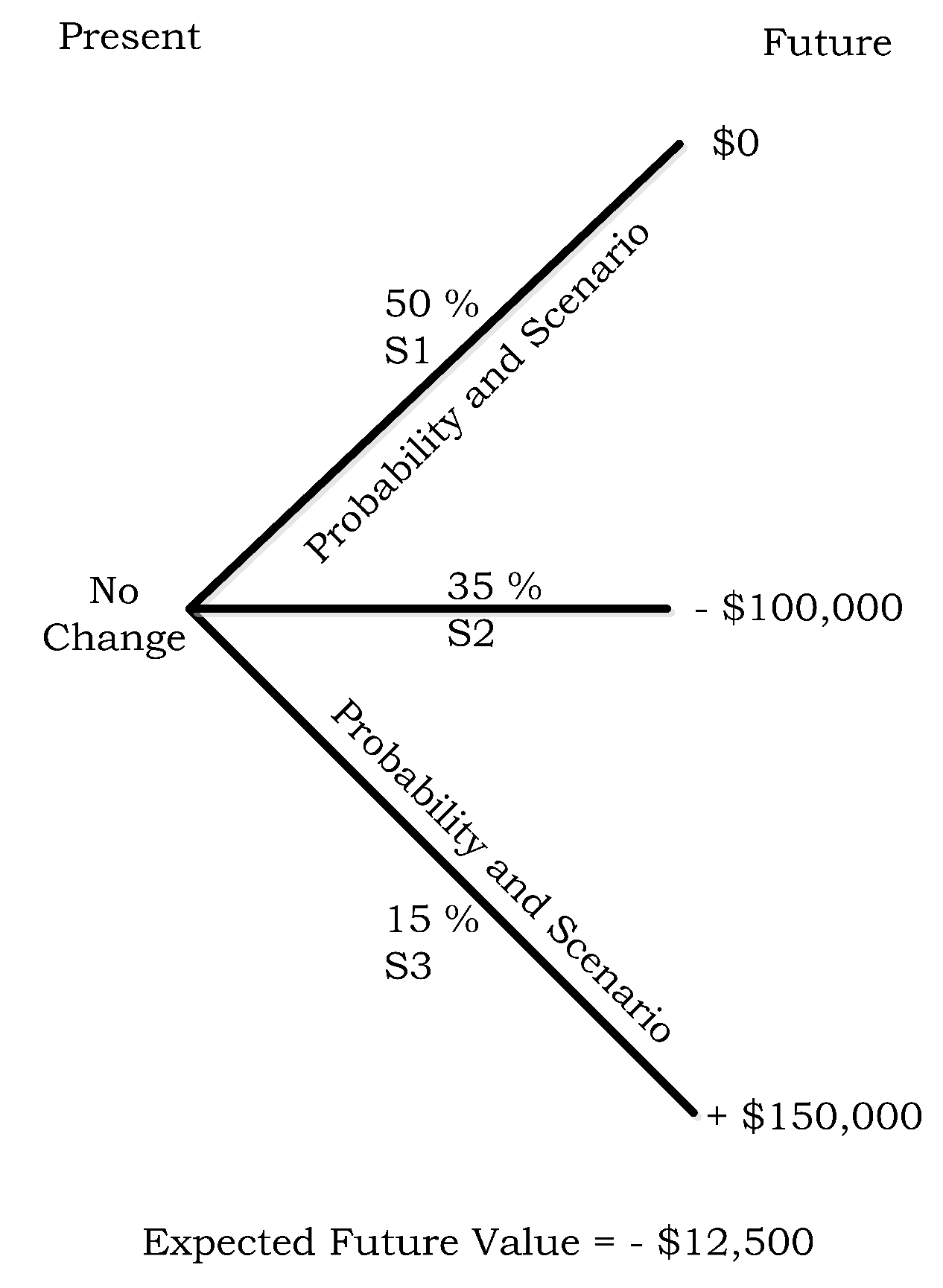

Based on the company’s risk estimate the expected future value in an unhedged scenario can be calculated as shown in Equation (41).

where, αc is the company’s expected future value (Unhedged), ρs1 is the probability of s1, µu1 is the impact value (unhedged) for state 1, ρs2 is the probability of s2, µu2 is the impact value (unhedged) for state 2, ρs3 is the probability of s3, and µu3 is the impact value (unhedged) for state 3.

The expected future value from the company’s perspective in an unhedged scenario is shown in Figure 12, and calculated as shown in Equation (42).

Thus, if the company remains unhedged then it would suffer a significant loss if the ISVO underlying information security event occurs.

(2.2) Hedged Scenario

If the company decides to hedge its maximum risk exposure of $30,000, then the first step is to determine the number of ISVO contracts that are required to perfectly hedge the risk exposure. We use the Equation (28) to calculate the required number of ISVO contracts. Thus, to perfectly hedge the risk exposure of $30,000, number of ISVO contracts required are computed in Equation (43).

For the sake of clarity and simple demonstration, we ignore the cost of transaction and the Equation (44) gives the number of ISVO contracts required to hedge $30,000 loss.

