The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential

1

College of Business, Abu Dhabi University, P.O. Box 59911, Abu Dhabi, UAE

2

Jagran Lakecity Business School, Jagran Lakecity University, Bhopal 462044, India

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(2), 494; https://doi.org/10.3390/su10020494

Submission received: 10 December 2017

/

Revised: 19 January 2018

/

Accepted: 9 February 2018

/

Published: 13 February 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:This paper presents an analysis of the literature concerning the impact of corporate sustainability on corporate financial performance. The relationship between corporate sustainable practices and financial performance has received growing attention in research, yet a consensus remains elusive. This paper identifies developing trends and the issues that hinder conclusive consensus on that relationship. We used content analysis to examine the literature and establish the current state of research. A total of 132 papers from top-tier journals are shortlisted. We find that 78% of publications report a positive relationship between corporate sustainability and financial performance. Variations in research methodology and measurement of variables lead to the divergent views on the relationship. Furthermore, literature is slowly replacing total sustainability with narrower corporate social responsibility (CSR), which is dominated by the social dimension of sustainability, while encompassing little to nothing of environmental and economic dimensions. Studies from developing countries remain scarce. More research is needed to facilitate convergence in the understanding of the relationship between corporate sustainable practices and financial performance.

1. Introduction

Markets are becoming increasingly competitive, and the pace of change is putting companies under unprecedented pressure to not only succeed, but sustain their success into the future. Corporate sustainability has gained a lot of attention in recent years, as companies, investors, and consumers alike are turning their attention towards increasingly critical corporate sustainability [1,2]. Companies are expected to go beyond the narrow- and short-term financial focus, and stretch into an encompassing economic, environmental, and social sustainability [3]. Developing corporate strategies to do “well” by doing “good” and turning companies into responsible organizations that care about the environment, and the social aspect is becoming increasingly a must rather than a choice to lead in future markets [4,5].

Sustainability is defined as meeting our needs today without compromising future generations’ ability to meet theirs [6]. Corporate sustainability is about expanding the financial bottom line into a triple bottom line, which includes environmental and social aspects of corporate performance [7]. As companies scramble to stay relevant in changing markets, they have come to realize that it is no longer enough to focus on the economics of their businesses alone [8]. Designing a robust business strategy is becoming increasingly dependent on how well a company positions itself in terms of sustainable development that balances financial, environmental, and human development [9].

The body of literature around the subject is far from mature. In fact, research is still struggling to find universality in the accepted understanding of corporate sustainability, or what constitutes an adequate suite of corporate financial measures to correlate to corporate sustainability practices [6,10,11]. Maybe the lack of universality is not such a problem when it comes to a wide range of industries and varying businesses, in terms of the relationship between sustainability and financial performance [12]. However, the fact remains that a comprehensive synthesis of the body of literature is greatly needed at this junction in the progress of the subject in the literature [13,14,15].

Two competing theories attempt to describe the impact of sustainability on corporate financial performance: value creating and value destroying [12]. The value-creation approach theorizes that firm risk is reduced with the adoption of environmental and social responsibility. In contrast, the value-destruction theory predicts that companies engaged in environmental and social responsibility lose focus on profitability, and instead pursue pleasing stakeholders at the expense of shareholders. Several other theories attempt to explain the relationship between sustainability and corporate financial performance. Those theories are linked to the influence (positive, negative, or neutral) and the causality (direction) of the relationship. Like with value-destruction theory, the trade-off theory suggests a negative relationship when resources are channeled towards less profitable sustainable activities [10,16]. A positive relationship is explained in resource-based view (RBV) theory and Stakeholder theory. RBV stipulate that a firm possesses unique capabilities which, if strategically exploited, can achieve competitive advantage leading to better financial performance [3]. In stakeholder theory, fulfilling the requirements of stakeholders (environmental or social) contributes to financial performance [5]. Slack resources theory suggests a reverse causality, where superior financial performance results in enough slack to entertain sustainable activities [17]. Furthermore, a positive relationship and a reverse causality lead to a virtuous cycle [18]. Finally, mixed results exist in literature regarding the relationship between sustainability and corporate financial performance, and some researchers even argue that a generalizable, unidirectional relationship applicable to all organizations in all situations simply does not exist [19].

While most reviews focus on a single or a combination of two dimensions of sustainability, those that focus on all three dimensions, such as this paper, are rare. Single-dimension reviews tend to be mostly about the environmental dimension, and do not serve as a comprehensive approach to all three dimensions of sustainability, as in this review [15,20]. On the other hand, reviews that examine all three dimensions of sustainability are scarce and outdated. For example, the most recent literature examined by Goyal et al., in their review on all three dimensions of sustainability, is from 2011 [21]; as this paper shows, some of the most substantial literature trends only start to appear in 2012 and onwards. Other recent reviews only examine influencers on the relationship between sustainability and corporate financial performance as reported in literature, such as firm, managerial and industry characteristics [19]. Similarly, other recent reviews only focus on single dimensions of sustainability. None of those recent reviews examine all three dimensions of sustainability and their impact on corporate financial performance.

This paper describes the progress of literature in the subject of the corporate sustainability impact on financial performance. It also identifies trends in literature while revealing future research paths. Furthermore, this work helps structure future research in the subject, by offering a much-needed critique of shortcomings in current literature trends while also identifying opportunities to advance the topic towards a universal conclusion. Publications are identified from the literature using content analysis and bibliometric listing principles. The review considers time, country, and industry trends, while establishing the evolving use of different financial measures in the evaluation of corporate performance.

2. Methodology

A systematic content analysis approach was used to shortlist relevant publications from literature. A complete bibliographic listing of collected literature has been compiled, which includes titles, journals, authors, years of publication, etc. Descriptive statistics were also utilized, such as number of publications per unit of time and journal distribution of publications [3,22,23].

This review focuses on major peer-reviewed journals indexed in quality and impact rankings, such as Scopus and ABDC. Those publications that are ranked as Q1 or Q2 in Scopus and A* or A in ABDC list were included in this review [19]. This selection of the best ranked papers ensured not only the quality of the articles by being the most reviewed and validated, but also it was closest to the current state of research during their respective times of publication [24].

In selecting articles that research the impact of sustainability practices on corporate financial performance, several keywords were used: corporate sustainability, financial performance, sustainability practices, sustainability impact, corporate social responsibility (CSR), economical sustainability, environmental sustainability and social sustainability [20,25,26]. Only peer-reviewed articles available with their full text in the English language were included in the research. Rounds of article elimination took place to shortlist articles related to the subject of the impact of sustainability practices on corporate financial performance. Starting with an initial list of articles, a series of validation and re-focus of research keywords resulted in further elimination of articles and the addition of new ones from various databases:

- ProQuest

- EBSCO

- Science Direct

- Emerald

- JSTOR

- Springer Link

- Scopus

This systematic approach shortlisted a total of 132 publications for examination. Most of the excluded literature focused on agricultural science, sustainability reporting, integration of sustainability practices, and measurement. Other excluded literature did not include the link between practices and financial performance [27,28]. Furthermore, some research focused on the feasibility of investment in firms characterized as high in sustainability practices, while others examined the “virtuous cycle” of a bidirectional relationship between corporate sustainability and financial performance [29]. Those research areas are in contrast with the focus of this literature review, which is on publications that examine financial performance between firms based on their sustainability.

The articles are classified according to the time period they were published [19]. The time periods start before 2002, because of the scarcity of articles every year between 1984 and 2002. Only after that time did we start to see a trend taking shape in the number of articles. This coincides with the topic gaining momentum and focus in the literature. Hence, the papers preceding 2002 are consolidated in one time period for practicality. After the time period pre–2002, the time periods continue in constant two-year intervals, until the last time period from 2016 to October 2017.