Thus, the hedger would pay $3000 to purchase 100 ISVO contracts at the rate of $30 per ISVO, ignoring the other costs such as exchange fee, cost of capital, etc.

We use the Equation (31) to do an ex-ante assessment of hedge effectiveness, as shown in Equation (45).

Therefore, the above hedge strategy with ISVO is expected to be 90.91% effective in mitigating the underlying information security risk.

In a perfectly hedged scenario the expected future value from the market’s perspective can be calculated as shown in Equation (46).

where, βm is the market’s expected future value (hedged), ρs1 is the probability of s1, µh1 is the impact value (hedged) for state 1, ρs2 is the probability of s2, µh2 is the impact value (hedged) for state 2, ρs3 is the probability of s3, and µh3 is the impact value (hedged) for state 3.

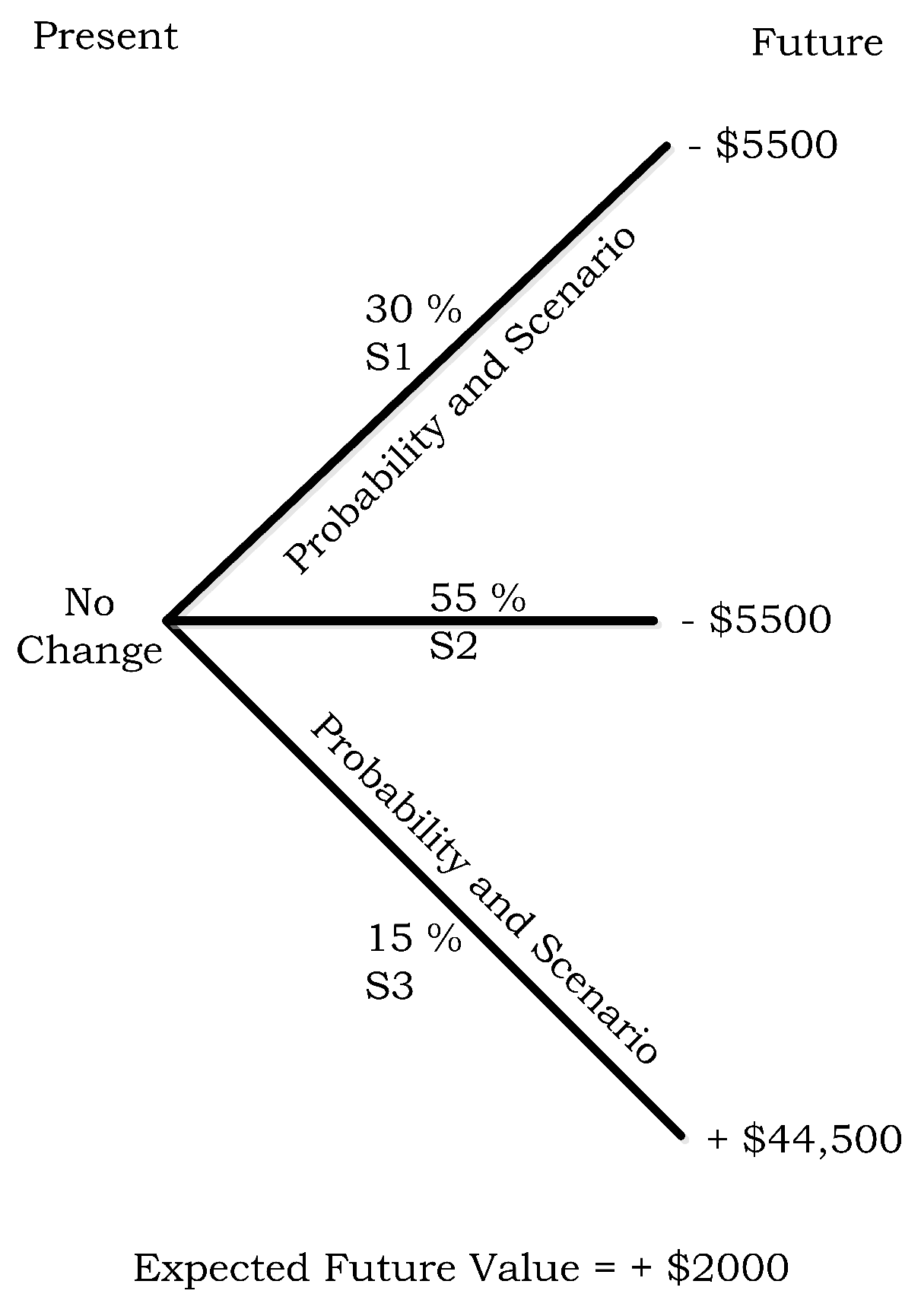

The expected future value from the market’s perspective in a hedged scenario is shown in Figure 13, and calculated as shown in Equation (47).

- µh1 = $0 loss due to no cyber-attack − $3000 cost to buy 100 ISVO contracts.