3. Results

3.1. Time Period Distribution

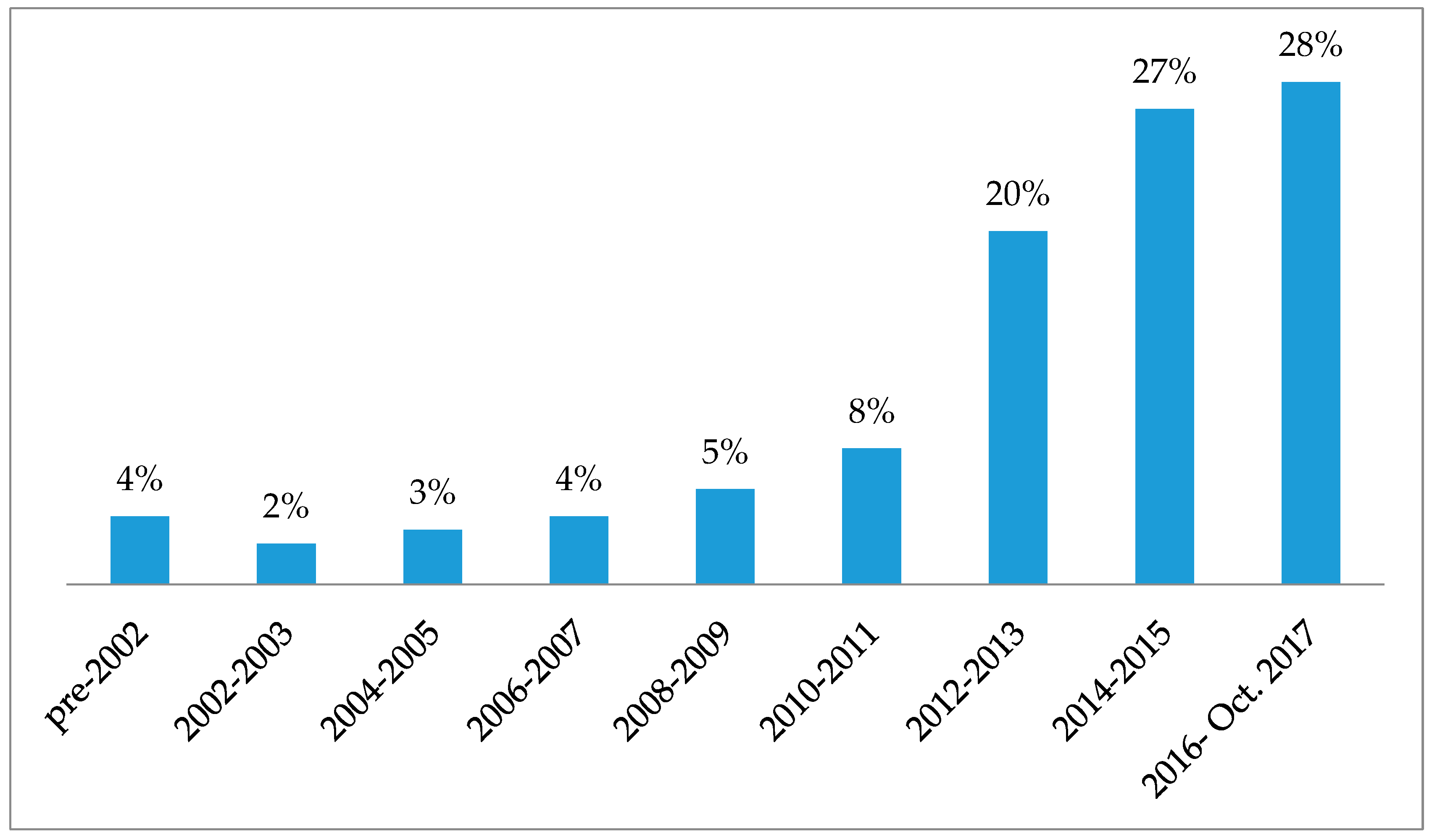

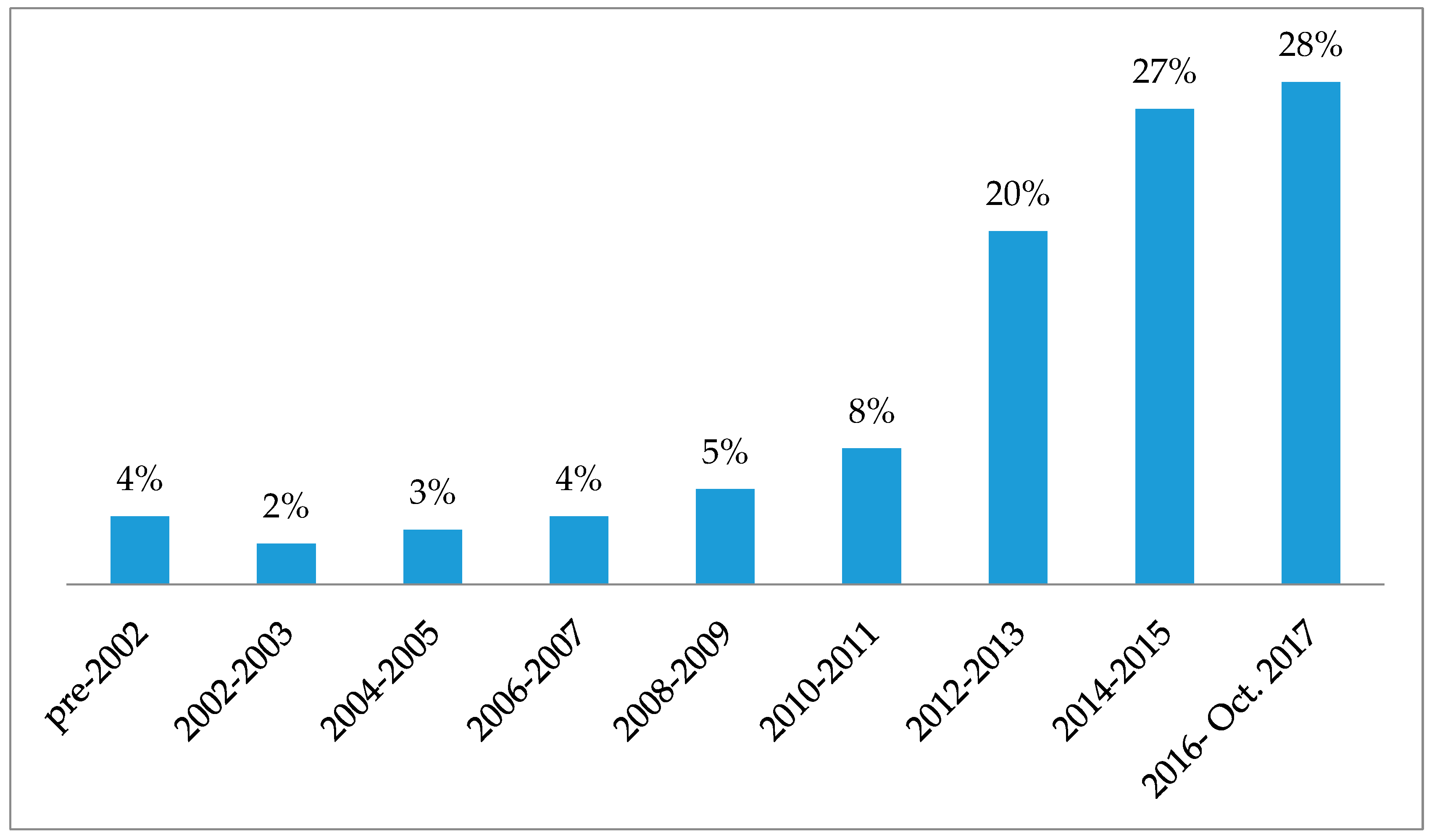

The percent distribution of publications across the time periods shows a steady and gradual increase in the research on sustainability impact on corporate financial performance. This classification quantifies the growth in the research in correlation to time periods (see Figure 1).

Only 4% of the total 132 articles in the review occurred before 2002. Starting in the period 2002–2003, research gained momentum and continued to grow steadily until the period 2010–2011. A significant increase in research occurs starting in the period 2012–2013, more than doubling from the previous period. Starting in the period 2012–2013 onward, the number of publications continued to increase uniformly. In the last three periods, 75% of the 132 articles were published. This shows a three-phase growth in research, where the topic was taking shape prior to 2002 and started to gain focus between 2002 and until 2011, after which a significant shift occurred in the number of articles.

3.2. Country Distribution

The distribution of articles according to where authors are based is significant in establishing the global state of the research in the topic of sustainability impact on corporate financial performance [21]. The author-based distribution shows the overall maturity of literature across the world (see Table 1).

The US has dominated the literature on the subject from the topic’s infancy in the period pre–2002 and throughout the rest of the periods studied. Other significant countries include Spain, Taiwan, and China, among others. It is worth noting that the growth in research is highest in China in the last two periods. Taiwan, China, and Malaysia are leading countries of developing economies [30] in the number of articles.

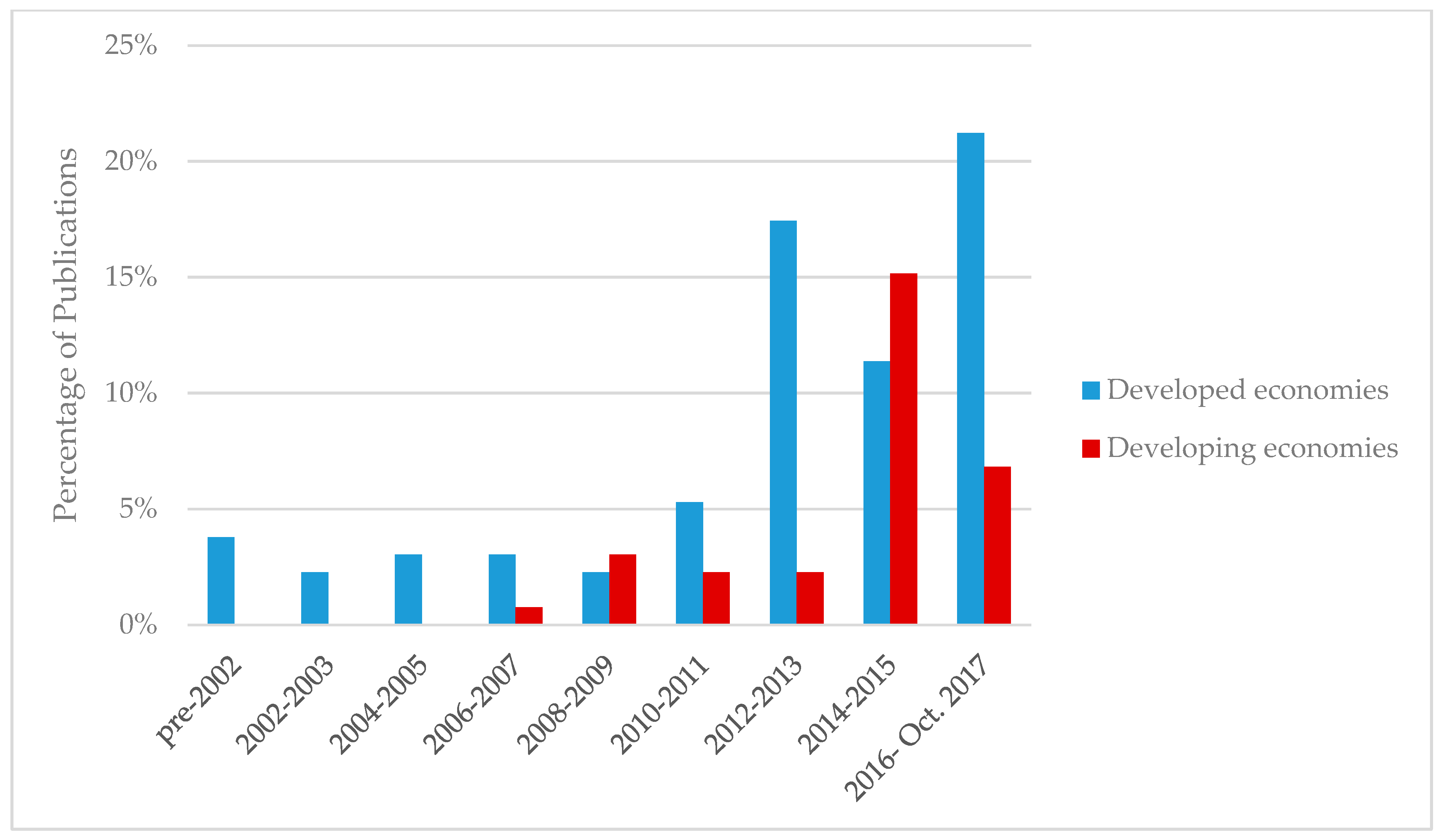

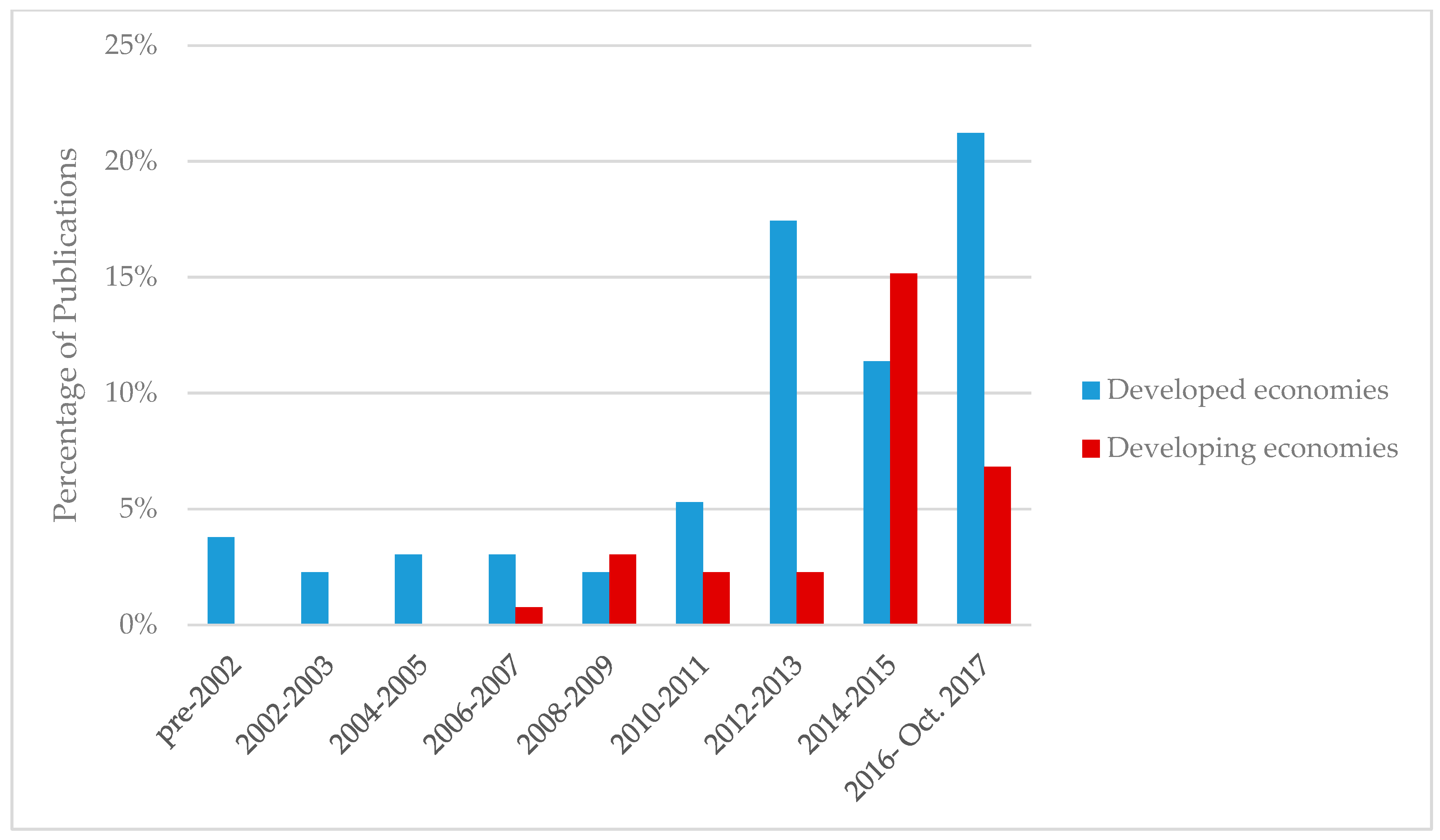

Country distribution of developed and developing economies shows a significant lead by developed economies in the number of publications in corporate sustainability impact on financial performance (see Figure 2). It is interesting to note that up to the period 2006–2007, there were no publications from developing economies. Developing economies stayed at roughly the same number of publications for the next three-time periods. In the period 2014–2015, a spike was observed in the number of publications from developing economies. In general, the number of publications from developing economies is significantly lower than that from developed economies. This suggests more research is needed in developing economies, despite the fact that some developing economies, such as Taiwan and China, are witnessing the highest rate of growth in the number of publications. As more research becomes available from developing economies, research in this field is expected to benefit by becoming more generalizable.

3.3. Industry Distribution

An industry-based classification shows 114 articles out of the total 132 in the multi-industry category regarding sustainability impact on corporate financial performance (see Table 2).

The multi-industry category refers to publications that examine more than one industry, such as when authors use indices and secondary stock market data [21]. The next highest classification is manufacturing-related articles, with seven publications, and hospitality with three. The remaining industries have one publication each. Multi-industry publications offer a more universal applicability to organizations than the rest of the categories. Although specific industries offer valuable insights in specific industries, they are limited in their generalizability. The fact that most of literature fell into the multi-industry category comes as no surprise for this research topic, as authors have sought to find universal applicability.