- µh2 = −$10,000 loss due to unavailability of services for one hour + $10,000 payout from 100 ISVO contracts − $3000 cost of purchasing 100 ISVO contracts.

- µh3 = −$30,000 loss due to unavailability of services for three hours + $30,000 payout from the 100 ISVO contracts − $3000 cost of purchasing 100 ISVO contracts.

In a perfectly hedged scenario, the expected future value based on the probability estimates obtained from the company’s CVaR model can be calculated with the Equation (48).

where, βc is the company’s expected future value (hedged), ρs1 is the probability of s1, µh1 is the impact value (hedged) for state 1, ρs2 is the probability of s2, µh2 is the impact value (hedged) for state 2, ρs3 is the probability of s3, and µh3 is the impact value (hedged) for state 3.

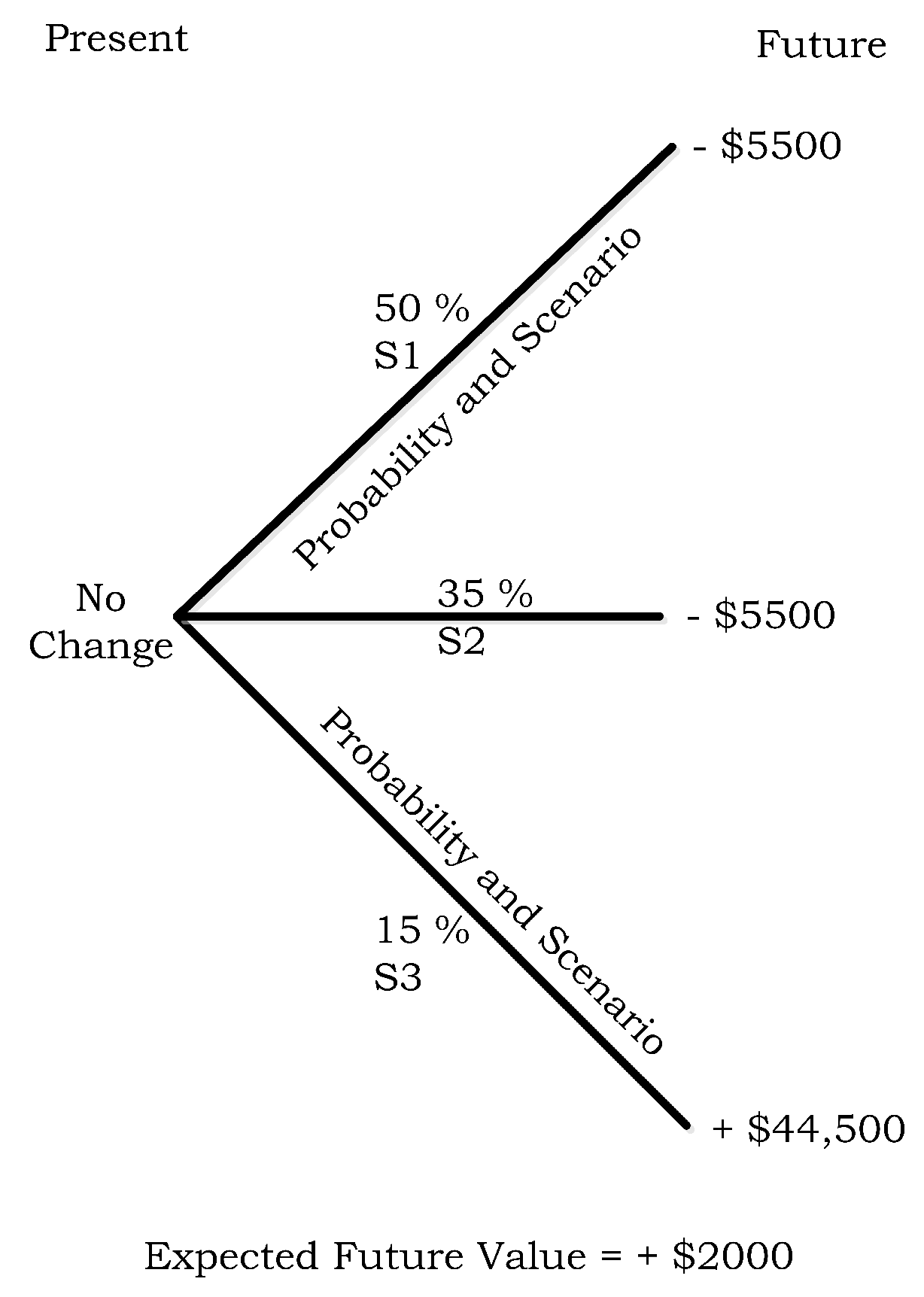

The expected future value from the company’s perspective in a hedged scenario is shown in Figure 14 and calculated as shown in Equation (49).

- µh1 = $0 loss due to no cyber-attack − $3000 cost to buy 100 ISVO contracts.

- µh2 = −$10,000 loss due to unavailability of services for one hour + $10,000 payout from 100 ISVO contracts − $3000 cost of purchasing 100 ISVO contracts.