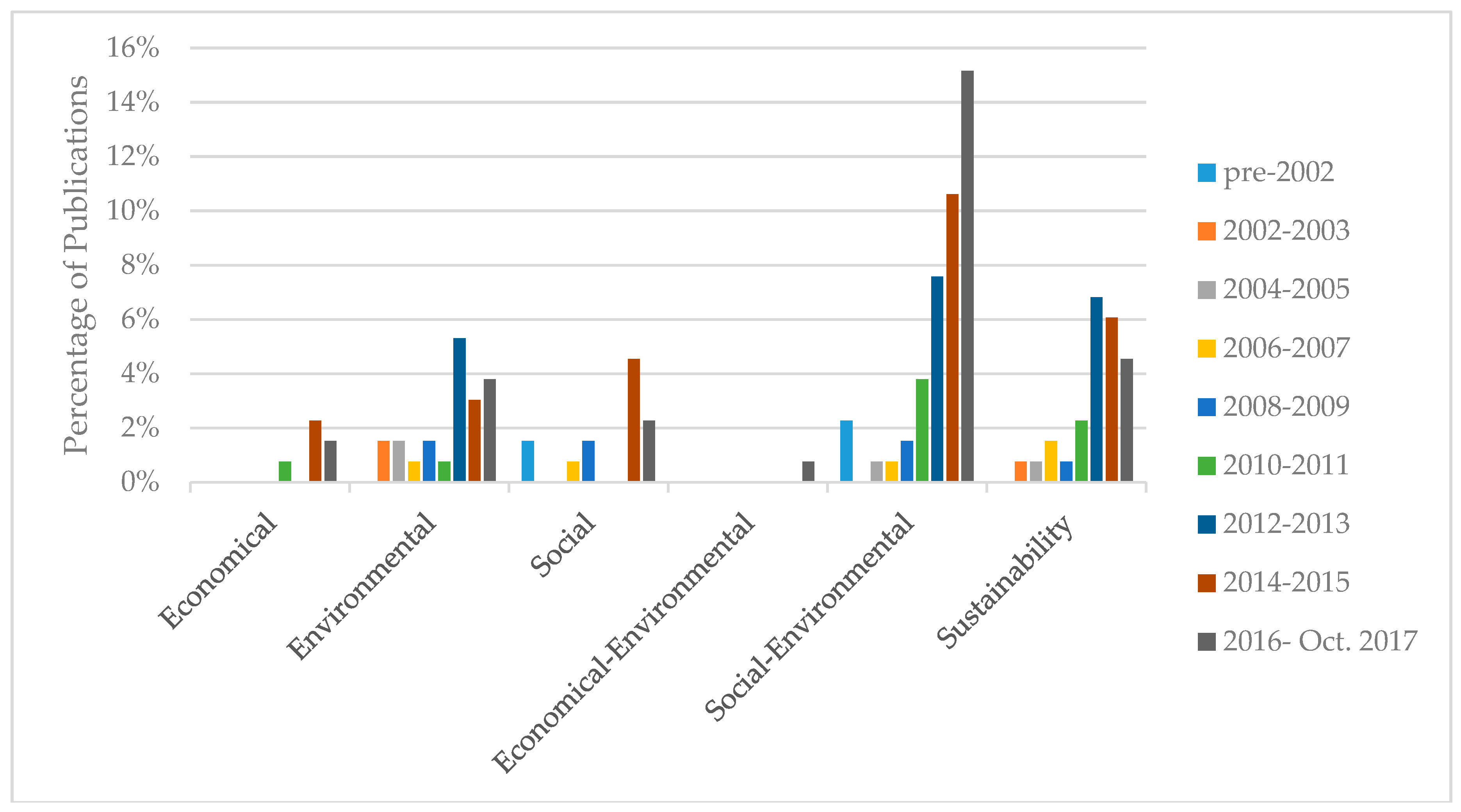

3.4. Sustainability Dimension Distribution

The distribution of articles based on the sustainability dimensions researched shows three major groups: single dimension, combination of dimensions, and total sustainability. More specifically, dimension-based research is broken down into these general sub-divisions:

- Single Dimension:

- Economic

- Environmental

- Social

- Bi-Combination of Dimensions:

- Economical–Environmental

- Social–Environmental

- Sustainability

Articles in the single-dimension group tackle only one dimension of sustainability: economic, environmental, or social. There are two combinations of dimensions: economical–environmental and social–environmental. The third group is made up of total sustainability, with the combined effect of the three dimensions rather than individual or a combination of dimensions. In the single-dimension group, the environmental dimension dominated over the entire time period, in comparison to economic or social dimensions. The combination social–environmental dimension, also denoted as CSR in those articles, shows a strong and consistent growth, especially in the last five time periods, starting in 2008 onward. This growth is in contrast with the decline in the last group, total sustainability, which peaked the time period 2012–2013 and went into a steady decline after that. The decline in the encompassing total sustainability dimension coincides with the growth in the social–environmental combination. This suggests that the literature is using the combination social–environmental dimension as a substitute for a holistic sustainability notion in the assessment of sustainability impact on corporate financial performance. Given the popularity of CSR research, the social–environmental dimension offers a convenient replacement for total sustainability, even though it is not an exact fit. CSR research underplays the environmental dimension, while completely overlooking the economic dimension. When focusing on the last three-time periods, the combination social–environmental dimension (or CSR) not only dominated other dimensions, it was also the only one growing (see Figure 3). This suggests that theory in the subject is not converging yet, and needs further development to mature.

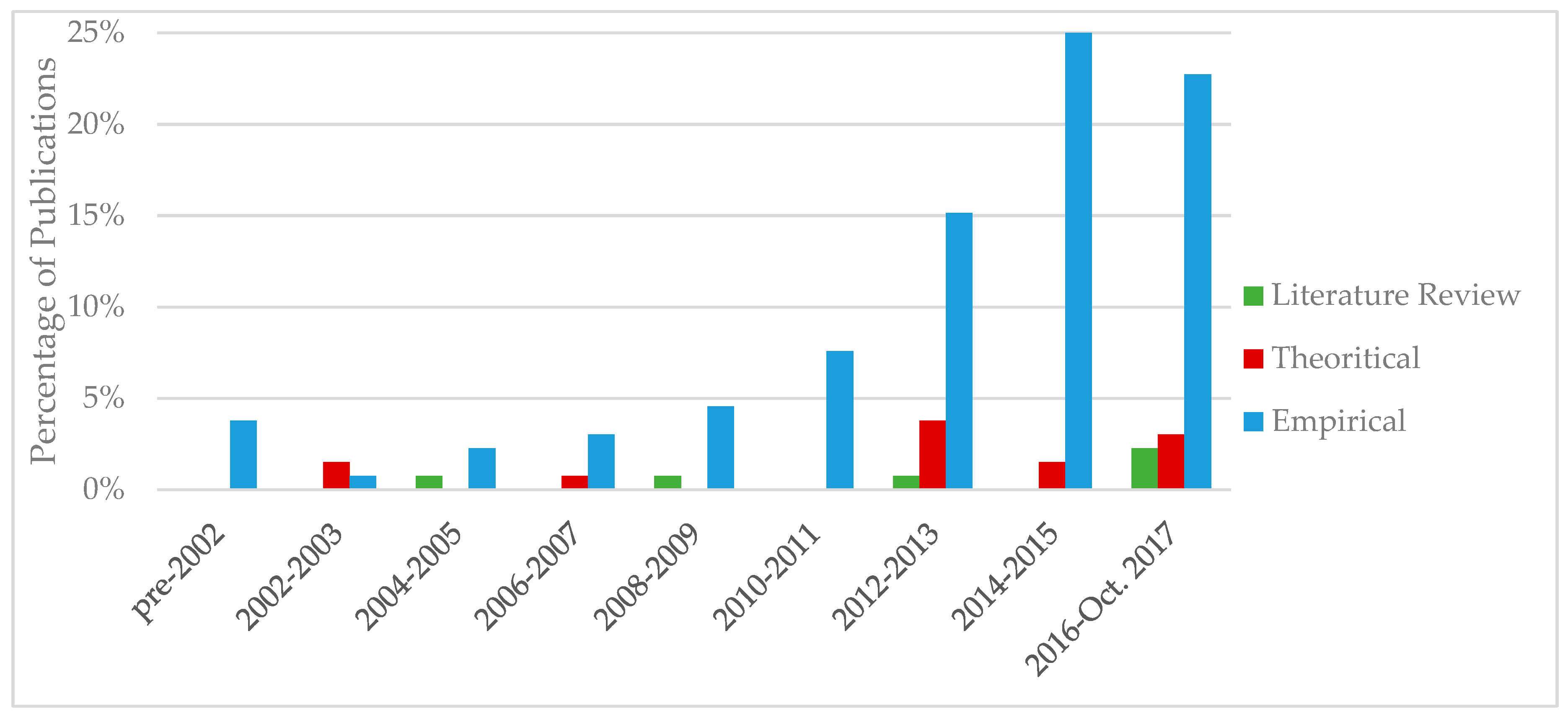

3.5. Research Type Distribution

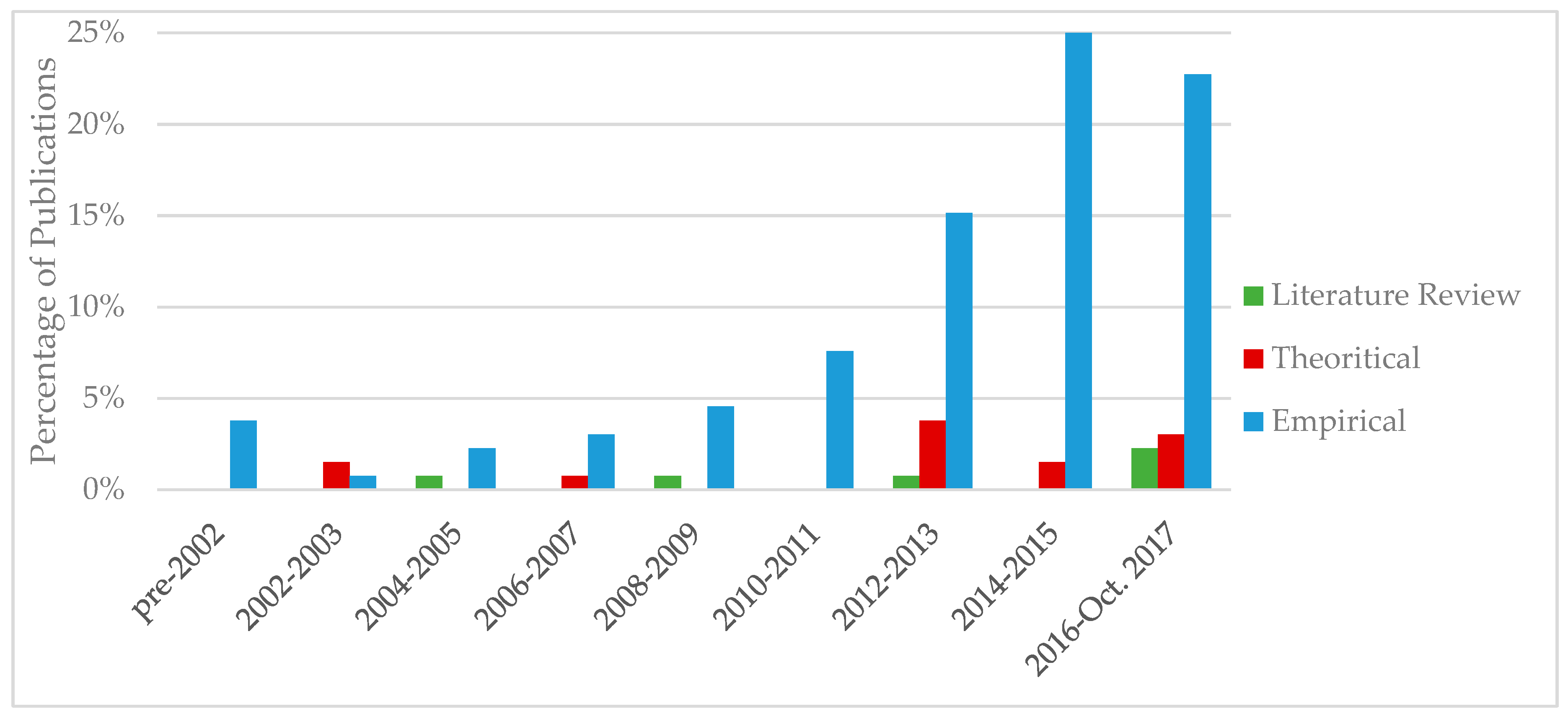

The distribution of articles based on research type shows a clear lead for empirical publications over theoretical and literature review papers. It is worth noting that theoretical publications are rare, and they only started to show a significant appearance in the time period 2012–2013, which coincided with the spike in overall number of publications witnessed in the same period. Another interesting correlation that exists in the same time period, 2012–2013, was that the number of publications that considered total sustainability peaked (see Figure 3). The number of empirical publications continued to increase and naturally follow the same growth trend as the total number of publications (see Figure 1 and Figure 4).

3.6. Journal-Wise Distribution

This literature review examines highest-ranking publications from reputable journals. Those publications represent the most validated publications with the highest impact on literature.

A total of 68 reputable journals have published in the subject of sustainability impact on corporate financial performance during the specified time periods. The Journal of Business Ethics published the most articles on the subject, with 36 publications. Other notable journals include Social Responsibility Journal and Management Decision, with eight and six publications, respectively (see Table 3).

3.7. Distribution of Methodology Approaches

The distribution of research methodologies adopted in the literature shows that most articles used regression analysis in examining the relationship between corporate sustainability and financial performance, scoring 48 articles out of 132. Some articles use more than one methodology when carrying out analysis. An interesting observation is that the literature uses a wide selection of methodologies. This further exacerbates the problem of inconclusive literature when it comes to the relationship between corporate sustainability and financial performance. Even though those articles examine different contexts, using a wide selection of methodologies can affect convergence of results on the nature of the subject relationship (see Table 4).

3.8. Measures of Total Sustainability

The complexity in measuring corporate sustainability comes from the multidimensional nature of the concept itself and how different corporate contexts influence it [31]. Stock market indices offer a suitable tool to measure sustainability performance of firms, such as the widely used Dow Jones Sustainability Index (DJSI) [32,33,34]. Critics to this approach argue about the inherent problem of establishing suitable weighting for the contribution of different dimensions towards total sustainability [6]. Other approaches to measurement include efficiency, in terms of value created per unit of environmental or social damage [35,36]. Several other measurement tools exist, such as qualitative sustainability initiatives, benchmarking standards, and survey-based approaches [37,38]. While each approach has its critics, researchers argue in favor of separating sustainability into its three dimensions for operational level decision-making. However, they also argue for the necessity of considering total sustainability (the aggregate of economic, environmental, and social dimensions) to achieve sound strategic decisions [35].

3.9. Distribution of Financial Measures

The publications use different types of corporate financial measures in examining the impact of sustainability practices on financial performance. Those measures are important in understanding the relationship between corporate sustainability practices and financial performance.

The articles were examined for measures used in studying the dependent variable of corporate financial performance (see Table 5 and Table A1). Accounting-based measures, such as return on assets (ROA), return on equity (ROE), return on investment (ROI), and earning per share (EPS) lead market-based measures that appear later in the time periods [22]. ROA was used in 53 out of the 132 articles, which is almost twice as many times as ROE, the second most-used measure. Other significant measures included Sales, ROI, EPS, Tobin’s Q, etc. Profitability-related measures like ROA, ROE, ROI, and ROS appear throughout the time periods and make up the majority of the measures. In contrast, market-related measures such as Tobin’s Q, Price to Earning (P/E) Ratio, Market Valuation, Cash Flow, etc. appear later in the time periods especially from 2012–2013 onward. The surge in the literature that started in the time period 2012–2013 coincides with a surge in the number of unique financial measurements used. Several market-related financial measures started to appear for the first time in the publications in 2012–2013, such as market return, market share, market valuation, market share, etc. In search for more reflective measures of corporate financial performance in relation to sustainability practices, the literature increasingly used market-based financial measures. Those measures offer a better ability to predict long-term corporate financial performance [9].

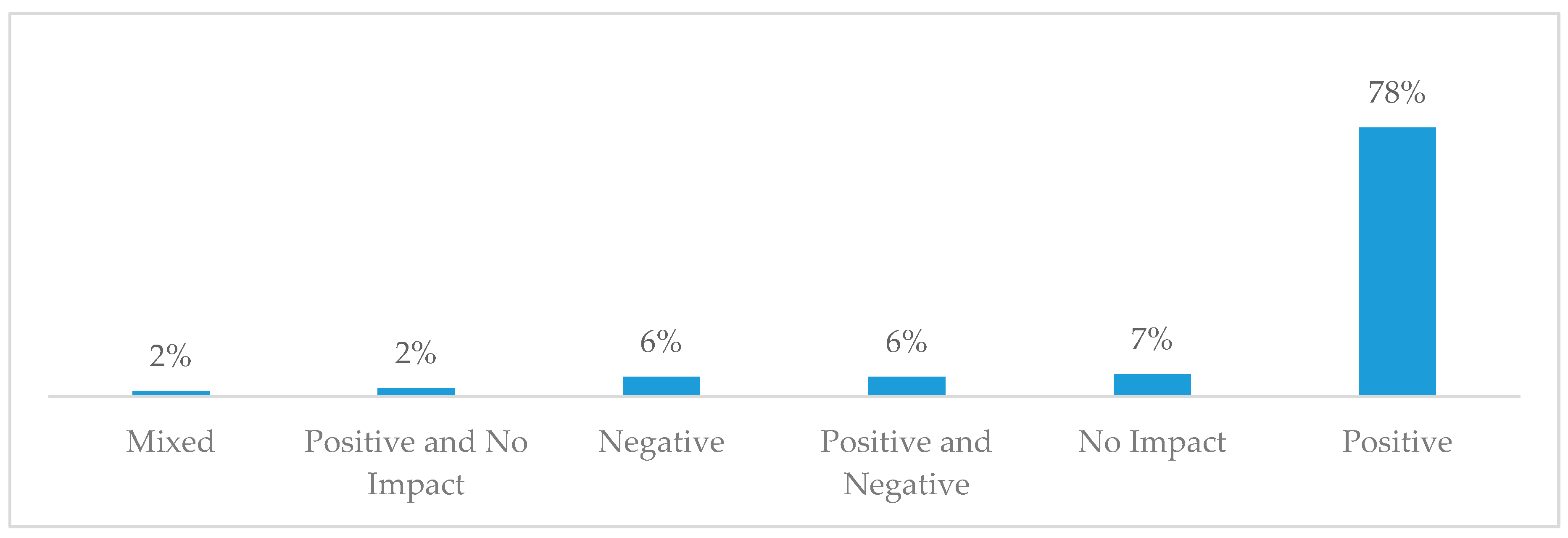

3.10. Impact of Sustainability Practices on Corporate Financial Performance

The articles were distributed in different combinations of the three possible outcomes of a relationship between sustainability practices and corporate financial performance: positive, negative or no impact. The percentage of articles that reported a positive relationship was 78% out of the total 132 articles (see Figure 5). Those that reported a no-impact relationship were 7%. Articles that reported both a positive and negative relationship were 6%, where some of the studied sustainability practices resulted in a positive impact, while others resulted in a negative relationship. Negative impact was reported in 6% of the articles, while those that reported both a positive and no impact relationship were at 2%. Articles that report a mixed result of positive, negative, and a no-impact relationship were 2% of the entire population of articles. The results of the distribution of sustainability impact on corporate financial performance suggest that a positive relationship is more probable between sustainability practices and corporate financial performance. Several reasons are suggested, which contribute to the differing results. First, the subject articles use different research methodologies and study designs, especially in terms of measurements of the dependent variable corporate financial performance. Moreover, the results they obtain are representative of the specific data, industry, firm size, or market they examined. Despite those differences, a positive impact of sustainability on corporate financial performance dominates the literature.

4. Discussion

Literature moved from studying the impact of single sustainability dimensions on corporate financial performance towards a more encompassing total sustainability impact, which later morphed into a strictly environmental–social combination, such as in CSR. The problem with this approach is that the environmental part of CSR is small, and can easily miss the full impact of environmental sustainability. This, however, seems to be compensated for by a healthy number of articles that have continued to appear in the last six years on the single dimension of environmental sustainability, in comparison to either of the single economic or social dimensions of sustainability.

Literature continues to add new financial measures, especially market-based ones, when examining the impact of sustainability practices on corporate financial performance. Although some accounting financial measures continue to dominate the spectrum of measures in literature, we are yet to witness a universal agreement among researchers on what constitutes a suitable suite of financial measures. Market-based financial measures complement accounting measures, by offering better insights on corporate performance that incorporate future performance expectations. Market-based financial measures contribute to the sharp rise in the number of unique measures starting in 2012. This sharp rise coincided with another sharp rise in the number of articles on the sustainability impact on corporate financial performance during the same time period. While those trends were taking place, another interesting trend appeared, when the literature started moving towards consolidating a holistic sustainability approach to corporate performance with a social–environmental combination. The problem with this combination approach is that it overlooks economical sustainability while closely resembling CSR, which underplays the environmental sustainability.

The literature exhibits an overwhelmingly positive relationship between sustainability practices and corporate financial performance. A minority of literature reports a negative or mixed relationship, or reports no significant relationship between corporate sustainability and financial performance. There are several contributing factors to this variation in results. First, the use of different research methodologies in literature is a direct contributor [18]. Another contributing factor to the variation in results includes the varying financial measures used to assess performance. Similarly, differences in firm size, industry, and analyzed sustainability practices all contribute to the variation in results regarding the relationship between corporate sustainability practices and financial performance [39].

The number of publications from countries with developing economies continues to lag behind those of developed economies [40]. A gap in literature exists for publications that examine the subject of corporate sustainability impact on financial performance in countries of developing economies. Further research is needed for countries of developing economies.

The review outcomes are limited to the databases and the top-tiered journals examined, as well as to the time boundaries described. This review does not include the entire possible universe of literature on the topic. These limitations can influence the outcomes of this research. However, several opportunities exist to expand the coverage of the subject.

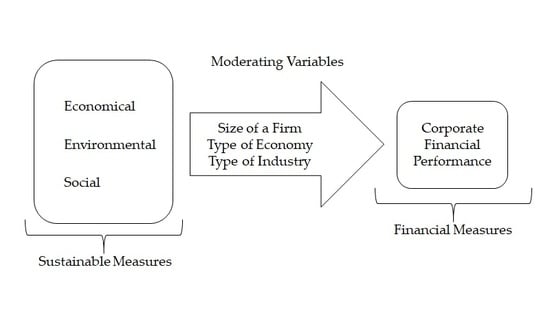

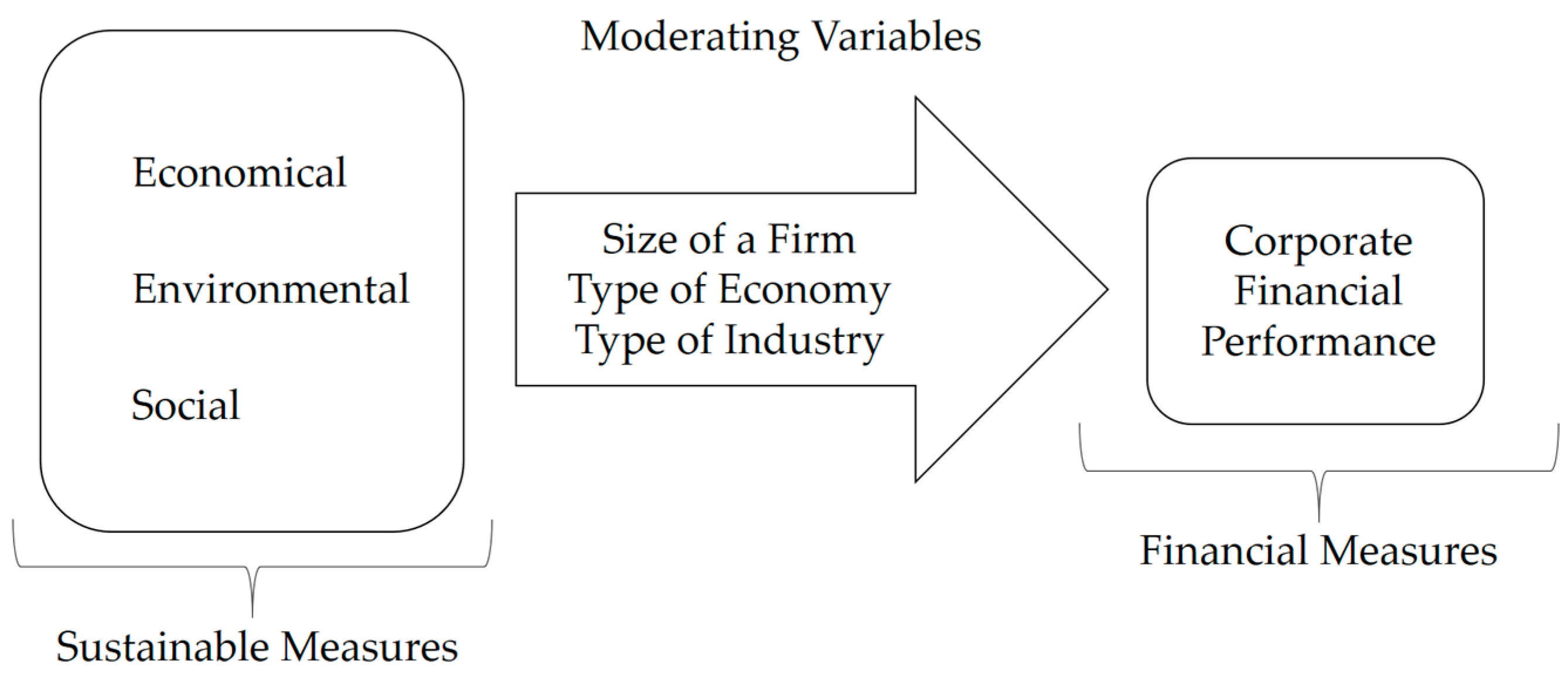

Literature trends are gravitating towards CSR as a replacement for a holistic sustainability notion when it comes to examining sustainability impact on corporate financial performance. This shift risks oversimplifying corporate sustainability into CSR. The problem with CSR is that it is mostly about the social element of sustainability, and little to nothing about environmental and economic dimensions. This problem is further amplified by the lagging number of theoretical research in the literature, which is still struggling to establish a universal definition for corporate sustainability between the three competing dimensions of sustainability. Research is needed not only to consolidate this competition between the dimensions of sustainability, but also to synthesize a universal understanding of corporate sustainability within the proposed framework (see Figure 6). This is also directly linked to the still-missing consensus in selecting corporate financial measures when examining the impact of sustainability. The role of moderating variables like firm size, economy, and industry type need to be further examined in different contexts, not only to broaden the applicability of research, but also to identify potential groupings along the lines of those variables. Identifying those groups can help produce customized universal sets of measures and methodologies to analyze the subject relationship and reduce variation in results. Further research is needed to map out and categorize suitable corporate financial measures, and how they relate to sustainability practices. Finally, more research is needed to examine the impact of total sustainability, in order to closely establish the combined effect of all three dimensions. This is needed not only to improve our understanding of the relationship between corporate sustainability and financial performance, but also to reduce variation in theory and results.

Author Contributions

Ali Alshehhi and Haitham Nobanee conceived and designed this research; Nilesh Khare also contributed to research idea. Ali Alshehhi performed the research and analyzed the data; Haitham Nobanee contributed analysis tools and editing. Ali Alshehhi and Haitham Nobanee wrote the paper. Nilesh Khare helped build the idea further and offered critical editing support.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

List of articles and associated financial performance measures.

| Authors | Title | Year | Performance Measure |

|---|---|---|---|

| Leonidou, Constantinos N.; Katsikeas, Constantine S.; Morgan, Neil A. | “Greening” the marketing mix: do firms do it and does it pay off? | 2013 | ROA |

| Wiengarten, Frank; Lo, Chris K.; Lam, Jessie Y. | “How does Sustainability Leadership Affect Firm Performance? The Choices Associated with Appointing a Chief Officer of Corporate Social Responsibility” | 2017 | ROA |

| Golicic, Susan L.; Smith, Carlo D. | A Meta-Analysis of Environmentally Sustainable Supply Chain Management Practices and Firm Performance | 2013 | - |

| Morali, Oguz; Searcy, Cory | A Review of Sustainable Supply Chain Management Practices in Canada | 2013 | - |

| Rettab, Belaid; Brik, Anis Ben; Mellahi, Kamel | A Study of Management Perceptions of the Impact of Corporate Social Responsibility on Organisational Performance in Emerging Economies: The Case of Dubai | 2009 | ROA, ROI, Sales Growth |

| Shen, Chung-hua; Chang, Yuan | Ambition Versus Conscience, Does Corporate Social Responsibility Pay off? The Application of Matching Methods | 2009 | ROA, ROE, PTI, RGM, EPS |

| Jacobs, Brian W.; Singhal, Vinod R.; Subramanian, Ravi | An empirical investigation of environmental performance and the market value of the firm | 2010 | Return of Stock |

| Xiao, Yuchao; Faff, Robert; Gharghori, Philip; Lee, Darren | An Empirical Study of the World Price of Sustainability | 2013 | Market Return |

| Verbeeten, Frank H. M.; Gamerschlag, Ramin; Möller, Klaus | Are CSR disclosures relevant for investors? Empirical evidence from Germany | 2016 | Share price, Return Per Share RET |

| Gallego-Álvarez, Isabel; Prado-Lorenzo, José-Manuel; Rodríguez-Domínguez, Luis; García-Sánchez, Isabel-María | Are social and environmental practices a marketing tool? | 2010 | Market Value, Capital |

| Dixon-Fowler, Heather; Slater, Daniel J.; Johnson, Jonathan L.; Ellstrand, Alan E.; Romi, Andrea M. | Beyond “Does it Pay to be Green?” A Meta-Analysis of Moderators of the CEP—CFP Relationship | 2013 | ROA, Market Share |

| Hahn, Tobias; Figge, Frank | Beyond the Bounded Instrumentality in Current Corporate Sustainability Research: Toward an Inclusive Notion of Profitability | 2011 | Capital Efficiency, Market Efficiency, Total Sales |

| Haffar, Merriam; Searcy, Cory | Classification of Trade-offs Encountered in the Practice of Corporate Sustainability | 2017 | - |

| Surroca, Jordi; Tribó, Josep A.; Waddock, Sandra | Corporate responsibility and financial performance: the role of intangible resources | 2010 | Tobin’s Q |

| Harrison, Jeffrey S.; Berman, Shawn L. | Corporate Social Performance and Economic Cycles | 2016 | GDP |

| Guiral, Andrés | Corporate Social Performance, Innovation Intensity, and Financial Performance: Evidence from Lending Decisions | 2012 | - |

| Kevin Huang, Shihping; Yang, Chih-Lung | Corporate social performance: why it matters? Case of Taiwan | 2014 | ROA, ROE |

| Kang, Hsin-hong; Liu, Shu-bing | Corporate social responsibility and corporate performance: a quantile regression approach | 2014 | ROA, ROE, Pre Tax Income to Net Sales PTI, Gross Profit to Net Sales (GPS), EPS |

| Simionescu, Liliana Nicoleta; Gherghina, Stefan Cristian | Corporate social responsibility and corporate performance: empirical evidence from a panel of the Bucharest Stock Exchange listed companies | 2014 | ROA, ROE, ROS |

| Balabanis, George; Phillips, Hugh C.; Lyall, Jonathan | Corporate social responsibility and economic performance in the top British companies: are they linked? | 1998 | ROE, ROCE, Gross Profit to Sales Ratio (GPS) |

| Cochran, Philip L.; Wood, Robert A. | Corporate social responsibility and financial performance | 1984 | Operating Earnings to Assets Ratio, Operating Earnings to Sales Ratio, Excess Market Valuation |

| Lech, Aleksandra | Corporate Social Responsibility and Financial Performance. Theoretical and Empirical Aspects | 2013 | ROA, ROE |

| Karagiorgos, Theofanis | Corporate Social Responsibility and Financial Performance: An Empirical Analysis on Greek Companies | 2010 | Stock Return |

| McGuire, Jean B.; Sundgren, Alison; Schneeweis, Thomas | Corporate Social Responsibility and Firm Financial Performance | 1988 | ROA, Total Assets, Sales Growth, Asset Growth, Operating Income Growth |

| Bai, Xuan; Chang, Jeanine | Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment | 2015 | Growth Rate, ROI, Overall Profitability |

| Gregory, Alan; Tharyan, Rajesh; Whittaker, Julie | Corporate Social Responsibility and Firm Value: Disaggregating the Effects on Cash Flow, Risk and Growth | 2014 | Book Value Per Share (BVPS), Net Income Per Share (NIPS), Long Term Debt, Total Asset, Sales |

| Chang, Yuan; Shen, Chung-Hua | Corporate Social Responsibility and Profitability—Cost of Debt as the Mediator | 2014 | ROA |

| Lizhen Chen, lzhchen ujs edu cn; Marfo, Emmanuel Opoku kwench hotmail com; Hu Xuhua, xuhuahu com | Corporate Social Responsibility behavior: Impact on Firm’s Financial Performance in an information technology driven society | 2016 | ROA, Stock Return Rate |

| Fernández-gago, Roberto; Cabeza-garcía, Laura; Nieto, Mariano | Corporate social responsibility, board of directors, and firm performance: an analysis of their relationships | 2016 | Firm Value |

| Zhu, Yan; Sun, Li-yun; Leung, Alicia S.; M | Corporate social responsibility, firm reputation, and firm performance: The role of ethical leadership | 2014 | ROE, ROI, ROS |

| Vicente Lima, Crisóstomo; Fátima de Souza, Freire; Felipe Cortes de, Vasconcellos | Corporate social responsibility, firm value and financial performance in Brazil | 2011 | Tobin’s Q, ROA, ROE |

| Przychodzen, Justyna; Przychodzen, Wojciech | Corporate sustainability and shareholder wealth | 2013 | Sustainable Growth Rate |

| Venkatraman, Sitalakshmi; Nayak, Raveendranath Ravi | Corporate sustainability: an IS approach for integrating triple bottom line elements | 2015 | Top dividends to shareholders, Business profitability, Return on average capital employed, Meeting tax obligations, Debt/Equity ratio |

| Hart, Stuart L.; Milstein, Mark B. | Creating sustainable value | 2003 | - |

| Porter, Terry; Miles, Patti | CSR Longevity: Evidence from Long-Term Practices in Large Corporations | 2013 | EBIT, EBI, Return on Pretax Income |

| Wang, Chung-Jen | Do ethical and sustainable practices matter? Effects of corporate citizenship on business performance in the hospitality industry | 2014 | ROI, Profit Growth |

| Rodgers, Waymond; Choy, Hiu Lam; Guiral, Andrés | Do Investors Value a Firm’s Commitment to Social Activities? | 2013 | Tobin’s Q, ROA, Financial Leverage, Liquidity Measure |

| Cheung, Yan-Leung; Connelly, J. T.; Jiang, Ping; Limpaphayom, Piman | Does Corporate Governance Predict Future Performance? Evidence from Hong Kong | 2011 | Tobin’s Q, Market to Book Ratio |

| Mishra, Supriti; Suar, Damodar | Does Corporate Social Responsibility Influence Firm Performance of Indian Companies? | 2010 | ROA |

| Hou, Mingjun; Liu, Heng; Fan, Peihua; Wei, Zelong | Does CSR practice pay off in East Asian firms? A meta-analytic investigation | 2016 | ROA, ROE, ROI, Profit Growth, Return of Equity, Cash Flow, Sales Growth, Tobin’s Q, Market Share, Market to Book, Stock Market Returns, Market Share Growth, Export Growth |

| Albertini, Elisabeth | Does Environmental Management Improve Financial Performance? A Meta-Analytical Review | 2013 | ROA, ROE, ROI, ROS, EPS, Tobin’s Q |

| Chien, Chin-Chen; Peng, Chih-Wei | Does going green pay off in the long run? | 2012 | ROE, ROA, EPS, Cash Flow to Total Assets (CFA) |

| Brammer, Stephen; Millington, Andrew | Does It Pay to Be Different? An Analysis of the Relationship between Corporate Social and Financial Performance | 2008 | Market Performance (share price growth plus dividend), Risk adjusted market performance (RAMP) (using government bonds returns as risk free) |

| Thornton, Ladonna M.; Autry, Chad W.; Gligor, David M.; Brik, Anis Ben | Does Socially Responsible Supplier Selection Pay Off for Customer Firms? A Cross-Cultural Comparison | 2013 | Relative Sales Revenue, Sales Growth, Market Share |

| Wahba, Hayam | Does the market value corporate environmental responsibility? An empirical examination | 2008 | Tobin’s Q |

| Chernev, Alexander; Blair, Sean | Doing Well by Doing Good: The Benevolent Halo of Corporate Social Responsibility | 2015 | - |

| Jia, Ming; Zhang, Zhe | Donating Money to Get Money: The Role of Corporate Philanthropy in Stakeholder Reactions to IPOs | 2014 | IPO agents and financing costs (Underwriter prestige, VC-backed shareholding, ration of IPO cost to financing scale), Issue market valuation premium, Retail market valuatin premium |

| Delmas, Magali A.; Nairn-Birch, Nicholas; Lim, Jinghui | Dynamics of Environmental and Financial Performance: The Case of Greenhouse Gas Emissions | 2015 | ROA, Tobin’s Q |

| Van de Velde, Eveline; Vermeir, Wim; Corten, Filip | Finance and accounting: Corporate social responsibility and financial performance | 2005 | Fama and French |

| Scholtens, Bert | Finance as a Driver of Corporate Social Responsibility | 2006 | - |

| Revelli, Christophe; Viviani, Jean-Laurent | Financial performance of socially responsible investing (SRI): what have we learned? A meta-analysis | 2015 | Return of Stock |

| Hull, Clyde Eirikur; Rothenberg, Sandra | Firm performance: the interactions of corporate social performance with innovation and industry differentiation | 2008 | ROA |

| Aguilera-Caracuel, Javier; Ortiz-de-Mandojana, Natalia | Green Innovation and Financial Performance: An Institutional Approach | 2013 | ROA |

| Molina-Azorín, José F.; Claver-Cortés, Enrique; López-Gamero, Maria D.; Tarí, Juan J. | Green management and financial performance: a literature review | 2009 | - |

| García-Sánchez, Isabel-María; Prado-Lorenzo, José-Manuel | Greenhouse gas emission practices and financial performance | 2012 | ROA, Market to Book (MtoB) |

| Nguyen, Dung K.; Slater, Stanley F. | Hitting the sustainability sweet spot: having it all | 2010 | ROA, Revenue Growth Rate, Share Value Appreciation Rate |

| Hyoung Koo, Moon; Byoung Kwon, Choi | How an organization’s ethical climate contributes to customer satisfaction and financial performance | 2014 | ROI |

| Wei, Yu-chen; Lin, Carol Yeh-yun | How can Corporate Social Responsibility Lead to Firm Performance? A Longitudinal Study in Taiwan | 2015 | ROA, Productivity (sales per employee) |

| Tang, Zhi; Hull, Clyde Eiríkur; Rothenberg, Sandra | How Corporate Social Responsibility Engagement Strategy Moderates the CSR-Financial Performance Relationship | 2012 | ROA |

| Saeidi, Sayedeh Parastoo; Sofian, Saudah; Saeidi, Parvaneh; Saeidi, Sayyedeh Parisa; Saaeidi, Seyyed Alireza | How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction | 2015 | ROA, ROE, ROI, ROS, Market Share Growth, Growth in Sales |

| Koo, Chulmo; Chung, Namho; Ryoo, Sung Yul | How does ecological responsibility affect manufacturing firms’ environmental and economic performance? | 2014 | Decreased Costs |

| Lourenço, Isabel Costa; Branco, Manuel Castelo; Curto, José Dias; Eugénio, Teresa | How Does the Market Value Corporate Sustainability Performance? | 2012 | Market Value of Equity, Book Value of Equity, Net Operating Income |

| Jia, Ming; Zhang, Zhe | How Does the Stock Market Value Corporate Social Performance? When Behavioral Theories Interact with Stakeholder Theory | 2014 | Stock Return |

| Goyal, Praveen; Rahman, Zillur; Kazmi, Absar Ahmad | Identification and prioritization of corporate sustainability practices using analytical hierarchy process | 2015 | - |

| Molla, Alemayehu | Identifying IT sustainability performance drivers: Instrument development and validation | 2013 | - |

| Murtaza, Iqra Ali; Akhtar, Naeem; Ijaz, Aqsa; Sadiqa, Ayesha | Impact of Corporate Social Responsibility on Firm Financial Performance: A Case Study of Pakistan | 2014 | ROA, ROE, EPS |

| Valmohammadi, Changiz | Impact of corporate social responsibility practices on organizational performance: an ISO 26000 perspective | 2014 | ROI, Sales Growth |

| Watson, Kevin; Klingenberg, Beate; Polito, Tony; Geurts, Tom G. | Impact of environmental management system implementation on financial performance: A comparison of two corporate strategies | 2004 | ROA, Profit Margin, Operating Margin, Price to Earnings Ratio, Market to Book Ratio |

| Garg, Priyanka | Impact of Sustainability Reporting on Firm Performance of Companies in India | 2015 | ROA, Tobin’s Q |

| Shank, Todd M. PhD; Shockey, Benjamin M. B. A. | Investment strategies when selecting sustainable firms | 2016 | Return (risk related) |

| Hsu, Feng Jui; Chen, Yu-Cheng | Is a firm’s financial risk associated with corporate social responsibility? | 2015 | - |

| Shih-Fang, Lo; Sheu, Her-Jiun | Is Corporate Sustainability a Value-Increasing Strategy for Business? | 2007 | Tobin’s Q |

| Cegarra-Navarro, Juan-Gabriel; Reverte, Carmelo; Gómez-Melero, Eduardo; Wensley, Anthony K. P. | Linking social and economic responsibilities with financial performance: The role of innovation | 2016 | ROE, Sales Growth, ROA and Market Share, Before-Tax Income |

| Endrikat, Jan; Guenther, Edeltraud; Hoppe, Holger | Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance | 2014 | - |

| Kiessling, Timothy; Isaksson, Lars; Yasar, Burze | Market Orientation and CSR: Performance Implications | 2016 | ROA |

| Endrikat, Jan | Market Reactions to Corporate Environmental Performance Related Events: A Meta-analytic Consolidation of the Empirical Evidence | 2016 | - |

| de Souza Cunha, Felipe Arias Fogliano; Samanez, Carlos Patricio | Performance Analysis of Sustainable Investments in the Brazilian Stock Market: A Study About the Corporate Sustainability Index (ISE) | 2013 | Return (risk related) |

| Tippayawong, K. Y.; Tiwaratreewit, T.; Sopadang, A. | Positive Influence of Green Supply Chain Operations on Thai Electronic Firms’ Financial Performance | 2015 | ROA, Inventory Turnover Ratio, Operating Cost Ratio, Net Profit Margin, Asset Turnover Ratio |

| Torugsa, Nuttaneeya Ann; O’Donohue, Wayne; Hecker, Rob | Proactive CSR: An Empirical Analysis of the Role of its Economic, Social and Environmental Dimensions on the Association between Capabilities and Performance | 2013 | ROA, Net Profits to Sales, Liquidity |

| Nakao, Yuriko; Amano, Akihiro; Matsumura, Kanichiro; Genba, Kiminori; Nakano, Makiko | Relationship between environmental performance and financial performance: an empirical analysis of Japanese corporations | 2007 | ROA, EPS, Tobin’s Q |

| Martínez-Ferrero, Jennifer; Frías-Aceituno, José Valeriano | Relationship Between Sustainable Development and Financial Performance: International Empirical Research | 2015 | Market Value, Book Value, Equity, Net Operating Income |

| Venkatraman, Sitalakshmi; Nayak, Raveendranath Ravi | Relationships among triple bottom line elements | 2015 | - |

| Robinson, Michael; Kleffner, Anne; Bertels, Stephanie | Signaling Sustainability Leadership: Empirical Evidence of the Value of DJSI Membership | 2011 | Cumulative Abnormal Return (CAR) |

| Wang, Taiyuan; Bansal, Pratima | Social responsibility in new ventures: profiting from a long-term orientation | 2012 | ROA, ROE, ROS, Sales Level, Market Share, Sales Growth, Cash Flow, Ability to fund business growth from profits, Overall firm performance/success |

| Quazi, Ali; Richardson, Alice | Sources of variation in linking corporate social responsibility and financial performance | 2012 | ROA, ROE, ROI, Market Return, Market Valuation, Stock Returns, Share Price, EPS, Survey Measures |

| Yu, Minna; Zhao, Ronald | Sustainability and firm valuation: an international investigation | 2015 | Tobin’s Q |

| Ameer, Rashid; Othman, Radiah | Sustainability Practices and Corporate Financial Performance: A Study Based on the Top Global Corporations | 2012 | ROA, Sales Growth, Profit Befor Tax (PBT), Cash Flow from Operating Activities (CFO) |

| Movassaghi, Hormoz; Bramhandkar, Alka | Sustainability Strategies of Leading Global Firms and Their Financial Performance: A Comparative Case Based Analysis | 2012 | ROA, ROE, EPS, Net Profit Margin, Book Value, Market Value |

| López, M. Victoria; Garcia, Arminda; Rodriguez, Lazaro | Sustainable Development and Corporate Performance: A Study Based on the Dow Jones Sustainability Index | 2007 | ROA, ROE, Profit Before Tax (PBT), Revenue, Capital, Profit Margin, Cost of Capital |

| Salzmann, Oliver; Ionescu-somers, Aileen; Steger, Ulrich | The Business Case for Corporate Sustainability: Literature Review and Research Options | 2005 | - |

| Simpson, Soni; Fischer, Bruce D.; Rohde, Matthew | The Conscious Capitalism Philosophy Pay Off: A Qualitative and Financial Analysis of Conscious Capitalism Corporations | 2013 | Stock Price, Compound Annual Growth Rate |

| Griffin, Jennifer J.; Mahon, John F. | The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research | 1997 | ROA, ROE, ROS, Total Assets, Asset Age |

| Waddock, Sandra A.; Graves, Samuel B. | The Corporate Social Performance financial Performance Link | 1997 | ROA, ROE, ROS |

| Moneva, Jose M.; Rivera-Lirio, Juana M.; Muñoz-Torres, María J. | The corporate stakeholder commitment and social and financial performance | 2007 | ROA, Return on Shareholder Fund |

| Lee, Sunghee; Jung, Heungjun | The effects of corporate social responsibility on profitability | 2016 | ROA |

| Nor, Norhasimah Md; Bahari, Norhabibi Aishah Shaiful; Adnan, Nor Amiera; Kamal, Sheh Muhammad Qamarul Ariffin Sheh; Ali, Inaliah Mohd | The Effects of Environmental Disclosure on Financial Performance in Malaysia | 2016 | ROA, ROE, EPS, Profit Margin |

| Chang, Dong-shang; Kuo, Li-chin Regina | The effects of sustainable development on firms’ financial performance - an empirical approach | 2008 | ROA, ROE, ROS |

| Isidro, Helena; Sobral, Márcia | The Effects of Women on Corporate Boards on Firm Value, Financial Performance, and Ethical and Social Compliance | 2015 | ROA, ROS, Tobin’s Q |

| Oikonomou, Ioannis; Brooks, Chris; Pavelin, Stephen | The Financial Effects of Uniform and Mixed Corporate Social Performance | 2014 | Book-Value to Market-Value Ratio |

| Chetty, Sukanya; Naidoo, Rebekah; Seetharam, Yudhvir | The Impact of Corporate Social Responsibility on Firms’ Financial Performance in South Africa | 2015 | ROA, ROE, EPS, Stock Returns |

| Feng, Taiwen; Wang, Dan | The Influence of Environmental Management Systems on Financial Performance: A Moderated-Mediation Analysis | 2016 | ROA, ROI, ROS, Net Profit Margin, Growth in Sales, Growth in Profit, Growth in Market Share |

| Singal, Manisha | The Link between Firm Financial Performance and Investment in Sustainability Initiatives | 2014 | Credit Rating |

| Schaltegger, Stefan; Synnestvedt, Terje | The link between ‘green’ and economic success: Environmental management as the crucial trigger between environmental and economic performance | 2002 | - |

| Wu, Junjie; Lodorfos, George; Dean, Aftab; Gioulmpaxiotis, Georgios | The Market Performance of Socially Responsible Investment during Periods of the Economic Cycle—Illustrated Using the Case of FTSE | 2017 | Share Price |

| Al-Tuwaijri, Sulaiman A.; Christensen, Theodore E.; Hughes, K. E. | The relations among environmental disclosure, environmental performance, and economic performance: a simultaneous equations approach | 2004 | Stock Return |

| Maletic, Matjaz; Maletic, Damjan; Dahlgaard, Jens J.; Dahlgaard-Park, Su Mi; Gomiscek, Bostjan | The Relationship between Sustainability- Oriented Innovation Practices and Organizational Performance: Empirical Evidence from Slovenian Organizations | 2014 | ROI, Sales Growth, Profit Growth, Market Share |

| Wagner, Marcus; Nguyen Van, Phu; Azomahou, Theophile; Wehrmeyer, Walter | The relationship between the environmental and economic performance of firms: an empirical analysis of the European paper industry | 2002 | ROE, ROS, ROCE, EBIT |

| Malik, Mahfuja | Value-Enhancing Capabilities of CSR: A Brief Review of Contemporary Literature | 2015 | Market Value of Outstanding Shares |

| Kang, Charles; Germann, Frank; Grewal, Rajdeep | Washing Away Your Sins? Corporate Social Responsibility, Corporate Social Irresponsibility, and Firm Performance | 2016 | Tobin’s Q |

| Aguinis, Herman; Glavas, Ante | What We Know and Don’t Know About Corporate Social Responsibility: A Review and Research Agenda | 2012 | - |

| Afza, Talat; Ehsan, Sadaf; Nazir, Sajid | Whether Companies Need to be Concerned about Corporate Social Responsibility for their Financial Performance or Not? A Perspective of Agency and Stakeholder Theories | 2015 | ROA, ROE, EPS, Sales growth, Tobin’s Q, Price to Earnings Ratio |

| Du, Xingqiang; Weng, Jianying; Zeng, Quan; Chang, Yingying; Pei, Hongmei | Do Lenders Applaud Corporate Environmental Performance? Evidence from Chinese Private-Owned Firms | 2017 | Interest Rate on Debt |

| Panwar, Rajat; Nybakk, Erlend; Hansen, Eric; Pinkse, Jonatan | Does the Business Case Matter? The Effect of a Perceived Business Case on Small Firms’ Social Engagement | 2017 | ROI, ROS, Sales Growth, Net Profit, Cash Flow |

| Karim, Khondkar; Suh, SangHyun; Tang, Jiali | Do ethical firms create value? | 2016 | Market Return |

| Yawar, Sadaat Ali; Seuring, Stefan | Management of Social Issues in Supply Chains: A Literature Review Exploring Social Issues, Actions and Performance Outcomes | 2017 | - |

| Rego, Arménio; Cunha, Miguel Pina; E.; Polónia, Daniel | Corporate Sustainability: A View from the Top | 2017 | - |

| Tuppura, Anni; Arminen, Heli; Pätäri, Satu; Jantunen, Ari | Corporate social and financial performance in different industry contexts: the chicken or the egg? | 2016 | ROA, Market Capitalization |

| Schmidt, Christoph G.; Foerstl, Kai; Schaltenbrand, Birte | The supply chain position paradox: green practices and firm performance | 2017 | ROI, Profits as percent of Sales, Labor productivity (sales/employees), Sales Growth |

| Busse, Christian | Doing well by doing good? the self-interest of buying firms and sustainable supply chain management | 2016 | - |

| Wang, Dan; Feng, Taiwen; Lawton, Alan | Linking Ethical Leadership with Firm Performance: A Multi-dimensional Perspective | 2017 | ROA, ROI, ROS, Sales Growth, Profit Growth, Market Share Growth, Overall Efficiency of Operations |

| Grewatsch, Sylvia; Kleindienst, Ingo | When Does It Pay to be Good? Moderators and Mediators in the Corporate Sustainability–Corporate Financial Performance Relationship: A Critical Review | 2017 | - |

| Cuadrado-Ballesteros, Beatriz; Garcia-Sanchez, Isabel-Maria; Martinez Ferrero, Jennifer | How are corporate disclosures related to the cost of capital? The fundamental role of information asymmetry | 2016 | EPS, Cost of Capital, Price Earnings Growth |

| Arouri, Mohamed; Pijourlet, Guillaume | CSR Performance and the Value of Cash Holdings: International Evidence | 2017 | EBIT, Market Value (market capitalization and total liabilities), Fama-French |

| Auer, Benjamin R. | Do Socially Responsible Investment Policies Add or Destroy European Stock Portfolio Value? | 2016 | Sharpe Ratio |

| Osazuwa, Nosakhare Peter; Che-Ahmad, Ayoib | The moderating effect of profitability and leverage on the relationship between eco-efficiency and firm value in publicly traded Malaysian firms | 2016 | ROA, Market value, Net Book Value, EPS, Leverage |

| Lipiec, Jacek | Does Warsaw Stock Exchange value corporate social responsibility? | 2016 | CAPM |

| Arevalo, Jorge A.; Aravind, Deepa | Strategic Outcomes in Voluntary CSR: Reporting Economic and Reputational Benefits in Principles-Based Initiatives | 2017 | Revenue Growth, Productivity Improvements, Cost Savings, Access to Capital |

| Oh, Hannah; Bae, John; Kim, Sang-joon | Can Sinful Firms Benefit from Advertising Their CSR Efforts? Adverse Effect of Advertising Sinful Firms’ CSR Engagements on Firm Performance | 2017 | Stock Return, Idiosyncratic Risk |

| Ibikunle, Gbenga; Steffen, Tom | European Green Mutual Fund Performance: A Comparative Analysis with their Conventional and Black Peers | 2017 | CAPM |

| Faris Alshubiri | The impact of green logistics-based activities on the sustainable monetary expansion indicators of Oman | 2017 | - |

| Székely, Nadine; Jan vom Brocke | What can we learn from corporate sustainability reporting? Deriving propositions for research and practice from over 9,500 corporate sustainability reports published between 1999 and 2015 using topic modelling technique | 2017 | - |

| (Jean) Jeon, Hyo Jin; Gleiberman, Aaron | Examining the role of sustainability and green strategies in channels: evidence from the franchise industry | 2017 | ROS |

References

- Ameer, R.; Othman, R. Sustainability Practices and Corporate Financial Performance: A Study Based on the Top Global Corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Lourenço, I.C.; Branco, M.C.; Curto, J.D.; Eugénio, T. How Does the Market Value Corporate Sustainability Performance? J. Bus. Ethics 2012, 108, 417–428. [Google Scholar] [CrossRef]

- Haffar, M.; Searcy, C. Classification of Trade-offs Encountered in the Practice of Corporate Sustainability. J. Bus. Ethics 2017, 140, 495–522. [Google Scholar] [CrossRef]

- Busse, C. Doing Well by Doing Good? The Self-Interest of Buying Firms and Sustainable Supply Chain Management. J. Supply Chain Manag. 2016, 52, 28–47. [Google Scholar] [CrossRef]

- Chernev, A.; Blair, S. Doing Well by Doing Good: The Benevolent Halo of Corporate Social Responsibility. J. Consum. Res. 2015, 41, 1412–1425. [Google Scholar] [CrossRef]

- Hahn, T.; Figge, F. Beyond the Bounded Instrumentality in Current Corporate Sustainability Research: Toward an Inclusive Notion of Profitability. J. Bus. Ethics 2011, 104, 325–345. [Google Scholar] [CrossRef]

- Albertini, E. Does Environmental Management Improve Financial Performance? A Meta-Analytical Review. Organ. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.; Slater, D.J.; Johnson, J.L.; Ellstrand, A.E.; Romi, A.M. Beyond “Does it Pay to be Green?” A Meta-Analysis of Moderators of the CEP–CFP Relationship. J. Bus. Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef]

- Shank, T.M.P.; Shockey, B.M.B.A. Investment strategies when selecting sustainable firms. Financ. Serv. Rev. 2016, 25, 199–214. [Google Scholar]

- Endrikat, J.; Guenther, E.; Hoppe, H. Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance. Eur. Manag. J. 2014, 32, 735–751. [Google Scholar] [CrossRef]

- Shah, K.U. Strategic organizational drivers of corporate environmental responsibility in the Caribbean hotel industry. Policy Sci. 2011, 44, 321. [Google Scholar] [CrossRef]

- Yu, M.; Zhao, R. Sustainability and firm valuation: An international investigation. Int. J. Account. Inf. Manag. 2015, 23, 289–307. [Google Scholar] [CrossRef]

- Salzmann, O.; Ionescu-somers, A.; Steger, U. The Business Case for Corporate Sustainability: Literature Review and Research Options. Eur. Manag. J. 2005, 23, 27–36. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The Corporate Social Performancefinancial Performance Link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Yawar, S.A.; Seuring, S. Management of Social Issues in Supply Chains: A Literature Review Exploring Social Issues, Actions and Performance Outcomes. J. Bus. Ethics 2017, 141, 621–643. [Google Scholar] [CrossRef]

- Rivera, J.M.; Munoz, M.J.; Moneva, J.M. Revisiting the Relationship Between Corporate Stakeholder Commitment and Social and Financial Performance. Sustainable Dev. 2017, 25, 482–496. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: the role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef] [Green Version]

- Martínez-Ferrero, J.; Frías-Aceituno, J.V. Relationship between Sustainable Development and Financial Performance: International Empirical Research. Bus. Strategy Environ. 2015, 24, 20–39. [Google Scholar] [CrossRef]

- Grewatsch, S.; Kleindienst, I. When Does It Pay to be Good? Moderators and Mediators in the Corporate Sustainability–Corporate Financial Performance Relationship: A Critical Review. J. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What We Know and Don’t Know About Corporate Social Responsibility: A Review and Research Agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Morali, O.; Searcy, C. A Review of Sustainable Supply Chain Management Practices in Canada. J. Bus. Ethics 2013, 117, 635–658. [Google Scholar] [CrossRef]

- Verbeeten, F.H.M.; Gamerschlag, R.; Möller, K. Are CSR disclosures relevant for investors? Empirical evidence from Germany. Manag. Decis. 2016, 54, 1359–1382. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Podsakoff, N.P.; Bachrach, D.G. Scholarly Influence in the Field of Management: A Bibliometric Analysis of the Determinants of University and Author Impact in the Management Literature in the Past Quarter Century. J. Manag. 2008, 34, 641–720. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; Claver-Cortés, E.; López-Gamero, M.D.; Tarí, J.J. Green management and financial performance: A literature review. Manag. Decis. 2009, 47, 1080–1100. [Google Scholar] [CrossRef]

- Székely, N.; Jan vom, B. What can we learn from corporate sustainability reporting? Deriving propositions for research and practice from over 9500 corporate sustainability reports published between 1999 and 2015 using topic modelling technique. PLoS ONE 2017, 12, e0174807. [Google Scholar] [CrossRef] [PubMed]

- Bai, C.; Sarkis, J.; Dou, Y. Corporate sustainability development in China: Review and analysis. Ind. Manag. Data Syst. 2015, 115, 5–40. [Google Scholar] [CrossRef]

- Kang, H.-H.; Liu, S.-B. Corporate social responsibility and corporate performance: A quantile regression approach. Qual. Quant. 2014, 48, 3311–3325. [Google Scholar] [CrossRef]

- Singal, M. The Link between Firm Financial Performance and Investment in Sustainability Initiatives. Cornell Hosp. Q. 2014, 55, 19–30. [Google Scholar] [CrossRef]

- United Nations (UN). World Economic Situation and Prospects 2017; United Nations Publication: New York, NY, USA, 2017; pp. 151–159. [Google Scholar]

- Moldavska, A. Defining Organizational Context for Corporate Sustainability Assessment: Cross-Disciplinary Approach. Sustainability 2017, 9, 2365. [Google Scholar] [CrossRef]

- De Souza Cunha, F.A.F.; Samanez, C.P. Performance Analysis of Sustainable Investments in the Brazilian Stock Market: A Study about the Corporate Sustainability Index (ISE). J. Bus. Ethics 2013, 117, 19–36. [Google Scholar] [CrossRef]

- Robinson, M.; Kleffner, A.; Bertels, S. Signaling Sustainability Leadership: Empirical Evidence of the Value of DJSI Membership. J. Bus. Ethics 2011, 101, 493–505. [Google Scholar] [CrossRef]

- Xiao, Y.; Faff, R.; Gharghori, P.; Lee, D. An Empirical Study of the World Price of Sustainability. J. Bus. Ethics 2013, 114, 297–310. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Wasiluk, K.L. Beyond eco-efficiency: Understanding CS through the IC practice lens. J. Intellect. Cap. 2013, 14, 102–126. [Google Scholar] [CrossRef]

- Truant, E.; Corazza, L.; Scagnelli, S.D. Sustainability and Risk Disclosure: An Exploratory Study on Sustainability Reports. Sustainability 2017, 9, 636. [Google Scholar] [CrossRef]

- Wang, T.; Bansal, P. Social responsibility in new ventures: Profiting from a long-term orientation. Strateg. Manag. J. 2012, 33, 1135–1153. [Google Scholar] [CrossRef]

- Quazi, A.; Richardson, A. Sources of variation in linking corporate social responsibility and financial performance. Soc. Responsib. J. 2012, 8, 242–256. [Google Scholar] [CrossRef]

- Shah, K.U.; Arjoon, S.; Rambocas, M. Aligning Corporate Social Responsibility with Green Economy Development Pathways in Developing Countries. Sustain. Dev. 2016, 24, 237–253. [Google Scholar] [CrossRef]

Figure 1.

Percentage of publications by time period.

Figure 2.

Percentage of publications distribution by development of economy.

Figure 3.

Percentage distribution of publications by sustainability dimension.

Figure 4.

Percentage distribution of publications by research type.

Figure 5.

Impact of sustainability dimensions on corporate financial performance.

Figure 6.

Proposed framework for future research.

Table 1.

Country distribution of publications.

| Country | pre–2002 | 2002–2003 | 2004–2005 | 2006–2007 | 2008–2009 | 2010–2011 | 2012–2013 | 2014–2015 | 2016–October 2017 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| Japan | - | - | - | 1 | - | - | - | - | - | 1 |

| Liechtenstein | - | - | - | - | - | - | - | - | 1 | 1 |

| Belgium | - | - | 1 | - | - | - | - | - | - | 1 |

| Oman | - | - | - | - | - | - | - | - | 1 | 1 |

| Egypt | - | - | - | - | 1 | - | - | - | - | 1 |

| Romania | - | - | - | - | - | - | - | 1 | - | 1 |

| Iran | - | - | - | - | - | - | - | 1 | - | 1 |

| Slovenia | - | - | - | - | - | - | - | 1 | - | 1 |

| Denmark | - | - | - | - | - | - | - | - | 1 | 1 |

| South Africa | - | - | - | - | - | - | - | 1 | - | 1 |

| UAE | - | - | - | - | 1 | - | - | - | - | 1 |

| Thailand | - | - | - | - | - | - | - | 1 | - | 1 |

| Greece | - | - | - | - | - | 1 | - | - | - | 1 |

| Turkey | - | - | - | - | - | - | - | - | 1 | 1 |

| Netherlands | - | - | - | 1 | - | - | - | - | 1 | 2 |

| Pakistan | - | - | - | - | - | - | - | 2 | - | 2 |

| Switzerland | - | - | 1 | - | - | - | - | - | 1 | 2 |

| Finland | - | - | - | - | - | - | - | - | 2 | 2 |

| Brazil | - | - | - | - | - | 1 | 1 | - | - | 2 |

| India | - | - | - | - | - | 1 | - | 2 | - | 3 |

| South Korea | - | - | - | - | - | - | - | 2 | 1 | 3 |

| Poland | - | - | - | - | - | - | 2 | - | 1 | 3 |

| Portugal | - | - | - | - | - | - | 1 | 1 | 1 | 3 |

| France | - | - | - | - | - | 1 | 1 | 1 | 1 | 4 |

| Canada | - | - | - | - | - | 1 | 1 | - | 2 | 4 |

| Malaysia | - | - | - | - | - | - | 1 | 1 | 2 | 4 |

| Germany | - | 2 | - | - | - | - | - | 1 | 3 | 6 |

| Australia | - | - | - | - | - | - | 4 | 2 | 1 | 7 |

| UK | 1 | - | - | - | 1 | - | 2 | 2 | 2 | 8 |

| China | - | - | - | - | - | 1 | - | 4 | 4 | 9 |

| Taiwan | - | - | - | 1 | 2 | - | 1 | 6 | - | 10 |

| Spain | - | - | - | 2 | 1 | 2 | 4 | 1 | 3 | 13 |

| US | 4 | 1 | 2 | - | 1 | 2 | 8 | 5 | 8 | 31 |

Table 2.

Industry distribution of publications.

| Industry | pre–2002 | 2002–2003 | 2004–2005 | 2006–2007 | 2008–2009 | 2010–2011 | 2012–2013 | 2014–2015 | 2016–October 2017 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| IT | - | - | - | - | - | - | 1 | - | - | 1 |

| Banking | - | - | - | - | - | - | 1 | - | - | 1 |

| Chemical | 1 | - | - | - | - | - | - | - | - | 1 |

| Oil & Gas | - | - | - | - | - | - | - | - | 1 | 1 |

| Electronics | - | - | - | - | - | - | - | 1 | - | 1 |

| Automotive | - | - | - | - | - | 1 | - | - | - | 1 |

| Paper | - | 1 | - | - | - | - | - | - | - | 1 |

| Food | - | - | - | - | - | - | - | 1 | - | 1 |

| Hospitality | - | - | - | - | - | - | - | 3 | - | 3 |

| Manufacturing | - | - | - | 1 | - | 1 | 1 | 2 | 2 | 7 |

| Multi Industry | 4 | 2 | 4 | 4 | 7 | 8 | 23 | 28 | 34 | 114 |

| Total | 5 | 3 | 4 | 5 | 7 | 10 | 26 | 35 | 37 | 132 |

Table 3.

Journal-wise distribution of publications.

| Country | Total |

|---|---|

| Academy of Management Executive | 1 |

| Total Quality Management & Business Excellence | 1 |

| International Review of Management and Business Research | 1 |

| Academy of Management Journal | 1 |

| Accounting, Organizations and Society | 1 |

| Academy of Management Journal (pre–1986) | 1 |

| Business and Society | 1 |

| Journal of Business Strategy | 1 |

| Chinese Management Studies | 1 |

| Journal of Consumer Research | 1 |

| Contemporary Economics | 1 |

| Journal of environmental management | 1 |

| Corporate Governance | 1 |

| Journal of Environmental Planning & Management | 1 |

| Corporate Social Responsibility & Environmental Management | 1 |

| Journal of Global Responsibility | 1 |

| European Business Review | 1 |

| Journal of Industrial Engineering and Management | 1 |

| European Online Journal of Natural and Social Sciences | 1 |

| Journal of Leadership, Accountability and Ethics | 1 |

| Financial Management | 1 |

| Journal of Management | 1 |

| Industrial Management & Data Systems | 1 |

| Journal of Marketing | 1 |

| International Journal of Accounting and Information Management | 1 |

| Journal of Marketing Theory and Practice | 1 |

| International Journal of Contemporary Hospitality Management | 1 |

| Journal of Modelling in Management | 1 |

| International Journal of Marketing & Business Communication | 1 |

| Journal of Operations Management | 1 |

| Behavioral Research in Accounting | 1 |

| Journal of the Academy of Marketing Science | 1 |

| Comparative Economic Research | 1 |

| Management & Marketing | 1 |

| Corporate Governance: An International Review | 1 |

| Management of Environmental Quality | 1 |

| European Journal of Innovation Management | 1 |

| Managerial and Decision Economics | 1 |

| Financial Services Review | 1 |

| Organizacija | 1 |

| International Journal of Climate Change Strategies and Management | 1 |

| PLoS One | 1 |

| The Journal of Applied Business and Economics | 1 |

| Procedia Economics and Finance | 1 |

| Cornell Hospitality Quarterly | 1 |

| Procedia Engineering | 1 |

| European Research Studies | 1 |

| Quality and Quantity | 1 |

| International Journal of Engineering Research in Africa | 1 |

| Review of Managerial Science | 1 |

| Corporate Social Responsibility and Environmental Management | 1 |

| Strategic Management Journal (1986–1998) | 1 |

| Business Ethics | 1 |

| Sustainable Development | 1 |

| Information Systems Frontiers | 1 |

| Taipei Economic Inquiry | 1 |

| Journal of Business Research | 2 |

| Corporate Reputation Review | 2 |

| Business Strategy and the Environment | 2 |

| Organization & Environment | 3 |

| Asia Pacific Journal of Management | 3 |

| The Journal of Management Studies | 3 |

| European Management Journal | 3 |

| Strategic Management Journal | 4 |

| Journal of Supply Chain Management | 4 |

| Management Decision | 6 |

| Social Responsibility Journal | 8 |

| Journal of Business Ethics | 36 |

Table 4.

Count of methodology approaches adopted in examining the relationship between variables in examined literature.

Table 4.

Count of methodology approaches adopted in examining the relationship between variables in examined literature.

| Methodology Approach | Count |

|---|---|

| Partial Least Squares | 1 |

| Path model | 1 |

| Analytic hierarchy process | 1 |

| Performance Matrix | 1 |

| ANOVA | 1 |

| Practicability | 1 |

| Predective model differences | 1 |

| Conceptual theory-building | 1 |

| Propensity score matching | 1 |

| CSRI | 1 |

| Quantile regression | 1 |

| Cumulative Portfolio | 1 |

| Risk-adjusted analysis | 1 |

| Experiment (controlled subjects) | 1 |

| Score matching | 1 |

| Granger causality test | 1 |

| Semi-structured interviews | 1 |

| Group analysis (Interviews) | 1 |

| Shareholder value creation model | 1 |

| Instrumental finality | 1 |

| Shareholder value framework | 1 |

| Active stakeholders | 1 |

| Sharpe & Treynor | 1 |

| Behavioral perspective of appointed chief officer of CSR | 1 |

| Simultaneous equation model | 1 |

| Wilcoxon signed-rank test | 1 |

| Simultaneuos equation system | 1 |

| Cumulative abnormal return | 1 |

| Socially responsible investment | 1 |

| Firms of endearment | 1 |

| Sortino and Omega | 1 |

| Hausman–Taylor modelling | 1 |

| Stakeholder/shareholder orientation | 1 |

| Annual Supersector Leader Portfolio | 1 |

| Structural modeling | 1 |

| Corporate reputation model | 1 |

| Sustainalytics Platform database | 1 |

| GRI | 1 |

| Teleological integration | 1 |

| Capital Asset Pricing Model | 1 |

| Theoretical | 1 |

| Multi-factor regressions | 1 |

| Two stage investor decision-making model | 1 |

| Environmental Kuznets curve (EKC) | 1 |

| Two-way random effects model | 1 |

| Portfolio construction | 2 |

| Structural panel vector autoregression | 2 |

| Paired t-test | 2 |

| Structural equation modeling (PLS) | 2 |

| Interviews | 2 |

| Fama and French | 2 |

| Event study | 3 |

| Hierarchical regression analysis | 3 |

| Panel data regression models | 4 |

| Content analysis | 6 |

| Structural equation modeling | 7 |

| Literature review | 7 |

| Meta analysis | 8 |

| Survey | 11 |

| Regression analysis | 48 |

Table 5.

Time period distribution of publications based on financial measures.

| Financial Performance Measure | pre–2002 | 2002–2003 | 2004–2005 | 2006–2007 | 2008–2009 | 2010–2011 | 2012–2013 | 2014–2015 | 2016–October 2017 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| Long Term Debt | - | - | - | - | - | - | - | 1 | - | 1 |

| Book to Market Ratio | - | - | - | - | - | - | - | 1 | - | 1 |

| Market Efficiency | - | - | - | - | - | 1 | - | - | - | 1 |

| Asset Age | 1 | - | - | - | - | - | - | - | - | 1 |

| Access to Capital | - | - | - | - | - | - | - | - | 1 | 1 |

| Asset Growth | 1 | - | - | - | - | - | - | - | - | 1 |

| Book Value of Equity | - | - | - | - | - | - | 1 | - | - | 1 |

| Asset Turnover Ratio | - | - | - | - | - | - | - | 1 | - | 1 |

| Capital Efficiency | - | - | - | - | - | 1 | - | - | - | 1 |

| Cash flow to total assets CFA | - | - | - | - | - | - | 1 | - | - | 1 |

| Credit Rating | - | - | - | - | - | - | - | 1 | - | 1 |

| Net Book Value | - | - | - | - | - | - | - | - | 1 | 1 |

| Debt/Equity Ratio | - | - | - | - | - | - | - | 1 | - | 1 |

| Net Profit | - | - | - | - | - | - | - | - | 1 | 1 |

| Operating Ratio | - | - | - | - | - | - | - | 1 | - | 1 |

| Idiosyncratic Risk | - | - | - | - | - | - | - | - | 1 | 1 |

| Pretax Income | - | - | - | - | 1 | - | - | - | - | 1 |

| Inventory Turnover Ratio | - | - | - | - | - | - | - | 1 | - | 1 |

| Pretax Profit Margin | - | - | - | - | - | - | - | 1 | - | 1 |

| Book Value Per Share | - | - | - | - | - | - | - | 1 | - | 1 |

| Price Earnings Growth | - | - | - | - | - | - | - | - | 1 | 1 |

| Compound Annual Growth Rate | - | - | - | - | - | - | 1 | - | - | 1 |

| Ratio of IPO Cost to Financing Scale | - | - | - | - | - | - | - | 1 | - | 1 |

| Firm Value | - | - | - | - | - | - | - | - | 1 | 1 |

| Risk Adjusted Market Performance | - | - | - | - | 1 | - | - | - | - | 1 |

| Interest Rate on Debt | - | - | - | - | - | - | - | - | 1 | 1 |

| Sharpe Ratio | - | - | - | - | - | - | - | - | 1 | 1 |

| Stock Price | - | - | - | - | - | - | 1 | - | - | 1 |

| Equity | - | - | - | - | - | - | - | 1 | - | 1 |

| Venture Capital Backed Shareholding | - | - | - | - | - | - | - | 1 | - | 1 |

| Cumulative Abnormal Return | - | - | - | - | - | 1 | - | - | - | 1 |

| Underwriter Prestige | - | - | - | - | - | - | - | 1 | - | 1 |

| Book Value | - | - | - | - | - | - | 1 | 1 | - | 2 |

| Dividend | - | - | - | - | 1 | - | - | 1 | - | 2 |

| Revenue | - | - | - | 1 | - | - | 1 | - | - | 2 |

| Revenue Growth | - | - | - | - | - | 1 | - | - | 1 | 2 |

| Cost of Capital | - | - | - | 1 | - | - | - | - | 1 | 2 |

| Fama-French | - | - | 1 | - | - | - | - | - | 1 | 2 |

| Market Valuation | 1 | - | - | - | - | - | 1 | - | - | 2 |

| Cost Savings | - | - | - | - | - | - | - | 1 | 1 | 2 |

| Profitability | - | - | - | - | - | - | - | 2 | - | 2 |

| Labor Productivity | - | - | - | - | - | - | - | 1 | 1 | 2 |

| Return (risk related) | - | - | - | - | - | - | 1 | - | 1 | 2 |

| Operating Margin | 1 | - | 1 | - | - | - | - | - | - | 2 |

| (P/E) Ratio | - | - | 1 | - | - | - | - | 1 | - | 2 |

| Leverage | - | - | - | - | - | - | 1 | - | 1 | 2 |

| Market Valuation Premium | - | - | - | - | - | - | - | 2 | - | 2 |

| Liquidity | - | - | - | - | - | - | 2 | - | - | 2 |

| Profit Before Tax | - | - | - | 1 | - | - | 1 | - | - | 2 |

| Capital | - | - | - | 1 | - | 1 | - | - | - | 2 |

| Capital Asset Pricing Model | - | - | - | - | - | - | - | - | 2 | 2 |

| Gross Profit Ratio | 1 | - | - | - | - | - | - | 1 | - | 2 |

| Market Return | - | - | - | - | - | - | 2 | - | 1 | 3 |

| Return on Capital Employed (ROCE) | 1 | 1 | - | - | - | - | - | 1 | - | 3 |

| Operating Income | 1 | - | - | - | - | - | 1 | 1 | - | 3 |

| Total Assets | 2 | - | - | - | - | - | - | 1 | - | 3 |

| Cash Flow | - | - | - | - | - | - | 2 | - | 2 | 4 |

| Market to Book Ratio | - | - | 1 | - | - | 1 | 1 | - | 1 | 4 |

| Profit Growth | - | - | - | - | - | - | - | 2 | 3 | 5 |

| Share Price | - | - | - | - | 1 | 1 | 1 | - | 2 | 5 |

| Earnings (EBI, EBT, EBIT) | - | 1 | - | - | - | - | 3 | - | 2 | 6 |

| Market Capitalization | - | - | - | - | - | 1 | 2 | 2 | 3 | 8 |

| Profit Margin | - | - | 1 | 1 | 1 | - | 2 | 1 | 3 | 9 |

| Stock Return | - | - | 1 | - | - | 2 | 1 | 3 | 3 | 10 |

| Market Share | - | - | - | - | - | - | 3 | 2 | 5 | 10 |

| ROS | 2 | 1 | - | - | 1 | - | 2 | 4 | 4 | 14 |

| Tobin’s Q | - | - | - | 2 | 1 | 3 | 2 | 5 | 2 | 15 |

| EPS | - | - | - | 1 | 1 | - | 4 | 5 | 4 | 15 |

| ROI | - | - | - | - | 1 | - | 2 | 7 | 5 | 15 |

| Sales | 1 | - | - | - | 1 | 1 | 4 | 5 | 6 | 18 |

| ROE | 3 | 1 | - | 2 | 2 | 1 | 6 | 8 | 4 | 27 |

| ROA | 4 | - | 1 | 3 | 4 | 3 | 14 | 13 | 11 | 53 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Alshehhi, A.; Nobanee, H.; Khare, N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 2018, 10, 494. https://doi.org/10.3390/su10020494

AMA Style

Alshehhi A, Nobanee H, Khare N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability. 2018; 10(2):494. https://doi.org/10.3390/su10020494

Chicago/Turabian StyleAlshehhi, Ali, Haitham Nobanee, and Nilesh Khare. 2018. "The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential" Sustainability 10, no. 2: 494. https://doi.org/10.3390/su10020494

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.